Earnings Recession Coming Was Originally Published At MarketWatch

An earnings recession is coming as the Fed hikes rates which accelerates an economic recession. Such should be no surprise given earnings are derived from economic activity.

However, despite economic growth already showing signs of weakness, inflation running at the highest level in 40-years, and the Fed moving aggressively to tighten monetary policy, Wall Street analysts continue to suggest strong profit margins and rising earnings into 2023.

The Fed raised interest rates last week by 75 basis points, the biggest increase since the mid-1990s, to curb inflation. The central bank indicated it would keep lifting rates, a strategy that will inevitably hurt the economy and the jobs market.

For the purposes of this article, we are defining an earnings recession as a period in which corporate earnings, or profits, are below the year-earlier level for two consecutive quarters. Using this measure, there have been 19 earnings recessions since 1948, with at least three instances in the past 10 years.

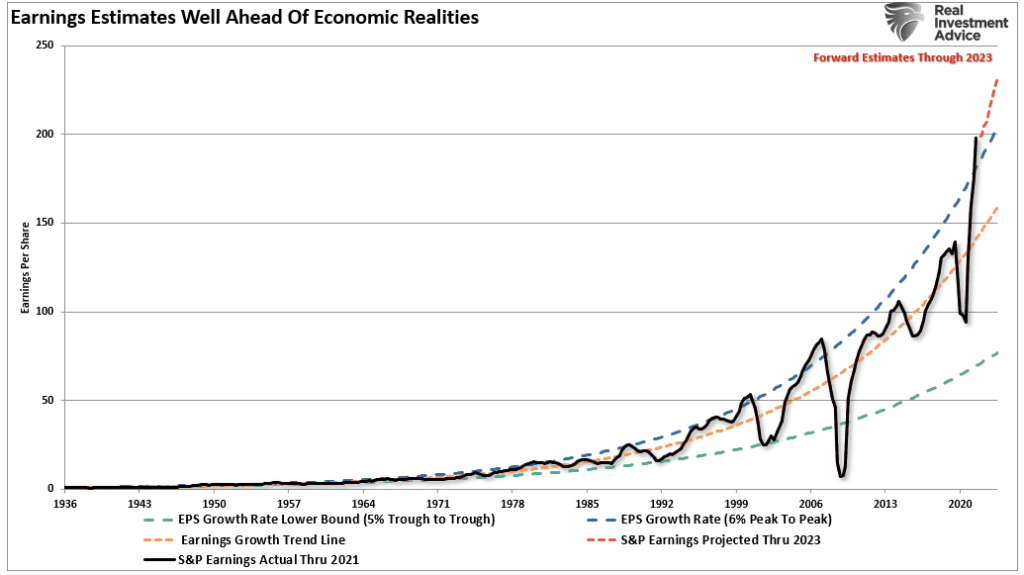

Over the long term, the economy grows at about 6%. Therefore, earnings growth also runs at roughly ~6% on a peak-to-peak basis. However, analysts suggest that earnings growth into 2023 will run well above the historical growth rate despite forecasts of much slower economic activity.

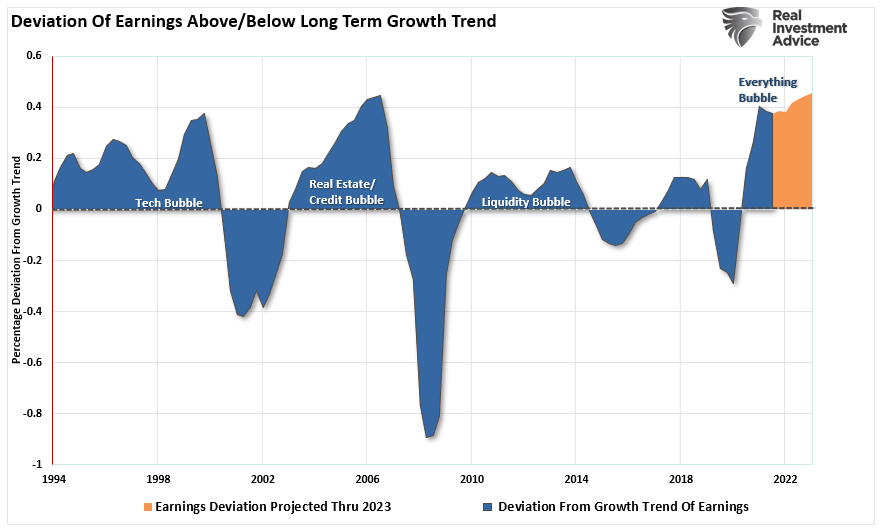

To put that into perspective, analysts’ estimates are currently at the most significant deviation above that 6% earnings growth trend.

The only two previous periods with similar deviations are the “Financial Crisis” and the “Dot.com” bubble.

While Wall Street analysts currently remain exuberant about earnings growth, an economic reversion resulting from tighter monetary policy will lead to an earnings recession.

The Fed Will Cause An Earnings Recession

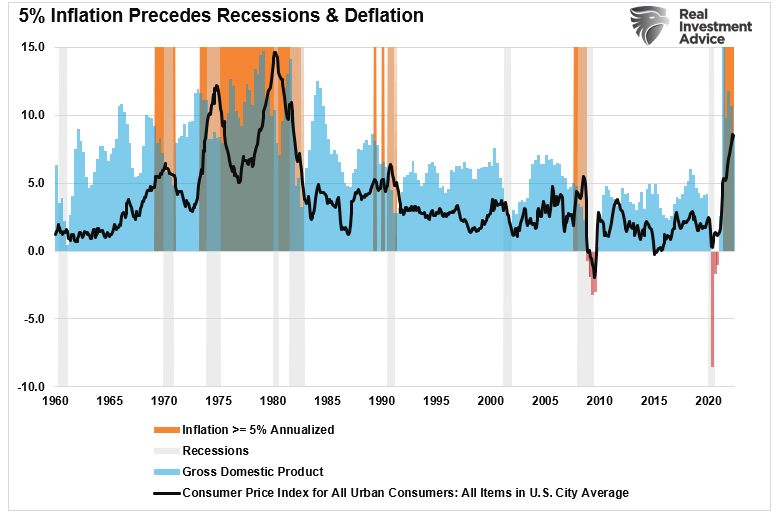

As noted, with inflation already running at 40-year highs, the risk of an economic recession has risen markedly in 2022. Historically, when inflation rises by more than 5% annually, such has triggered an economic contraction.

As shown, inflation tends to be its cure as “high prices cure high prices” by slowing economic demand. However, as the Fed hikes rates to slow economic growth, thereby reducing inflation, they risk pushing the economy into a contraction. Given consumers’ dependence on low rates to support economic growth, the risk of a policy mistake remains elevated.

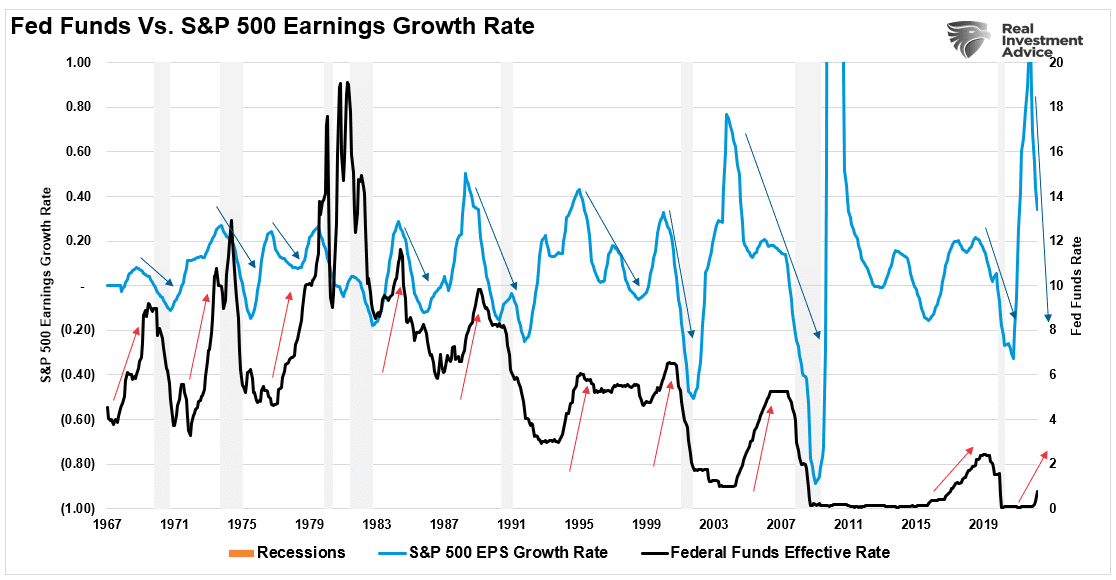

Of course, since earnings are highly correlated to economic growth, earnings don’t survive rate hikes. As the arrows show, Fed rate increases consistently lead to an earnings recession.

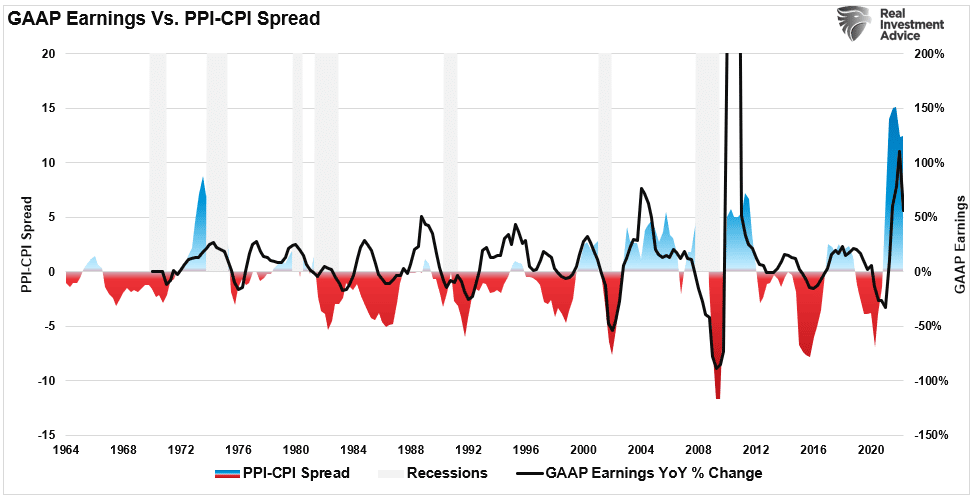

The Fed is in a difficult position. Producer prices, as shown below, have risen substantially faster than consumer prices. Such suggests that companies are absorbing input costs they can’t pass on to consumers. Eventually, the absorption of higher costs impairs profitability and reduces earnings.

When the inflation spread rises enough to impair profitability, corporations take defensive measures to reduce costs (layoffs, cost cuts, automation.) As job losses increase, consumers contract spending, which pushes the economy towards a recession.

The economy slows even faster if the Fed hikes rates to slow inflation. While no one currently expects an earnings recession, few tailwinds are supporting economic growth. The combination of geopolitical events and Fed policy will make continued growth even more challenging.

The Market Is Sending A Signal

Many analysts hope the Fed can engineer a “soft landing” for the economy. Such is an outcome where the economy slows, and inflation comes down but avoids a recession. Given that the surge in economic growth and inflation resulted from the massive liquidity injections in 2020-2021, the “reversion” will be just as significant.

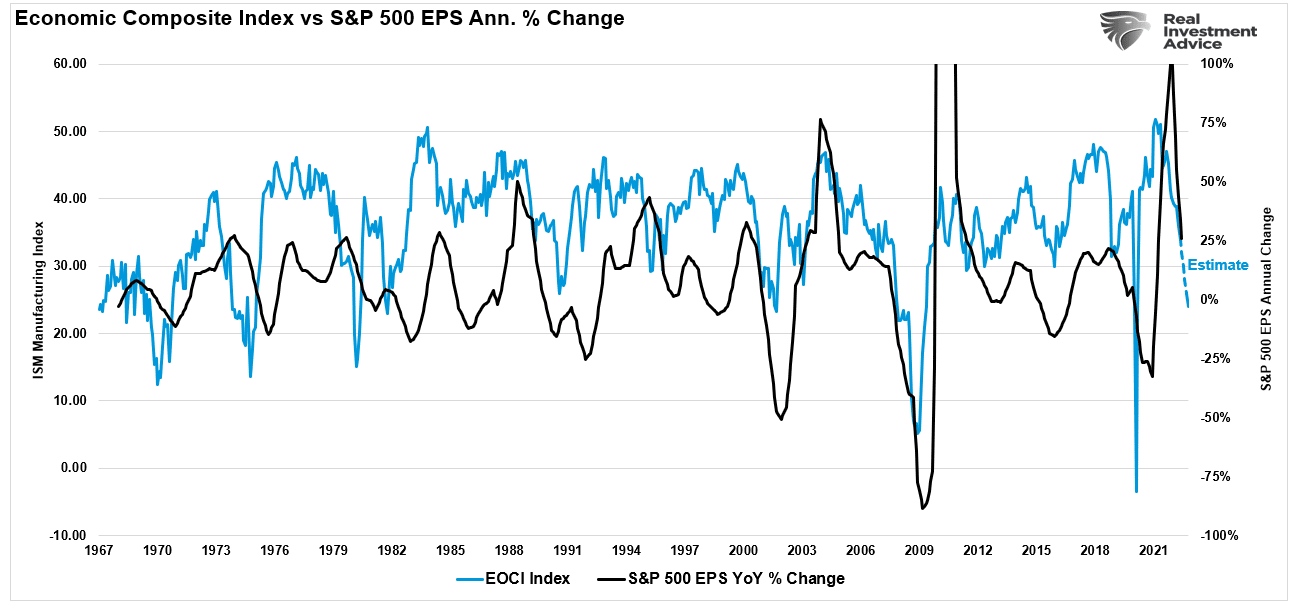

Our composite economic indicator closely tracks the economy using more than 100 data points. Not surprisingly, the surge in the composite from the 2020 lows has already reversed along with earnings growth rates. As noted, the economic and earnings correlation should be no surprise.

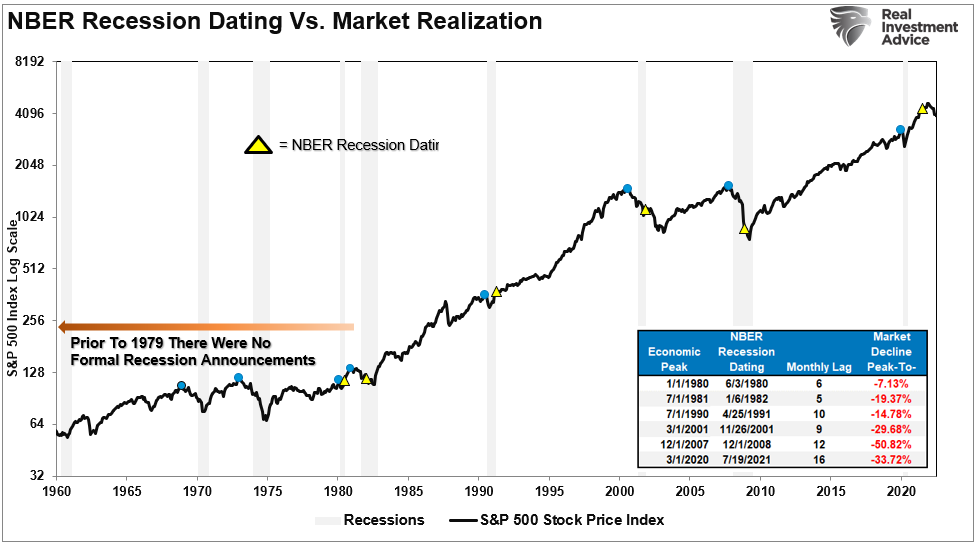

The market is also confirming the same. Historically, the stock market leads economic recessions by 6 to 9 months. When the National Bureau of Economic Research announces a recession, it is much too late to matter.

Lastly, during the previous four recessions and subsequent bear markets, the typical revision to consensus EPS estimates before the onset of a recession ranged from -6% to -18%, with a median of 10%. Coming out of recession, analysts start to increase estimates markedly.

Notably, while forward P/E ratios have declined, much of that is due to the decline in the “P” and not the “E.” Therefore, if an earnings recession is coming, as the data suggests, then the current “bear market” cycle still has more work to do.

The realignment of market prices and valuations is always a brutal process. While many believed the Fed had eliminated bear markets and economic recessions, the business cycle can only be delayed but never repealed.

We are just starting the negative revision phase which makes risk management in portfolios a key priority for now. However, the reversal of those earnings trends will be key in identifying the bear market end and the beginning of the next investible bull market cycle.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read