The “Fear Of Missing Out,” or “F.O.M.O.” is a centuries-old behavioral trait that began to get studied in 1996 by marketing strategist Dr. Dan Herman.

“Fear of missing out (FOMO) is the feeling of apprehension that one is either not in the know or missing out on information, events, experiences, or life decisions that could make one’s life better. The fear of missing out is also associated with a fear of regret. Such may lead to concerns that one might miss an opportunity. Whether for social interaction, a novel experience, a memorable event, or a profitable investment.” – Wikipedia

Over the last couple of years, the “fear of missing out” went mainstream. Young retail investors armed with a “stimmy check,” the Robinhood app, and membership to WallStreetBets piled into the financial markets. The lure of easy money and lavish lifestyles was too hard to pass up.

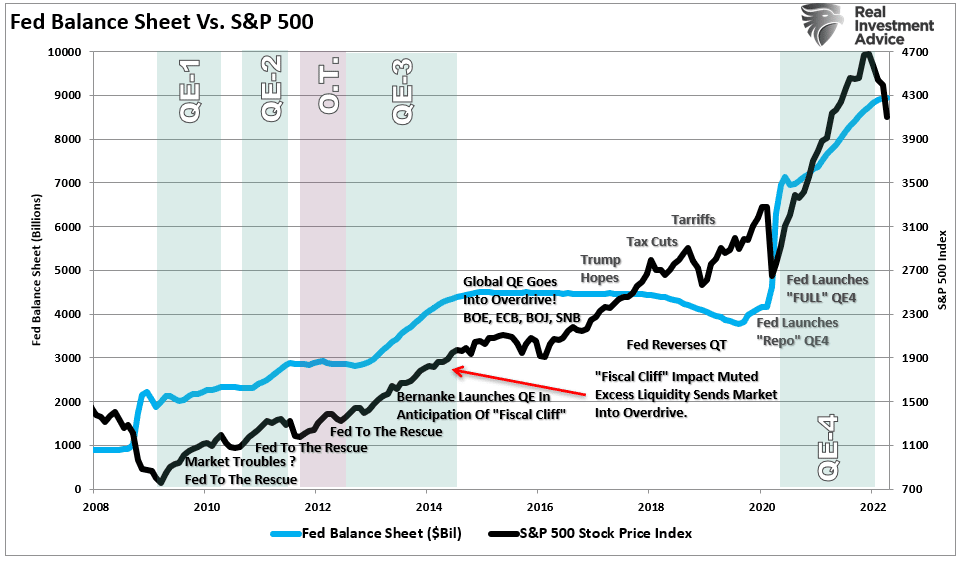

However, recent events are the point where F.O.M.O. became most visible. In reality, the “fear of missing out” has been with us for over a decade. As shown, repeated rounds of monetary interventions created a sense of moral hazard in the financial markets.

What exactly is the definition of “moral hazard.”

Noun – The lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.

The massive Federal Reserve interventions provided a perverse incentive to take on extreme forms of risk. From speculative I.P.O.s, S.P.A.C.s, or Cryptocurrencies, investors believed the Fed was protecting them from the consequences of risk. In other words, the Fed effectively “insured them” against potential losses.

The lesson taught to investors was that the Fed would bail out any market decline. Therefore, the “fear of missing out” overrides the “need to get out.”

Such is the case we see currently in the markets.

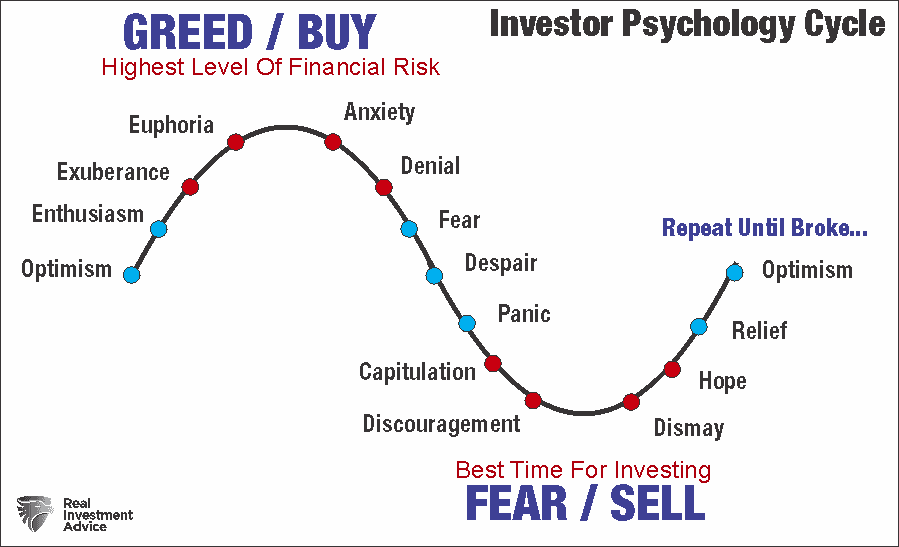

I’m Terrified, But I’m Not Selling

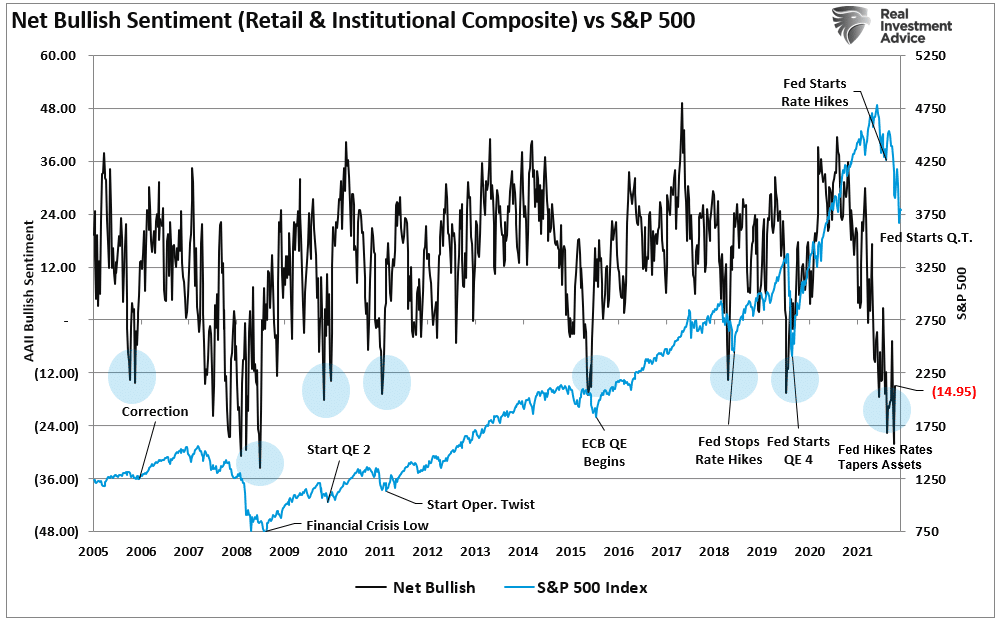

Not surprisingly, investors are terrified with the market down nearly 20% so far this year. As shown by our composite index of both retail and institutional investors, fear is rampant. The net bullish sentiment is currently at the lowest level since the depths of the financial crisis.

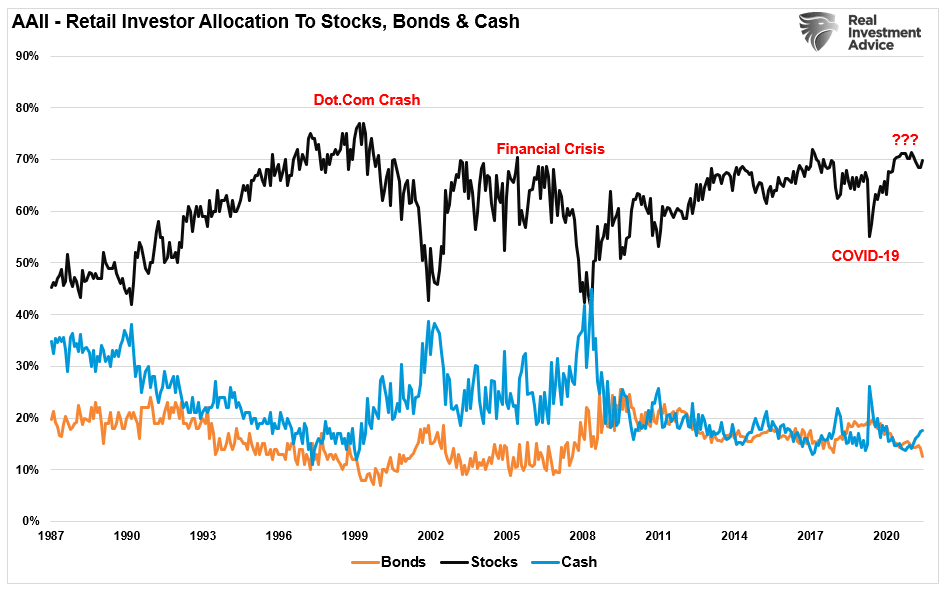

This extreme bearishness would suggest investors are reducing their exposure to equity risk. However, the reality is quite different. As shown below, the A.A.I.I. investor allocation to stocks, bonds, and cash tells the story. Despite A.A.I.I. sentiment at very bearish levels, the allocation to equities remains very high while bonds and cash remain low.

Interestingly, seemingly terrified investors are still unwilling to sell for the “fear of missing out.“ It is worth noting that during previous bear markets, equity allocations fell as investors fled to cash. Such has not been the case in 2022.

Investors seem more afraid of missing the bottom should the Federal Reserve suddenly reverse course on monetary policy. Much like Pavlov’s dogs, after years of being trained to “buy the dip,” investors are awaiting the Fed to “ring the bell.“

However, if a recession is approaching, the question will be how deep of a price declination investors can emotionally withstand.

The Coming Correction Of “E”

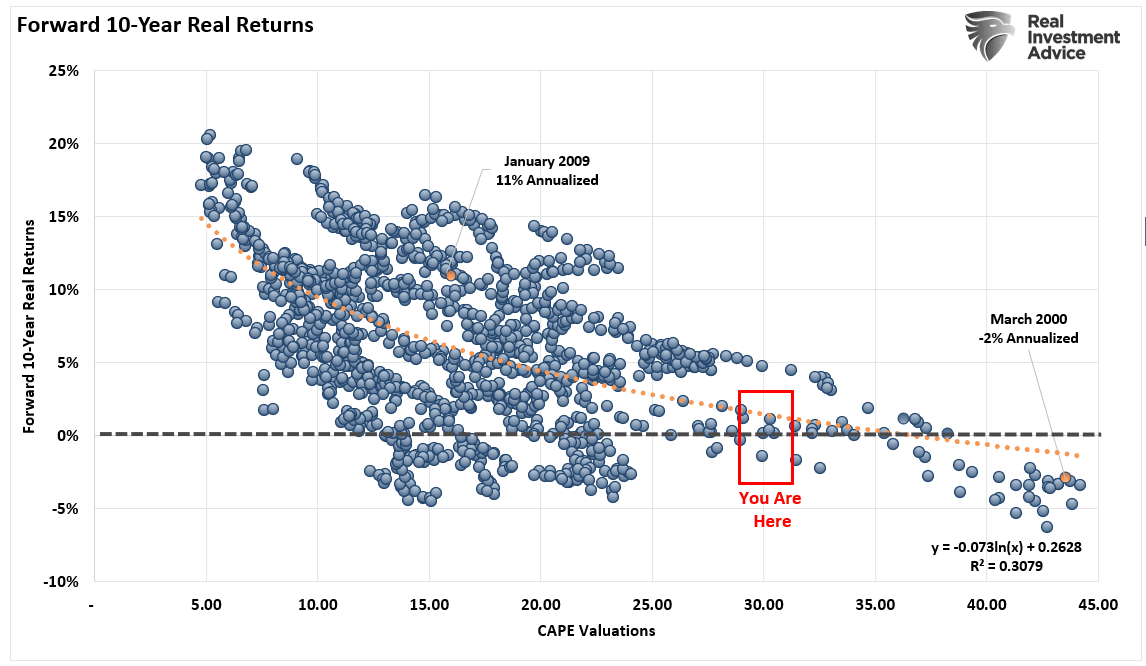

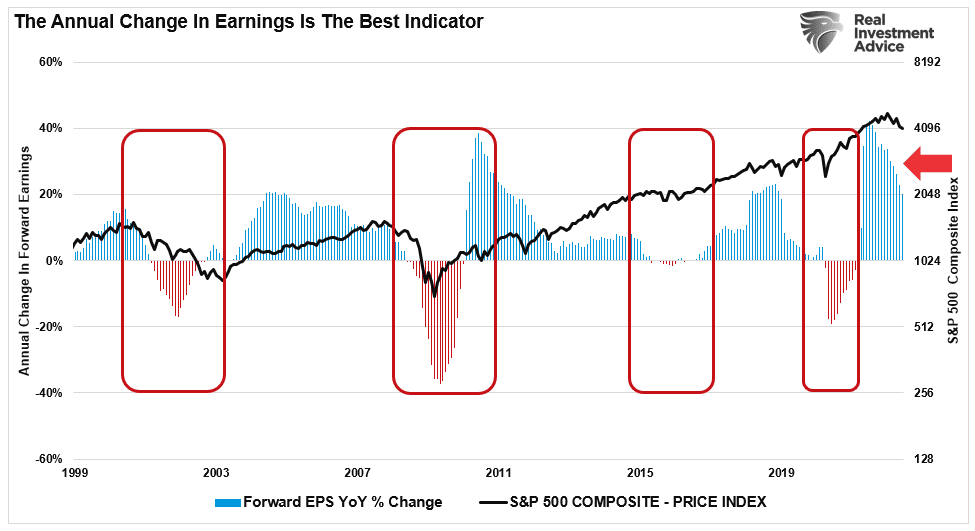

As discussed many times, valuations are the most critical determinant of investment returns over long-term periods. As shown below, valuations, as measured by P/E ratios (price divided by earnings), highly correlate to future returns.

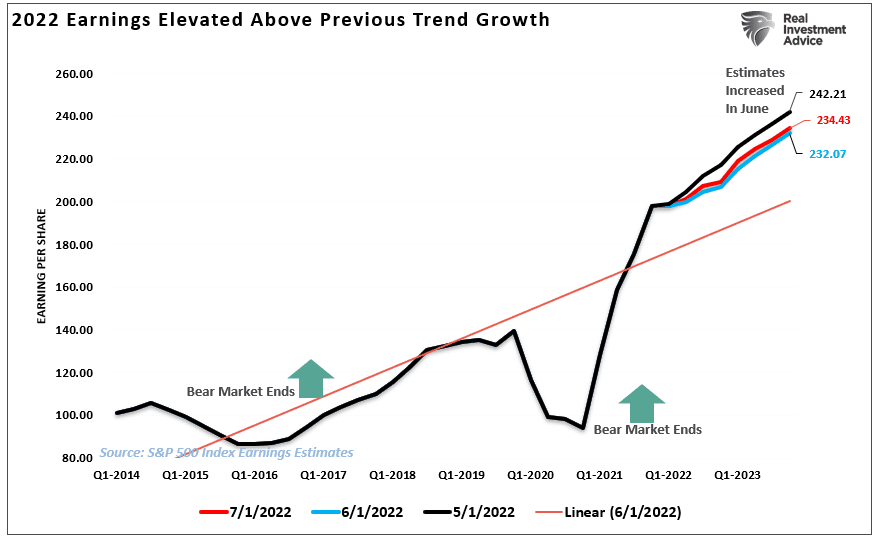

While the price (P) of the valuation calculation has fallen in 2022, forward earnings estimates (E) have not. In fact, as shown below, earnings estimates through the end of 2023 increased during the month of June and remain well above the long-term exponential earnings trend.

Currently, as shown below, Wall Street continues to expect earnings to grow through the end of 2024 despite the growing risk of a recession.

However, while estimates, and forward expectations of rising equity prices, history clearly shows that earnings do not survive recessions. Such is because earnings come from economic activity, and therefore recessions result in earnings reversions. Given that earnings expectations are at the top of the long-term growth channel, a reversion below the trendline should be no surprise.

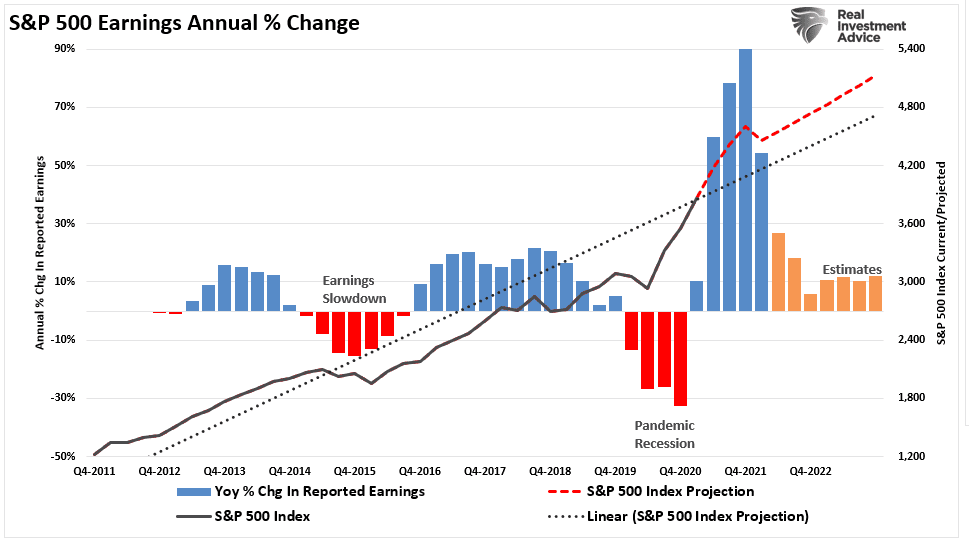

During the previous four recessions and subsequent bear markets, the typical revision to consensus EPS estimates before the onset of a recession ranged from -6% to -18%, with a median of 10%. Coming out of recession, analysts start to increase estimates markedly. Such makes for a great indicator of when to be a buyer of equities.

Notably, while forward P/E ratios have declined, much of that is due to the decline in the “P” and not the “E.” Therefore, if the data suggests that an earnings recession is coming, then the current “bear market” cycle still has more work to do.

The realignment of market prices and valuations is always a brutal process.

This Time Is Likely Not Different

As noted recently by Nick Colas, there are downside risks to equities if the “E” gets reduced.

“The second-order guess might be 3,386 if we assume investors will think other market participants will key off either pre-pandemic highs and/or discount a modest earnings recession.

- Such was the last S&P 500 high before the Pandemic Recession (February 19th, 2020).

- It is also 18x S&P earnings of $188/share, roughly 15% below current earnings of $220/share.

- While earnings typically decline 25% in a recession, perhaps any upcoming economic downturn will be milder than most.

The third-order guess is around 3,000 if investors believe markets must discount a full-blown recession before there is enough general interest in stocks to make for a durable low.

- Assume an average decline of 25% to S&P earnings from a recession, and you get $165/share.

- Put an 18x multiple on that $166/share, and you get an S&P of 2,970.“

There is currently a large contingent of investors who have never seen an actual “bear market.” As noted above, their entire investing experience consists of continual interventions by the Federal Reserve. Therefore, it is not surprising that despite the recent price decline, they aren’t selling out of the market. Wall Street also suffers from the same “fear of missing out.” as they hope the Fed can engineer a soft-landing.

Unfortunately, the risk of disappointment is high as history suggests the Fed will cause a “hard landing” in the economy. If we use history as a guide, a more severe reversion in earnings is logical.

This time is not likely different.

The most significant risk to investors is when the “fear of missing out” changes to the “fear of being in.”

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read