Earnings At Risk

In this 07-08-22 issue of “Earnings At Risk”

- Quarter Ends…Finally. What Next?

- What Are We Watching Now?

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Weekly Market Recap With Adam Taggart

Administrator Note

The family and I are on vacation this week to visit our son who lives in Germany. Due to the Covid pandemic lockdowns and restrictions, we have been unable to see him for almost 2-years. So, we organized a quick trip to meet up in Maiori, Italy for a few days.

Given the travel time and lack of access to my normal databases, this week and next, some of the usual charts and analytics will be missing. However, I wanted to provide you with some thoughts about what we are watching and keep you abreast of the risks and changes we are making to our portfolios.

Thank you in advance for your understanding, and I hope you have a great week.

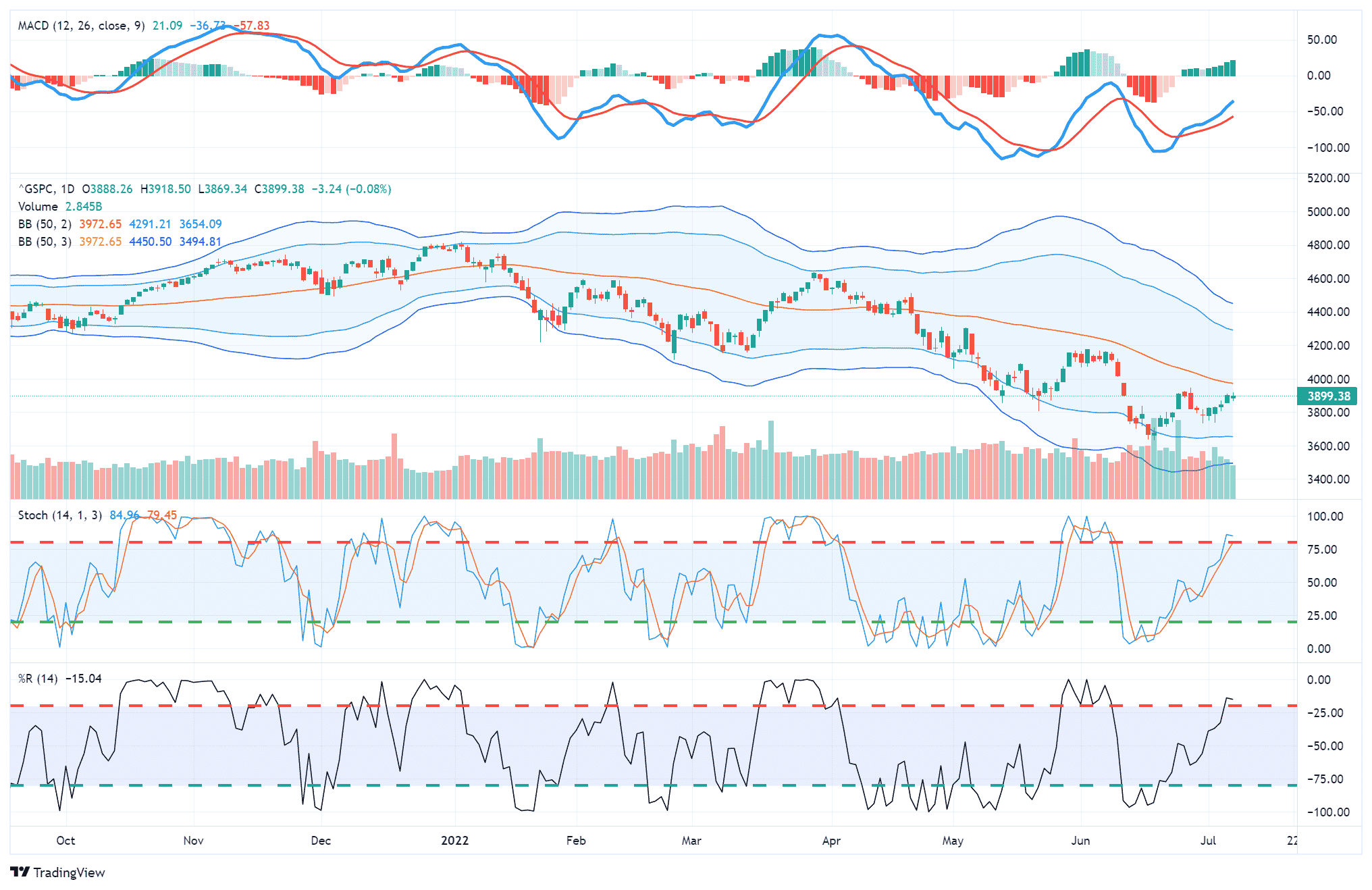

Market Trading Update

With relief, the quarter-end came after a dismal performance for markets over the last 3-months. The message has been consistent for the quarter to “sell rallies” and “raise cash,” but even with markets deeply oversold, bounces remain short-lived. As noted last week, we suspected a rally was likely given the deep oversold condition and the MACD “buy signal” (top panel).

However, that rally has lacked a strong pickup in volume and the advance lacked commitment by traders. Unfortunately, the small advance consumed the majority of the oversold condition with the 50-dma remaining stiff resistance for the time being. We had taken on some index trading positions in both the Nasdaq (QQQ) and the S&P 500 Equal Weight Index (RSP) to trade the rally. However, given the weakness of that rally, we took profits in the QQQ position last week, and will likely close out RSP next week.

As we will discuss in today’s commentary, the big risk heading into the third quarter is not only continued slowing of economic growth but earnings are at risk.

“Of the 103 S&P 500 companies have issued quarterly EPS guidance for the second quarter, 71 have issued negative EPS guidance and 32 have issued positive EPS guidance. The number of companies issuing negative EPS guidance is above the five-year average of 59 and above the 10-year average of 66. In fact, the second quarter has the highest number of S&P 500 companies issuing negative EPS guidance for a quarter since Q4 2019 (73).” – FactSet

As we enter 3rd-quarter earnings season, the big risk to the market won’t be the reported earnings but the forward guidance. With the increases in input costs, labor costs, and bulging inventories which will get discounted, the risk of an earnings recession have increased as consumption slows.

Monetary Tightening Puts Earnings At Risk

What hasn’t yet changed has been the consensus outlook on how S&P 500 companies’ profits will in aggregate be affected by a souring backdrop. And once these estimates begin to reflect those economic concerns, that could make the case for stocks to take another leg lower.

As the macroeconomic environment becomes more challenging, earnings estimates may face negative revisions. As a result, the ongoing bear market may have further room to fall as cheapening valuations begin to share the reins with earnings in pushing risk assets lower, justifying an underweight risk posture.” – Yahoo Finance

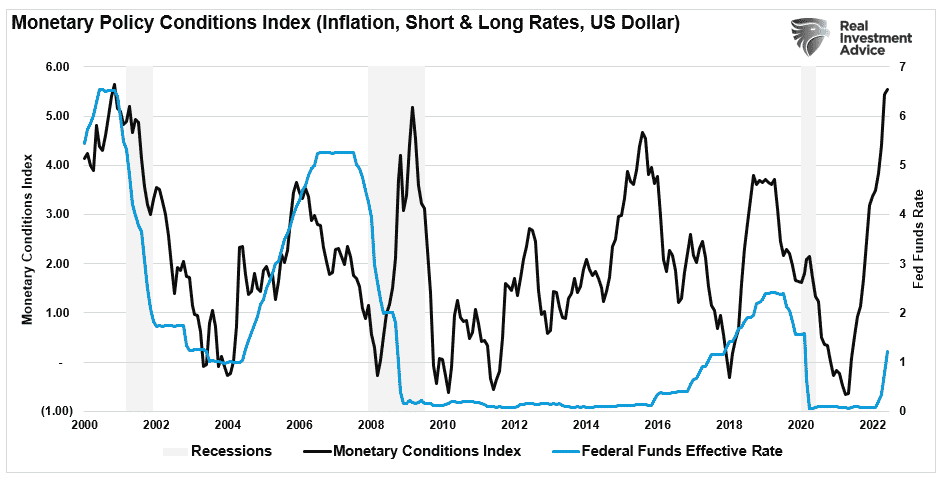

That note from Yahoo Finance picks up on our commentary from last week. While the Fed is aggressively tightening monetary policy, the economy’s monetary conditions are already substantially tighter due to higher rates, a stronger dollar, and inflation.

Those conditions are weighing on consumption and economic growth and estimates for second-quarter GDP are suggesting a contraction. As inflation impacts consumption and slows economic growth, market will have to reprice for slower earnings.

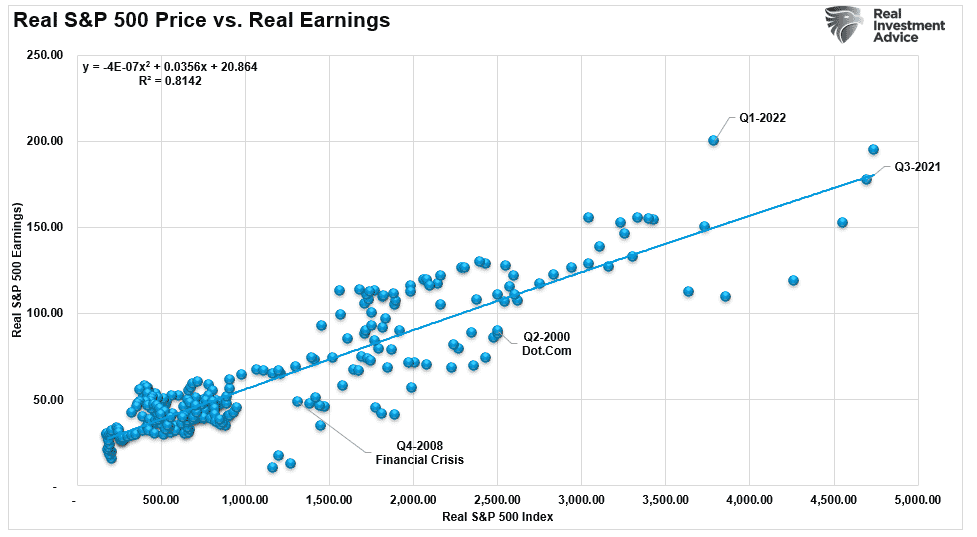

“Currently, earnings estimates for stocks are not accounting for much slower economic activity. While the “P” in the valuations (P/E) calculation has declined, the “E” has not. During a recession, earnings tend to fall quite significantly.”

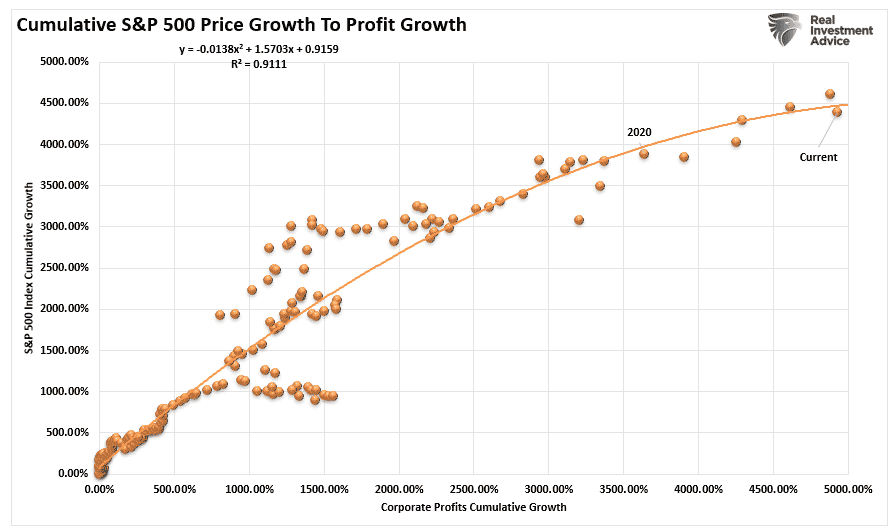

The rather significant correlation between price and earnings should be of no surprise. However, there are times, like now, when the price deviates from the underlying earnings. Given the current deviation, the price of the market will have to adjust lower to compensate.

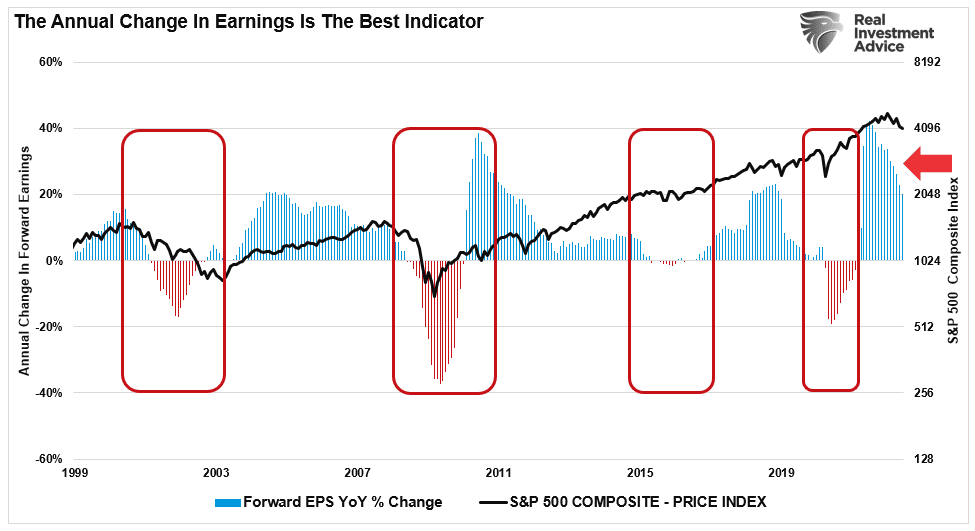

While many analysts point to strong employment as a reason the economy could avoid a recession, trailing economic data, is typically wrong at turning points. As noted last week, forward earnings estimates have fallen, but if history is any guide, they are still too optimistic.

However, there are other indications that earnings are at risk.

MacroView

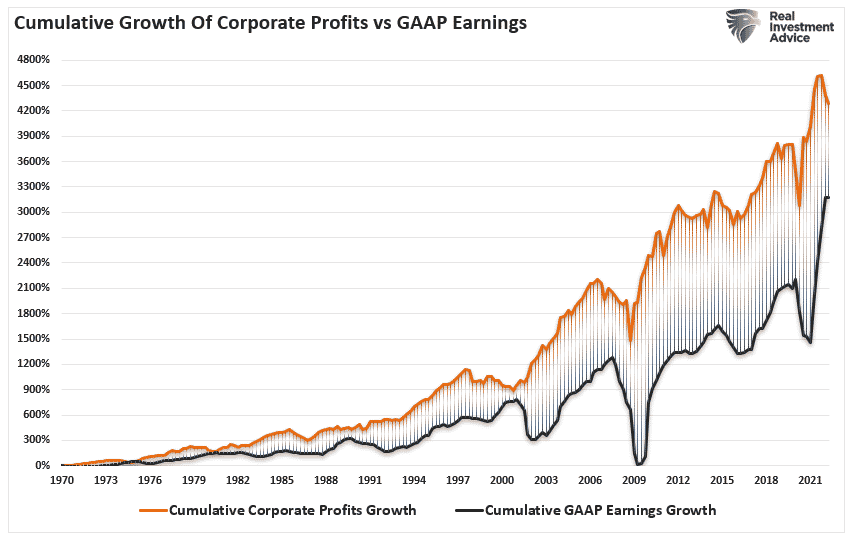

Corporate Profits Suggest Earnings Are At Risk

“Consensus profit margin forecasts have further to fall which will likely lead to downward EPS revisions whether or not the economy falls into recession. Assuming no change in expected revenues, the margin compression we model would reduce the median stock’s expected 2023 EPS growth from +10% to 0%.” – David Kostin

Profits, which get reported to the IRS for tax purposes, also put current high estimates of earnings at risk. As we noted in “Earnings Recession,” the economy grows at about 6% historically. Therefore, earnings growth also runs at roughly ~6% on a peak-to-peak basis. However, analysts currently suggest that earnings growth into 2023 will run well above the historical growth rate despite forecasts of much slower economic activity.

To put that into perspective, analysts’ estimates are currently at the most significant deviation above that 6% earnings growth trend.

However, as noted, corporate profits have already turned lower. As such earnings, which are derived from revenue and are part of the profits reporting, will turn lower as well.

Therefore, the price of the market must get revalued to compensate for lower profitability. As with earnings, there is a high correlation between cumulative price growth and profits.

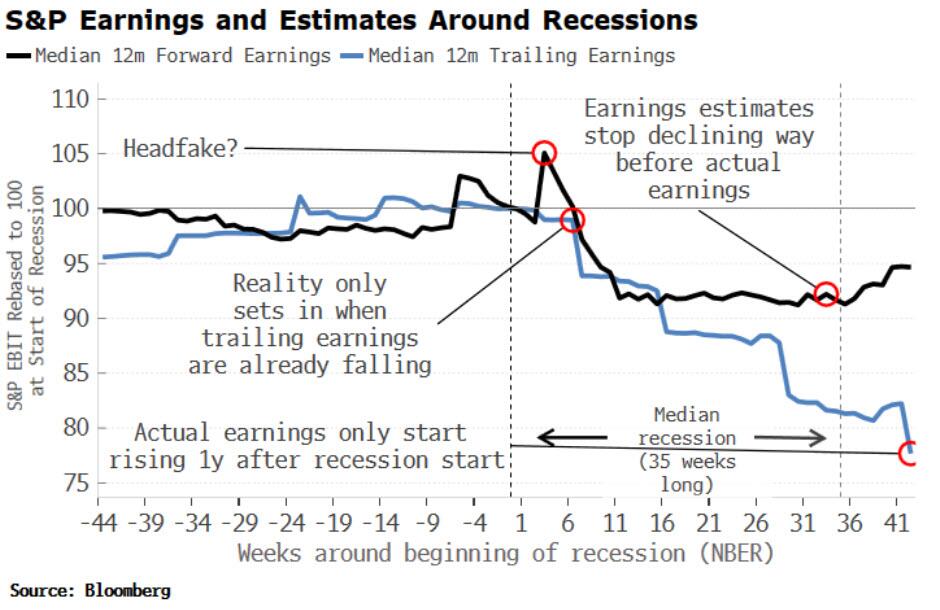

Simon White at Bloomberg confirmed the same concern that earnings are at risk stating:

“I showed that earnings estimates are most wrong in recessions. Earnings themselves don’t start to fall for several weeks, while forward earnings have one last burst of optimism, jumping higher, before reflecting reality and falling.”

The takeaway is that earnings estimates have yet to adjust for an economic slowdown, or worse, a recession. Today, the macro warnings for a recession are mounting, leaving earnings looking increasingly exposed.

Stay focused on estimates as we head into Q2 reporting. They will tell you all you need to know.

A Recession Will Cause It

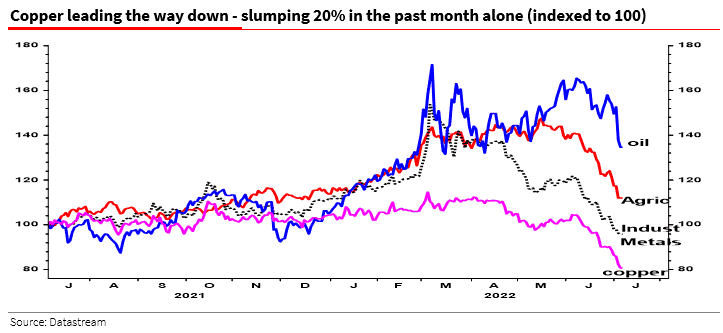

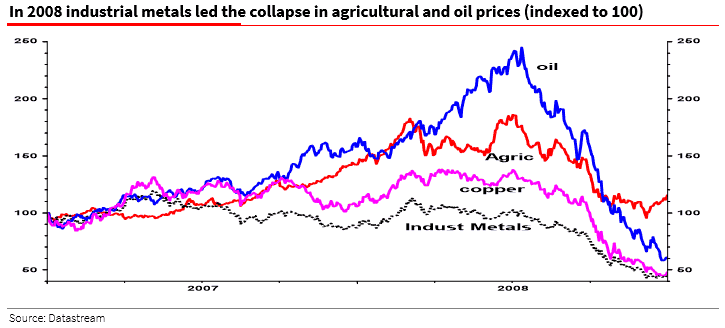

What will cause earnings and profits to contract, potentially putting more pressure on the S&P 500 index? A recession will do the trick, and commodities which are a real-time economic barometer say one is on the way. My colleague Albert Edwards had a terrific note on this on Thursday.

“There are times in economics when it is obvious the game is up and it’s time to get your head out of the sand.“

“All these data are consistent with the global economy plunging into a deep recession. Soft‑landers (now as rare as flat-earthers) claim that this is just excess speculative froth being blown off, but the bulls said that too in 2008 and look how that ended up!“

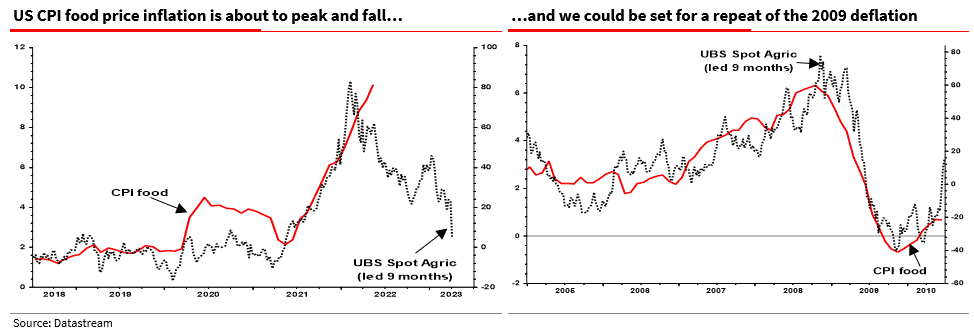

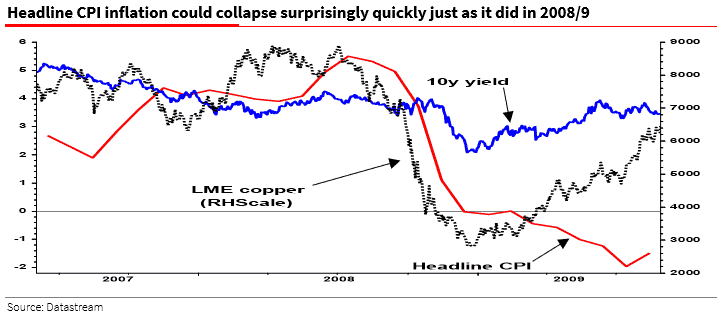

“The long and the short of it is that US CPI food price inflation is set to collapse into yoy deflation, just as it did in 2008/9 (see chart above). The same thing should happen with oil if there is a global recession despite the war in Ukraine. Oil prices this time last year were between $75-80/b, so it won’t take much of a fall from here to get into a yoy deflationary environment.“

“And that will be the big surprise in the next six months. As commodity prices slump – reflecting the unfolding global recession – headline CPIs will collapse around the world, and with them the inflation narrative.

But just to quickly remind ourselves of the power of ‘Dr Copper’ to accurately spot an ailing economy well ahead of economists, let’s look at what happened in 2008 in the chart below where headline CPI fell from 5½% to below zero in just a few short months.”

We agree.

Portfolio Update

To wrap up, during the previous four recessions and subsequent bear markets, the typical revision to consensus EPS estimates before the onset of a recession ranged from -6% to -18%, with a median of 10%. As noted, while forward P/E ratios have declined, much of that is due to the decline in the “P” and not the “E.” Therefore, if an earnings recession is coming, as the data suggests, then the current “bear market” cycle still has more work to do.

We are just starting the negative revision phase which makes risk management in portfolios a key priority for now. However, the reversal of those earnings trends will be key in identifying the bear market end and the beginning of the next investible bull market cycle.

As noted last week, we continue carrying higher cash levels and focusing on risk management for now. There is no easy way to navigate markets at the moment, but for those who have never been through a bear market, this is just part of the process.

Remain cautious for now. There is no rush to jump into markets trying to speculate a bottom is in. It likely isn’t.

We continue to suggest following the basic risk-management rules for now.

- Tighten up stop-loss levels to levels where you are comfortable selling if markets reverse again.

- Hedge portfolios against significant market declines. (swap equity funds for money market, stable value, or bond funds.)

- Take profits in positions that have been big winners (Rebalance funds that are above the normal weightings for your portfolio. Same with Company stock in your plan.)

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings. (Rebalancing risk regularly keeps hidden risks somewhat mitigated.)

Have a great week.

Market & Sector Analysis

Will Return In Two Weeks

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

July 7

“We sold our trading position in QQQ for a slight profit. As we have been discussing, the reflexive rally is eating into its oversold levels and approaching important resistance such as the 50dma. Further, we are being a little cautious heading into the unemployment data due tomorrow morning.”

- Sell 100% of QQQ

Lance Roberts, CIO

Have a great week!