Is The Great “Bear Market” Of 2021 Finally Over?

In this October 8, 2021 issue of “Is The Great ‘Bear Market’ Of 2021 Finally Over.?

- Is The “Great Bear Market” Finally Over?

- Debt Ceiling Resolution Is Only Temporary

- Odds Are We’ve Seen The Highs For The Year

- Portfolio Positioning

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Is It Time To Get Help With Your Investing Strategy?

Whether it is complete financial, insurance, and estate planning, to a risk-managed portfolio management strategy to grow and protect your savings, whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Is The Great “Bear Market” Finally Over?

In last week’s newsletter, we stated:

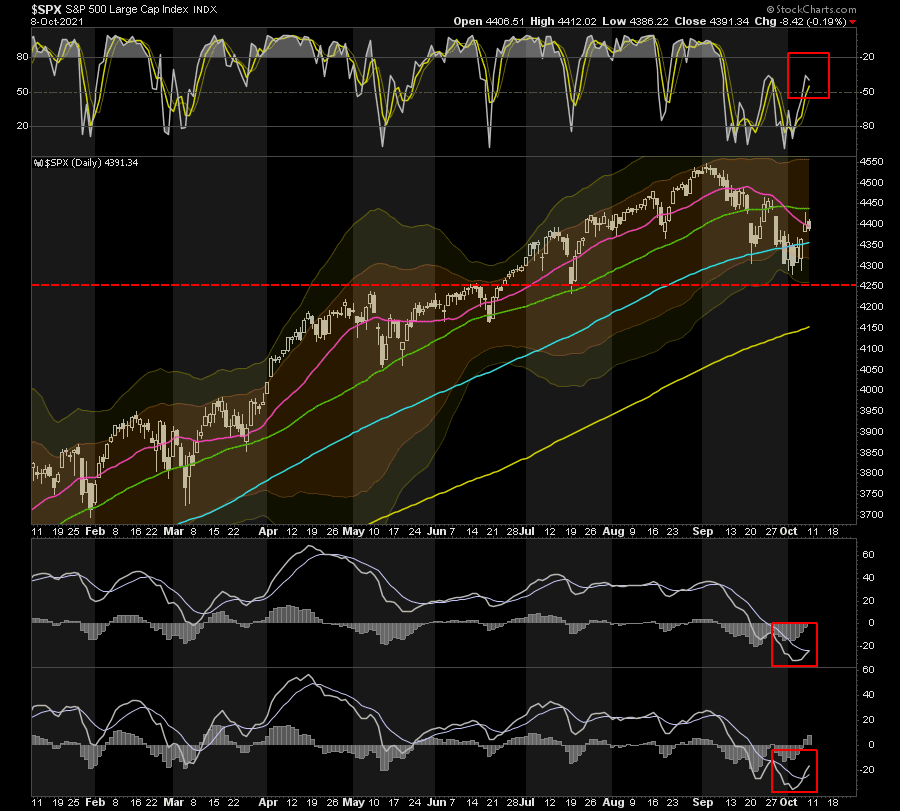

“It is worth noting there are two primary support levels for the S&P. The previous July lows (red dashed line) and the 200-dma. Any meaningful decline occurring in October will most likely be an excellent buying opportunity particularly when the MACD buy signal gets triggered.

The rally back above the 100-dma on Friday was strong and sets up a retest of the 50-dma. If the market can cross that barrier we will trigger the seasonal MACD buy signal suggesting the bull market remains intact for now.“

Chart updated through Friday

Notably, the very short-term moving average convergence divergence (MACD) indicator (lower panel) did trigger this past week. With markets not yet back to extremely overbought territory, and sentiment still very negative, the bulls are trying to reclaim the 50-dma.

Our seasonal MACD indicator (next to the bottom panel) also triggered, but just barely. We need to see some follow-through buying action next week.

Money Flow Buy Signal Also Positive

The RIAPRO Money Flow indicator also triggered a buy signal, becoming more robust support for a short-term rally this past week.

So, do all these signals mean the “Great Bear Market Of 2021” is behind us?

After a harrowing 5% decline, sentiment is now highly negative, supporting a counter-trend rally in the markets. Thus, we think there is a tradeable opportunity between now and the end of the year. But, as we will discuss below, significant headwinds continue to accrue, suggesting higher volatility in the future.

I want to reiterate our conclusion from last week:

“If you didn’t like the recent decline, you have too much risk in your portfolio. We suggest using any rally to the 50-dma next week to reduce risk and rebalance your portfolio accordingly.

While the end of the year tends to be stronger, there is no guarantee such will be the case. Once the market “proves” it is back on a bullish trend, you can always increase exposures as needed. If it fails, you won’t get forced into selling.“

That advice remains apropos this week as well. The biggest mistake investors make is allowing emotion to dominate their investment decision-making process. Such is why “buy and hold” investing is appealing during a bull market because it removes decisions from portfolio management.

However, as we discussed this past week in “The Best Way To Invest.”

“Buy and hold” strategies are the “best way” to invest until they aren’t.“

The Debt Ceiling Non-Crisis

As discussed in the “Debt Ceiling Non-Crisis,” the hyperbole surrounding the debt limit was on full display, culminating with this tweet from Bernie Sanders:

While “Ole’ Bernie” is trying to coerce his counterparts to raise the debt limit, his statement is full of misinformation to scare individuals. As noted in our article:

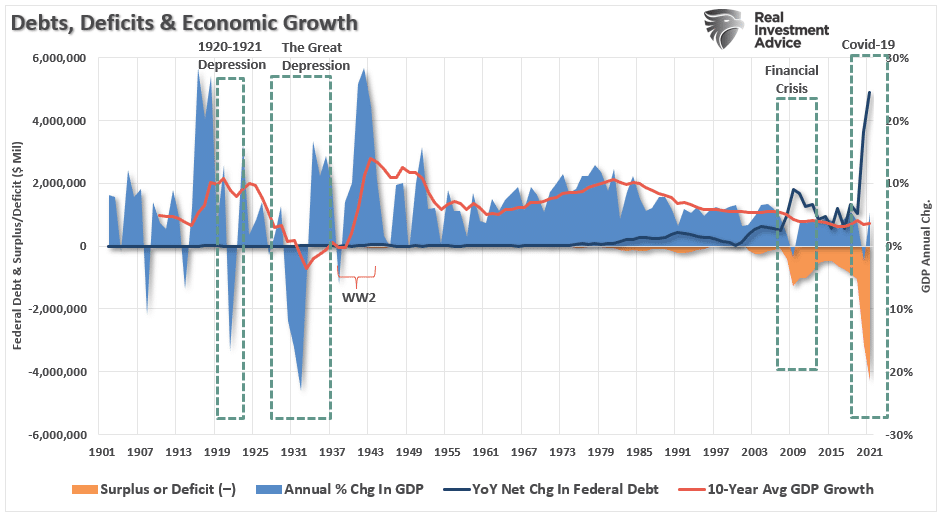

“In 1980, that all changed, and seven administrations and four decades later, Government debt surged, deficits exploded, and the debt ceiling rose 78 times. (49 times under Republicans and 29 times under Democrats.)

As Congress lifts the debt ceiling for the 79th time, the runaway spending and deficit increases continue to accelerate. The consequence of increasing debts and deficits is evident in the declining economic growth rates over the past 40-years.”

In other words, this isn’t about paying bills from the Trump Administration, but also every President before him back to Ronald Reagan. For each year that we amass more enormous debts and deficits, the interest payments increase along with the growing burden of “mandatory spending.”

The problem today, as discussed in the “Insecurity Of Social Security,”

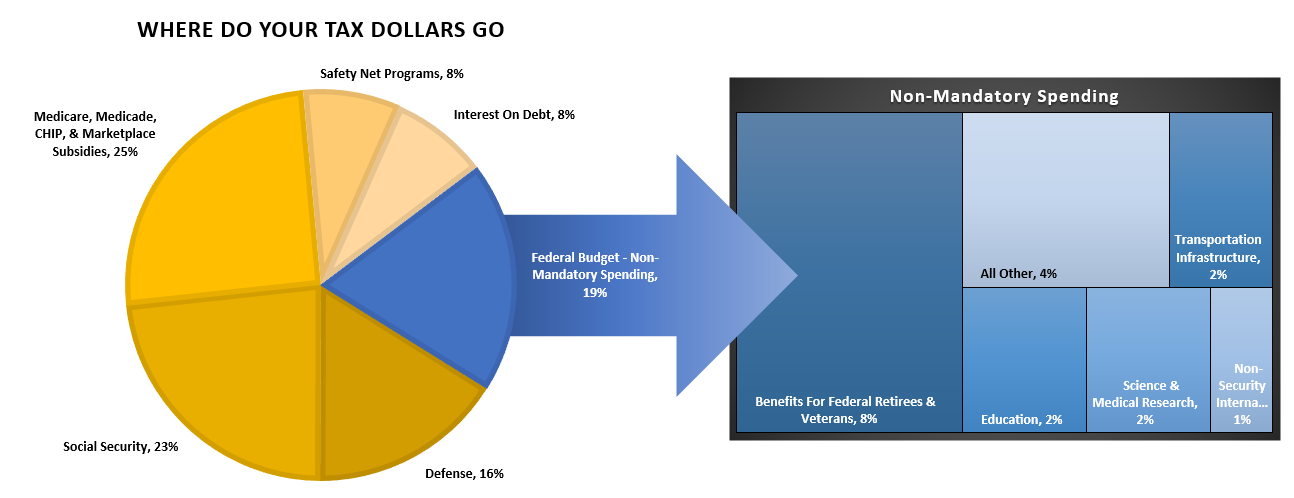

“In the fiscal year 2019, the Federal Government spent $4.4 trillion, amounting to 21 percent of the nation’s gross domestic product (GDP). Of that $4.4 trillion, federal revenues financed only $3.5 trillion. The remaining $984 billion came from debt issuance. As the chart below shows, three major areas of spending make up most of the budget.”

In 2019, 75% of all expenditures went to social welfare and interest on the debt. Those payments required $3.3 Trillion of the $3.5 Trillion (or 95%) of the total revenue collected. Given the decline in economic activity during 2020, those numbers become markedly worse. For the first time in U.S. history, the Federal Government will have to issue debt to cover the mandatory spending.“

Only A Temporary Fix

Think about that for a moment. In 2021, we will spend more on our “mandatory spending” than “revenue” will cover. Such means the Government will continue to go further into debt every year just to run the country. On top of the required spending, our politicians now want to add another $5 trillion in debt for “infrastructure.”

See the problem here.

The “debt ceiling” was always a “non-crisis.” It was just political brinksmanship playing out on national television. The resolution, as expected, came last week with Senate Minority Leader, Mitch McConnell, proposing a debt limit ceiling lift to $29 trillion. Such will fund the government through December.

“Senate leaders reached a bipartisan agreement Wednesday to defuse the impending debt limit crisis by allowing for a short-term increase in the statutory borrowing cap while lawmakers negotiate a longer-term solution.

Democrats said they would agree to an offer from Minority Leader Mitch McConnell that would pave the way for an increase in the debt limit into December. But the two parties still disagreed on any long-term strategy.” – Roll Call

While raising the debt ceiling may look like a victory for the Democrats, it may not be.

“While raising the debt ceiling just once is proving to be a challenge, the only thing worse would be having to vote to raise it twice

‘From a political perspective, the only thing less attractive than voting to raise the debt limit to $31 trillion is voting to raise it to $29 trillion and then voting a second time to raise it to $31 trillion’” – Zerohedge

In Case You Missed It

Odds Increasing We’ve Seen The Highs For This Year

There are reasons to be optimistic as we head into the seasonally strong period of the year. However, while the seasonal and technical backdrop is improving short term, we should not dismiss the numerous headwinds.

- Valuations remain elevated.

- Inflation is proving to be sticker than expected.

- The Fed will likely move forward with “tapering” their balance sheet purchases in November.

- Economic growth continues to wane.

- Corporate profit margins will shrink due to inflationary pressures.

- Earnings estimates will get downwardly revised keeping valuations elevated.

- Liquidity continues to contract on a global scale

- Consumer confidence continues to slide.

While none of these independently suggest a significant correction is imminent, they will limit the market’s advance making new highs less attainable. Furthermore, given the “debt crisis” will return in December, the risk of volatility remains elevated.

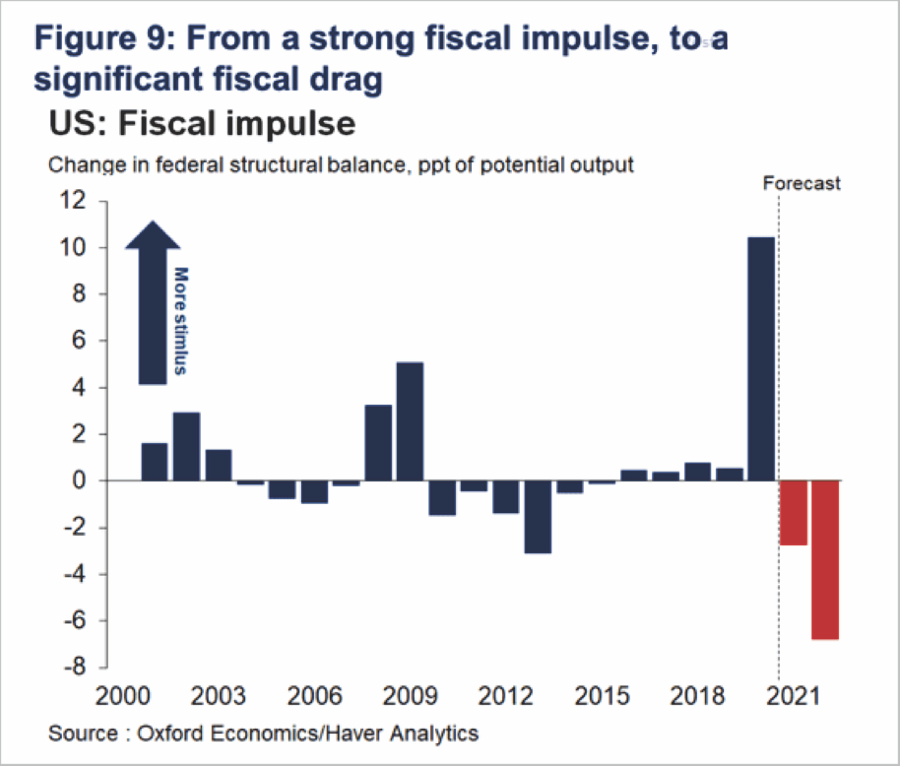

Much of the mainstream media overlooks the rapid decline in liquidity that supported the market over the last year. While the “human infrastructure” bill will provide some support, the difference is the spending is spread out over 10-years versus the “checks to households” in 2020.

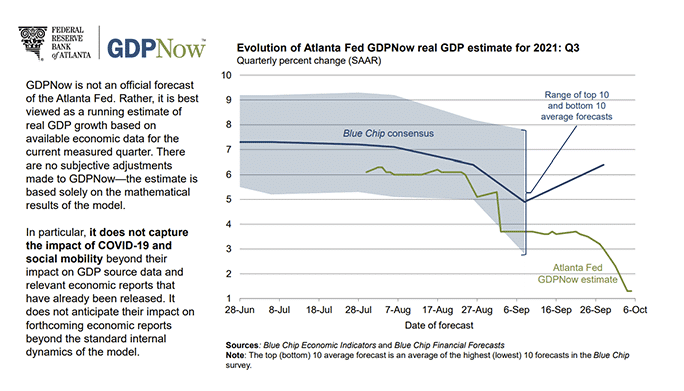

Furthermore, that liquidity drain is rapidly deteriorating the outlook for economic growth. Here is the latest report from the Atlanta Federal Reserve:

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2021 is 1.3 percent on October 5, down from 2.3 percent on October 1. “

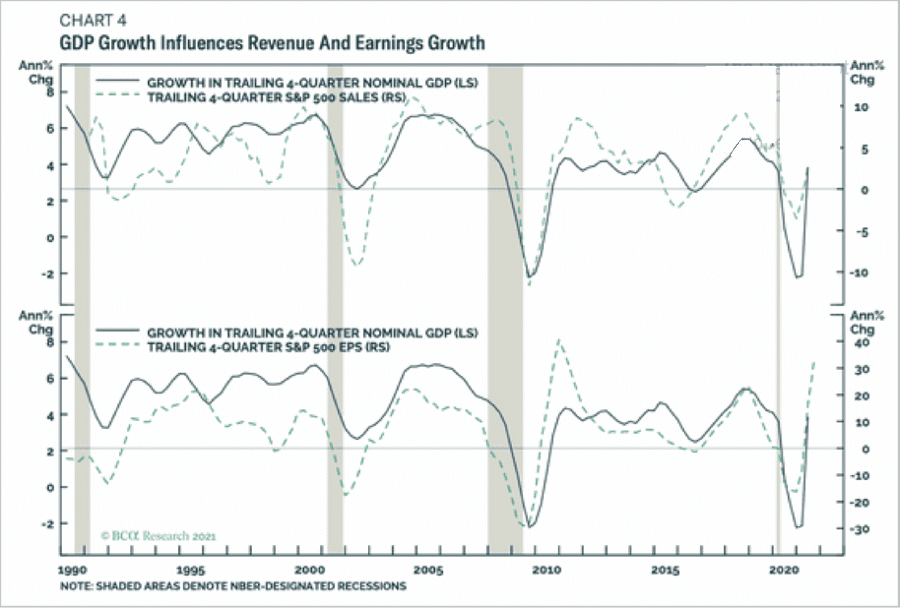

As BCA Research shows, as we head into the last quarter of the year and 2022, the slower economic growth rates will coincide with corporations’ weaker revenue and earnings growth.

As noted, with valuations already elevated, a reversal in earnings growth will likely limit a stronger advance.

Portfolio Update

We discussed last week that after taking profits in August and raising cash, we slowly started adding back into our equity holdings. The recent spike in bond yields also allowed us to increase the duration of our bond portfolio this week.

We continued that process early this week, adding additional exposures and rebalancing portfolio risk by reducing laggards.

We are now at target weight in our equities, slightly overweight in cash, and our duration is somewhat shorter than our benchmark. As noted above, while we are looking for a market recovery through year-end, we are keeping a slightly cautious positioning bias to our models. If we are wrong and the market breaks vital support levels, we will reverse our positioning.

For now, we are giving the market the benefit of the doubt. However, we are keeping our positioning on a very short leash. With valuations still elevated, the technical deterioration of the market remains a primary concern. Such was a point we made in our Daily Market Commentary this week:

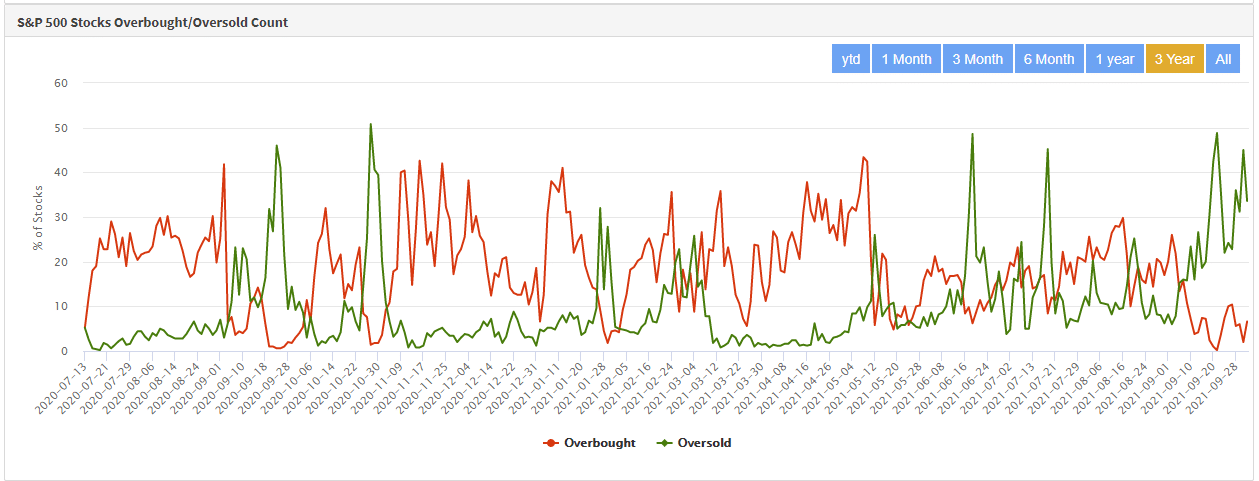

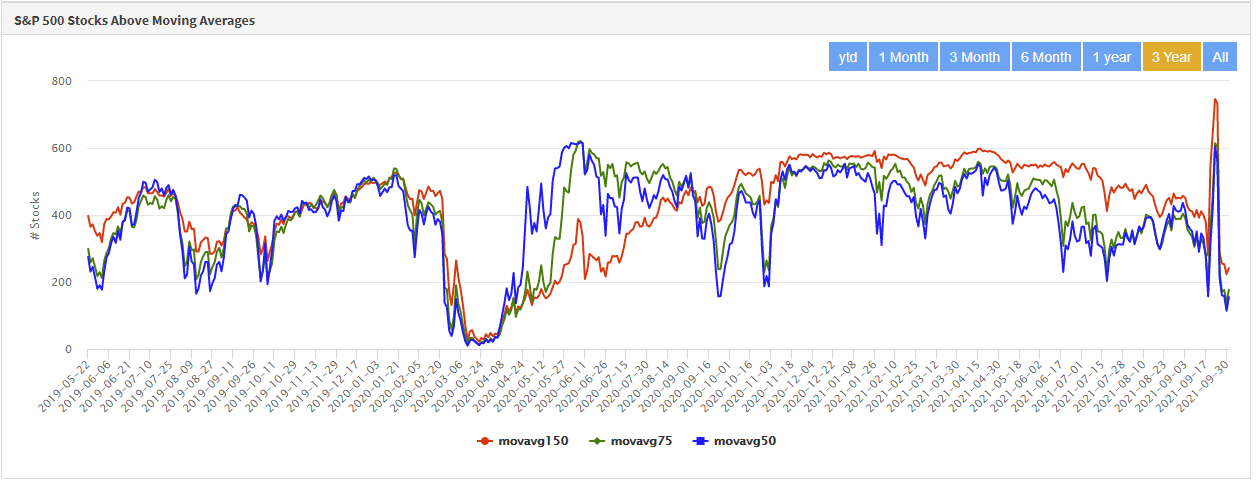

On RIAPRO, we provide the sentiment and technical measures we follow. The number of oversold stocks is back towards extremes, which supports the idea of a short-term rally.”

“However, the overall “breadth” and “participation” of the market remains highly bearish. Thus, to avoid a deeper correction, breadth must improve.“

We are watching these technical measures very closely as they will dictate our next course of action.

Have a great weekend.

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

Discover All You Are Missing At RIAPRO.NET

Come find out what our RIAPRO.NET subscribers are reading right now! Risk-Free For 30-Day Trial.

- Sector & Market Analysis

- Technical Gauge

- Fear/Greed Positioning Gauge

- Sector Rotation Analysis (Risk/Reward Ranges)

- Stock Screens (Growth, Value, Technical)

- Client Portfolio Updates

- Live 401k Plan Manager

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

Attention: The 401k plan manager will no longer appear in the newsletter in the next couple of weeks. However, the link to the website will remain for your convenience. Be sure to bookmark it in your browser.

Commentary

This past week, the markets finally bounced solidly off of support and above the 100-dma. With the markets approaching the “seasonally strong” period of the year, we are looking for our MACD signals to confirm our current positioning. As noted in this week’s newsletter, we may have seen the highs for this year, and 2022 may well see an increase in volatility.

As noted last week:

“With the correction complete, and markets very oversold short-term, portfolio allocations can remain at current levels. Cash that accumulated over the past few weeks can now get deployed to allocations. Also, rebalance your bonds back to weightings after the recent rise in rates.”

That remains the case again this week. Importantly, continue to remain overweight large-cap domestic stocks and vastly underweight international, emerging markets, small and mid-capitalization stocks. Inflationary pressures will hit those areas the hardest in the future.

There is no need to be aggressive here. There is likely not a lot of upside between now and the end of the year.

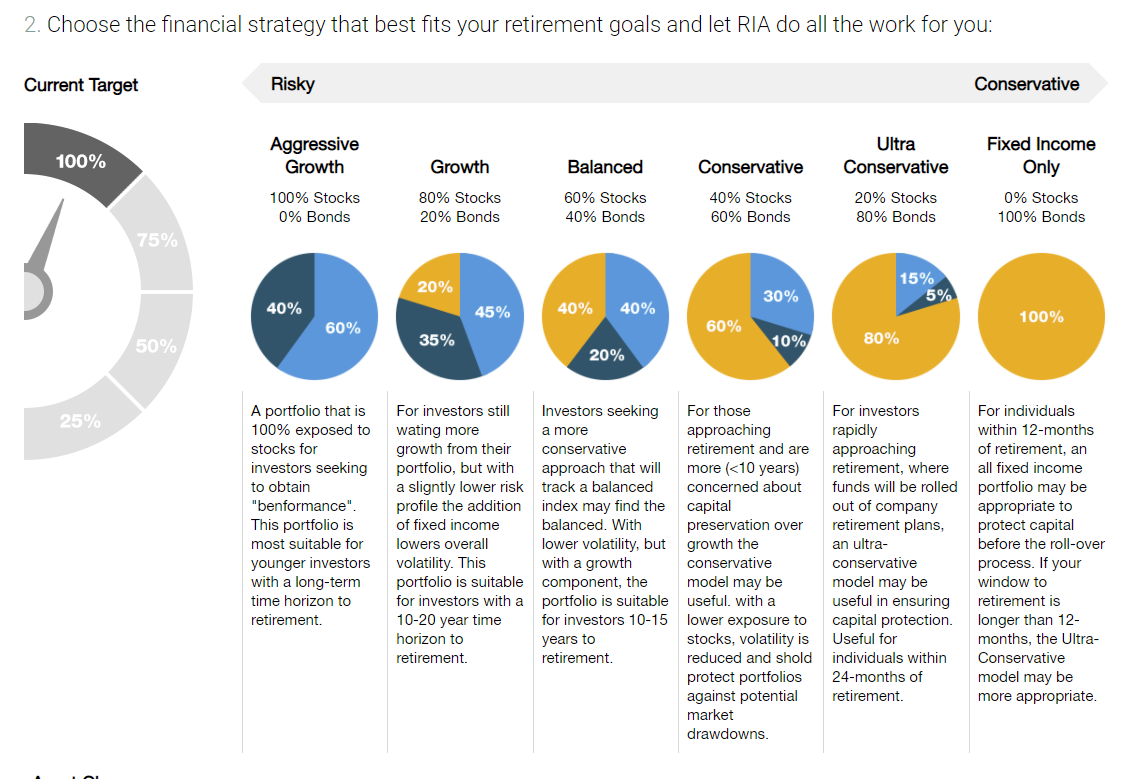

Model Descriptions

Choose The Model That FIts Your Goals

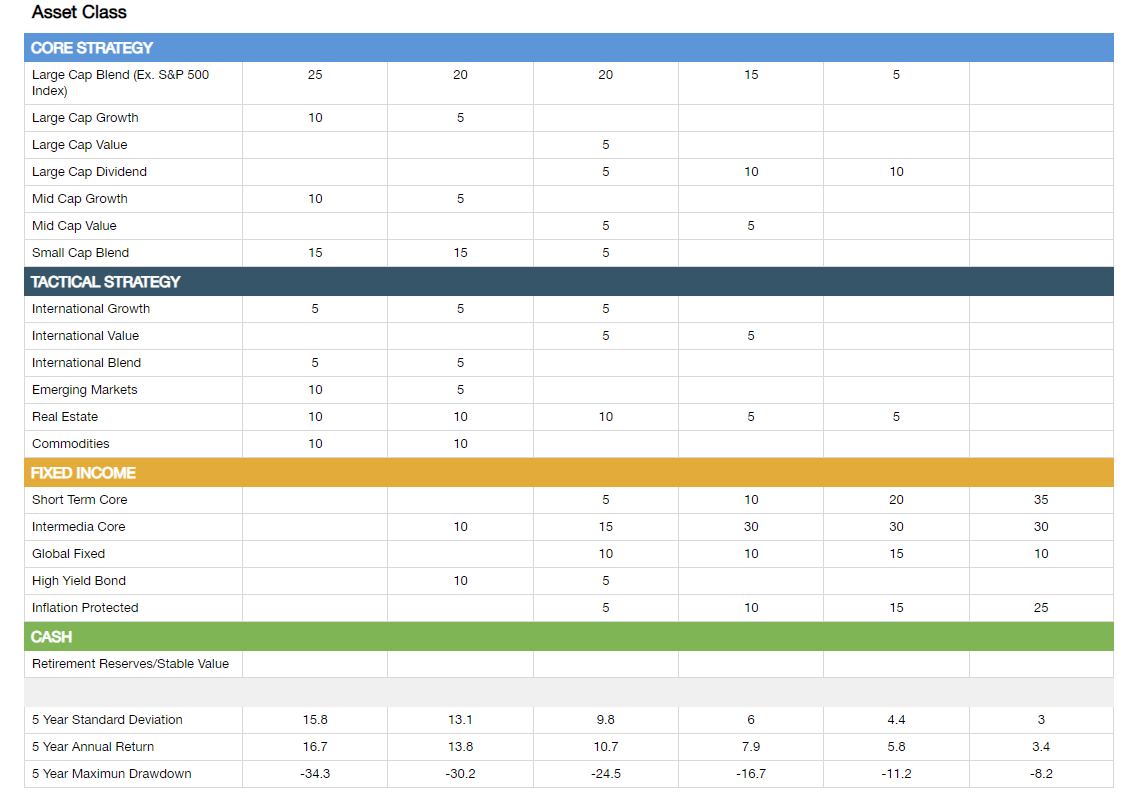

Model Allocations

If you need help after reading the alert, do not hesitate to contact me.

Or, let us manage it for you automatically.

401k Model Performance Analysis

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

Have a great week!