Inside This Week’s Bull Bear Report

- The FOMC Meeting Approaches

- Head Fake Or Breakout?

- How We Are Trading It

- Research Report – Is The Fed Trying To Wean Markets Off Monetary Policy

- Youtube – Before The Bell

- Stock Of The Week

- Daily Commentary Bits

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

The FOMC Meeting Approaches

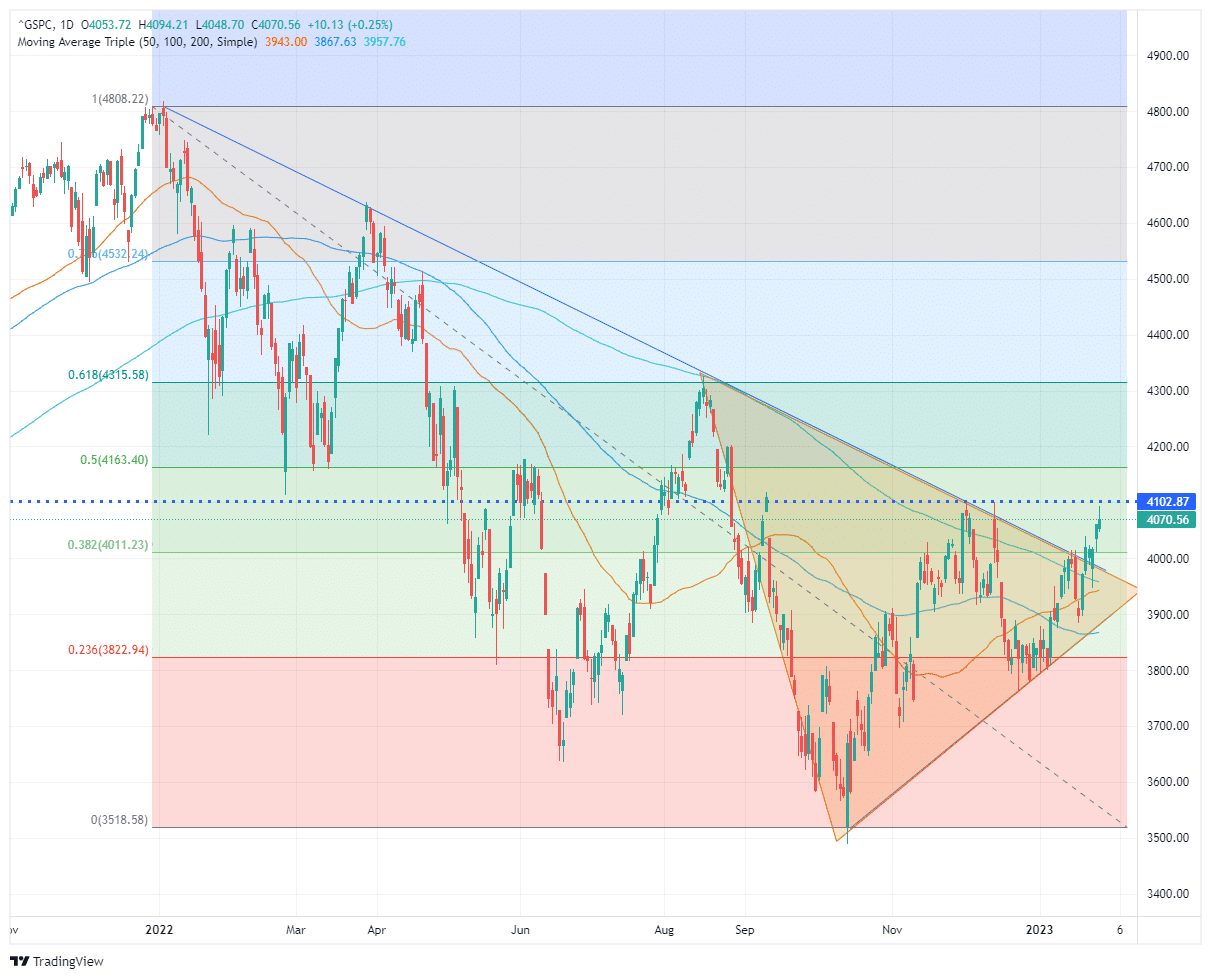

Was the break above the long-running downtrend line a “head fake?” Maybe. However, before we get into the analysis, let’s review where we left off last week. Such is critically the case as we head into this coming week’s FOMC meeting and policy announcement.

The upcoming FOMC meeting will likely determine the market’s direction over the next few weeks. While many market participants are hoping for a “kinder, gentler Fed,” As noted previously, the recent commentary suggests such may not be the case.

“The most critical tidbit came from St Louis Fed president Jim Bullard (a non-voter this year), who spoke to the WSJ’s Fed Mouthpiece Nick Timiraos. He stated that while US interest rates have to rise further to ensure that inflationary pressures recede, ‘the US is now ‘almost’ in the restrictive territory.

That point was echoed by Loretta Mester, as the Fed wants to ensure inflation will come down on a steady path to the 2% target. ‘I just think we need to keep going, and we’ll discuss how much to do at the next meeting.’ Mester said that she expects the Fed’s policy rate to go ‘a bit higher’ than 5% and stay there for some time to slow inflation further.”

As we further noted, our concern remains that while the Fed is suggesting further tightening, the 3-month average of inflation has already returned to the Fed’s target rate. Such means the Fed is running a significant risk in overtightening policy and causing a sharper economic downturn than is currently priced into asset prices.

The reason for the rehash is this coming week’s FOMC meeting, where the Fed is widely expected to hike rates by 0.25%, will impact market direction. The risk to the markets is that while the bulls have been driving asset prices higher since the beginning of this year, that increase in price works against the Fed’s agenda. The goal of tighter monetary policy by the Fed is to tighten monetary conditions to slow economic growth, thereby reducing inflation. However, higher asset prices boost consumer confidence and loosen monetary conditions. As noted by Liz Ann Sonders, financial conditions have eased dramatically since October.

Per a speech Jerome Powell gave in early December:

“Officials seek to reduce inflation by slowing the economy through tighter financial conditions—such as higher borrowing costs, lower stock prices, and a stronger dollar—which typically curb demand.”

Given that “easier” financial conditions risk keeping inflation elevated, it will not be surprising to see Jerome Powell deliver a starkly hawkish message next week. Such was what Powell did following previous market rallies in September and December to push markets lower and tighten financial conditions.

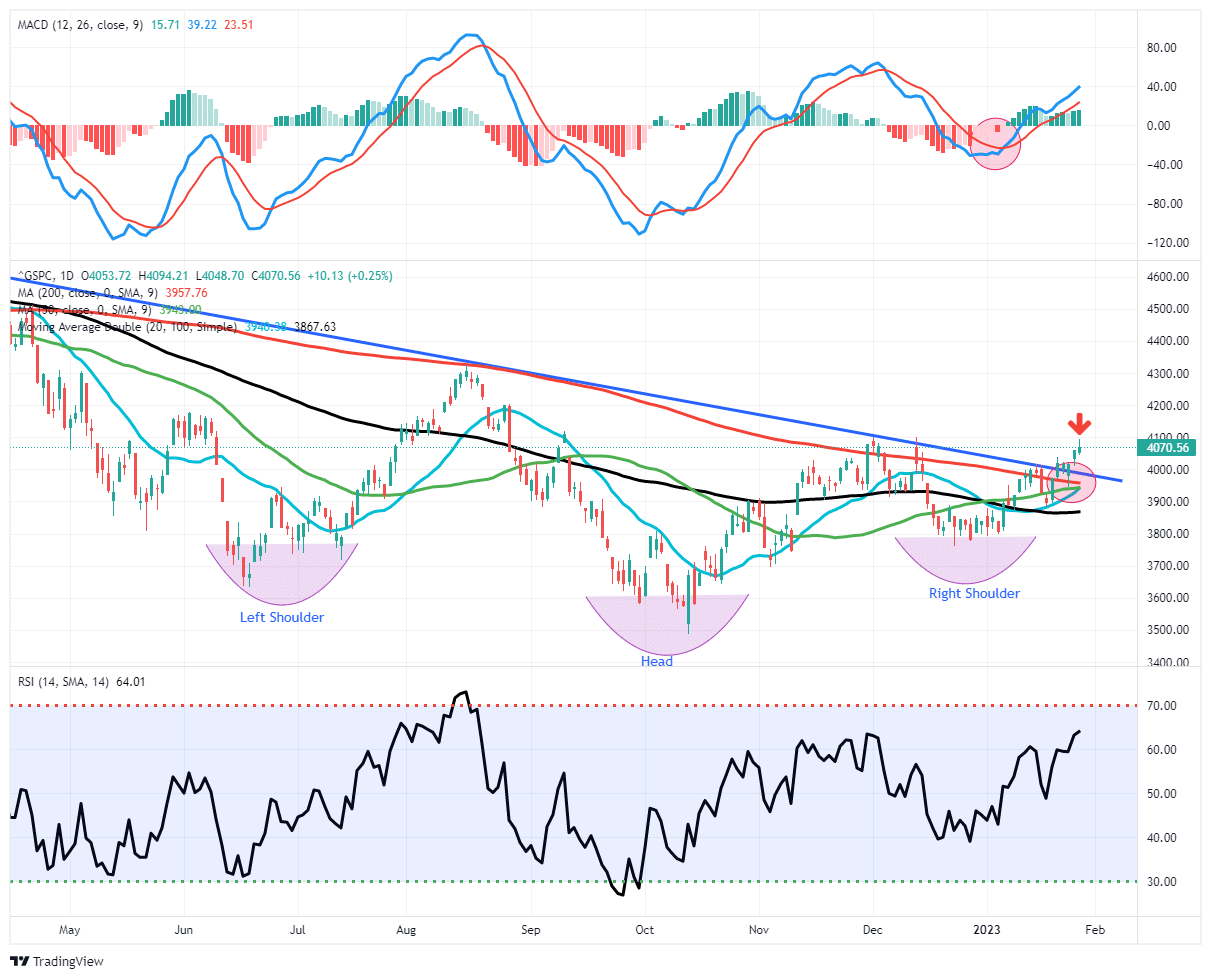

This brings us to this week’s analysis. Was this week’s technical breakout valid and leading to a further market advance, or was it just another “head fake?”

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Just Another “Head Fake?”

Over the last few weeks, we repeatedly discussed the consolidation occurring in the market. The compression of prices between the downtrend line from the January 2022 peak and the rising lows since October was an important focal point for investors. Such is shown in the chart below.

As you will note, since January’s market peak, each attempt to break above the falling downtrend line was a “head fake,” leading to lower prices. The good news is that, eventually, this cycle will end. At some point, the market will effectively “price in” the worst outcomes, and a break above the downtrend line will become sustainable. Such will confirm the beginning of a new bullish cycle for prices.

The evidence of a clear sustained break above the downtrend is not evident. That keeps the risk of a “head fake” higher for now. But, as shown below, several technical improvements to the broad market are worth watching.

While the flow of economic news and media headlines are filled with stories of an impending recession, the market has been firming since October, suggesting a potentially different outcome. As we noted, the inverse “head-and-shoulder” pattern already suggests a market bottom has formed. A solid break above the downtrend line (with a successful retest) would confirm the completion of that pattern.

Furthermore, the market is not extremely overbought, and shorter-term moving averages are slopping positively. Notably, the 50-DMA is rapidly closing in on a cross above the declining 200-DMA. Such is known as the “golden cross” and historically signifies a more bullish setup for markets moving forward.

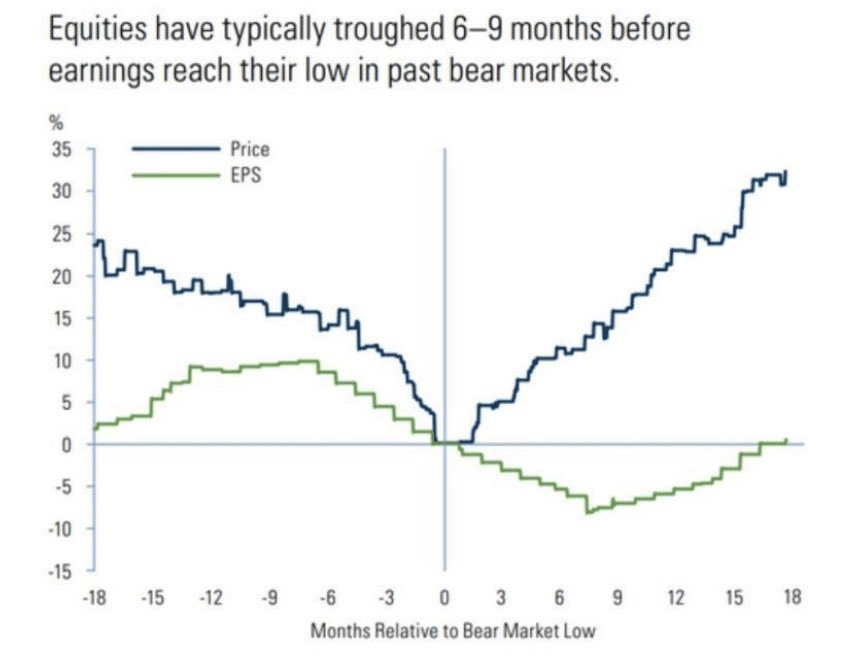

While it is possible that some bad news or an overly aggressive Fed could cause a “head fake” short-term, many of these bullish signals will complete in the months ahead. While that seems odd given the negative flow of economic and earnings data near term, historically, market prices tend to trough 6-9 months before earnings bottom. Such is because the market anticipates outcomes and was the subject of this week’s post on “Contrarianism.”

“As a contrarian investor, excesses get built when everyone is on the same side of the trade. Everyone is so bearish the markets could respond in a manner no one expects. This is why equities have historically bottomed between 6-to-9 months before the earnings trough.”

There are plenty of reasons to be very concerned about the market over the next few months. Given the market leads the economy, we must respect the market’s action today for potentially what it is telling us about tomorrow.

While this may be a “head fake” currently, I wouldn’t entirely dismiss the message of improving technicals either.

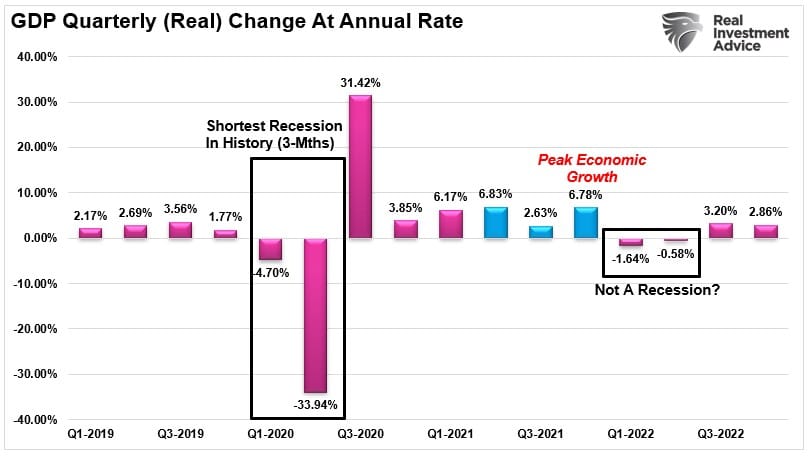

Q4 GDP Stronger Than Expected

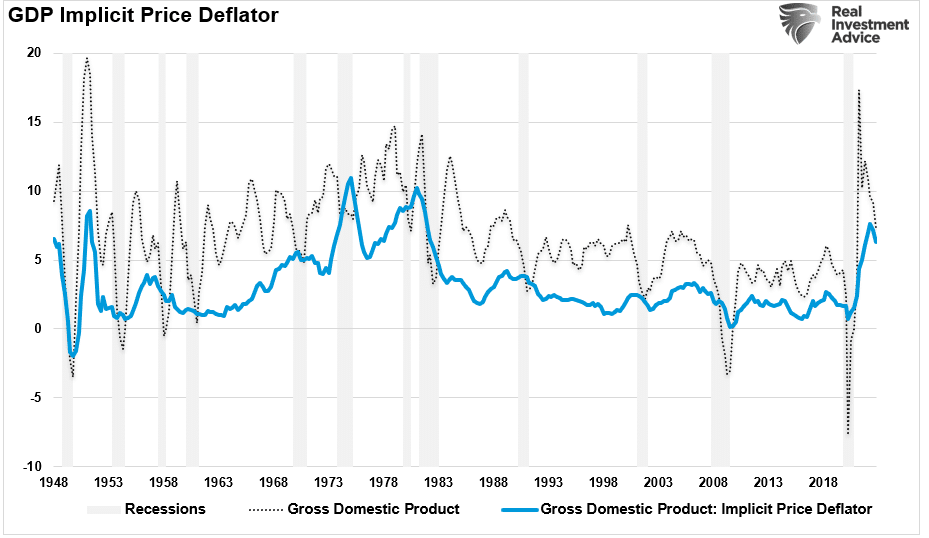

On Thursday, the Bureau of Economic Analysis reported the first estimate of the gross domestic product for Q4 2022. The initial read was stronger than expected on two fronts. The actual measure of economic growth was 2.9% annualized for 2.6% expected, but the inflation measure was also stronger at 3.5% versus 3.2%.

For the year, the economy grew slightly below 1%. Such does not allow the economy to slow without slipping into a recession. As Mish Shedlock noted:

“Money supply is falling off a cliff, another sign of economic weakness.”

That is a critical point, as the surge in monetary supply kept the economy afloat last year. However, that “pig in the python” is now exiting rapidly, exposing the underbelly of the economy. Such will also exacerbate the slowdown when the lag effect of monetary policy catches up with consumers.

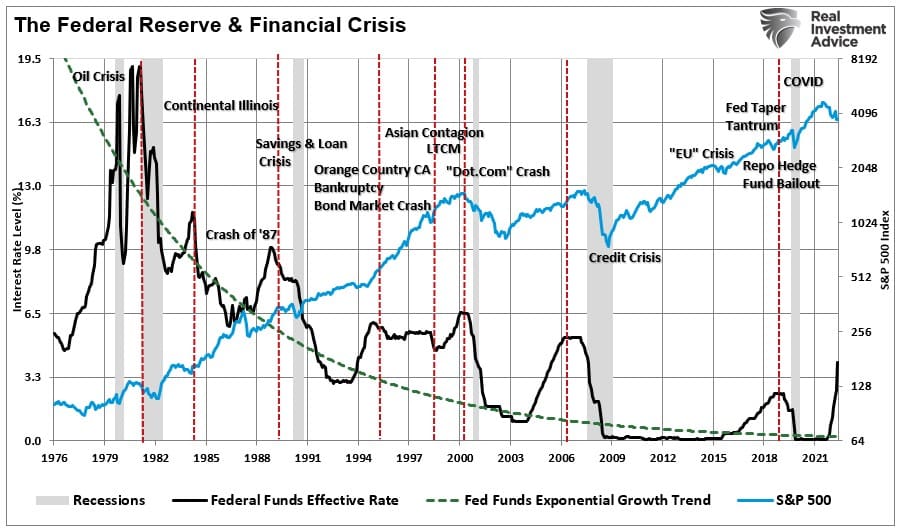

The Soft Landing Scenario

While ignored by the market, that stronger deflator will likely cause heartburn for the Federal Reserve heading into the FOMC meeting next week. As noted above, with monetary policy conditions easing sharply, the market rally is working against the Fed’s attempt to reduce inflation.

Nonetheless, the stronger-than-expected GDP report feeds into the “soft landing” scenario. As we discussed on Friday, the definition of a “soft landing” is:

“A soft landing, in economics, is a cyclical slowdown in economic growth that avoids a recession. A soft landing is the goal of a central bank when it seeks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation without causing a severe downturn.” – Investopedia

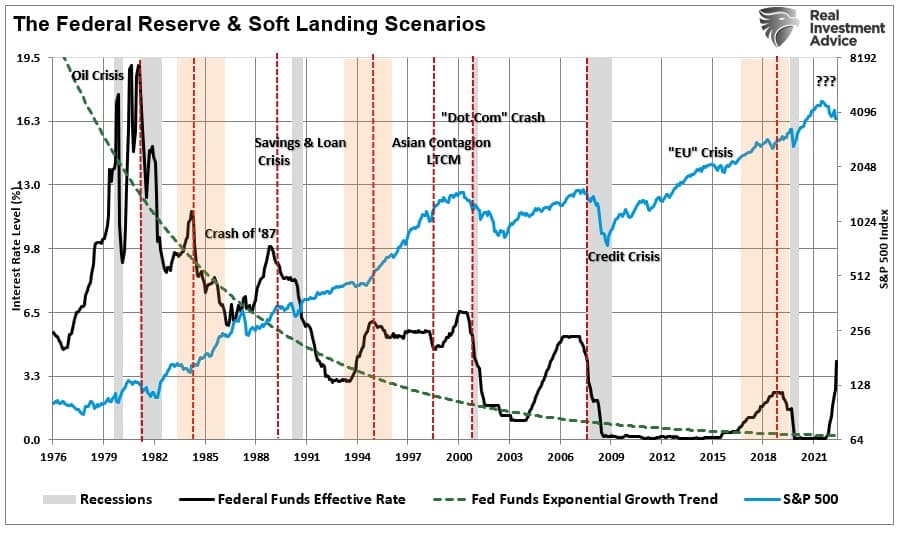

The term “soft landing” came to the forefront of Wall Street jargon during Alan Greenspan’s tenure as Fed Chairman. He was widely credited with engineering a “soft landing” in 1994-1995. The media has also pointed to the Federal Reserve engineering soft landings economically in both 1984 and 2018.

The chart below shows the Fed rate hiking cycle with “soft landings” notated by orange shading. I have also noted the events that preceded the “hard landings.”

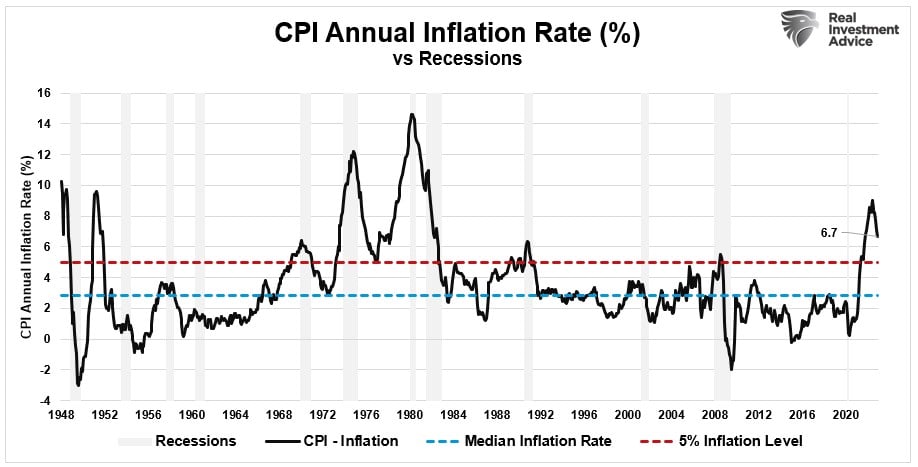

There is another crucial point regarding the possibility of a “soft landing.” A recession, or “hard landing,” followed the last five instances when inflation peaked above 5%. Those periods were 1948, 1951, 1970, 1974, 1980, 1990, and 2008. Currently, inflation is well above 5% throughout 2022.

Could this time be different? Absolutely, but there is a lot of history that suggests otherwise.

Furthermore, the technical definition of a “soft landing” is “no recession.“ The track record worsens if we include crisis events caused by the Federal Reserve’s actions. As noted above, there were three periods where the Federal Reserve hiked rates and achieved a “soft landing,” economically speaking. However, the reality was that those periods were not “pain-free” events for the financial markets. The chart below adds the “crisis events” that occurred as the Fed hiked rates.

The point is that the “bull versus bear” argument is not resolved.

This is why, at least for now, we are allowing the technical formations to drive investment decisions in the short term. However, we fully expect the fundamental realities to emerge by this summer, which is why we remain cautious.

Not Getting The Bull Bear Report Each Week In Your Mailbox? Subscribe Here For Free.

How We Are Trading It

It is a very confusing and challenging market to navigate currently. Last year, defense won the game, with Dow outperforming the Nasdaq by the widest margin in over two decades. This year, the Nasdaq is up more than 9%, and the “Generals” have re-emerged as market leaders.

Yet, this all occurs against a fairly dismal backdrop of data, as discussed in our recent post on “Contrarianism:”

- The Fed is remaining aggressive on monetary policy.

- Central banks are reducing liquidity to markets.

- Inflation remains problematic.

- Earnings remain elevated.

- The economy is slowing.

- Consumers are running out of savings.

We certainly agree with the more dismal outlook and continue to suggest that investors should be more cautious in their portfolio allocations. However, this is also the point where investors make the most mistakes. Emotions make us want to avoid all risks of loss. That is why investors almost always “sell” at the bottom of markets when they should buy.

Such is the point where we are today. There are lots of reasons to be bearish. However, the technical improvements in the market suggest investors should be buying. It’s hard. It also doesn’t mean it will immediately work, as the markets could correct first before the final bottom.

But this is the risk of investing. To make money investing in the financial markets, you have to put capital at risk of losing it. No “risk-free” investment will provide substantial rates of return over the long term. The question that investors must answer for themselves is how much of the “risk” has been removed from the financial equation.

Unfortunately, no one knows the answer. All we can do is make our best guess.

And that is the hard part.

Such is why over the last three weeks, we have repeatedly discussed the technical improvement of the market and the message it was sending. That technical improvement continues to push us to increase exposure cautiously. As noted last week:

“We did add some equity exposure this past week by adding back some of our energy positions we sold near recent peaks and a trading position in the S&P 500 equal weight index. We are also contemplating an increase in the duration of our bond portfolio following the most recent CPI report. The spread now between Treasury bonds, and the 3-month rate of inflation has now become extremely attractive. As we noted previously, there is a rising probability that bonds will outperform stocks in 2023. Such will result from disinflation becoming a deflationary (read: recessionary) environment.”

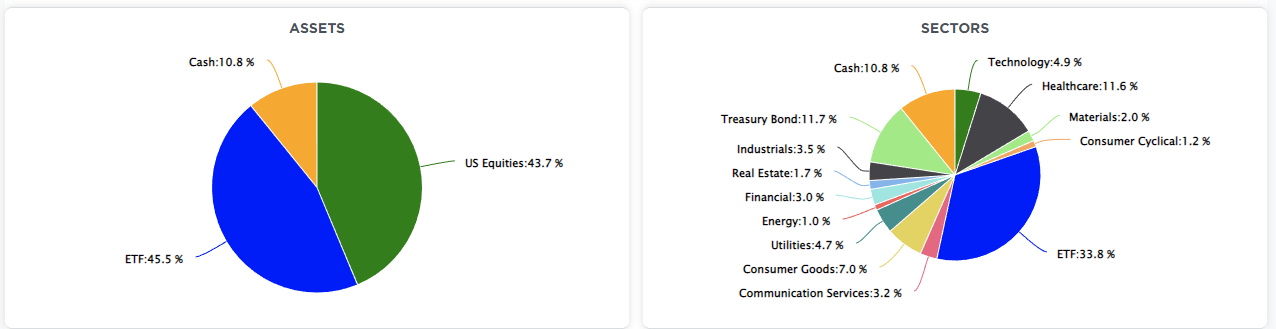

We continued to add exposure this week on the equity side of the portfolio and further reduced our overweight position in cash. We remain underweight in stocks and bonds and heavy cash and short-term Treasuries. (The ETF allocation comprises short-duration Treasury bonds and floating rate Treasuries, with a lesser allocation to long-dated Treasuries. You can view our models in real-time at SimpleVisor.com)

As we add exposure, we continue to tighten up stop-loss levels, hedging our portfolios as needed and looking to rebalance the portfolio back to target weightings.

Until the market confirms the “bear market” is over, we continue to trade cautiously. We DO NOT have to be early for the next bull market. When it comes, there will be plenty of time to participate in it and grow capital successfully.

See you next week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates (Formerly 3-Minutes)

We have set up a separate channel JUST for our short daily market updates. Be sure and subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Stock Of The Week In Review

After posting Part 2 of our Dividends and Value series we received multiple emails requesting we do the same analysis but for all of the 63 Dividend Aristocrat stocks. To reiterate, Aristocrats have paid and increased their dividends every year for at least 25 consecutive years.

Like we do in Part Two, we rank the 63 Dividend Aristocrat stocks on Dividend Yield, P/E, P/S, and Free Cash Flow Yield. The rank for each of the three valuations is twofold. The first ranking is outright. For instance, the stock with the lowest P/E will rank first, and so on. The second ranking is statistically based. We determine where each valuation is versus its 10-year range. For example, Williams Sonoma (WSM), a stock we highlighted in Part 2, has a P/E of 7.08. Its minimum and maximum for the last ten years is 7.08 and 25.69. WSM is at the bottom end of the range. WSM’s P/E is -2.10 standard deviations below its mean and ranks first in this category.

Here is a link to the full SimpleVisor Article For Step-By-Step Screening Instructions.

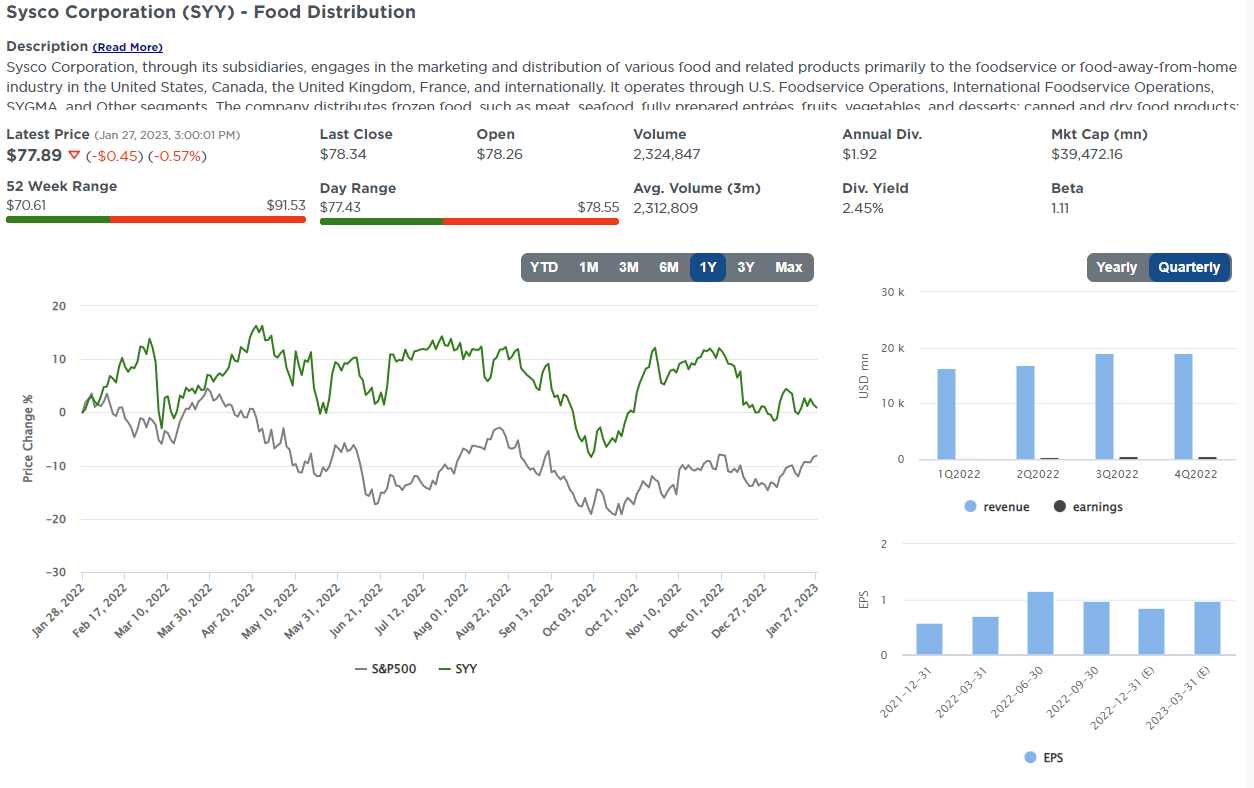

Here is one of the companies we screened.

Sysco Corporation (SYY)

Login to Simplevisor.com to read the full 5-For-Friday report.

Daily Commentary Tidbits

Is ChatGPT Good For Microsoft?

We asked Chat GPT, the new artificial intelligence (AI) engine, that exact question. The answer follows below:

Chat GPT is a good way to improve Microsoft’s earnings because it allows users to communicate with each other directly, which can help improve customer service and product quality. Additionally, it can help Microsoft attract new customers and retain existing ones.

Chat GPT is a fantastic advance in AI that can be used for many businesses and individual applications. Don’t believe us? Click HERE and let Chat GPT write an essay, song lyrics, a Valentine’s Day poem, or even computer code. Earlier this month, Microsoft bought approximately a third of Chat GPT for $10 billion. Microsoft’s Bing web browser plans on introducing Chat GPT technology to the public in late March. Instead of providing links to keywords you search for, Bing may provide you directly with the information. Further, the Microsoft suite of Office products can easily become a platform for users to take advantage of Chat GPT functionality. The potential Chat GPT applications are immense, and the benefits will likely flow to Microsoft shareholders. As the graph shows, Bing has a lot of market share it can steal from Google.

Click Here To Read The Latest Daily Market Commentary (Subscribe For Pre-Market Email)

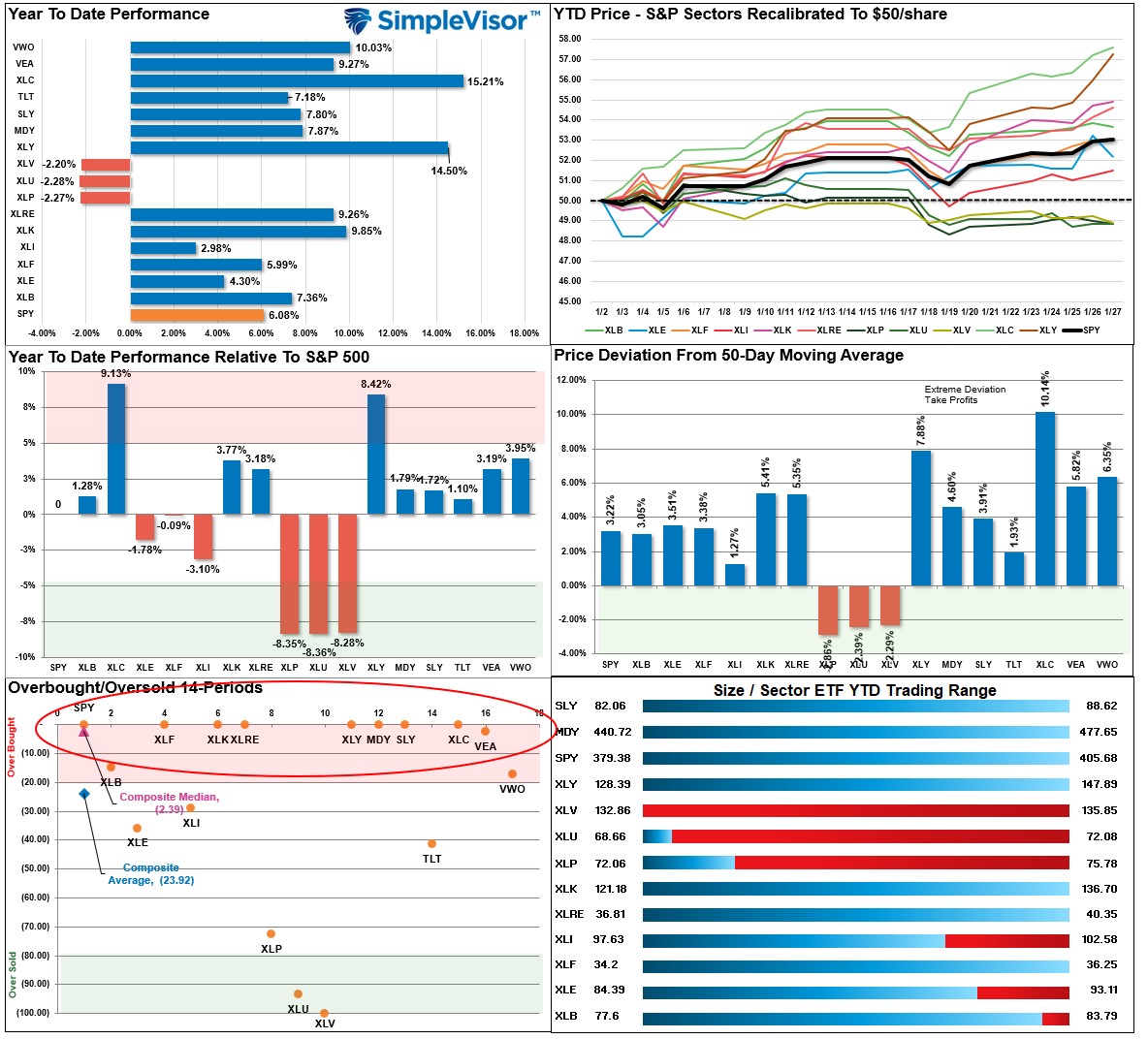

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

Broad Market Performance

Relative Performance Analysis

As noted last week: “The mid-week sell-off did not revert much of the overbought condition, and Communications, International, and Emerging Markets are well deviated above their moving averages.” The outperformance is beginning to wane, so look for a rotation towards laggards. Also, while still hated, technology has been improving technically. Staples, Healthcare, and Utilities are the most oversold due to the recent rise in bond yields. The massive surge in Communications and Discretionary in January, leaves these sectors ripe for profit taking.

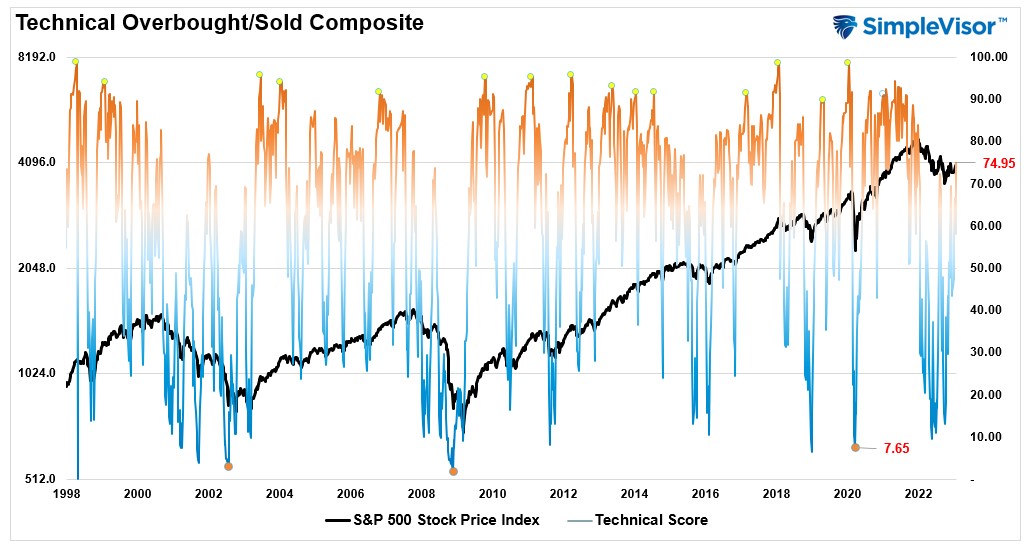

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. Markets tend to peak when those readings are at 80 or above, which suggests profit-taking and risk management are prudent. The best buying opportunities exist when those readings are 20 or below.

The current reading is 74.95 out of a possible 100 and rising. Remain long equities for now.

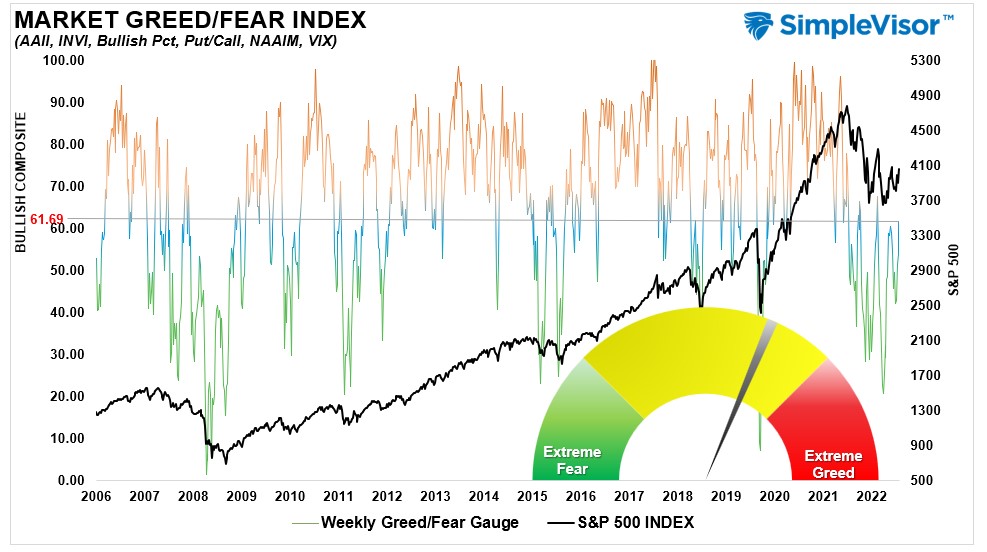

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” Gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 61.69 out of a possible 100.

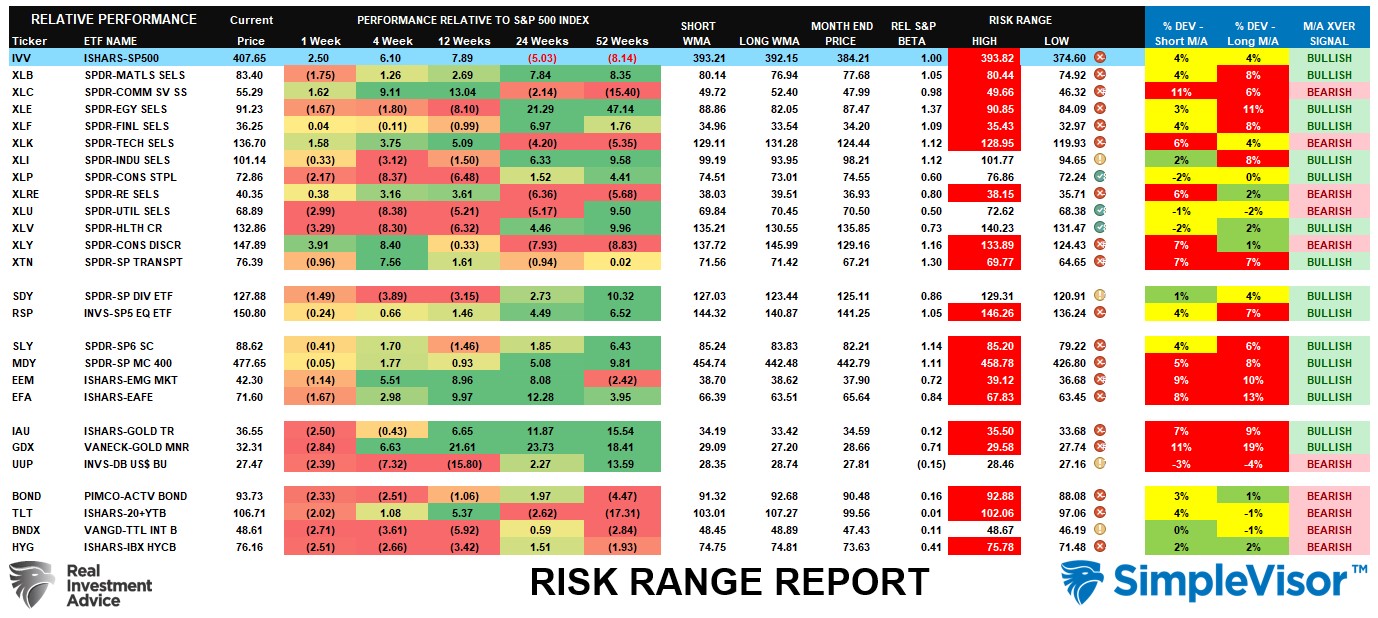

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M” XVER” “Moving Average Cross Over) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

As noted last week, “The sell-off came mid-week but regained most losses by Friday’s close. Despite the short-term volatility, the bullish backdrop remains with numerous sectors and markets back on intermediate-term weekly “buy signals.” Continue to look for pullbacks in areas where you want to add exposure and “buy dips” accordingly.

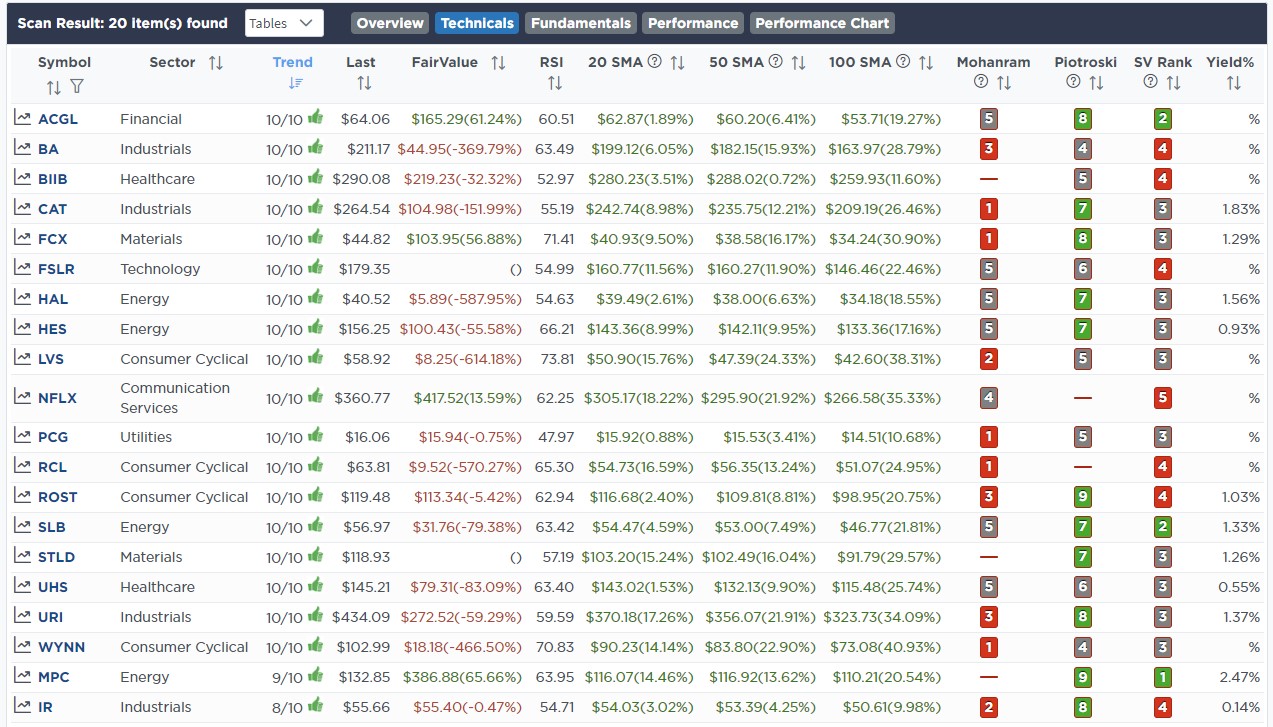

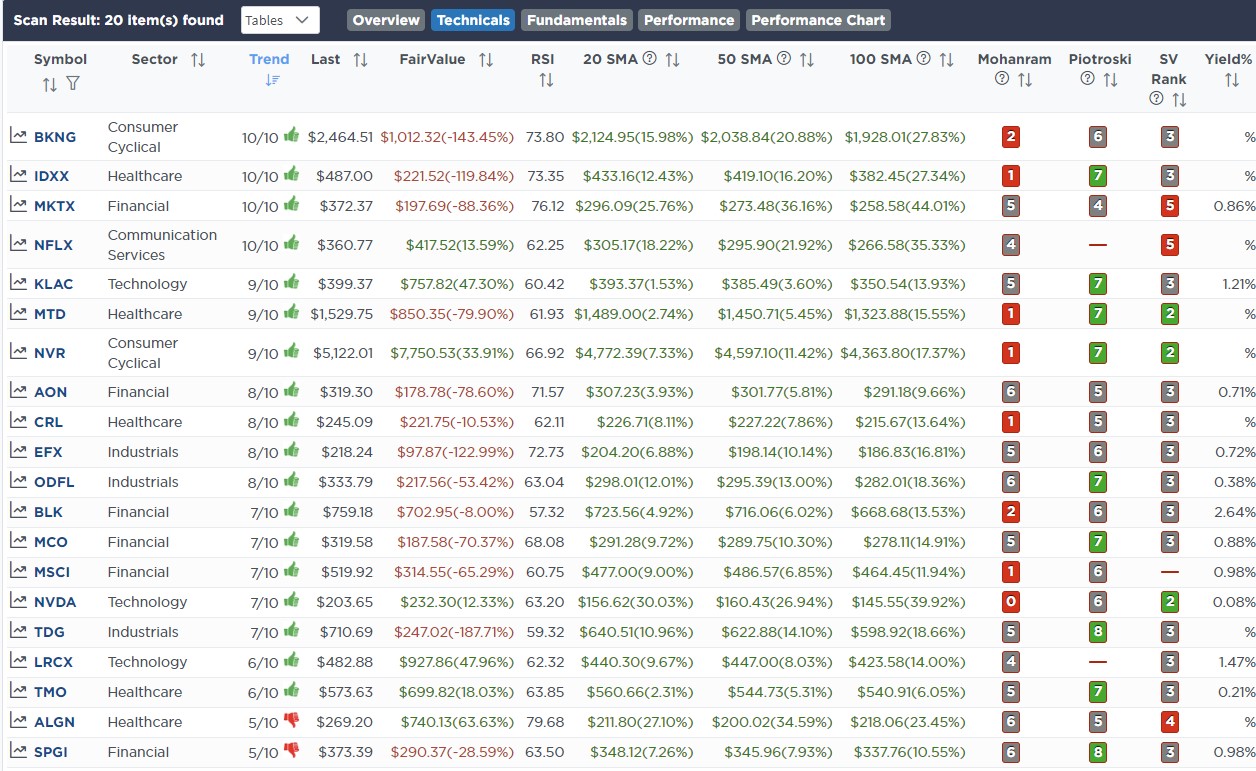

Weekly SimpleVisor Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Highest Rated Stocks With Dividends

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Highest Rated Stocks With Dividends

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

January 23rd

This morning we added two positions to our portfolio that continue to follow our theme of value and dividend. The first was Stanley Black & Decker (SWK), which trades at a 0.72 Price/Sales ratio and sports a dividend of 3.73%. In an economic slowdown, sales should be maintainable as home projects shift to DIY mode.

The second position is T. Rowe Price (TROW) which has a very annuitized stream of cash flows from fees charged for its mutual funds. TROW has no debt, a yield of 4%, and fee revenue will grow as the market begins to recover over the next 12-18 months. It also gives us more exposure to financials where we are currently underweight.

Equity Model

- Initiate a 1.5% position in Stanley Black & Decker (SWK)

- Buy a 1% position of T. Rowe Price (TROW) into the portfolio.

January 26th

As the market technicals continue to improve, we are cautiously adding some exposure to our S&P Equal Weight (RSP) trading position. At the same time, we are also nibbling at some value companies with high dividends and adding to stocks responding positively to poor earnings.

Such was the case with Microsoft (MSFT), which reported poor guidance, and the stock has rallied since, suggesting the bulk of the bad news is priced in. Furthermore, their investment into ChatGPT will likely be a game changer for the company, so we are adding to our current position after taking good profits from it last year.

Equity Model

- Buy 1% of the portfolio of Microsoft (MSFT) to increase the position.

- Add 2% of the portfolio to the S&P 500 Equal Weight ETF (RSP)

ETF Model

- Add 2% of the portfolio to the S&P 500 Equal Weight ETF (RSP)

Lance Roberts, CIO

Have a great week!