Q2 Earnings Season Begins – Will It Support The Bulls?

Inside This Week’s Bull Bear Report

- Market Review & Update

- Q2 Earnings Season Begins

- How We Are Trading It

- Research Report – Could Student Loan Payments Be The Trigger?

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Market Review & Update

I am having a belated “Independence Day” trip with my family this weekend, so this week’s discussion on Q2 earnings will be a bit brief. The full newsletter will return next week.

Last week we noted that:

“With bullish optimism quickly returning to the market, the pressure to chase performance from the “Fear Of Missing Out” will continue to provide a “bid” under stocks.

However, such does not remove the potential for a 5-10% correction. Such corrections are normal within any given year and will provide the best entry point to increase equity exposure near term. Using Fibonacci retracement levels, investors should consider adding exposure at 4250, down to the 200-DMA. A violation of the 200-DMA would suggest a larger corrective process at work, most likely coinciding with some market-related event.”

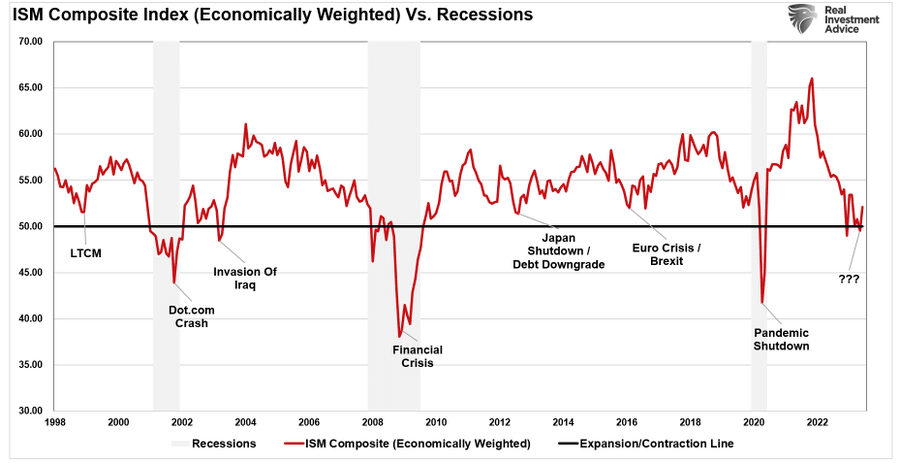

This week’s economic data sent confusing messages through the market. A stronger-than-expected ISM Services number suggests that no recession is on the horizon currently. As noted in the chart below, there has never been a recession since the turn of the century when services (which comprise 80% of the economy) are not in contraction.

However, on Friday, there was some deterioration in the employment report which suggests the economy is slowing down. That news was received as bullish, sending stocks higher, as hope rose that the Fed would not need to continue hiking rates.

With Q2 earnings season set to start next week, the current momentum behind the market remains strong as investors continue to buy even the slightest dips in fear of missing out (F.O.M.O.) on further upside. Unfortunately, the bulk of the advance remains driven mainly by only a small handful of stocks, but breadth has improved somewhat in recent weeks.

Regardless, the market remains short-term overbought and deviated above longer-term moving averages. As noted, while momentum will continue to propel markets, such does not preclude an eventual correction resetting some of the overbought conditions. It is unknown when such a correction will occur or what will cause it. However, such a correction would provide a much better entry point to increase portfolio equity risk.

For now, hope remains that the Q2 earnings season will continue to support the bulls.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Q2-Earnings Season Begins

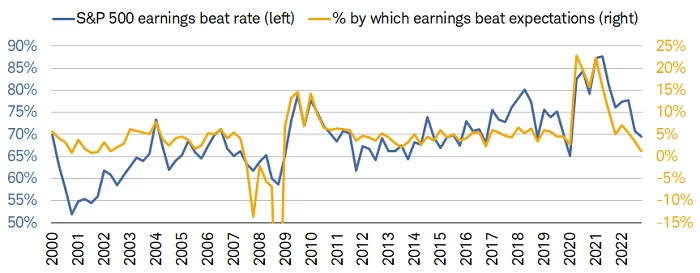

No matter what is happening in the market, or the economy, there is always a high number of companies regularly beating estimates from Wall Street. Are Wall Street analysts that poor at predicting future corporate earnings, or is there something else potentially going on? Furthermore, what does that mean for investors using those estimates in making investment decisions?

As noted in “Trojan Horses,” analysts are always wrong, and by a large degree.

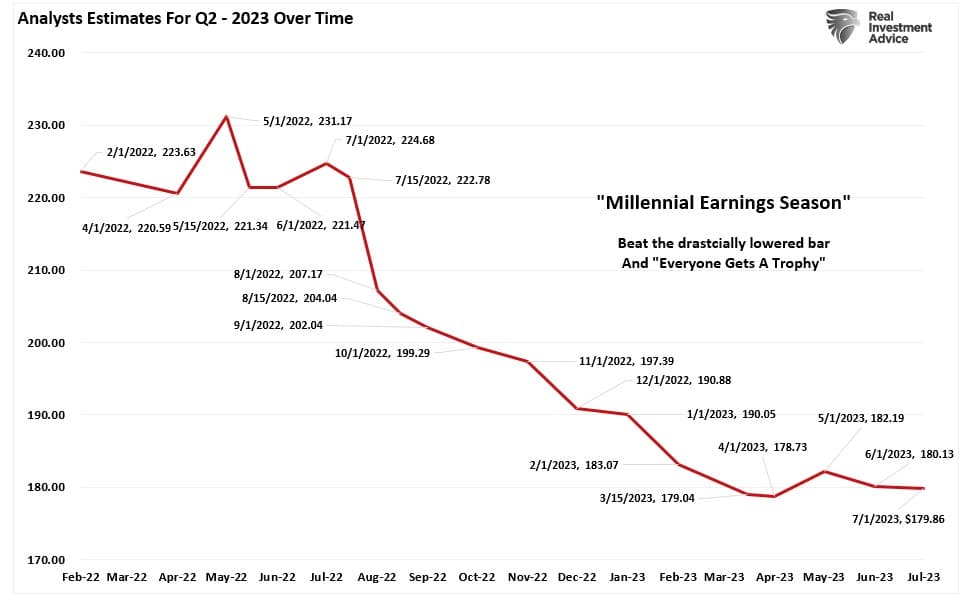

“This is why we call it ‘Millennial Earnings Season.’ Wall Street continuously lowers estimates as the reporting period approaches so ‘everyone gets a trophy.’”

The chart below shows the estimate changes for Q2 earnings from February 2022, when analysts provided their first estimates.

“An easy way to see this is the number of companies beating estimates each quarter, regardless of economic and financial conditions. Since 2000, roughly 70% of companies regularly beat estimates by 5%. Again, that number would be lower if analysts were held to their original estimates.”

As shown, for companies to win the “beat the estimate game,” they need the bar lowered far enough to ensure they can clear it. Many companies would miss, rather than beat, if not for these downward revisions in analysts’ estimates. Such would weigh on stock price performance which directly impacts executive compensation due to the now standard practice of using stock options.

Read that last sentence again.

4-Tools To Win The “Beat The Estimate Game”

However, the analysts are only one-half of the equation. The other half comes from corporations.

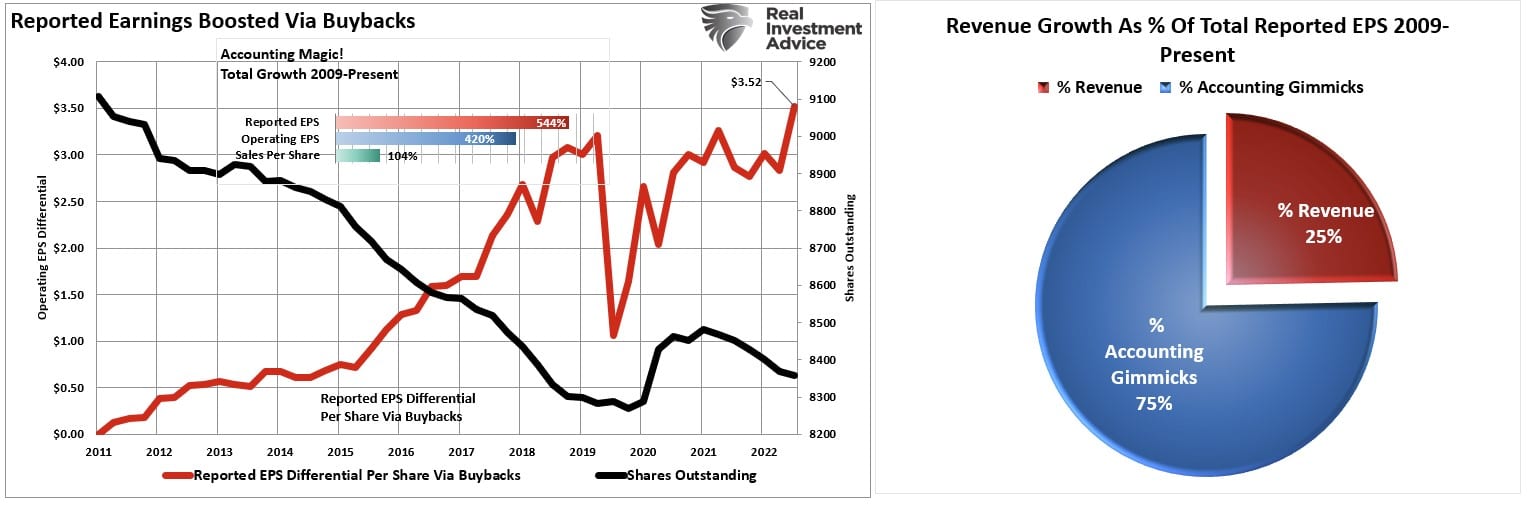

Since 2009, the reported earnings per share of corporations has increased by an astounding 544%. Such is the sharpest post-recession increase in history. However, reported sales per share, which happens at the top line of the income statement, has only risen by a marginal 104%.

For profitability to surge, corporations have resorted to four primary tools:

- Wage growth suppression,

- Productivity increases,

- Labor reduction via offshoring; and,

- Stock buybacks.

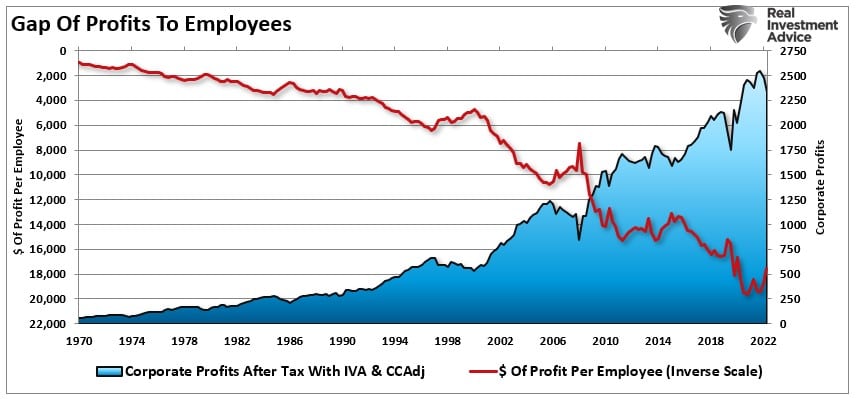

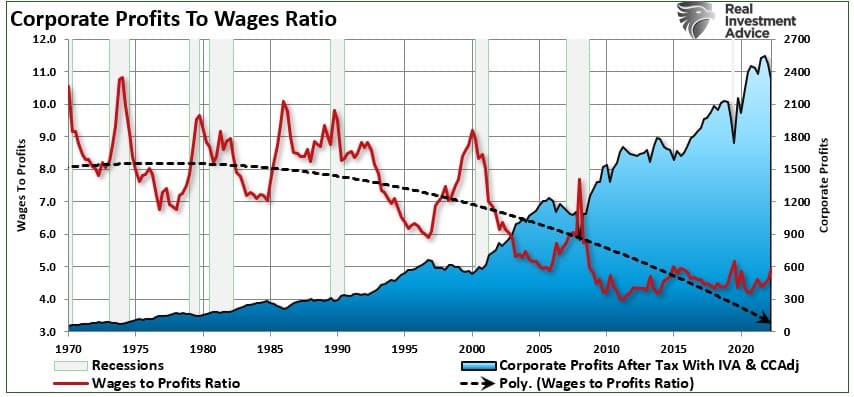

The problem is that these tools create a mirage of corporate profitability. None of these tools increase revenue growth which comes from economic activity. An excellent way to visualize the issue is the two charts below, which compare corporate profitability to the number of workers and wages.

It is worth noting that when the profits-to-wages ratio starts to spike higher, as it is currently, such aligns with economic recessions. Not surprisingly, during recessionary periods, corporations act to protect profitability by reducing wages and the labor force (the highest costs to any business.)

As shown above, outside of the labor force and wage controls, corporations have heavily engaged in share buybacks to increase earnings per share for reporting purposes.

The problem with this, of course, is that stock buybacks create only the illusion of profitability. If a company earns $0.90 per share and has one million shares outstanding – reducing those shares to 900,000 will increase earnings per share to $1.00. No additional revenue was created, and no more product was sold; it is simply “accounting magic.”

Such activities do not spur economic growth or generate real wealth for shareholders, but they boost asset prices to increase executive compensation.

It is unsurprising why the “wealth gap” between workers and executives has soared since the financial crisis.

Profit Margins At Risk

Now that you understand how companies manipulate their bottom line earnings to win the “Beat The Estimate Game,” there is only so much they can do in a higher interest rate environment weighing on consumption. My colleague Albert Edwards from Societe Generale had a great note out this week on the risk to earnings and profit margins.

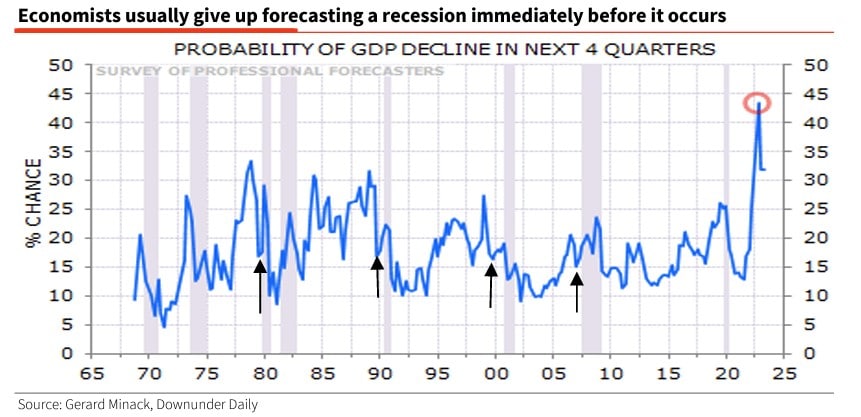

“The over-anticipation of an imminent recession last year helps account for the snap back in equities this year. Our excellent cross-asset derivatives strategist, Jitesh Kumar, pointed out the great chart below from JP Morgan (H/T @dailychartbook on Twitter) showing that, within the equity market, belief in a cyclical upswing is really taking a firm grip. That chart certainly suggests that investors believe the threat of recession has passed.

But if you take a closer look at Gerard Minack’s chart, one thing is clear – economists having apparently got their recession call wrong, always give up on it just at the point when it arrives. Indeed, I can remember even I, an uber bear, finding myself doubting my own recession forecast as we went through 2007.“

Of course, if Wall Street economists are giving up on the idea of a recession, then analysts start upgrading earnings estimates in anticipation of more robust growth. To wit:

“Surely, just as night follows day, once analysts start upgrading their profit forecasts, better times lie ahead for the corporate sector. No wonder equities are rallying.”

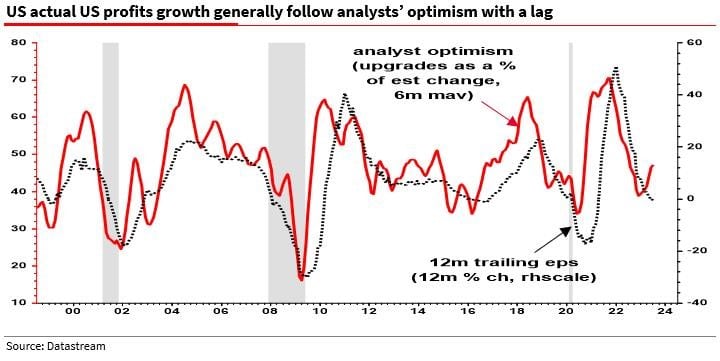

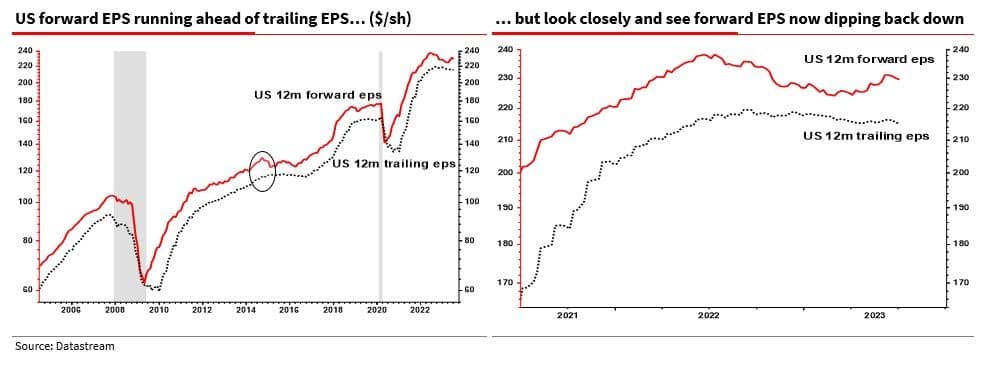

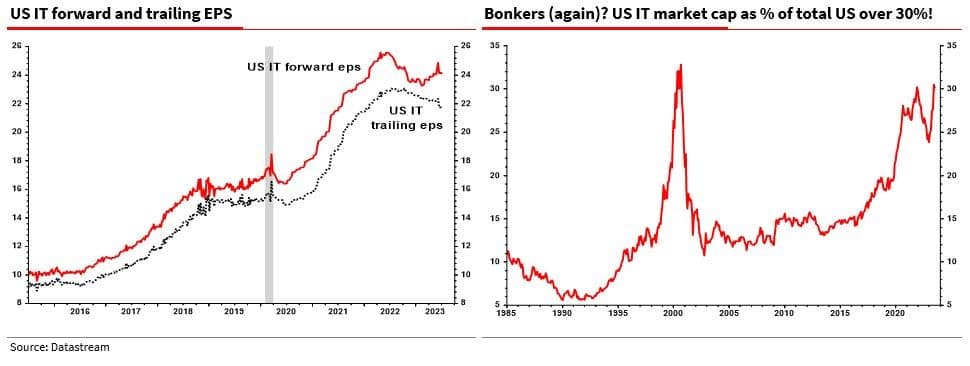

“So, let’s look at what is happening to analysts’ 12-month forward EPS forecasts and trailing EPS. You can see below left that forward EPS (red line) has indeed begun to rise again but trailing profits (dotted line) have barely moved. Homing in on the most recent data (right-hand chart) it looks to me as if analysts’ forward EPS forecasts may be rolling back down. And looking at 2014 on the left-hand chart, we see that rising optimism among analysts is not always to be trusted.”

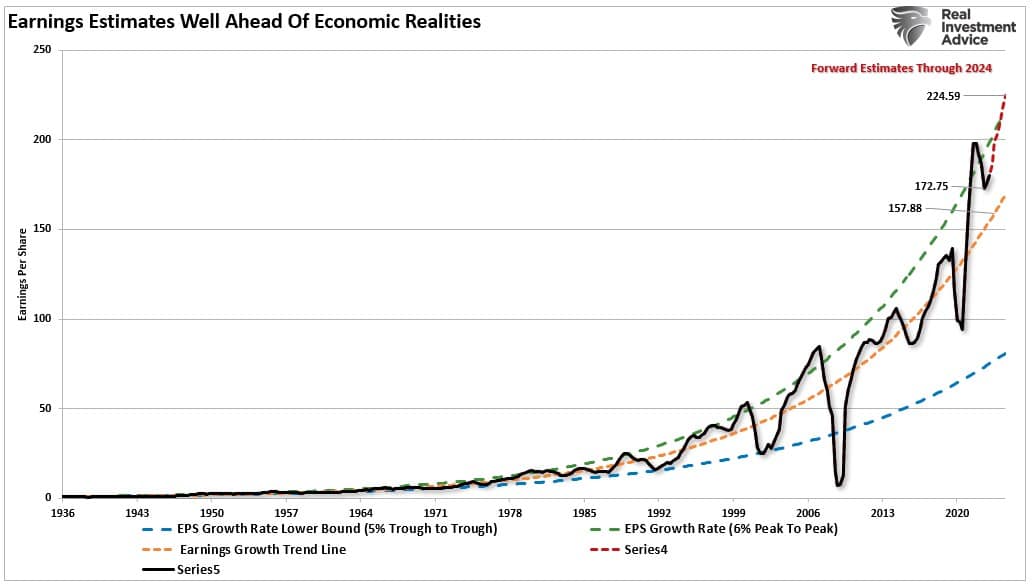

As noted above, while analysts have raised future earnings estimates, the underlying data does not necessarily support such. More importantly, there is a limit to how much companies can “massage” the bottom-line earnings if top-line sales growth slows. As higher rates continue to weigh on consumption, particularly in a highly indebted economy, the risk of a slowdown in sales remains elevated. If that statement is valid, the earnings must decline to align with organic economic activity. Such is why, historically, a reversion eventually occurs when earnings are well deviated above the long-term growth trend.

While anything is certainly possible, the surge in analysts’ estimates since the end of 2022 seems based more on “hope” than economic realities. The correlated rise in equity prices has logically followed suit, such as Alberts concluding point.

“The US tech sector has surged on the back of what may prove to be nothing but hope – mainly AI related. Actual earnings are poor in absolute and relative terms. Yet the sector is again over 30% of total market cap. Of all the strange things I have seen over the years, that looks simply nuts.”

Something worth considering.

How We Are Trading It

Despite the Federal Reserve becoming more vocal about the need for further rate hikes, investors mostly ignore higher real rates, which will eventually impact growth stocks. However, such can last longer than logic would suggest. Therefore, we remain bullishly positioned near term but do not dismiss the risk of “something breaking.”

The current challenge is aligning equity exposures with a more bullish market outlook while maintaining some measure of risk controls. As noted last week,

“We remain underweight in overall equity exposure and overweight in defensive, value-oriented positions. Such will protect the portfolio from any short-term market declines, at which time we will use our existing cash holdings to increase our cyclical exposure accordingly. However, that defensive posture is penalizing our performance this year after last year’s significant outperformance. We suspect we will get an opportunity, particularly as we move into 2024, to make up that performance gap and rebalance risk tolerances accordingly.”

That challenge remains, but we wait patiently for a better risk/reward entry point to make appropriate changes. We hope we get that opportunity sooner rather than later.

Let me reiterate our rules from last week as we head into the potential “summer malaise.”

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against potential market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings.

Have a great weekend.

The full report will return next week.

Lance Roberts, CIO, RIA Advisors

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates (Formerly 3-Minutes)

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

Will Return Next Week

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O.

Have a great week!