Bearish Sentiment Crushed As Powell Gives Hope

Inside This Week’s Bull Bear Report

- Market Rally Crushes Bearish Sentiment

- Is The Bull Market Back

- How We Are Trading It

- Research Report – More Bear Before The Bull Run

- Youtube – Economic & Market Q&A With Lance Roberts

- Stock Of The Week

- Daily Commentary Bits

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Market Rally Crushes Bearish Sentiment

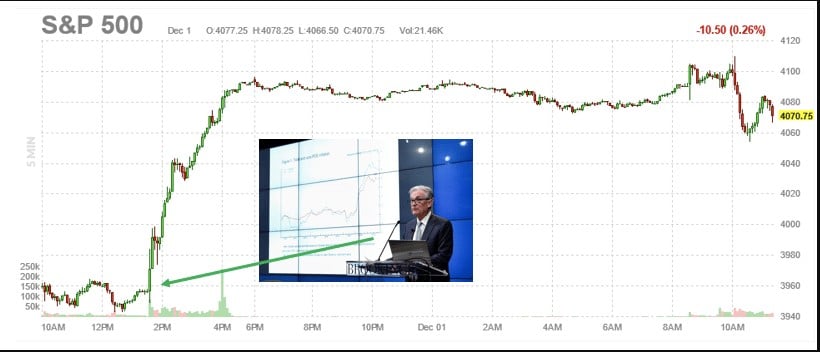

On Wednesday, the market surged following Powell’s press conference, crushing bearish sentiment. However, let’s start with a review from last week.

“This past week, the market jumped to the top of its recent trading range and continues to work in a consolidative manner. While the MACD “buy signal” is overbought, the market’s momentum is still bullish.

The rally reversed a majority of the previous oversold conditions and net bearishness. Therefore, some profit-taking and risk reduction in portfolios remain prudent. While the expectation for a rally into year-end remains, we could see some selling in the first half of December from tax loss harvesting and portfolio rebalancing. Such will likely provide a tradeable opportunity into year-end and the beginning of 2023.”

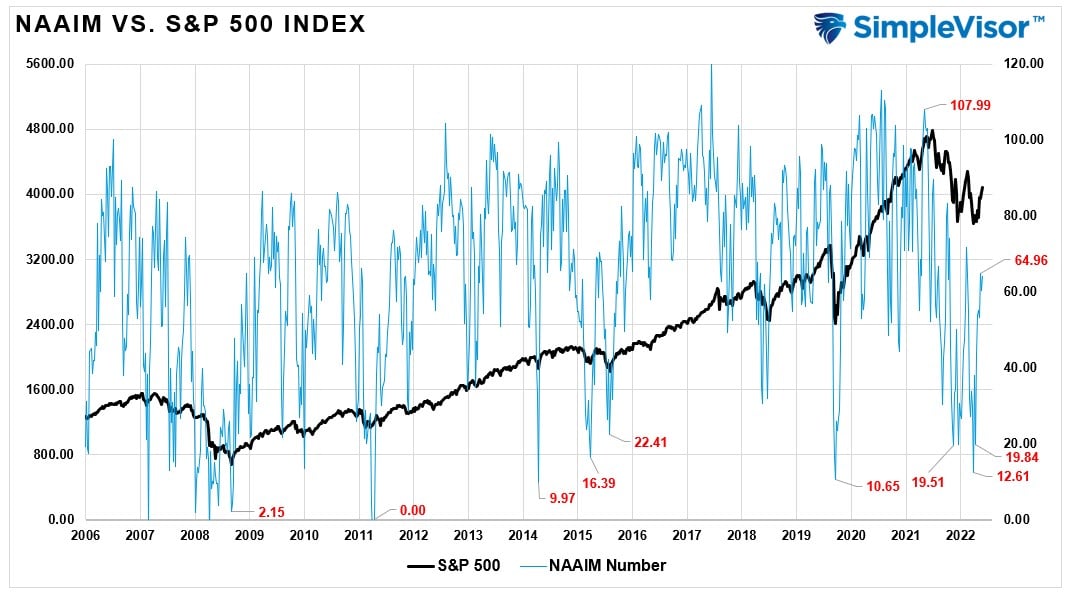

The surge in the market crushed bearish sentiment following a perceived “dovish” twist to Jerome Powell’s Brookings Institution speech.

“It makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting.”

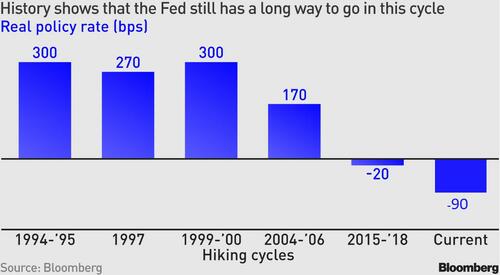

However, this is not “new news,” but rather what the markets have been rallying on for the last several weeks. The market overlooked the much more hawkish statement, as we will discuss momentarily, of “higher for longer.” More importantly, inflation-adjusted policy rates are now around -90 basis points, far below where the Fed will look to stop.

“In other words, if key surveys about short-term inflation expectations stay around current levels, there is just no way the Fed can afford to stop before rates get to 5.25%. And that would probably be the lowest possible level. In other words, the current terminal rate of around 4.90% is not quite where it needs to be. The Fed has never really been able to wind down its tightening before real rates went significantly higher — which has been circa 200 basis points on average.” – Ven Ram, Bloomberg

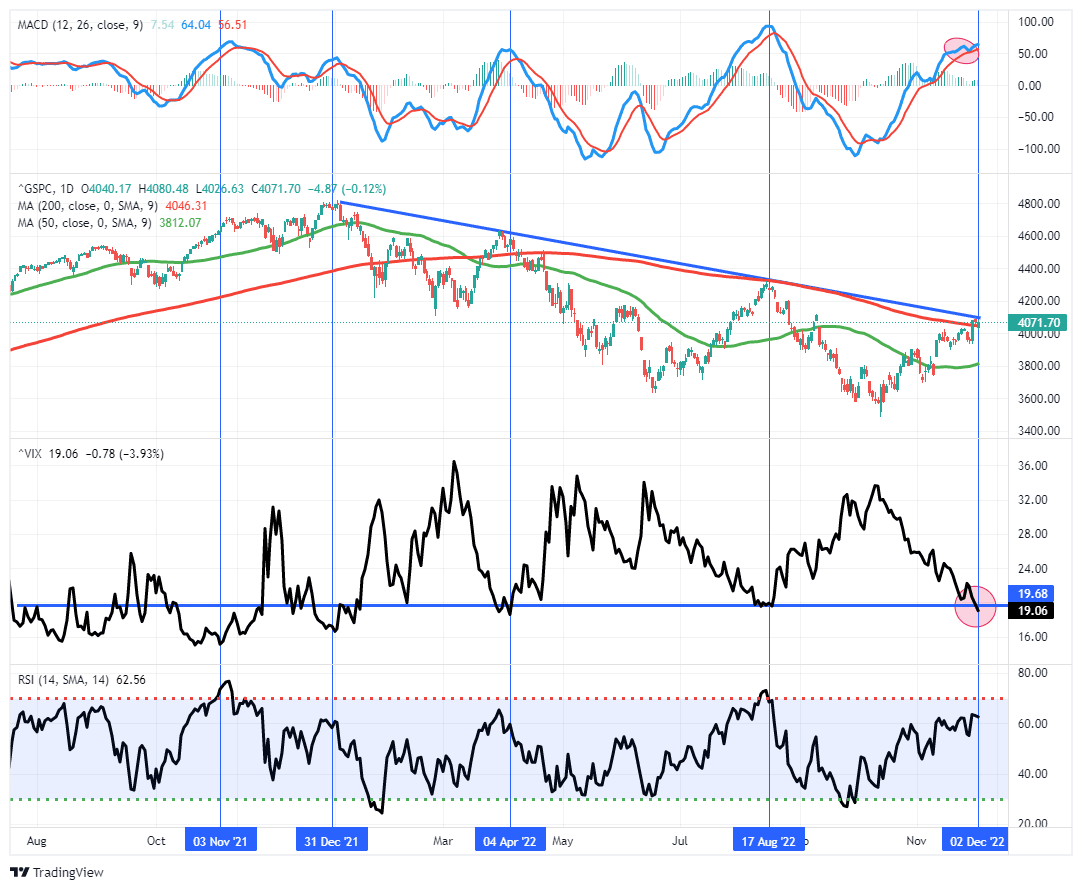

Regardless, the market rally sent the volatility index below 20, which has historically denoted market peaks rather than the beginning of a bullish rally.

However, Friday, the stronger-than-expected jobs report hit the market, but as shown, it hung onto support at the 200-dma. If the market can look past the employment report next week and rally, we will have a successful first test of the 200-dma as support.

It is no surprise the recent action has pushed bullish optimism higher.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Is The Bull Market Back?

With the market breaking above the 200-dma, investors are starting to ask the obvious question.

“Is the bearish market over? Is now the time to jump back in?”

It is an interesting psychological phenomenon.

Before 2022, the bullish mantra for the preceding decade was, quite simply, “Don’t fight the Fed.”

“The primary bullish argument for owning stocks over the last decade is that low-interest rates support high valuations.

The assumption is that the present value of future cash flows from equities rises, and so should their valuation. Assuming all else is equal, a falling discount rate does suggest a higher valuation. However, as Cliff Asness noted previously, that argument has little validity.

“Instead of regarding stocks as a fixed-rate bond with known nominal coupons, one must think of stocks as a floating-rate bond whose coupons will float with nominal earnings growth. In this analogy, the stock market’s P/E is like the price of a floating-rate bond. In most cases, despite moves in interest rates, the price of a floating-rate bond changes little, and likewise the rational P/E for the stock market moves little.” – Cliff Asness

The problem for the bulls is simple: You can’t have it both ways.

Either low-interest rates are bullish, or high rates are bullish. Unfortunately, it can’t be both.”

Such is an important point, considering where we are currently.

Despite the Fed continuing to hike rates, which is bearish from a valuation standpoint, investors continue to chase stocks in hopes the Fed will reverse monetary tightening. Instead, investors continue to “fight” the Fed hoping for a pivot. Such is due to the F.O.M.O. (Fear of Missing Out) of missing the bottom of the market.

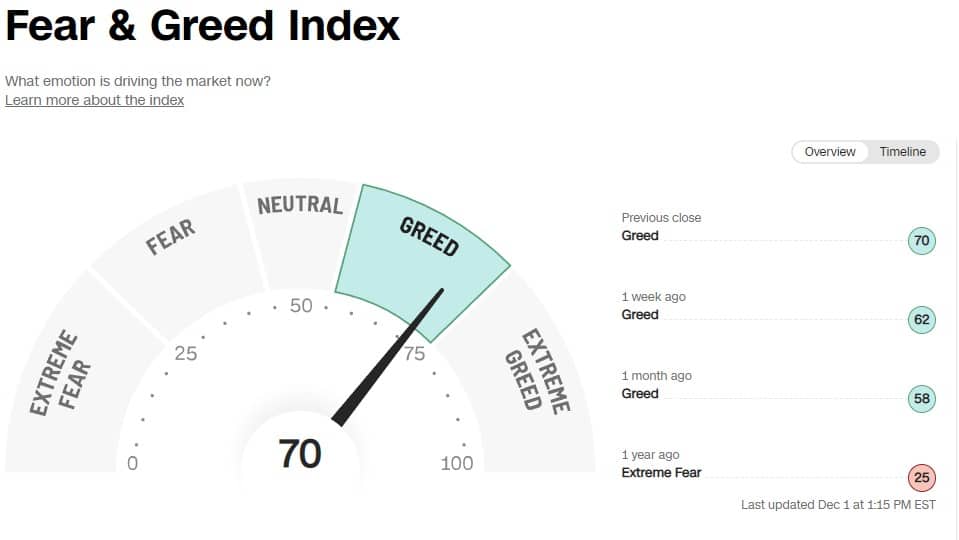

I said it is an interesting psychological phenomenon because investors continue to choose whatever narrative they need to support the bullish or defy the bearish case. The reality is that as asset prices increase, individuals quickly find “rationalizations” for buying stocks. Such is why the CNN Fear Greed Index is now pushing back toward more extreme greed levels, despite the market remaining in a bearish trend since the beginning of the year.

Nonetheless, as noted above, Powell’s comments on Wednesday sent the markets screaming above the 200-dma, which excited the bulls. But is the bull market back, or is this another “bearish” setup waiting to maul overly enthusiastic investors?

Technical Reasons To Be Bullish

There are currently several “technical” reasons supporting the bulls.

As we have discussed previously, we are NOT in a “bear market.”

“The 20% rule is completely arbitrary.

- A bull market is when the market’s price trends higher over a long-term period.

- A bear market is when the previous advance breaks, and prices begin to trend lower.

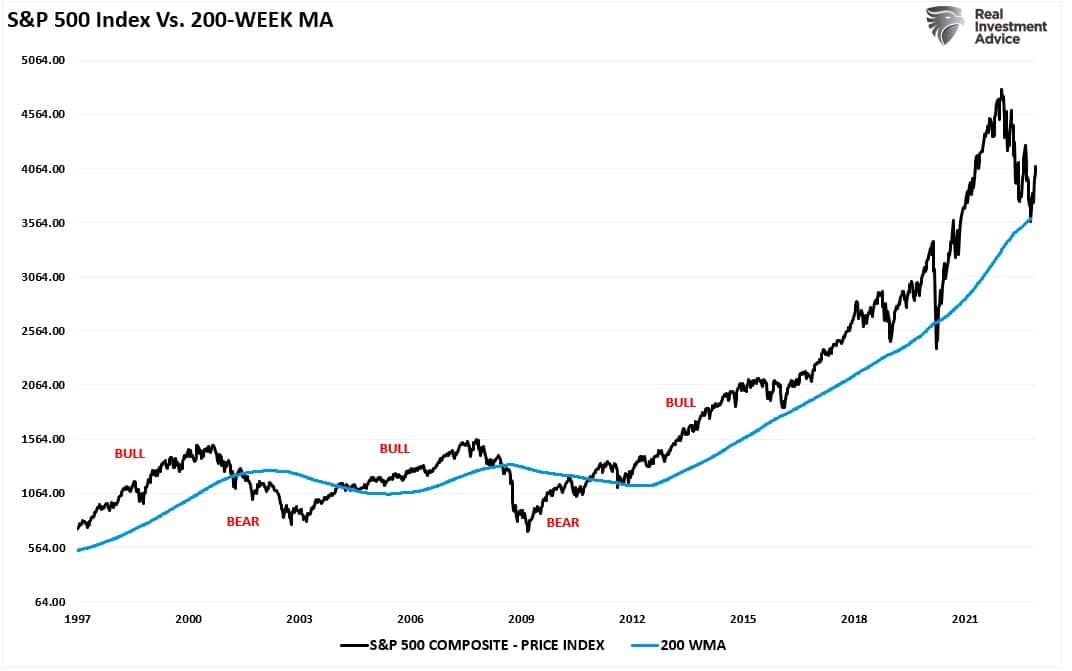

The market recently bounced from the 200-week moving average (WMA), which defined the rising price trend (bull market) from the 2009 lows. You will note that bear markets occur when the 200-WMA gets broken. Bull markets exist when above. Besides a brief stent below the 200-WMA in March 2020, the recent correction bounced solidly off that running bullish trend, and prices remain in a long-term uptrend.

The reason this distinction is crucial is because of how markets respond.

- “Corrections” generally occur over short time frames, do not break the prevailing price trend, and are quickly resolved by markets reversing to new highs.

- “Bear Markets” tend to be long-term affairs where prices grind sideways or lower over a year or more as valuations are reverted.

Notably, given the market is not constrained by a previously broken bullish trend, such provides less resistance to the recovery. Given that valuations remain elevated by historical standards, the market continues to avoid the mean reversion that occurs during bearish markets.

Such also keeps the bullish bias intact, and professional investors rapidly increased their equity allocations to chase the rally.

Lastly, breadth has improved markedly, with the number of stocks trading above their respective moving averages broadening.

While these technical foundations suggest a more bullish short-term backdrop, the fundamentals remain bearish.

The Fed Statement Was Bearish

The comments from Mr. Powell on Wednesday were interesting because they suggested concern by the Federal Reserve of increasing risks in the economy. In early November, we noted that Jerome Powell had made two critical comments:

- There is “significant uncertainty” around the end-point of rate hikes, which he indicated by stating, “we have some ways to go.” Furthermore, “the question of when to moderate the pace of increases is now much less important than the question of how high to raise rates and how long to keep monetary policy restrictive.”

- “If we overtighten, we can support economic activity.”

Just one month later, Powell effectively backtracked on these statements.

- “The time for moderating hike pace may come as soon as December.”

- “I don’t want to overtighten. Cutting rates is not something we want to do soon. So that’s why we’re slowing down, and we will try to find our way to what that right level is.”

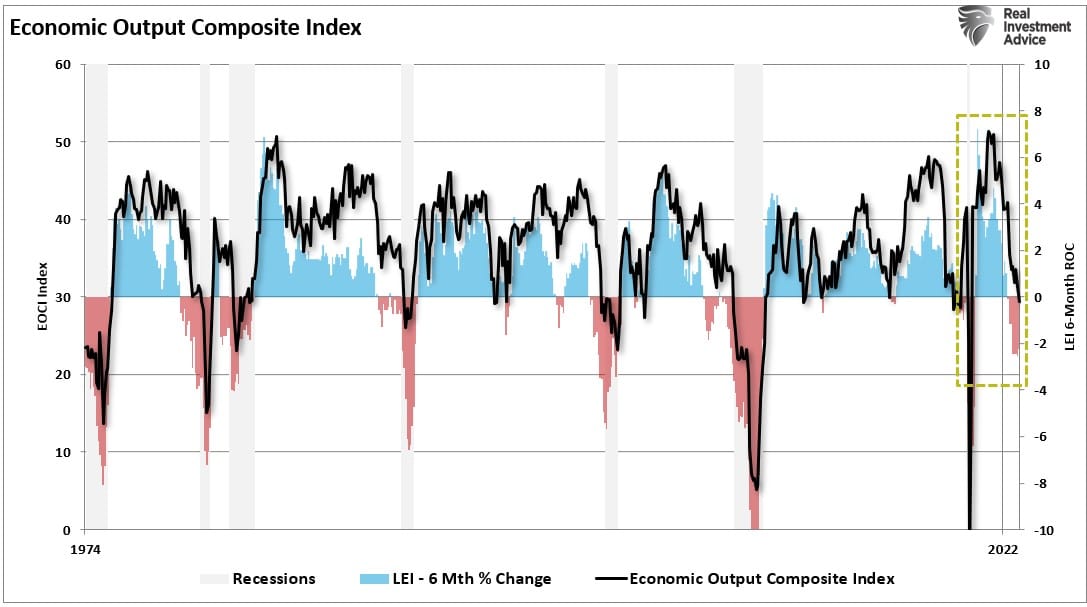

While the markets took the twist in the language as a “bullish” sign, it signals a more “bearish” concern from the Fed. One month ago, the Fed was NOT worried about overtightening because they felt they could support economic activity. However, in the last month, employment has begun to show cracks, with the latest ADP report showing 100,000 manufacturing jobs lost and multiple manufacturing gauges slipping into recessionary territory. Our Economic Composite Index and the 6-month rate of change of the Leading Economic Index warn of recessionary risks.

The question those with a bullish bias need to ask is, “why” did Mr. Powell change his language from not worrying about “overtightening” to now it being a concern?

More importantly, Mr. Powell’s discussion of how long monetary policy will remain restrictive should be a concern.

“Given our progress in tightening policy, the timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level.

History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.”

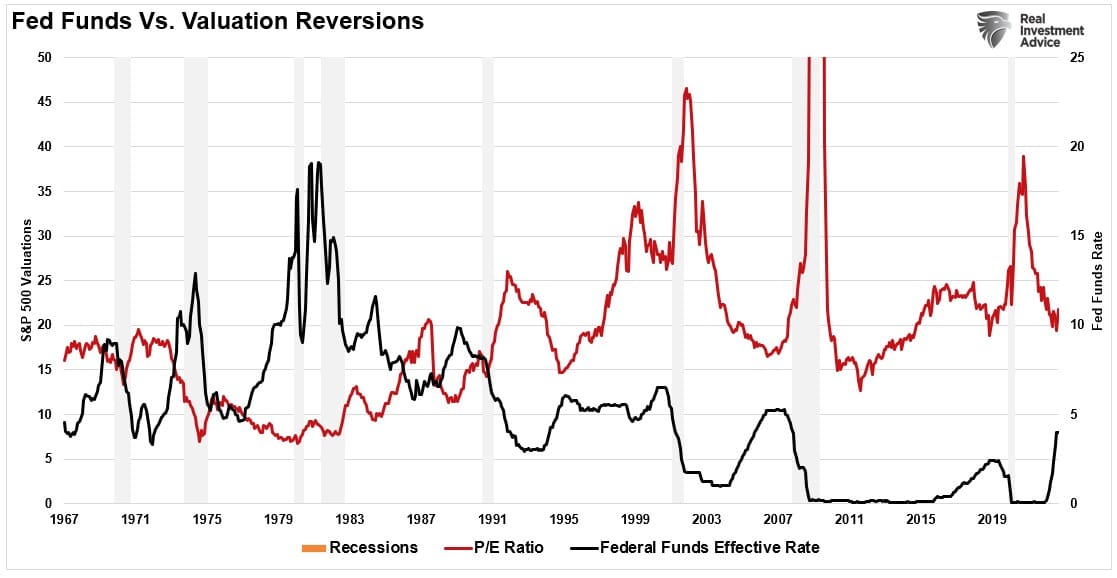

Back to our commentary above, IF the Fed will maintain a higher level of interest rates for longer, the discount rate applied to forward earnings is not conducive to keeping valuations at current levels. As higher interest rates slow economic activity, to reduce inflationary pressures, earnings must decline. If such is the case, prices must also fall to revalue the markets for lower earnings. Valuations tend to complete their respective “mean reversion” following the reversal of monetary tightening.

Pay attention to that last sentence.

While the Fed is suggesting their want to hold rates “higher for longer,” such has historically led to bearish market and economic outcomes. When the Fed reverses monetary accommodation, such is because they are combatting a recession, bear market, or worse.

Not Getting The Bull Bear Report Each Week In Your Mailbox? Subscribe Here For Free.

How We Are Trading It

While investors seem to have the proverbial “bull by the horns,” we have seen this action previously. We discussed this in more detail in Thursday’s 3-Minutes Video.

As stated in that video, we have been here before, and the “risk on” chase is quite extended, and markets are back to more overbought levels. Furthermore, while investors are chasing equities, they are also buying Treasury bonds. Such is not surprising, as lower inflation and slower economic growth will lead to lower yields and higher bond prices.

However, falling yields are typically an early warning signal of recessionary onsets and other bearish events for equity investors. Such is why, despite the recent push higher above the 200-dma, we remain cautious temporarily. We are maintaining our much-reduced equity exposure and overweight cash and bond holdings. (The ETFs are all fixed income of different durations.)

Last week, I concluded by stating:

“While we could see a bit of a rally next week, the risk of a correction is rising.”

That rally occurred, and the risk of a correction is rising. We suggest continuing to follow our portfolio management guidelines for now and that you take some action if you have not done so as of yet.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against significant market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers. Raise cash and rebalance portfolios to target weightings.

See you next week.

Research Report

Encore Presentation – Year-End Economic Review

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Stock Of The Week In Review

Stocks Trading Below Fair Value

This week we are using new screening criteria in SimpleVisor to find stocks trading well below their respective fair value. A stock’s fair value is estimated based on its expected cash flows. SimpleVisor uses the average of three fair value models- Peter Lynch, Warren Buffett, and our proprietary DCF model.

In addition to screening for stocks trading at deep discounts to their fair value, we added a forward valuation measure. And given the growing odds of a recession, we included a Piotroski score threshold. The Piotroski score measures a company’s financial position with a score of 0 to 9, 9 being the best.

Here is a link to the full SimpleVisor Article For Step-By-Step Screening Instructions.

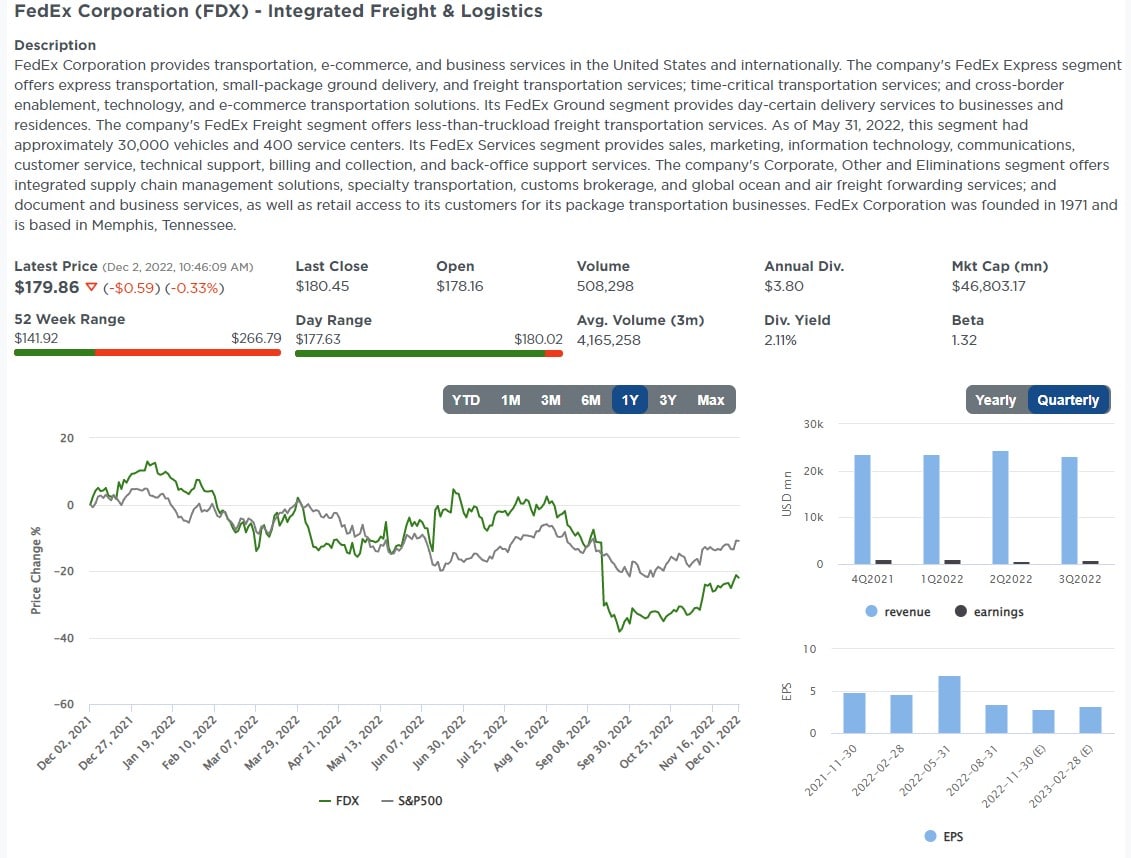

FedEx Corporation (FDX)

Login to Simplevisor.com to read the full 5-For-Friday report.

Daily Commentary Bits

Timiraos Pours Cold Water on Powell Bulls

Stocks shot higher on Wednesday after Chair Powell’s speech. Looking for good news, the bulls heard the Fed is moderating its policy stance. Further, it appears the Fed is now concerned about over-tightening. Powell’s comments were very similar to previous comments of many Fed speakers. Wall Street Journal reporter Nick Timiraos followed Jerome Powell’s “bullish” speech with words of caution.

Nick Timiraos makes two critical points. For starters, he quotes Powell. “Officials seek to reduce inflation by slowing the economy through tighter financial conditions—such as higher borrowing costs, lower stock prices, and a stronger dollar—which typically curb demand.” Timiraos follows up on Twitter- “Powell may not have intended to ease financial conditions, but his comments about avoiding unnecessary weakness overshadowed his concerns about labor-market imbalances.” The stock and bond market rallies are not conducive to fighting inflation and likely not the result Powell wants. This has potentially bearish implications for how Powell addresses reporters after the December 14th Fed meeting.

Second, Powell blames early retirements and deaths due to covid and reduced immigration for making the job market tighter than normal. As a result, Timiraos tweets that rates may stay higher for longer and the “(Fed’s) ability and room to ease is less than before since inflation will return quickly in an undersupplied labor market.” Translation- it may take longer for the Fed to ease, and the rate of easing may not be as aggressive as in the past.”

Click Here To Read The Latest Daily Market Commentary (Subscribe For Pre-Market Email)

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

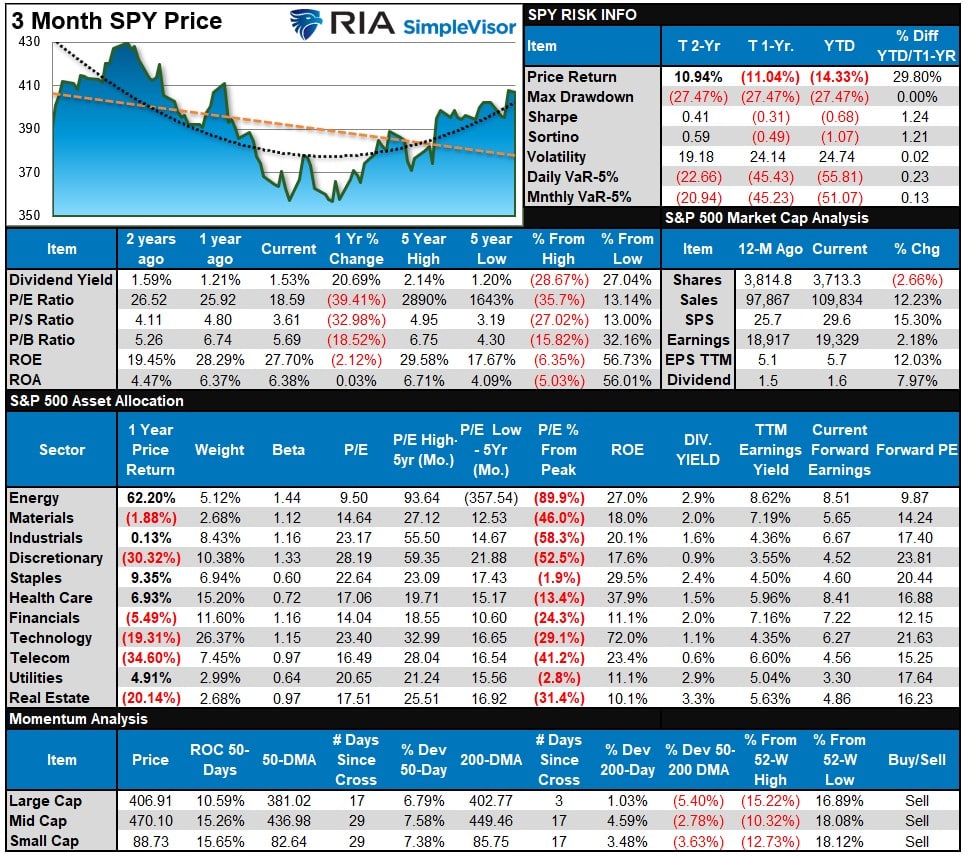

S&P 500 Tear Sheet

Relative Performance Analysis

The market rallied again last week post the perceived “dovish” tilt to Jerome Powell’s speech. minutes. The rally pushed the market above the 200-dma, which is bullish, but remains exceedingly overbought for a second week in most every market and sector. With the weekly Technical Gauge (below) increasing to more overbought levels, some profit-taking is advised next week.

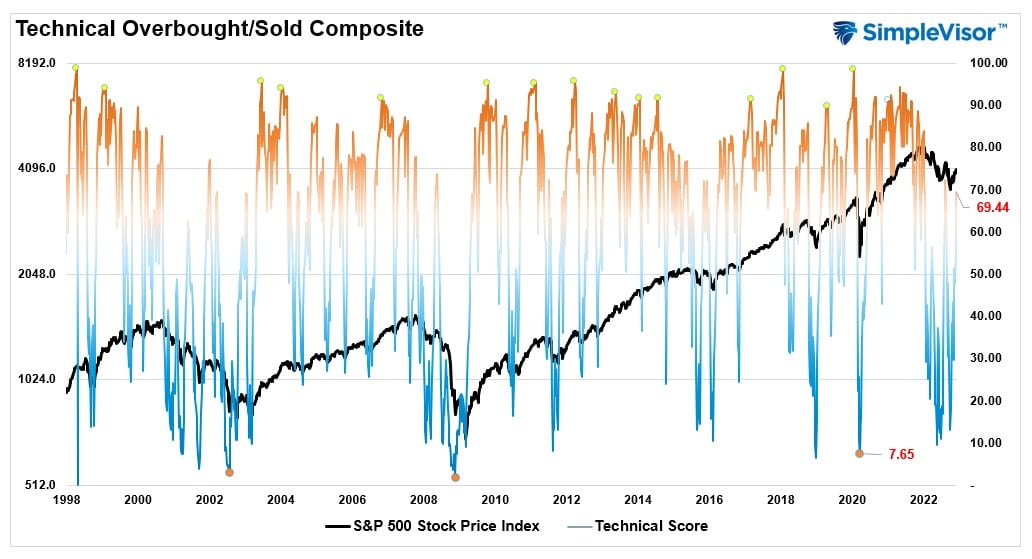

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. Markets tend to peak when readings are at 80 or above, which suggests profit-taking and risk management are prudent. The best buying opportunities exist when readings are 20 or below.

The current reading is 69.44 out of a possible 100 and rising. Remain long equities for now.

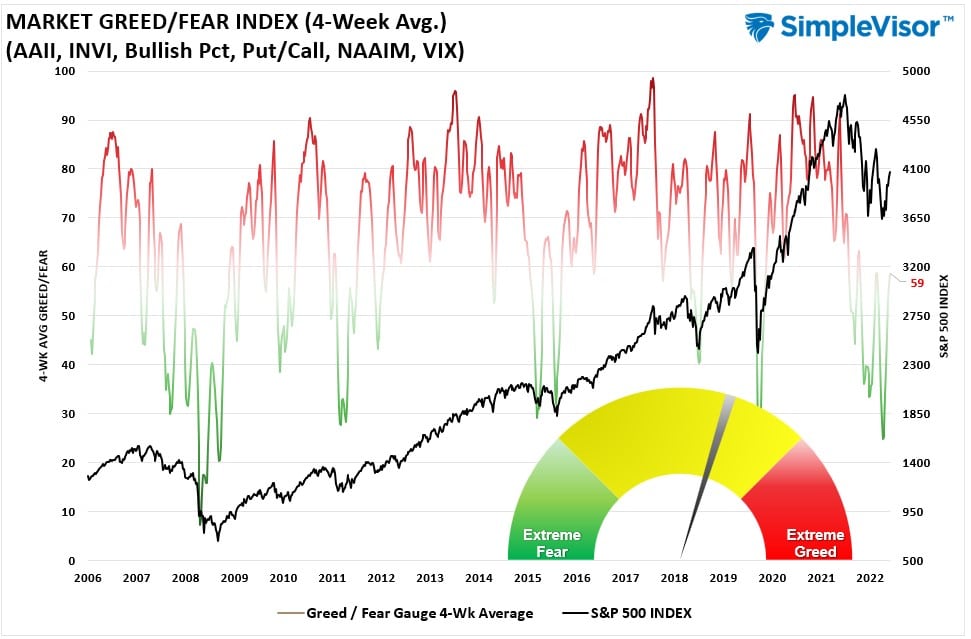

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” Gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current 4-week Average is 59 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Cross Over) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

The risk ranges reset at the beginning of each month. Interestingly, the bond rally in the first two days of the month has already pushed bonds above their month range. Look for a bit of pullback before adding to exposures.

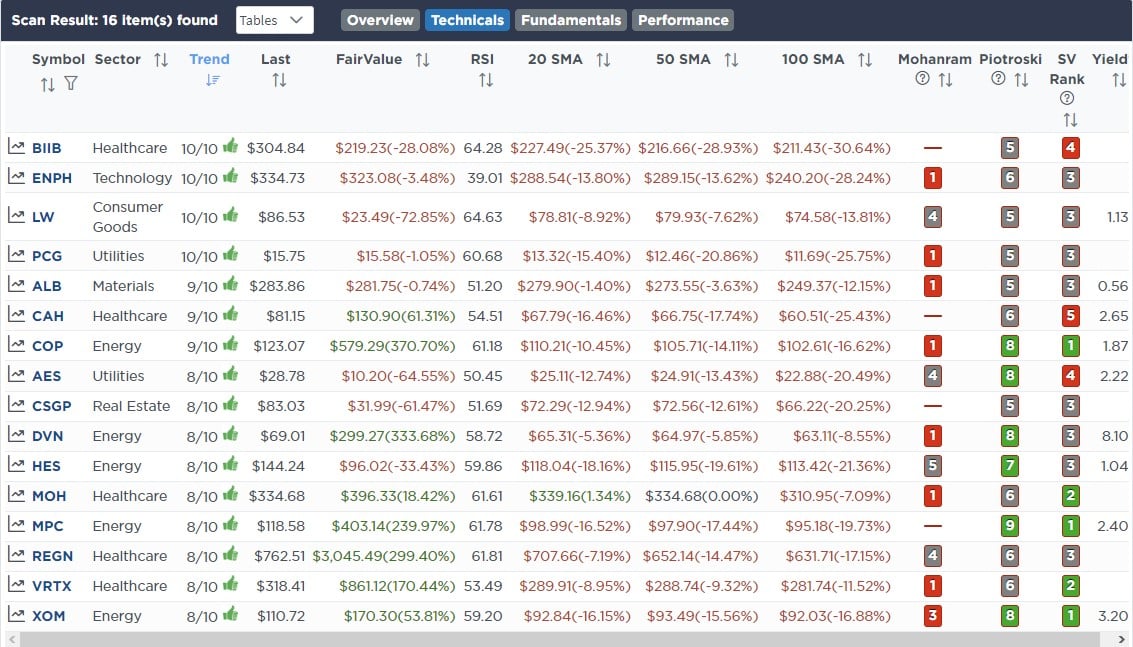

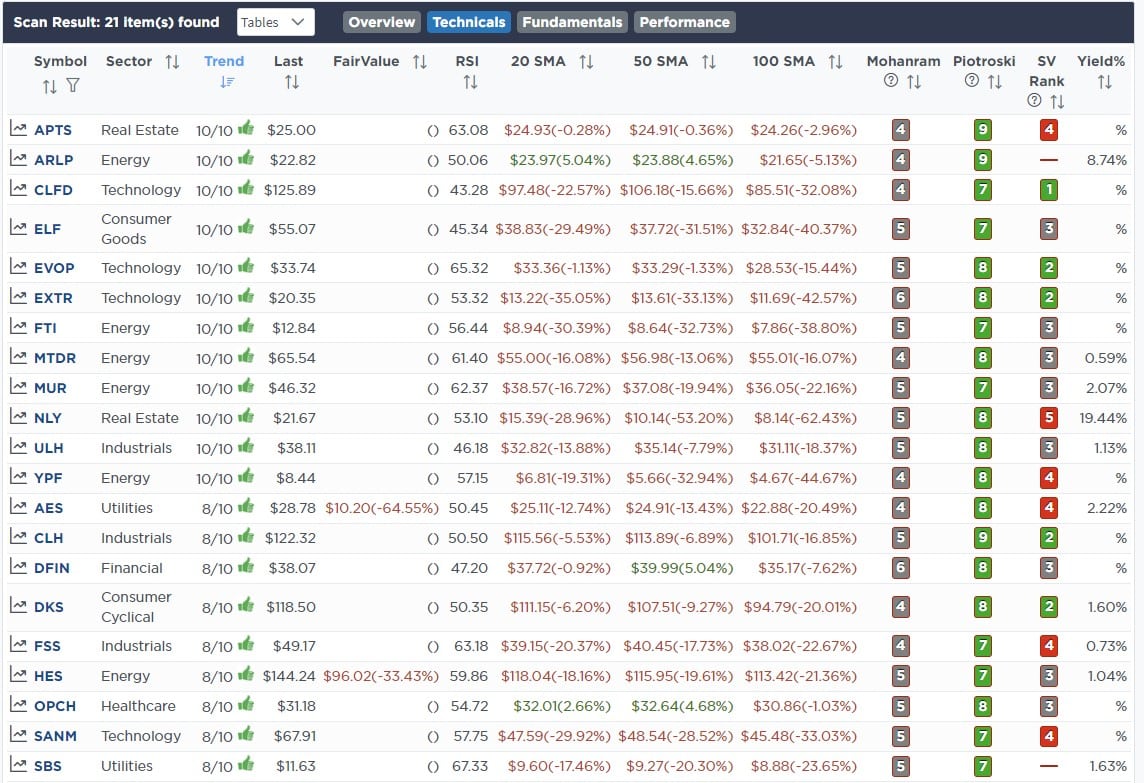

Weekly SimpleVisor Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Highest Rated Stocks With Dividends

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Highest Rated Stocks With Dividends

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

November 28th

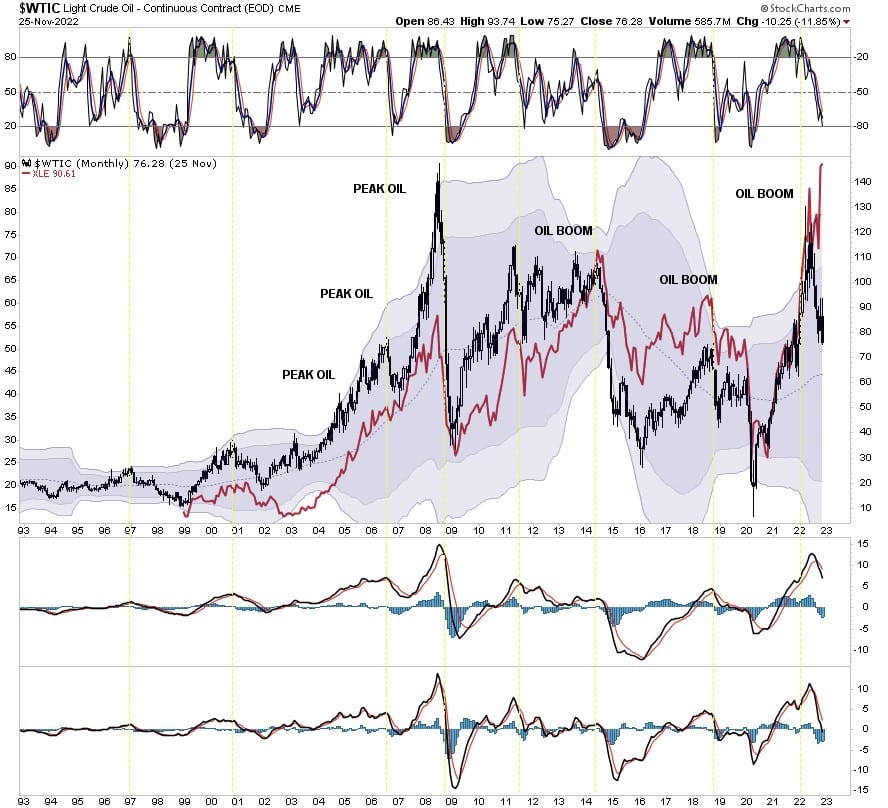

As shown in the chart below, there is a historic and obvious correlation between oil prices and energy stocks. Currently, while oil prices have declined, energy stocks have not. However, we suspect that as demand weakens from slower economic growth, energy stocks will eventually catch up to fundamental realities.

As such, we sold the rest of our energy positions in both models. We will look to add back to our energy exposure at a more opportune time.

Equity Model

- Sell 100% of both Exxon Mobil (XOM) and Devon Energy (DVN)

ETF Model

- Sell 100% of iShares Energy ETF (XLE)

The equity model is now at 35% equity exposure, and the ETF model is at 40.5%.

Lance Roberts, CIO

Have a great week!