Inside This Week’s Bull Bear Report

- Market Review & Update

- Complacency Seems Overly Complacent

- How We Are Trading It

- Research Report – Could Student Loan Payments Be The Trigger?

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

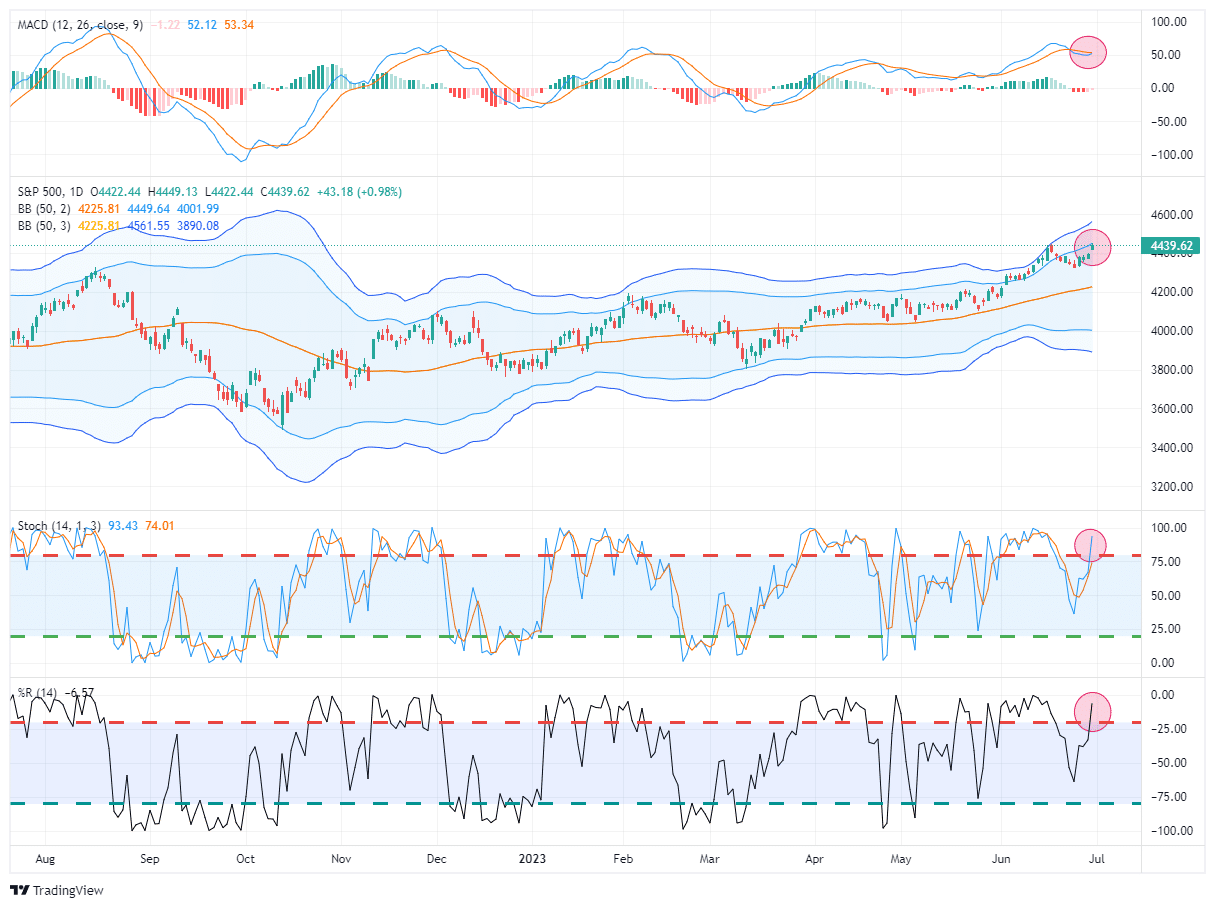

Market Review & Update

Despite the recent correction, complacency remains highly complacent.

Last week we noted that the correction had triggered a market sell signal. As stated, when triggered from relatively elevated levels, these sell signals suggest a more protracted correction or consolidation. However, the correction was shortlived as a successful test of the 20-day moving average brought traders back into the market. In a bullish advance, it is not uncommon for buy and sell signals to flip back and forth at elevated levels.

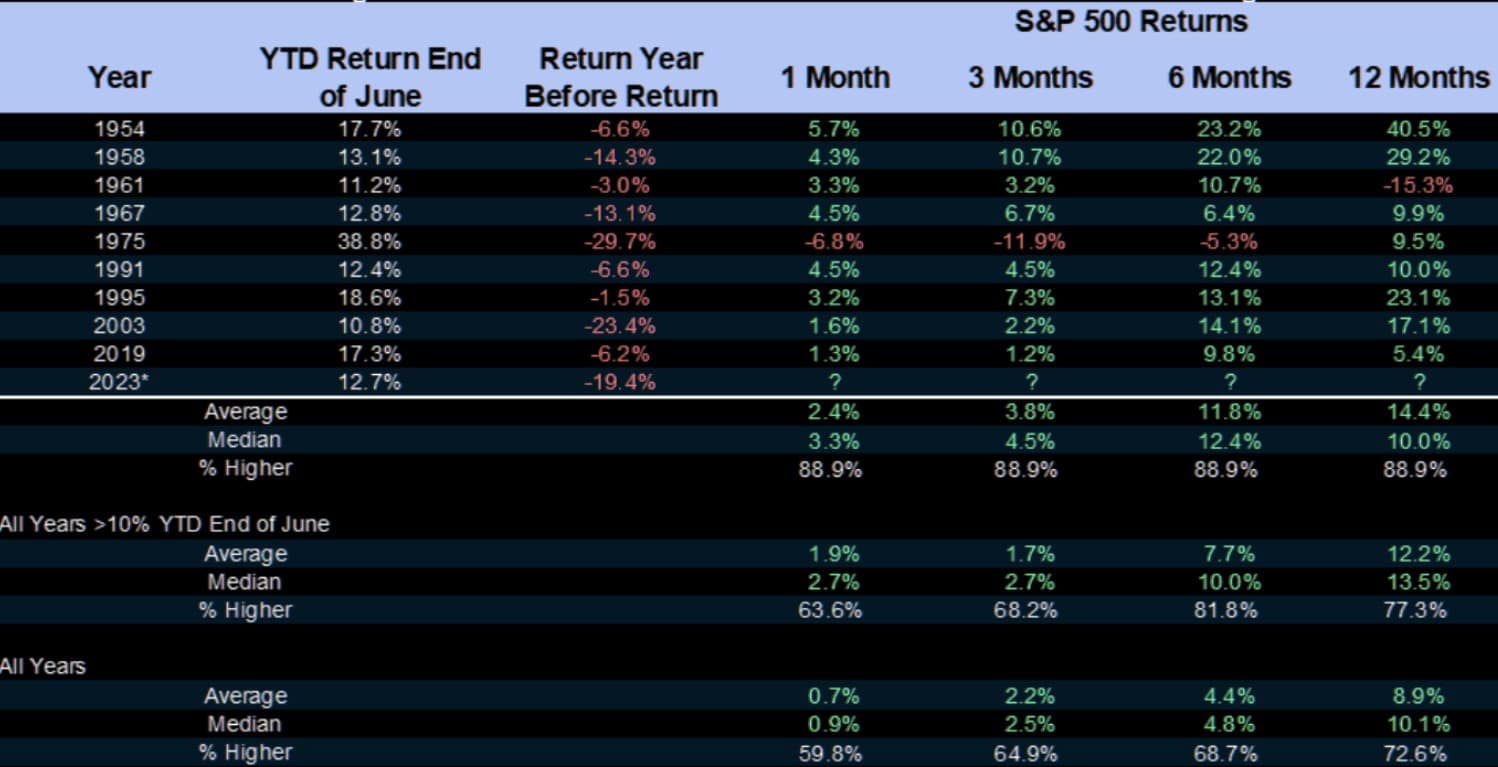

With the end of the quarter behind us, portfolio managers are trying to play “catch up” with returns over the next six months. The table below shows that the second-half returns tend to be strong when the market is up 10% in the year’s first half.

With bullish optimism quickly returning to the market, the pressure to chase performance from the “Fear Of Missing Out” will continue to provide a “bid” under stocks.

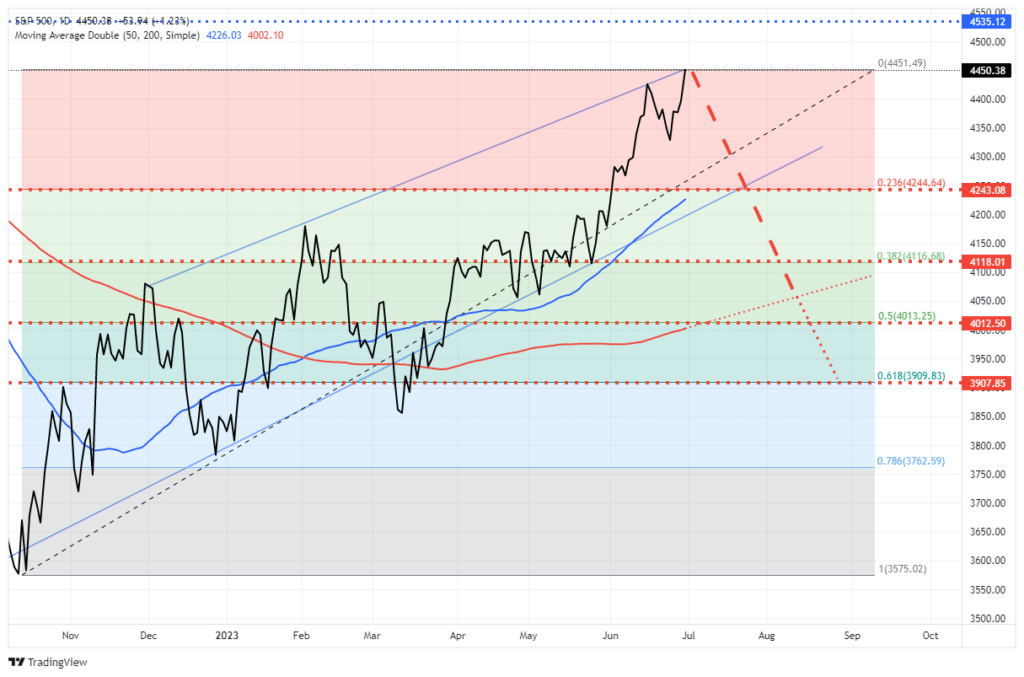

However, such does not remove the potential for a 5-10% correction. Such corrections are normal within any given year and will provide the best entry point to increase equity exposure near term. Using Fibonacci retracement levels, investors should consider adding exposure at 4250, down to the 200-DMA. A violation of the 200-DMA would suggest a larger corrective process at work, most likely coinciding with some market-related event.

While such an event is unlikely, we can not entirely dismiss the risk of a more significant contraction, given the more extreme deviations from longer-term moving averages. What would cause such a contraction? Such would be an exogenous and unexpected event that changes market participants’ complacency about risk.

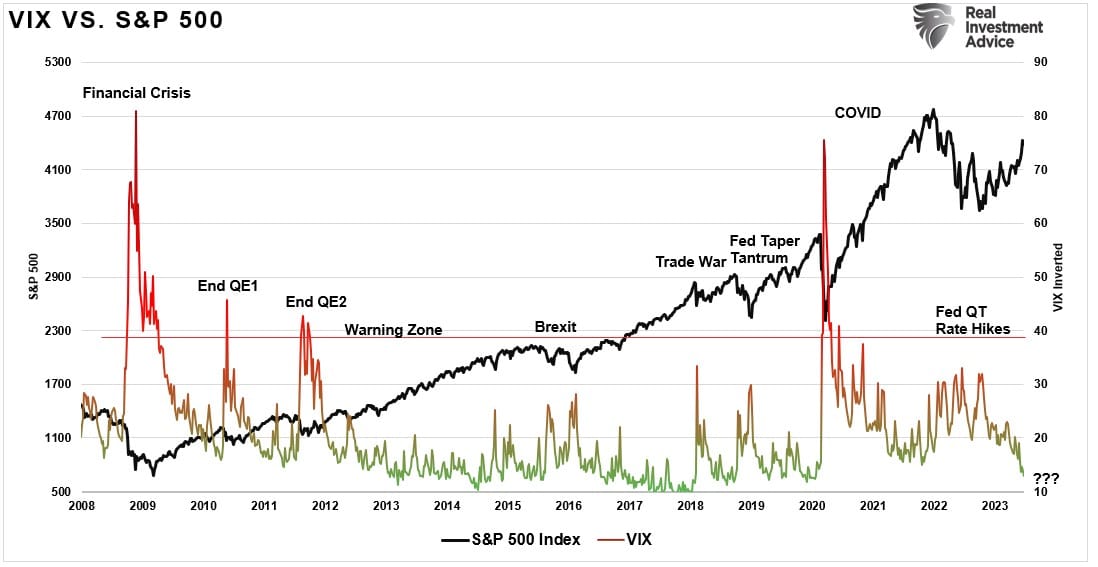

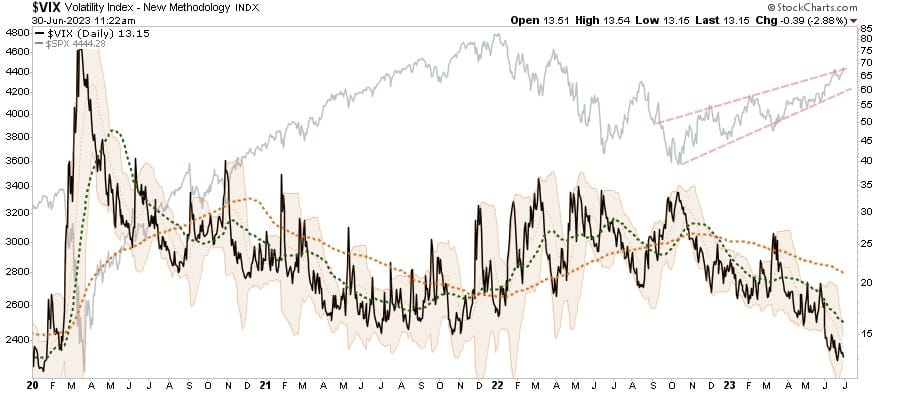

The volatility index has historically reflected that concern, but investors hope it’s different this time.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Complacency Is Very Complacent

In last week’s discussion, we noted our concern about market complacency.

“Another concern we have about the current rally is the collapse in market volatility. While there is strong momentum, and bullish psychology, behind the rally, extremely low volatility readings tend to align with short-term market peaks and corrections.

Historically, the volatility index has sharply increased during market downturns as investors scrambled to buy protection against the market decline. This week, Bank of America also took notice, asking, “What is driving the equity volatility crush and when will the VIX base, and how long can it stay?”

It is certainly an interesting issue with the markets currently. But as BofA notes:

“While equity vol has fallen in tandem with cross-asset vol in June, the VIX was already so complacent about the macro risk that its further compression seems to us better explained by positioning and psychology than fundamentals alone.“

Such is a good point considering that volatility was declining even as earnings deteriorated over the last two quarters, and the bulk of the advance this year has been driven purely by a valuation expansion. That advance is further challenged by the Fed’s aggressive rate hikes, which should slow economic activity even though it appears delayed.

However, as is always the case, the market can do illogical things in the short term.

“Seasonality suggests a VIX floor could be near – even if the catalyst higher remains elusive – while still-elevated data vol/policy uncertainty, the near-record gap between equity & rates vol, and the lagged effect of higher rates all make today’s macro backdrop antithetical to the 2013-19 regime that set records for futility in equity vol.“ – BofA

In other words, to put a twist on John Maynard Keynes’ famous saying, “Equity volatility could remain lower for longer than you can remain solvent.”

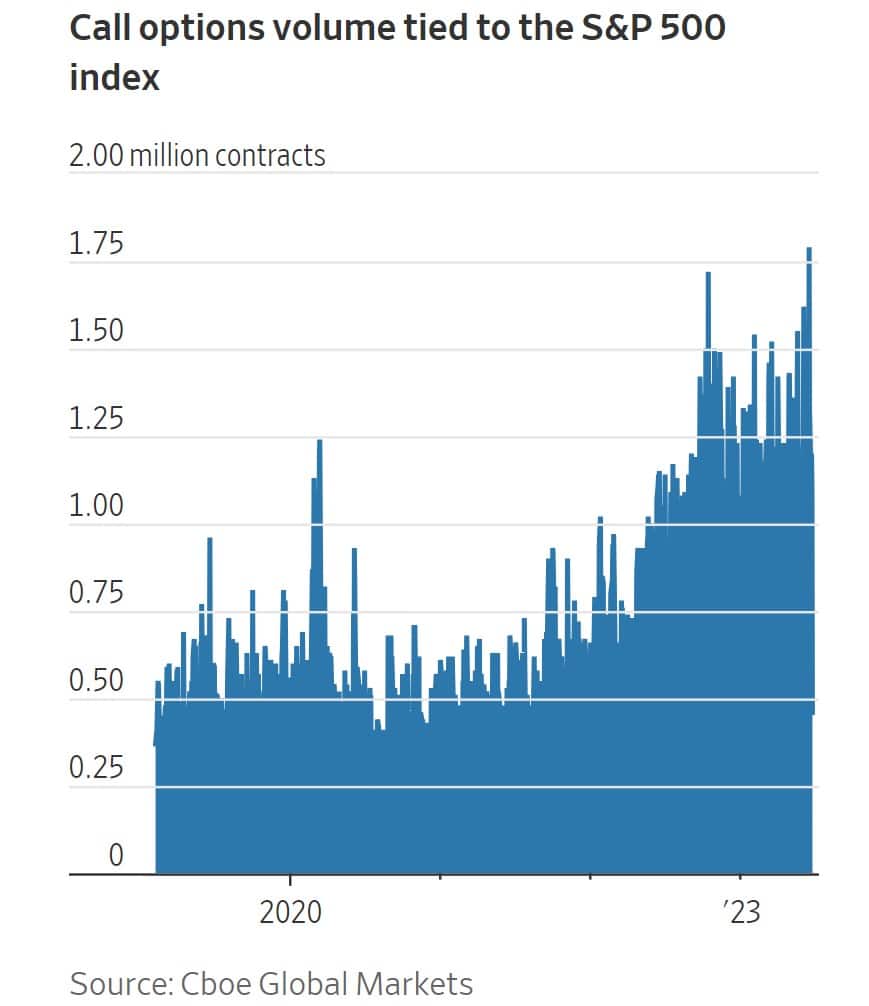

Of course, given the large number of call options outstanding on the S&P 500, many people are betting that low equity volatility is here to stay. However, from a purely technical basis, the current deviation from the 20, 50, and 200-day moving averages is getting rather extreme. Historically, such deviations result in a short-term reversion that should, in theory, coincide with a market correction. But, such a correction remains elusive amid the current complacency and “F.O.M.O.”

Risk Certainly Remains

As the WSJ noted:

“If you started the year bearish, you’ve been really under-allocated. Investors are looking at a market that’s rallied 14% and, almost not by choice, they feel the need to hop on the train.”

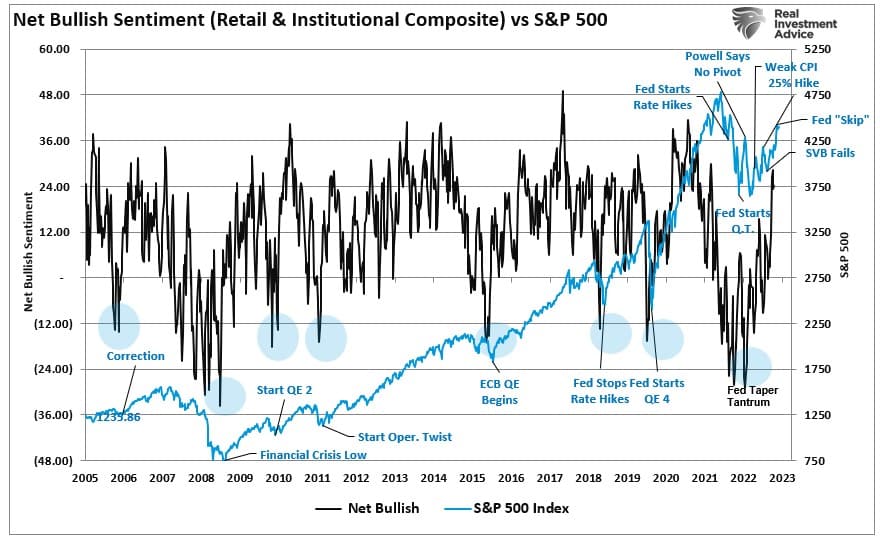

Investor sentiment remained decently bearish until a few weeks ago when it exploded higher. As the market continued its advance and fears of another down leg faded, complacency rose, and the fear of missing out, or F.O.M.O, set in. Our composite index shows that investor sentiment has returned to more bullish levels.

Not surprisingly, with investor complacency elevated, they are piling into the market to gain the most leverage they can on bullish bets.

“Options wagers on the tech-led rally have also extended to other corners of the market, such as small-cap stocks. Even without a big market drawdown, should stocks begin moving in lockstep, that could boost turbulence in the broader market.

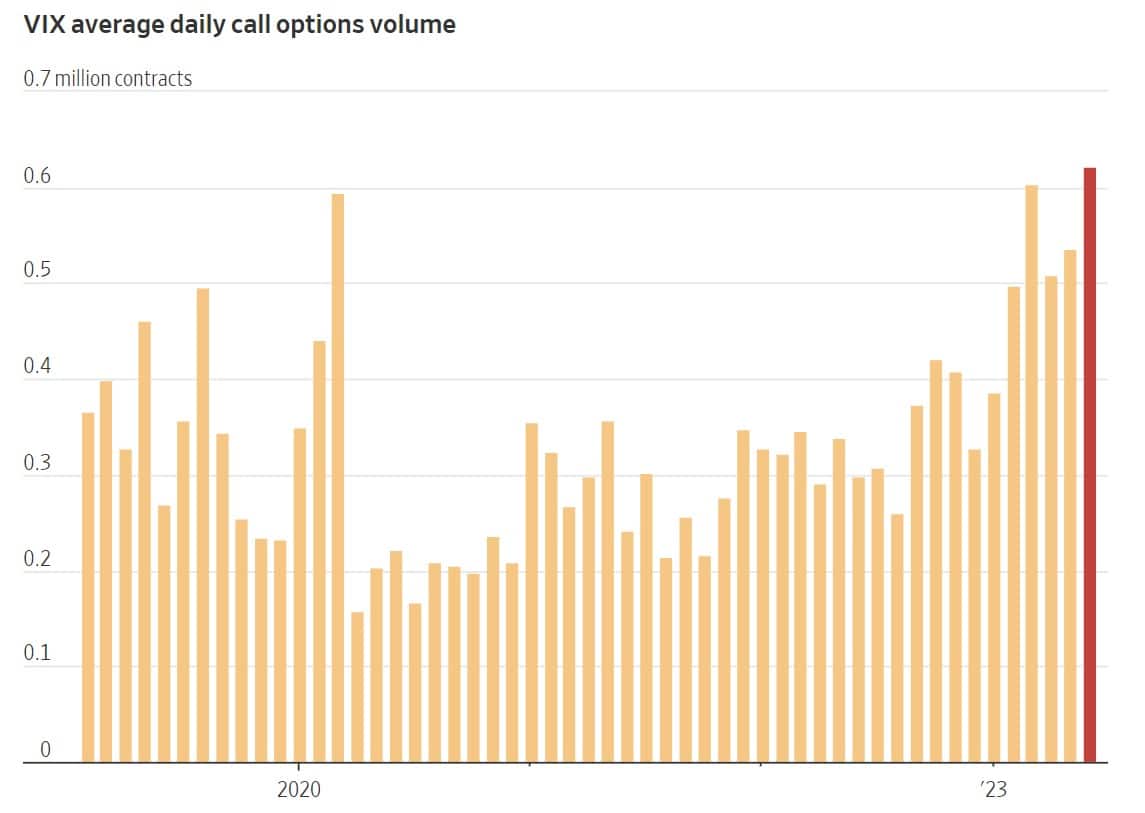

Traders are piling into wagers that would profit if that occurred. More call options tied to the VIX have changed hands on an average day in June than in any other month on record, according to Cboe Global Markets data.” – WSJ

As volatility collapses, investor complacency rises as they become emboldened to make more aggressive bets.

“It has now been more than three months since the S&P 500 has pulled back at least 3%, one of the longest such stretches since World War II, Deutsche Bank research shows. The average weekly move for the benchmark has been less than 1% in either direction since the end of March, according to FactSet. In late 2022, the index averaged swings of roughly 2.6% each week.” – WSJ

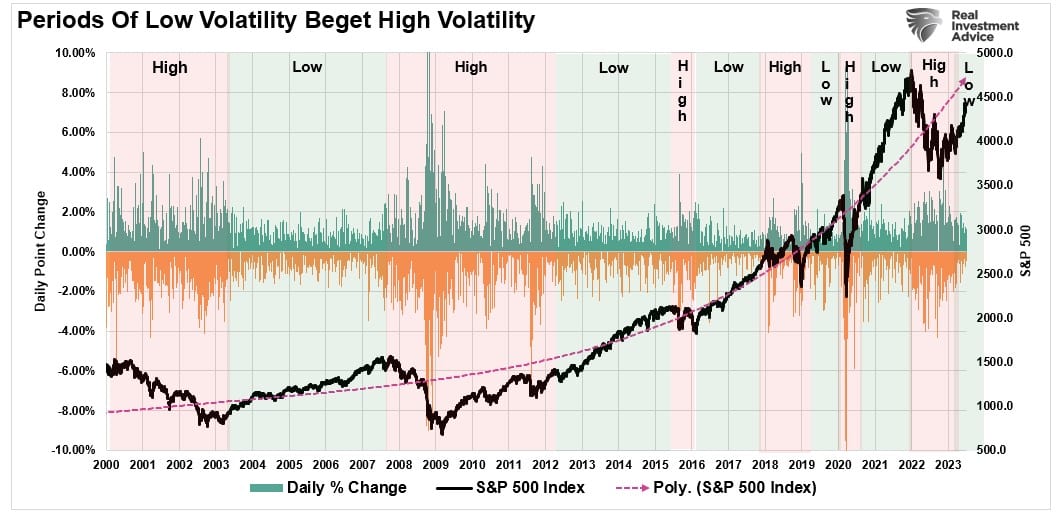

As is always the case, periods of low volatility lead to periods of high volatility. Those alternating periods have become more frequent in recent years as monetary interventions have gone into overdrive.

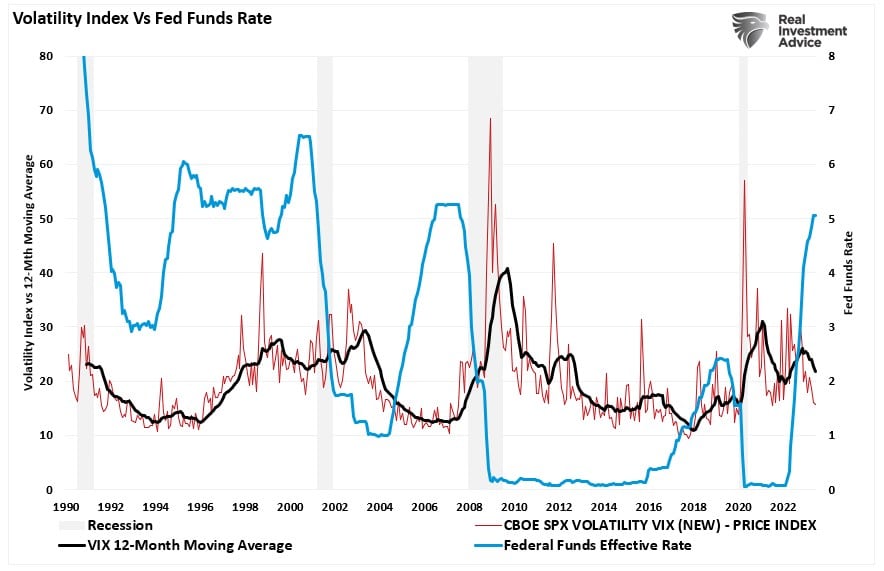

While volatility is low currently, it is unlikely that volatility has been permanently suppressed. There is a decent correlation between volatility and the Fed’s rate-hiking campaign. Given that rate hikes eventually “break something,” particularly given the impact of higher borrowing costs on an increasingly leveraged economy, this time is likely no different. However, there is undoubtedly a lag effect between volatility and rate hikes, suggesting a recession remains a key risk.

Notably, while investors are becoming exceedingly complacent about a continued low volatility environment, they may be walking into a trap. Unfortunately, investors never know with certainty until the “trap is sprung.”

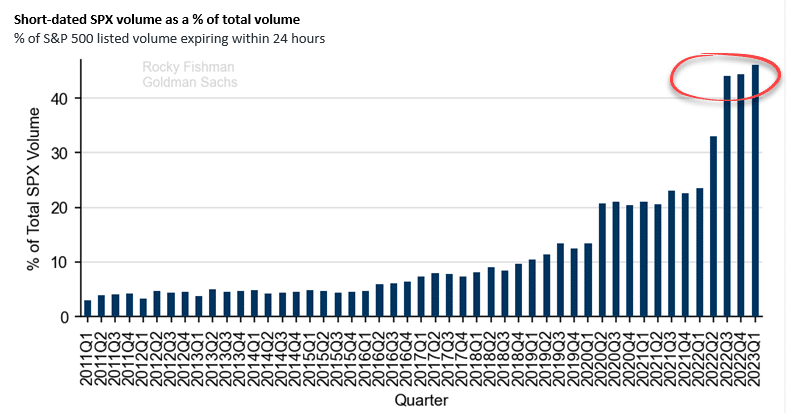

Nonetheless, the current environment has many suggesting that “The volatility index (VIX) is broken.” One reason supporting that claim is the rise of short-term options termed “0DTE” or “Zero Days To Expiration.”

0DTE (Zero Days To Expiration)

There has been a significant change in the options market over the last several quarters, explaining this change in the behavior of the volatility index.

These extremely short-term put-and-call options on individual stocks and indexes expire within 24 hours. As the chart shows, almost half of the options volume on the S&P 500 is 0DTE. Such dwarfs the single-digit rates existing before the pandemic.

More importantly, the traditional measure of “fear and greed” in the financial markets, the VIX, does not consider these 0DTE options.

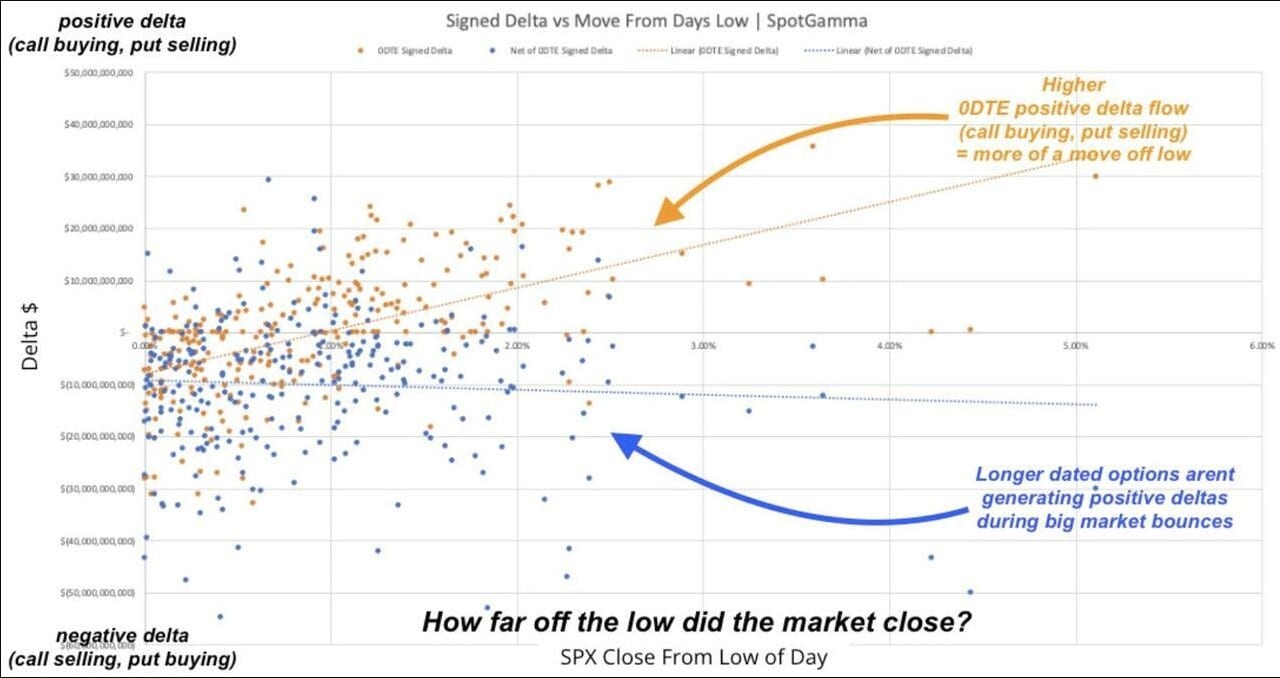

Given the minimal time until these options expire, most of the activity in 0DTE options is likely due to speculators. In many cases, volume on 0DTE options spikes before crucial economic data releases. Wall Street banks, which reside on the other side of 0DTE trades, must hedge them. To hedge those 0DTE options, Wall Street must buy or short the underlying index or stock as it moves in favor of the owner of the option.

The growing concern is that as 0DTE option interest grows, dealers must actively hedge more significant amounts. Banks must buy or sell aggressively if the options trades are correct, either bullish or bearish. Such could exaggerate an already significant market move.

It is certainly possible the rise of 0DTE options may be contributing to the suppression of the volatility index, making it appear to be less effective near term. However, we won’t know with certainty until the next “volatility event” arrives. Unfortunately, it could be too late for many investors to do much about risk management.

“The risk from 0DTE (in our view) comes from a heavy imbalance (ex: too many non-hedgers short downside). We think a lot of 0DTE is one dynamic-hedger trading with another dynamic hedger, and/or underlying replacement (i.e., buy calls instead of long stock).” – SpotGamma

Sure, maybe the “VIX is broken.” But these “low volatility regimes” can last longer than you expect. As Nick Colas recently explained:

“Once we’re in a [low-volatility] regime, it tends to last unless a true ‘unknown unknown’ comes along. With the VIX well below average now, we look to be in a low-vol/good return environment until a genuine shock comes along. It is hard, but not impossible, to ‘surprise’ the VIX with new information which switches it from running below trend to suddenly above trend.

This is not a bright green light for further equity gains in 2023, but it does set the bar quite high regarding what sort of catalyst is needed to derail the current rally.”

We agree, which is why we have increased our equity exposures but remain focused on risk controls.

How We Are Trading It

This past week, the Federal Reserve is becoming more vocal about the need for further rate hikes. While investors and consumers ignore the Fed, it is unlikely the economy will come out unscathed. However, as we discussed previously, the lag effect of rate hikes may take longer, given the massive monetary interventions in the economy. While we are certainly more bullishly positioned near term, the risk of “something breaking” has not been entirely resolved.

As noted last week, mounting evidence shows that October marked the low of the current market cycle.

“However, such does not mean that a meaningful decline can’t occur within a ‘new bull market’ context if Fed resumes a more aggressive stance. As such, we continue to make tiny moves to align the risk profile of portfolios to the market. Given the recent buy signals from our indicators, we increased exposure but are looking for pullbacks to support providing better risk/reward entry points for further additions.”

We remain underweight in overall equity exposure and overweight in defensive, value-oriented positions. Such will protect the portfolio from any short-term market declines, at which time we will use our existing cash holdings to increase our cyclical exposure accordingly. However, that defensive posture is penalizing our performance this year after last year’s significant outperformance. We suspect we will get an opportunity, particularly as we move into 2024, to make up that performance gap and rebalance risk tolerances accordingly.

Let me reiterate our rules from last week as we head into the potential “summer malaise.”

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against potential market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings.

Have a great 4th of July holiday.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates (Formerly 3-Minutes)

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

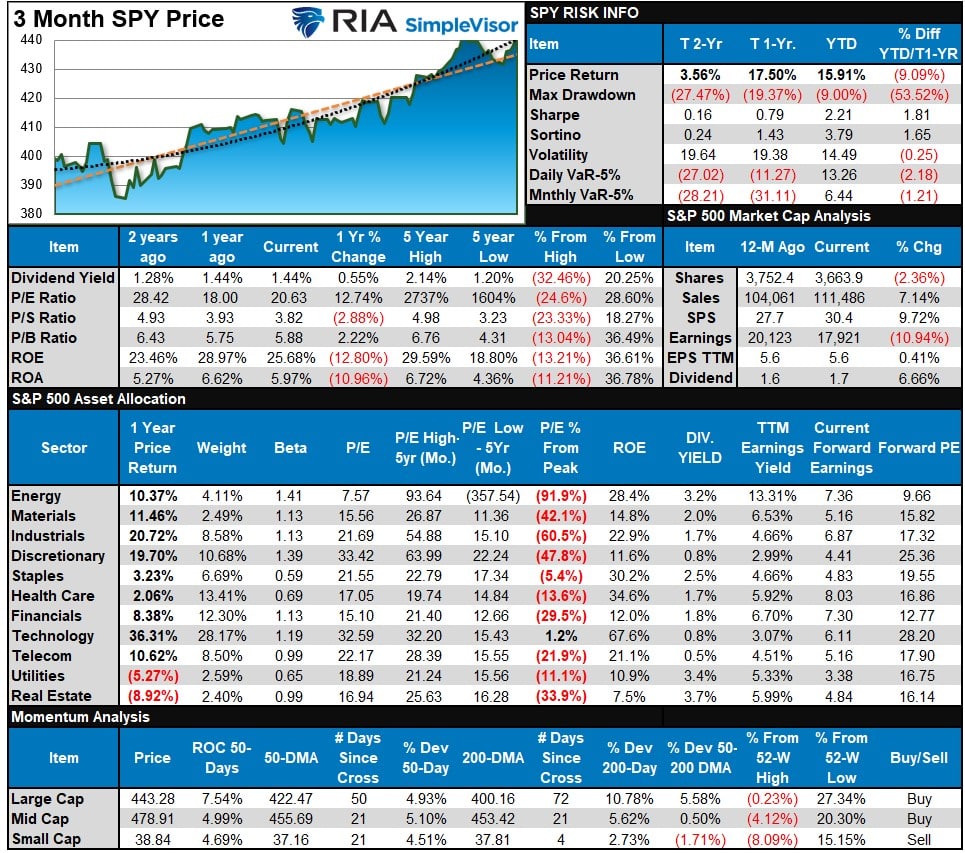

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

Last week we noted that the expected correction did resolve some of the more extreme short-term overbought conditions and that “while a bounce is likely next week, prices likely have to work themselves lower.”

The market did indeed bounce rather strongly amid high levels of complacency, taking the market to a new 52-week high this past week. However, that bounce pushed much of the broad market complex back into extreme short-term overbought conditions. Such suggests more consolidation is needed, but any dips to support levels should be bought.

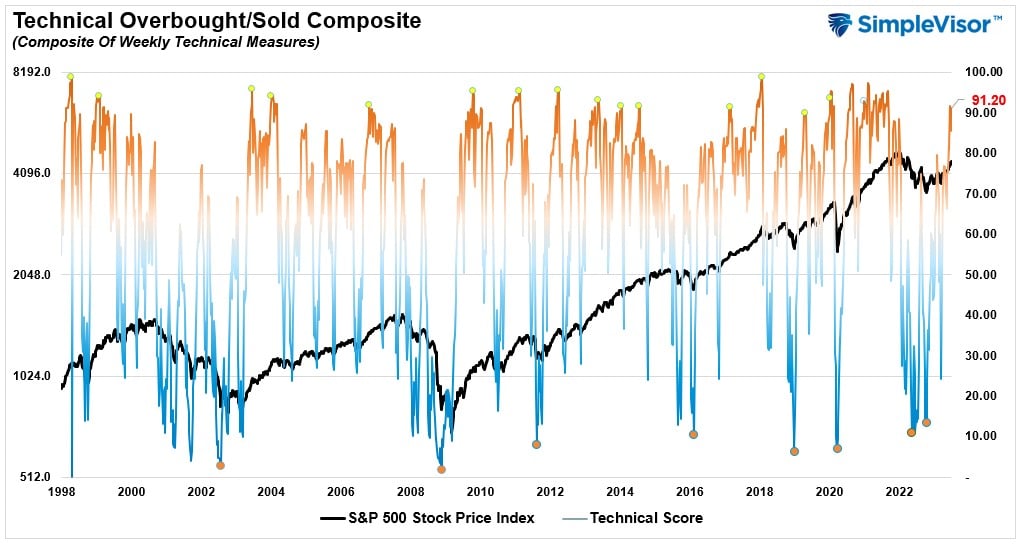

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 91.20 out of a possible 100.

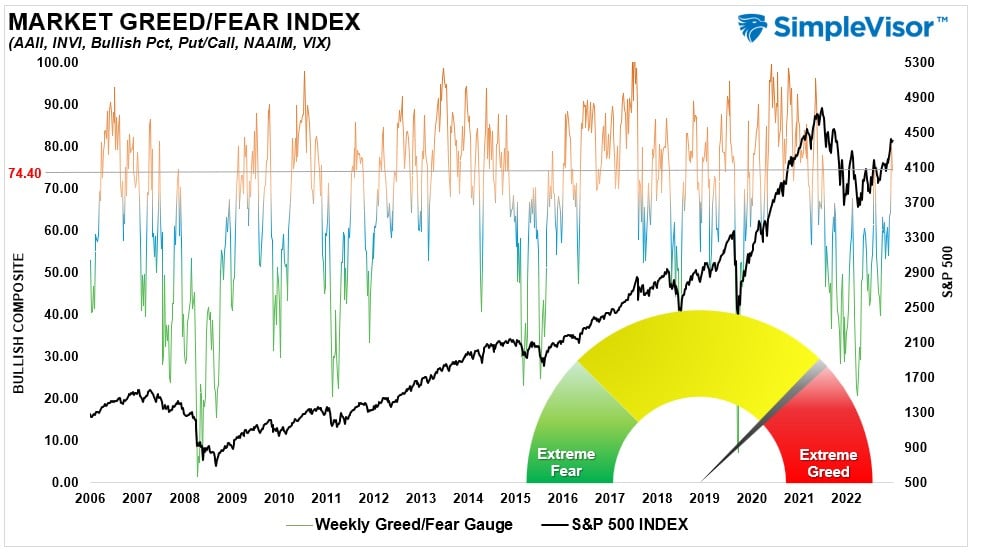

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 74.40 out of a possible 100.

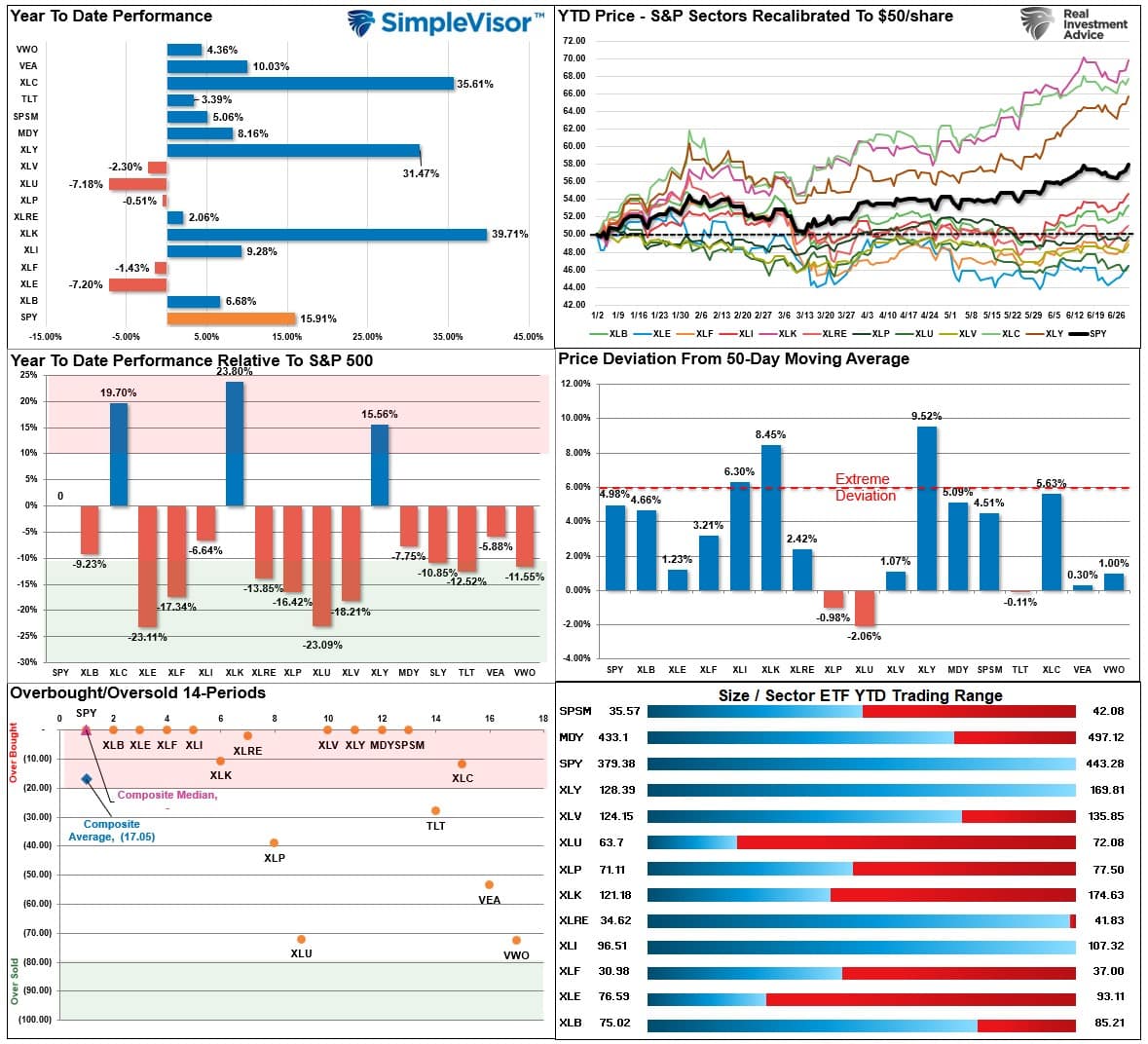

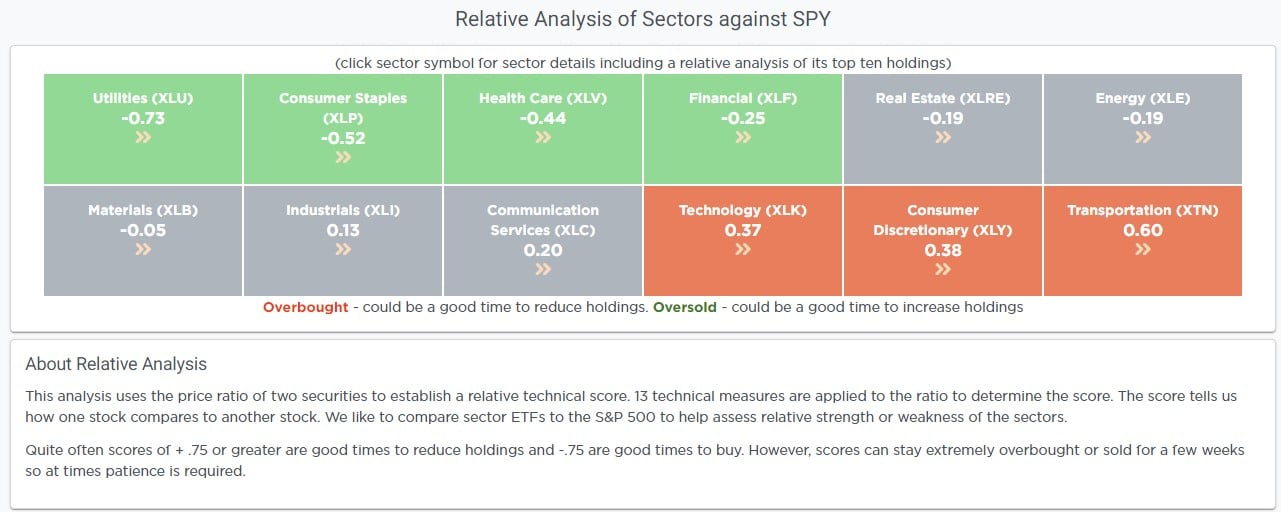

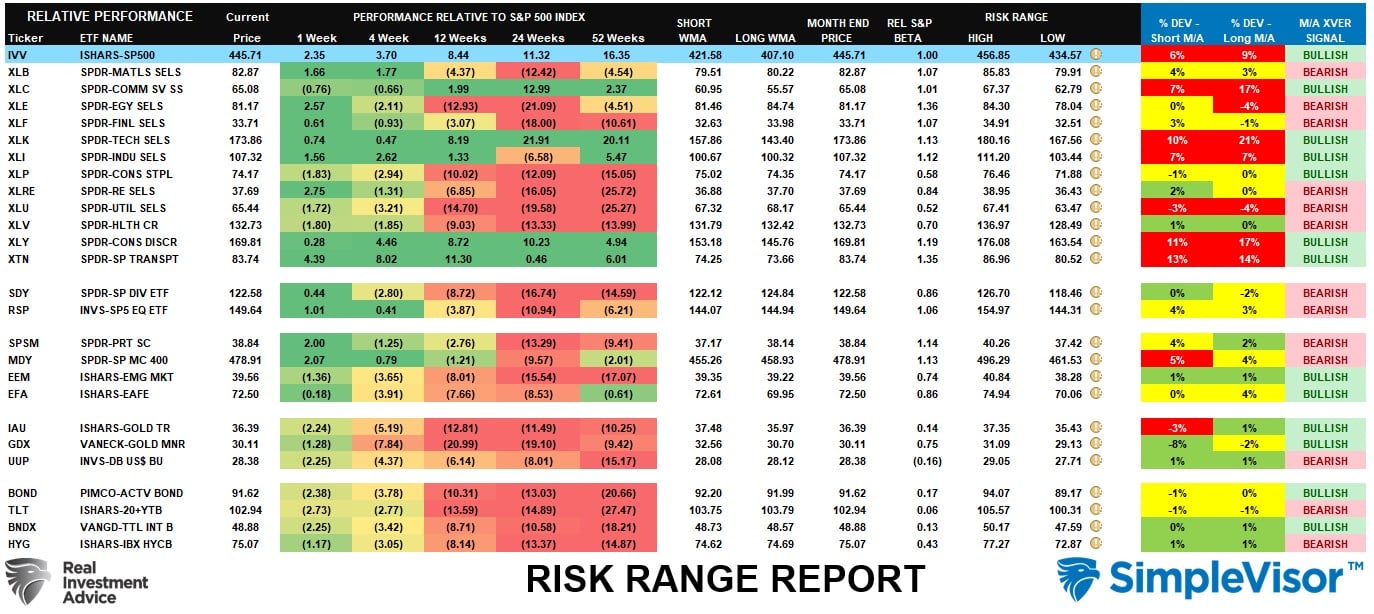

Relative Sector Analysis

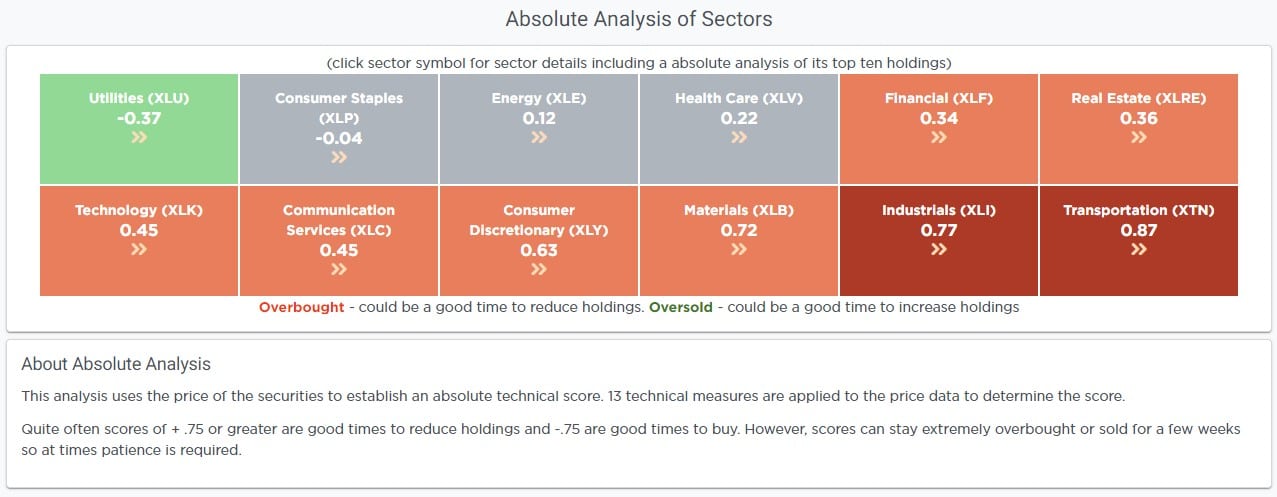

Absolute Sector Analysis

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Cross Over) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

The monthly risk and reward ranges have reset for the beginning of the month.

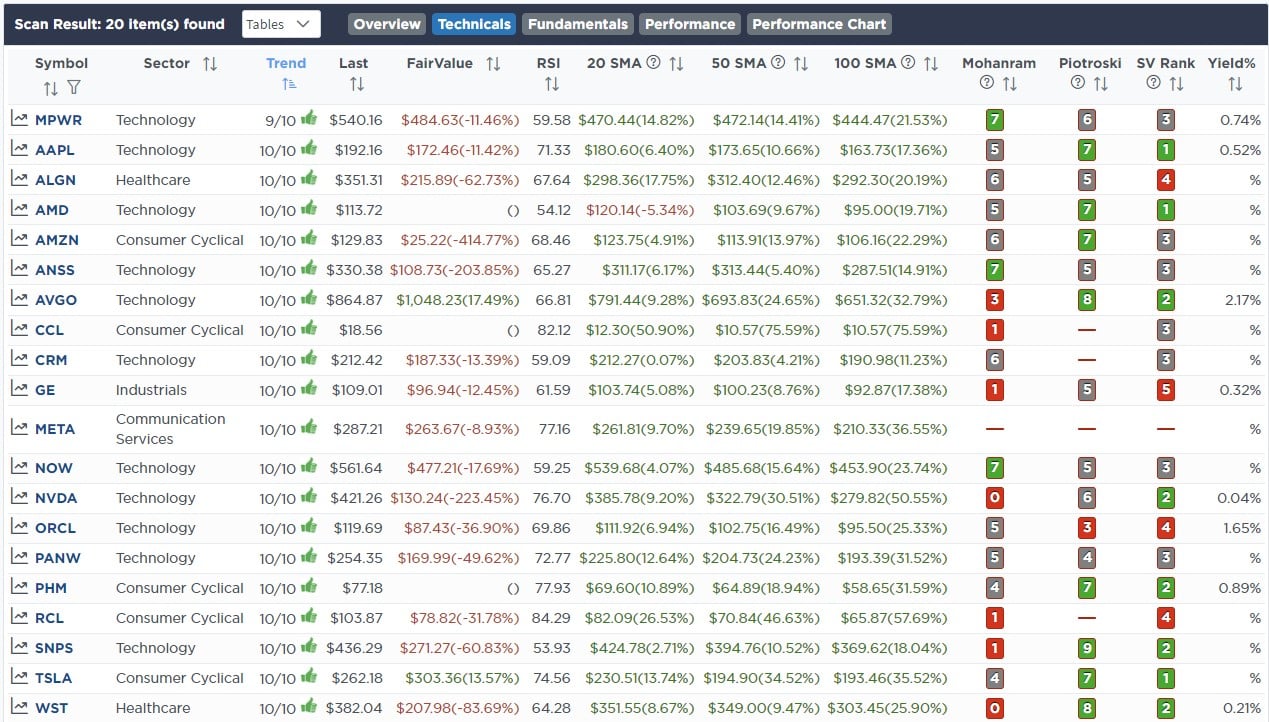

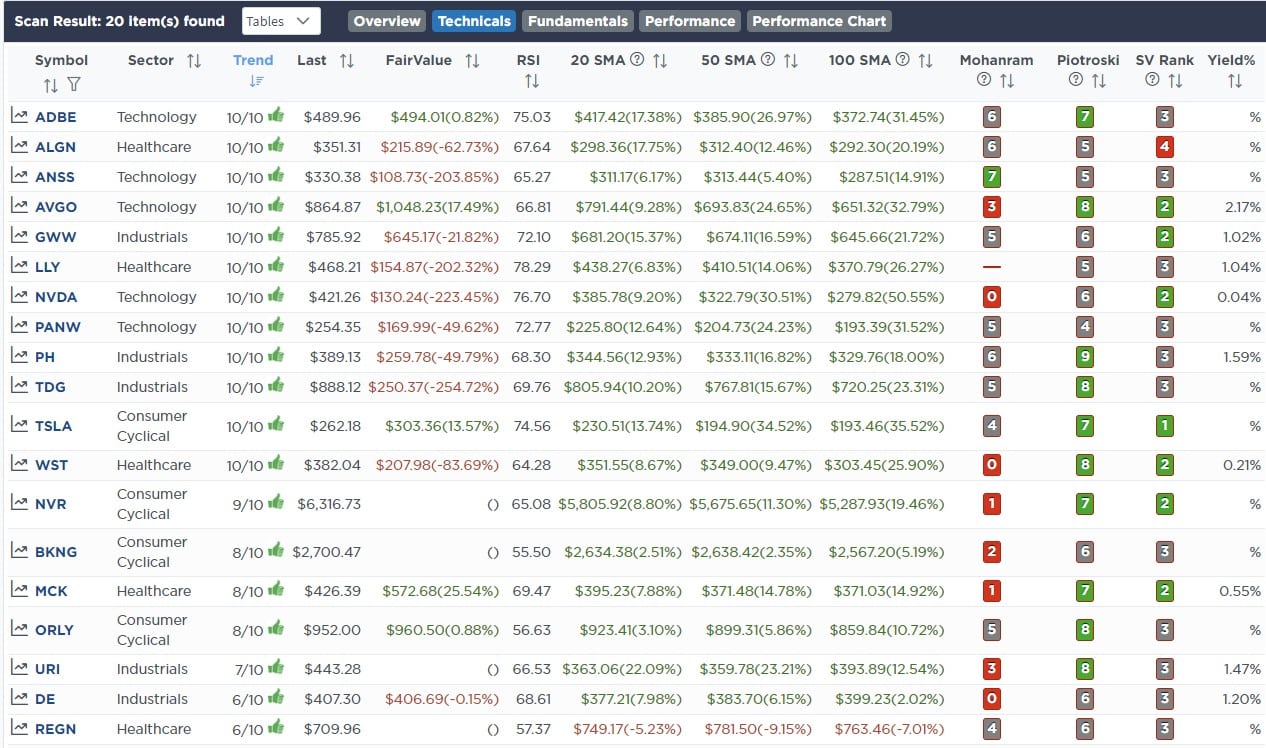

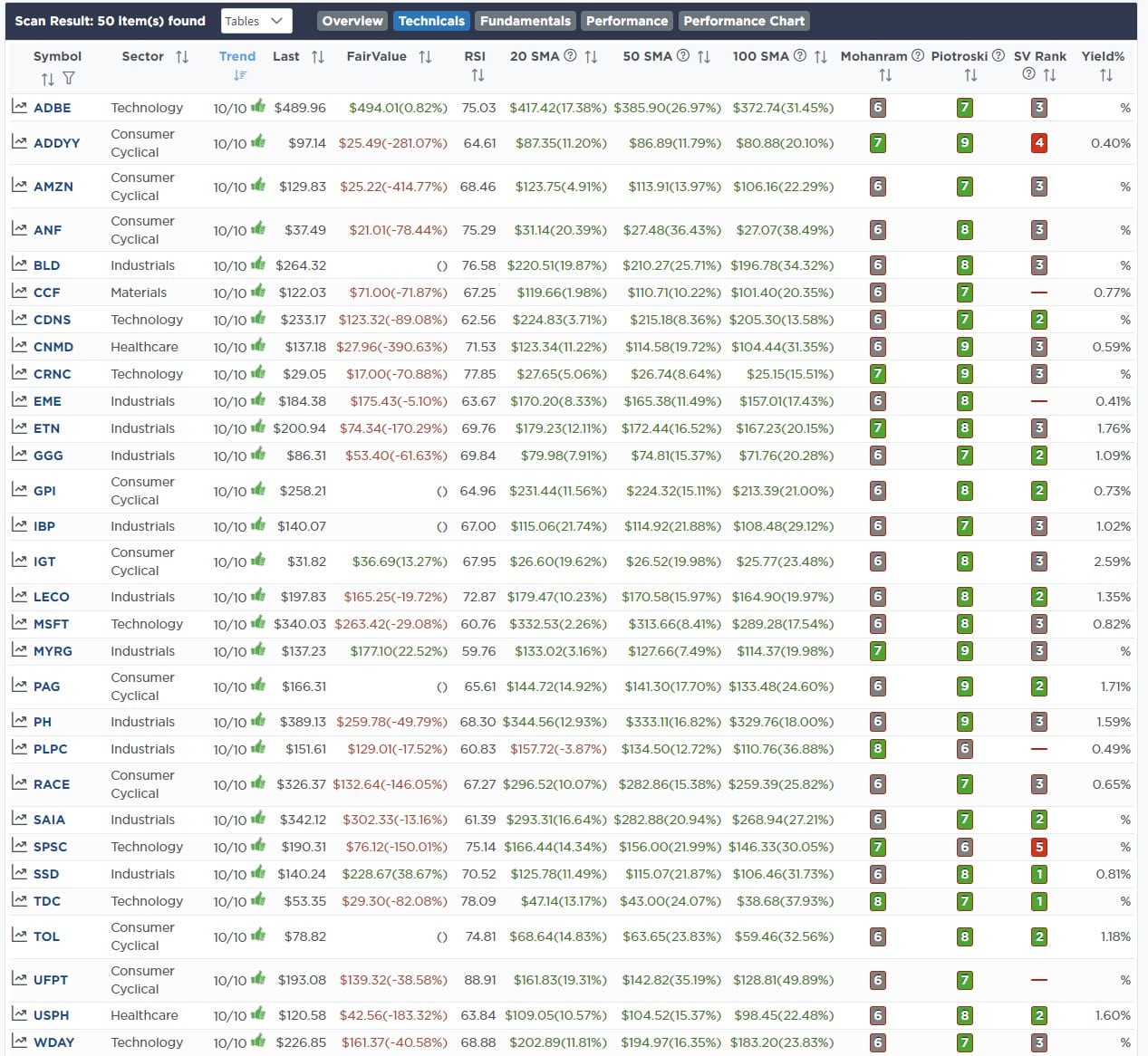

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong Stocks With Dividends

(Click Images To Enlarge)

R.S.I. Screen

Momentum Screen

Technically Strong With Dividends

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O.

Have a great week!