Rate Hike Starts Countdown To Next Recession

In this 03-18-22 issue of “Rate Hike Starts Countdown To Next Recession.”

- Market Review & Update

- Fed Rate Hike Starts Recession Clock

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Weekly Market Recap With Adam Taggart

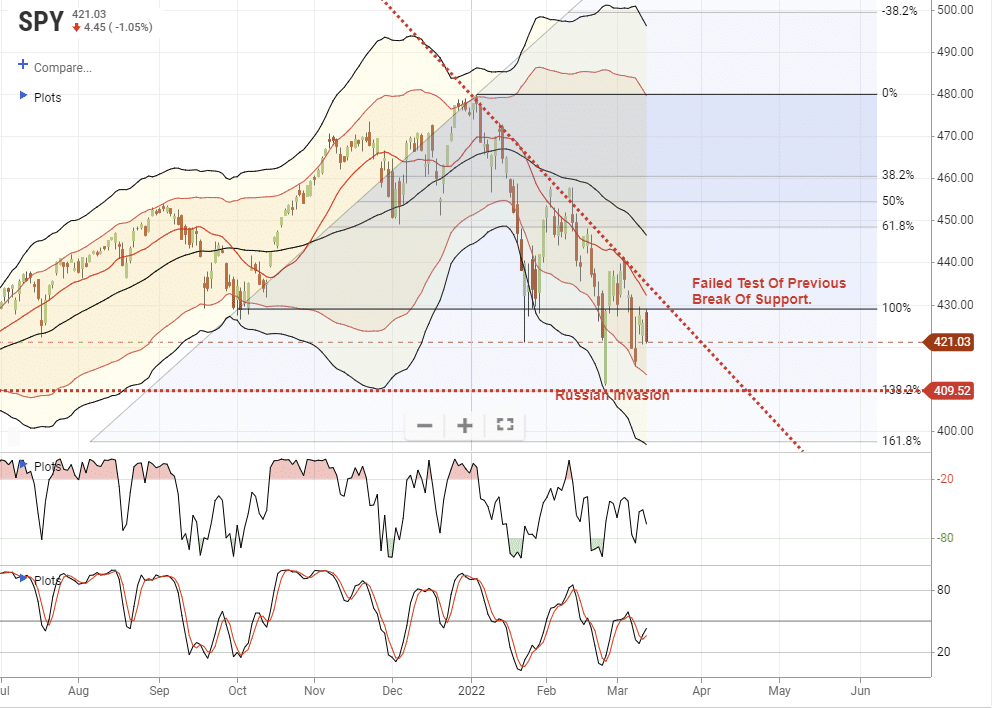

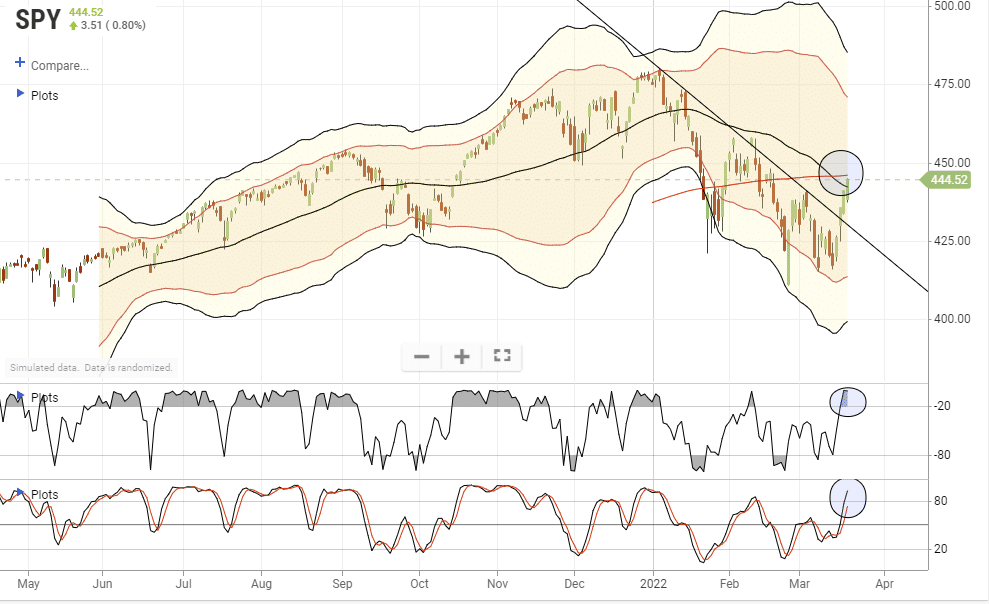

Stocks Rally As Fed Hikes Rates

What a difference a week can make. As discussed last week, the market slid and broke support as the Russia/Ukraine conflict continued.

However, this week was very different as the FOMC meeting went off largely as expected. The Fed hiked rates by 0.25% and maintained its more “dovish” tones during the presser. We previously stated that any rally above the downtrend would test the 50- and 200-dma averages. That test occurred on Friday, with the index clearing the 50- and sitting just below the 200-dma. With markets back to short-term overbought, it may be challenging for markets to clear resistance next week.

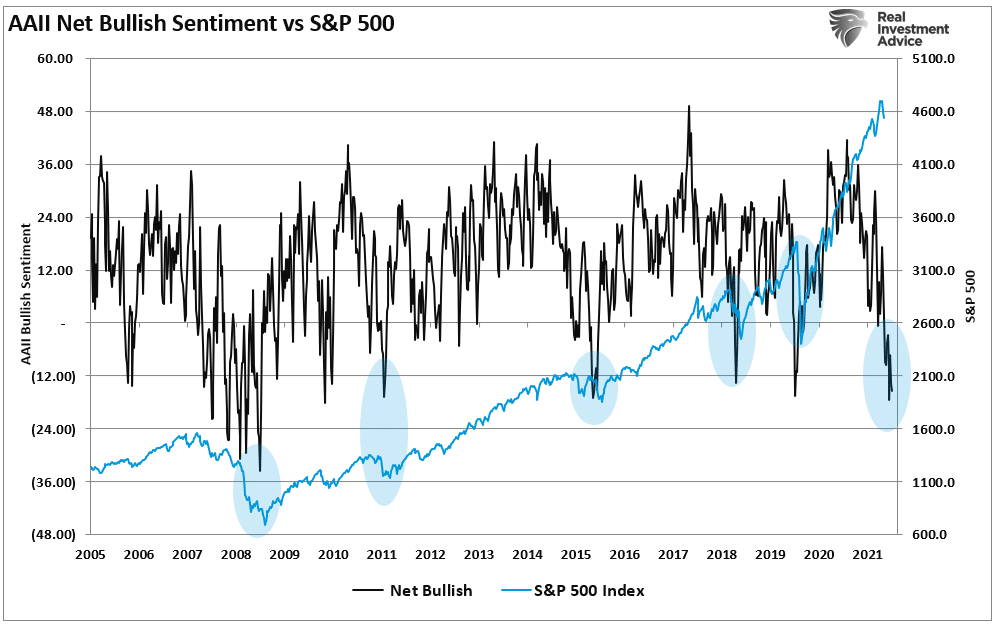

On the bullish side, investor sentiment and positioning remain negative. While the rally did reverse some negativity, it still provides “fuel” for a rally through the end of the month.

Several things currently suggest a follow-through rally is possible, encouraging the “bulls” to declare the “bottom is in.”

- Extremely negative investor sentiment.

- High cash levels

- Low equity positioning by fund managers.

- Equity fund flows are strong.

- Stock buybacks remain strong

But other issues suggest this rally may be limited to the upside, keeping this a more tradeable rally.

- Liquidity that drove the rally from the 2020 lows is reversing.

- The Fed is hiking interest rates

- Inflation is hot

- Earnings will slow along with economic growth.

- There are a lot of “trapped longs” that need an exit.

That negative sentiment is very constructive for a relatively strong counter-trend rally that will likely surprise the bears. But it could also be a set-up to trap the bulls later this year as we potentially face a “policy mistake.”

That brings us to the Fed.

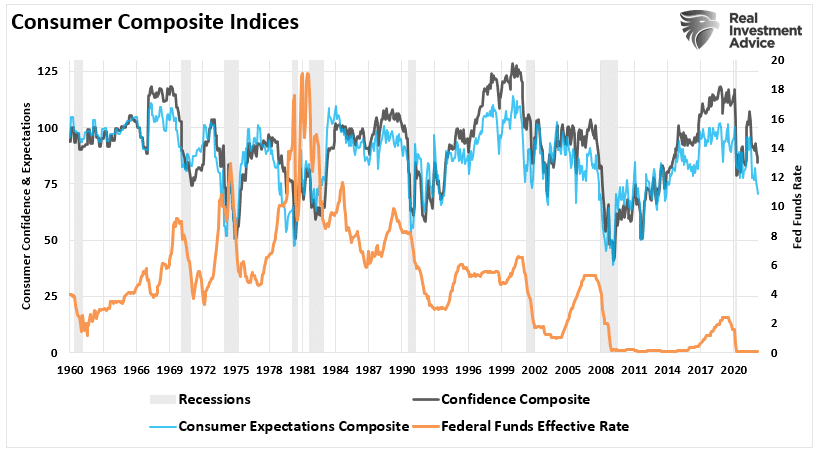

Fed Rate Hike Starts Recession Countdown

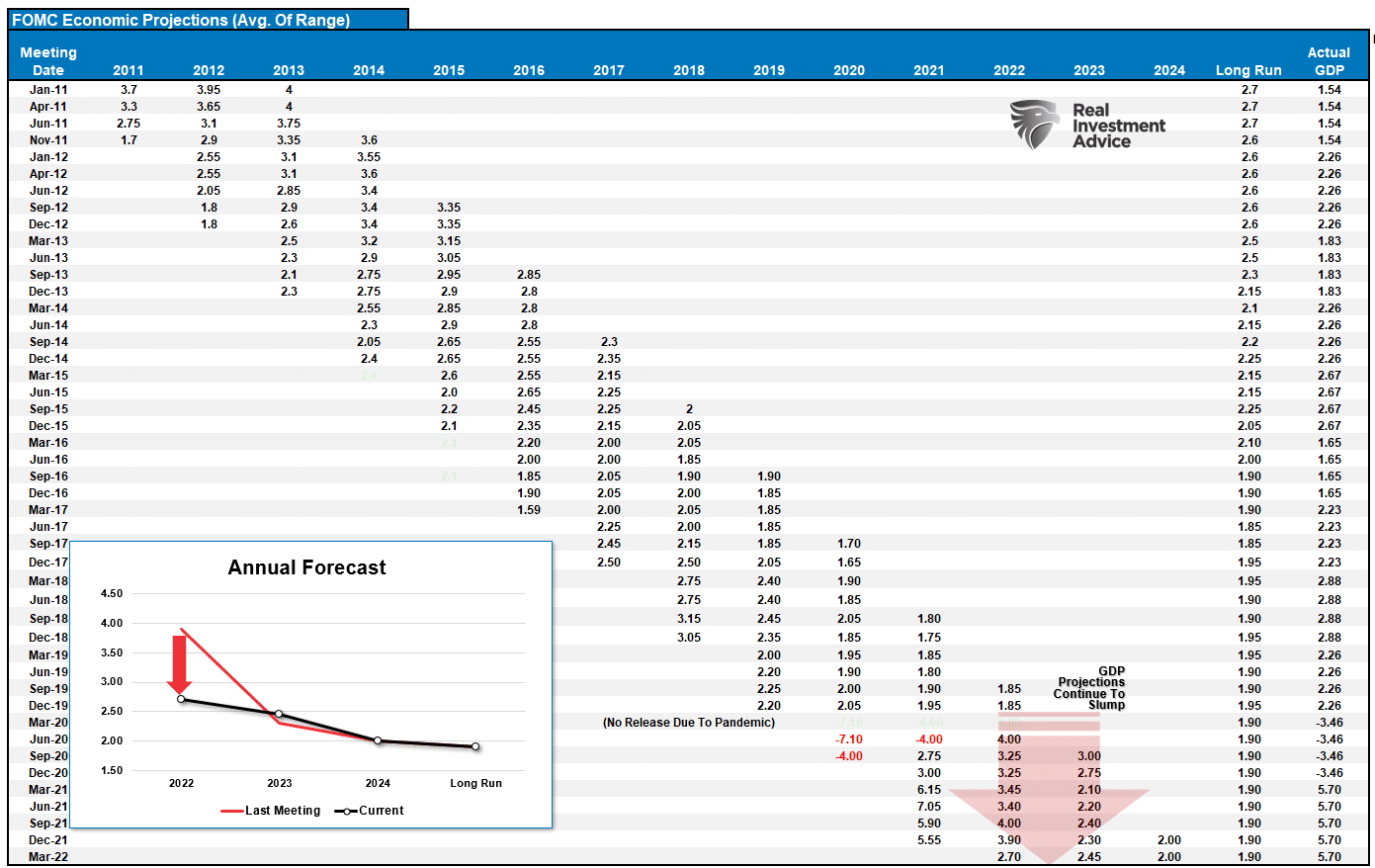

On Wednesday, the Federal Reserve took its first step in tightening monetary policy by hiking the overnight lending rate by 0.25%. According to its “dot plot,” they currently expect to hike rates at every meeting for the rest of 2022. At the same time, the Fed lowered its projections for economic growth while increasing inflation.

Such is not surprising for the “World’s Worst Economic Forecasters.” The Fed is always overly optimistic in its forecasts, as shown below.

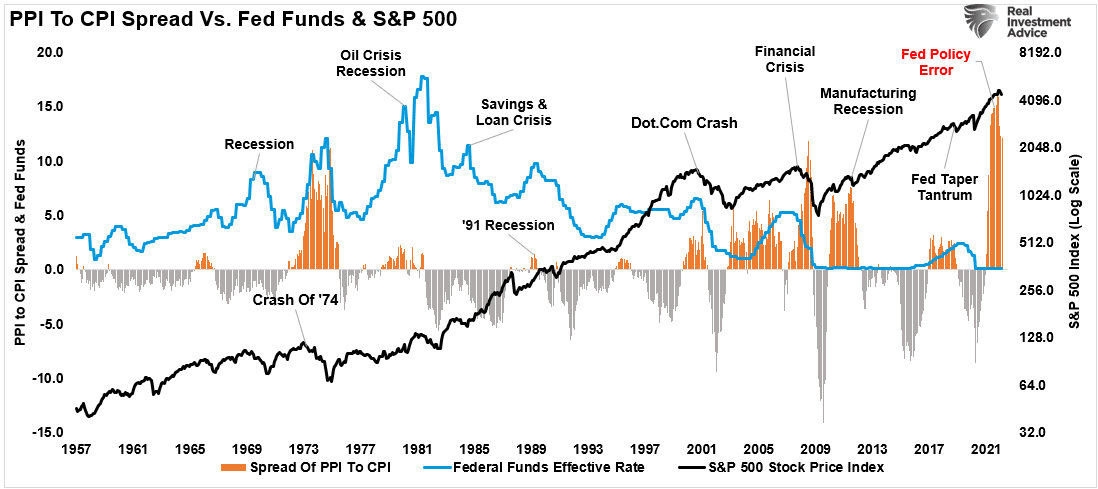

However, the Fed had no option but to hike rates with consumer inflation running at nearly 8% annualized and producer inflation at 10%. As discussed previously, the spread between consumer and producer inflation is the largest on record.

Such suggests that corporations cannot “pass-through” the entirety of the input cost increase. Eventually, inflation will erode profit margins leading to layoffs, automation, and other actions to reduce overall costs. Simultaneously, the consumer will retrench spending as real wages fail to keep up with higher living costs.

As shown, during previous periods where the inflation spread was positive, and the Fed was hiking rates, such preceded either a recession, bear market, or a crisis.

This Week’s MacroView

The Clock Just Started To Tick

In August 2021, I discussed the “3-Things That Will Warn Of The Next Recession.” They are:

- Fed balance sheet tapering

- Yield curve inversion

- Fed hiking rates.

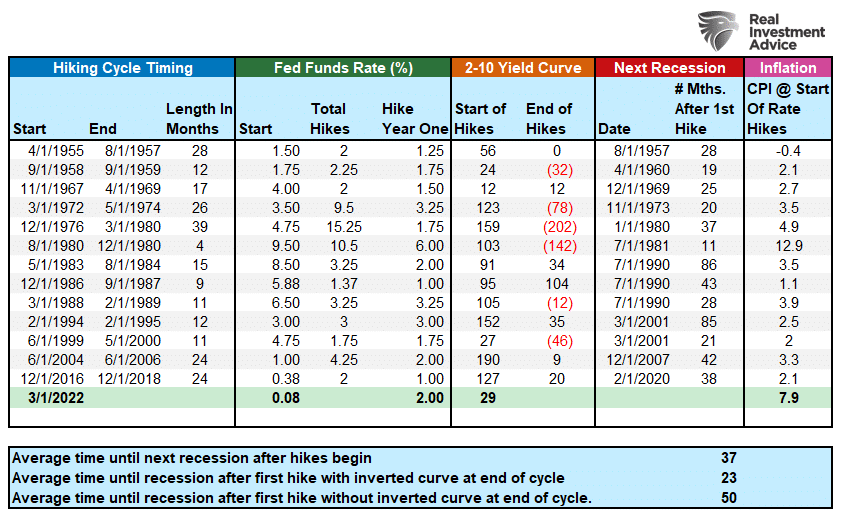

With the recent Fed rate hike, the clock has started ticking. There is no previous period where Fed rate hikes did not lead to a crisis, recession, or bear market.

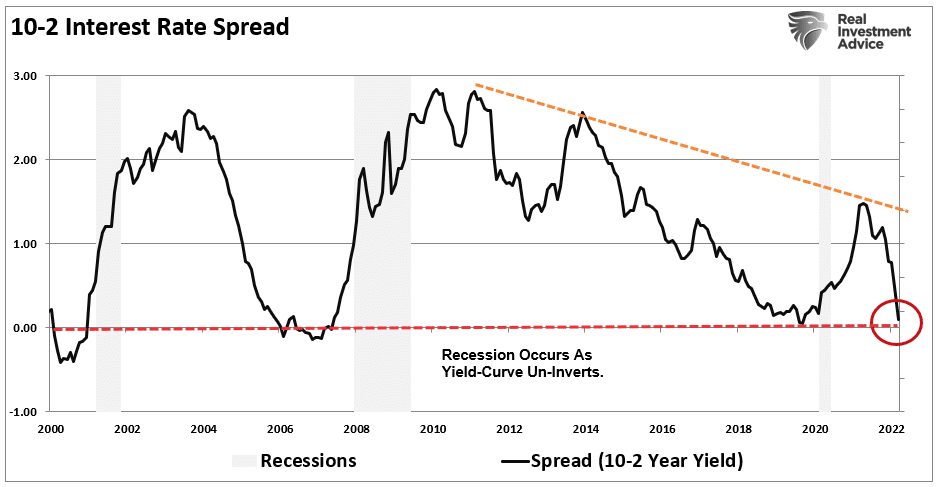

However, the most accurate of the 3-indicators of a recession is an “inversion” of the yield curve. As noted in Potemkin Economy:

“The most significant risk is the Fed becoming aggressive with tightening monetary policy to the point something breaks. That concern will manifest itself as a disinflationary impulse that pushes the economy towards a recession. The yield curve may be telling us this already.”

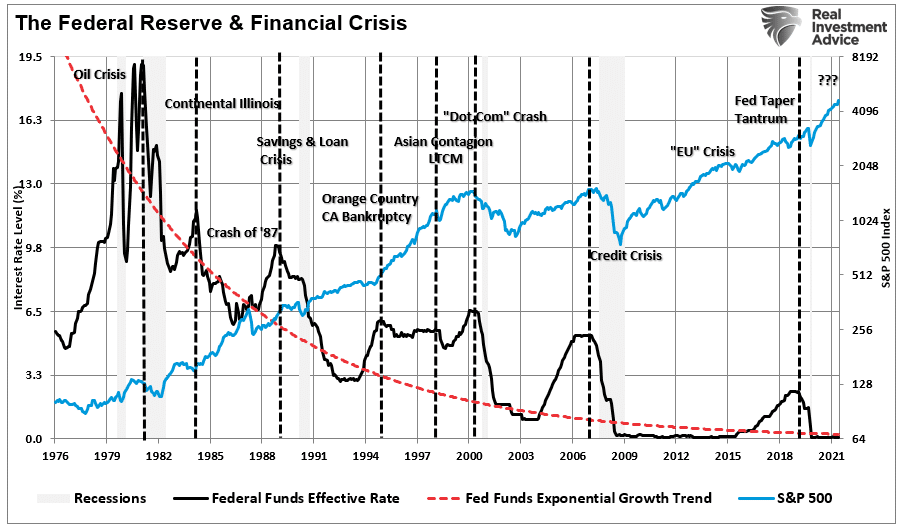

The yield curve suggests the economy is rapidly weakening, and the Fed may be “behind the curve” on rate hikes. Notably, rate hikes get used to slow economic growth by raising borrowing costs and reducing economic demand. However, surging inflation, rising Treasury rates, and a contraction in consumer liquidity have significantly tightened liquidity already. Such leaves the Fed a lot less “wiggle room.”

The Fed has little room for error between an inverting yield curve, declining consumer confidence, and increasing geopolitical risk. While they try to hike rates, we suspect they will wind up “breaking something.”

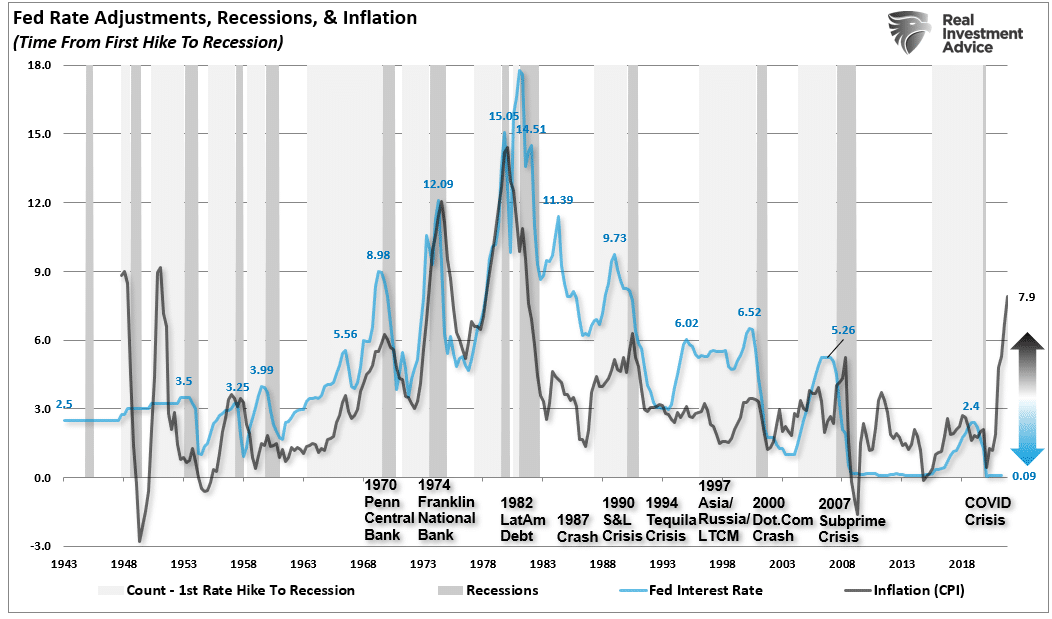

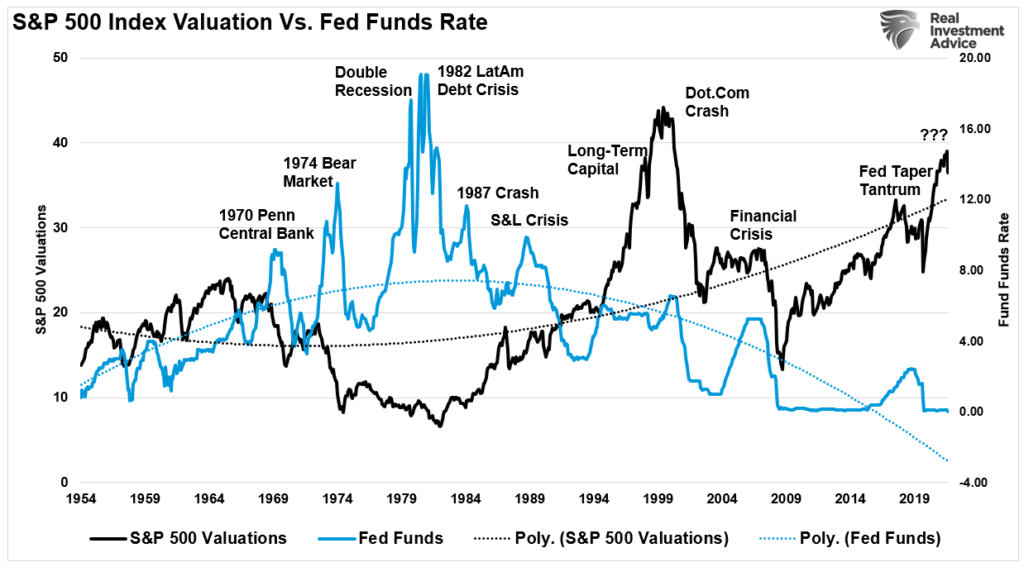

Fed Hikes And Peak Valuations

There is one very critical difference in this rate hiking cycle. Since 1980, each time the Fed hiked rates, inflation remained “well contained.” As noted below, the Fed is now hiking rates with inflation running at nearly 8%.

Such brings us to three essential points.

- The Fed tends to hike rates along with inflation, to the point it “breaks something” in the market.

- For the majority of the last 30-years the Fed has operated with inflation averaging well below 3%.

- The current spread between inflation and the Fed funds rate is the largest on record.

Notably, many of the previous crisis points were credit-related. With debt and leverage near historic high levels, increasing interest rates inevitably causes a problem.

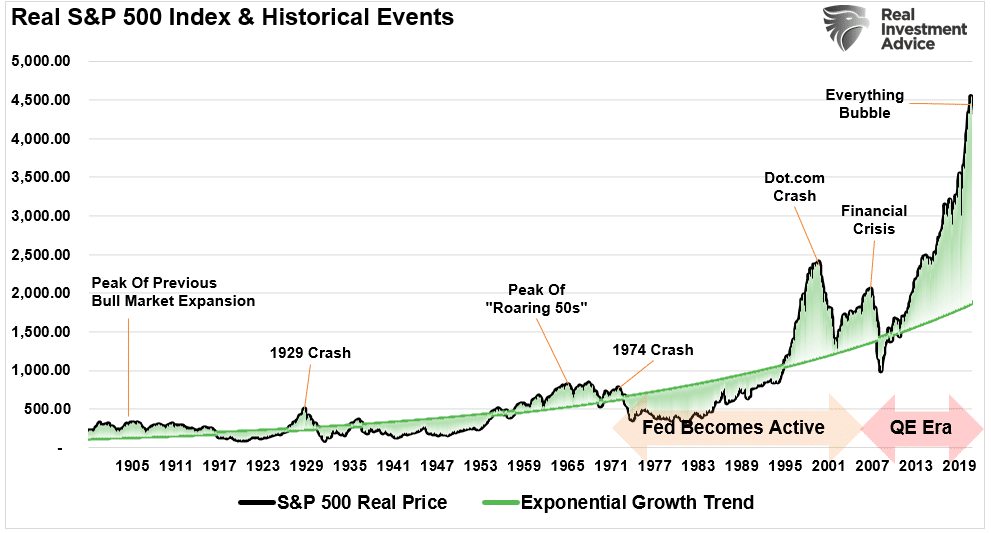

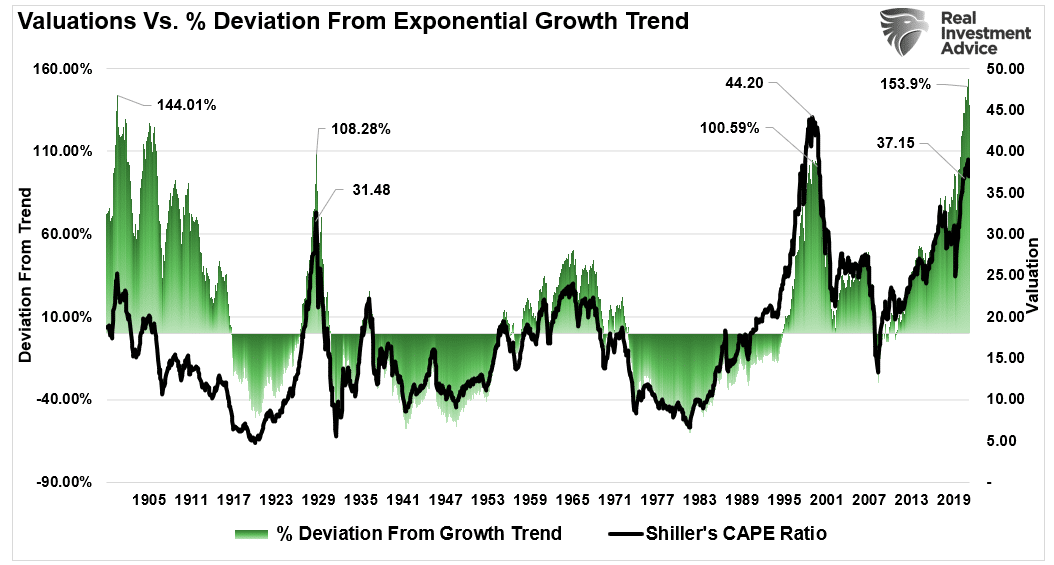

Lastly, the Fed is hiking rates with the financial market’s deviated from long-term growth trends.

Over the last 12-years, the pace of price increases accelerated due to massive fiscal and monetary interventions, extremely low borrowing costs, and unrelenting “corporate buybacks.” As shown, the deviation from the exponential growth trend is so extreme it dwarfs the “dot.com” era bubble.

The massive flood of liquidity from the Government, the Fed’s zero-interest-rate policy, and $120 billion in QE created inflation in consumer prices and financial assets. Currently, market valuations are more extended than at any other point in history other than the “Dot.com” bubble. We can realign the data above with valuations.

History shows that previous rate hiking cycles, particularly with elevated valuation levels in 1972, 1999, and 2007, led to poor outcomes.

Investors buy stocks on expectations of continued economic and earnings growth. As the Fed hikes rates to slow economic growth, such will lead to a reversal in earnings.

Notably, an earnings recession will be coincident with an economic recession.

Portfolio Update

I have an upcoming article on how investing is like gardening. As noted above, with market sentiment very negative, the counter-trend rally is not surprising.

However, we must still deal with the mounting risk of a reversal of monetary policy, weaker economic growth, and higher inflation. Therefore, to have a bountiful garden, we must:

- Prepare the soil (accumulate enough cash to build a properly diversified allocation)

- Plant according to the season (build the allocation based on the current market cycle.)

- Water and fertilize (add cash regularly to the portfolio for buying opportunities)

- Weed (sell loser and laggards, weeds will eventually “choke” off the other plants)

- Harvest (take profits regularly otherwise “the bounty rots on the vine”)

- Plant again according to the season (add new investments at the right time)

Like all things in life, everything has a “season” and a “cycle.” When it comes to markets, seasons get dictated by “technical constructs,” and “cycles” get dictated by “valuations.”

Therefore, we can “tend our garden” to prepare for a potentially harsher climate.

The Portfolio Process

Step 1) Clean Up Your Portfolio

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Step 2) Compare Your Portfolio Allocation To The Model Allocation.

- Determine areas requiring new or increased exposure.

- Calculate how many shares need to be purchased to fill allocation requirements.

- Determine cash requirements to make purchases.

- Re-examine portfolio to rebalance and raise sufficient cash for requirements.

- Determine entry price levels for each new position.

- Evaluate “stop-loss” levels for each position.

- Establish “sell/profit taking” levels for each position.

Step 3) Have positions ready to execute accordingly, given the proper market set-up. In this case, we are looking for positions with either a “value” tilt or “strong earnings growers” sitting on support with a lower-risk entry opportunity.

This past week, we reduced our overbought energy positions and added to our core technology holdings as part of the “tending process.” With target portfolio exposures down, and cash holdings up, we can withstand some harsh weather while looking for investible opportunities.

There are TWO specific benefits to our actions.

- If the market corrects further, these actions clear out the “weeds” and allow for protection of capital against a subsequent decline.

- If the market continues to rally, then the portfolio is ready for new positions that can participate in the next leg of the advance.

No one knows where markets are headed in the next week, much less the next month, quarter, year, or five years. However, we know that not managing “risk” to hedge against a decline is most detrimental to the achievement of long-term investment goals.

I hope this helps.

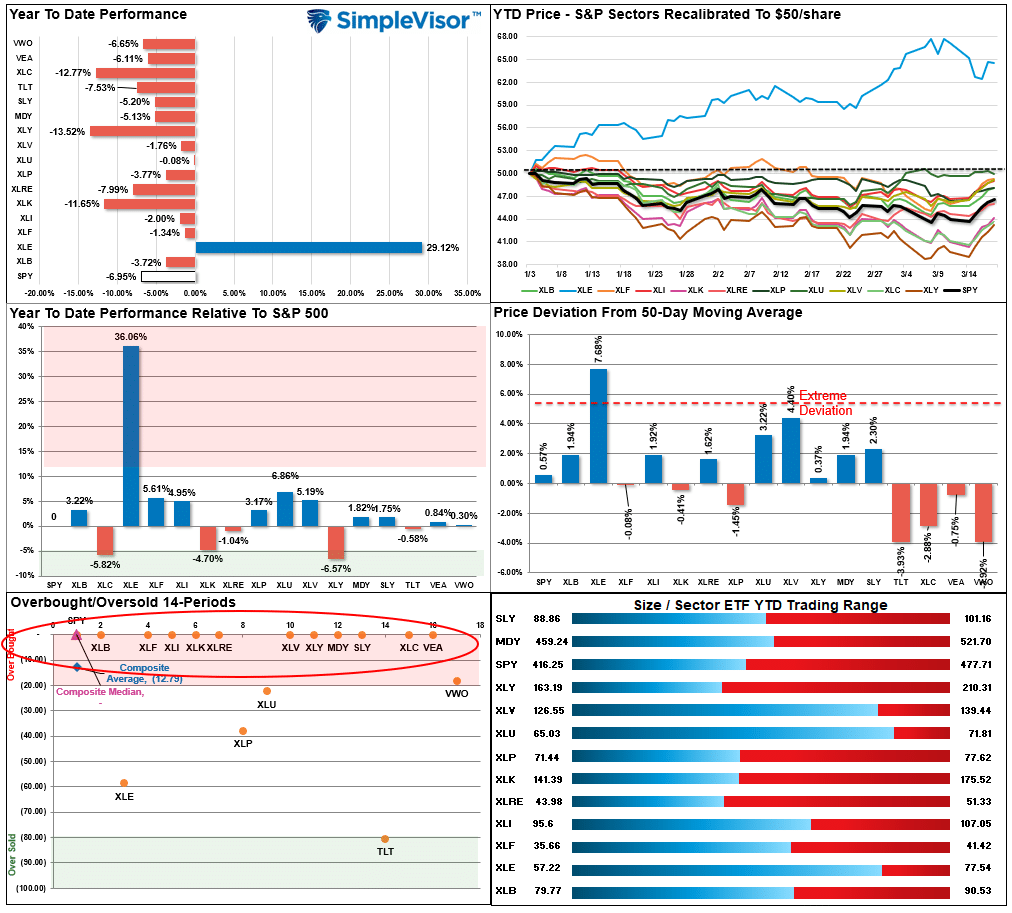

Market & Sector Analysis

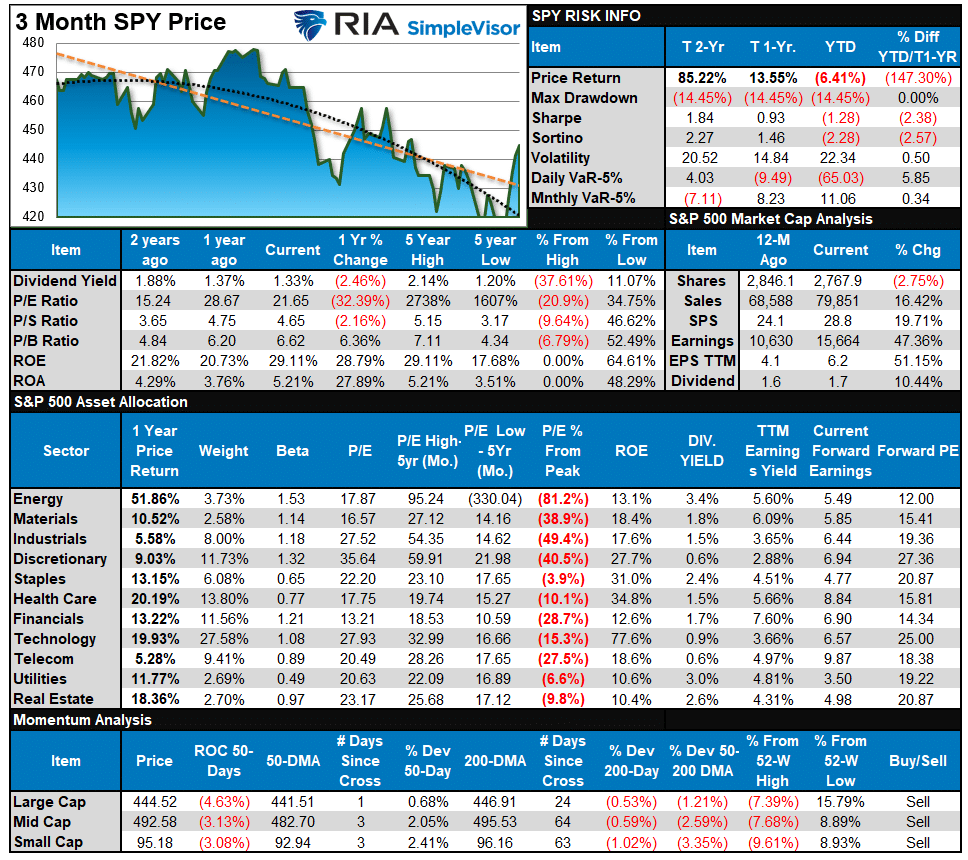

S&P 500 Tear Sheet

Relative Performance Analysis

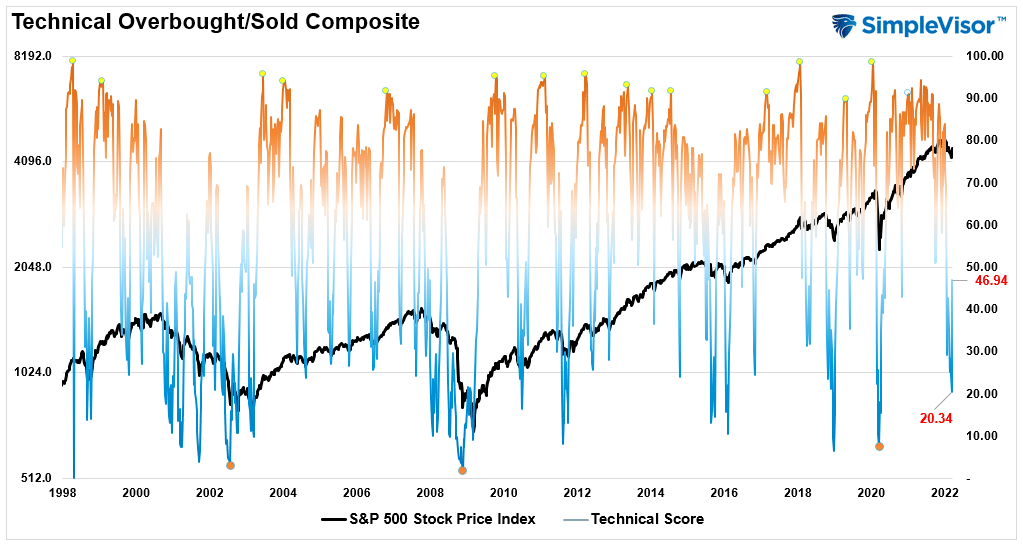

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 46.94 out of a possible 100.

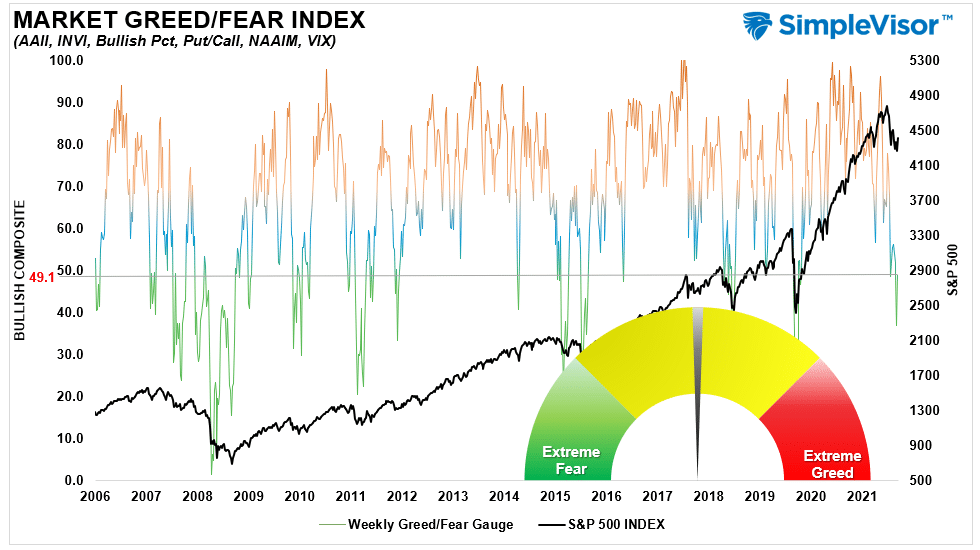

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 49.05 out of a possible 100.

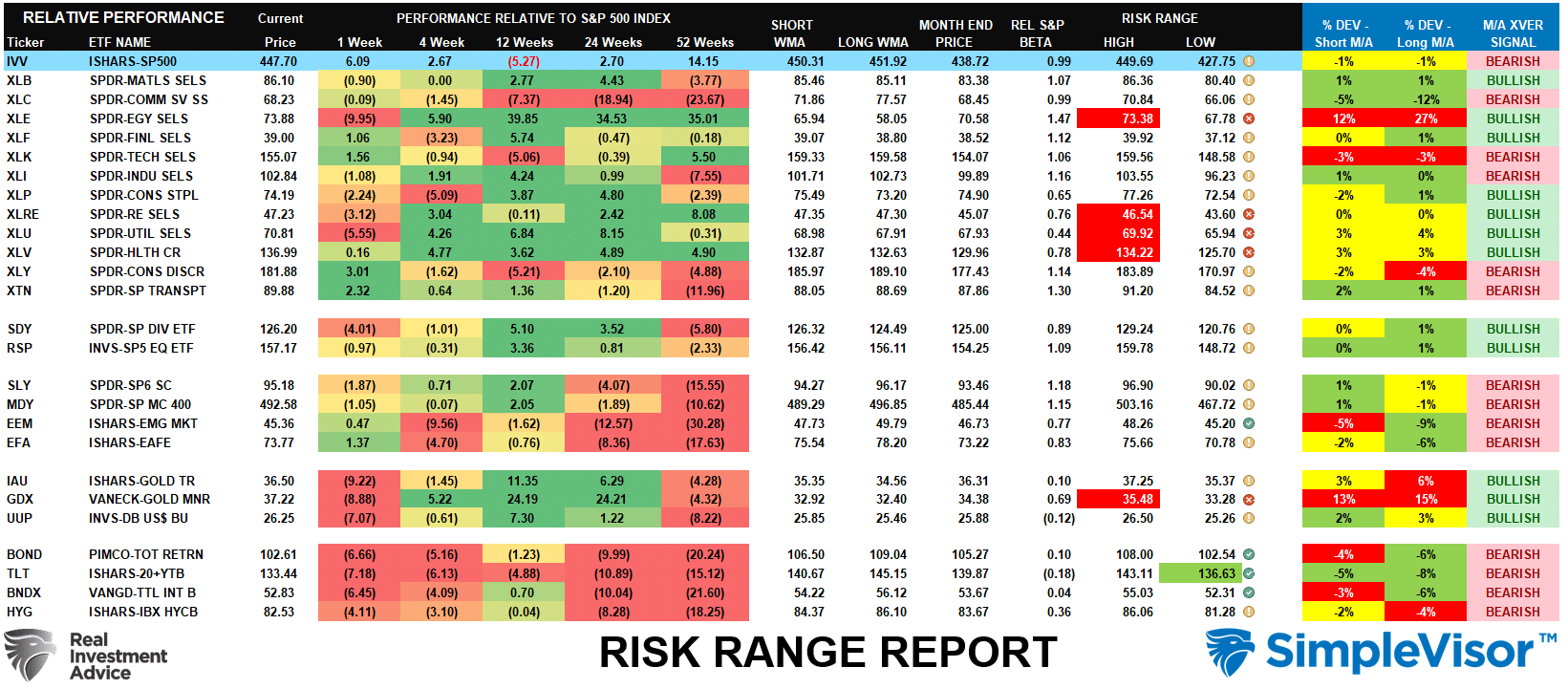

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is on under the Dashboard/Sentiment tab at SimpleVisor

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

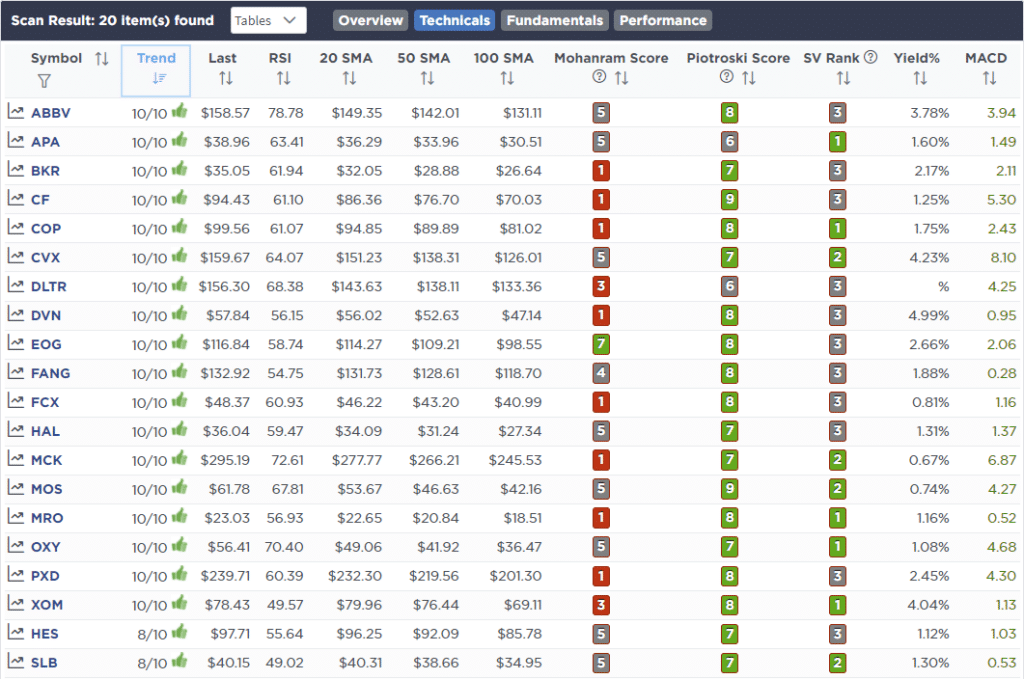

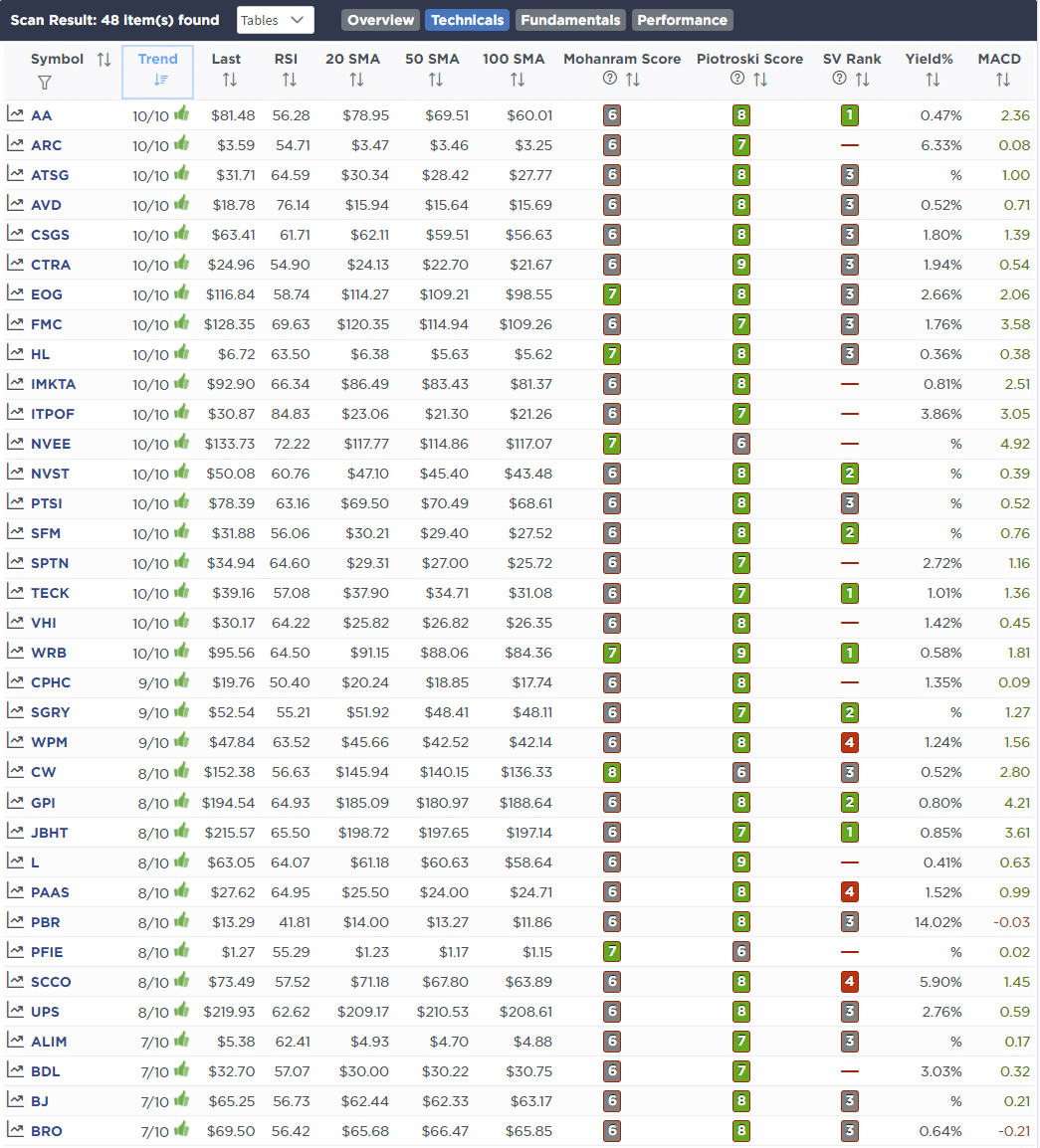

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

March 14th

For the second time this year, we are rebalancing our energy holdings back to model weights at the market open this morning.

Energy stocks are grossly overbought and the price of oil is way above fundamental demand levels. That demand will worsen as a recession sets in this year, leading to a reversion in energy prices. We are taking profits now and will look to reduce holding sizes as needed later this year.

Equity Model

- Reduce Exxon Mobil (XOM) to 2% of the portfolio.

- Reduce Marathon Oil (MRO) to 1.5% of the portfolio.

ETF Model

- Reduce SPDR Energy ETF (XLE) to 3% of the portfolio.

March 15th

With prices down in our long-term core portfolio holdings, along with the deeply depressed sentiment and investor allocations, we are using some of the stored cash to rebalance those positions back to market weight. As noted previously, we are looking for a short-term counter-trend reflexive rally, that we will again rebalance portfolio risks into. However, adding to our core positions, and bringing holdings back to weight, allows us the opportunity to take advantage of depressed prices.

Equity Model

- Increasing Ford (F) from 2% to 3% of the portfolio.

- Adding 0.5% to AMD (AMD) and Nvidia (NVDA)

- Rebalancing Microsoft (MSFT) and Apple (AAPL) to model weights of 3% each.

ETF Model

- Increasing SPDR Technology ETF (XLK) by 2% of the portfolio.

March 18th

We are adding to our position in Proctor & Gamble (PG) today after its recent pullback to support. We are increasing our position size from 2% to 2.5% of the portfolio. Also, after adding to the growth side of our portfolio, we are adding a bit to our value holdings. We are not convinced the market bottom is in, so we are nibbling on opportunities slowly. Sentiment remains VERY depressed and after options expiration today, we will have a better handle on the next potential move.

Equity Model

- Increase PG by 0.5% of the portfolio.

Lance Roberts, CIO

Have a great week!