Market Stumbles As Stimulus Hopes Fade 10-16-20

In this issue of “Market Stumbles As Stimulus Hopes Fade.”

- Hopes For More Stimulus

- Election Night Risk

- Economic Disappointment

- Portfolio Positioning Update

- MacroView: Recessions Are A Good Thing, Let Them Happen

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

The Pre-Election Event

“Policies, Not Politics.”

Join Richard Rosso, CFP, and Danny Ratliff, CFP, for an in-depth look at both party’s platforms and how upcoming changes could affect your retirement, social security, medicare, and how you invest. From taxes to the markets, they will provide the answers you are looking for.

- When: Saturday, October 24th, 2020

- Time: 8-9am

- Where: An exclusive GoTo Webinar Event (Register Now)

Catch Up On What You Missed Last Week

Market Stumbles As Stimulus Hopes Fade

Over the past couple of weeks, we have discussed the market rally from the recent oversold lows.

“The Federal Reserve needs ‘more stimulus’ to monetize the underlying debt issuance for investors. Such is how, ultimately, liquidity gets into the markets. With markets only about 3% away from all-time highs, there is really nothing to stop it from getting there unless stimulus talks break down once again.”

Unfortunately, the latter happened as the stalemate between House Democrats and Treasury Secretary Mnuchin continued. While both the Treasury Secretary and the President have signaled they are open to a much bigger stimulus package, the House’s Speaker isn’t budging off her demands for State bailouts. Neither is Senate Majority Leader Mitch McConnell, who has already stated he will not take up any House bill. He stated he would put a roughly $500 billion targeted relief bill to vote in the Senate as soon as next week. That bill is also doomed.

However, even without a stimulus package, the market rallied nicely from recent lows. The good news is the bit of trading sloppiness last week allowed the market to start working off the overbought condition. While we could see some additional weakness early next week, the downside risk is fairly limited going into the election.

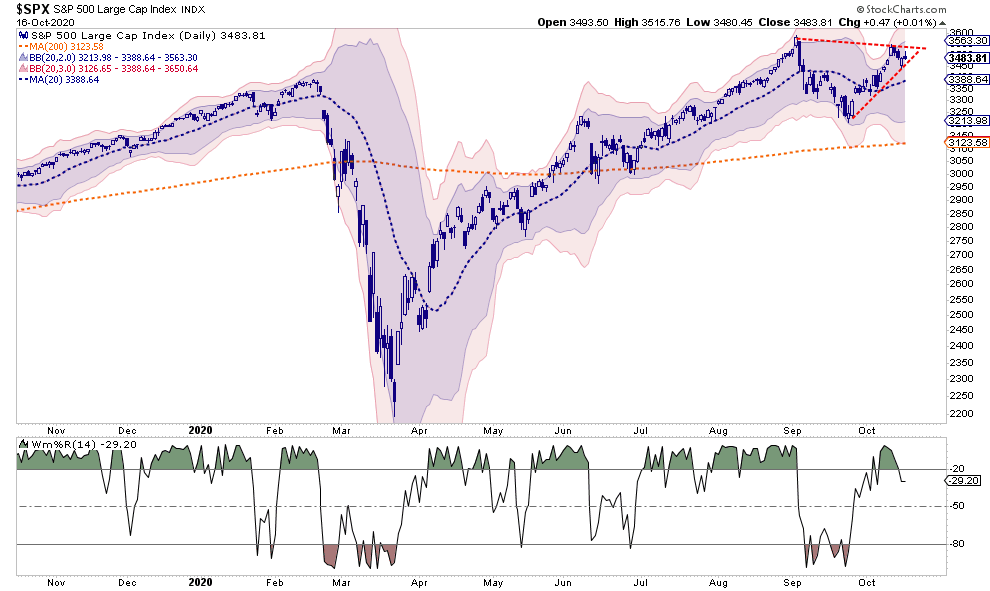

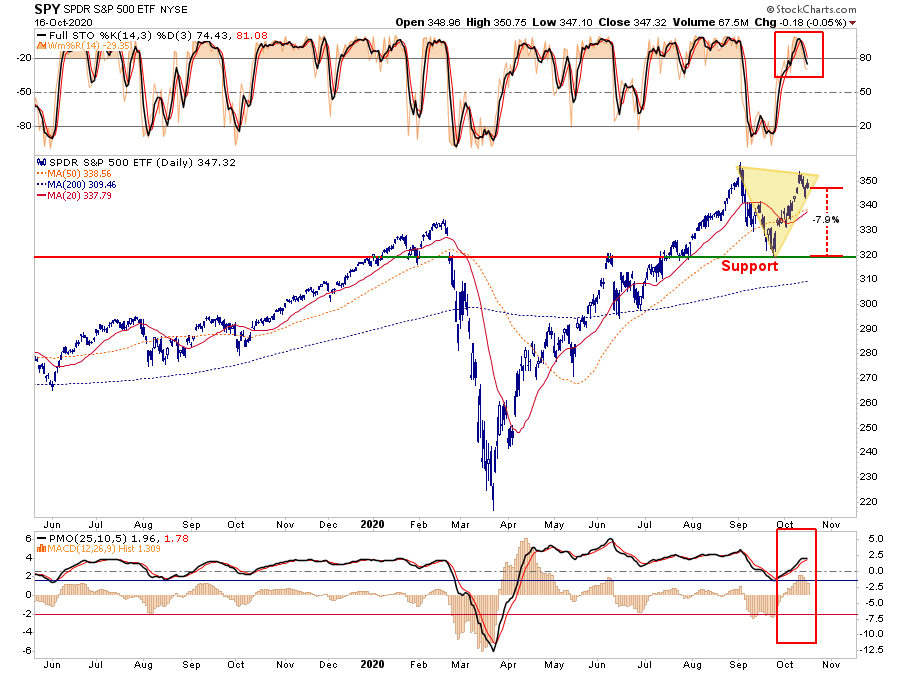

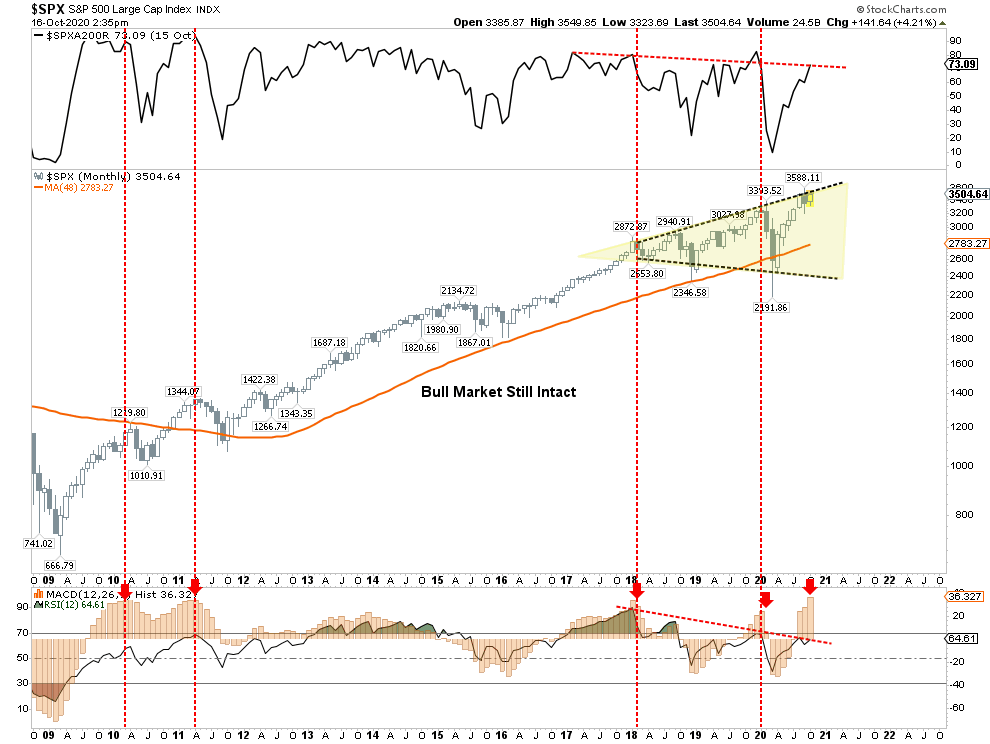

Conditions Are Less Favorable

As shown below, both the 20- and 50-dma’s sit just below current levels. Those averages should act as initial support. Below that support are the recent lows, which will likely contain the market within the current range. Such would entail a roughly 8% decline from current levels and certainly well within the context of a normal market correction.

However, a break of that important support will quickly find the 200-dma, which is currently about 11% below current levels. As we will discuss momentarily, a “contested election” could certainly provide the catalyst for such a decline.

The fuel for a bigger decline remains this week. With speculation ramping up again, the risk/reward in the short-term has become less favorable. Call option buying remains extremely elevated relative to historical norms and exacerbates market declines when those positions are unwound.

On a longer-term basis, we remain concerned about the dichotomy of signals from the market. Negative divergences of RSI, the number of stocks above their respective 200-dma, and the more extreme monthly overbought condition are concerning.

The previous extensions over the last decade have led to decent corrections. Could this time be different? Sure, anything is possible. However, as investors, we want to remain focused on the “probabilities.”

While the market seems assured that more stimulus is coming sooner rather than later, one risk facing the market may be a “contested election.”

An Election Night Risk

Over the last few weeks, we have discussed much of what happens to the stock market both pre- and post-Presidential elections.

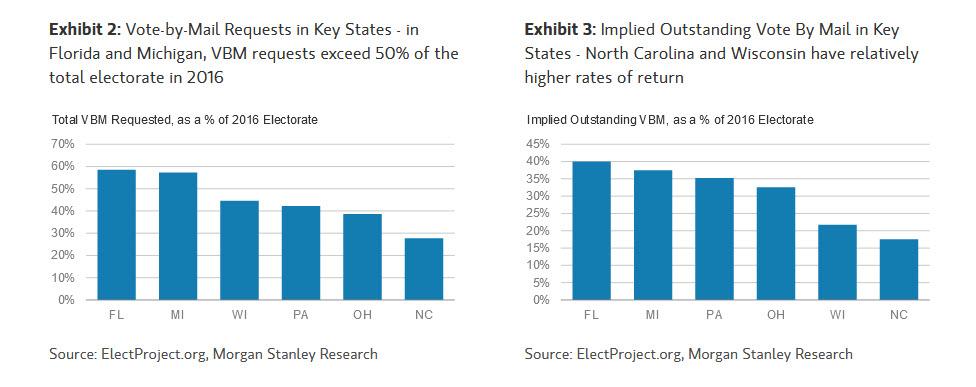

However, there is the potential for a delayed election outcome this year, which could rattle the stock market. As noted by Morgan Stanley via Zerohedge:

“Contrary to some expectations that the election outcome could take as much as a month to be decided – a la Gore vs Bush – new data cited by Morgan Stanley suggests ‘the worst-case outcome is the least likely.’ And while vote-by-mail (VBM) requests are breaking records, a concern given the slower process for counting those ballots, voters appear to be returning those ballots at a rapid pace in key battleground states according to Morgan Stanley’s Michael Zezas.”

“Morgan Stanley says that ‘there is an 80% chance the result is not determined on election night.'”

Is there a precedent for such an outcome?

Markets Don’t Like Uncertainty.

From a historical perspective, we have the precedent of the Gore/Bush election in 2000.

What does this mean for financial markets? The outcome of the election between George W. Bush and Al Gore was not decided on election day. Instead, Gore demanded a recount in Florida, where the vote was close, and “hanging chads” were at issue. It took over a month before we knew the election outcome when the U.S. Supreme Court decided Bush v. Gore on December 12, 2000.

What markets don’t like is uncertainty; over the course of the next several weeks, the S&P 500 decline by 7.5% at its nadir. However, the volatile swings of the market over that period were excruciating for investors. While not the “devastating event” the media has portrayed such an outcome to be, it is still worth noting. The inherent risk of a sharp rise in volatility and potential loss of gains if the unexpected does indeed occur.

Here’s the point.

If you are about to get on a boat and go out deep sea fishing, it generally never hurts to take a Dramamine if the seas get rough. Otherwise, the entire experience becomes a single nauseating memory.

Economic Disappointment

Another risk is a further economic disappointment. Coming off of the March lows and the economic shutdown, expectations for recovery had gotten extremely dire. However, as the Federal Reserve and the Government injected money directly into the financial system, sent checks to households, and provided additional benefits, the data improved faster than expected.

However, what is important to remember is that we measure data on a “rate of change” basis.

For example, think about a restaurant that was shut down entirely. When they are allowed to reopen, they go from ZERO customers to just ONE. That is a 100% increase from the prior period. Next period they have TWO customers, which is a 50% increase from the period. The business remains on the brink of bankruptcy, but the growth rate of sales is stunning.

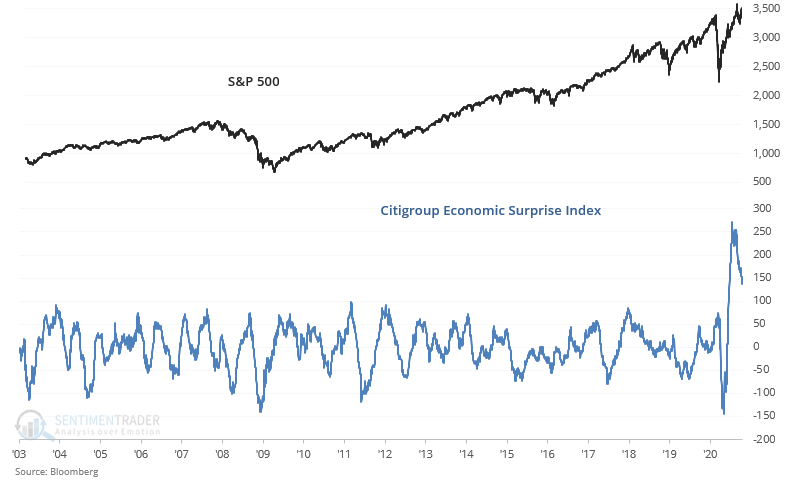

This is what is happening with the economic data currently. The Citigroup Economic Surprise Index measures the difference between Wall Street’s expectations for economic data versus what is actually reported. If the data is better, the index rises, and vice versa. The chart below, courtesy of Sentimentrader, shows the index compared to the S&P 500 index.

“The Citigroup Economic Surprise Index is retreating after the biggest spike in this data series’ history.”

Why is this important?

Back To Uncertainty

With no stimulus currently on the horizon and a resurgence of economic weakness, there is more than a reasonable risk we may see more disappointment in economic data ahead. Such could have return implications for the stock market.

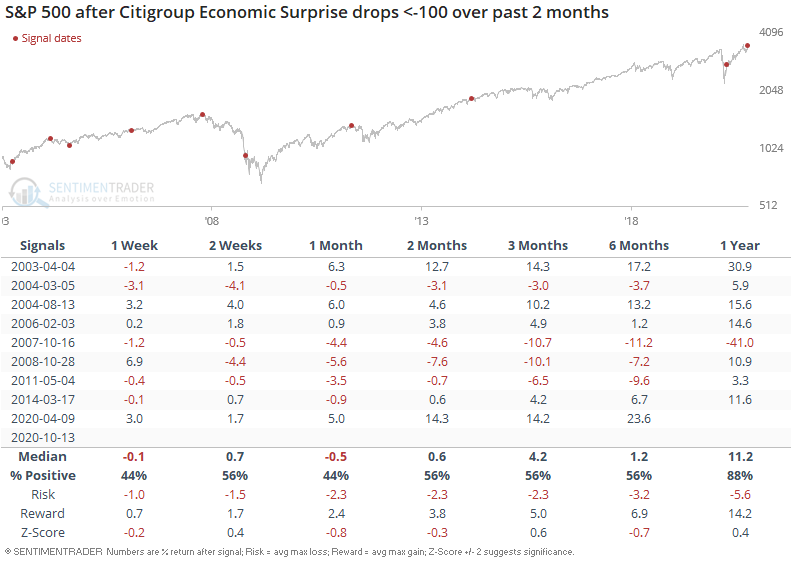

“When the Citigroup Economic Surprise Index dropped rapidly in the past, the S&P’s returns over the next month were slightly more bearish than random.” – Sentimentrader

With the potential for a delayed or contested election, weaker economic data, no stimulus, and already elevated asset prices and valuations, the risk of a correction has certainly risen.

All that is need is an “unexpected, exogenous event,” which sends traders scrambling for the exits.

Such leads us to this week’s portfolio positioning.

Portfolio Positioning Update

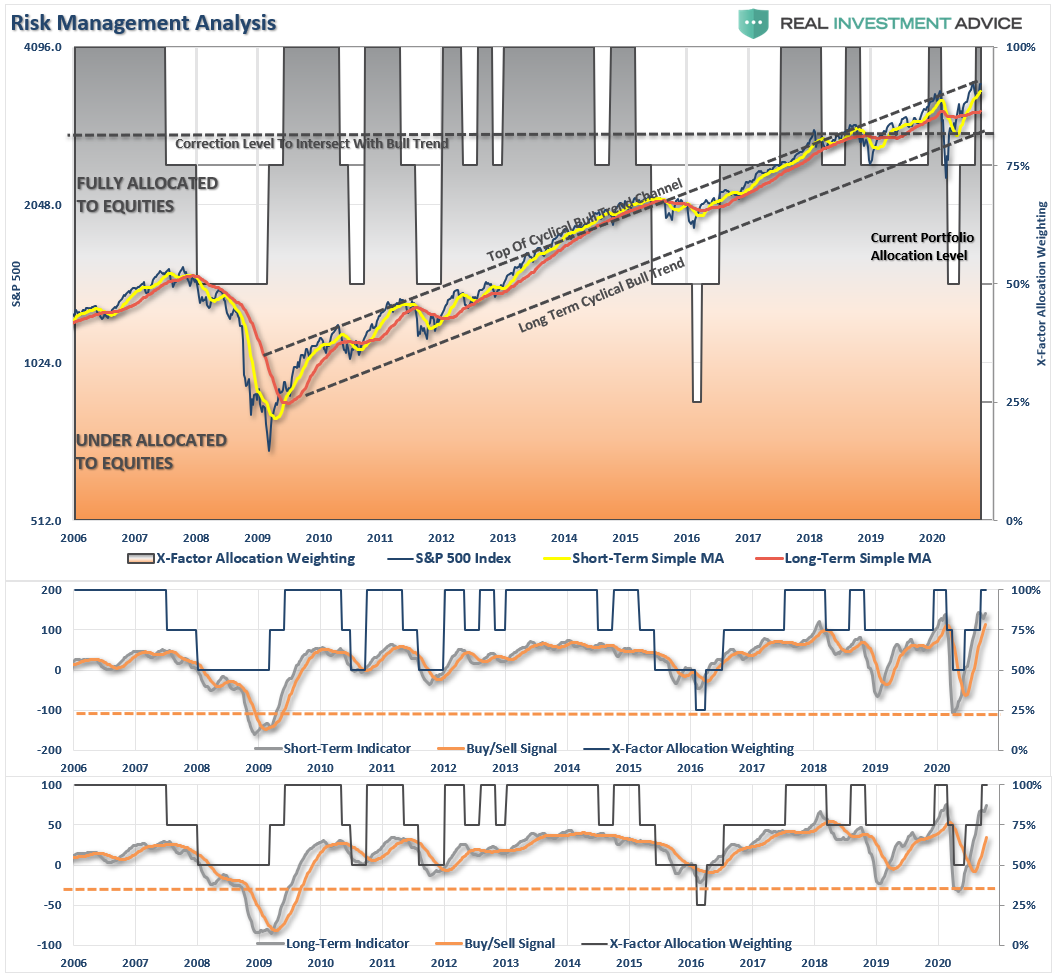

As we have noted previously, we currently have more equity exposure than we are comfortable with. However, technically, there is no reason to reduce exposure as trends remain positive sharply, the sentiment remains clearly bullish, and volatility remains suppressed.

With that said, we are still hedging portfolios by holding slightly higher levels of cash and adjusting the duration of the bond portfolio to mitigate drawdown risk. It’s challenging to hedge portfolios in an environment driven by daily news flows and sentiment and ignoring a wide range of “risks.”

The following quote from Sven Heinrick seems apropos at this juncture:

“Markets have been rallying not only on stimulus hope but also on the premise that the risk of a contested election is diminished or so the popular pablum goes. Well, for there to not be a contested election there needs to be a concession speech on the eve of the election. If that doesn’t happen, there is no election clarity until at least December 14 when the electoral college votes. That’s 6 weeks of uncertainty. And what if this gets contested, or what if there are legal challenges in between or beyond?

I’m raising these questions to highlight that there are all sorts of risks floating about that this market is not pricing in. At all. Rather the market is making all kinds of positive presumptions in terms of what it appears to perceive as the most positive outcomes. And they may well be correct, But whether these presumptions are correct, or not, I’m not one to say. However, it appears that if these presumptions are wrong, then the risk is very much under-appreciated. For now, this market hears of no risk, sees no risk, and speaks of no risk.”

Risk Happens Fast

His comments are certainly worth considering, even if you are “uber” bullish and completely disagree with my assessment. The reason is that when markets heavily discount downside risk or become exceedingly complacent, such creates an atmosphere where a rapid unwinding of markets can occur.

“When we superimpose the market structure (with so many in one side of the investment boat), the secondary market implication is a continuation of a new regime of heightened volatility and a wide trading range. Such favors trading sardines over eating sardines.” –Doug Kass

Investors tend to make critical mistakes in managing their portfolios.

- Investors are slow to react to new information (they anchor), which initially leads to under-reaction but eventually shifts to over-reaction during late-cycle stages.

- The “herding” effect ultimately drives investors. A rising market leads to “justifications” to explain over-valued holdings. In other words, buying begets more buying.

- Lastly, as the markets turn, the “disposition” effect takes hold, and winners are sold to protect gains, but losers are held in the hopes of better prices later.

While the market is bullish now, and there is clearly an upside bias, an unexpected, exogenous event will cause a sharp reversal. Such suggests hedging equity risk until there is more “clarity” concerning the risk and reward.

As we have stated previously, “risk happens fast.”

Why We Hold Cash

The great thing about holding extra cash is that it is a simple process to make the proper adjustments to increase portfolio risk if we’re wrongs. However, if we are right, we protect investment capital from destruction and spend far less time “getting back to even.”

Importantly, I want to stress that I am not talking about being 100% in cash.

I am suggesting that holding higher levels of cash during periods of uncertainty provides both stability and opportunity. With heightened political, fundamental, and economic risks, understanding the value of cash as a “hedge” against loss becomes more important.

Given the length of the current market advance, deteriorating internals, high valuations, and weak economic backdrop, reviewing cash as an asset class in your allocation may make some sense. Chasing yield at any cost has typically not ended well for most.

Of course, since Wall Street does not make fees on investors holding cash, maybe there is a reason they are so adamant that you remain invested all the time.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

Discover All You Are Missing At RIAPRO.NET

This is what ourRIAPRO.NET subscribers are reading right now! Risk-Free For 30-Day Trial.

- Sector & Market Analysis

- Technical Gauge

- Fear/Greed Positioning Gauge

- Sector Rotation Analysis (Risk/Reward Ranges)

- Stock Screens (Growth, Value, Technical)

- Client Portfolio Updates

- Live 401k Plan Manager

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert, do not hesitate to contact me.

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free), you can access our live 401k plan manager.

Compare your current 401k allocation to our recommendation for your company-specific plan and our on 401k model allocation.

You can also track performance, estimate future values based on your savings and expected returns, and dig down into your sector and market allocations.

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.