Technically Speaking There Are Some Bullish Signs

In this 07-22-22 issue of “Technically Speaking.”

- Market Trading Update

- Technically Speaking Bullish Signs Appear

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Weekly Market Recap With Adam Taggart

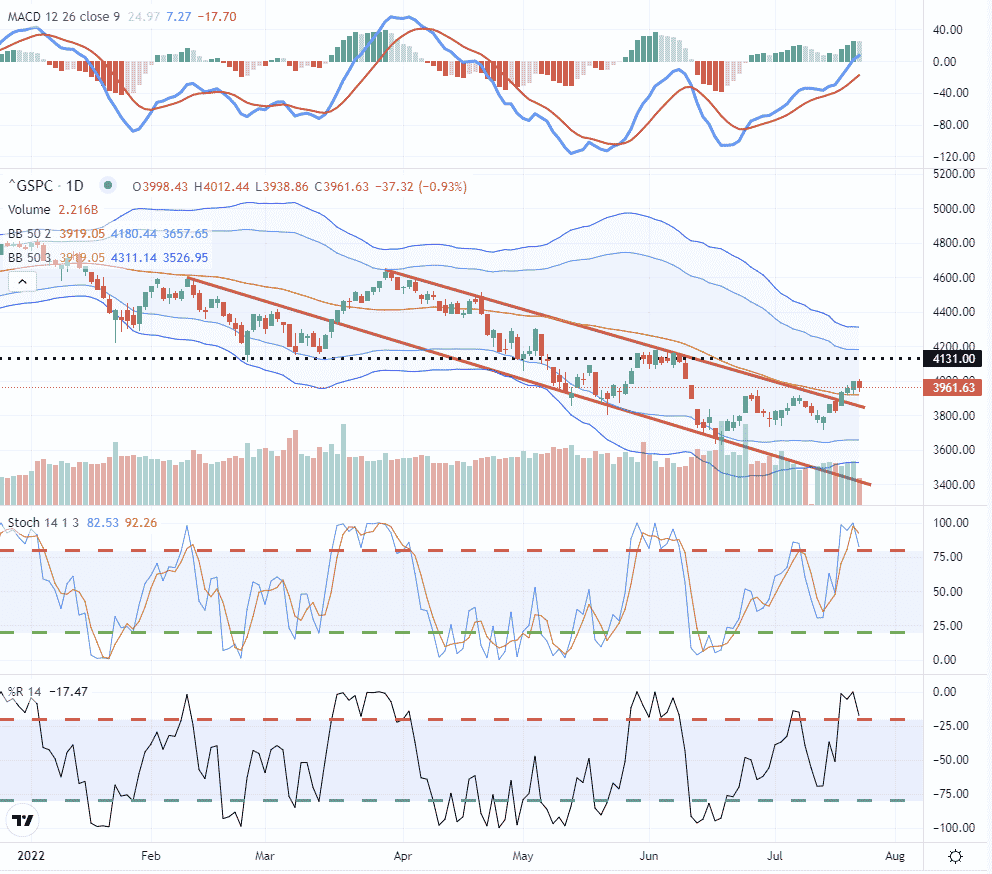

Market Trading Update

Over the last week, the market finally gained a decent rally. The break above the 50-dma and the declining trend channel gave the bulls the signal to jump back into stocks. While much of the rally was short-covering, the market did push into the upper resistance of the longer-term downtrend channel.

The sell-off on Friday was not surprising and could be bullish for the markets in the short term. With the markets very short-term overbought, a pullback to the 50-dma which holds would turn that previous resistance level into key support. If such occurs, without triggering a MACD sell signal, such could provide the setup for the bulls to rally the market a bit further.

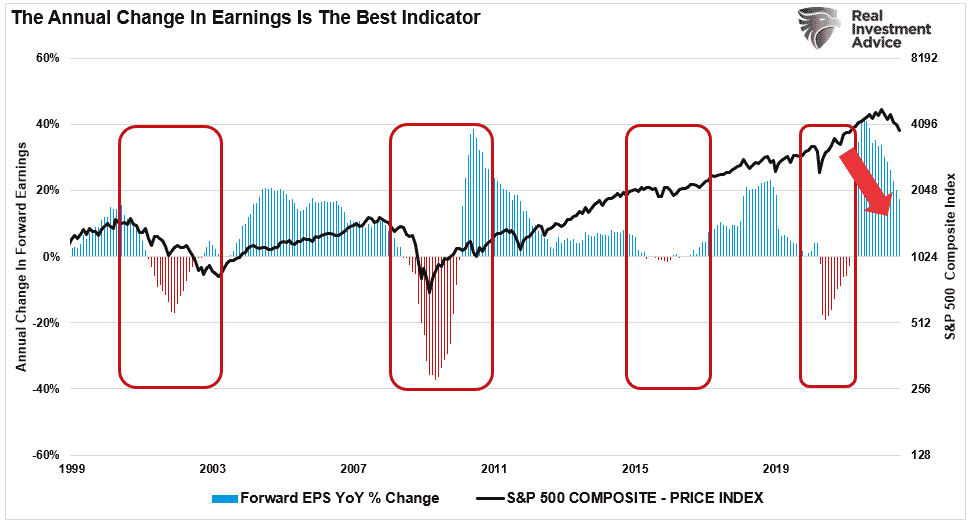

As we proceed through earnings season, which will pick go into high gear next week, the big issue short term is whether estimates and stock prices have fallen enough to account for slower growth. As shown below, forward estimates have fallen but remain at a positive growth rate. Historically, if the economy is indeed slowing, the growth rate tends to go negative.

As far as a recession is concerned, the single best recession indicator is the Leading Economic Index’s 6-month annual rate of change.

Whether or not a recession is imminent, the market tends to bottom before the economy. As such, could longer-term analysis be signaling a turning point is coming?

Technically Speaking Bullish Signs Appear

As noted, over the last couple of weeks, despite market volatility, the S&P 500 index has been forming a basing pattern with higher lows and a break above resistance. Technically speaking, as noted above, such suggests a rally to 4100-4200 is possible.

However, if we look at the market on a weekly basis, a very different picture emerges. Notably, despite the recent decline from record highs, the market remains in a rising bullish trend. In other words, despite much commentary suggesting we are in a bear market, technically, we remain in a correction.

Secondly, note that the moving average convergence divergence indicator or MACD (bottom panel) and the relative strength index or RSI (top panel) are at very oversold levels. Those levels previously coincided with market lows.

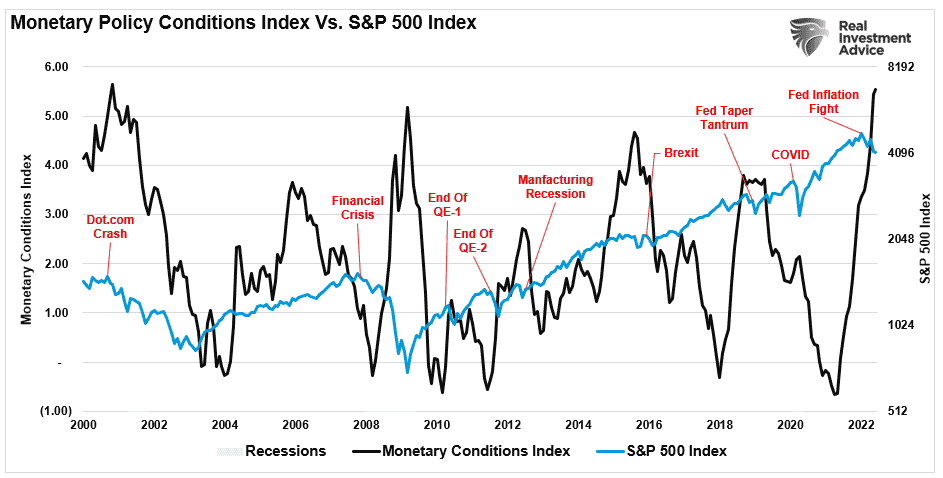

Notably, the massive liquidity-driven surge in 2020-2021 skewed the MACD signal to extremely high levels. Such was a clear warning the bullish move from the 2020 lows was not sustainable. Given the massive surge was driven by copious quantities of artificial stimulus, we should stay cautious of current oversold conditions. The reason is that even though the market is oversold, liquidity is reversing, the economy is slowing, and monetary policy is restrictive. The monetary policy chart below is a composite index of short and long-term rates, inflation, and the dollar. It suggests policy is already very restrictive and coincides with previous market events.

Monthly Signals Mixed

However, on a monthly basis, the market remains more neutral. Technically, the market held support at the critical 3-year moving average. A break of that “last line in the sand” would suggest a much deeper correction is possible. By holding that support, the bullish trend remains intact. As noted, such keeps the current market in an ongoing correction within the long-term bull market.

However, the monthly MACD (lower panel) remains on a sell signal, suggesting the market likely has more work to do before a lasting bottom is seen. Nonetheless, the market is deeply oversold (top panel), which suggests the current rally could continue with the 12-month moving average, a likely target at 4350.

However, with that said, there is one significant difference to consider.

MacroView

The Inflation Question

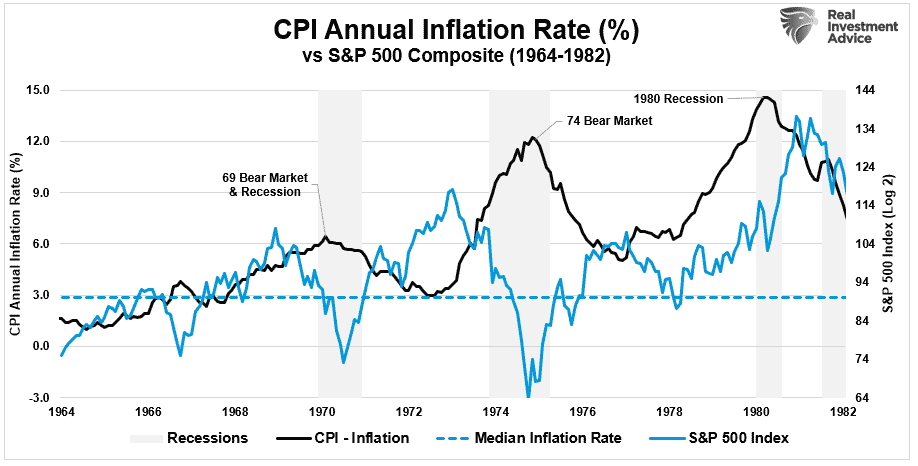

The one very important difference between the current market environment and any market in the last 40 years is inflation. To understand the impact of inflation on the market, we need to review the 1970s. Such is the only recent period in market history where inflation was high, and the Fed hiked interest rates to combat price pressures.

Not surprisingly, as inflation increased, markets tended to stumble, as in 1966-1967. Of course, sharper increases in inflation sparked recessions, leading to more significant corrections and bear markets as in 1970, 1973-1974, and 1980. Notably, the 1974 bear market pushed market valuations to roughly 7x earnings versus the roughly 28x valuations currently.

It is also worth noting in the chart above and below that stocks bounced from the deeply oversold MACD signal as inflation fell. That market rally, while strong, was cut short as inflation started to accelerate again. But as inflation rose into the early 80s, stocks, while volatile, did gain ground as a 5% dividend yield and low valuations attracted investment.

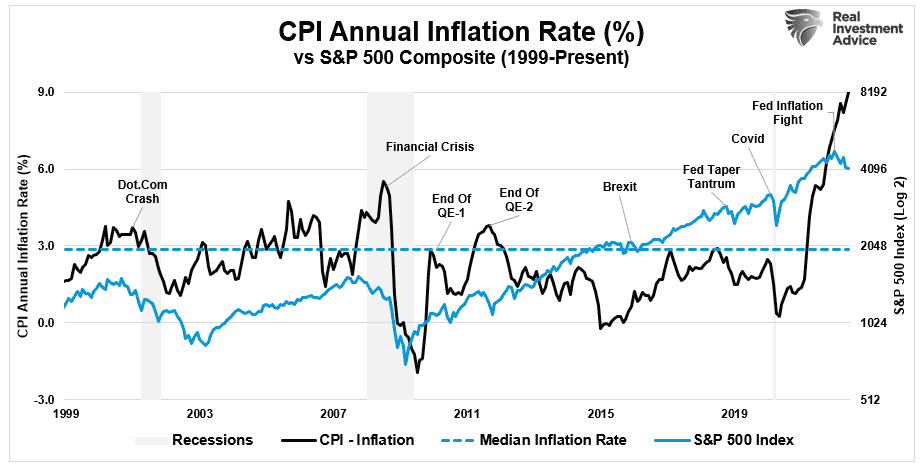

It is a very different story today, with inflation running at 9%, dividend yields below 2%, and valuations at historically high levels. Coincidentally, the Fed is remaining aggressive about hiking interest rates and reducing liquidity in the financial markets.

As Michael Lebowitz noted on Wednesday:

“Valuations help investors gauge the potential downside risk and upside potential in a stock or market. At the same time, assessing liquidity conditions, including technical analysis, and defining short-term trends help with investment timing and asset selection.

Current liquidity conditions dictate conservatism. The Fed is aggressively raising interest rates and reducing its balance sheet. Further, fiscal spending is falling well short of that in the prior two years. As a result, liquidity is exiting the financial markets, which augurs a bearish trend.

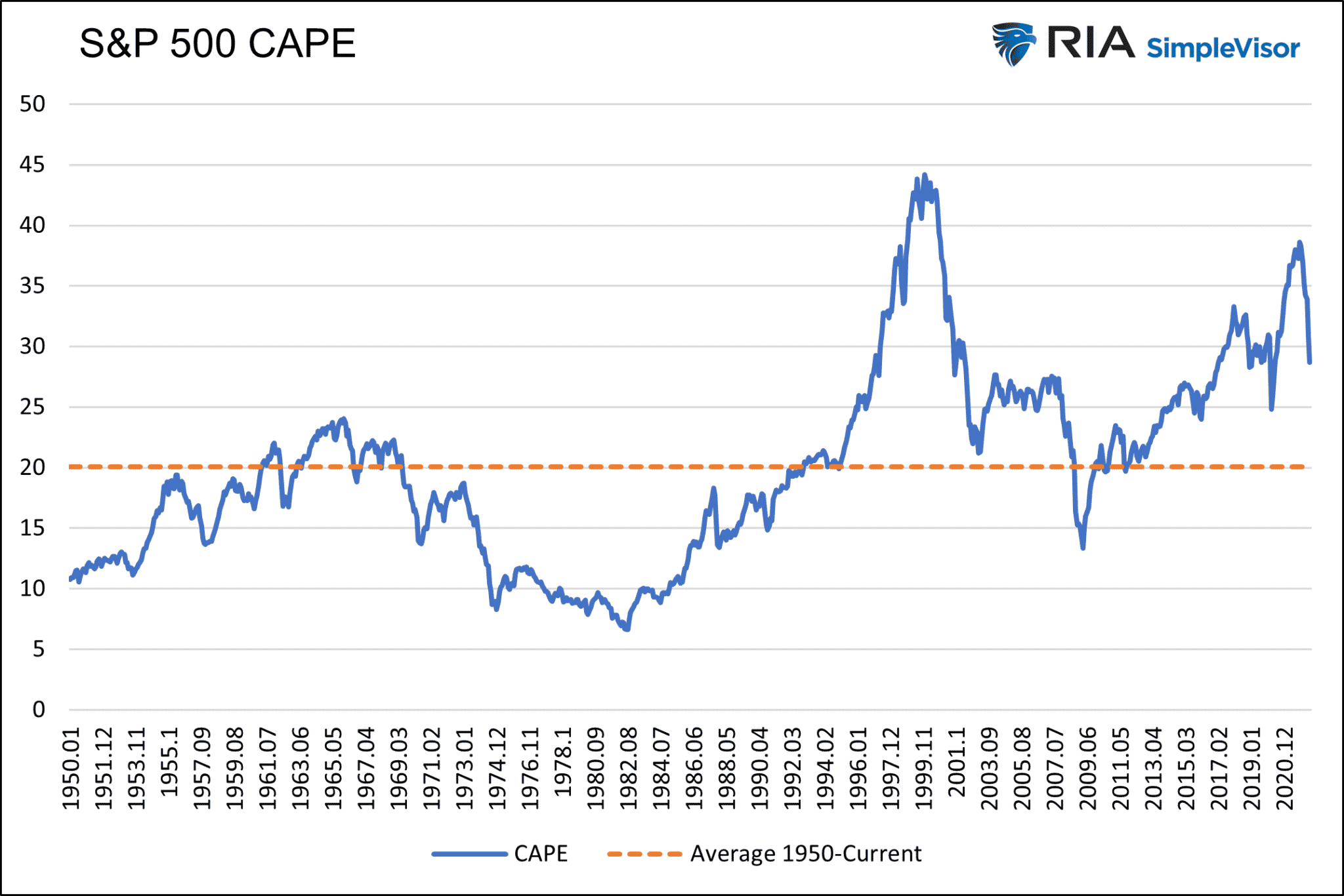

We are not fearmongering, but consider that CAPE fell to seven in the bear market and recession of 1981-1982. That was the last time with comparable inflation as today. Assuming no change in earnings, the S&P 500 would have to drop to 925 to reach a CAPE of 7!“

Technically Speaking, Is A Break Above The 50-DMA Bullish?

It is crucial to understand that while short-term conditions are indeed bullish biased at the moment, we are currently swimming in waters very few investors have ever witnessed. (45-year market veterans are a rarity today.) While we need to rely on our technical analysis for short-term market guidance, it is worth remaining cautious until longer-term signals confirm short-term trends.

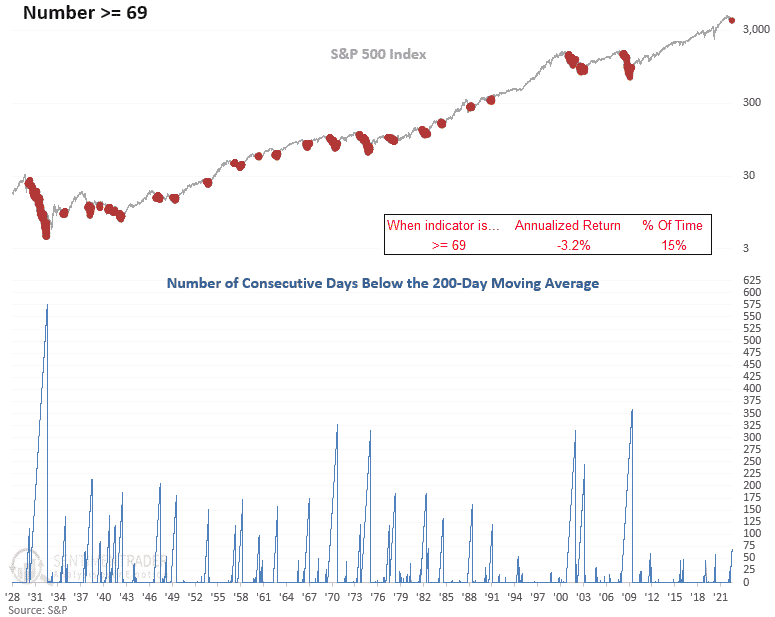

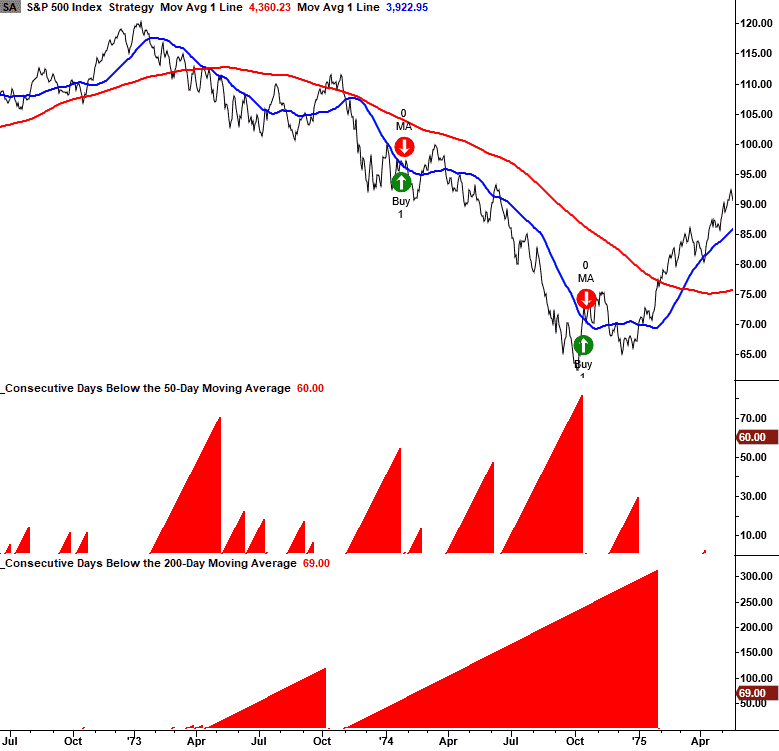

For example, while the market did indeed break above the 50-dma, as Sentiment Trader notes, such may not be as bullish of a signal as many think. To wit:

“For the first time since the global financial crisis, the S&P 500 traded below its 50-day average for 60 consecutive sessions. At the same time, the index is also trading well below its 200-day moving average for more than 69 days.”

There have been 36 times such an environment has occurred over the last 92 years. Following previous signals, S&P returns, win rates, and z-scores were unfavorable across most short and medium-term time frames. The market also had a negative return at some point in the first 2-months in 30 out of 35 instances.”

Since we are comparing the current market environment to the 1973-74 market, where inflation was present, the chart below shows repeated failed breaks above the 50-dma.

As Sentiment Trader concludes:

“When the S&P 500 closes above its 50-day moving average for the first time in 50 sessions or more, and the index is in a well-established long-term downtrend, we need to remember that the trend is not our friend. Similar setups to what we’re seeing now have preceded flat to negative stock returns across short and medium-term time frames.”

That is likely good advice as we operate in a more uncertain market environment. While there is undoubtedly a more bullish setup short-term and certainly tradeable, it could be just as fleeting as we have seen repeatedly this year.

It is better to err to the side of caution, for now, maintain risk controls, and let the market tell you when it is safe to “return to the water.”

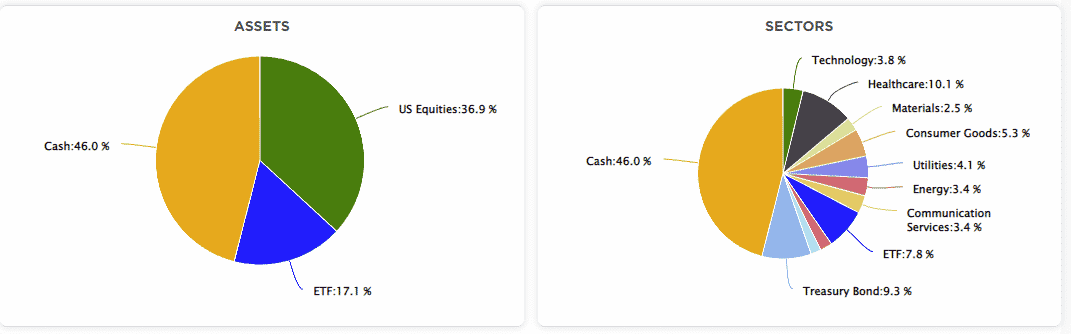

Portfolio Update

I want to reiterate the current market environment remains very challenging. On the one hand, sentiment remains extremely negative, portfolio managers are underweight equities, and corporate share buybacks are at record levels. From a contrarian view, such a setup is bullish and warrants adding stock exposure.

On the other hand, the Fed is tightening monetary policy, inflation is high, and the economy is weakening, which will weigh on corporate earnings and outlooks. From a fundamental view, a reduction of stock exposure is warranted.

I know. Confusing. However, such is why we remain cautious. We are observing markets carefully as we proceed through the earnings season. We are looking for companies that report earnings and their stock price rises regardless of the report. Such suggests a majority of the “bad news” is accounted for. We will look to start building small exposures and increase them as performance improves.

As noted, there are many reasons to remain cautious about the markets. However, we also need to be aware that markets will bottom before the Fed changes its course or a recession is complete. As such, while we continue to carry higher cash levels with a focus on risk management, we are also looking for early opportunities.

Remain cautious for now and continue following the rules from last week.

- Tighten stop-loss levels to where you are comfortable selling if markets reverse again.

- Hedge portfolios against significant market declines. (swap equity funds for money market, stable value, or bond funds.)

- Take profits in positions that have been big winners (Rebalance funds above their standard weightings for your portfolio. Same with Company stock in your plan.)

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings. (Rebalancing risk regularly keeps hidden risks somewhat mitigated.)

Have a great week.

Market & Sector Analysis

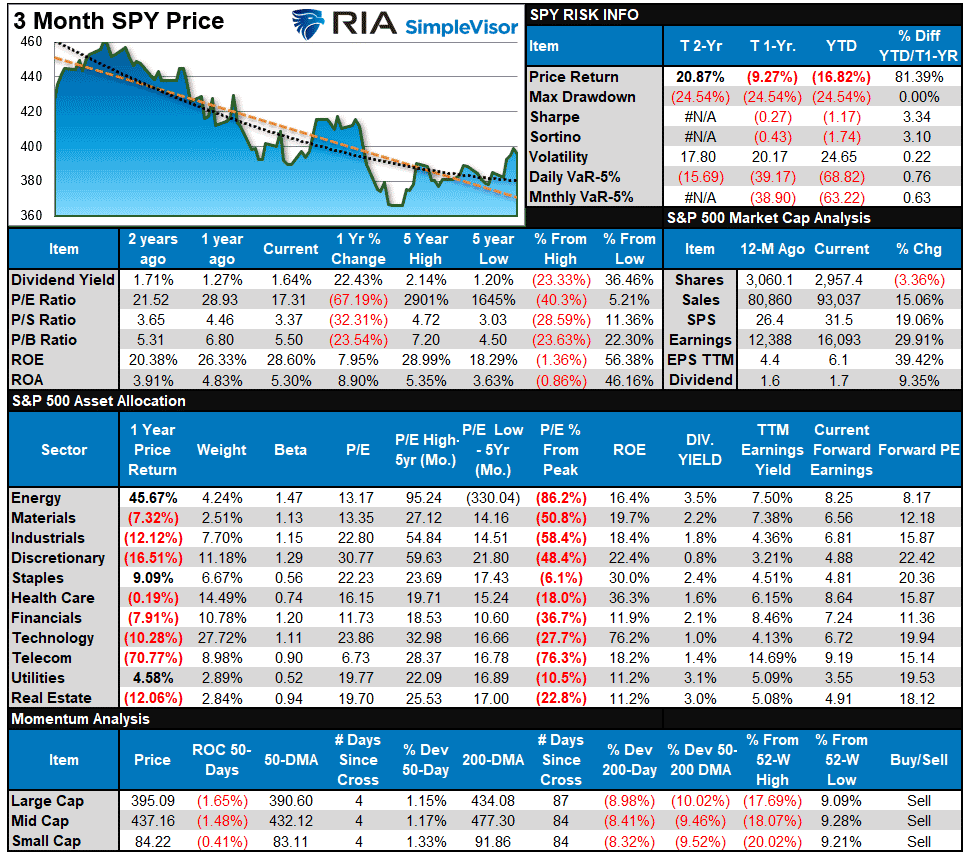

S&P 500 Tear Sheet

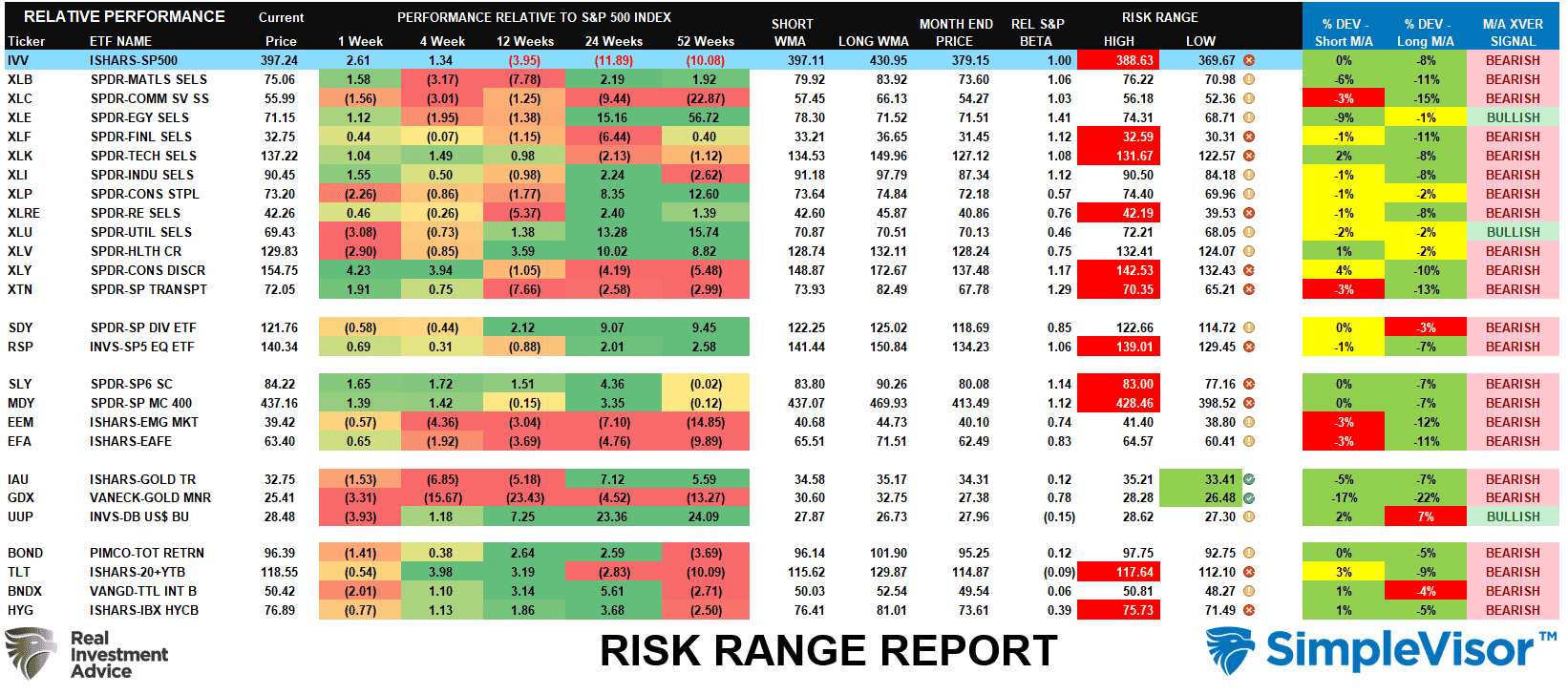

Relative Performance Analysis

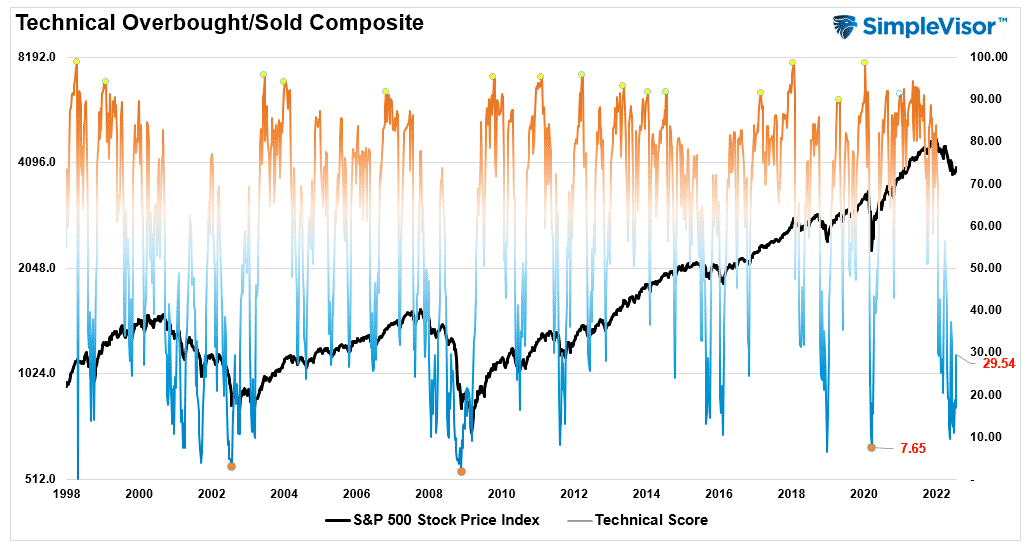

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 29.54 out of a possible 100.

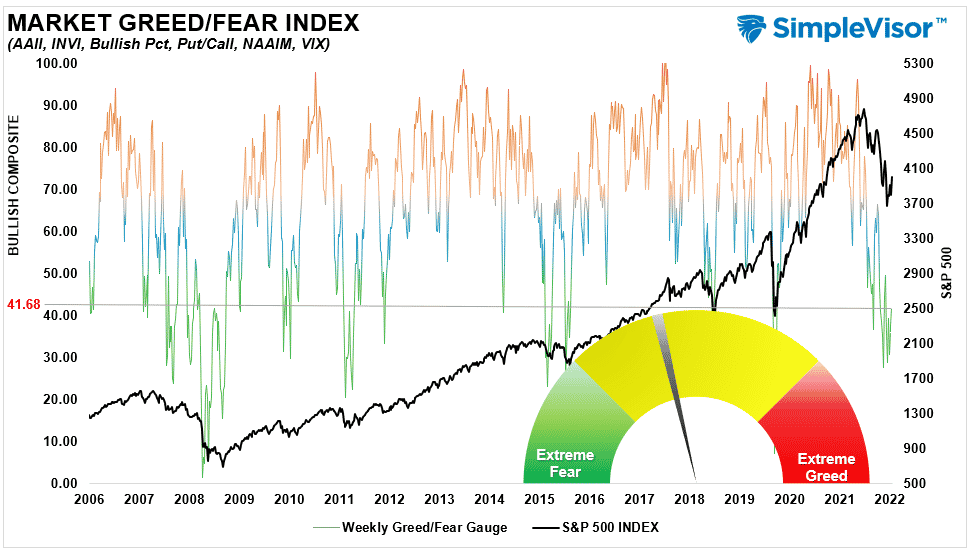

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 41.68 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M/A XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is under the Dashboard/Sentiment tab at SimpleVisor.

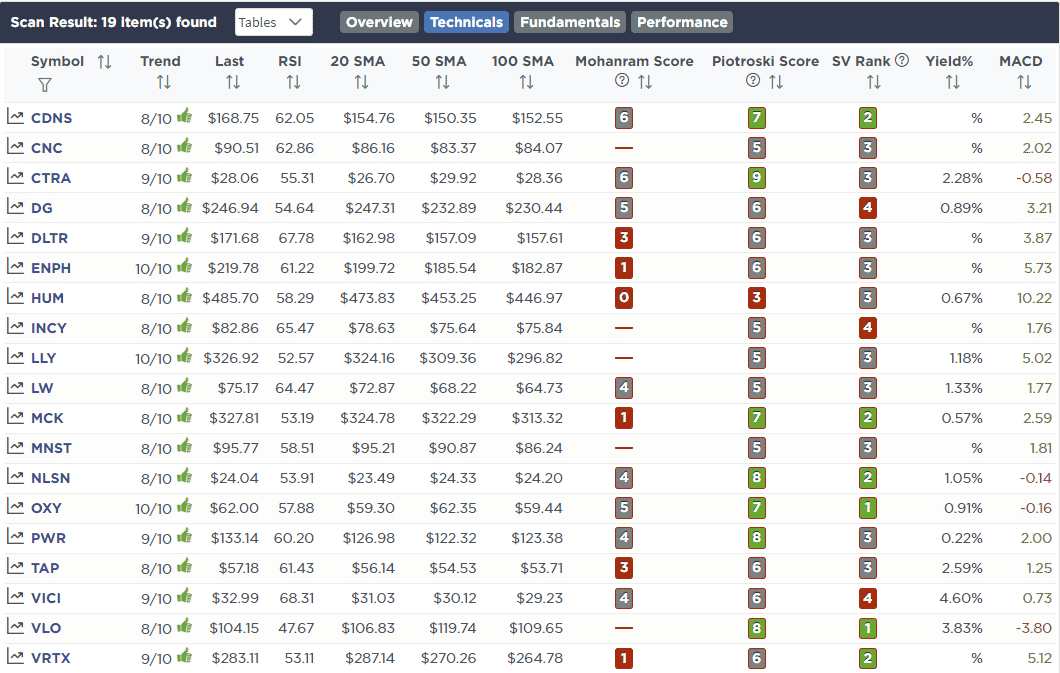

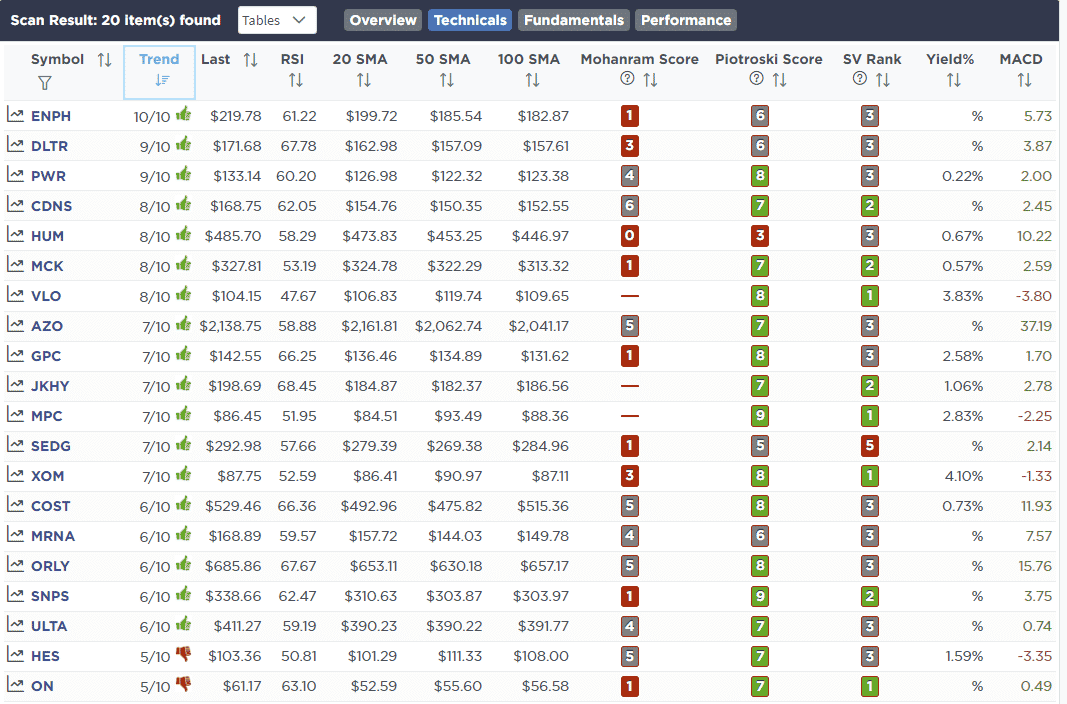

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No trades this week.

Lance Roberts, CIO

Have a great week!