Inside This Week’s Bull Bear Report

- Bond Rates Drop Sharply

- How We Are Trading It

- Research Report – The Most Overlooked Economic Indicator

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Market Review And Update

It was interesting that last week, we wrote:

“The problem with the market rallying and yields dropping is that it undoes the financial constriction they provided on the economy. Higher asset prices boost consumer confidence, and lower yields provide buying power. Both actions create the possibility of a resurgence in inflation, putting the Fed back into “hawkish” mode to ensure inflation falls.“

Mr. Powell heard our concerns, and on Thursday, he responded to the recent loosening of financial conditions.

“[The FOMC] is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time; we are not confident that we have achieved such a stance. We know that ongoing progress toward our 2 percent goal is not assured: Inflation has given us a few head fakes. If it becomes appropriate to tighten policy further, we will not hesitate to do so.” – Jerome Powell

As discussed below, the recent drop in bond rates and surge in the stock market works against the Fed’s goal of tightening monetary conditions. The Fed’s goal remains “tighter” conditions to reduce consumer spending and increase unemployment to reduce economic demand. The demand reduction is how inflation, which is solely a function of supply and demand, gets reduced.

The Fed faces a tricky balancing act of slowing demand without creating a recession, which, despite recent improvements in economic data, remains a risk in 2024.

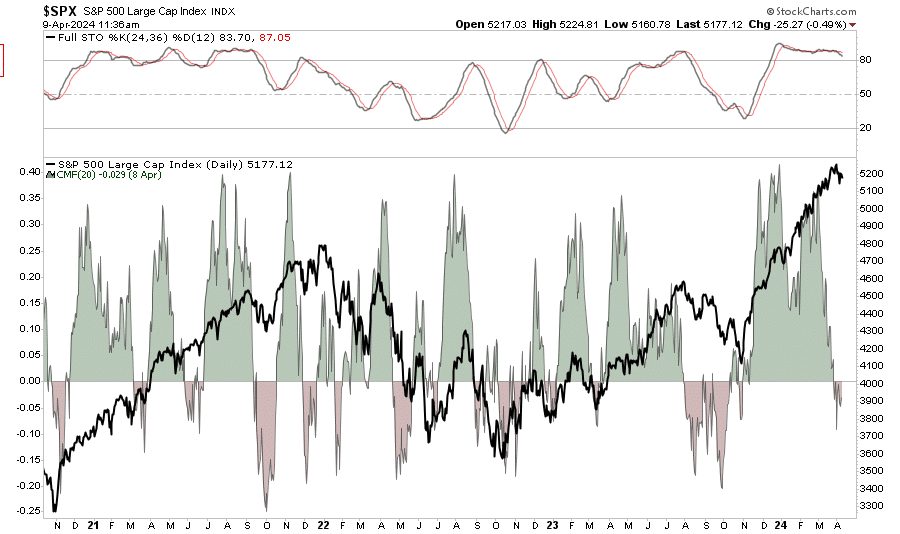

However, as stated, the market pullback on Thursday was well-needed after the longest “win streak” for stocks since 2021. After regaining the 200-DMA, the market surged through the 20- and 50-DMA. As we have discussed, pullbacks to support will be buying opportunities. Such was the case on Friday, as the test of the 50-DMA brought buyers into the market and rallied stocks sharply. With the upper-band of the downtrend channel from the July highs now broken, there is a much stronger bullish case for stocks through year-end. It will likely not be a straight move higher, so use short-term pullbacks to add exposure accordingly.

Seasonally, the market tends to be weak heading into the Thanksgiving holiday, which should work off some of that overbought condition. Following Thanksgiving, the market trades a bit stronger heading into the year’s final month. The chart below shows the seasonal tendencies.

We will use the next month to implement tax loss selling and rebalancing portfolio risk as needed.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Bond Rates And False Narratives

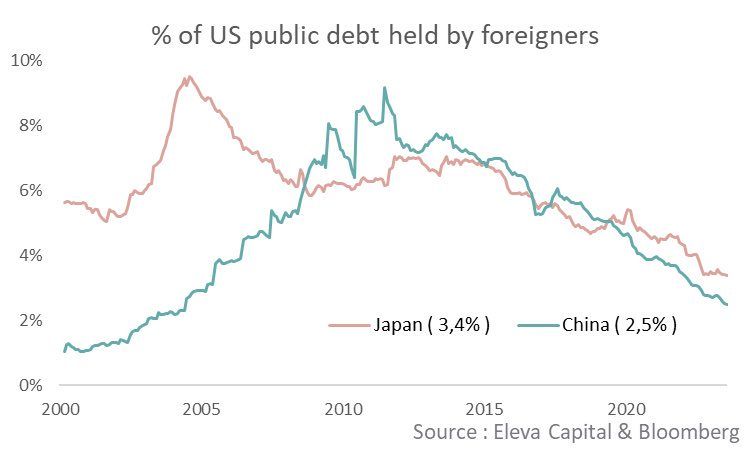

Bond rates surged for the last several months, which spun up many false narratives to explain why. Sometimes, they are factual. Often, legitimate-sounding false narratives are incorrect. One such narrative claimed foreign debt holders, specifically China and Japan, are selling sizeable amounts of U.S. Treasury bonds, which forces Treasury yields higher.

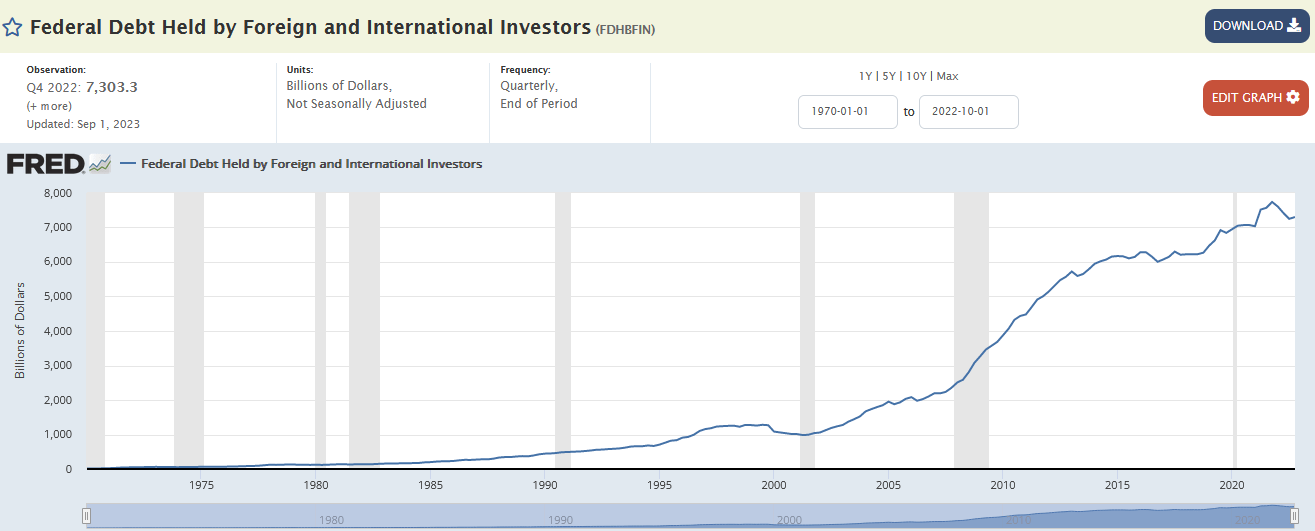

Based on U.S. Treasury data, the year-to-date change in Japan’s holdings of U.S. Treasury securities is up by $37 billion, and China’s have declined by $46 billion. The graph below, courtesy of Eleva Capital, shows a steady decline in their holdings. However, remember that the amount of debt has risen significantly while their holdings remain relatively constant. Further, the second graph shows that debt held by all foreigners is stable if not slightly increasing.

We would be remorseful if we didn’t discuss how much they own. Japan and China hold about $1.1 trillion and $800 billion of U.S. Treasuries. While that may seem significant, they pale compared to the largest holder of Treasuries, the Federal Reserve. The Fed owns about $8 trillion. Even if China or Japan were to sell aggressively, the Fed could easily step in and absorb their selling pressure.

Foreign selling doesn’t explain the recent jump in interest rates or “soaring” debt issuance.

Too Much Debt?

Another false narrative was that massive Treasury debt issuance overwhelmed the bond market. Consider the following comments we found on Twitter:

- This politician (Yellen) knows yields are ripping because of the debt she’s issuing. Yields are no longer moving up because of the FED, and they’re moving up because of debt issuance & foreign countries are selling.

- Soaring yields, partially driven by insatiable debt issuance by the US Treasury, are tightening conditions so fast.

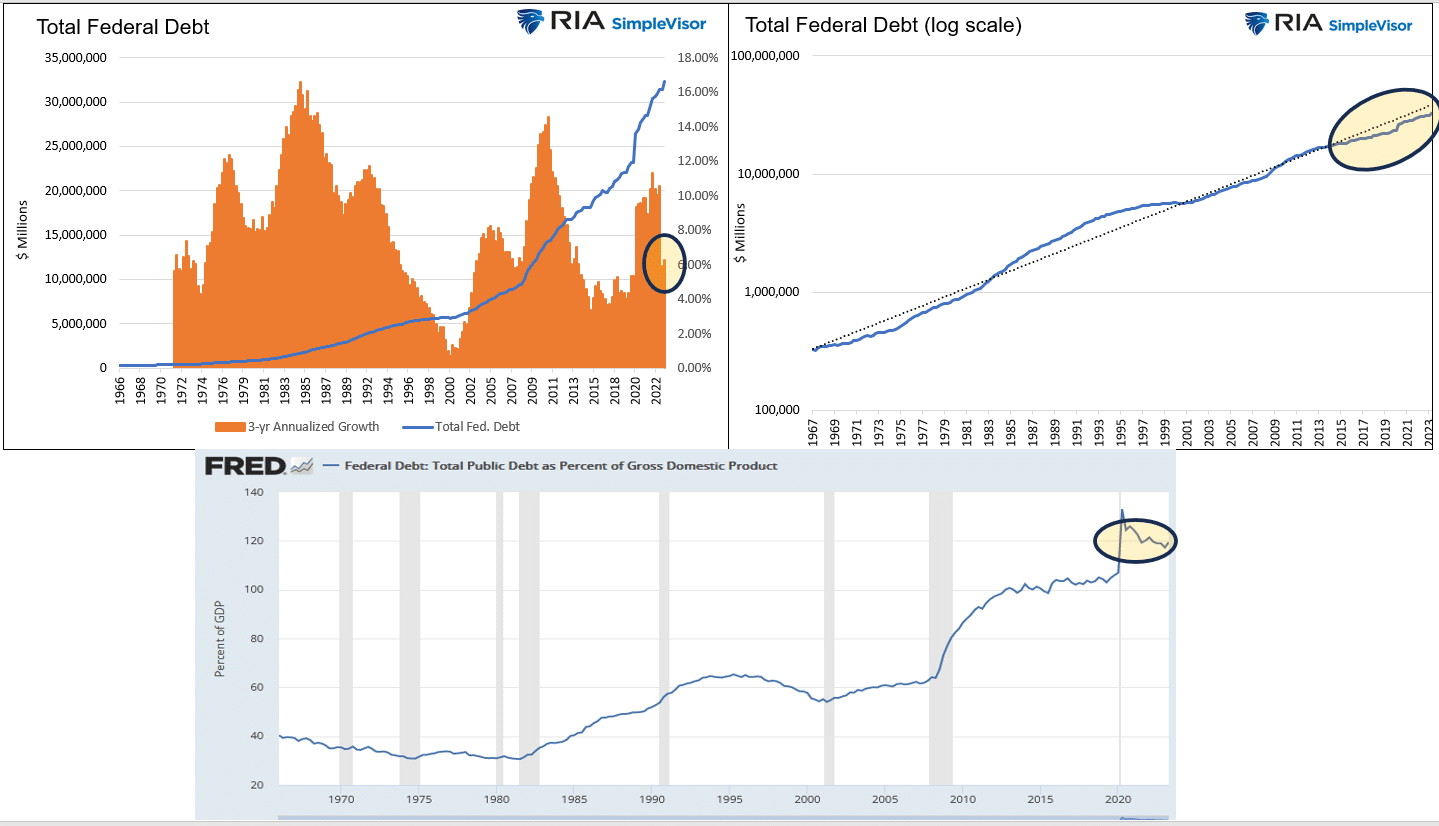

Listening to the media or Twitter, one might think Treasury debt issuance over the last six months is off the charts. Such stories are far from the truth from the proper perspective. Consider the graphs below. The top left graph shows federal debt is growing slightly faster than the pre-pandemic years but well below prior surges. The chart on the right puts debt growth on a log scale to show the current growth rate is slightly below the trend of the last fifty years. Lastly, the bottom graph shows the sharp increase in debt to GDP during the pandemic. However, it has declined since. A high debt-to-GDP ratio, as we have, is very problematic. But false narratives claiming recent issuance is well above average are flat-out wrong.

So, if those are all false narratives, what drove bond rates higher, and where are they heading next?

Bond Rates A Function Of The Economy

Unlike stocks, bonds have a finite value. At maturity, the lender receives its principal and final interest payment. Therefore, when a bond buyer “loans” money to another entity for a specific period, the “bond rate” takes into account several substantial “risks:”

- Default risk

- Rate risk

- Inflation risk

- Opportunity risk

- Economic growth risk

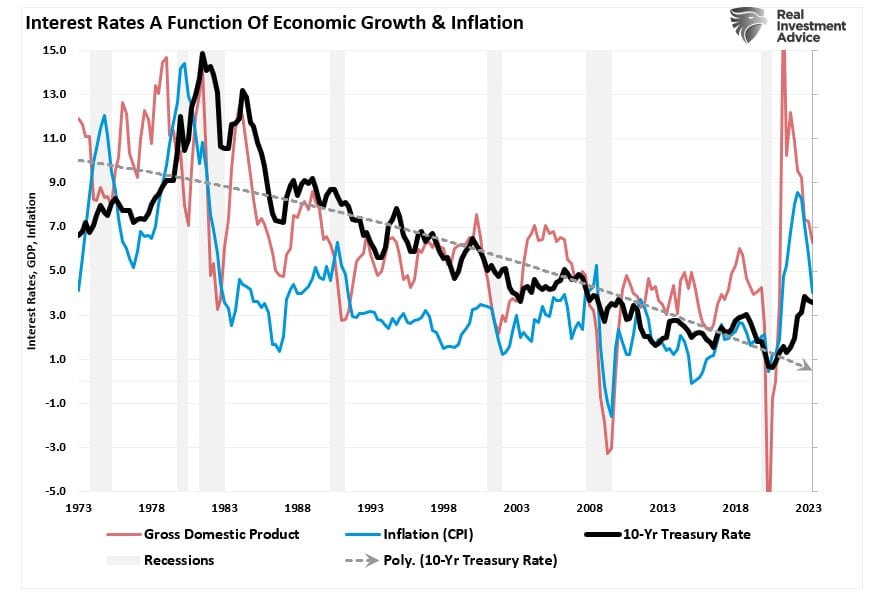

Therefore, since bonds are loans to borrowers, a bond’s interest rate is tied to the prevailing rate environment at the time of issuance. In other words, the interest rate reflects expectations for economic growth and inflation.

Since rates and expectations must adjust for the potential future impact on the current value of invested capital:

- Equity investors expect that as economic growth and inflationary pressures increase, the value of invested capital will increase to compensate for higher costs.

- Bond investors have a fixed rate of return. Therefore, the fixed return rate is tied to forward expectations. Otherwise, capital is damaged due to inflation and lost opportunity costs.

Therefore, the long-term correlation between rates, inflation, and economic growth is unsurprising.

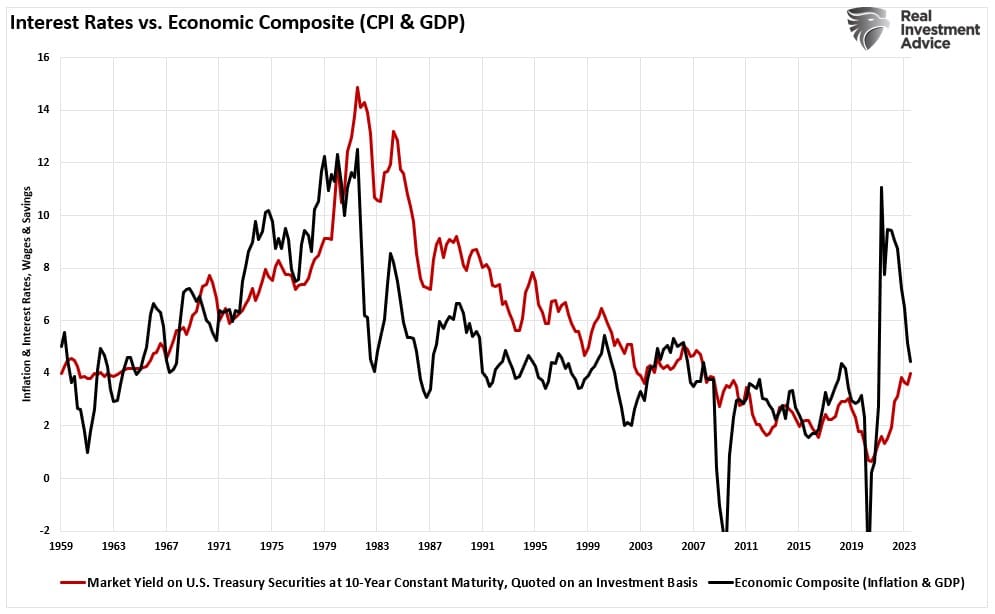

That is pretty cluttered, so the following chart is a composite index of inflation and economic growth compared to the 10-year Treasury yield.

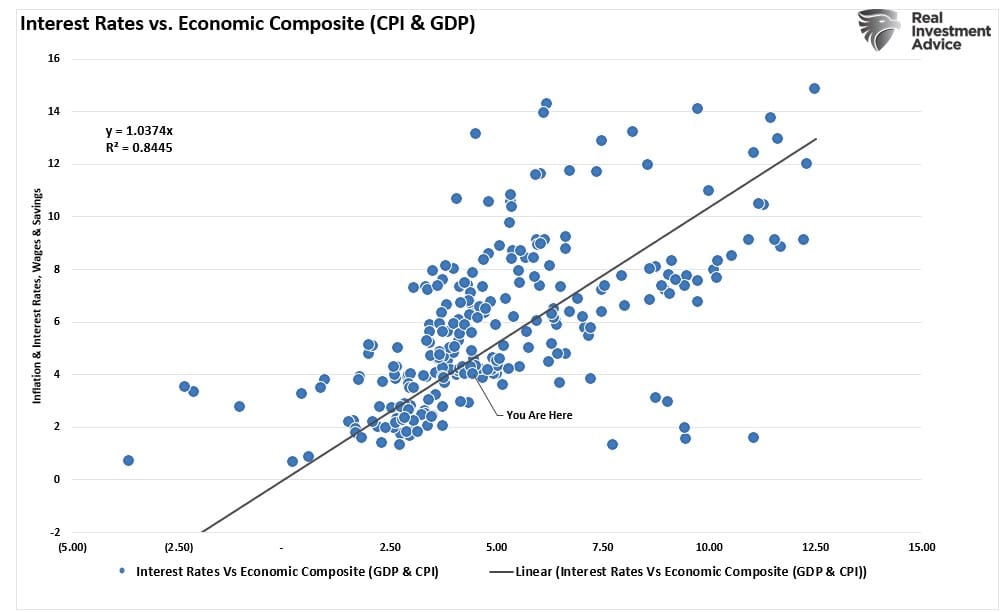

As expected, the surge in economic growth and inflation pulled longer-duration yields higher. With a correlation of nearly 85% between interest rates and a GDP/Inflation composite index, investors should expect rates to fall as economic growth and inflation decline.

Again, since bond buyers are loaning money to the bond issuers, their assessment of future inflation and economic growth affects the bond rate. Over the last week, that assessment has started to change.

Bond Rates Detached From Economics

The issue of inflation and economic growth and its correlation to bond rates should not be dismissed. As shown below, a rather large spread exists between future inflation expectations and Treasury yields. Historically, rates will decline towards inflation expectations and tend to do so rapidly during recessionary periods.

Furthermore, the economic growth component of the bond rate calculation is also not showing substantial strength to justify higher rates. The ISM Composite Index is currently hovering around recessionary levels. Historically, when the ISM Composite Index was at such levels, yields fell sharply. The detachment of that previous correlation suggests a mismatch between bond market participants and economic realities.

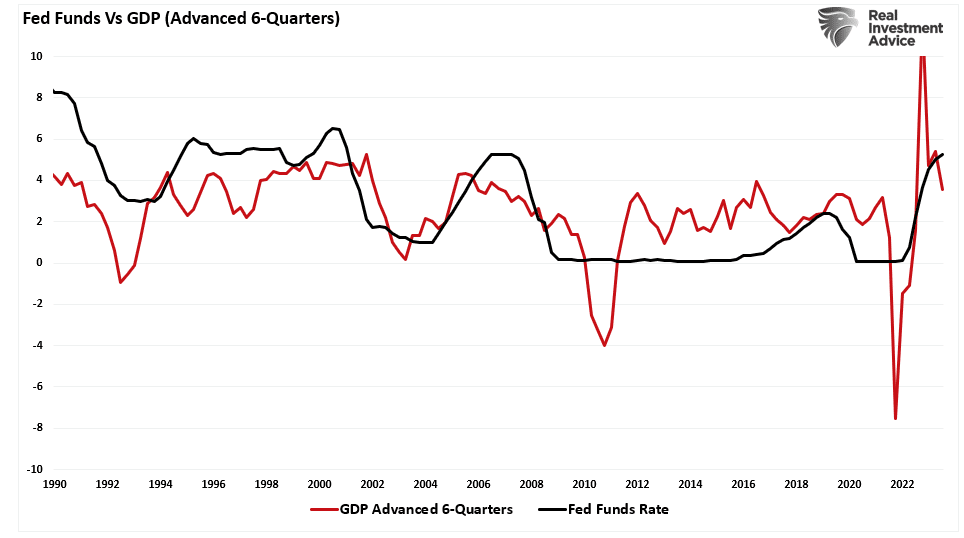

As noted previously, the massive monetary surge from the “Pandemic Bailouts” created a supply/demand imbalance, resulting in higher prices. Such was expected. However, as the monetary surge reverses, economic growth will continue to slow. Furthermore, the lag effect of the previous monetary tightening cycle is now beginning to impact economic growth. As shown below, there is a 6-quarter lag between rate hikes and economic impacts.

With the economic data showing signs of slowing and likely continuing into 2024, the detachment between bond rates and lower economic and inflation growth will close. Such provides a substantial tailwind for bond investors as markets reprice bond rates for economic realities.

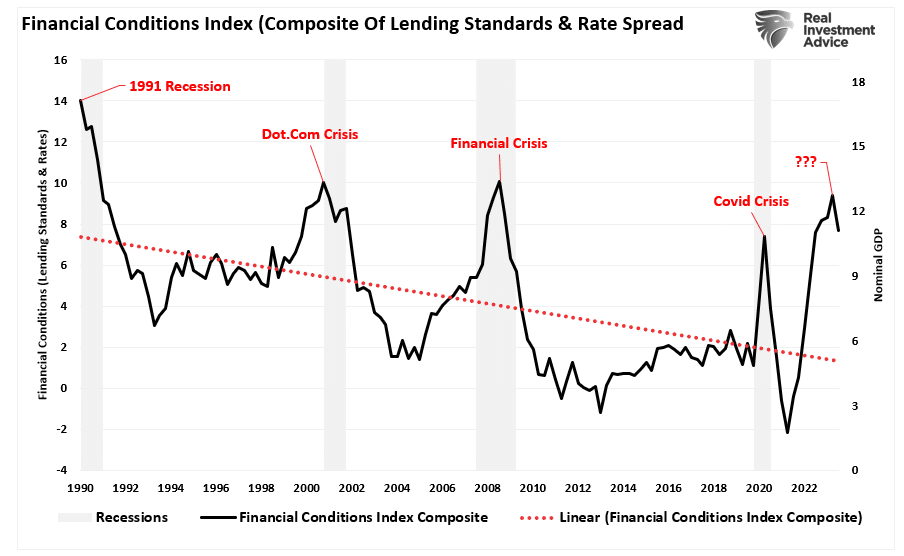

However, as we noted in “Bond Bear Market,” there are implications for the Federal Reserve as bond rates are repriced lower, particularly when it remains focused on inflation. Lower yields and potentially higher asset prices reverse the financial conditions the Fed hoped to tighten. As shown below, our financial conditions index has loosened over the past week.

The Fed’s Problem

As noted above, the problem for the Fed is that increased liquidity, higher asset prices, and lower yields remove the pressure from consumers. If consumer confidence improves, then so does consumption. That increased demand then fosters higher prices, which is not what the Fed wants, at least not yet.

The Fed’s challenge is potentially a trap of their own making. On the one hand, they want falling asset prices and weaker economic data to quell inflation. However, the Fed does NOT wish for an economic event to destabilize the financial system. Unfortunately, the Fed may soon face a difficult decision. Either allow a deeper recession to take hold, quelling inflation, or cut rates to keep a banking crisis from spreading.

We will likely know the answer sooner than later.

However, I believe that Treasury bonds will be the asset class of choice.

How We Are Trading It

As noted above, we will implement tax-loss selling in portfolios over the next few weeks as part of the risk rebalancing heading into year-end. This year has been a very bifurcated market, with only a handful of stocks performing well, with value and dividend stocks under pressure due to higher rates. The equal-weight index is virtually flat for the year, while the market-cap index is up 13%. That will most likely change drastically next year, but that is something we will focus on with the turn of the calendar.

While there is support for a rally into year-end, substantial risks are also ahead. We suggest using the rally to align your portfolio with your risk tolerance.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against more significant market declines.

- Take profits in positions that have been big winners.

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings.

While the August through October selloff may be over for now, there are still risks ahead. Trade accordingly.

See you next week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

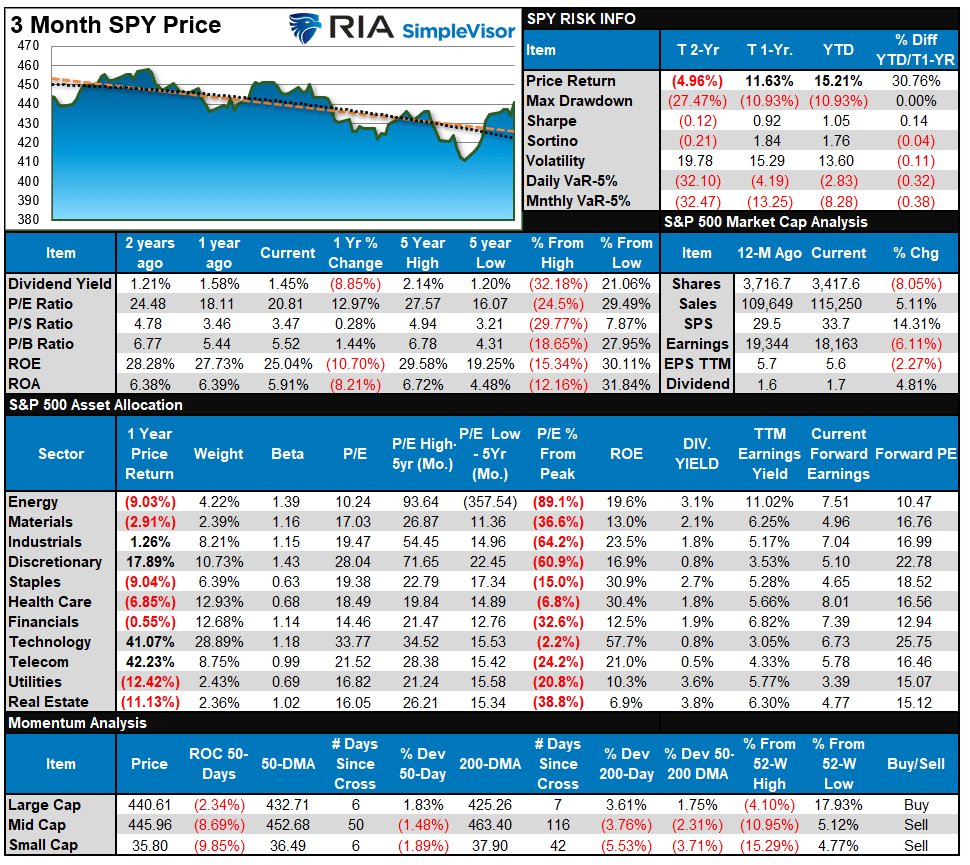

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

Last week, we stated:

“As shown below, that rally came with a vengeance this past week, with the S&P and Nasdaq rallying near 6%, respectively. The markets are returning to short-term overbought conditions, so a bit of consolidation next week is likely. If you have been waiting for a rally to reduce risk or rebalance allocations, this is likely the best opportunity we will have over the next few days. Look for pullbacks to support if you want to add exposure to your portfolio for a year-end push.”

That is what happened with the market retesting support at the 50-DMA and then rallying sharply on Friday. Buying opportunities will likely be limited in the short term. With the market still a bit overbought, look for small pullbacks or consolidation to add exposure as needed.

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 62.02 out of a possible 100.

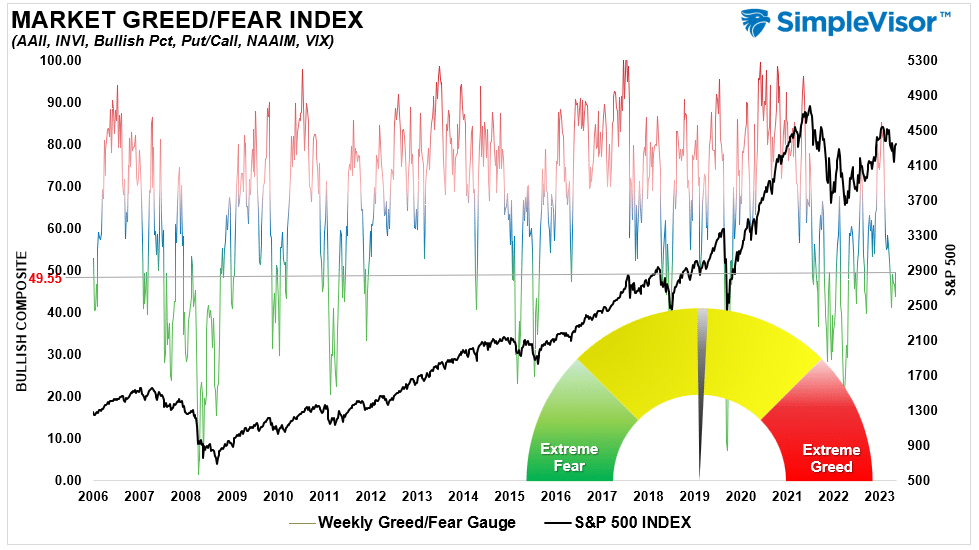

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 49.55 out of a possible 100.

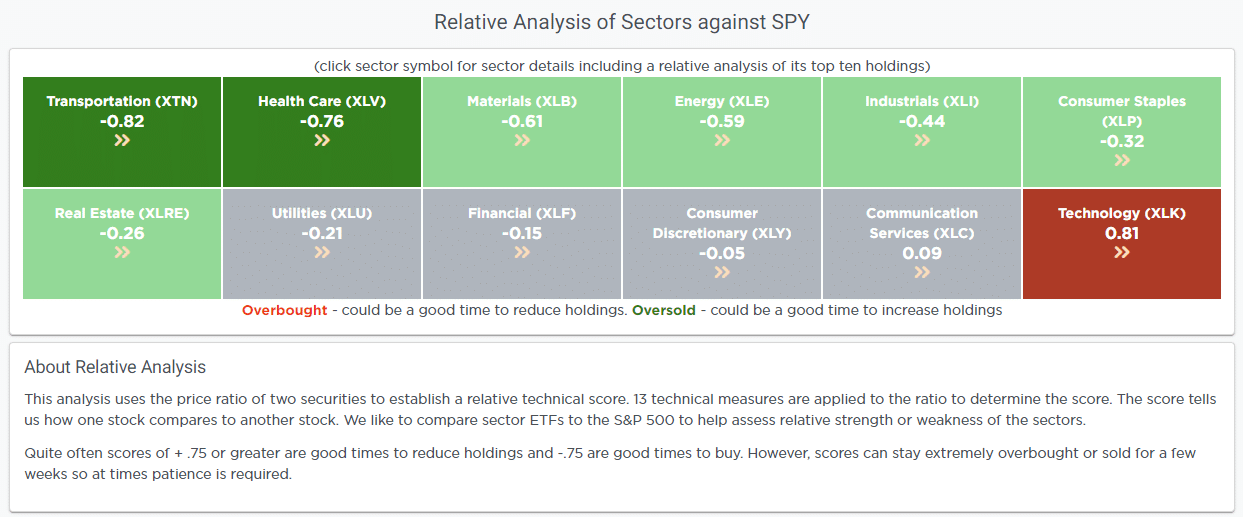

Relative Sector Analysis

Most Oversold Sector Analysis

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

Technical issue with the data feed. Will return next week.

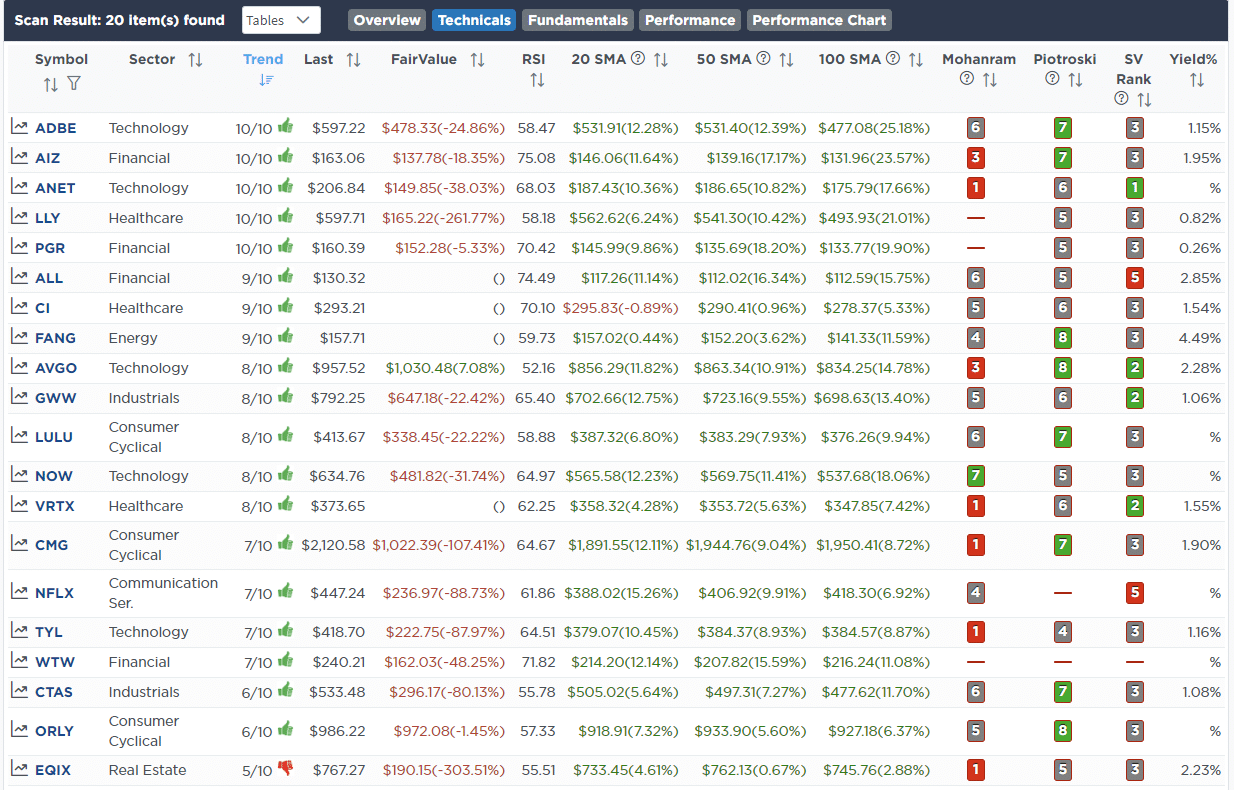

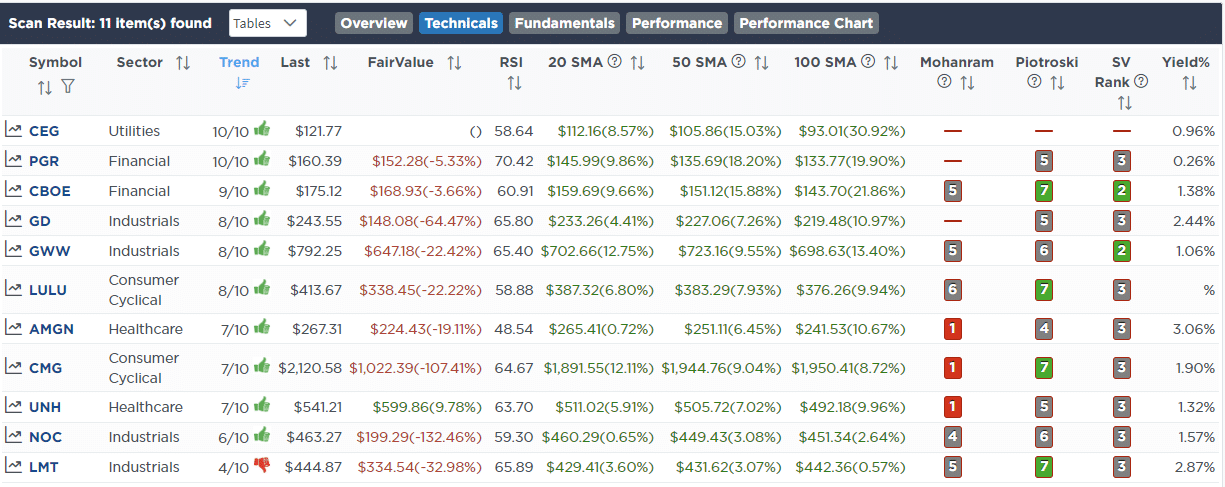

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week, we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental & Technical Strength

(Click Images To Enlarge)

R.S.I. Screen

Momentum Screen

Fundamental & Technical Strength

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

Nov 6th

“Given Apple’s string of weak revenue growth, we shifted 1% of Apple (AAPL) to Microsoft (MSFT) and Google (GOOG) which are continuing to show strong gains in both revenue and earnings growth. However, given AAPL’s weight in the index, and the implications of ETF flows, we are maintaining a sizable holding in the stock.

We also increased Comcast (CMCSA) by 0.50% and added 1% to Costco (COST.) CMCSA and COST look good technically, and we have been wanting to add to each. On the sector side, we added 1% to XLK and XLP and half a percent to XLC. We now stand at 58.5% equities in the equity model and 57% in the sector model.“

Equity Model

- Reduce Apple (AAPL) by 1% of the portfolio

- Add 0.5% of the portfolio each to Microsoft (MSFT) and Google (GOOG)

- Increase Comcast (CMCSA) by 0.50% of the portfolio.

- Add 1% of the portfolio to Costco (COST)

ETF Model

- Increase the iShares Technology Sector ETF (XLK) by 1% of the portfolio.

- Add 1% of the portfolio to the iShares Staples ETF (XLP)

- Increase the iShares Communications ETF (XLC) by 0.50% of the portfolio

Nov 8th

“On October 6th, as yields were shooting higher on the 10-year Treasury Bond, we discussed that we were adding a trading position to our portfolio by increasing our stake in the Vanguard Extended Duration Bond ETF (EDV).

That trade has worked out well, with EDV rallying sharply over the last week and hitting the 50-DMA, our initial target for the trade. We are now taking profits in that trade in both models and reducing EDV back to the portfolio model allocation.“

Both Models

- Reduce EDV back to its original portfolio model allocation weight of 12%.

Nov 10th

Over the last few weeks, we discussed using the potential market rally to rebalance risks and make portfolio adjustments. That rally has been very strong, and with the markets now overbought, we are continuing that process.

Today, we are using the rally to start our annual process of tax loss harvesting. While we fundamentally like the companies being sold, they are good candidates to reduce portfolio risks in the near term and provide a tax benefit in the future. We will potentially buy these companies back at some point after the 30-day period the IRS requires to avoid “wash sales.”

Equity Model

- Sell 100% of Abbott Laboratories (ABT). CVS (CVS) and Altria (MO).

- Reduce Public Storage (PSA) to 1.5% of the portfolio.

- Increase Stanley Black & Decker (SWK) to 2.5% of the portfolio.

ETF Model

- Sell 100% of the Vanguard High Dividend Yield ETF (VYM).

Lance Roberts, C.I.O.

Have a great week!