Despite Surging Inflation, The Bulls Shake Off Weakness

In this 05-14-21 issue of “Despite Surging Inflation, The Bulls Shake Off Weakness.“

- Market Review And Update

- Rates Doing The Fed’s Work

- The Fed Will Be Late

- Portfolio Positioning

- #MacroView: NFIB Data Says It’s Only A Recovery

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

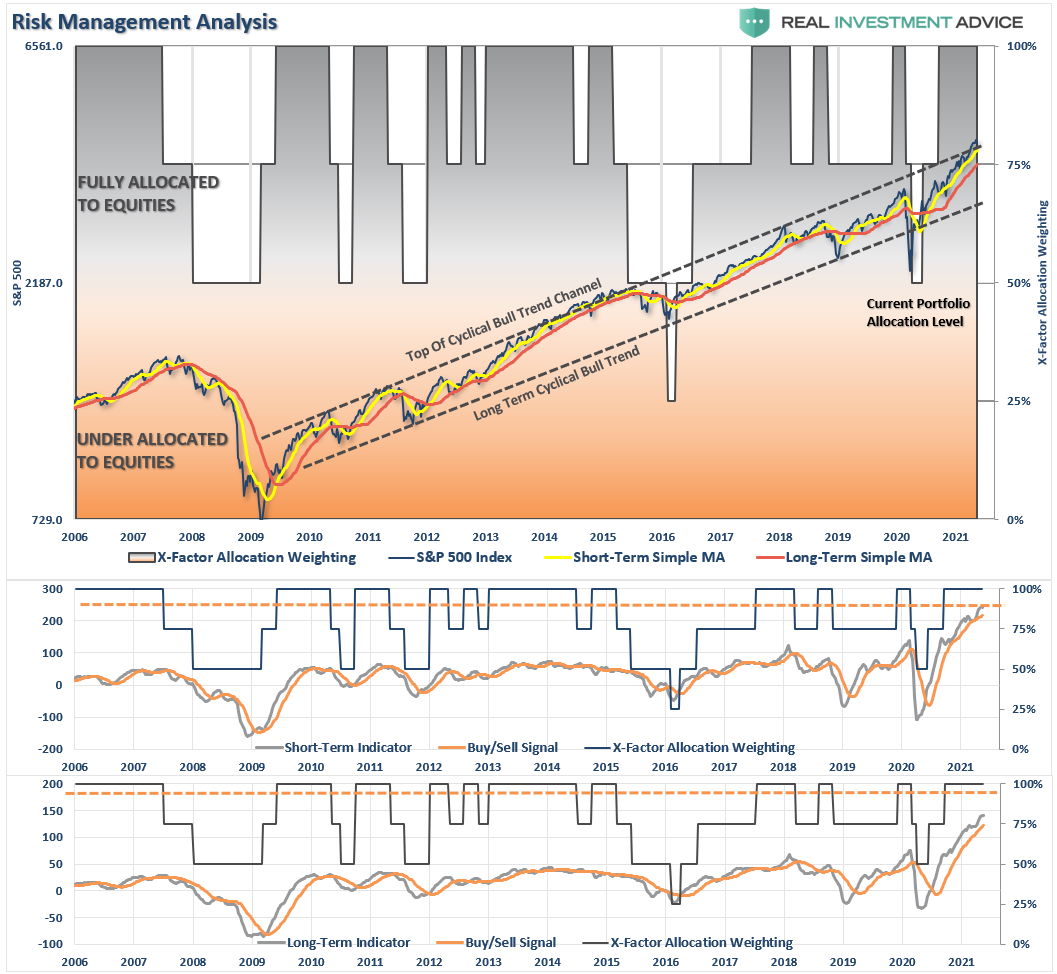

Market Review & Update

Well, that didn’t work out as planned. Last week, we said:

“Notably, the ‘money flow buy signal’ seemed to cross; however, we need some follow-through action on Monday to confirm. As shown, the uptick in money flows did allow us to add some exposure to portfolios in holdings we had taken profits in with the previous ‘sell’ signal.”

Well, that follow-through failed to occur. Not only did the “buy signal” not trigger, but the market also broke down through the previous consolidation range. As I said, it did not work out as planned. The last exposure we took on is now pressuring the portfolio momentarily, but we should benefit from the turn if we are correct.

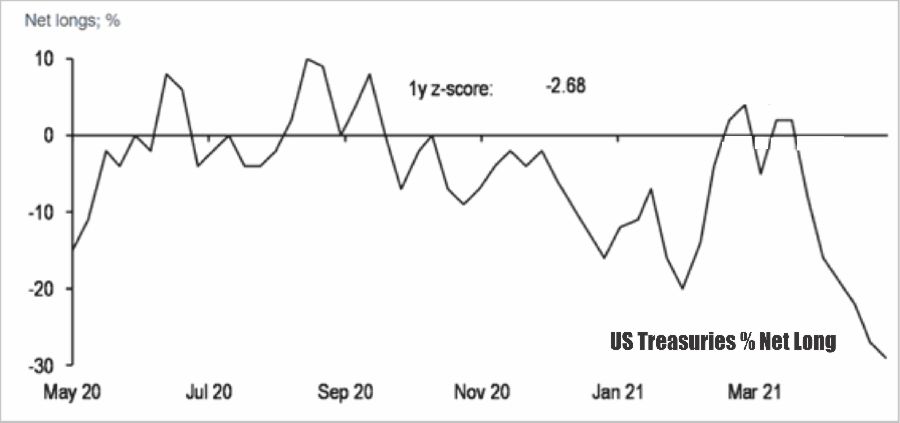

With markets deeply oversold on a short-term basis, with signals at levels that generally precede short-term rallies, the rally on Thursday and Friday was not unexpected. Notably, the S&P 500 did hold support at the 50-dma and rallied back into the previous trading range. Furthermore, institutional investors have cut their exposures by 50% in just two weeks, primarily big tech, which provides fuel for a rally.

We will hold exposures at current levels for now. However, instead of looking for a more extended rally into mid-summer, we suspect this rally will be pretty short-lived.

As stated last week, overall, the market trend remains bullish, so there is no need to be overly defensive. We still expect to see a deeper correction as stimulus fades from the system in the next month. At that point, we will become more defensive in positioning as the peak of economic growth and earnings becomes more apparent.

An Inflation Primer

On Thursday’s “3-Minutes” video, I review the recent inflation numbers to put them into perspective. While there is some panic over the headline numbers, there are valid reasons to expect inflationary pressures to be transient.

As stated above, we expect inflation to subside later this year, along with economic growth.

As such, we continue to focus on our risk management accordingly for now. If we are correct in our assessment about the roll-off effect of stimulus and liquidity, we could well see bonds outperform stocks in 2022. We are watching very closely as we currently hold minimal duration in our fixed-income portfolios. If we begin to see the very negative sentiment on bonds reverse, as inflationary pressures subside, we could well see an excellent buying opportunity.

The problem for the markets is the Fed is going to be late.

Rates Doing The “Fed’s Work”

In last week’s message, we said:

“Over the next couple of months, there will be an evident surge in inflation, which the Fed wanted. However, that surge in inflation may come in a lot “hotter” than they anticipated. If that occurs, bond yields will jump higher, effectively “tightening” monetary policy very quickly.”

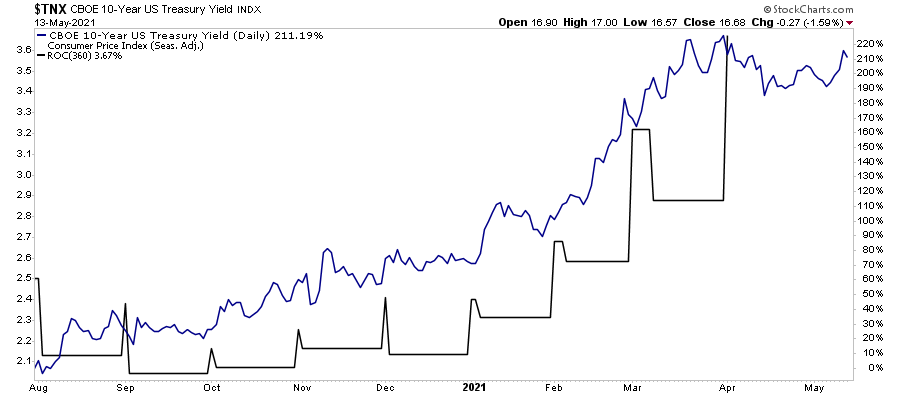

Such is what we saw on Thursday as bond yields jumped to nearly 1.7%. While rates did fall back mildly on Friday, the rise in rates from the August lows increases the cost of capital. (Chart shows the percentage increase in rates versus the annual inflation rate,)

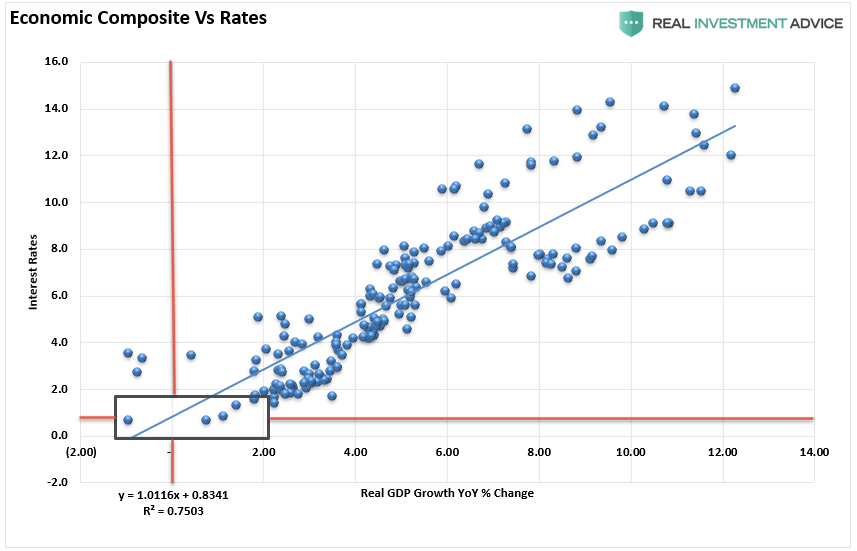

Given the long and highly correlated history of GDP, Inflation, and Interest Rates, it is no surprise to see rates pacing inflation currently. As noted in “No, Bonds Aren’t Over-Valued.”

“As shown, the correlation between rates and the economic composite suggests that current expectations of sustained economic expansion and rising inflation are overly optimistic. At current rates, economic growth will likely very quickly return to sub-2% growth by 2022.”

Note: The “economic composite” is a compilation of inflation (CPI), economic growth (GDP), and wages.

At the peak of nominal economic growth over the last decade, interest rates rose to 3% as GDP temporarily hit 6%. However, rates correctly predicted that economic growth would return to its long-term downtrend, and inflation would decline. Bonds were right as the economy fell into recession in 2020.

Once again, economists predict 6% or better economic growth, yet interest rates are roughly 50% lower than previously. The bond market is screaming that:

- Economic growth will average between 1.75% and 2% over the next few years; and,

- Deflation still trumps inflation.

Moreover, the Fed is manipulating inflation expectations.

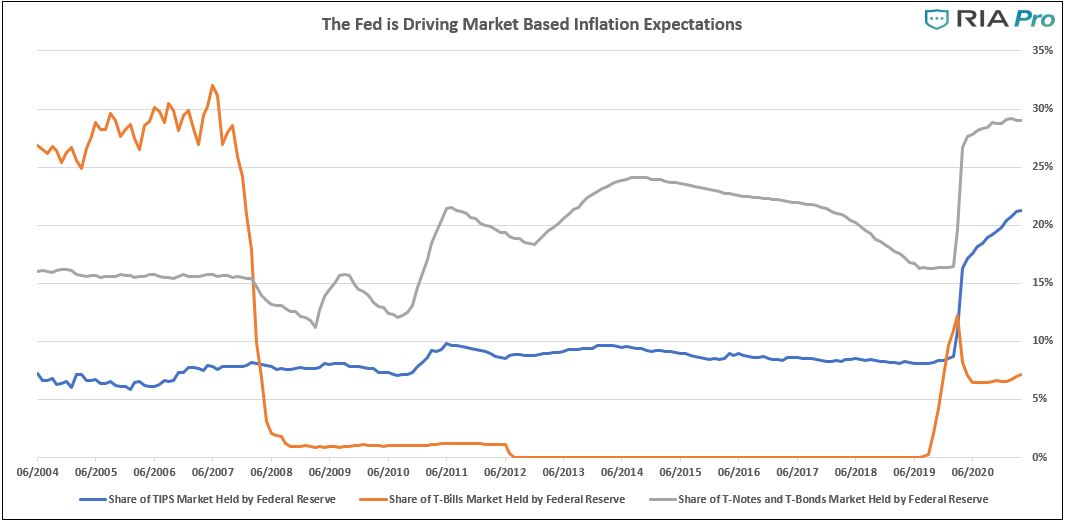

The Fed Is Driving Inflation Expectations

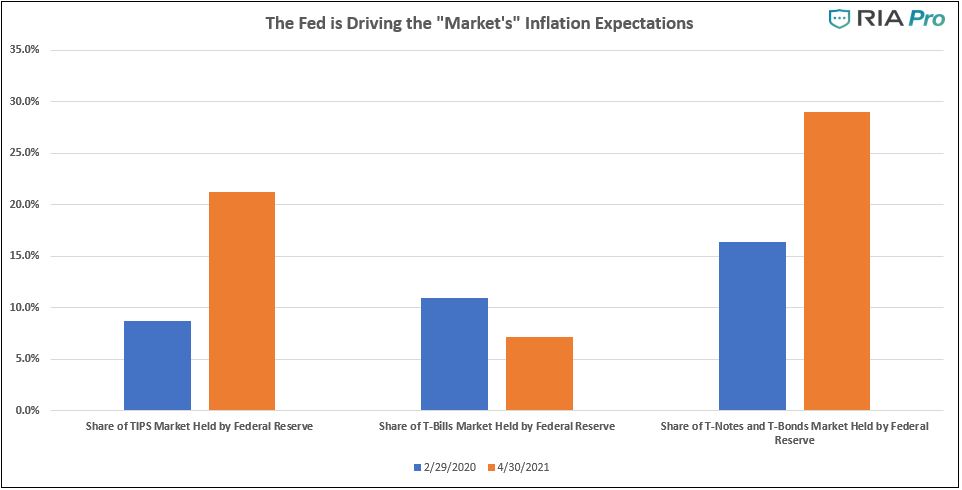

In recent months, market participants continue to rely heavily on implied inflation expectations. The reliance led to much media-driven commentary relating to allocation decisions in the “inflationary environment.” From that analysis, investors piled into materials, energy, and financial companies, which did indeed provide short-term outperformance. The more deflationary sectors of technology, staples, and utilities, not surprisingly, underperformed.

The problem is that the “market-based” expectations aren’t market-based at all. The first graph below shows the massive amounts of inflation-protected Treasury bonds and notes. Such large purchases create distortions in the very market investors are relying on for inflationary information. Instead, the Fed is skewing the implied inflation calculations.

The following chart from our analyst, Nick Lane, shows the history of these purchases and the impact on inflationary expectations.

Just as the Fed’s monetary interventions distorted signals in the asset market, those interventions are now distorting signals in the TIPs market.

In other words, investors depend on signals from the market to allocate capital and adjust allocations. However, when those signals get manipulated, false readings can lead to significant future dislocations when reality collides with fantasy.

Such is why the Fed will make a mistake.

The Fed Is Going To Make A Mistake

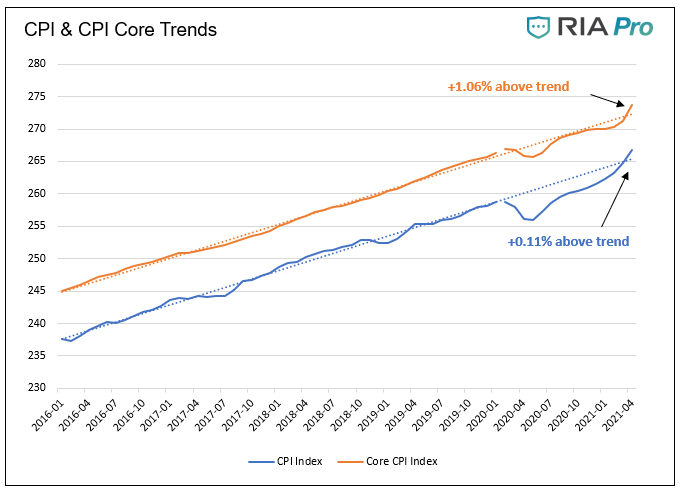

As discussed, the “base effects” (comparison versus last year’s data) make price inflation appear much higher than it is. The graph below puts the CPI indexes in context with their trends of the previous five years.

Currently, the broad CPI index is only .011% above its trend. The Core CPI, which excludes food and energy, is 1.06% above its trend. If the inflationary impulse is transitory and dies out over the next few months, inflation data will end close to where it was pre-pandemic.

The Fed is now potentially in a difficult position with inflationary “expectations” rising, caused by their actions, which increases the risk of a “policy mistake.”

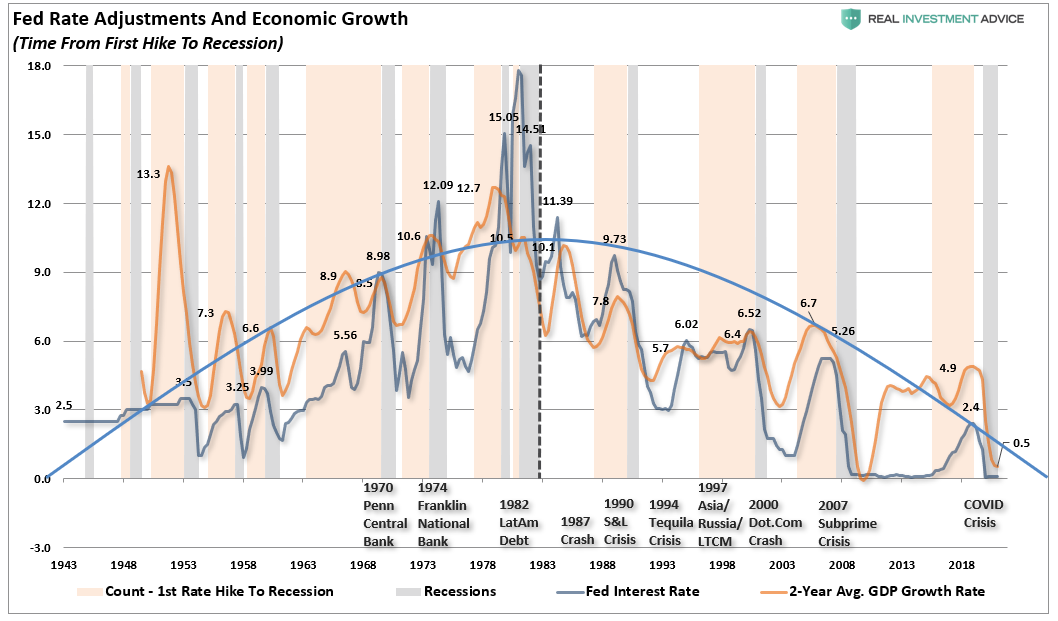

Given the Fed waited so long into the economic cycle to hike rates they weren’t able to gain much of a spread before the economy contracted. Historically, there have been ZERO times the Federal Reserve hiked rates that did not negatively affect outcomes.

The problem for the Fed is that the bond market is not worried about surging inflation. Despite economic growth expectations of as much as 6%, interest rates are trading below 2%. Given the close correlation shown above, it is a message you should not dismiss quickly.

The “real economy” is heavily debt-financed, and as such, cannot withstand substantially higher rates. Consequently, the Fed is caught between hiking rates to quell transient inflationary pressures, thereby deflating the most significant asset bubble in financial history, or doing nothing and hoping no one pushes the “big red button.”

Unfortunately, history is full of instances where someone panicked.

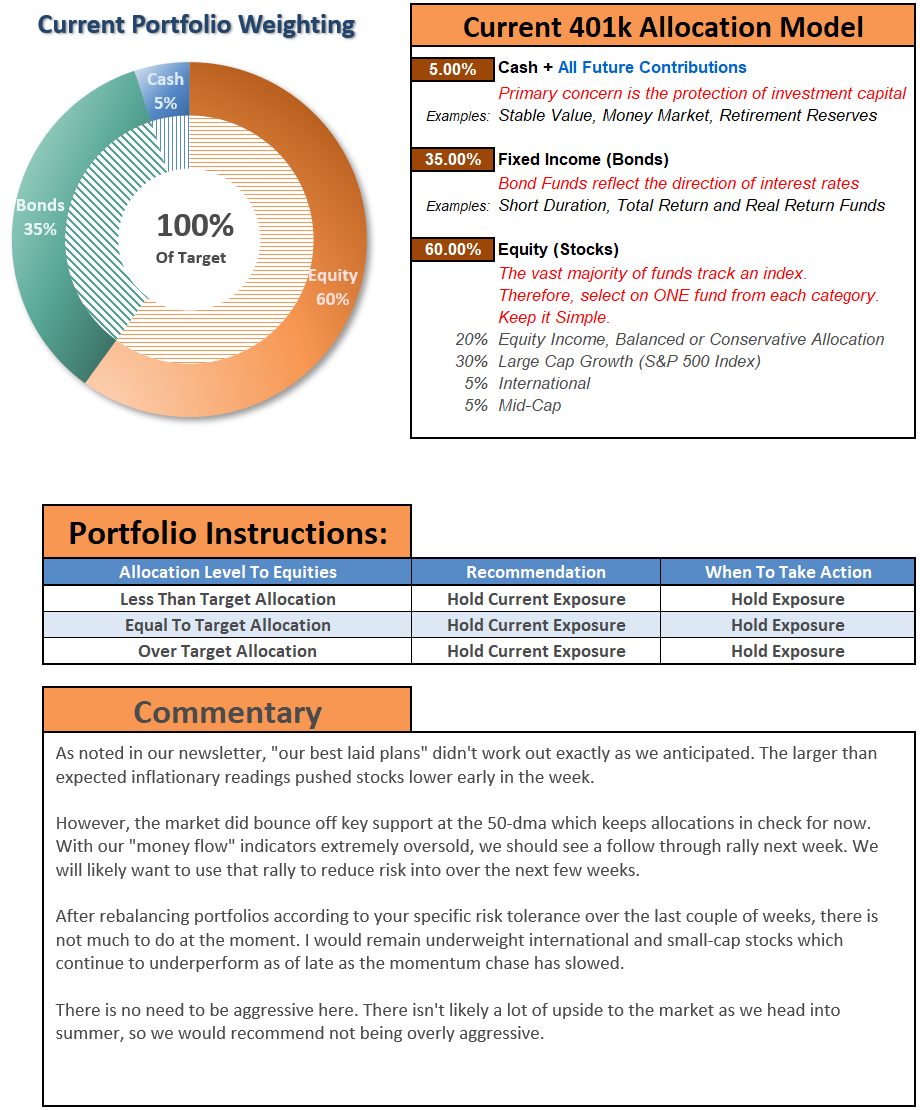

Portfolio Update

“The road to hell gets paved with good intentions.” – Unknown

As noted above, our attempt to “front-run” our “money flow signal” did not work out as planned as the signal did not turn. While we did not take on a tremendous amount of exposure, the increased exposure to the decline mid-week was certainly not part of our plans.

As is always the case, technical analysis works best when you wait for the signals to occur. While a harsh lesson to relearn, the damage was minimal. With market risk reduced, our entry levels should perform over the next couple of weeks.

Timing is always the tricky part.

As Michael Lebowitz concluded in “Fortify Your Wealth:”

“Given the economic climate and extreme market risks and rewards, we continue to take an agnostic view of markets. We do not get wed to opinions of economic activity or inflation, or how they may steer markets.

Paying top dollar for assets requires independent thinking and careful attention to market activity. From the brightest traders on Wall Street to the halls of the Federal Reserve and in the studios of the self-anointed media economic experts, there is zero appreciation for the potential of massive forecasting errors.”

Historically, investors get rewarded for going against the crowd. Such is especially the case when the masses are in agreement on what the future holds.

“When all experts agree, something else is bound to happen.” – Bob Farrell.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

Discover All You Are Missing At RIAPRO.NET

Come find out what our RIAPRO.NET subscribers are reading right now! Risk-Free For 30-Day Trial.

- Sector & Market Analysis

- Technical Gauge

- Fear/Greed Positioning Gauge

- Sector Rotation Analysis (Risk/Reward Ranges)

- Stock Screens (Growth, Value, Technical)

- Client Portfolio Updates

- Live 401k Plan Manager

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert, do not hesitate to contact me.

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

Have a great week!