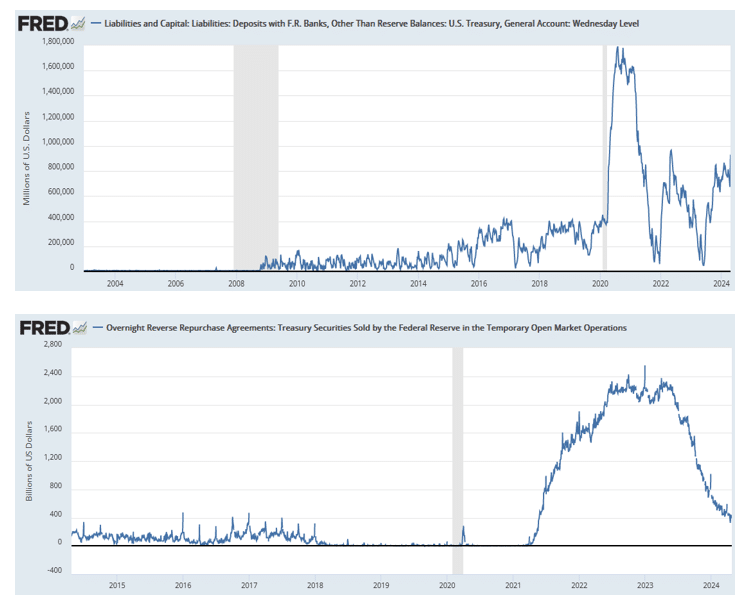

Treasury Cash Soars Providing A Liquidity Reprieve

The U.S. Treasury now has $930 billion in cash in its Treasury General Account (TGA) held at the Federal Reserve. The influx of cash into the Treasury account at the Fed is the result of April 15 tax payments. As shown in the top graph, this is the third highest level it has been and is still increasing. So you are probably asking why I should care. For starters, the surplus of cash means the Treasury can draw from the funds in its Fed account and, therefore, issue fewer Treasury bills, notes, and bonds. For context, in its latest borrowing estimate, the Treasury expects to borrow $202 billion between April and June. That is well below their expectations of $760 billion for the first quarter.

The importance of issuing fewer securities is that it should provide a temporary boost to liquidity. Our best gauge of excess liquidity is the Fed’s Reverse Repurchase Program (RRP), shown in the lower graph. At its peak, RRP was over $2.4 trillion. However, it dipped below $400 million as the excess liquidity is rapidly leaving the system. Further, excess liquidity fell at a quicker pace into the April 15 tax payment date as investors withdrew cash from money markets to pay their taxes. Now, the money sits in the TGA, and the liquidity will essentially return as the Treasury issues fewer securities. Consequently, this should stall the decline in the RRP for a couple of months. However, come June or July, the RRP will likely start declining, and with it, we should be on alert for new liquidity problems, barring any actions from the Fed between now and then.

What To Watch Today

Earnings

Economy

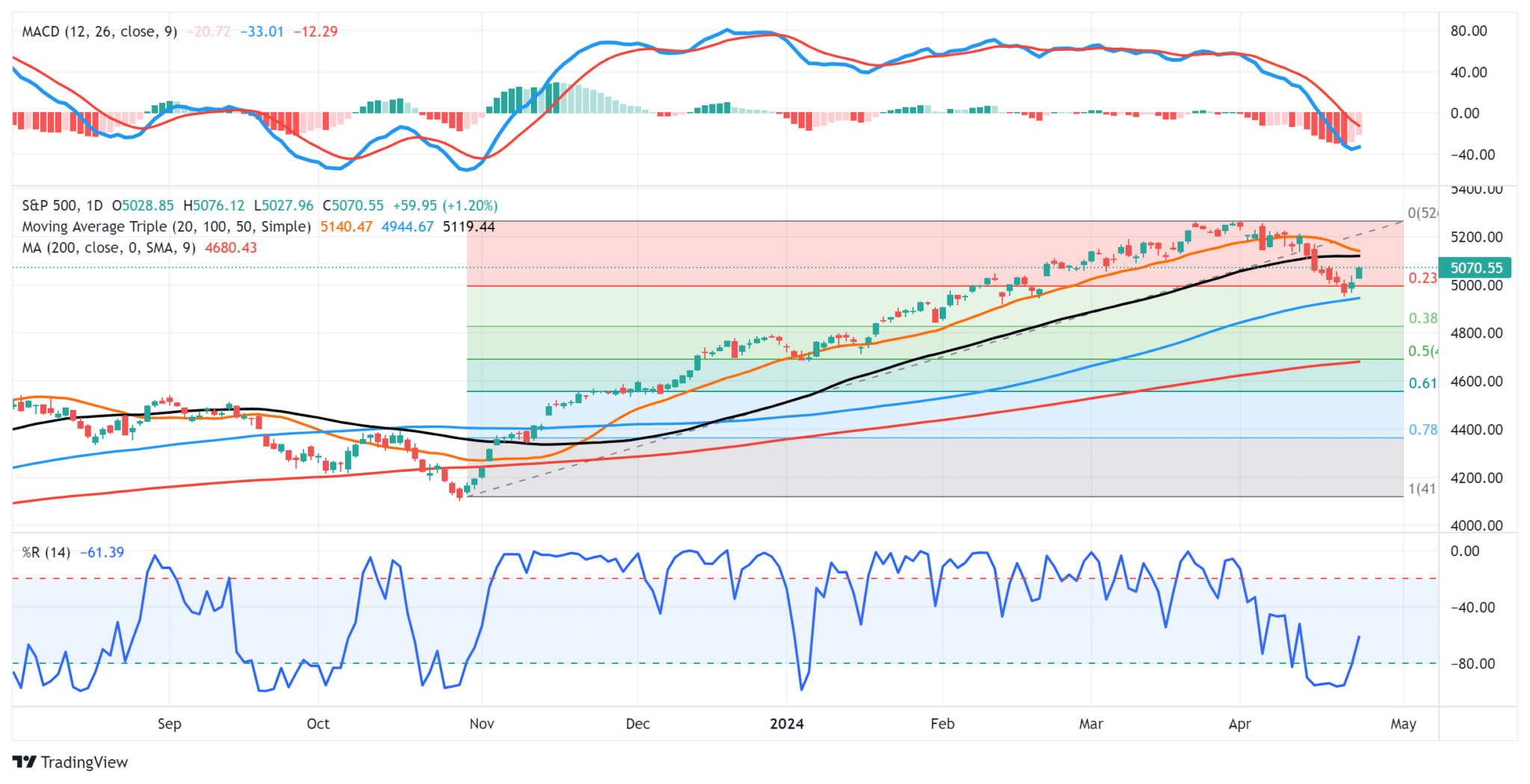

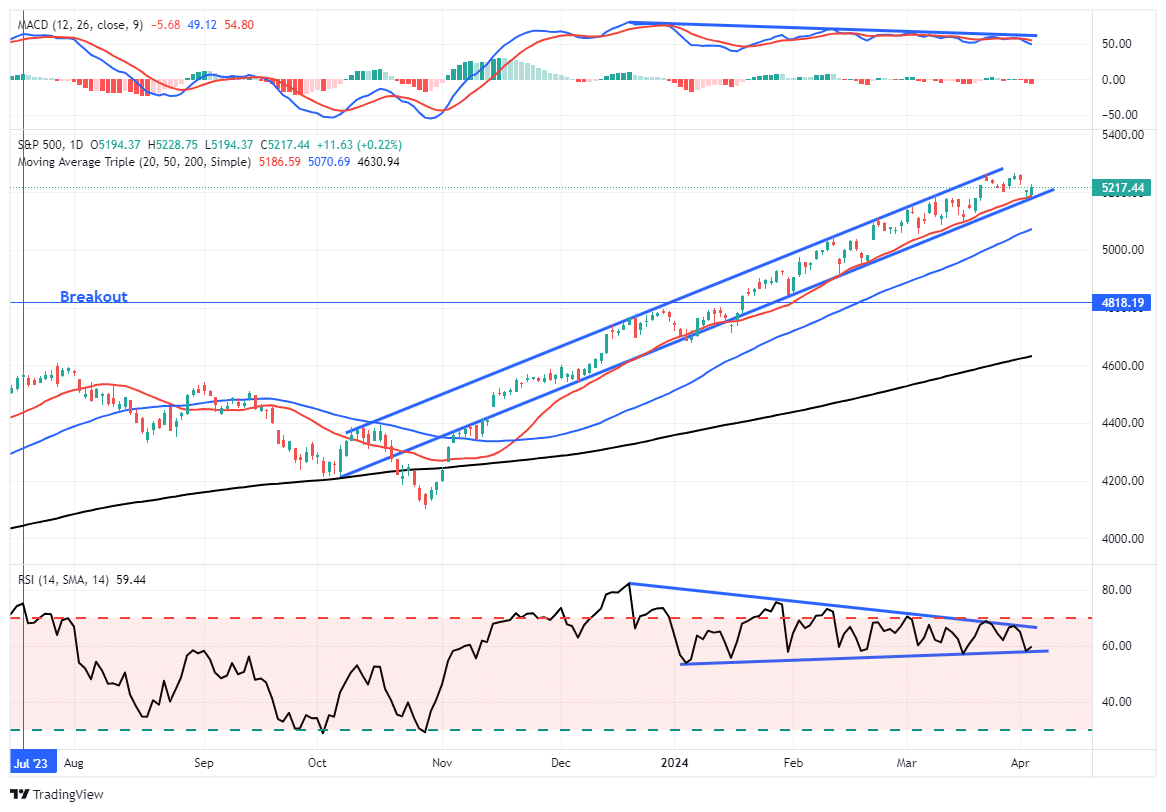

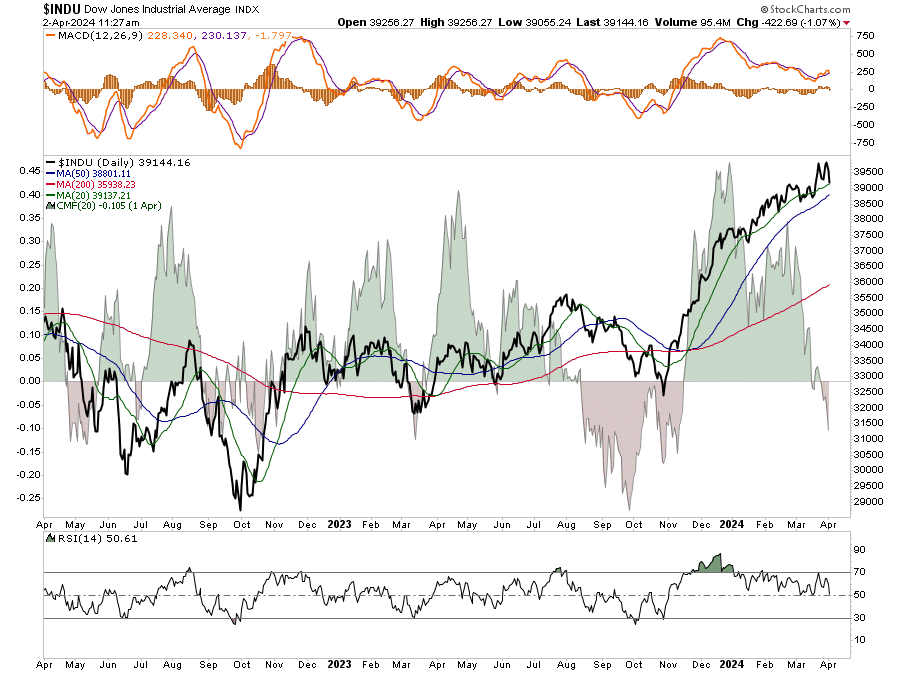

Market Trading Update

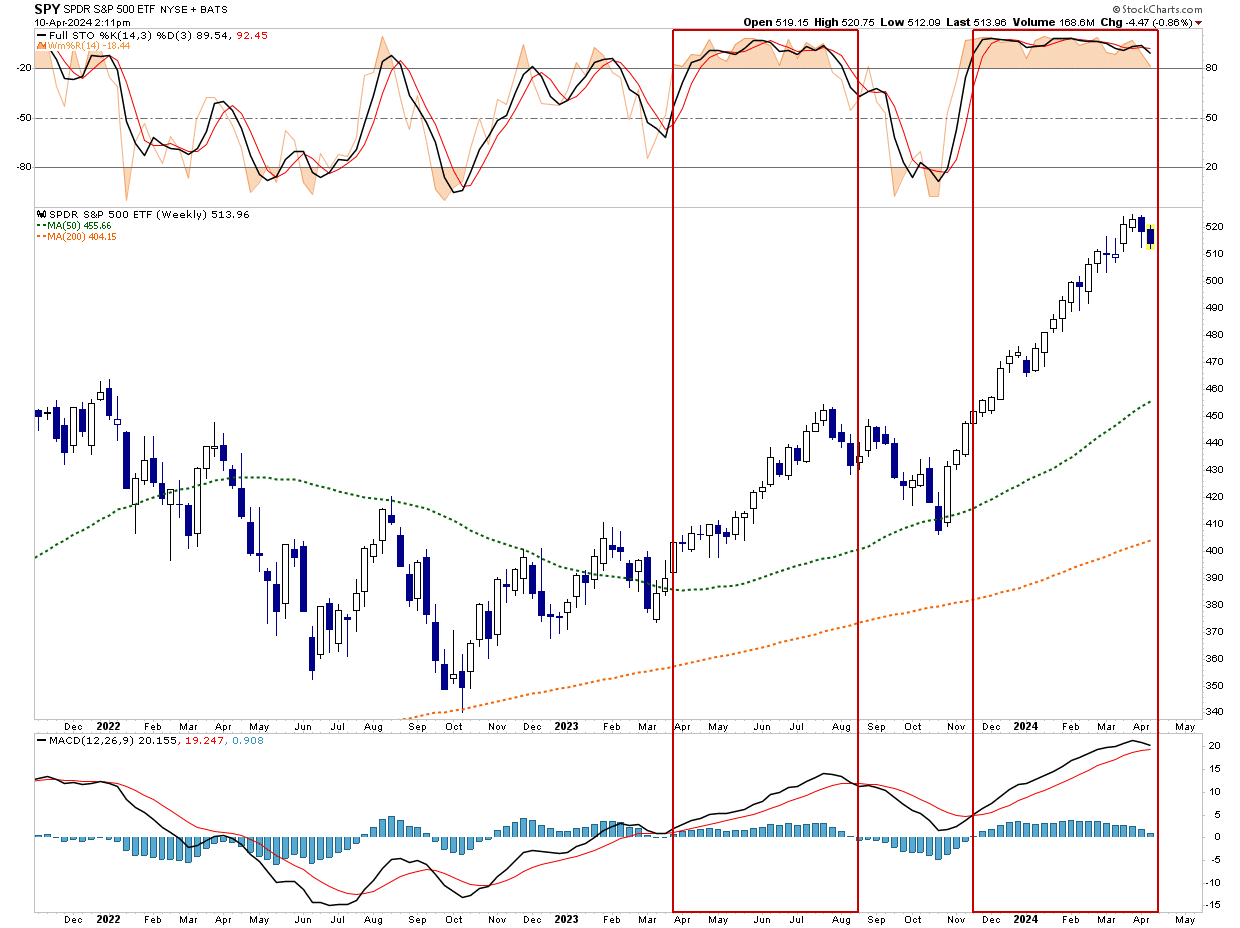

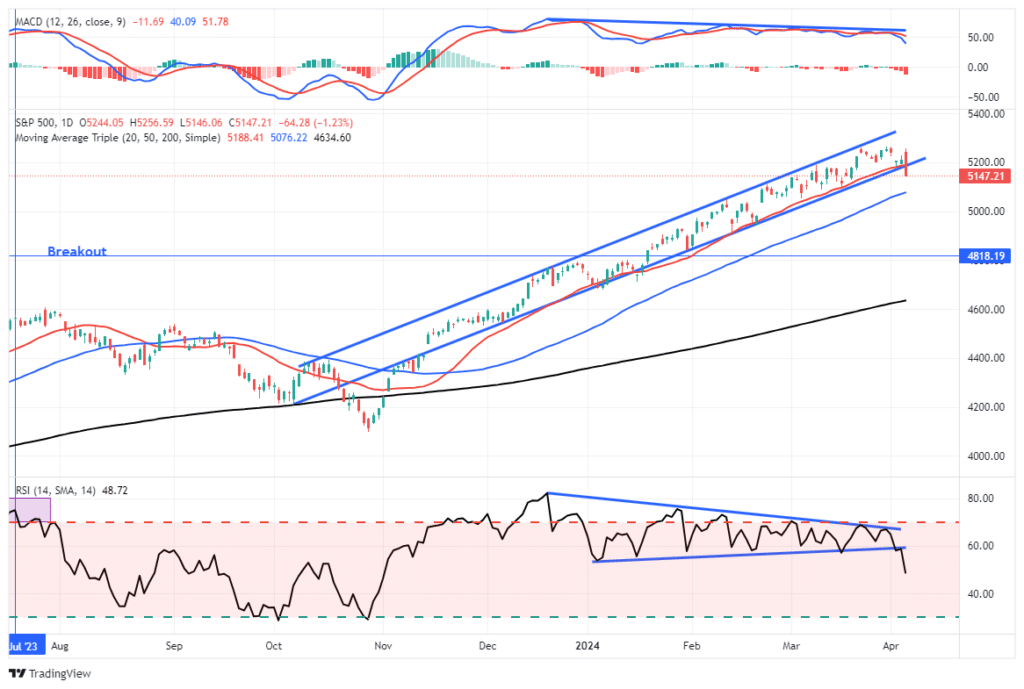

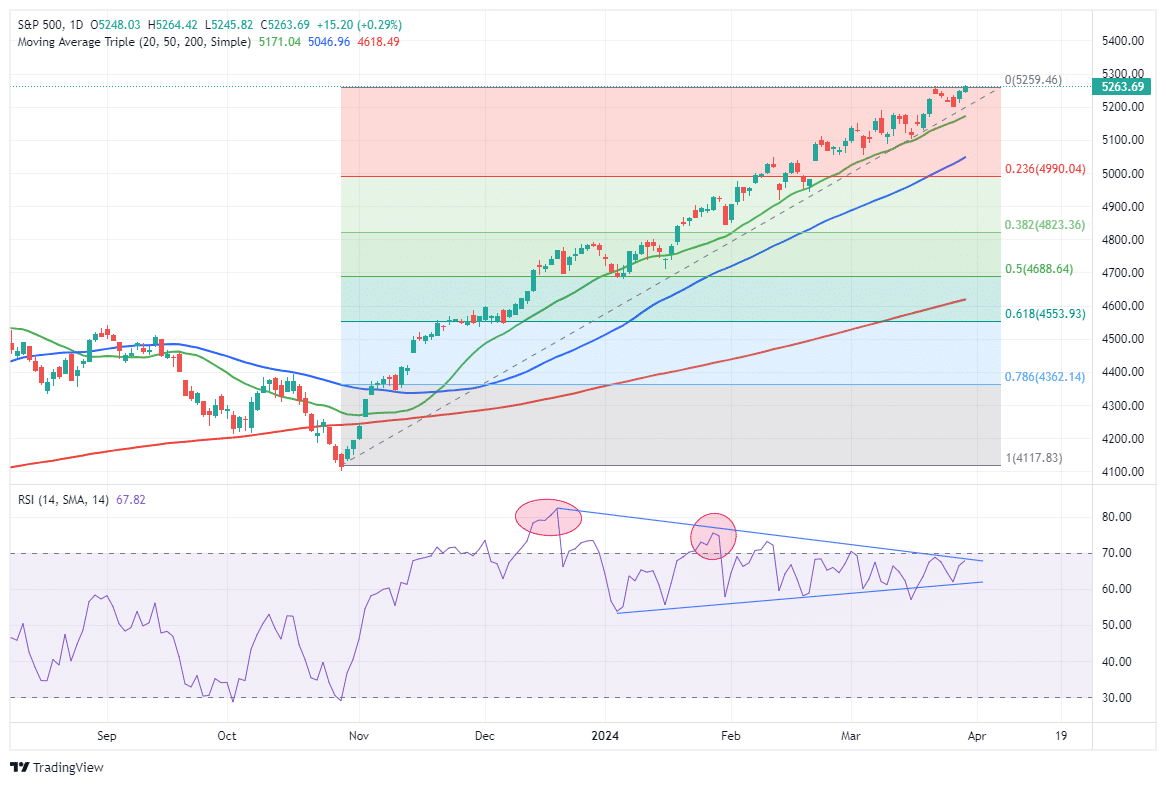

As noted yesterday, the market is in a reflexive rally, likely limited to initial resistance at the 50-DMA. However, as noted, there isn’t significant buying volume until between 4700-4800, which coincides with a retest of the 200-DMA. While the market did sell off some yesterday morning, we saw buying in the late afternoon to bring the market back to even. However, Meta (META) missed earnings after the close and will likely add some selling pressure to the market today. If the market can shrug off the impact of META and rally, then this rally likely still has some life left in it. However, I suspect we are getting closer to the end of this initial reflex, and we will likely see some further liquidation before the next buying opportunity arrives. Tread cautiously for the moment.

Tonight’s NFL Draft Speaks Teaches Us About Investor Behaviors

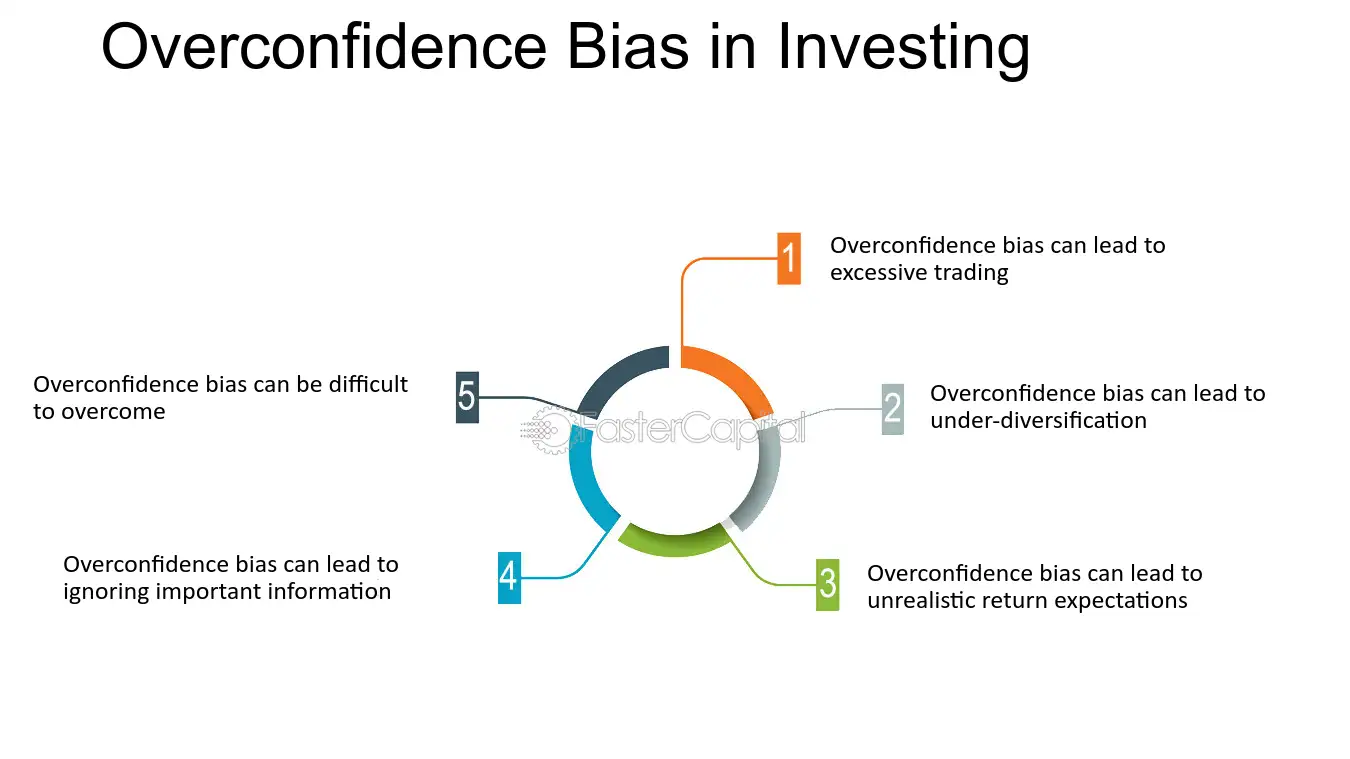

Tonight, the NFL will hold its annual draft. Especially notable in this draft is that four quarterbacks are likely to go in the top five picks. The GMs selecting these quarterbacks must be very confident they have the ability to draft a top-ten NFL quarterback. While many experts say this quarterback class is a sure thing, history shows that first-round quarterbacks are often busts. Not only are GMs overconfident in their selection abilities, but they suffer from groupthink. It turns out first first-round quarterbacks selected since 2011 have produced a sub-500 win/loss record.

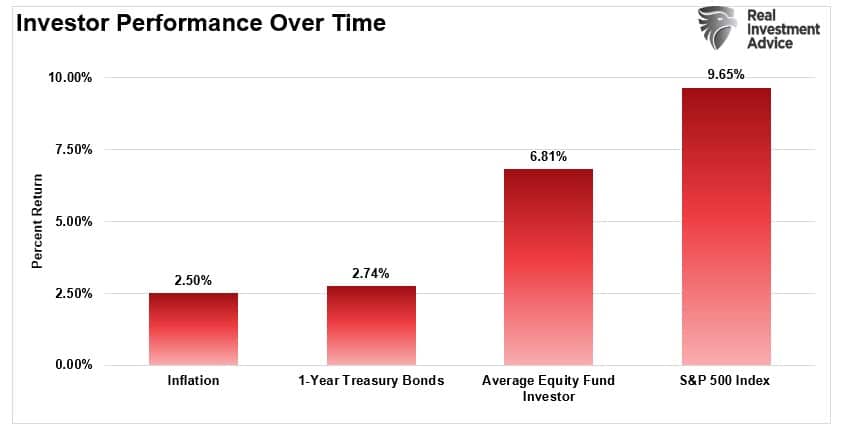

We quantified the odds of GMs picking above-average quarterbacks earlier. Per DFA Funds, the odds of an investor outperforming the market are even more daunting.

We saw from the data above that an investor has about a 75% chance of underperforming the market in any given year, which means you have a 25% chance of beating the market in any given year.

The message to take away from that statistic is to leave your confidence at the door!

In addition to pointing out similar traits to help you appreciate your investment biases, we also share some tools to combat as follows:

Zig, while others zag

Take profits

You have options

Let winners run

“Most importantly, remember that you are only human. The Patrick Mahomes of the investment world are few and far between. At times, overconfidence is a good trait, but it can also be a critical flaw.“

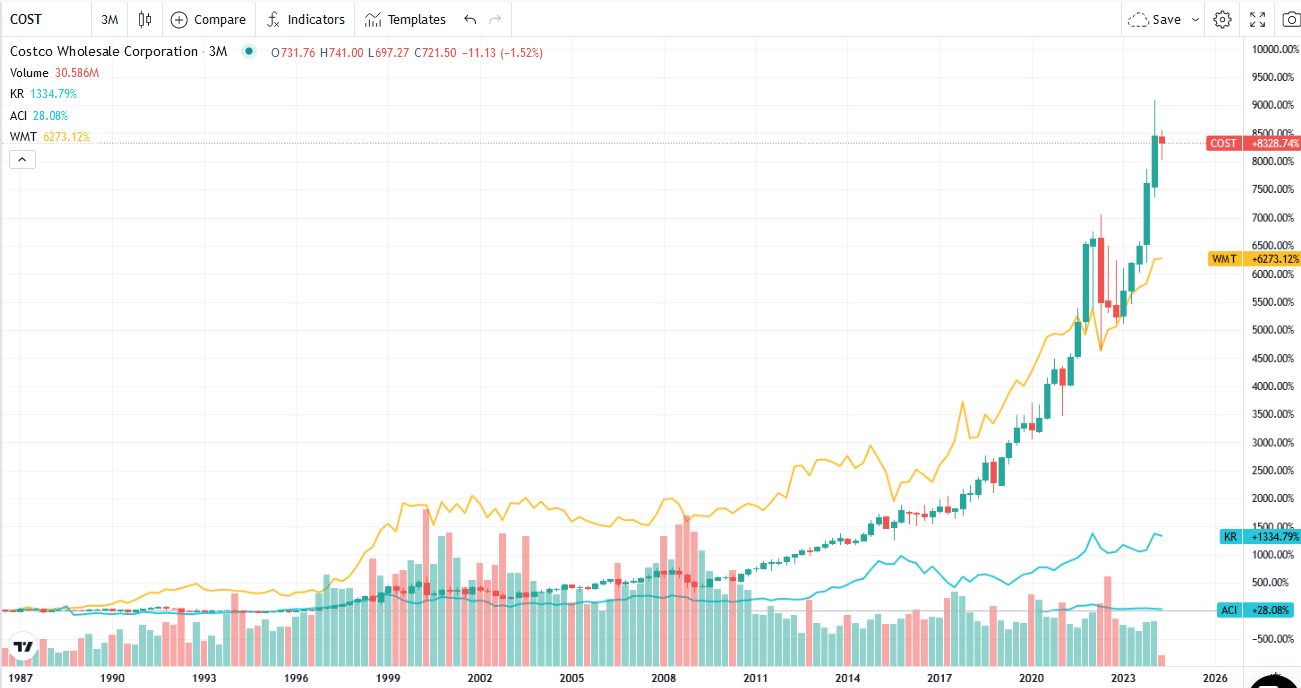

Costco’s Biggest Loss Leader Is A Winner

In 2023, Costco sold 137 million rotisserie chickens and 156 million hot dog combos. The prices, $4.99 for the chicken and $1.50 for the hot dog combo have remained the same for over 25 years. Therefore, you might be asking how they profited from this. They don’t. In fact, last year, they lost over $50 million on rotisserie chickens.

Costco uses chickens and hot dogs as loss leaders. In addition, the company spends significant effort and dollars quantifying its sales, margins, and returns. In the case of chickens, they can determine how receipts containing a chicken led to other sales and contributed to its return on investment. The chart below shows Costco’s (COST) stock, handily beating the top two grocery chains (Krogers and Albertsons) and Walmart.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Overconfidence In NFL Drafts: A Lesson For Investors

Most NFL general managers (GMs) are optimistic and displaying overconfidence today as they prepare for tomorrow’s NFL draft. The draft is a once-a-year opportunity for GMs to acquire talent.

Like investors, GMs often think they are smarter than their competitors, aka the market. Yet, they frequently have similar mindsets and follow the same narratives that drive their competition.

As we will share, overconfidence and groupthink among football GMs and investors are behavioral flaws that often harm performance. Having the tools and strategies to mitigate our behavioral traits is extremely valuable and can lead you to better returns.

Overconfidence In The NFL

Four of the first five picks in the draft are expected to be quarterbacks. Not only is the quarterback the most important position on the field but this year’s draft is hyped as having several future greats.

Based on data from Warren Sharp, an NFL analyst, most of the quarterbacks taken in the early rounds will be average. His Fox Sports article entitled The success rate of first round QBs makes Lamar Jackson’s case for him, quantifies just how poor the odds are of drafting the next Super Bowl-winning quarterback.

There have been 38 quarterbacks drafted in the first round since 2011, the year the NFL changed the collective bargaining agreement.

These 38 first-round quarterbacks have made a total of 1,909 starts. Their record? 1034-1035-7.

He claims that of those 38 quarterbacks, only one, Patrick Mahomes, has won a Super Bowl. Furthermore, of the 28 from that group who are no longer on their initial contracts, the average time they were a starter was a mere 3.4 years.

Despite the proven mediocrity of quarterbacks taken in the first round, we have little doubt that overconfidence will be on full display by the GMs drafting quarterbacks with their top picks after they make their selections.

Groupthink In The NFL

This behavioral trait arises when people seeking conformity think and act similarly. Typically, groups reach a consensus opinion without proper evaluation and with minimal alternative viewpoints.

For instance, it is widely accepted that the four quarterbacks likely to go in the top five, Williams, Daniels, Maye, and McCarthy, will be excellent pros. Most NFL analysts offer differences between the quarterbacks but praise the physical and mental traits they believe will make them NFL starts. Very few analysts have poor ratings on any of those four quarterbacks.

Choosing one of the four quarterbacks is comforting. Simply, GMs have cover if their pick is a dud. Who could have known? Every expert thought he would be a superstar!

Investor Overconfidence And Groupthink

Replace players with investment ideas and GMs with investors. The overconfidence and groupthink mentality impacting GM draft day decisions are similar to those investors always face.

We quantified the odds of GMs picking above-average quarterbacks earlier. Per DFA Funds, the odds of an investor outperforming the market are even more daunting.

We saw from the data above that an investor has about a 75% chance of underperforming the market in any given year, which means you have a 25% chance of beating the market in any given year.

The message to take away from that statistic is to leave your confidence at the door!

Regarding groupthink, most investors, like GMs, find comfort in knowing that many other investors are doing the same thing. Market narratives are a form of groupthink. Narratives help explain market movements and trends. Often, a narrative develops after a trend has started. In other words, rightly or wrongly, the narrative is the rationale.

Today, narratives appear to be quicker to form and longer lasting. Maybe the advent of social media has allowed for their quicker dissemination and growth.

Narratives describe the mindset of a group of investors. When you unknowingly invest based on a narrative, you are likely setting yourself up for failure.

Strategies To Combat Behavioral Traits

Appreciating that GMs have a one in three chance of successfully using a precious top-five draft pick on a quarterback or that only a quarter of investors will beat the market, we best have tools to manage our behavioral traits and improve our odds of success.

Zig

Warren Sharp advises GMs to “zig while others zag.”

To zig is to have a contrarian mindset. For instance, it’s important for your portfolio to have popular stocks leading the market higher. But at the same time, understand that confidence can wane quickly, and a new set of stocks will take the throne soon enough. Don’t overstay your welcome in a narrative.

It wasn’t that long ago that the Magnificent Seven stocks were all the rage. Their returns handily beat almost every stock and index. Holding a meaningful subset of the seven stocks was vital to keep up with the broad market indexes. However, the Magnificent Seven’s period of outperformance has either ended or is on pause. But, the narrative still thrives, and whether it’s already happening or will occur shortly, investing in the aged groupthink will catch many investors offside.

Take Profits

It’s hard to sell when others are buying. Still, when the narrative-driven stocks fall out of favor, the prior profits and reduced position sizes will bolster returns and lessen the risk of underperforming the market.

Appreciating what the market, and not popular narratives, tell you is equally vital. For instance, have you noticed that utilities and energy are the best-performing sectors lately? Those solely holding the Magnificent Seven and neglecting other sectors are falling behind.

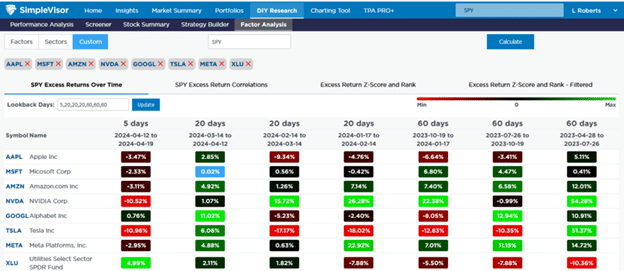

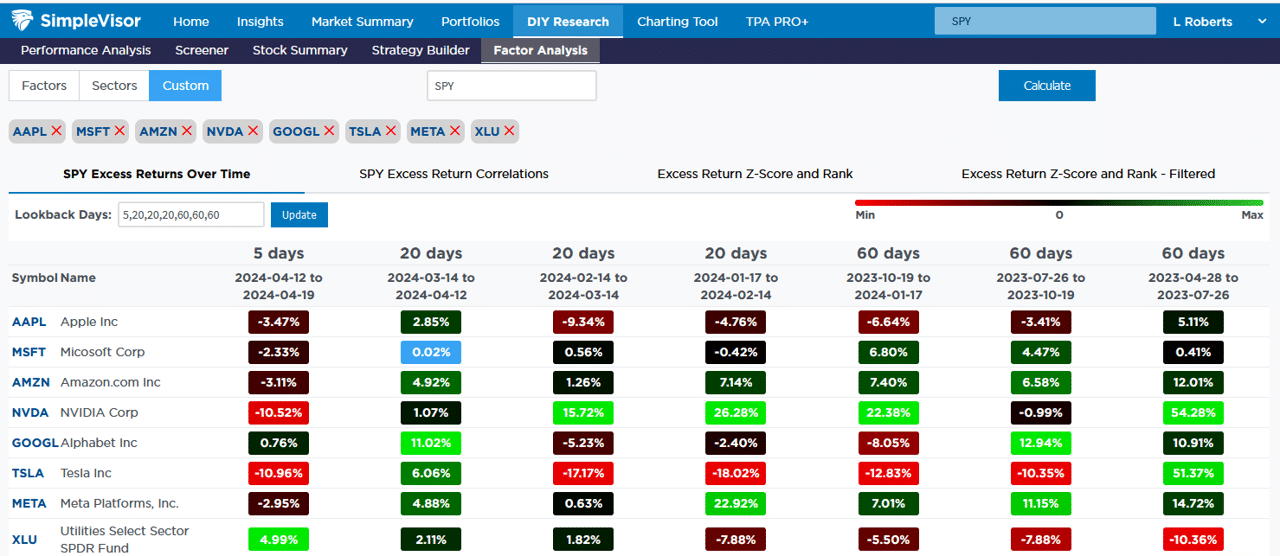

The SimpleVisor table below shows the relative performance of the Magnificent Seven stocks and XLU, the utility ETF, versus the S&P 500 over various time frames. Other than NVDA, most of the seven have been underperforming the market as of late. Also, the once poorly performing utility sector has been beating the market for the last 45 days. Selling the Magnificent Seven 45 days ago to buy utilities would go against groupthink, but it was a smart call.

Appreciate Your Options

The GMs with the top five picks have a precious option. Instead of picking a quarterback with limited odds of success, they can trade the pick to another team. In exchange, they might receive multiple high-level draft picks, boosting the odds of success.

Other positions in the NFL draft have much better success rates than quarterbacks. If a GM can set aside their confidence in their ability to pick the right quarterback, they can increase the odds that they could easily land at least two very good players and possibly a pro bowler. Maybe they can even use one of the picks to get a quarterback in the later rounds. Let’s not forget Brock Purdy, the San Francisco quarterback who led the 49ers to the Superbowl, was Mr. Irrelevant, the last person taken in the draft.

Investors have options, too. Many stocks, sectors, and factors will likely outperform the market but do not fit the narrative du jour. While buying what others aren’t may be uncomfortable, it may be more profitable.

The other lesson is to diversify. Putting most of your eggs in one basket can significantly impact your relative performance. You will underperform if you are proven wrong, as is most common.

Let Winners Run

One of the most popular Wall Street sayings is, “Cut your losses short and let your winners run.”

If our chances of beating the market are one in four, doesn’t it make sense to trade your portfolio actively? Many investors do the opposite. Their confidence and the attraction of groupthink keep them in underperforming stocks. At the same time, alternative stocks that are less followed may be the best bets.

It can be appropriate and profitable at times to follow the crowd. However, at all costs, don’t ignore alternative views.

Summary

We risk underperforming the market by falling victim to our natural behavioral traits. Therefore, we owe it to ourselves to entertain and understand alternative views. As odd as it may seem these days, we need to watch FOX News and read the New York Times. We must challenge ourselves to understand better things that may not be comfortable.

Seek out and study the views of others with whom you disagree. By better understanding opposing opinions, you will strengthen your existing views or better recognize flaws in your current logic. Either way, an investment thesis is better for it.

Most importantly, remember that you are only human. The Patrick Mahomes of the investment world are few and far between. At times, overconfidence is a good trait, but it can also be a critical flaw.

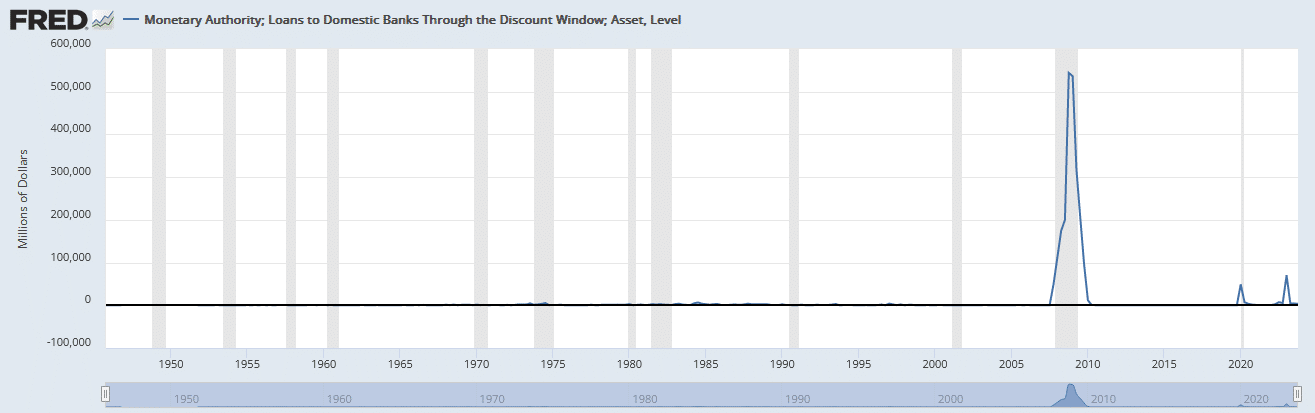

Bank Rule Changes To Help Fund The Deficit

The Wall Street Journal posted an article on bank rule changes entitled A Century-Old Lending Lifeline for Troubled Banks Has a Major Flaw. The Fed Wants to Fix It. The article discusses the Fed’s Discount Window and rule changes to bolster banks in times of need. This bank safety will also conveniently help the Treasury fund the deficit. The Fed’s Discount Window is a direct borrowing line for banks experiencing a cash crunch. It is infrequently used because it signals to banks, depositors, and stockholders that the bank is in trouble. The graph below shows the discount window was used extensively during the financial crisis. Besides two other smaller instances, it has barely been used.

If enacted, the new bank rules would force all banks to “preposition billions more in collateral” at the Fed to support future discount window borrowing. The article estimates that the Fed would require collateral matching up to 40% of a bank’s uninsured deposits, accounting for about 45% of the $17.5 trillion commercial bank deposits. Further, the new rules would require the banks to borrow from the window numerous times a year to help remove the program’s stigma.

In addition to bolstering the banking safety net, it would also force banks to hold significant collateral balances at the Fed. Collateral for Fed loans is quite often U.S. Treasury securities. Accordingly, this new bank rule is another way to help the Treasury fund its massive deficits and stock of outstanding debt from years past. This is just one plan for the Fed to help the Treasury fund its growing debts. Our Commentary about QE Light sheds light on a second rumored proposal.

What To Watch Today

Earnings

Economy

Market Trading Update

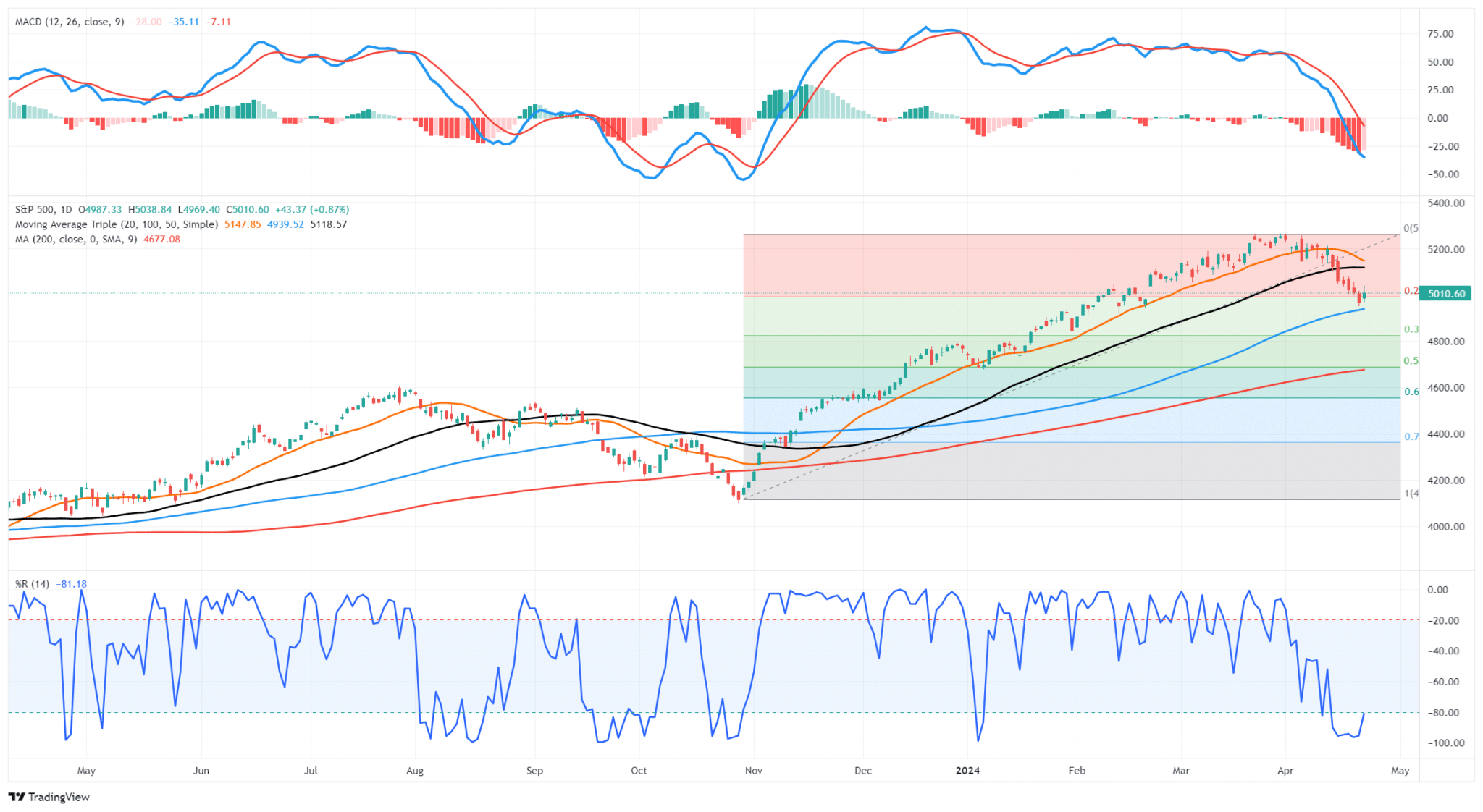

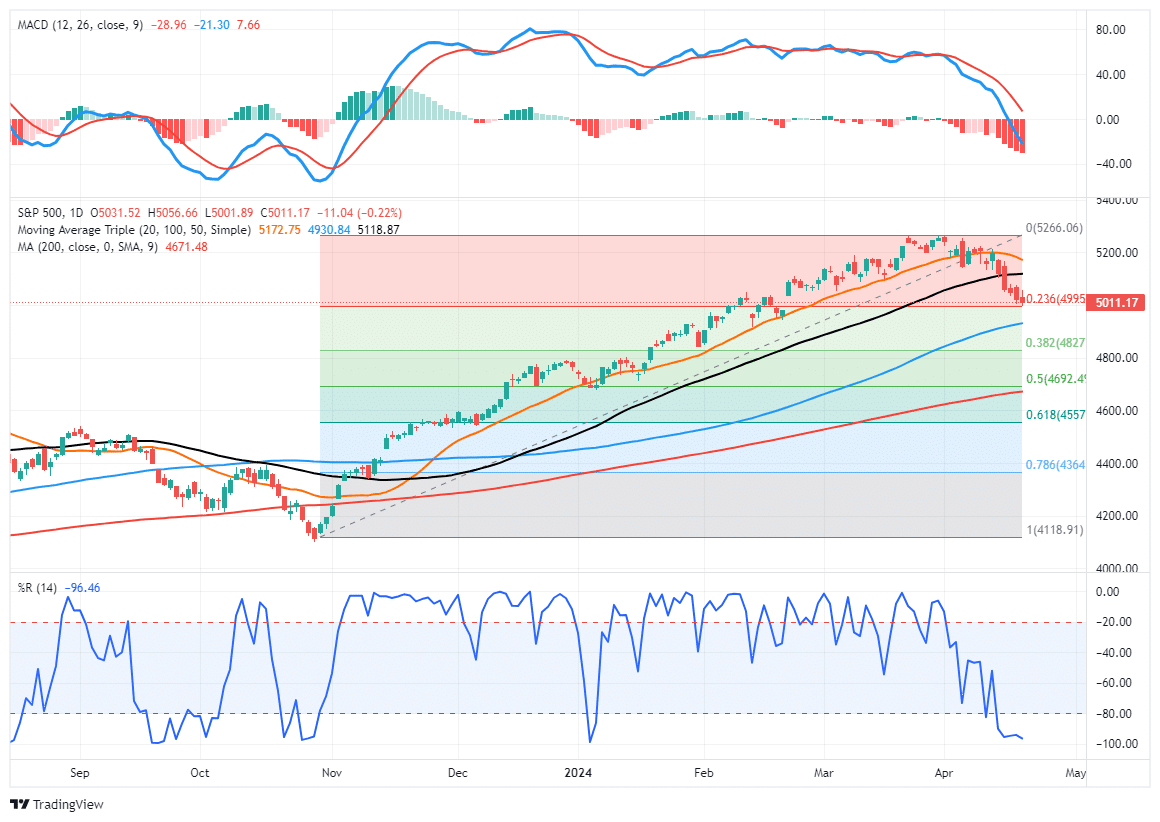

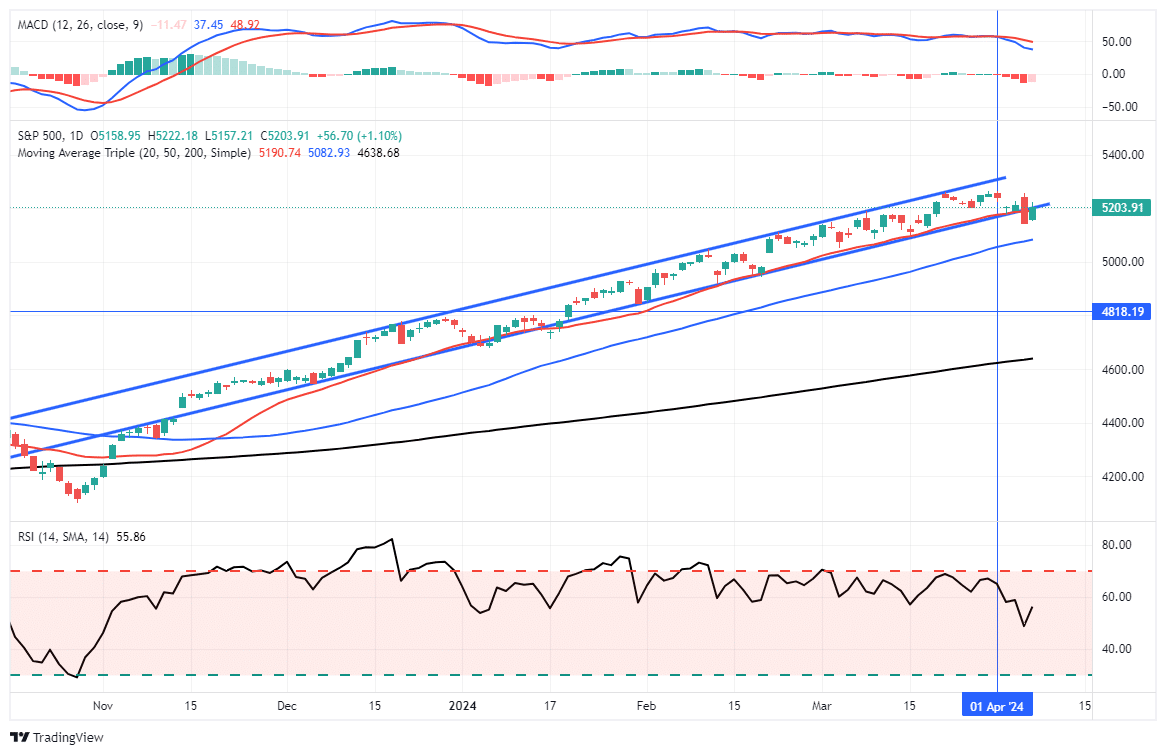

As discussed yesterday, the reflexive rally remains intact, bouncing nicely off support at the 100-DMA. The market has not returned to overbought, so a further rally toward the 50- and 20-DMAs remains possible. From a bullish perspective, the 5.5% pullback was needed to “reset” the market following an exhaustive rally from the October lows. An attempt at previous highs is likely if the market can clear resistance. However, I suspect that we will likely see a retest of some support before that final push higher happens. Continue to remain long equities and look for opportunities to add to positions opportunistically. When the MACD issues its next buy signal, it will coincide with an improvement in the overall market and provide a better entry point for investors.

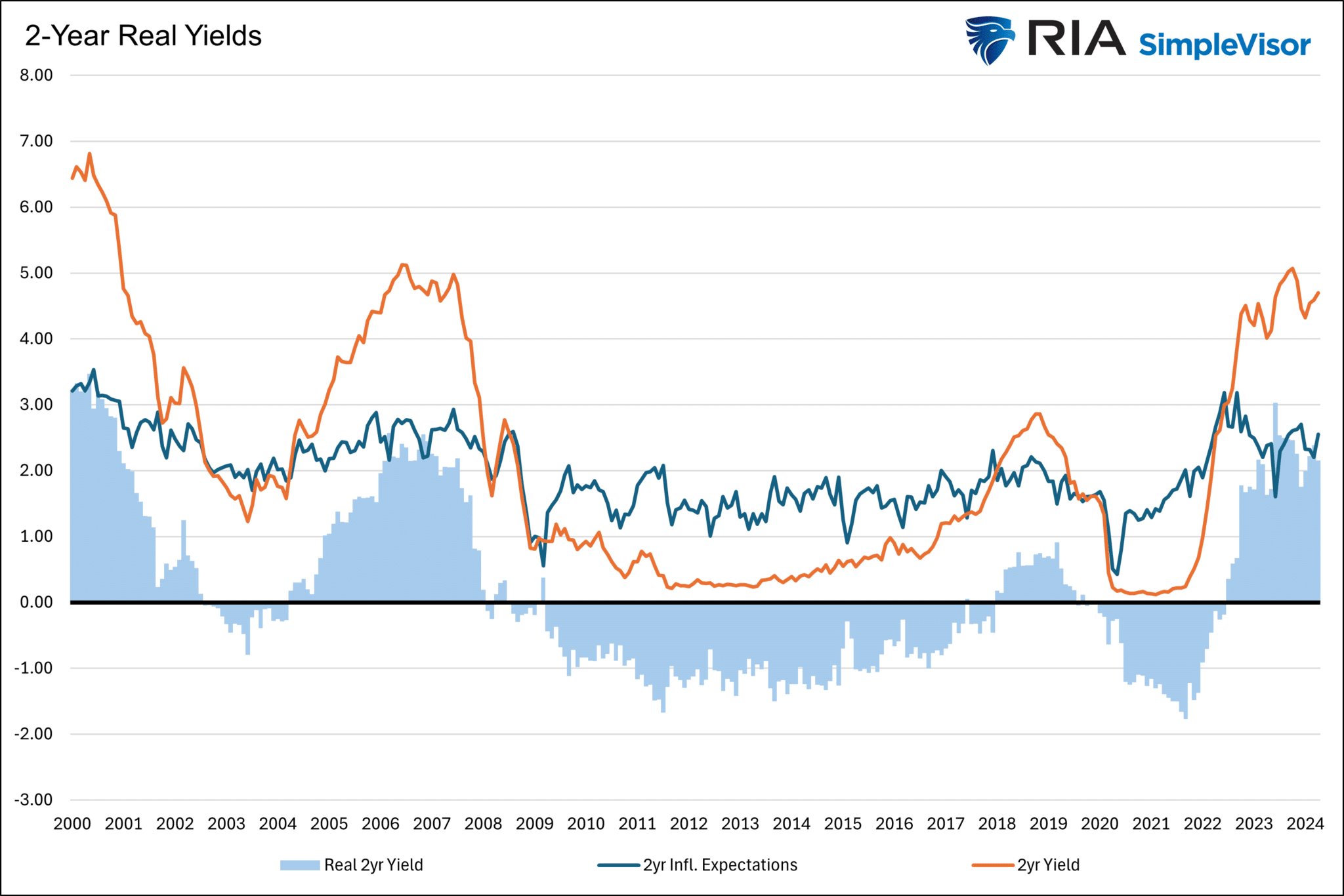

Yields and Inflation Expectations

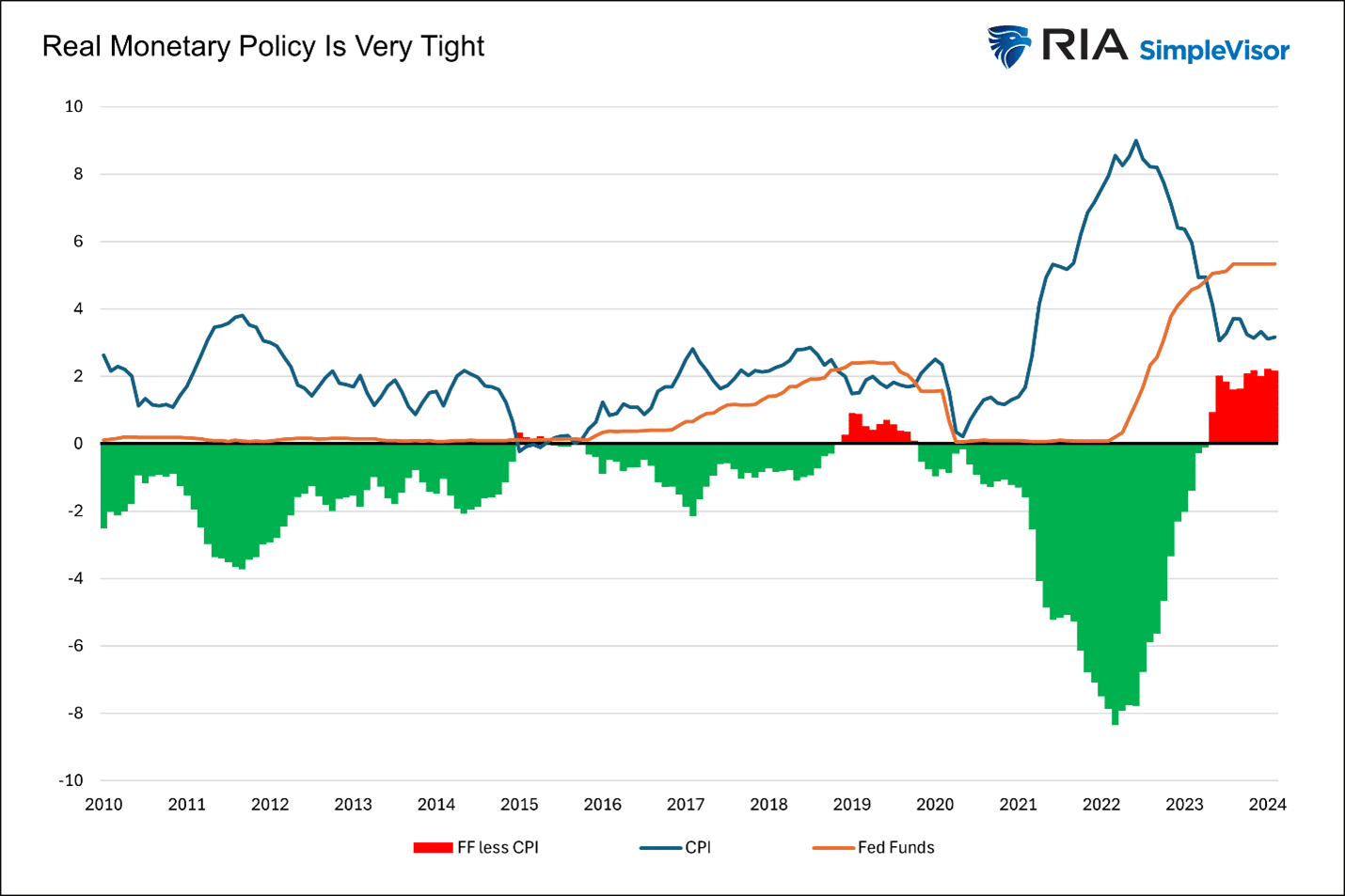

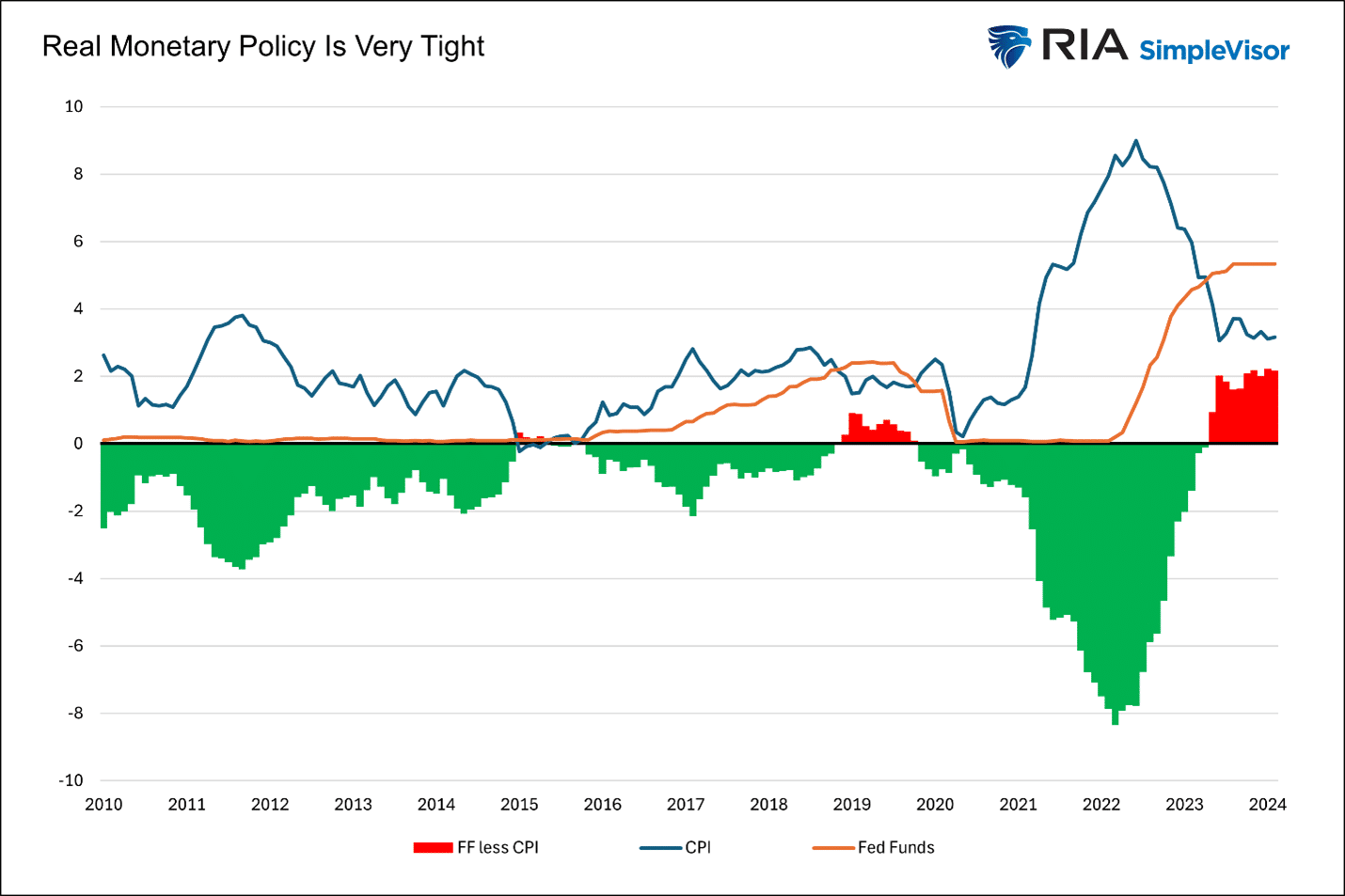

The Fed pays close attention to inflation expectations and the real yield on Treasury securities. One of their recent concerns is that higher inflation expectations result in consumers and corporations buying today instead of tomorrow because they fear prices will rise. Real yields, or the difference between the current yield and inflation expectations, tell the Fed how restrictive or easy their policy is. The graph combines all of this to help us appreciate the Fed’s mindset.

Inflation expectations have risen from mid-2023 lows and are about half a percent higher than the ten years leading to the pandemic. However, despite expectations only being .50% higher, the two-year yield is about 4% higher than that same ten-year period. As a result, 2-year real yields are over 2% and on par with those in 2007. The graph helps explain why the Fed is ok with cutting rates despite the strong economy and higher inflation. Essentially, with inflation expectations stable, albeit higher than they prefer, real yields are too high. The economic headwind from such a high real yield will be problematic in time. The Fed wants to get in front of that potential problem.

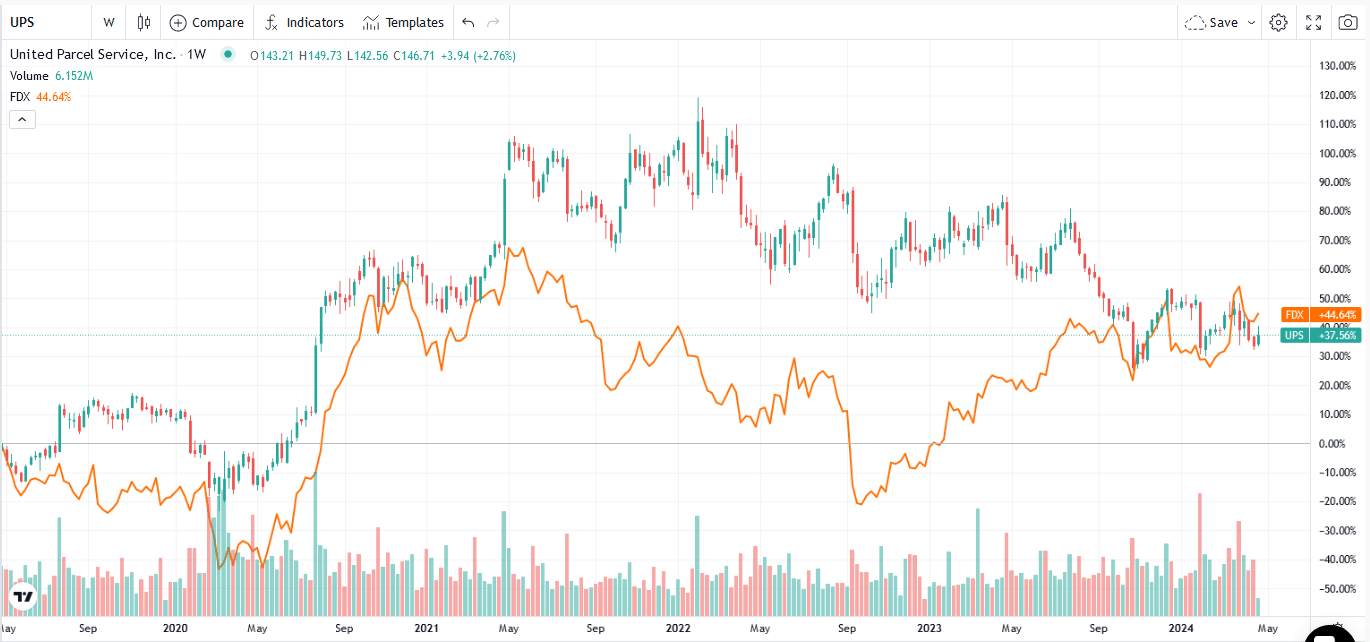

UPS Earnings

FedEx and UPS earnings are always interesting as they provide reliable information about personal and business consumption. UPS posted mixed results yesterday. EPS beat estimates by ten cents but came up a little short on sales ( $21.71 billion versus $21.91 billion). Due to weaker business conditions, UPS fired 12K employees in the quarter. FedEx laid off a similar number of workers in its most recent report.

UPS was up slightly on the news. The graph below shows that FedEx and UPS shares have been flat since 2021. While consumers and corporations continue to ship more, UPS and FedEx are increasingly losing market share to Amazon.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The Magnificent Seven Are Struggling- What Might It Mean?

Over the last few weeks, the market tone has changed. The S&P 500 is no longer tracking a steadily rising trend line higher. Further, the most recent market outperformers are very different from the Magnificent Seven, which led the way higher over the last six months. For investors, the changes lead to important questions. For instance, are the Magnificent Seven taking a break before retaking the outperformance throne? If not, which stocks, sectors, and factors may outperform the market? To help us answer these questions, we share analysis from the newly upgraded SimpleVisor.

The table below shows the relative performance of the Magnificent Seven stocks versus the S&P 500. Their performance has been dreadful over the last five days, but in the previous 20 days leading up to last week, they beat the market. NVDA and TSLA had last week’s worst relative performance, giving up over 10% to the S&P 500. However, NVDA has been consistently grossly outperforming the market over prior periods, while Tesla has been giving up ground since last July. If you notice, we added XLU, the utility sector ETF, to the list of the Magnificent Seven stocks. Suppose utilities are on the cusp of leading the market for a stretch of time. In that case, the SimpleVisor analysis we share further below will help us appreciate its performance and that of its underlying stocks versus the Magnificent Seven and the rest of the market.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, the market tried to rally early but sellers emerged early in the day. However, with the market has been down 6-consecutive days, a decently long stretch by historical standards, the rally into the close was unsurprising. Notably, as bearish sentiment rises, the odds of a decent reflexive rally increases. However, the first rally to resistance, which will likely fail at the 50-DMA will be an opportunity to reduce risk rather than adding exposure.

As noted yesterday, there are many “trapped longs,” that were swept up in the selloff and are now looking for an exit. The market will likely have another decline to retest current lows, or set new lows, before this correction is over. That second low will likely be a better entry point for adding exposure into year-end. As always, there are no guarantees in the market. While we expect another decline to buy into, things can and will change and we will update you accordingly.

The New SimpleVisor

We are thrilled to announce that SimpleVisor has a new look and feel as of Monday. Please let us know if you are a subscriber and have any questions. If you want to try SimpleVisor, give it a shot with a free 30-day trial. We share a little analysis of the utility sector to appreciate its value.

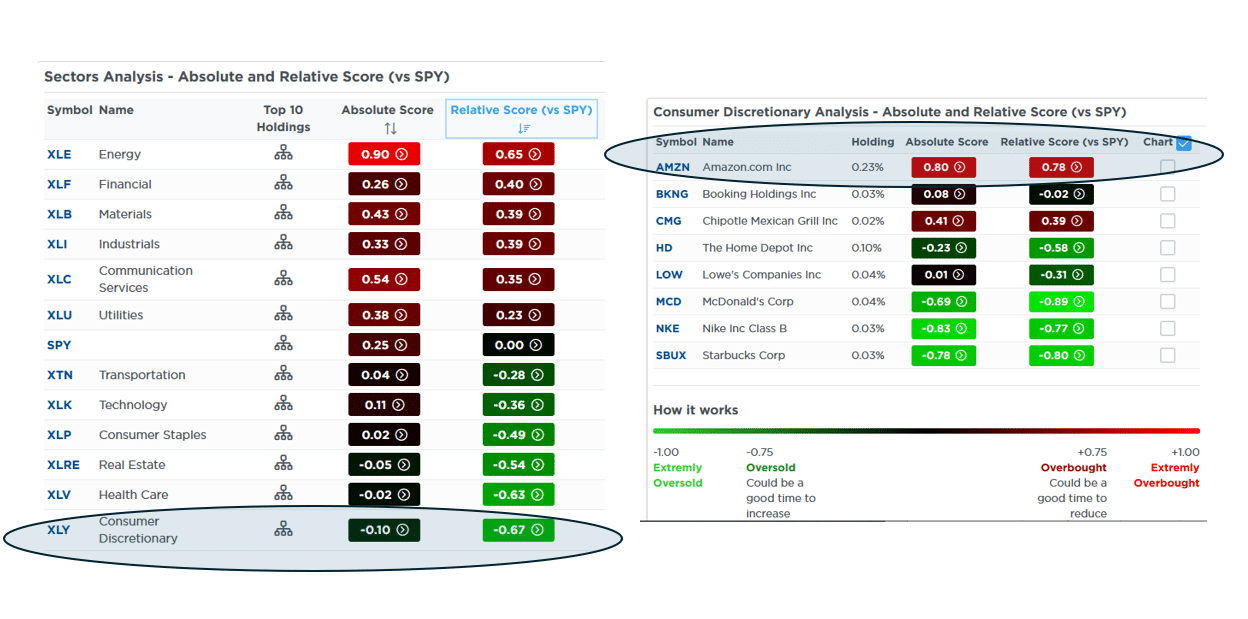

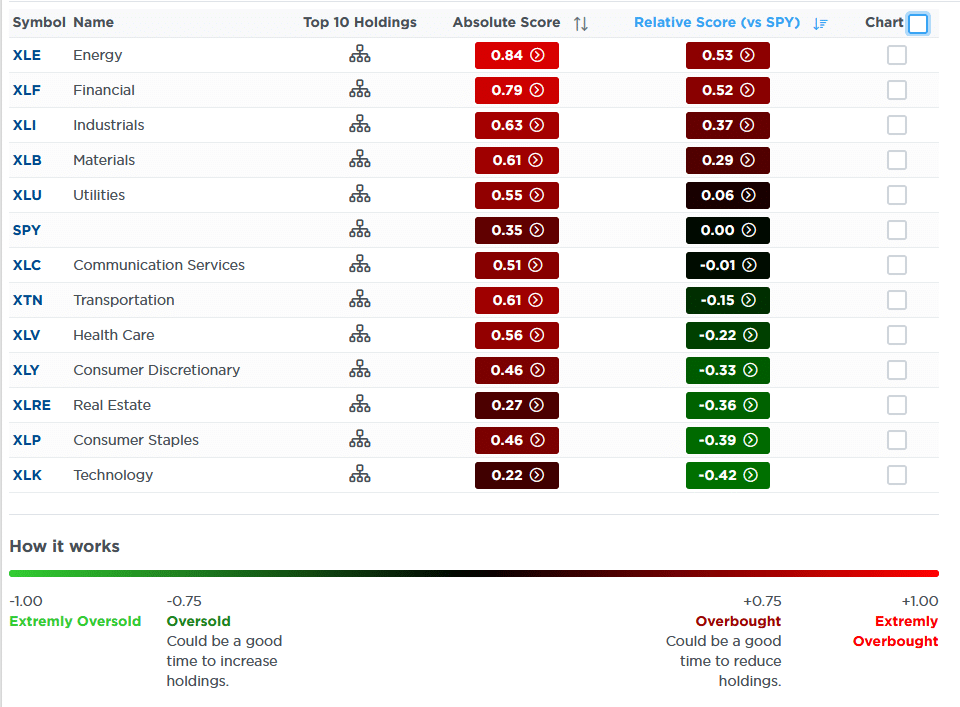

Utilities Are In Charge

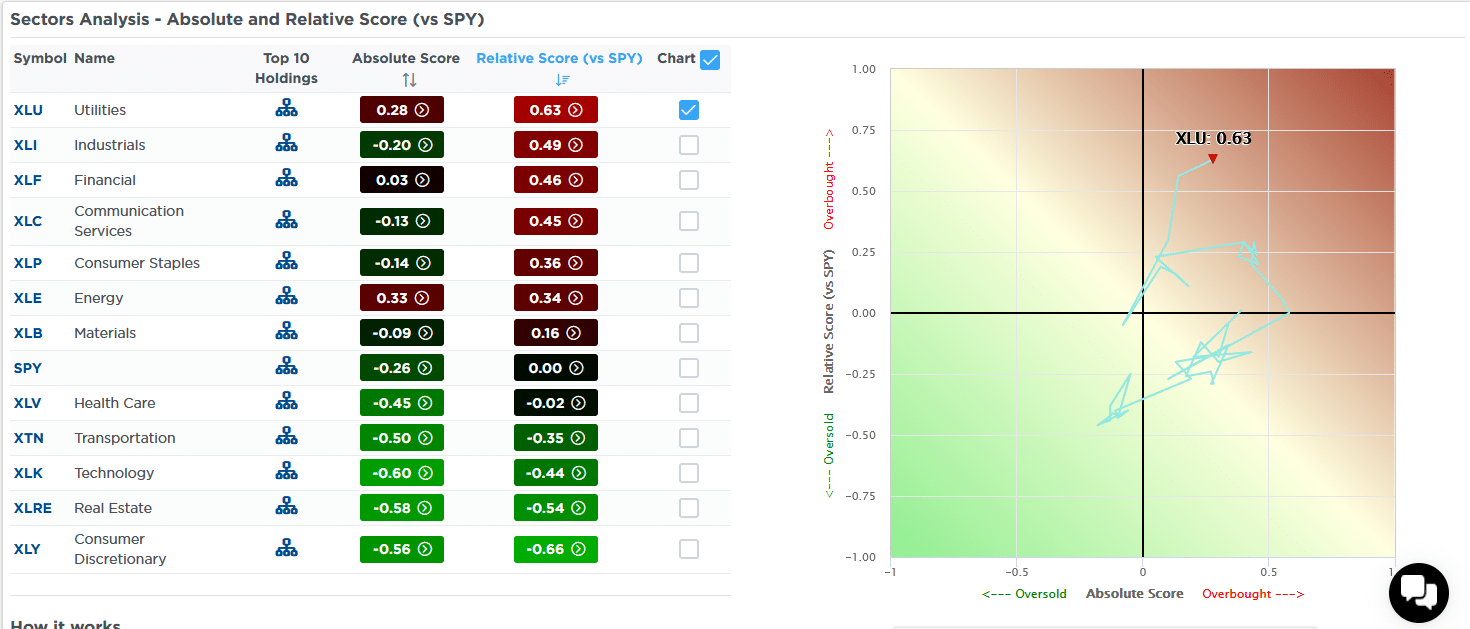

The SimpleVisor proprietary Absolute and Relative analysis uses many technical studies and assigns a relative (versus the S&P 500) and absolute score. We sorted by relative scores below. Note that utilities (XLU) are now the sector with the most overbought score versus the S&P 500 and the second most on an absolute basis, behind the energy sector. The graph on the right charts the daily absolute and relative scores over the last nine months. Accordingly, it went from decently oversold on both measures to overbought territory.

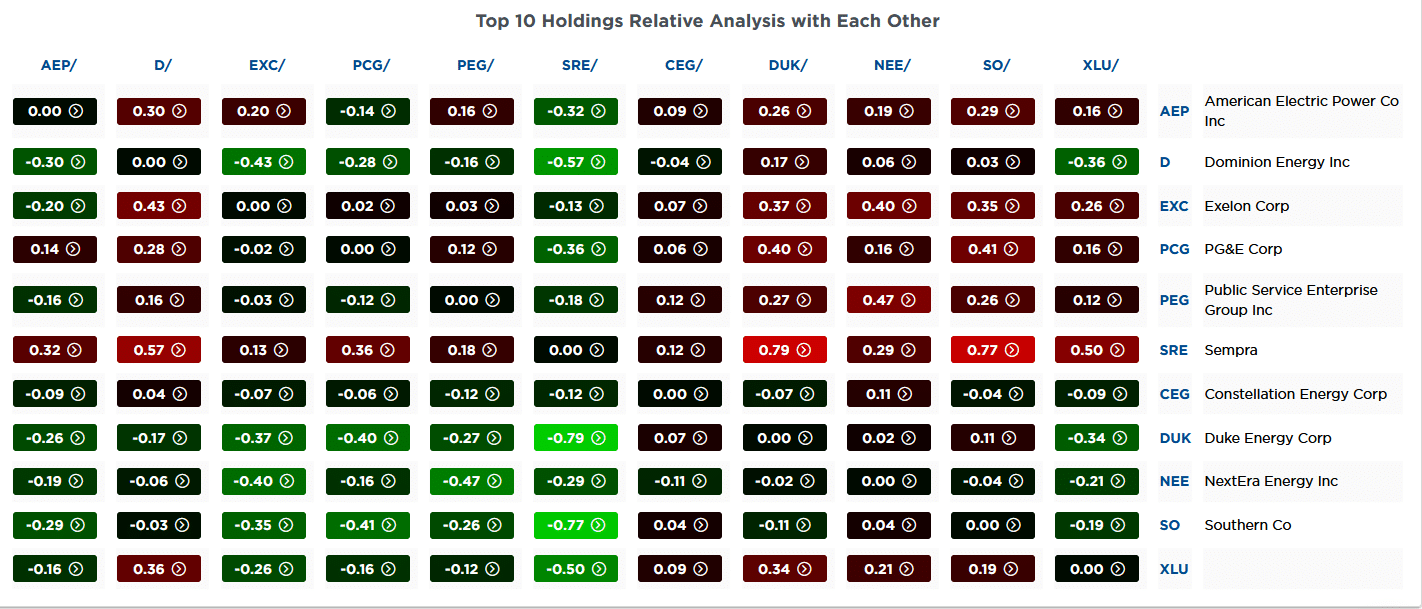

The second graphic breaks the sector down by its top ten holdings and performs a similar analysis. PEG, D, and NEE have the highest relative scores, while DUK and D have the best absolute scores. The third graph provides a relative analysis study using each utility stock against each other. This allows us to see better which utility stocks are leading the way and which are lagging.

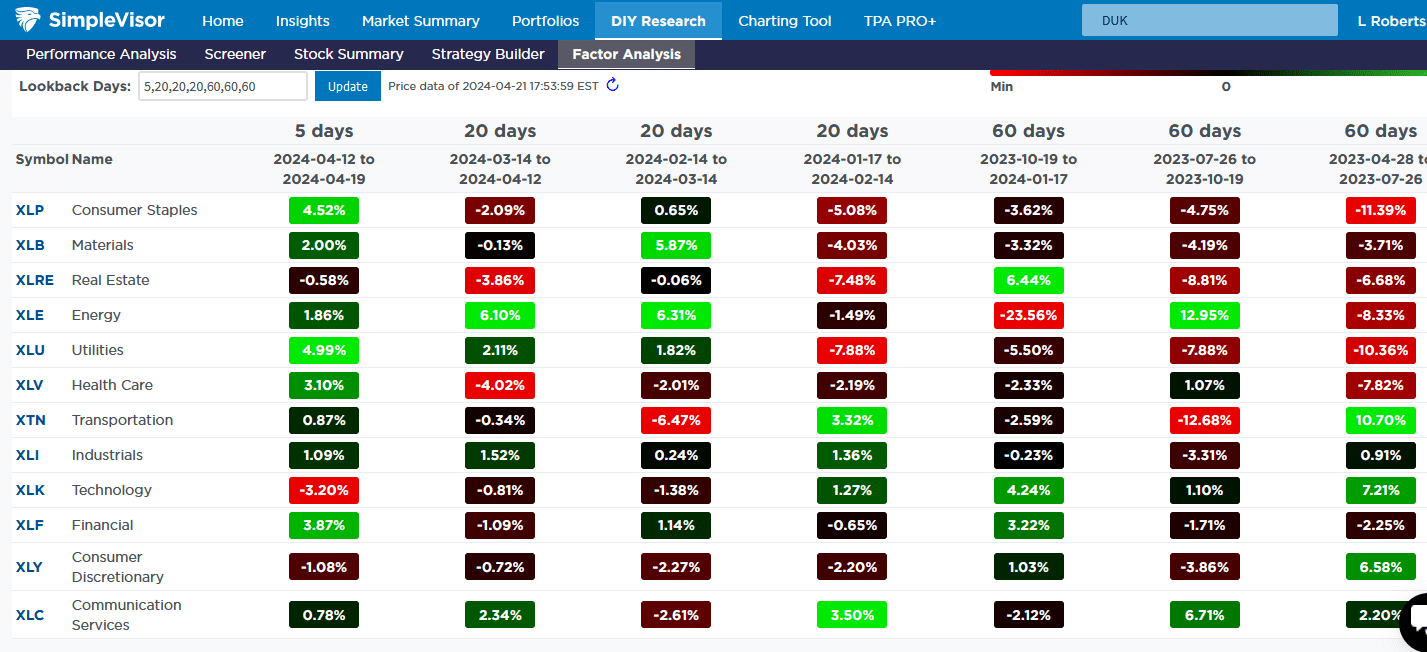

Lastly, the fourth screenshot shows the relative performance of each sector over various time frames going back a year. Over the last five days, utilities gained 4.99% on the S&P 500. While its relative performance has been good for the previous 45 days, it was atrocious from April 2023 through mid-January. The SimpleVisor data show how the market has clearly rotated since January from the mega-cap technology-oriented companies to those stocks left behind. If the market continues to decline, we expect this to continue. However, if this is a consolidation before another rally, it will be interesting to see if megacap stocks lead the way again or if the conservative sectors and factors will continue to lead.

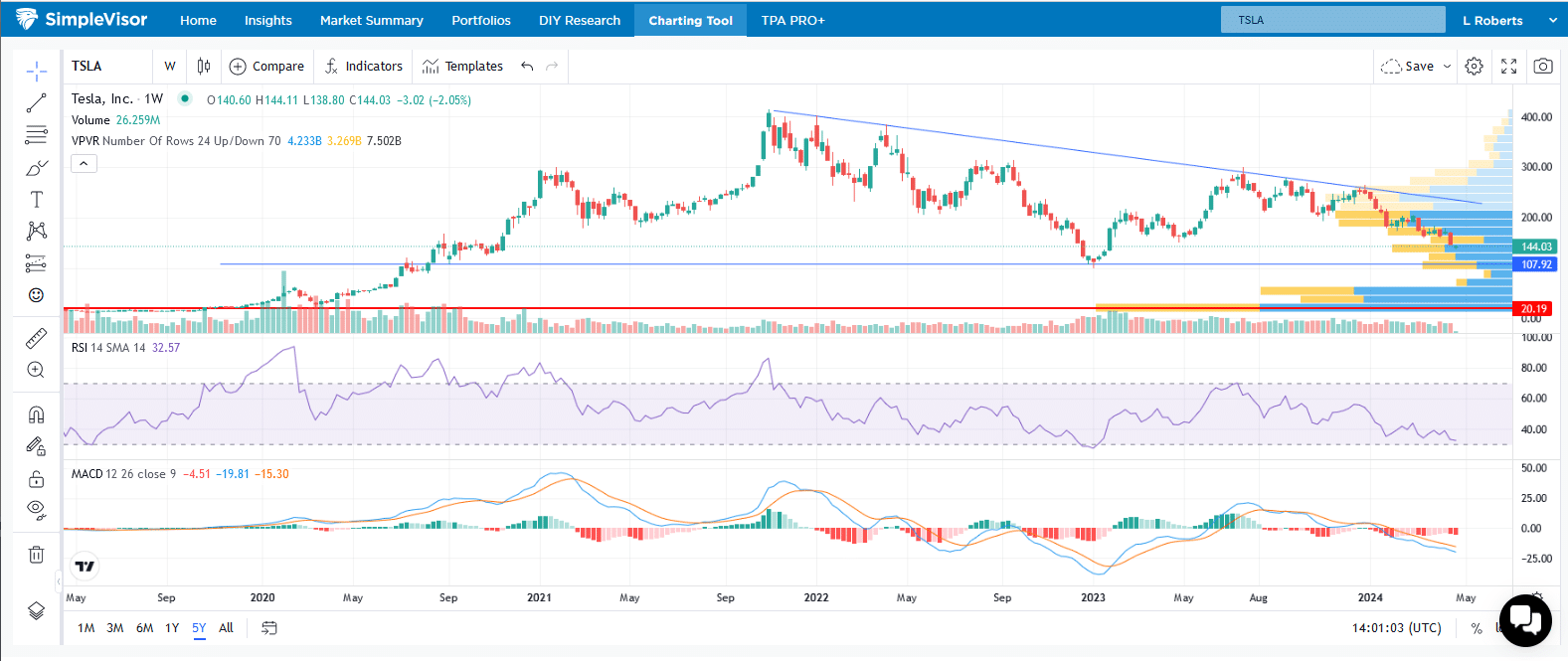

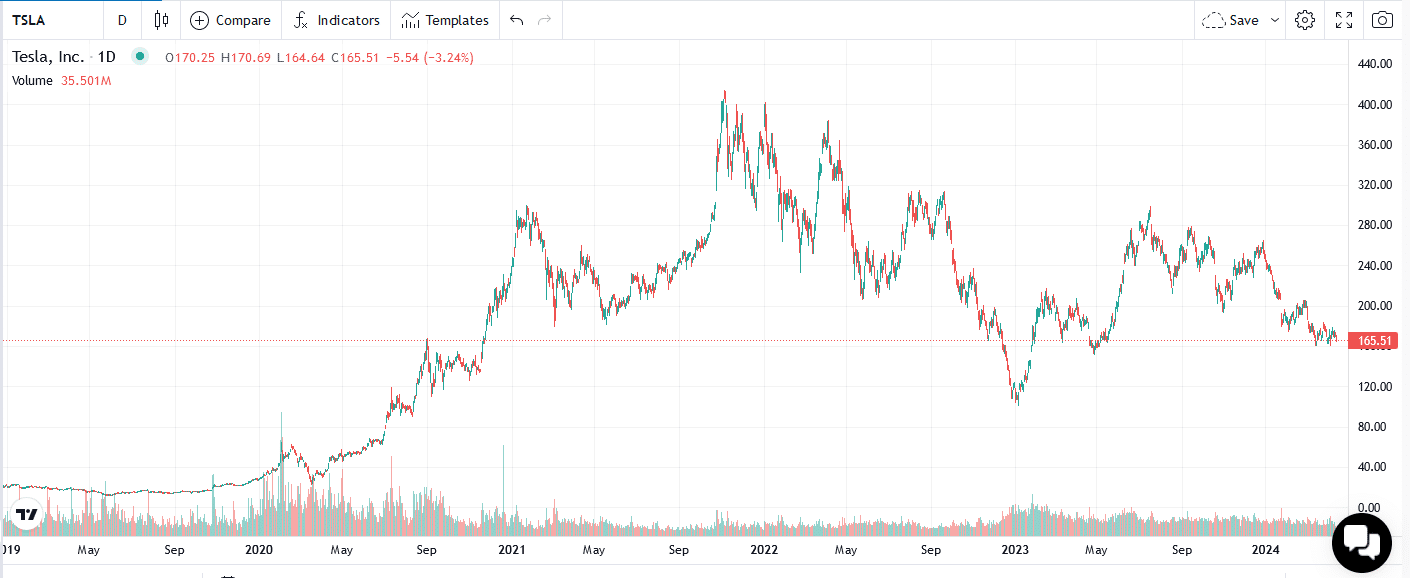

Tesla Continues to Slip

Our Daily Commentary from April 16th and others prior discussed the recent auto industry trend away from EVs. Tesla, like smaller EV makers and lithium producer shares, has been under significant pressure. As we share in the opening graphic, Tesla has been grossly underperforming the market, as well as the other Magnificent Seven stocks. Let’s look at its graph to better assess Tesla from a technical perspective.

For starters, note that the stock has fallen by over 50% since peaking in November 2021. The blue line highlights the downward resistance trend line that has kept a cap on rallies since November 2021. The horizontal bars on the right axis depict the volume occurring at each price interval. As it shows, a majority of buyers bought the stock at $75 or below or between $170 and $260. The stock is trading at $140, meaning that many holders are losing money, while those who bought it at much lower prices still have sizeable gains but are watching them erode. If Tesla continues lower, many trapped longs with losses may give in to their emotions and sell. Further, those with gains may be willing to sell to walk away with profits.

The MACD and RSI below the graph show that the stock is currently oversold, but it can certainly get more oversold. A corrective rally would not be surprising, but there is little indication that a low is in. For those inclined, the blue horizontal line at $108 may be a good place to start nibbling on Tesla shares.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Just A Correction, Or Is The Bull Market Over?

Is this just a correction after a strong bullish advance from November, or is the bull market ending? If you read some of the headlines, you would suspect the latter. As noted by MarketWatch last week:

“For the first time since early November 2023, less than 30% of S&P 500 stocks are trading above their 50-day moving average — a clear indicator of the current poor market’s breadth. This significant drop from the 85% observed in late March and 92% at the beginning of January highlights a dramatic reversal in market dynamics.

The 50-day moving average is often seen as a barometer for the short-term health of stocks. Falling below this level en masse suggests that a broad swath of the market is facing downward pressure. This shift comes amid escalating geopolitical tensions in the Middle East and renewed concerns over inflation, which have collectively nudged traders towards a more guarded stance in April.”

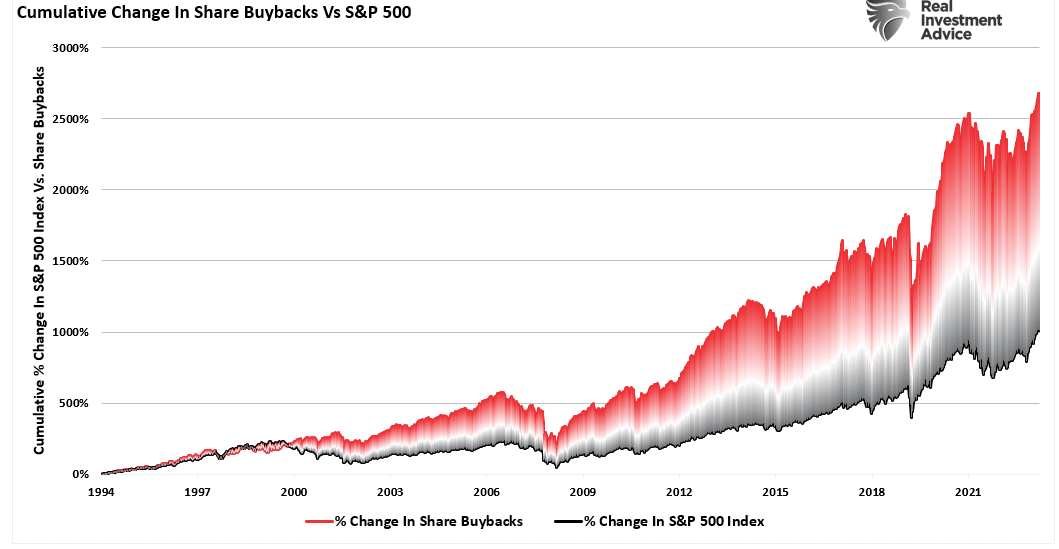

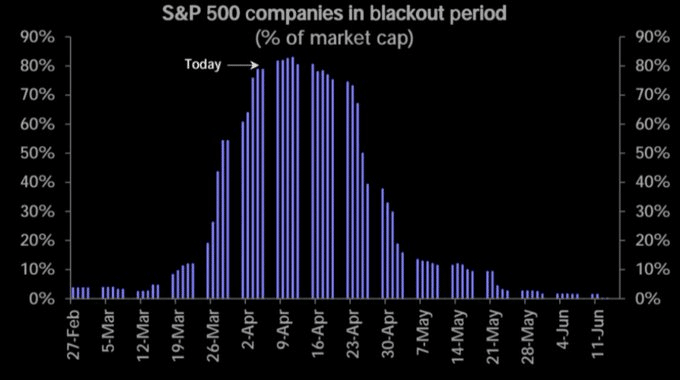

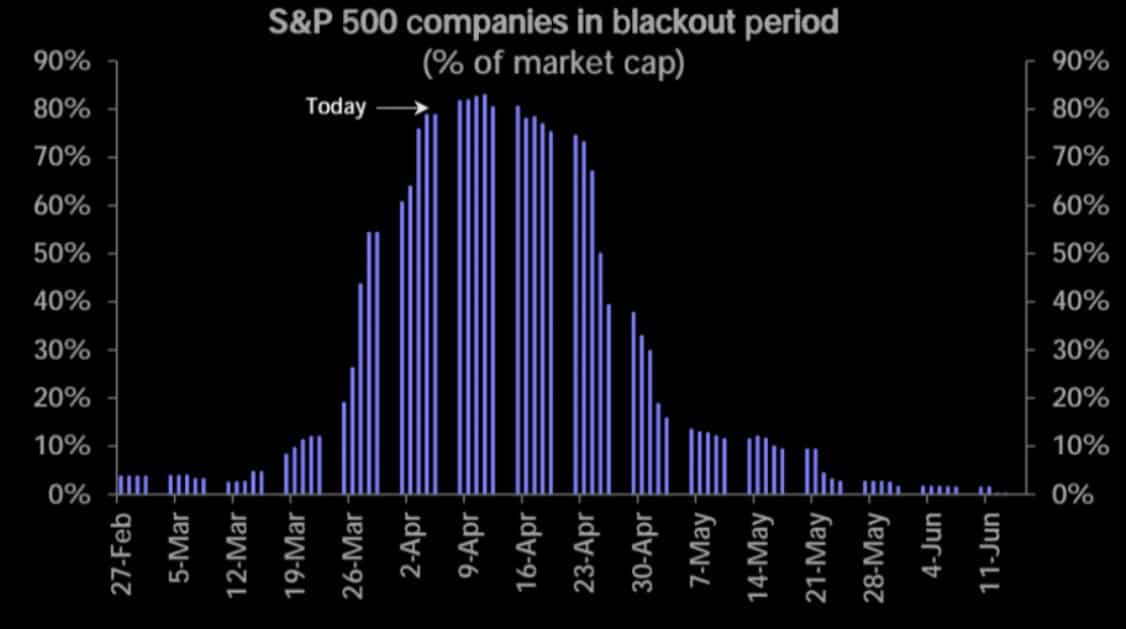

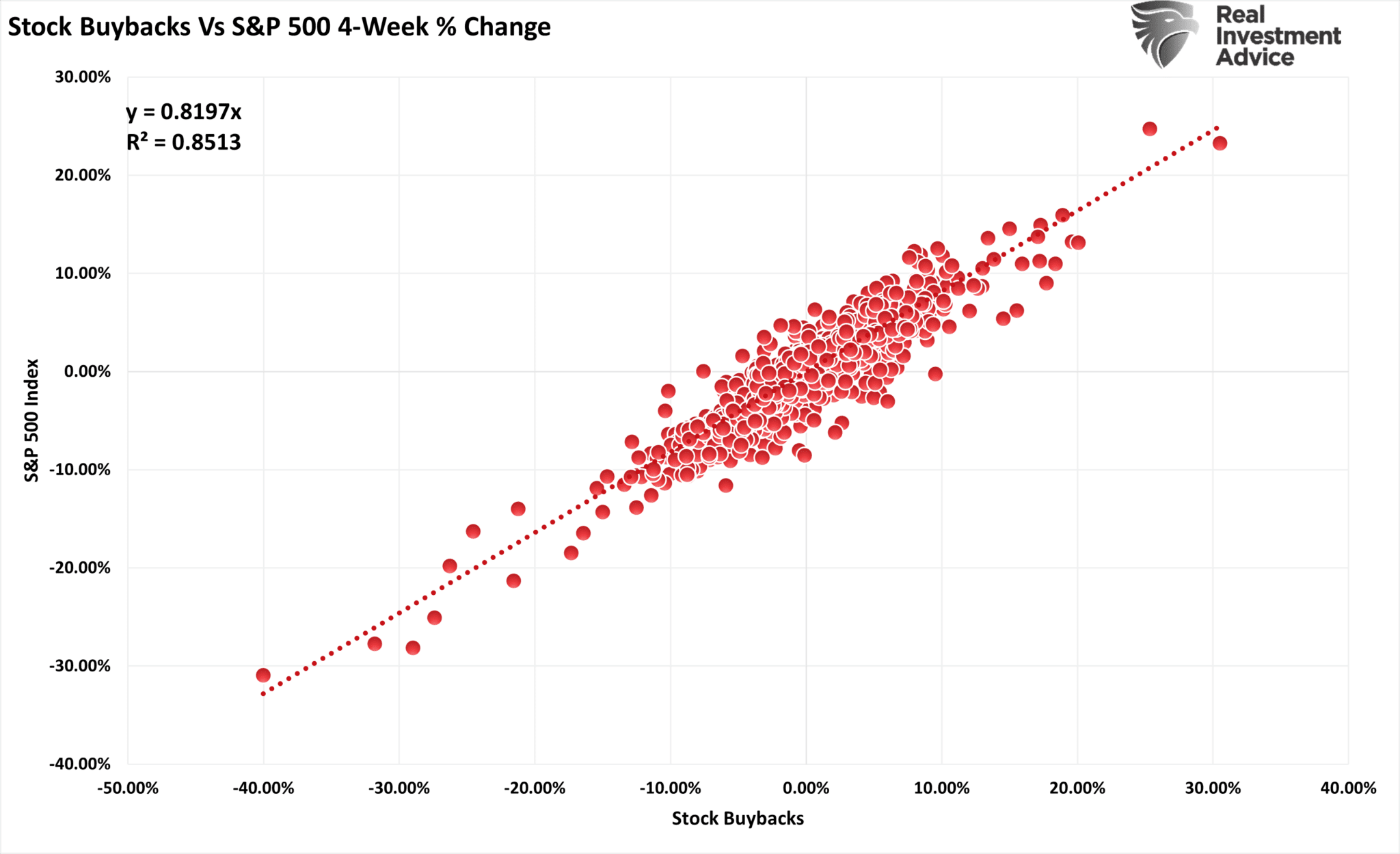

Of course, there are many “reasons” lately for the drop in stock prices. Geopolitical stress between Israel and Iran and hotter-than-expected inflation data that paused Fed rate cuts brought sellers into the market. However, none of this is shocking, as we previously noted in “Blackout Of Buybacks:”

“Notably, since 2009, and accelerating starting in 2012, the percentage change in buybacks has far outstripped the increase in asset prices. As we will discuss, it is more than just a casual correlation, and the upcoming blackout window may be more critical to the rally than many think.” – March 19, 2024

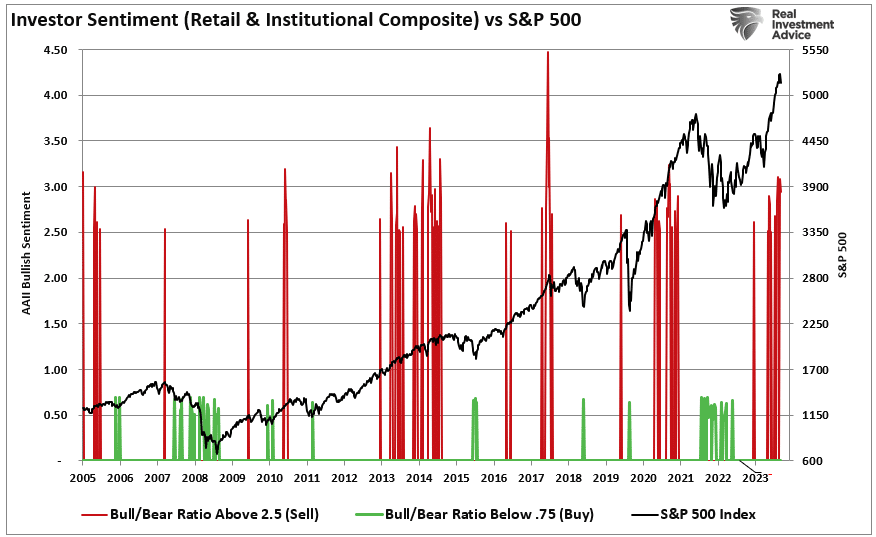

Furthermore, the “blackout” of corporate buybacks coincided with an aggressively bullish investor sentiment. As we noted in that same article:

“Investor sentiment is once again very bullish. Historically, when retail investor sentiment is exceedingly bullish combined with low volatility, such has generally corresponded to short-term market peaks.”

We will return to this chart momentarily, but given that corporate share buybacks have accounted for roughly 100% of net equity purchases over the last two decades, the blackout period combined with aggressive bullish sentiment was the recipe for a decline in asset prices.

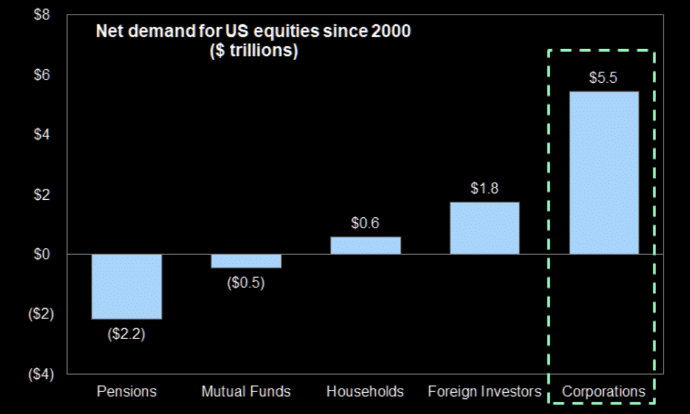

Here is the math of net flows if you don’t believe the chart:

Pensions and Mutual Funds = (-$2.7 Trillion)

Households and Foreign Investors = +$2.4 Trillion

Sub Total = (-$0.3 T)

Corporations (Buybacks) = $5.5T

Net Total = $5.2 Trillion = Or 100% of all equities purchased

Such is crucial to understand as we head into the rest of the year. It will determine whether this is just a correction within a bullish trend or something more significant.

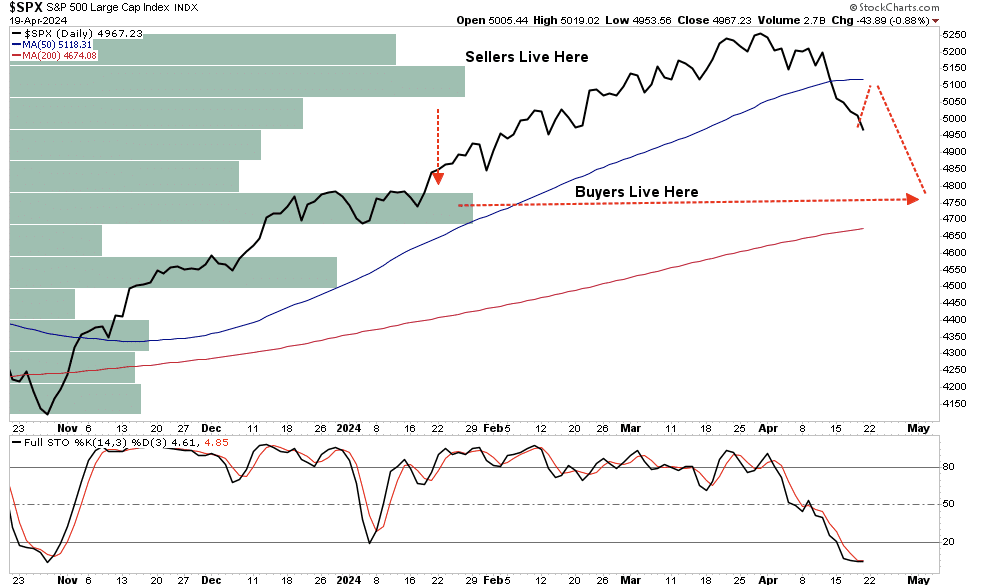

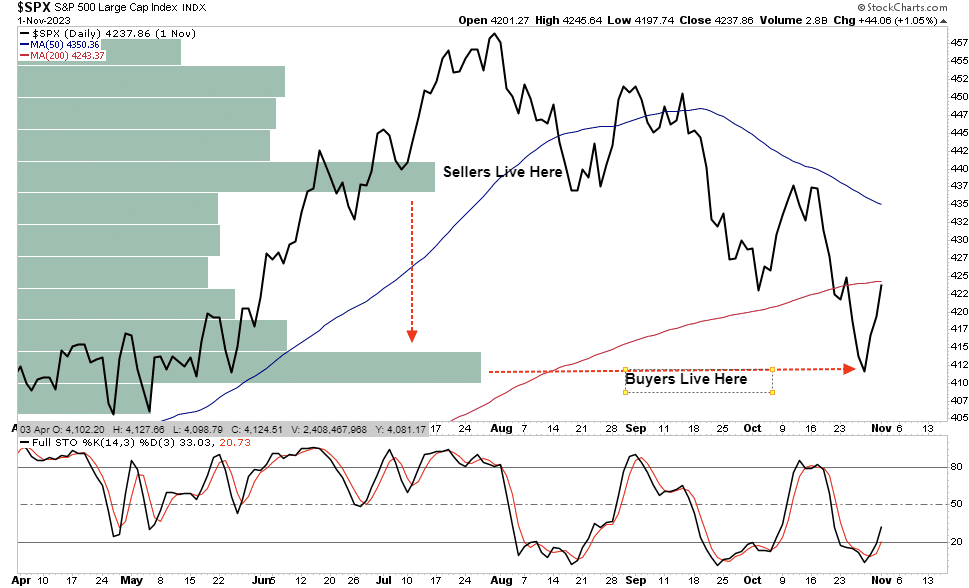

Buyers Live Lower

In “No Cash On The Sidelines,” we discussed the importance of understanding that “market prices” are set by the demand and supply between buyers and sellers. To wit:

“As noted above, the stock market is always a function of buyers and sellers, each negotiating to make a transaction. While there is a buyer for every seller, the question is always at “what price?”

In the current bull market, few people are willing to sell, so buyers must keep bidding up prices to attract a seller to make a transaction. As long as this remains the case and exuberance exceeds logic, buyers will continue to pay higher prices to get into the positions they want to own.

Such is the very definition of the “greater fool” theory.

However, at some point, for whatever reason, this dynamic will change. Buyers will become more scarce as they refuse to pay a higher price. When sellers realize the change, they will rush to sell to a diminishing pool of buyers. Eventually, sellers will begin to “panic sell” as buyers evaporate and prices plunge.”

In other words, “Sellers live higher. Buyers live lower.“

We can see where the buyers and sellers “live” in the following chart, which shows where the highest volume occurred.

This current correction is becoming increasingly oversold (bottom panel), which suggests a bounce is likely toward the previous support of the 50-DMA. For comparison, we can look at last year’s market correction. As noted, the bullish rally into July peaked late that month. As the market corrected, it bounced from oversold conditions, allowing investors to reduce risk and hedge portfolios. The markets will likely present investors with that opportunity soon.

Then, like today, many investors began to believe it wasn’t just a correction but something much more. However, the reality was that the “buyers lived lower.” Buyers stepped in as prices approached the October lows, coinciding with the return of corporate share buybacks.

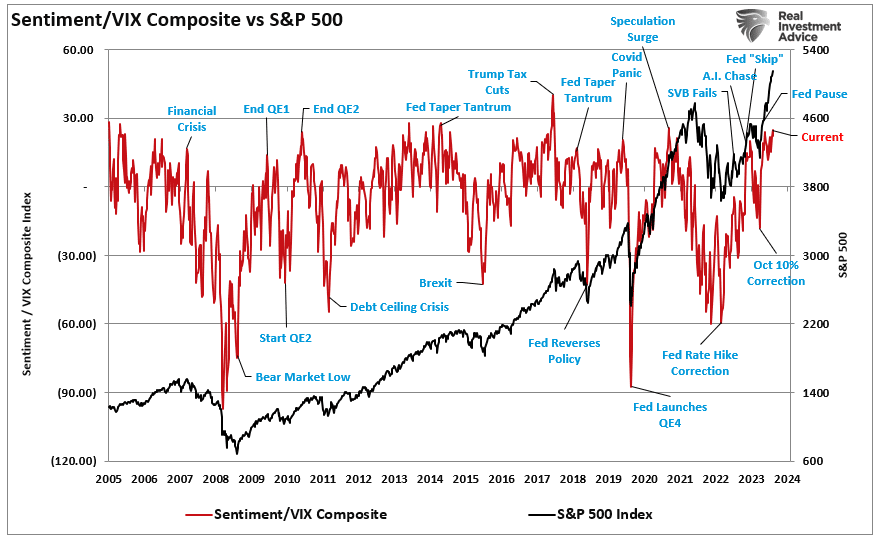

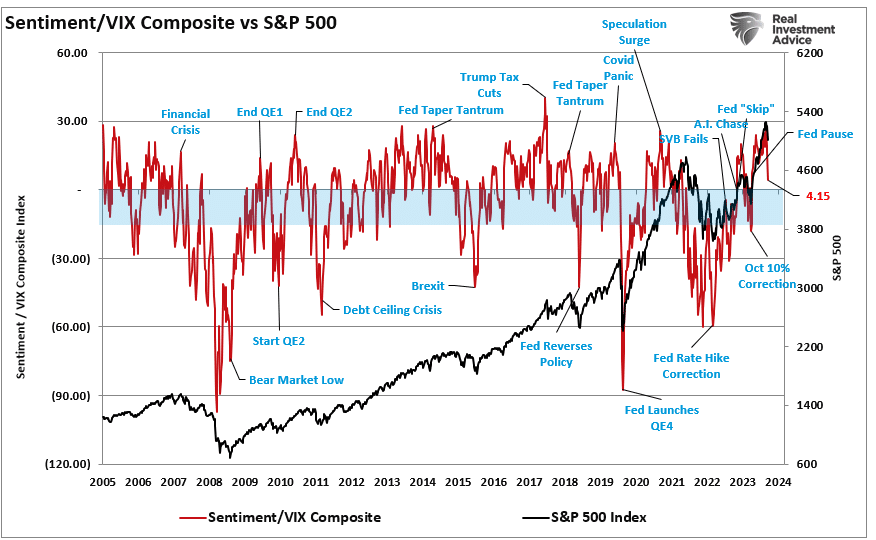

Sentiment Is Reversing Quickly

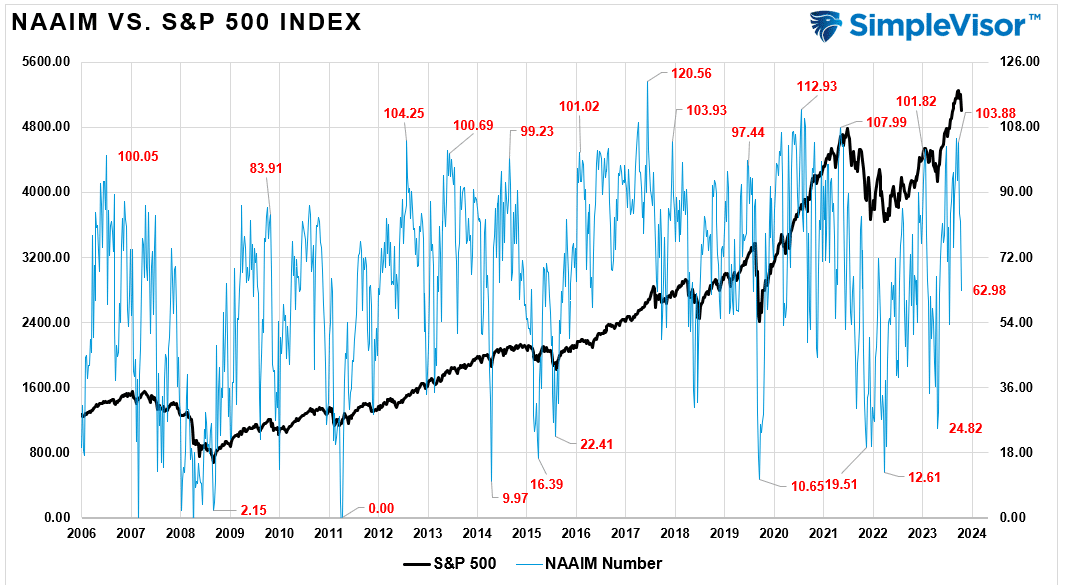

As I said, we need to revisit the sentiment chart above. Investors’ more frothy, bullish sentiment is reversing quickly on many fronts. The chart below, the same as above, is the composite net bullish sentiment index of retail and professional investors divided by the volatility index (VIX). If this is just a market correction, the index tends to bottom between zero (0) and negative (20). With a current reading of 4.15, down from 25.99 just two weeks ago, bullish sentiment has significantly reversed.

Notably, professional investor allocations to equities recently peaked at 103.88%, which has collapsed in just two weeks to just 62.98% exposure. (Professional investors are notorious for buying market peaks.)

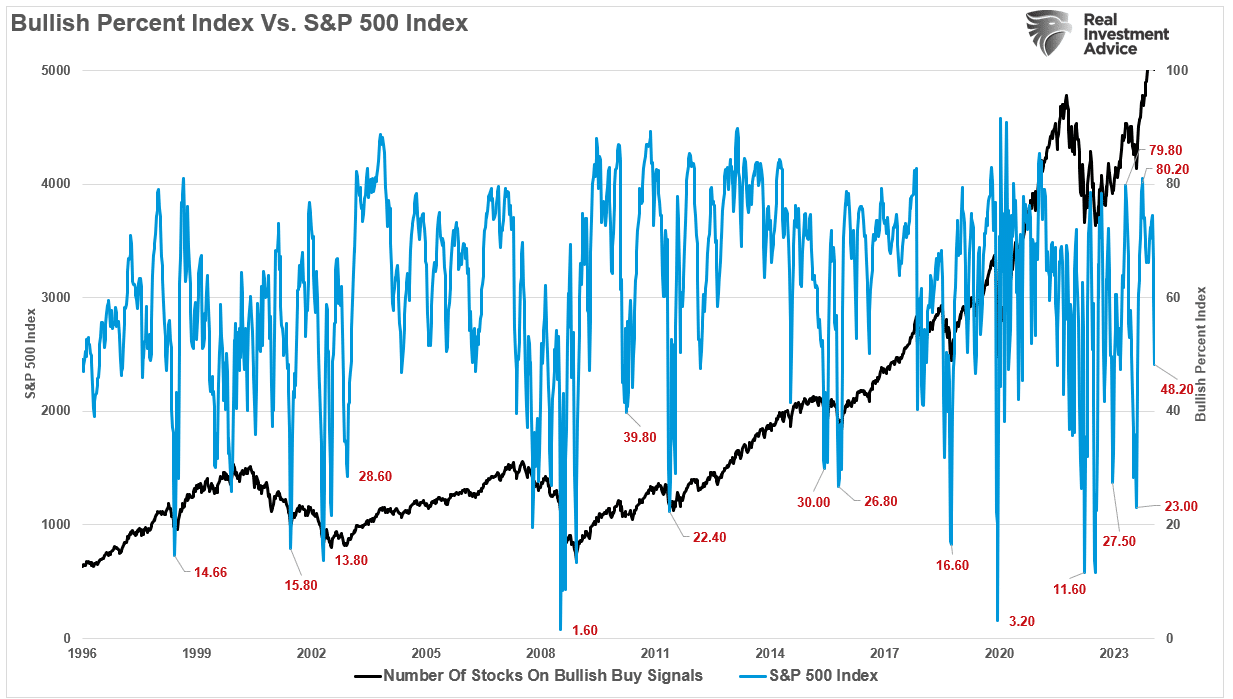

Also, the number of stocks on bullish “buy signals” has dropped from 80.2 to 48.2.

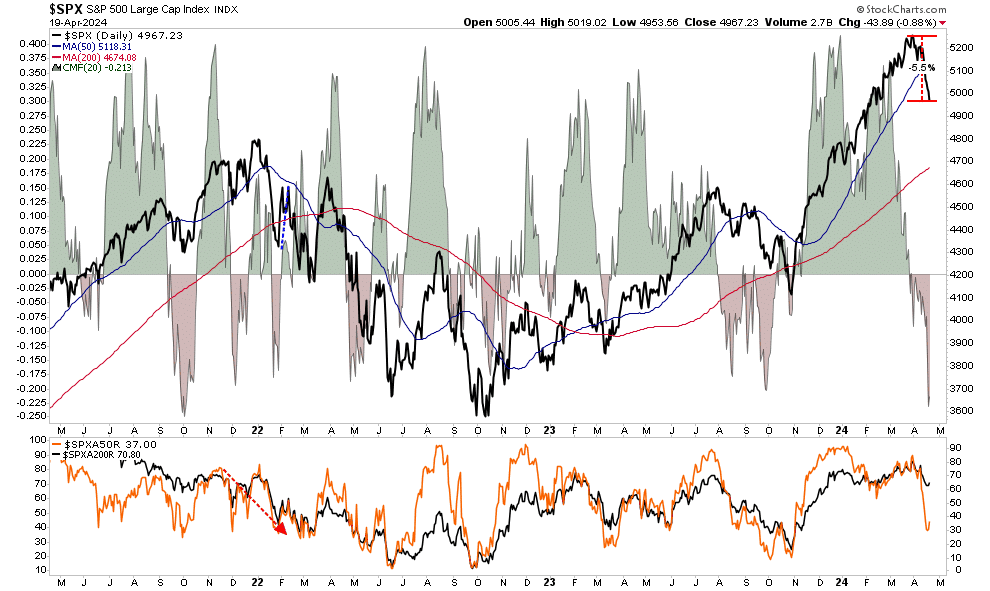

Furthermore, the number of stocks trading above the 50-DMA has fallen from over 80% to 37%, with money flows hitting levels lower than previous market bottom lows. Notably, with just a 5.5% correction from the recent peak (as of last Friday), much of the work of clearing the previous overbought conditions is completed.

Given the significant reversal in sentiment and short-term oversold conditions, we highly suspect the markets will provide a reflexive rally soon. However, with the number of bullish investors who got “trapped” in the selloff, any rallies will likely be met with further selling.

However, despite the current “panic” in the media headlines, this is likely just a correction within an ongoing bullish market. Such is particularly the case given that corporate share buybacks will resume in May, providing critical support for the markets heading into summer.

With that said, this correction, when complete, likely won’t be the last we see this year. Market history suggests we could see another “bumpy ride” heading into what many expect will be a somewhat contentious election.

But that is an article we will write when we get there.

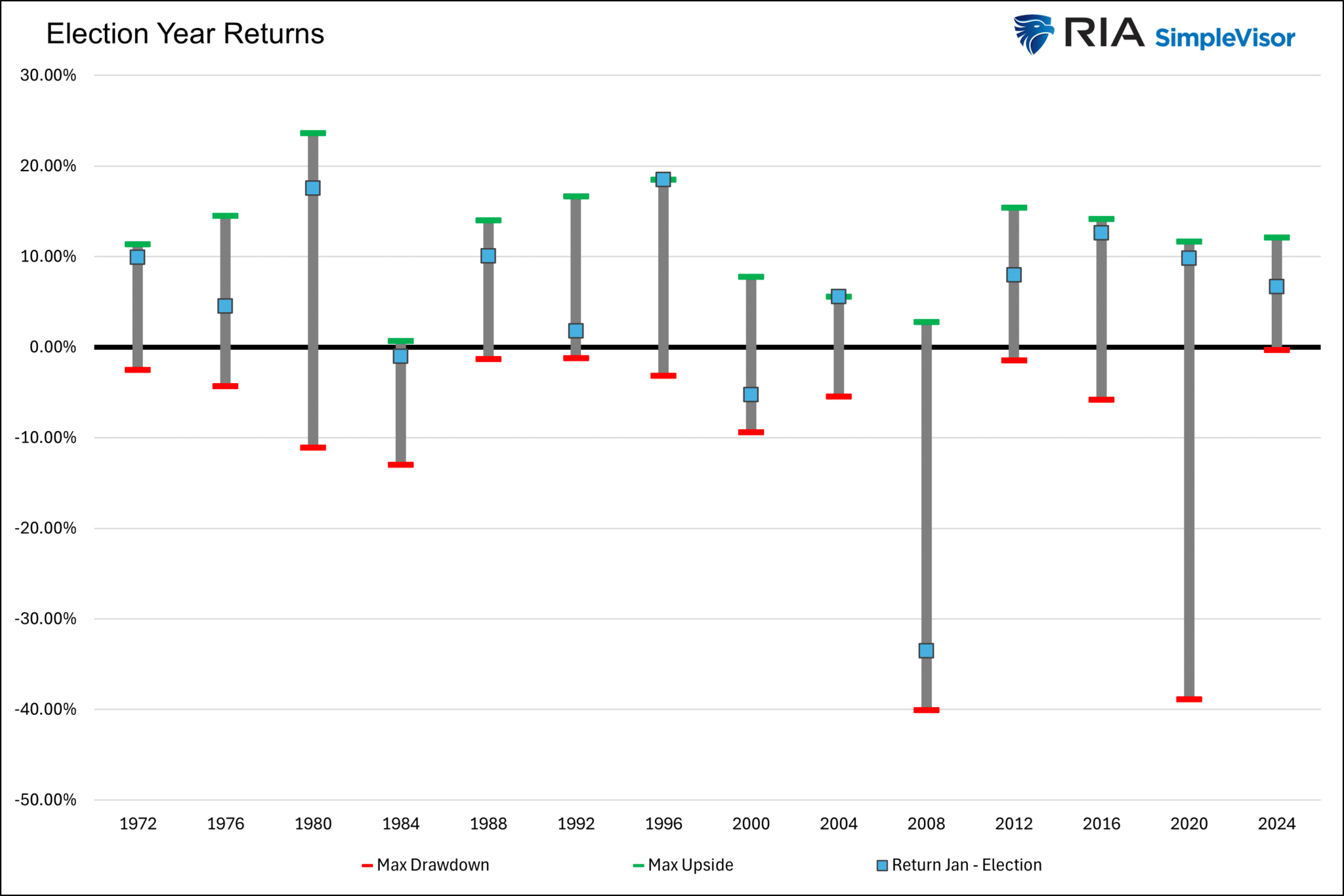

Election Year Market Expectations

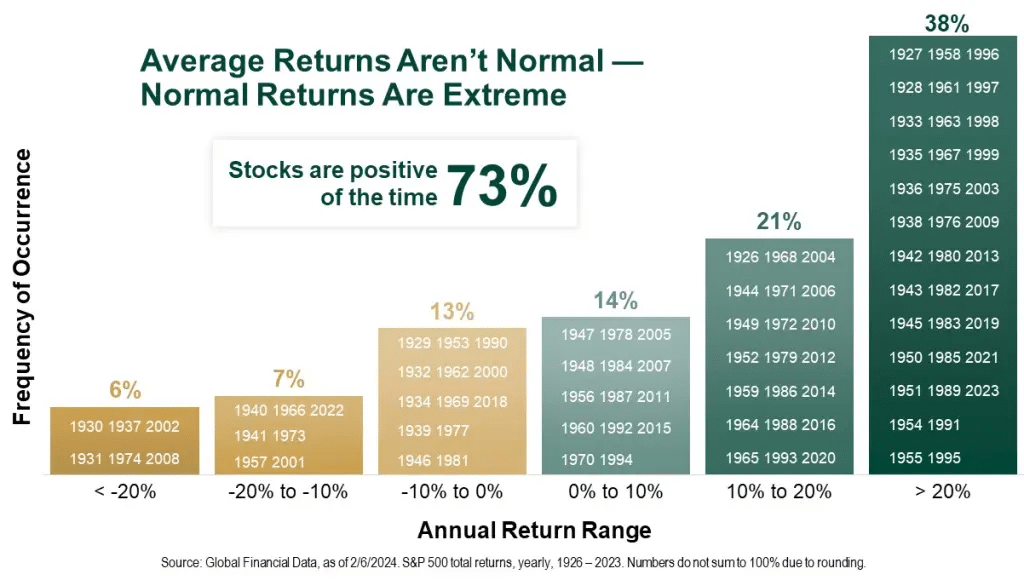

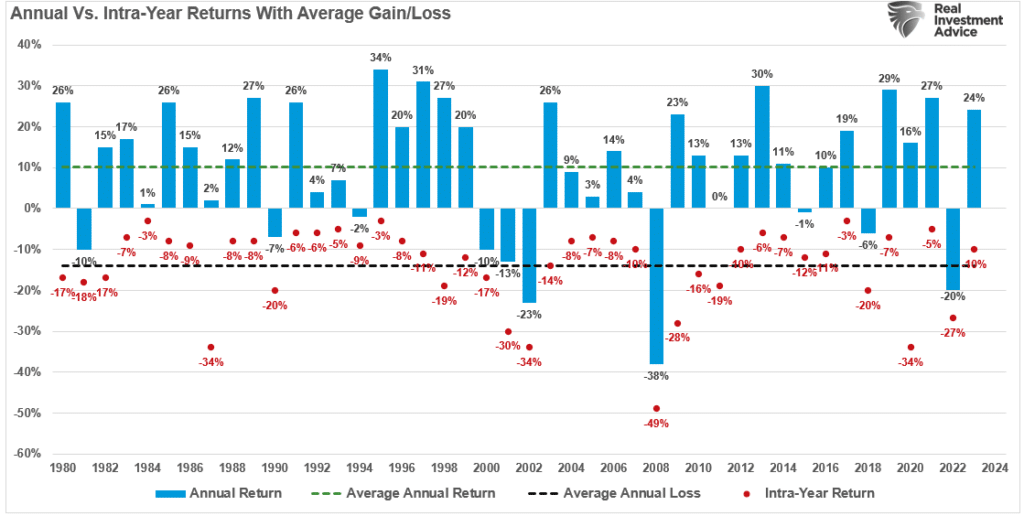

Investors tend to prefer periods of stability. However, as we share below, politicians’ promises appear to offset the potential instability associated with changes in the White House and/or Congress. We present the graph below to help appreciate how seasonal patterns may affect stock prices this election year. Since 1972, only three of the thirteen election periods had negative returns between January and the election. The 1984 election was slightly negative, although from January to July, the S&P 500 fell 13% but fully recovered by November. 2000 and 2008 were the worst years for returns.

The range of returns throughout the series of ten-month periods is also important to appreciate. Of the thirteen periods, only five had a maximum drawdown of 5% or worse. All but four of the years saw at least one point within the period in which the S&P 500 posted double-digit gains. The average gain for all election year periods is 4.65%, with an average maximum drawdown of 9.86% and an upside of 12.76%. The outsized losses in 2008 certainly skew the data. Excluding that year, the average gain is nearly 8%. While we are only four months into the current election period, the return is already 2% above the average, and the maximum return this year matches the average. Might we have already seen the best performance of the year, or do years like 1980, 1996, and 2016 provide hope for even better returns in the coming months?

What To Watch Today

Earnings

Economy

Market Trading Update

Last week, we discussed the market’s break of the bullish trend. To wit:

“The market did break below the previous low on Friday after failing to reclaim that previous support at the 20-DMA. The failure to reclaim that support turns the previous 20-DMA into resistance and makes the 50-DMA new critical support over the next few days. (Note: If the market makes a confirmed break of the 50-DMA, the 100- and 200-DMAs become the following logical targets.)”

Over the two months, we repeatedly warned that a correction process was likely. As noted in “Market Top or Bubble:”

“As noted, the market remains in a bullish trend. The 20-DMA, the bottom of the trend channel, will likely serve as an initial warning sign to reduce risk when it is violated. That level has repeatedly seen ‘buying programs’ kick in and suggests that breaking that support will cause the algos to start selling. Such a switch in market dynamics would likely lead to a 5-10% correction over a few months.“

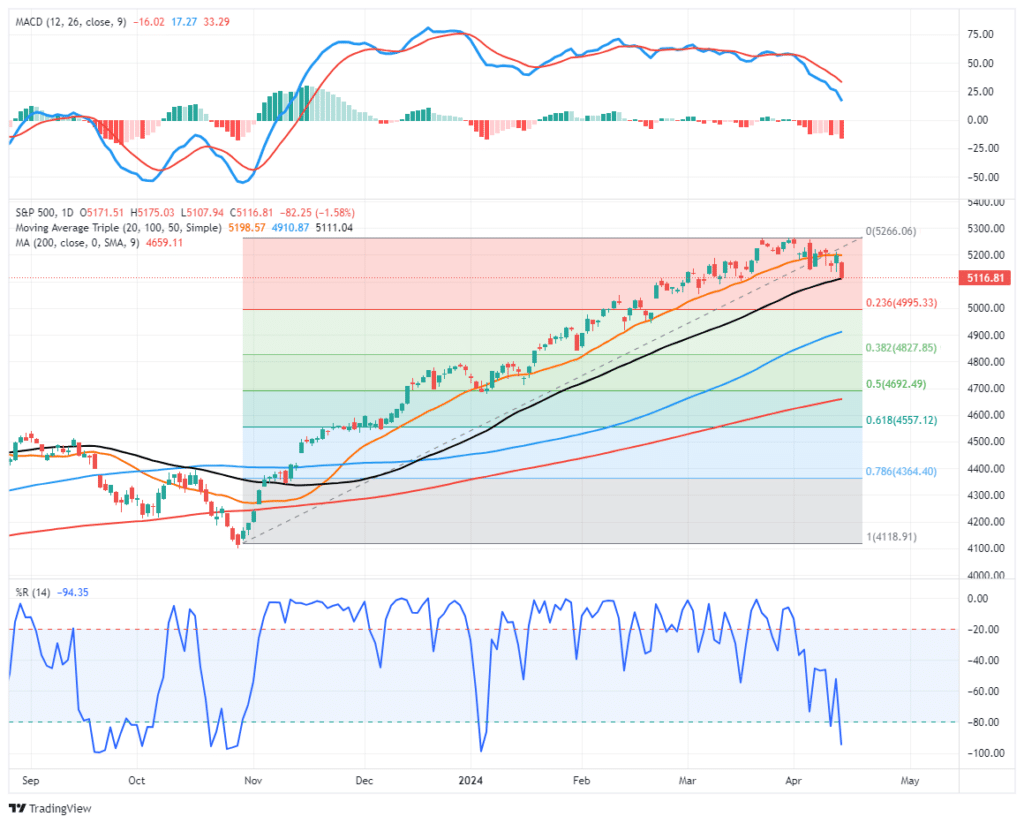

While it took longer than expected, that correction process arrived last week and continued earnestly with the market approaching the 100-DMA. With the market short-term oversold, a reflexive rally in the next week is likely, with the 50-DMA being notable resistance. Any rally toward 5100 should be used to rebalance risk and hedge portfolios as needed.

Notably, this has been a very orderly correction. While there has certainly been selling in the markets, particularly in some of the previous “momentum” names, volatility has risen in a controlled manner. Such suggests that this correction process is just a normal correction within an ongoing bullish trend. You will note very similar actions during the decline last summer.

As noted last week:

“The confirmed break of support suggests reviewing portfolio allocations and taking profits in well-performing positions. However, while some stocks have only begun to correct from previously overbought conditions, many have already corrected by 10% or more over the last few weeks. Those companies may see inflows as a rotation trade in the market occurs.

In other words, as is always the case, be careful “throwing the baby out with the bathwater.” Opportunities to acquire better-priced companies always exist, even during a corrective process.”

The Week Ahead

Earnings from the largest technology companies will be a big focus this week. Verizon will kick off earnings on Monday, followed by Visa, Tesla, Meta, Microsoft, Google, Amazon, and Exxon. Apple and AMD will post earnings next week. There are a significant number of earnings announcements from other large companies that we do not mention.

PCE prices on Friday will help us decipher if the hotter-than-expected CPI or relatively benign PPI inflation data is accurate. The Fed prefers PCE, so we expect market volatility if PCE is above or below expectations. Economists expect PCE and Core PCE to be 0.3%, which is in line with last month’s readings.

The Escalation Between Israel and Iran Sends Markets On A Rollercoaster To Nowhere

Later Thursday night, it was reported that Israel bombed Iran near areas where they house its nuclear capabilities. The market reaction was decidedly risk-off as traders assumed this action would further escalate their ongoing conflict. As it turns out, cooler heads prevailed, and Iran alluded that it would not retaliate. While nothing is off the table, the roller coaster ride in many asset classes tells us the market fears of escalation evaporated by Friday morning. Consider the following table showing the Thursday close, Friday open, and the maximum percentage gain or loss at the peak of panic.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

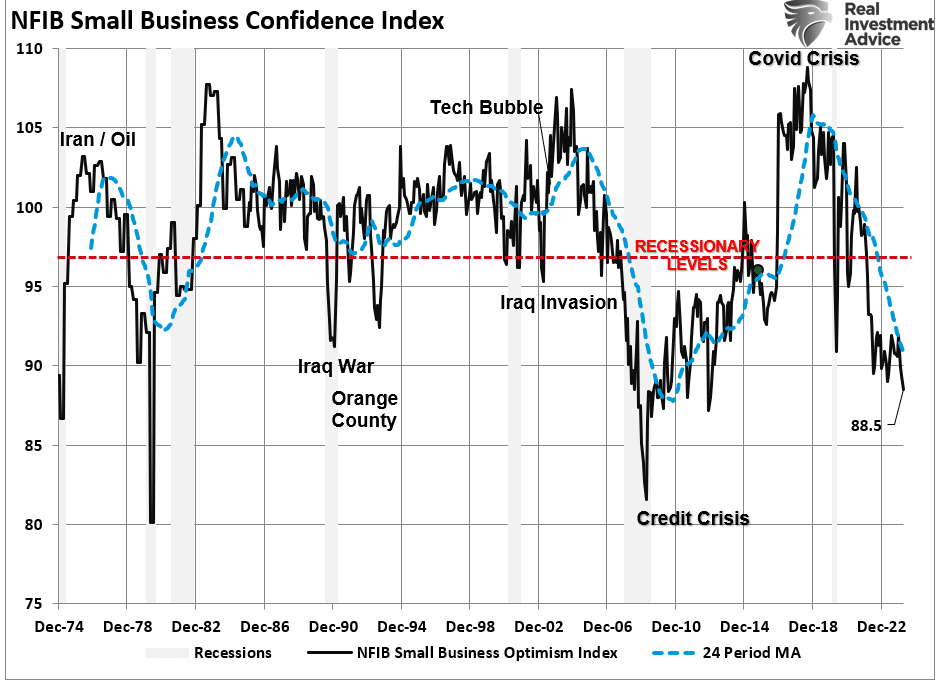

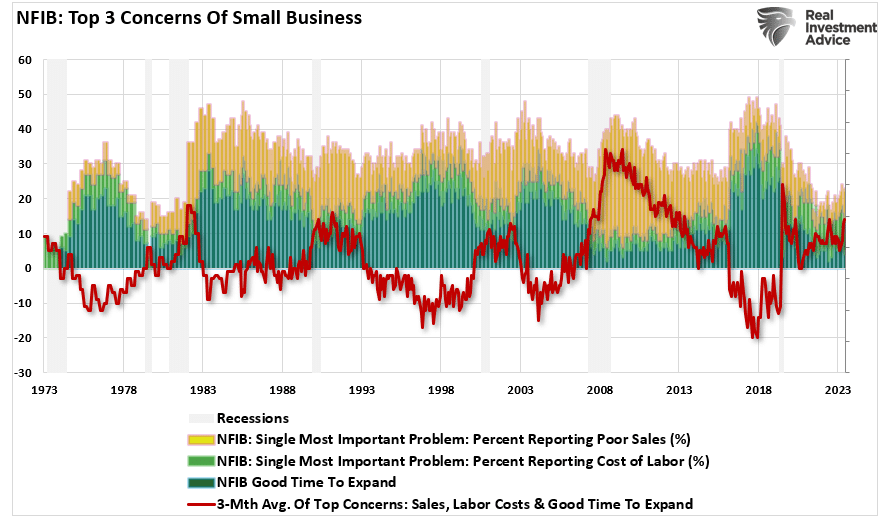

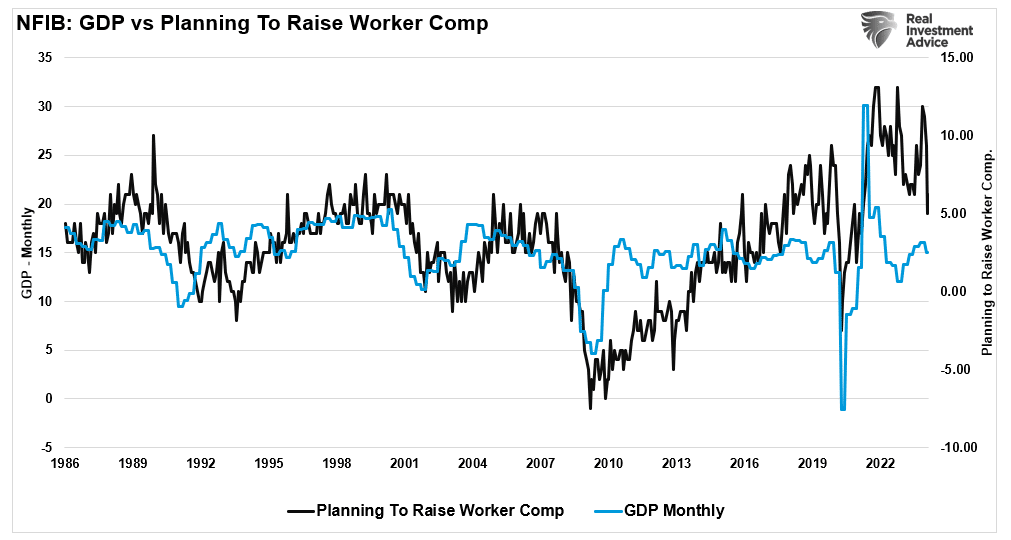

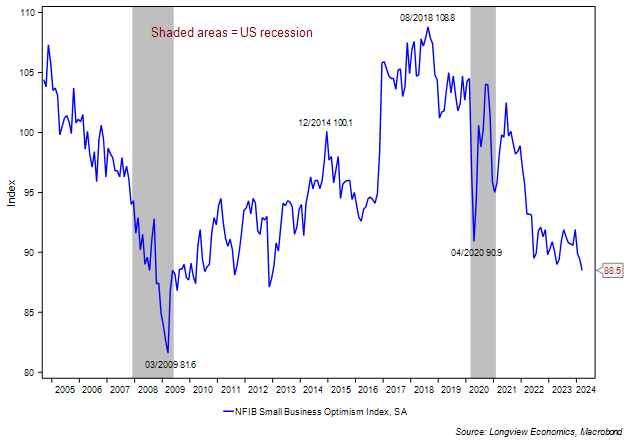

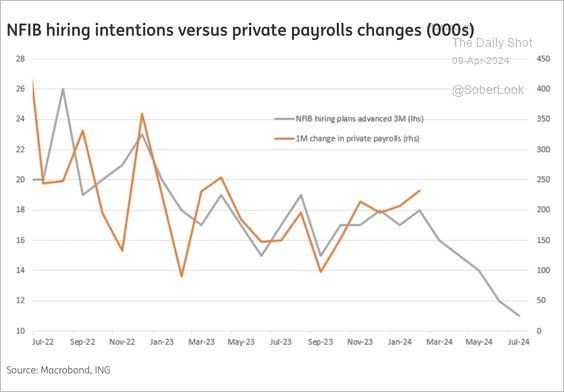

Economic Warning From The NFIB

The latest National Federation of Independent Business (NFIB) survey was an economic warning that departed widely from more robust governmental reports. Ina recent analysis of small businesses, we discussed the importance those business owners play in the economy.

“It is crucial to understand that small and mid-sized businesses comprise a substantial percentage of the U.S. economy. Roughly 60% of all companies in the U.S. have less than ten employees.

Small businesses drive the economy, employment, and wages. Therefore, the NFIB’s statements are highly relevant to the economy’s current state compared to the headline economic data from Government sources.”

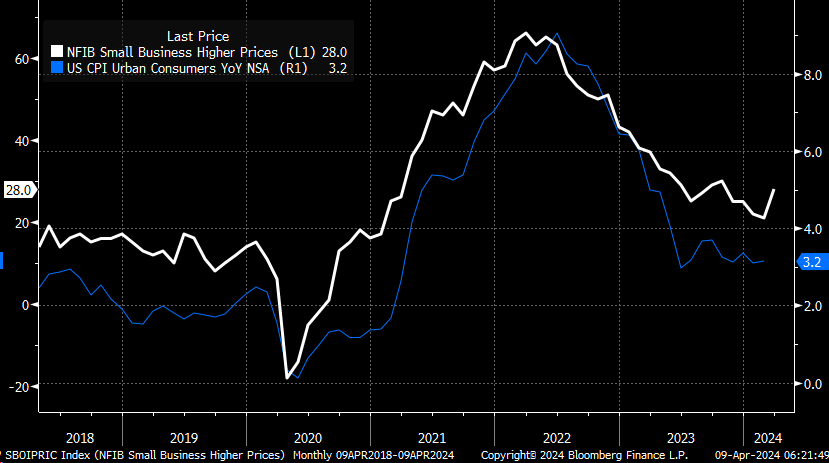

While recent government data on economic growth and employment remain robust, the NFIB small business confidence survey declined in its latest reading. Not only did it fall to the lowest level in 11 years, but, as far as an economic warning goes, it remained at levels historically associated with a recessionary economy.

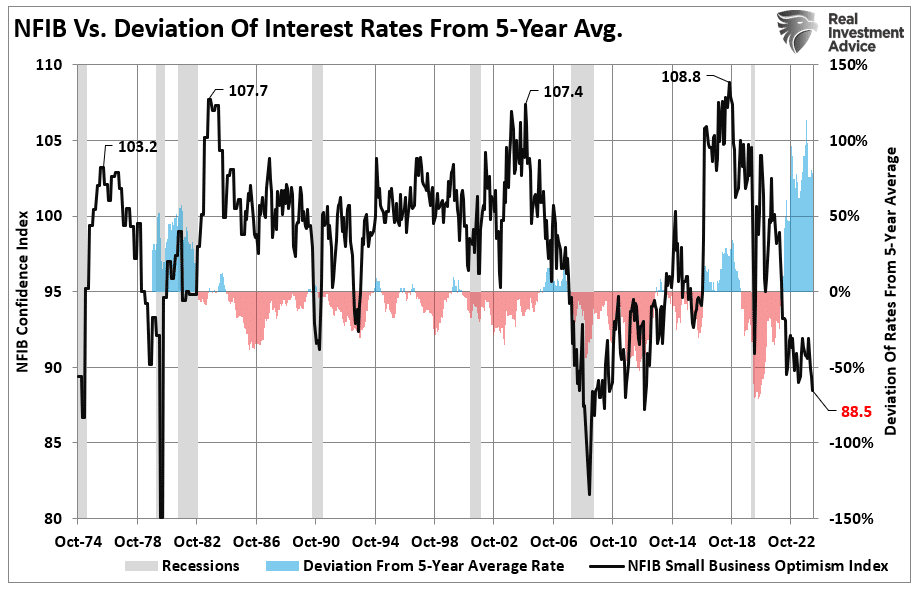

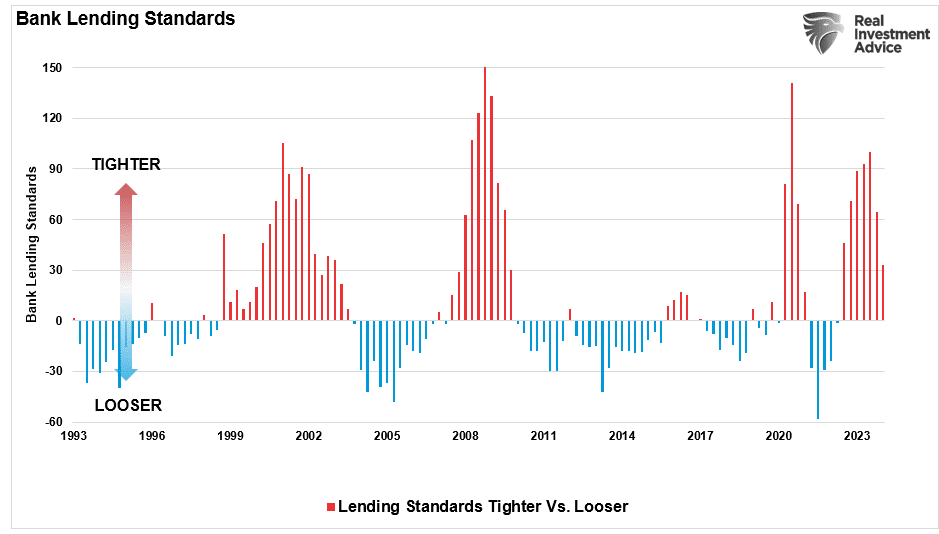

The decline in confidence should be unsurprising given the largest deviation of interest rates from their 5-year average since 1975. Higher borrowing costs impede business growth for small businesses, as they don’t have access to the bond market like major companies.

Therefore, as the economy slows and interest rates rise, small business owners turn to their local banks for operating loans. However, higher rates and tighter lending standards make access to capital more difficult.

Of course, given that capital is the lifeblood of any business, decisions on hiring, capital expenditures, and expansion hang in the balance.

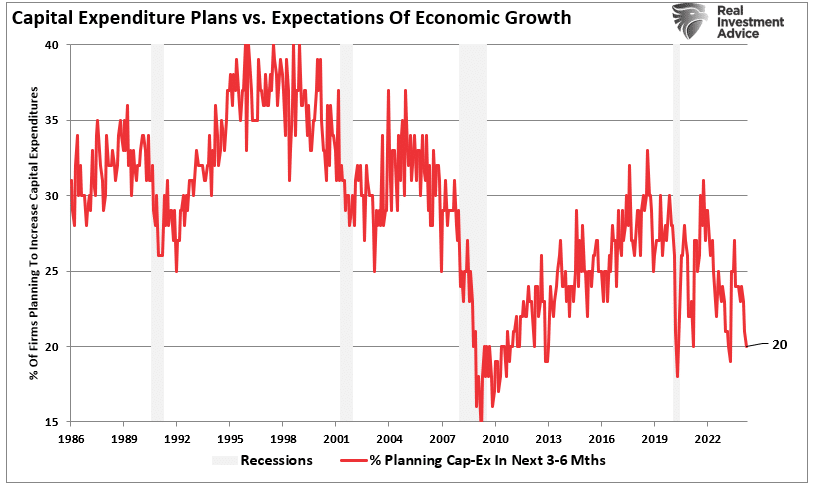

Economic Warning – Capital Expenditures

It should be unsurprising that if the economy were expanding as quickly as headline data suggests, business owners would be expending capital to increase capacity to meet rising demand. However, in the most recent NFIB report, the percentage of business owners planning capital expenditures over the 3-6 months dropped to the lowest level since the pandemic-driven shutdown.

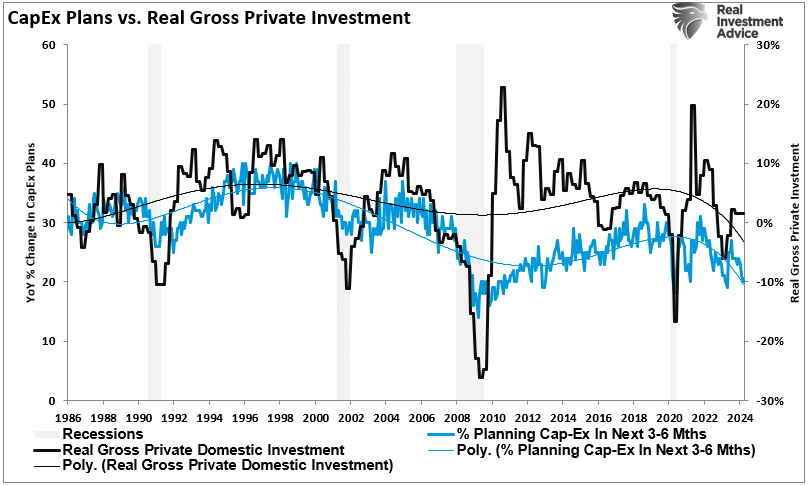

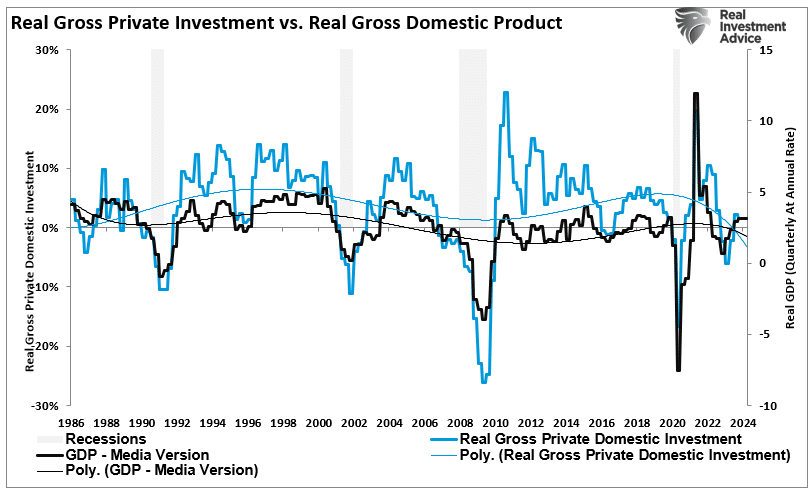

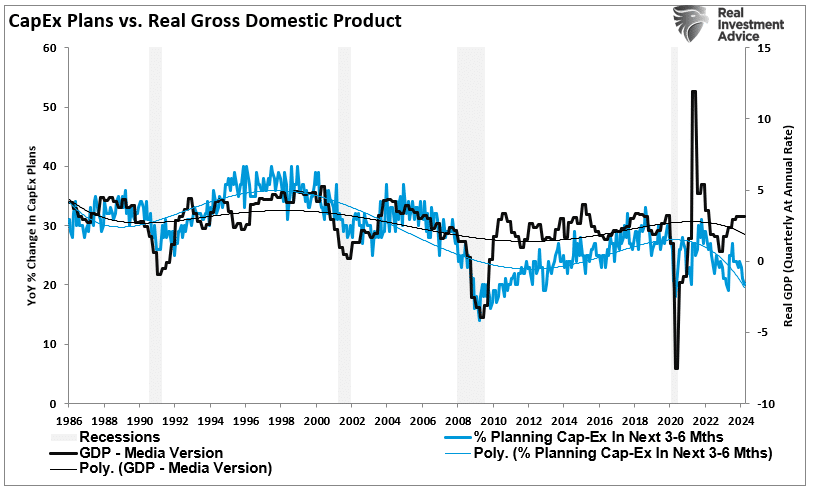

Again, given that small businesses comprise about 50% of the economy, there is more than just a casual relationship between their capital expenditure plans (CapEx) and real gross private investment, which is part of the GDP equation.

In other words, if small businesses cut back on CapEx, this will eventually translate into slower rates of private investment and, ultimately, economic growth in coming quarters.

As shown, the correlation between small business CapEx plans and economic growth should not be dismissed. While mainstream economists are becoming increasingly optimistic about an “economic reflation,” the economic warning between real GDP and CapEx suggests caution.

Of course, if small businesses are unwilling to increase CapEx, it is because there is a lack of demand to justify those expenditures. Therefore, if CapEx is falling, we should expect economic warnings from employment and sales.

Something Amiss With Sales

Many reasons feed into a small business owner’s decision NOT to invest in their business. As noted above, tighter bank lending standards and increased borrowing costs certainly weigh on that decision. However, if “business is booming,” business owners will find the capital needed to meet increased demand. However, looking deeper into the NFIB data, we find rising concerns about the “demand” side of the equation.

The NFIB publishes several data points from the survey concerning the “concerns” small business owners have. These cover many concerns, from government regulations to taxes, labor costs, sales, and other concerns confronting business owners. When it comes to the “demand” side of the equation, there are three crucial categories:

Poor sales (demand),

Cost of labor (the most significant expense to any business), and

Is it a “Good time to expand?”(Capex)

In the chart below, I have inverted “Good time to expand,” so it correlates with rising concerns about the cost of labor and poor sales. What should be obvious is that the average of these concerns escalates as economic growth weakens (recessionary periods) and falls during economic recoveries. Currently, these rising concerns should provide an economic warning to economists.

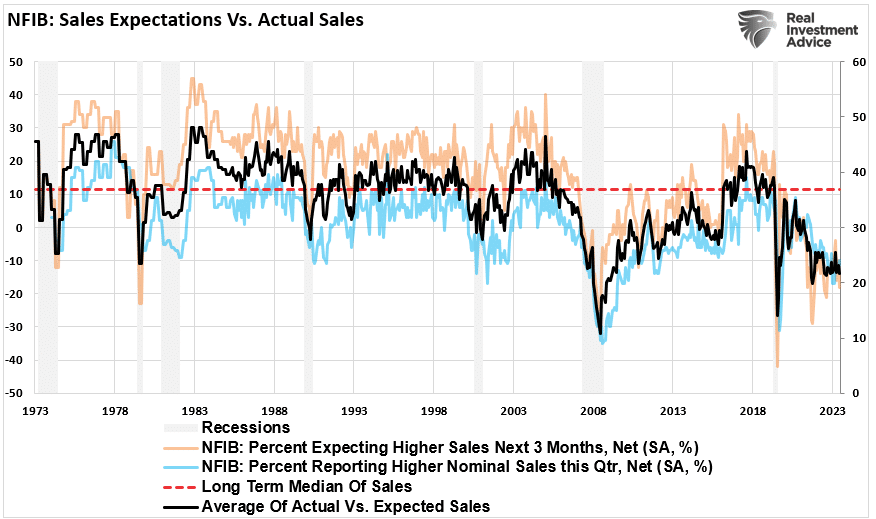

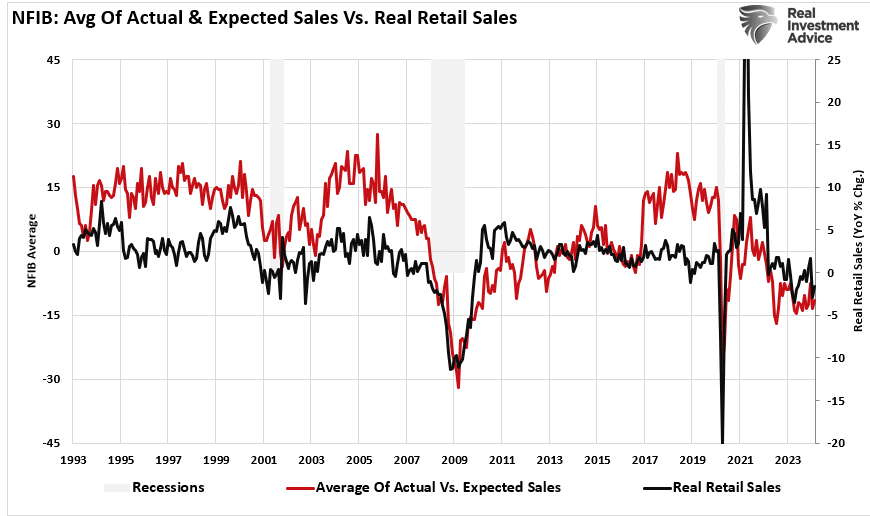

Examining sales and employment figures can help us understand why business owners remain pessimistic about the overall economy. The chart below shows the NFIB members’ sales expectations over the next quarter compared to the previous quarter. The black line is the average of both with a long-term median.

Unsurprisingly, business owners are always optimistic that sales will improve in the next quarter. However, actual sales tend to fall short of those expectations. The two have a very high correlation, which is why the average of both provides valuable information. Sales expectations and actual sales are well below levels typically witnessed during recessions. With sales (demand) weak, there is little need to increase production (supply) substantially.

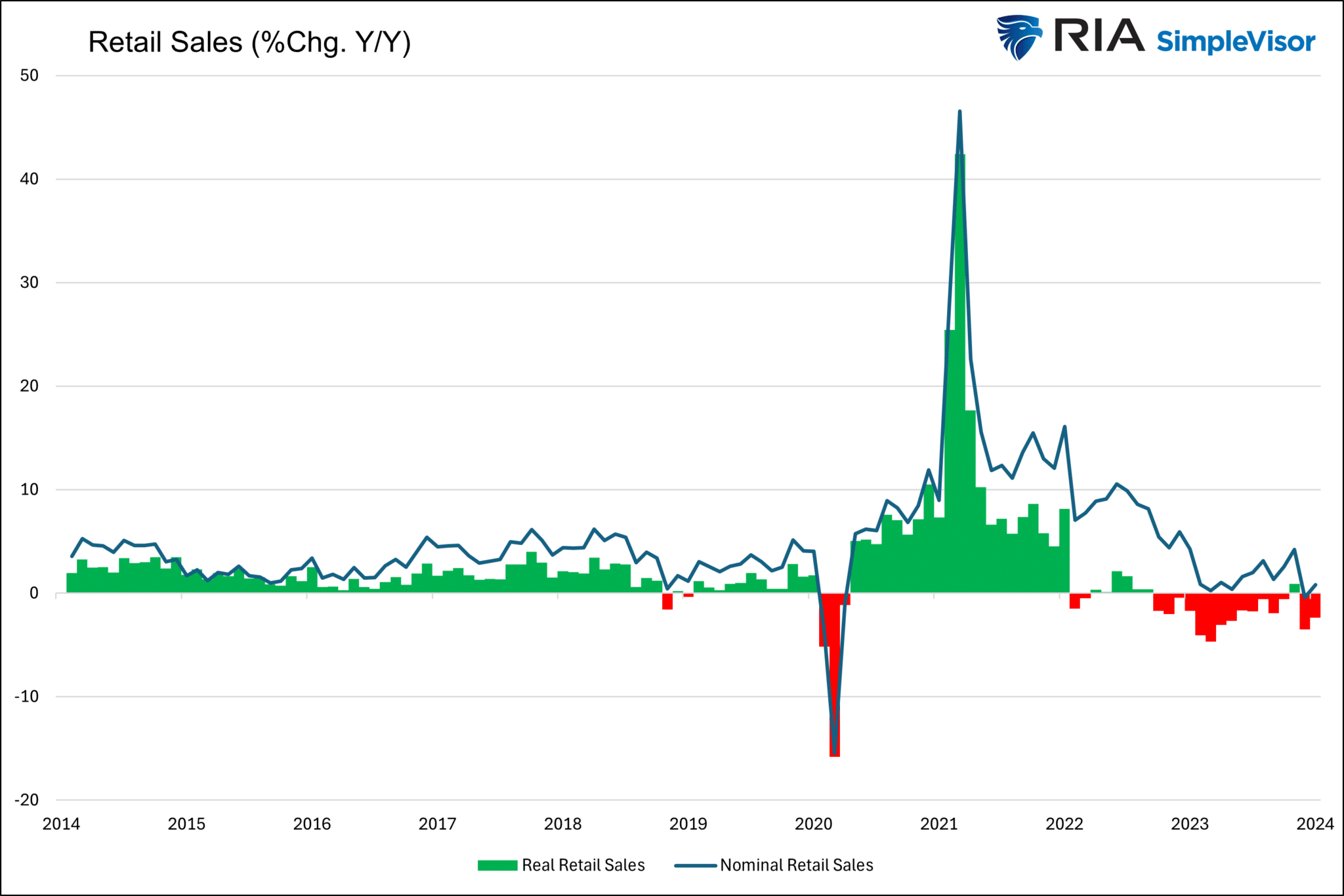

Here is the economic warning to pay attention to. Real retail sales comprise about 40% of personal consumption expenditures (PCE), roughly 70% of the economic growth rate. The decline in the average of actual and expected sales of small businesses suggests weaker retail sales and, by extension, a slower economic growth rate.

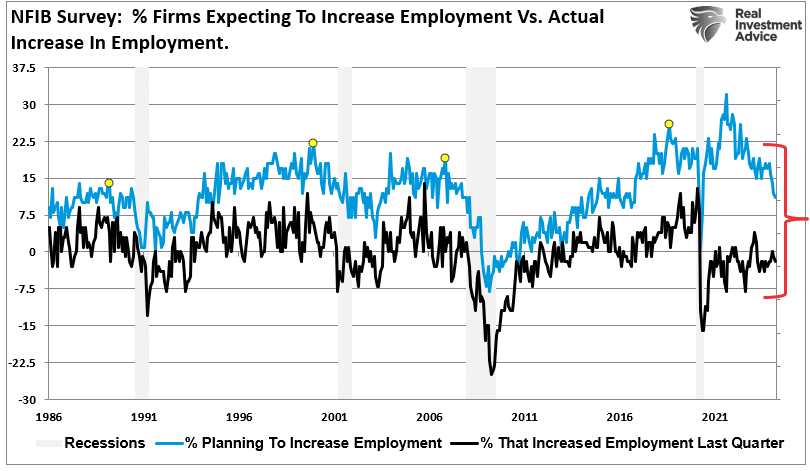

EmploymentWarning

The demand side of the economic equation is crucially important. If the demand for a business owner’s products or services declines, there is little need to increase employment. Therefore, if economic growth was as robust as headlines suggest, why are small businesses’ plans to increase employment declining sharply?

Furthermore, when demand falls, business owners look to cut operating costs to protect profitability. While cutting future employment is part of that equation, so are plans to raise worker compensation.

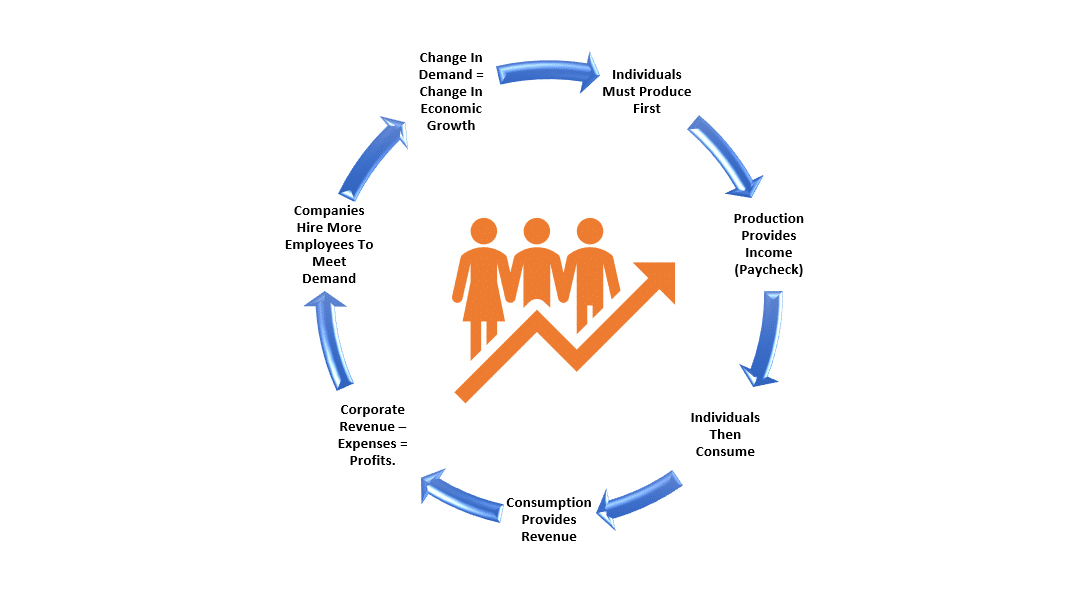

The last chart is crucial. The U.S. is a consumption-based economy. However, consumers can not consume without producing something first. Production must come first to generate the income needed for that consumption. The cycle is displayed below.

As employees receive fewer compensation increases (raises, bonuses, etc.) amid rising living costs, they cut consumption, which translates into slower economic growth rates. In turn, business owners cut employment and compensation further. It is a virtual spiral that historically ends in recession.

While this time could certainly be different, the economic warnings from the NFIB survey should not be dismissed. The data could explain why the Fed is adamant about cutting rates.

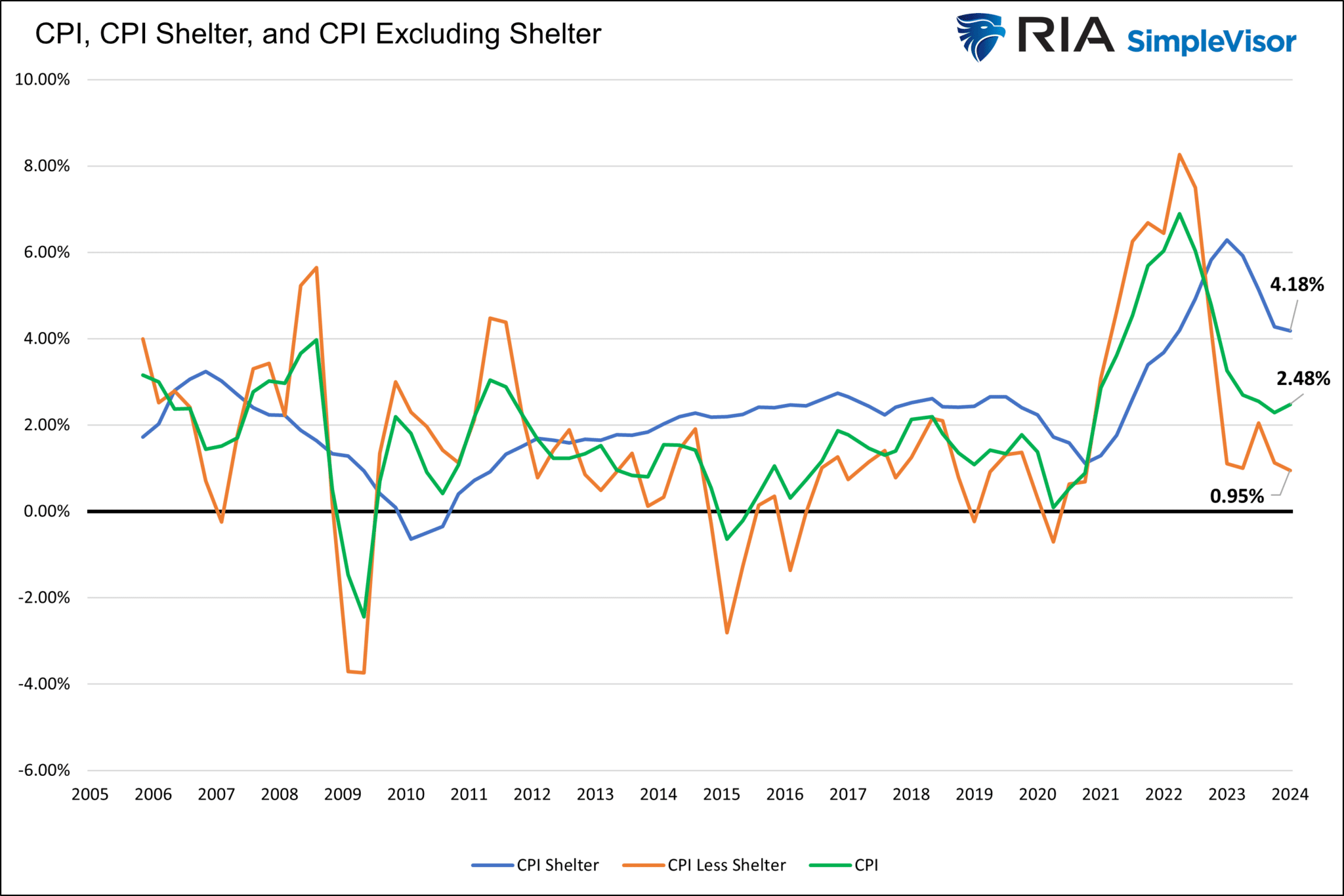

Inflation Is Heading Lower Despite The Reflation Narrative

The narrative de jour scaring bond investors is reflation. The recent stickiness and even uptick in prices have investors worried that inflation is headed higher again. The concern is not without merit, as several items in the inflation reports are increasing in price. However, before buying into the narrative, we want to share our research that argues CPI could be much lower in the coming nine months to a year.

We have often written about how the surge in shelter costs within the CPI inflation calculation grossly distorts CPI. The problem is not necessarily whether shelter costs, primarily rent and imputed rent, should be over a third of CPI. Instead, we bemoan the lagging nature of the BLS’ CPI shelter data. The price of bread, cell phones, and every other good and service in CPI is based on current prices. Rents, however, are based on surveys. Given that only about 1/12ths of rents are reset in any given month, 11/12ths of the data is old. Unlike the prices of other goods and services, the BLS effectively uses rent and imputed rental prices that are about six months stale on average.

With this lag in mind, we focus on the Cleveland Fed’s All Tenants Regressed Rent Index (ATRR) and its New Tenant Rent Index (NTR) along with the BLS’ CPI, CPI-Shelter, and CPI-less Shelter. Our analysis of this data exposes the lag and, more importantly, forecasts how current rental prices will impact CPI later this year. For starters, we share the graph below. CPI Shelter costs are well above CPI, and CPI excluding Shelter Costs are below CPI. After the Market Update below, we continue this discussion.

What To Watch Today

Earnings

Economy

Market Trading Update

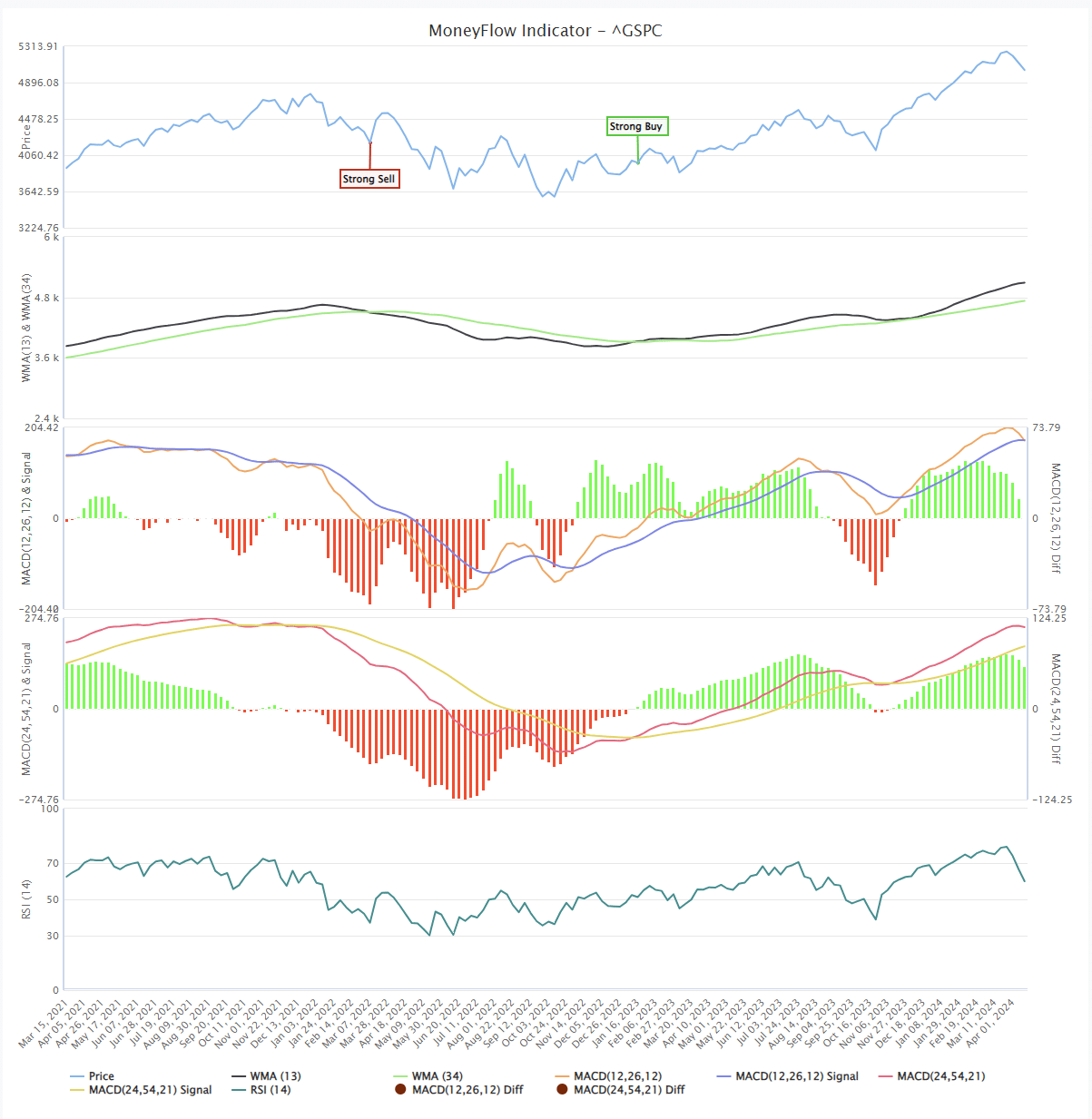

As noted yesterday, the market has been under decent selling pressure and declined for four consecutive days. With markets decently oversold, yesterday’s early bounce was unsurprising, but, as has been the case over the last several days, the rally failed. Notably, however, the market did close off the lows after an initial test of the 23.6% retracement from the previous peak. The market is oversold enough for a reflexive bounce that could last a few days. However, with the MACD on a solid “sell signal,” we should suggest using rallies to rebalance equity risk until a new “buy signal” is triggered.

The one thing to note is that the WEEKLY money flow signal is close to triggering a “sell signal.” The last time the weekly signal was triggered was in August of last year, preceding the sell-off into October. That signal suggests that we are likely not done with the current correction process, so we will want to navigate markets carefully until we know.

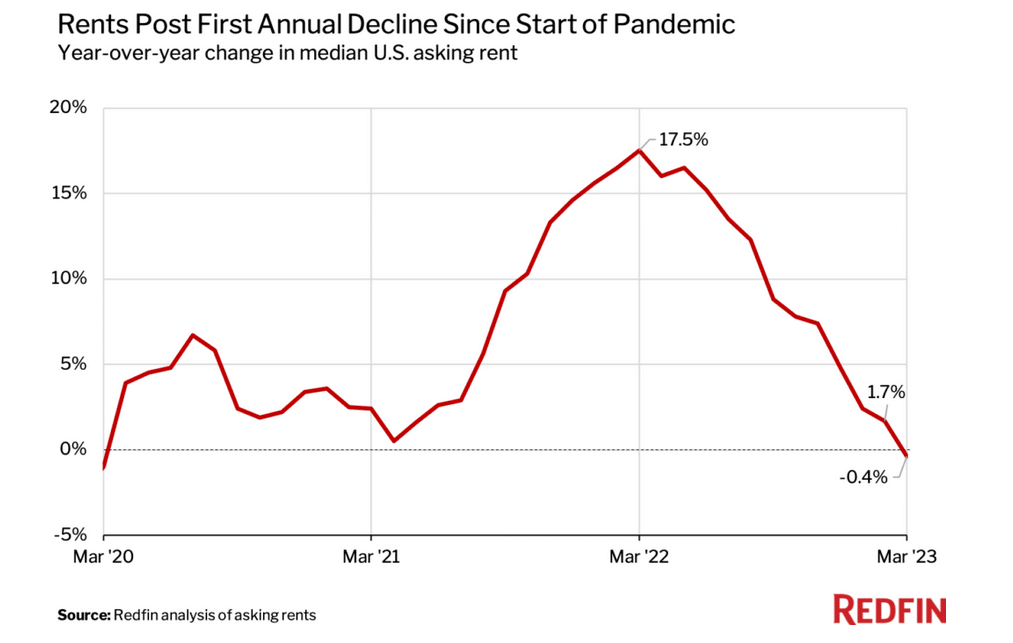

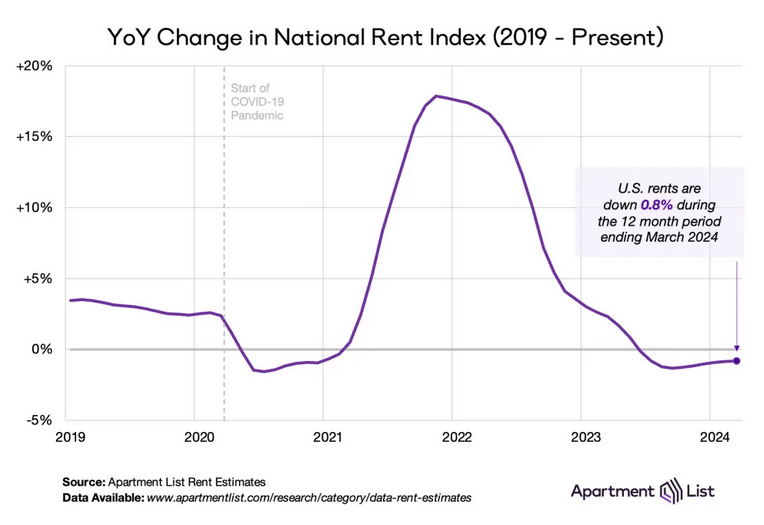

Shelter Costs Are Headed Lower

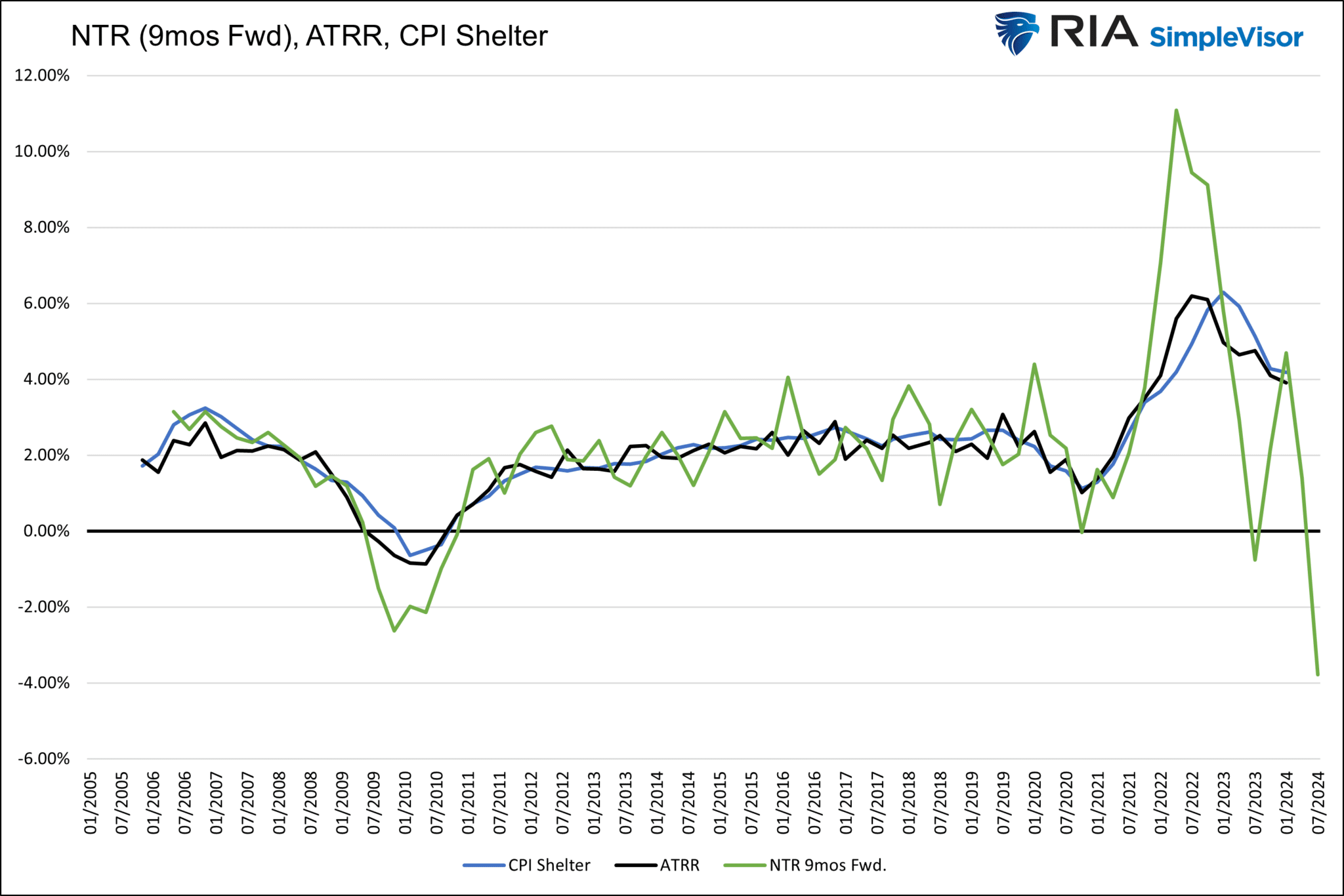

The graph below charts the Cleveland Fed’s Average Tenant Rentals (ATRR) and their New Tenant Rentals (NTR) alongside BLS CPI-Shelter. We pushed the NTR data forward nine months to better show how well it leads the ATRR and CPI Shelter prices. There are a few essential takeaways from the graph. First, the ATRR and CPI-Shelter are nearly identical. Second, NTR is more volatile than the other two rent indicators because it’s not an average. Third, and most importantly, NTR tends to lead CPI Shelter and ATRR by nine months.

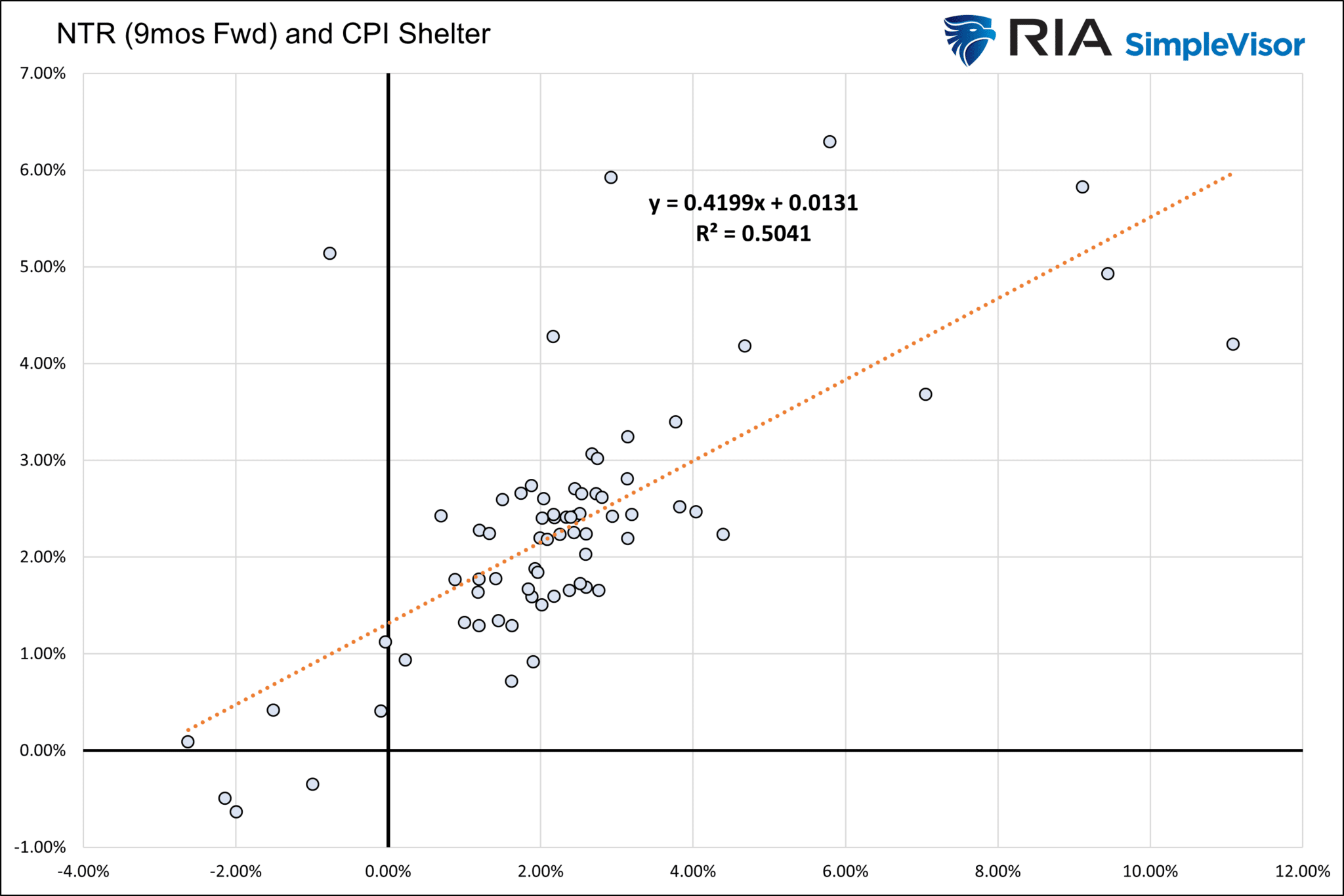

The scatter plot below highlights the strong correlation between NTR nine months in advance and CPI Shelter. The outliers are a function of the volatility of the NTR data. If we presume the relationship holds and, to be conservative, ATR is closer to zero than negative, we should expect inflation to be nearing 2% by year-end.

The NTR data is volatile from quarter to quarter, but it is in line with other private measures of rent. For example, the graphs below the scatter plot show that RedFin’s and Apartment List’s proprietary rent price indexes are also declining on a yearly basis.

When CPI Shelter catches up with market prices, we should see inflation figures decline again. With it, we suspect the market will start pricing in more rate cuts for later this year, and the Fed will likely become more dovish.

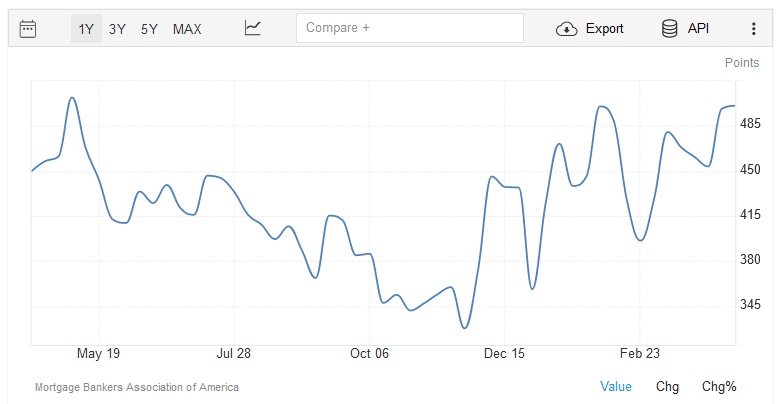

Mortgage Refinancings Are Picking Up…Why?

The Mortgage Bankers Association (MBA) mortgage refinance index just posted its highest point in nearly a year, as shown below. Given that mortgage rates have not fallen significantly, the rise in the index is troubling. Most likely, an increasing number of mortgage holders are draining equity from their houses at higher rates than their prior mortgage rate. Typically, customers would rely on credit cards to meet short-term crunches. Might those be maxed out?

While the refi index has been climbing over the past few months and is near the highs going back to late 2022, it is still well below levels when mortgage rates were much lower. From 1990 to the present, the average for the index is 1844, over three times higher than the current reading.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

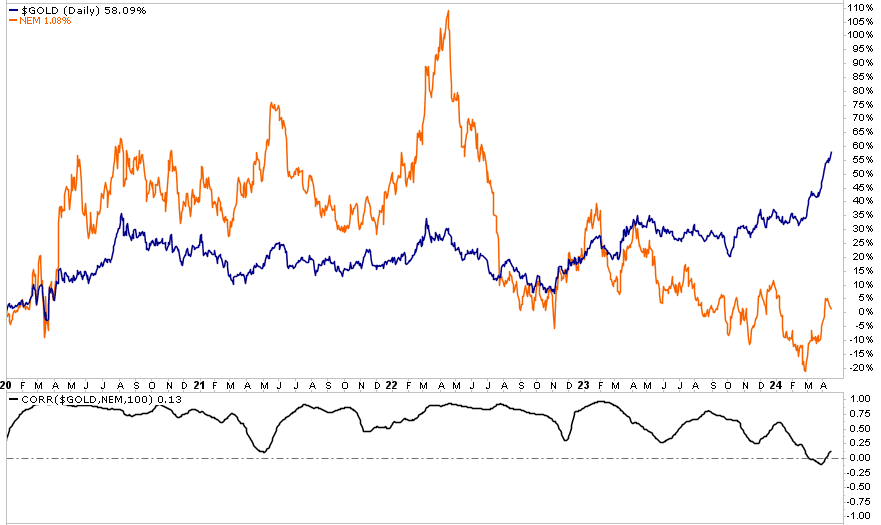

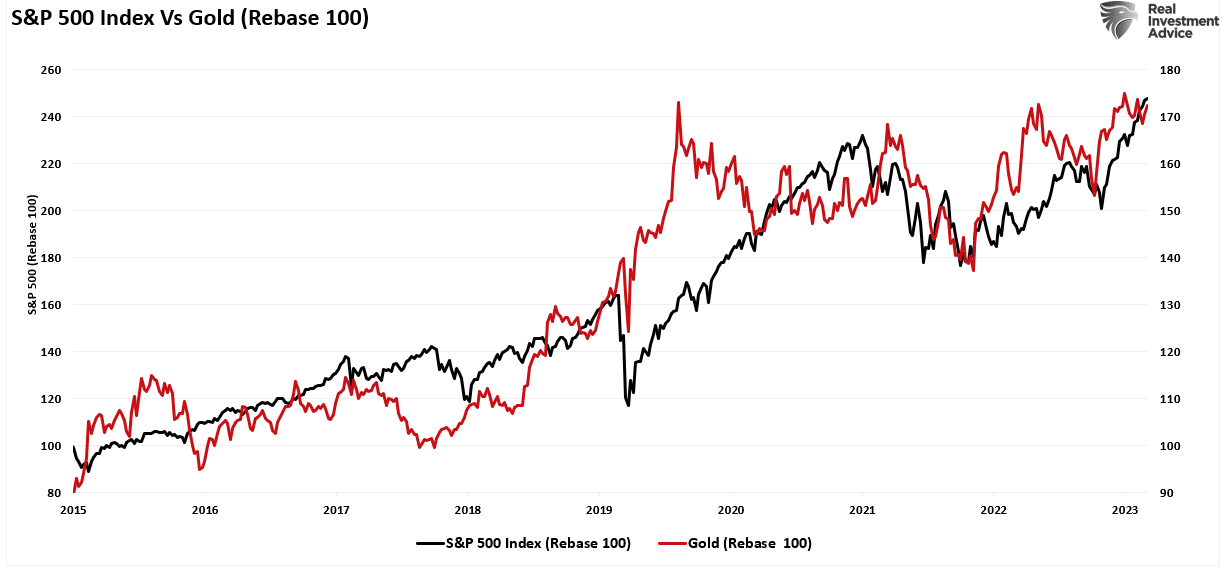

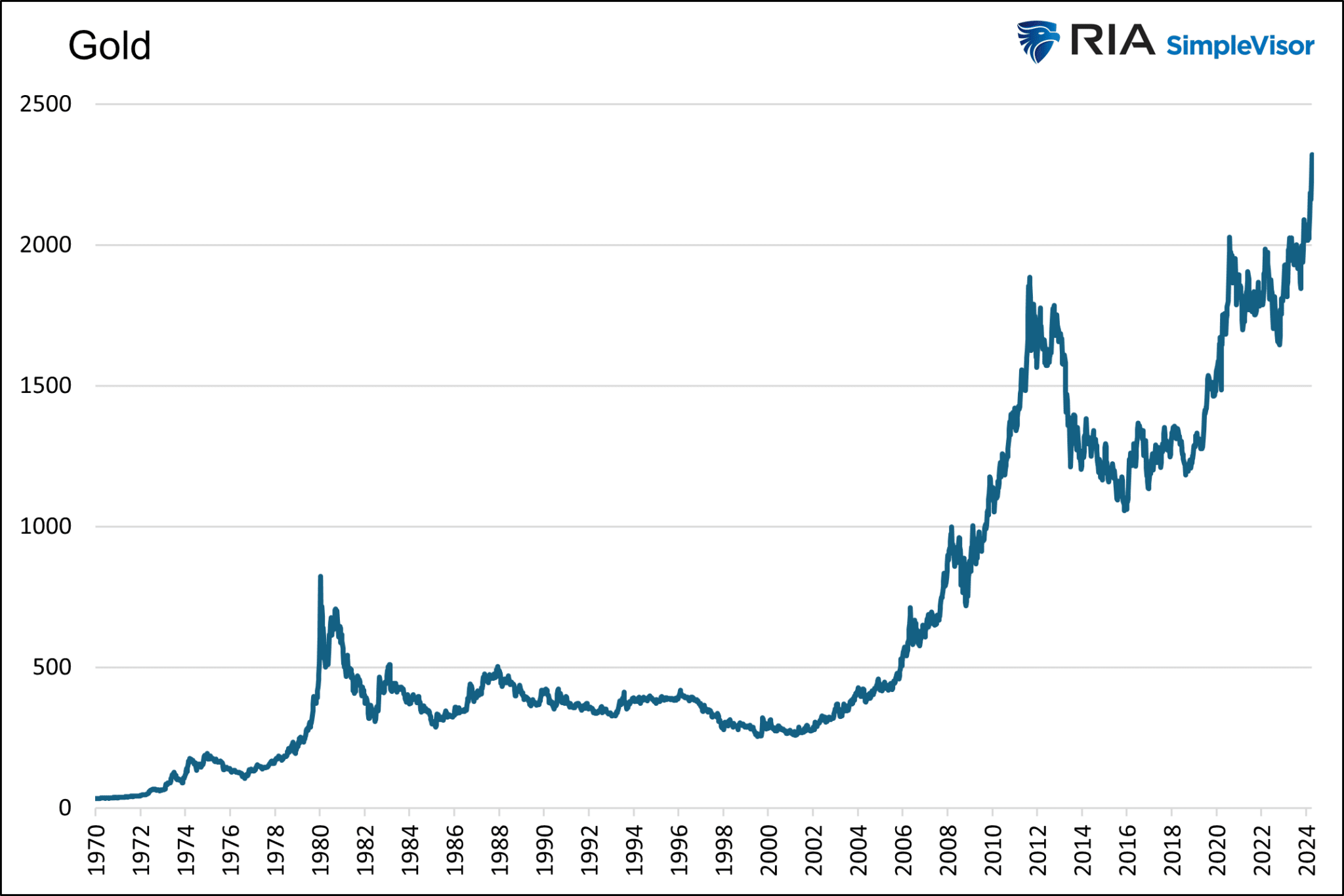

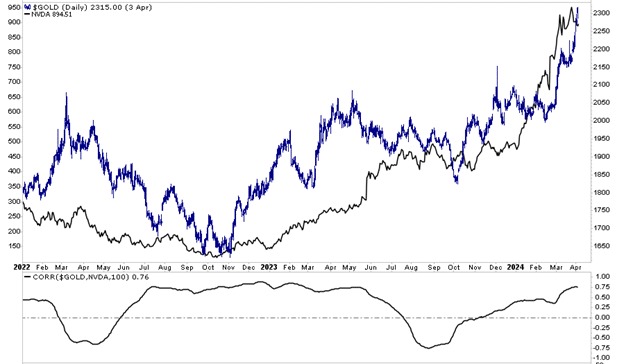

Gold Miners And Gold Are Not The Same

Yesterday’s Commentary discussed the coming halving of Bitcoin and its pros and cons for Bitcoin miners. While mining for gold is an entirely different endeavor, a couple of readers asked us to opine on the differences between holding gold and gold miners. One common thread between gold and Bitcoin miners is that the easiest, cheapest gold or Bitcoin is mined first. Each additional ounce of gold or bitcoin becomes more expensive to mine.

From a gold miners perspective, their labor and equipment expenses have risen considerably with inflation. Further, as it becomes more difficult to find gold, they must mine in more remote places. That comes with higher costs and less yield. While the added expenses of finding new gold are a slow upward trend, the inflation surge is hitting miners now. Accordingly, even though gold prices are up significantly, mining costs have also risen appreciably. If you want to own gold, we think buying gold bullion or an ETF is the best way to express such an investment. Suppose you want leverage on the price of gold. Further, you are willing to be subject to the costs of running a mining operation, including bad management decisions. In that case, gold miners may be a suitable investment. As with any stock, there are efficient and non-efficient gold miners. Do your due diligence.

The graph below shows that since 2020, gold has risen by 60%, while Newmont (NEM), the largest holding of the popular GDX gold mining ETF, is flat. The lower graph shows the correlation between gold and NEM has been close to zero for the last two months.

What To Watch Today

Earnings

Economy

Market Trading Update

The market continues its current correction process. This correction, which we discussed was coming for the last two months, is in process. We noted previously that “sellers live higher, buyers live lower,” which is why the market is declining to try and find where buyers are currently “living.”

As shown, there is a fairly sizable gap between the current and next levels, where most of the volume occurred. However, if that is where the market is ultimately headed, it most likely won’t do it in a straight line. With the market decently oversold and following several consecutive days of selling, a decent bounce toward the 50-DMA is likely. Use that bounce to reduce risk and add hedges as needed.

Given that algorithms and programmatic trading do a large chunk of daily trading activity, it is difficult to know exactly where those programs will turn from “selling rips” back to “buying dips.” However, we have been through these corrections before, and they will end. While corrections are never fun, they provide investors with a great opportunity to buy positions they want at cheaper prices.

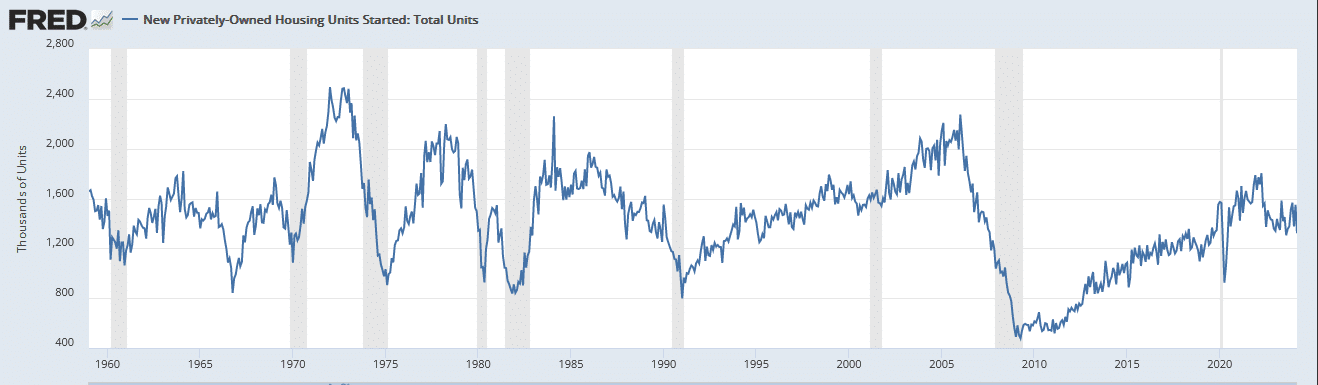

Housing Starts Like Multifamily Building Permits Normalize

Yesterday, we discussed the decline in multifamily building permits and the expected soon-to-come decline in multifamily construction projects. We also shared how the reductions will result in job losses in the construction industry and become a headwind for inflation. Similarly, new housing permits show weakness. Per the Census Bureau, housing starts plunged 14.7% month-over-month in March to an annualized rate of 1.321 million. That was well below forecasts of 1.48 million. It is the lowest reading since August and the biggest decline since April 2020. As we share below, housing starts are now close to pre-pandemic levels.

Wall Street Sticks With 2 Cuts While Powell Buys Time

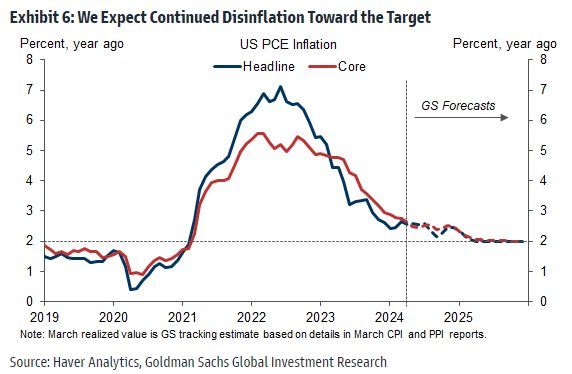

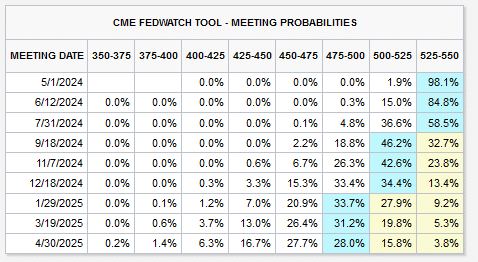

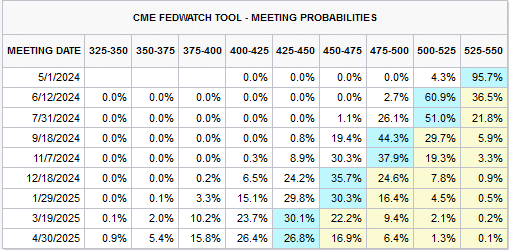

Per BofA, 76% of institutional fund managers polled still expect two or more Fed interest rate cuts in 2024, while 8% project no rate cut at all. The survey was conducted in early April before comments from Jerome Powell on Tuesday. The first graph below shows that Goldman Sachs forecasts that inflation’s rate of decline may be slowing, but it should reach the Fed’s 2% target in early 2025. The second table, courtesy of the CME, shows the market is mixed as to whether there will be one or two cuts by year-end. However, Fed Fund futures imply a zero chance of rate hikes.

On Tuesday, Jerome Powell confirmed what other Fed speakers have been saying. The expected rate cuts are still on the table but will likely be pushed back. Further, Powell raises some doubt about whether the Fed may cut at all this year. However, despite what appears to be a more hawkish tone, we are not hearing anything from Powell regarding the possibility of rate hikes. The recent tightening of financial conditions via higher bond yields and weaker stock prices may also provide the Fed a little comfort in their projections.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

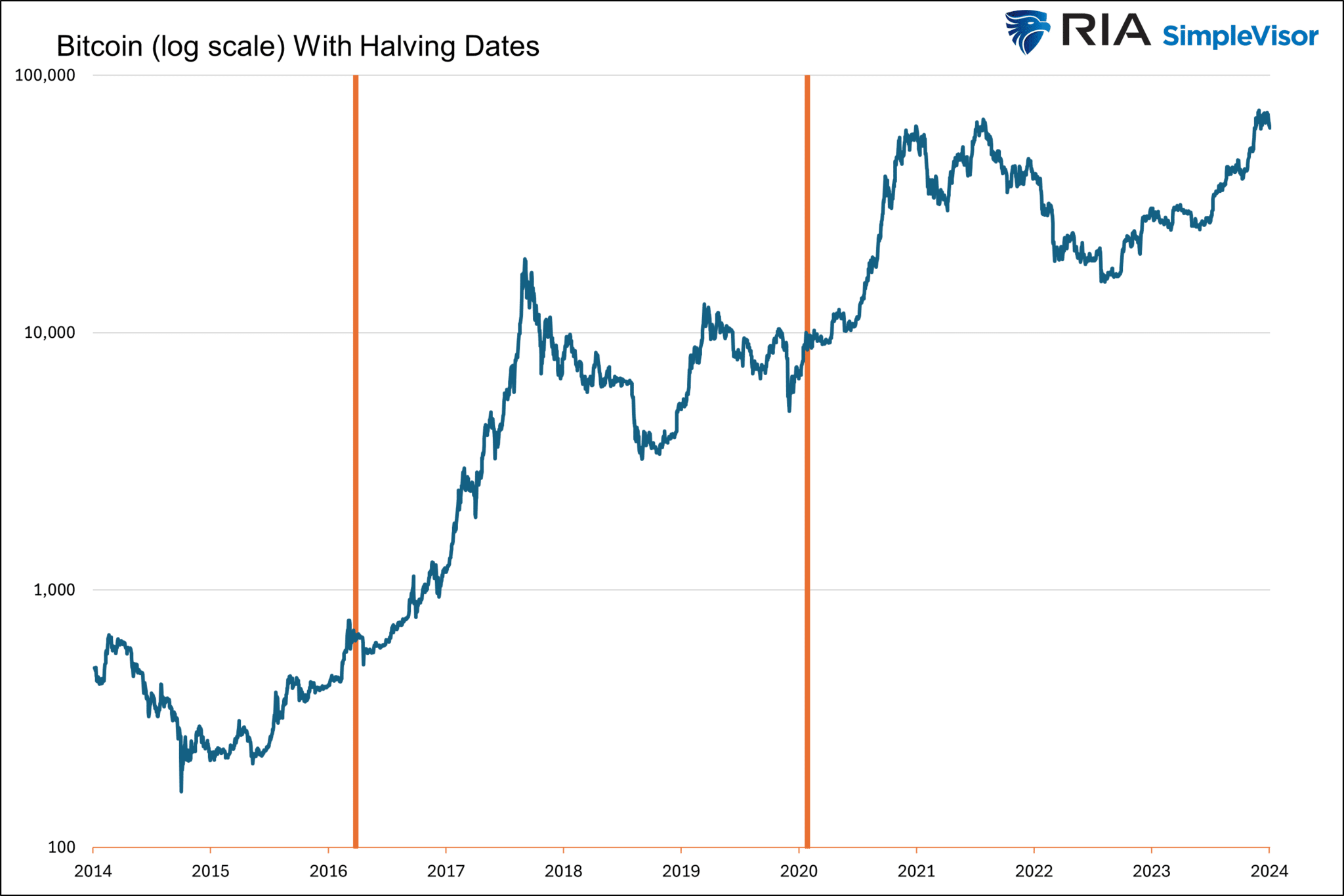

Bitcoin Is Halving On Saturday

On Saturday, April 20, Bitcoin will be halving. Halving is an essential part of what makes Bitcoin unique. The halving process means that bitcoin miners will receive half as many bitcoins for verifying blockchain transactions. Currently, they receive 6.25 bitcoin for every 210,000 network blocks they verify. After April 20, they will only get 3.125. The process is similar to the actual mining of precious metals and some other commodities. As the mineable supply of a commodity declines, mining costs rise. Similarly, the algorithms to verify transactions get more complex, and at the same time, the reward for mining is less. The mechanism is designed to keep a lid on the supply of Bitcoin. Remember that the number of Bitcoin is capped at 21 million tokens.

From an investor’s point of view, there is much discussion about what the halving may mean for prices. The easy takeaway is that halving removes incentives to mine Bitcoin, which, in theory, should reduce supply. However, the halving is a known event, and the market has plenty of time to price the event before it occurs. As the graph below shows, at the last halving in May 2020, Bitcoin rose 25% in the 30 days leading up to the event and another 15% in the following 30 days. The prior halving in 2016 saw Bitcoin increase by 13%, 30 days in advance, but it gave up 10% in the 30 days following. With Bitcoin already up 48% year to date, this coming halving may look more like the 2012 event than the last one.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we touched on the strong retail sales data that may not be as strong as headlines suggest. Nonetheless, while this may have longer-term implications for the market, it is all about the technical analysis in the short term. On Monday, the market broke below the 50-DMA, confirming the recent break of the 20-DMA as the start of a correction phase. Yesterday, the market attempted to rally, but selling pressure remained. As shown, money flows remain negative, suggesting lower prices in the near future, with the number of stocks below their 50-DMA dropping sharply. With the market down nearly 4% from the recent peak, we are likely close to a reflexive rally before the correction phase continues. Use any such rally to reduce equity risk as needed for now.

Crucially, this is likely the 5-10% correction we have written about previously. With still very bullish sentiment on the overall market, this will likely be a buying opportunity in the months ahead.

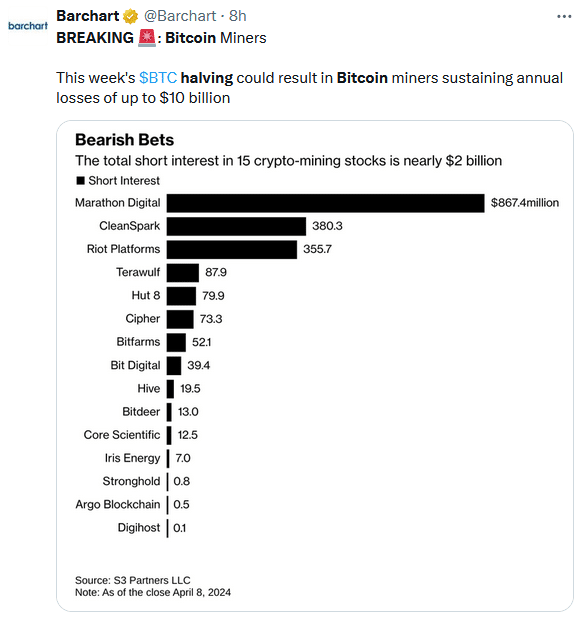

How Will The Halving Effect The Miners

Bitcoin miners will see some positive and negative effects from the coming halving. On the bright side, the higher cost of mining should reduce the competition. Additionally, larger, more efficient firms may be able to purchase the assets of lesser competitive smaller firms at a discount. However, the miners will essentially be paid less to do the same work they are currently doing. Therefore, they will have to increase their capital expenditures to upgrade to more efficient equipment and find ways to reduce their energy costs. Buying up smaller miners may also provide economies of scale to help further. Technology will advance over time, which should lead to more profitability. Still, the initial effect will be a drag on earnings for the largest miners and possibly bankruptcy for smaller, less productive miners.

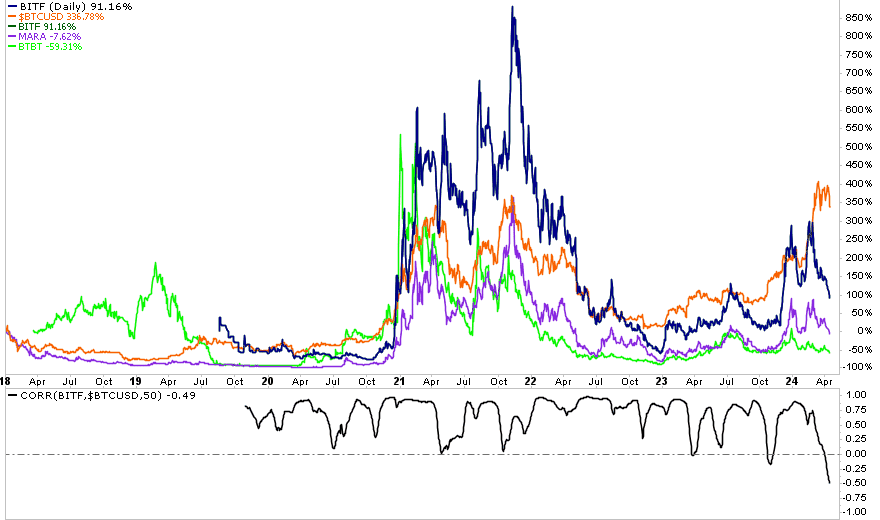

The bar graph below shows investors putting large short bets on Bitcoin miners in anticipation of the event. The second graph compares the price of Bitcoin to the three largest publicly traded miners. As shown, they have recently traded much weaker than Bitcoin, and as seen in the lower graph, the correlation between Bitcoin and the miner’s prices is now negative.

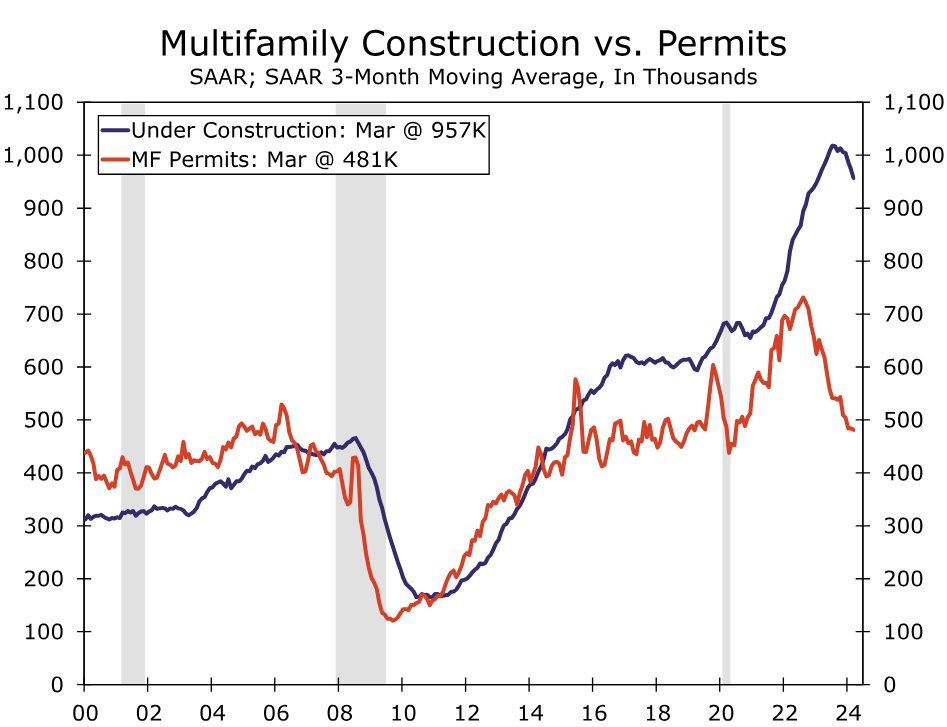

The Multifamily Construction Boom Is Ending

The graph below points to both a boom in new multifamily structures being built as well as a normalization going forward. The blue line shows that there are almost one million multifamily buildings that will soon be finished. That is about 400k more than before the pandemic. The construction boom helped increase construction payrolls and impacted construction materials’ prices. The red line shows that permits for new multifamily projects have now fallen entirely back to pre-pandemic levels. Therefore, we should expect the number of new buildings hitting the market to decline toward pre-pandemic levels. Equally important, the upward impact on payrolls and prices will also normalize.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

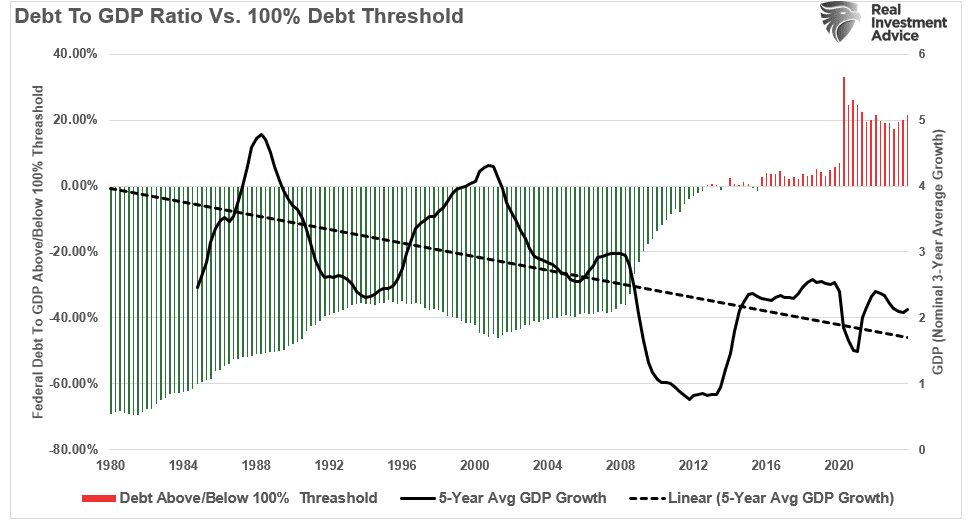

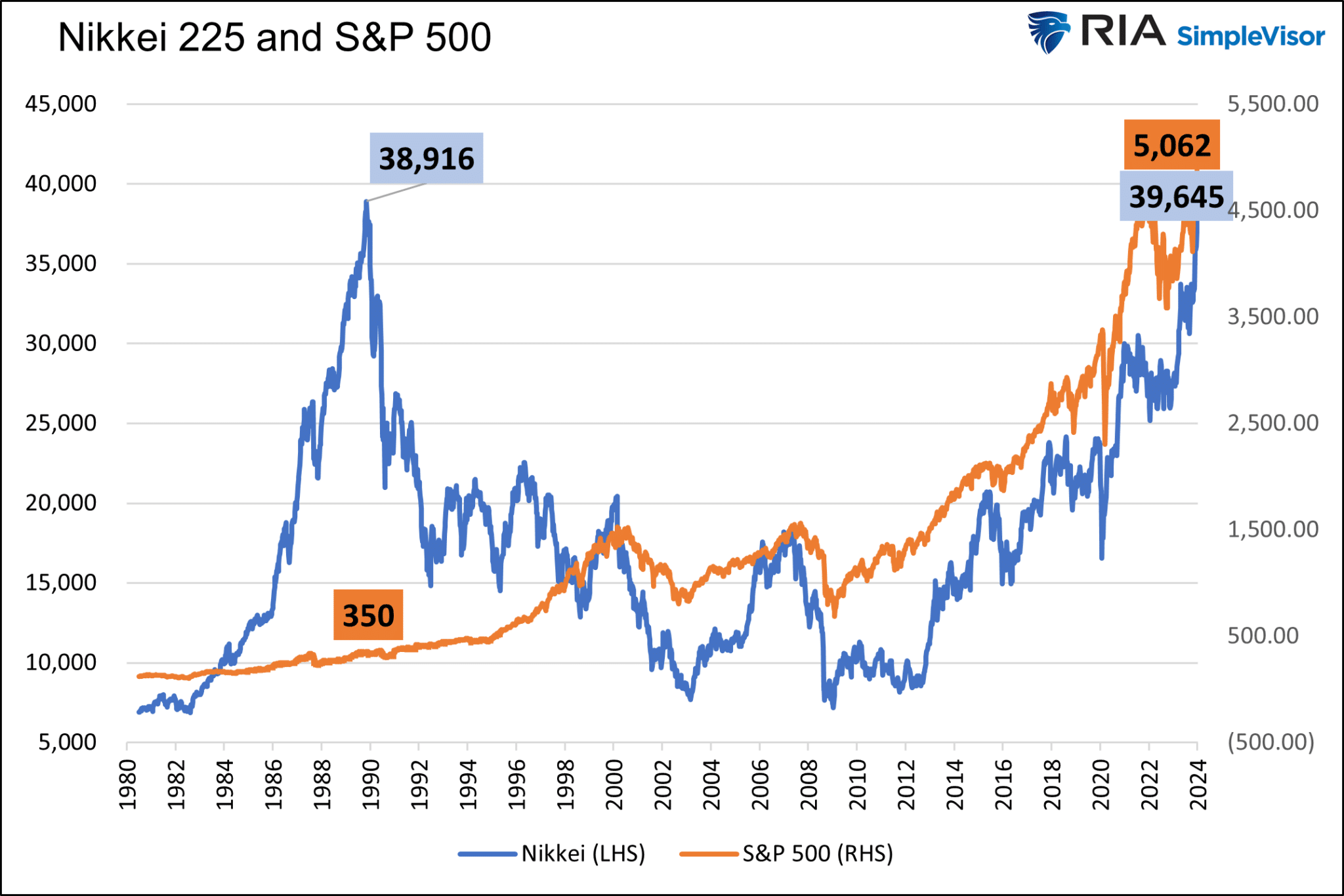

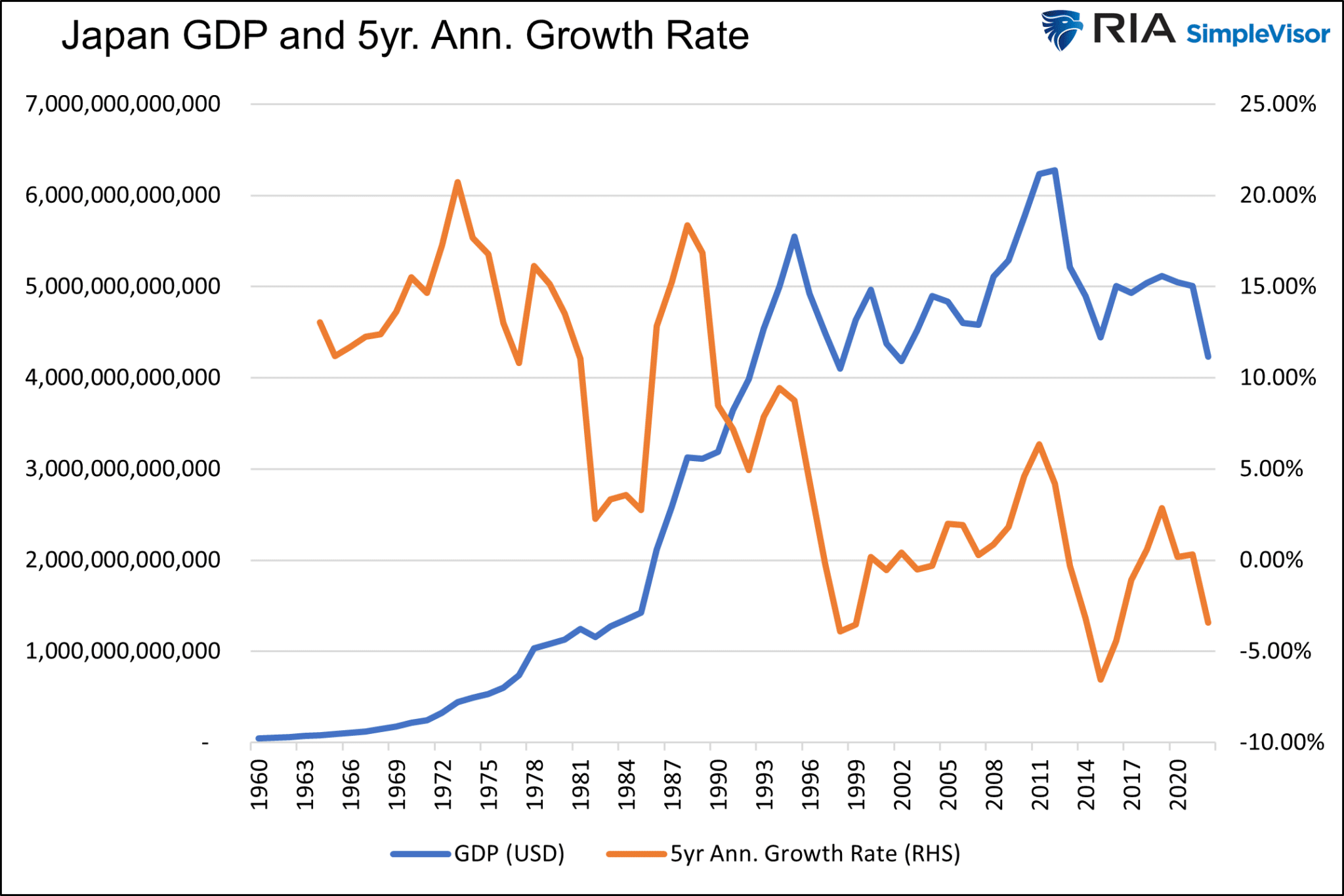

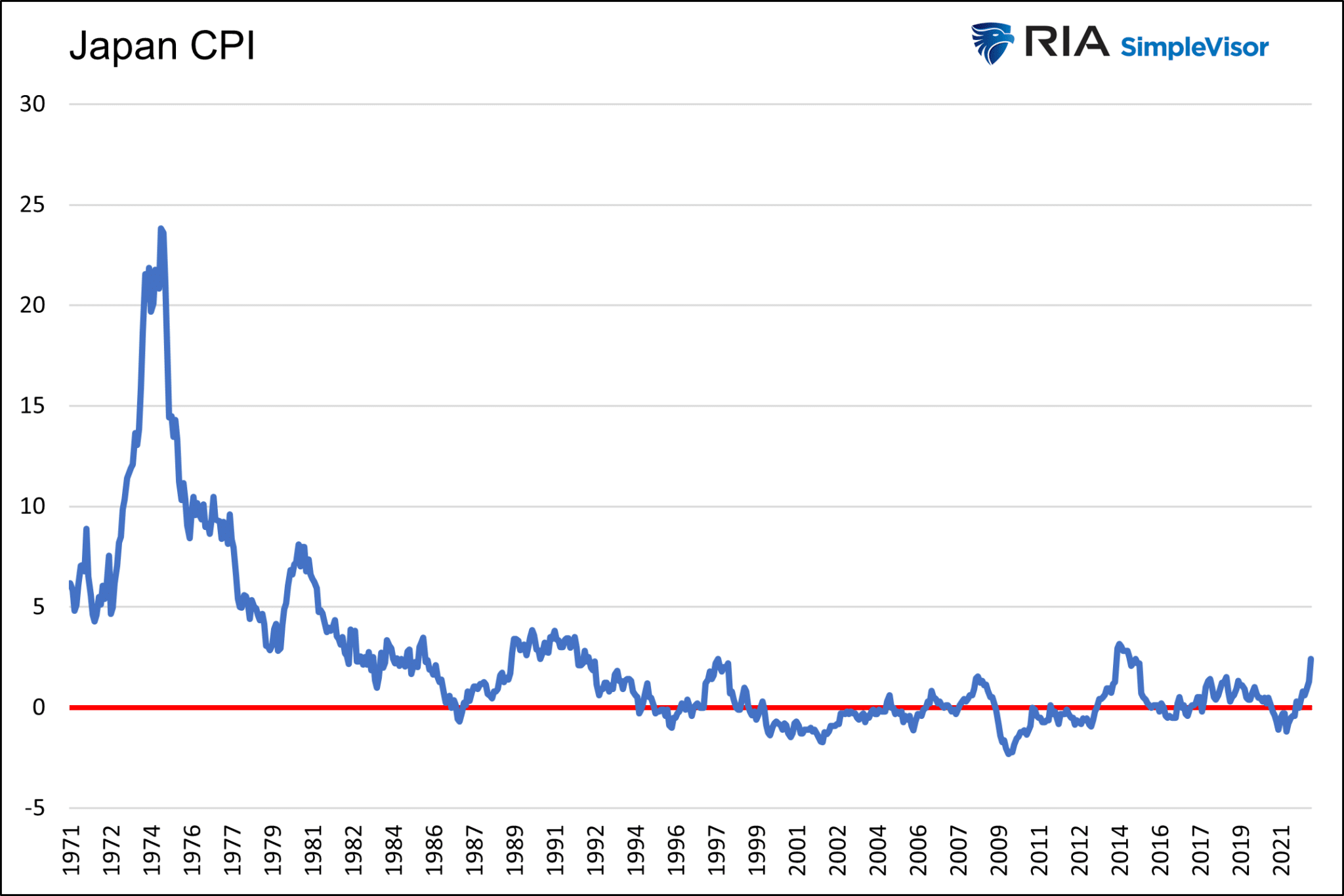

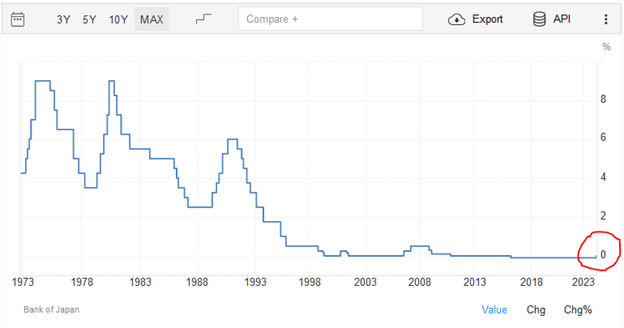

Are We On Japans Path Of Stagnation?

We recently wrote Japan’s Lost Decades to appreciate better why Japan’s GDP is smaller than it was in 1995 and why it took 35 years for its stock market to set its recent record high.

Many pundits claim the U.S. is following Japan’s path. The path includes a stagnant economy, massive government debt, and a central bank that must dominate financial markets to keep the economy and financial markets afloat.

There is merit to that opinion. The U.S. government has excessive debt and is increasingly negligent in managing its budget. Also, the nation’s economic growth rate has been trending lower for thirty years, and fiscal dominance is becoming the norm, not the exception.

While we may be on a similar path as Japan, we are not nearly as far along. There are many differences between Japan and the United States worth considering.

All Asset Bubbles Are Not Alike

At the heart of Japan’s current problems were its massive real estate and stock bubbles that popped in 1989.

From 1956 to 1986 land prices in Japan increased by 5000% even though consumer prices only doubled in that time.

By 1990 the Japanese real estate market was valued at 4x the value of real estate in the United States, despite being 25x smaller in terms of landmass and having 200 million fewer people.

Tokyo itself was on equal footing with the U.S. in terms of real estate values.

The grounds on the Imperial Palace were estimated to be worth more than the entire real estate value of California or Canada at the market peak.

There were over 20 golf clubs that cost more than $1 million to join.

In 1989 the P/E ratio on the Nikkei was 60x trailing 12-month earnings.

Japan made up 15% of world stock market capitalization in 1980. By 1989 it represented 42% of the global equity markets.

From 1970-1989, Japanese large cap companies were up more than 22% per year. Small caps were up closer to 30% per year. For 20 years!

Stocks went from 29% of Japan’s GDP in 1980 to 151% by 1989.

Japan was trading at a CAPE ratio of nearly 100x which is more than double what the U.S. was trading at during the height of the dot-com bubble.

The aftershock could have been dealt with in many ways, but at its core, it came down to whether to pay a dear price over a short period or draw out the costs over decades. They elected the latter, saving their banks and relying on massive government spending to insulate the economy.

Over the last 25 years, the U.S. dot com and subprime bubbles have popped. While economically costly, the bubbles were minor compared to Japan’s. Accordingly, when they popped, the economic and financial consequences paled compared to Japan’s.

Banking Sector

The real estate and stock bubbles were supported with massive leverage via bank loans. When the asset values plummeted, the debt supporting them was often worthless. The banking system would have collapsed if the banks had written off the bad loans. The government aimed to keep the banking system out of harm’s way. Essentially, the banks didn’t have to recognize the losses. However, the non-performing loans were still on their books, significantly impeding their lending capabilities.

Further crippling the banks were the BOJ monetary policies which pinned interest rates at zero and below zero for long periods. The result was a flat yield curve. In addition to having a limited ability to lend, BOJ policies severely reduced the financial incentive to lend. Japan’s private sector economy could not contribute to growth nearly as much as possible if the banking sector were healthy and incentivized to lend.

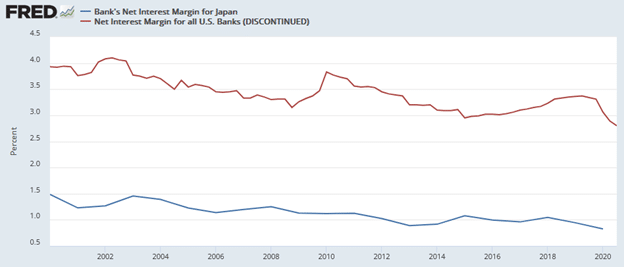

Conversely, U.S. banks are healthy and well-capitalized. Additionally, the Fed is very in tune with the amount of reserves in the banking system and stands ready to provide more when needed. Reserves are the fodder banks require to make loans.

The graph below compares the net interest margin for Japanese and American banks to show how much more financial incentive to lend versus their Japanese competitors.

Barring a significant financial crisis, there is no reason to expect U.S. banks to be as restricted as Japanese banks have been.

State-Led Capitalism

As noted in the prior section, Japanese banks have had a minimal ability to lend for much of the last 35 years. As a result of their zombie-like status, the government was heavily obligated to promote economic growth. Accordingly, the government played a much more significant role in managing the economy than is typical in a capitalistic economy.

A key tenant of capitalism states that when the free market sets prices based on the supply and demand for goods and services, it can most efficiently allocate resources to their most productive uses. Commonly, the most productive use of resources benefits economic growth and allows for higher wages and a broad distribution of wealth. Government interference reduces capitalism’s value as capital is often not put to its most productive uses.

Post-World War II Policies

Following World War II, Japan followed a path of capitalism, but it was state-led. Such was probably necessary in the decade or two after the war as the country was physically and emotionally devastated. Japan benefited immensely from the government’s push for rapid industrialization and economic development. But through loose monetary policy, financial deregulation, tax incentives, and infrastructure spending, its policies played a crucial role in inflating the real estate and stock bubbles.

After the bubble, the government was called upon to stimulate the economy. Their interference ultimately resulted in the unproductive allocation of resources, which, in the long term, likely reduced economic activity, thereby prolonging their weakness.

The United States form of capitalism is not as pure as it could be, but it is not nearly as dictated to the same degree as Japan. The Fed and government do reduce the value of capitalism and certainly foster speculation and leverage. But, they have yet to create policies that induce bubbles to the degree Japan saw in the 1980s.

The Yen Versus The World’s Reserve Currency

The U.S. dollar is the world’s reserve currency, and enormous rewards and complications come with it. In our article, Our Currency The World’s Problem we discuss the value of the reserve currency to the U.S.

Foreign nations accumulate and spend dollars through trade. They keep extra dollars on hand to manage their economies and limit financial shocks. These dollars, known as excess reserves, are invested primarily in U.S.-denominated investments ranging from bank deposits to U.S. Treasury securities and a wide range of other financial securities. As the global economy expanded and more trade occurred, additional dollars were required. As a result, foreign dollar reserves grew and were lent back to the U.S. economy.

Making the world even more dependent on the dollar, many foreign countries and companies issue U.S. dollar-denominated debt to better facilitate trade and take advantage of America’s liquid capital markets.

The bottom line is that the U.S. has a constant source of capital to fund our debts, support our asset markets, and buoy the economy. The Japanese Yen provides no such benefits to Japan.

Other Factors

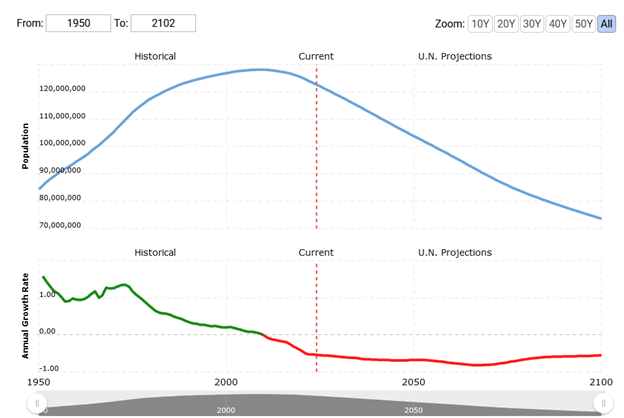

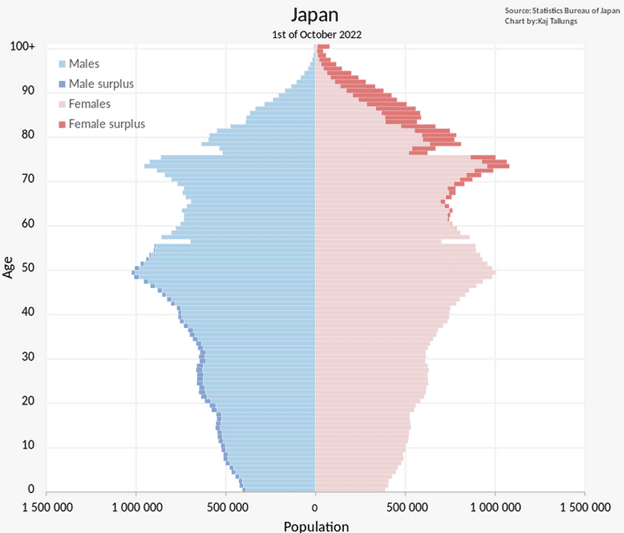

In Japan’s Lost Decades, we discuss Japan’s demographic challenges. To summarize, Japan has an aging population with low birth rates and a meager immigration rate. These factors and others have resulted in a declining population, which weighs on economic growth. While the United States also faces demographic headwinds that are and will negatively impact economic growth, they are not nearly as pronounced as those in Japan.

The United States has a much larger and more diverse economy. This is in part because we are rich in natural resources. The U.S. economy encompasses a wide range of industries, including technology, finance, manufacturing, agriculture, and services. In contrast, Japan’s economy focuses heavily on manufacturing and exports.

Various cultural differences also shape economic policies and affect consumer and corporate behaviors. The business culture in Japan is characterized by lifetime employment contracts and close relationships between corporations and banks (keiretsu). Japan’s population emphasizes consensus and harmony. In contrast, the United States has a more competitive culture centered more on the individual than the nation.

Summary

Fiscal dominance, whereby the Federal Reserve must help the Treasury fund their debts at reasonable costs, is upon us. Japan has relied on fiscal dominance for 35 years. This is one of a few clues that the U.S. is on Japan’s path.

However, as we have written, our nations have significant differences. While we may be on a similar path as Japan, our paths will differ. Since we have not traveled as far on the path as Japan, we have time to learn their lessons and fix them. Will this happen?

Tesla Cuts 15k Jobs As EVs Fall Out Of Favor

In our article Is Toyota The Next Tesla, we discuss recent trends in the automobile industry. In particular, EV sales growth has been declining as hybrid vehicles become more popular, and concerns specific to EVs are growing. With more competitors in the EV market and new hybrid models hitting the market, Tesla’s market share of total auto sales is at risk. In fact, its sales declined in the first quarter. To counteract the trend toward lower growth, Tesla has made some sacrifices. For starters, Tesla cut prices. Per Cox Automotive, “Tesla’s average transaction price was $52,315 in Q1, down roughly 13.5% year over year. However, lower prices did not generate higher volume.“

Since lower prices amid growing competition and waning demand aren’t spurring sales, Tesla announced it would cut 15,000 jobs or about 10% of its staff on Monday. As we wrote in our aforementioned article, EVs will gain market share but not likely at the pace they have, barring new technology. The Tesla job cuts and weakening sales greatly impact the producers of the metals used to make EVs. Consider the quote below from the Wall Street Journal.

Producers of lithium and nickel, which are used in lithium-ion batteries for EVs, have been stalling projects and closing mines to save cash after a painfully quick fall in commodity prices. Prices of lithium are down as much as 90% since the start of last year, while the price of nickel has roughly halved- The Boom In Battery Metals For EVs Is Turning To Bust

What To Watch Today

Earnings

Economy

Market Trading Update

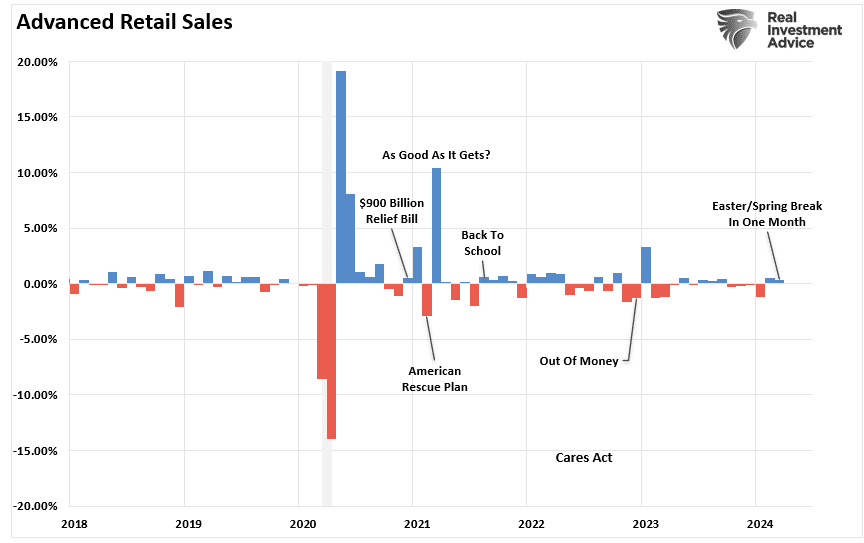

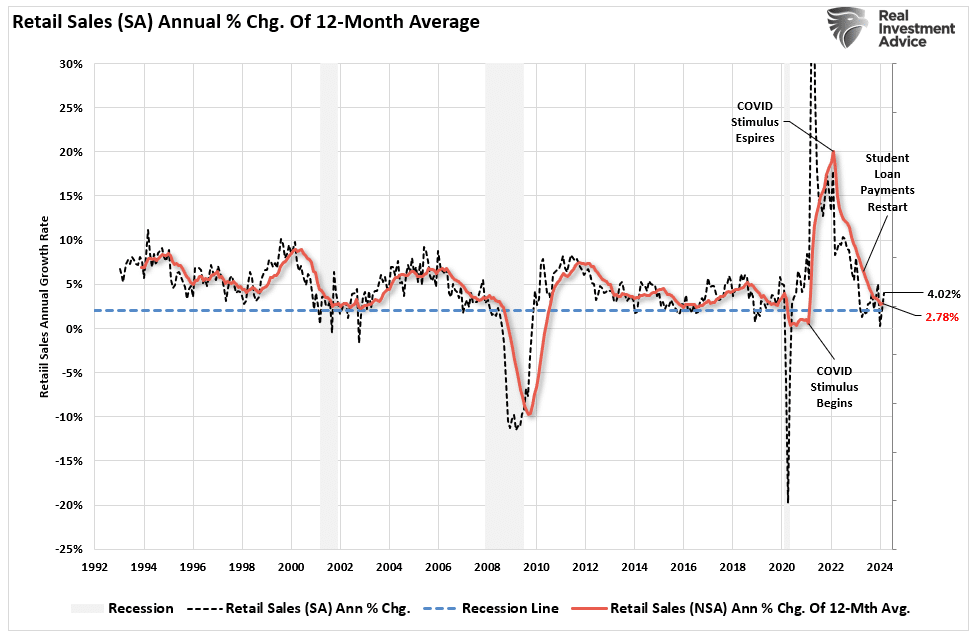

As discussed yesterday, the market is sitting on support at the 50-DMA and is oversold. Yesterday morning, the market opened up decently strong on cooling tensions between Iran and Israel, and stronger than expected retail sales data suggesting the consumer remains strong. However, it didn’t take long for the market to see through the sales data and realize that while sales were strong, it included Spring Break and Easter. Of course, both events require travel, hotels, food, and clothing. It is quite likely April will be substantially weaker as a payback for the pull-forward of spending in March. As shown, retail sales remain weak, and this is on a nominal basis, which is crucial as it means consumers are paying more for the same amount of goods.

Furthermore, the 12-month average of the non-seasonally adjusted spending data should be examined, removing all the seasonal adjustments and manipulations. We find that retail sales growth is substantially weaker than reported. Given that the reported numbers follow the unadjusted average, we will likely see weaker sales numbers heading into summer.

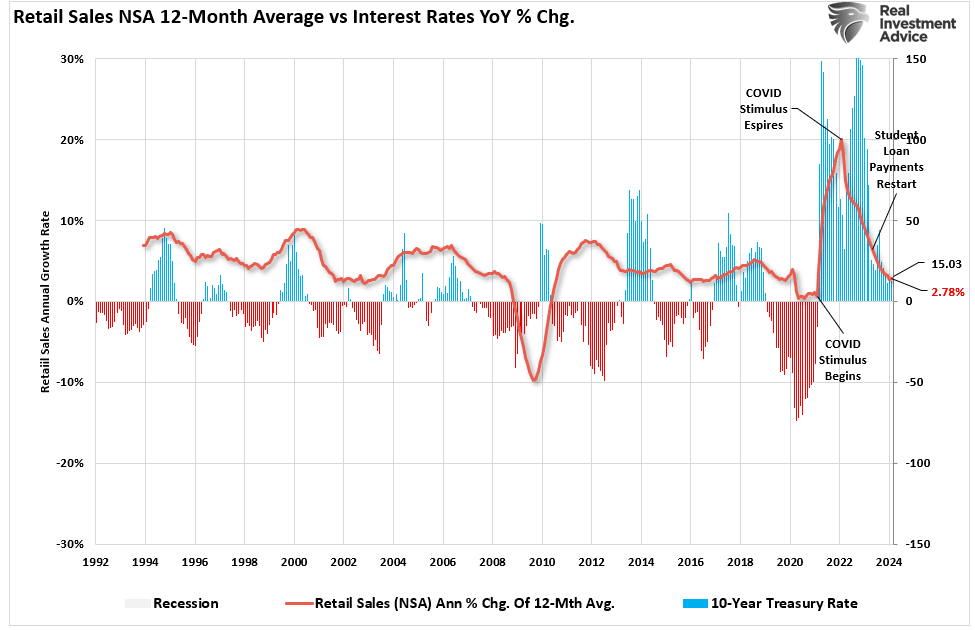

Notably, if retail sales slow down as they appear, interest rates will continue to follow. The chart below compares the 12-month average of retail sales to the annual change in interest rates. Over the months ahead, as retail sales and the overall economy continue to slow, interest rates will follow.

While interest rates are rising due to speculative market actions, the sustainability of higher rates is problematic for consumers and a heavily indebted economy.

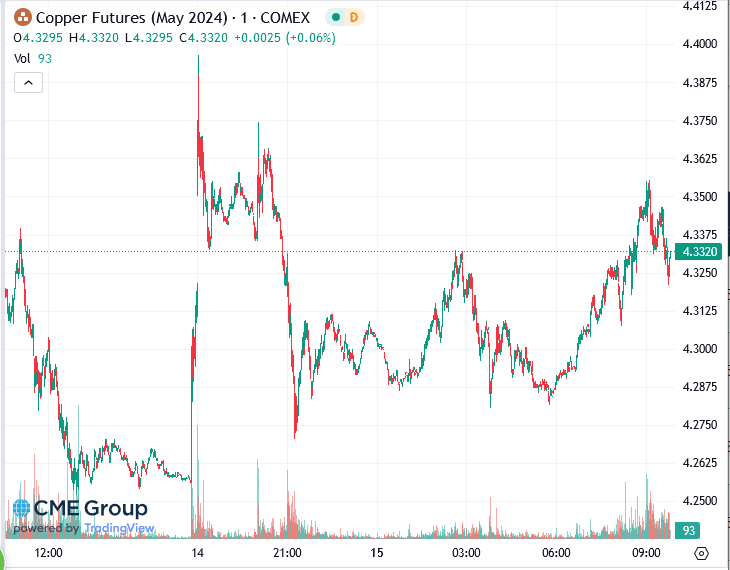

Industrial Metals Rally On Russian Sanctions

In further efforts to reduce Russia’s sources of military funding, the U.S. and British governments are banning Russian exports of nickel, aluminum, and copper. Further, the Chicago Mercantile Exchange (CME) and London Metal Exchange (LME) will make deliveries of the three metals produced by Russia ineligible for futures contracts. For context, Russia accounts for about 5% of the production of all three metals. On the margin, the ban may further add to price pressures. But keep in mind the markets for these metals are global. Therefore, China will buy more metals from Russia, while the U.S. and Britain buy more from other producers. Accordingly, the sanctions should have little effect on prices in the long run.

The prices of the metals spiked on the news but have since given back some of the gains. The graph below shows that Copper prices were up by about 4% when the news was released. However, it has retreated since then. Aluminum is up 2.5% but also down decently from Sunday night’s highs.

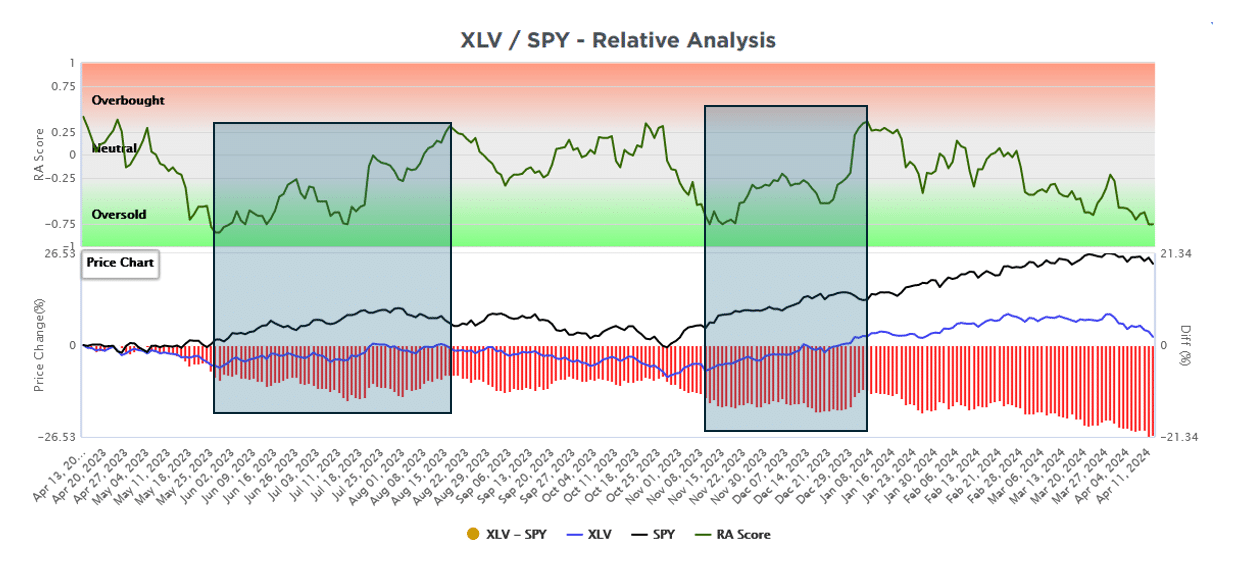

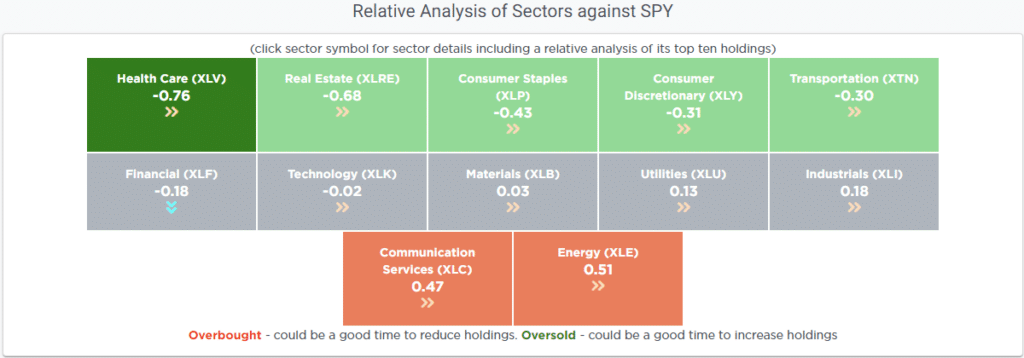

Healthcare Stocks Are Very Oversold, But…

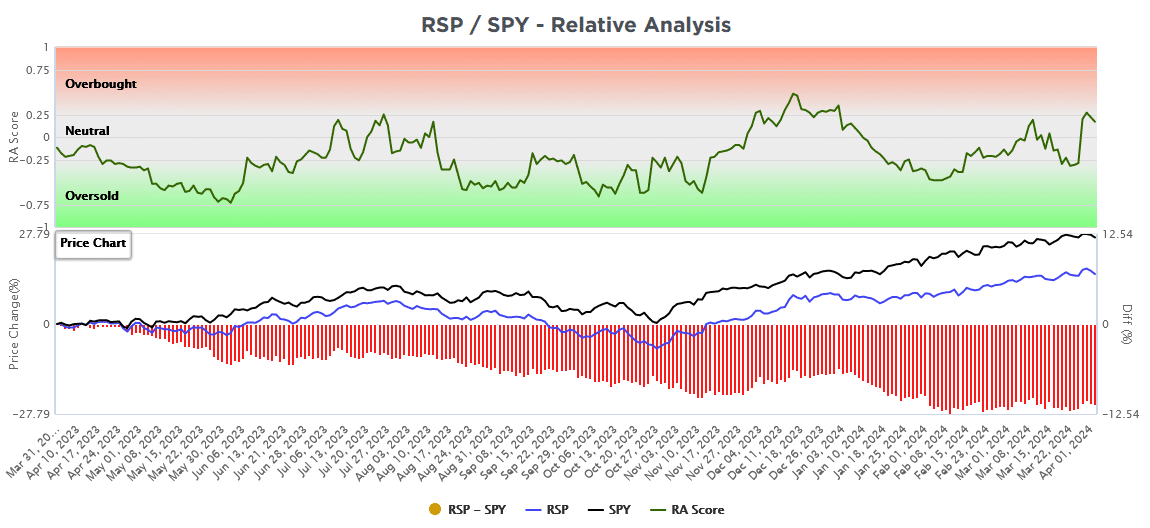

The SimpleVisor graph below shows our proprietary SimpleVisor relative technical score (green line) for the healthcare sector (XLV). The black and blue lines in the lower chart show the prices of XLV and SPY. The red bars show XLV’s relative performance. The top chart highlights the two prior instances when XLV was as oversold as it is today versus the S&P 500.

Given the significant oversold level, is it worth adding to healthcare on a relative basis?

The answer is maybe. The boxes show that the prior deeply oversold periods only produced marginal relative outperformance. These periods of consolidation of the XLV/SPY ratio allowed the technical gauges to become more balanced. If this instance marks an actual trend change and not a consolidation in a lower trend, we may be nearing a period to buy XLV versus SPY. Breaking into overbought territory might signal such a trend change.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

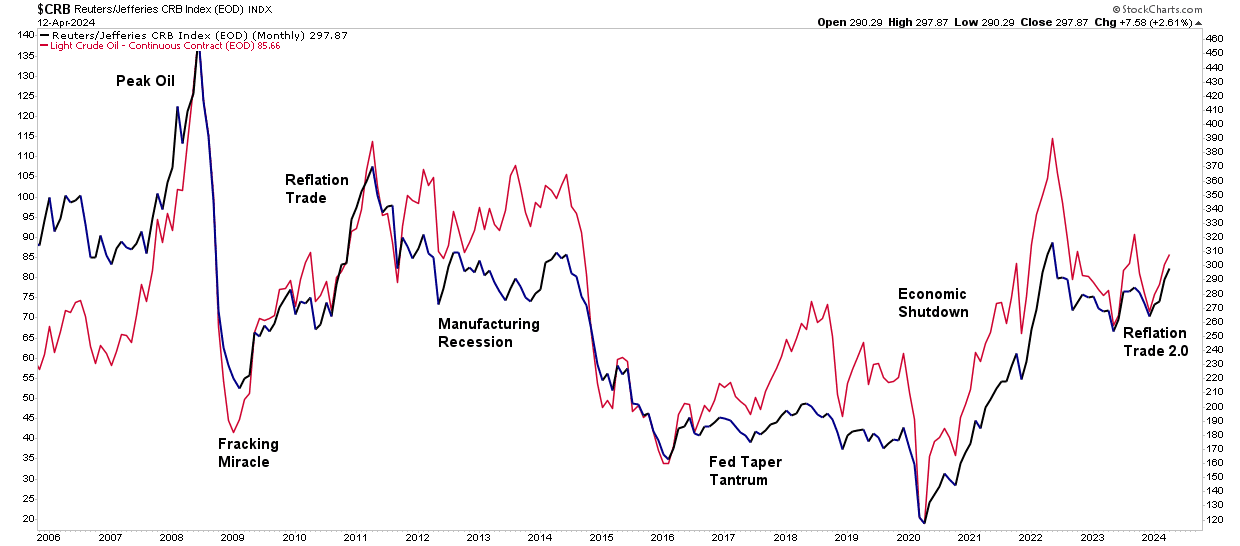

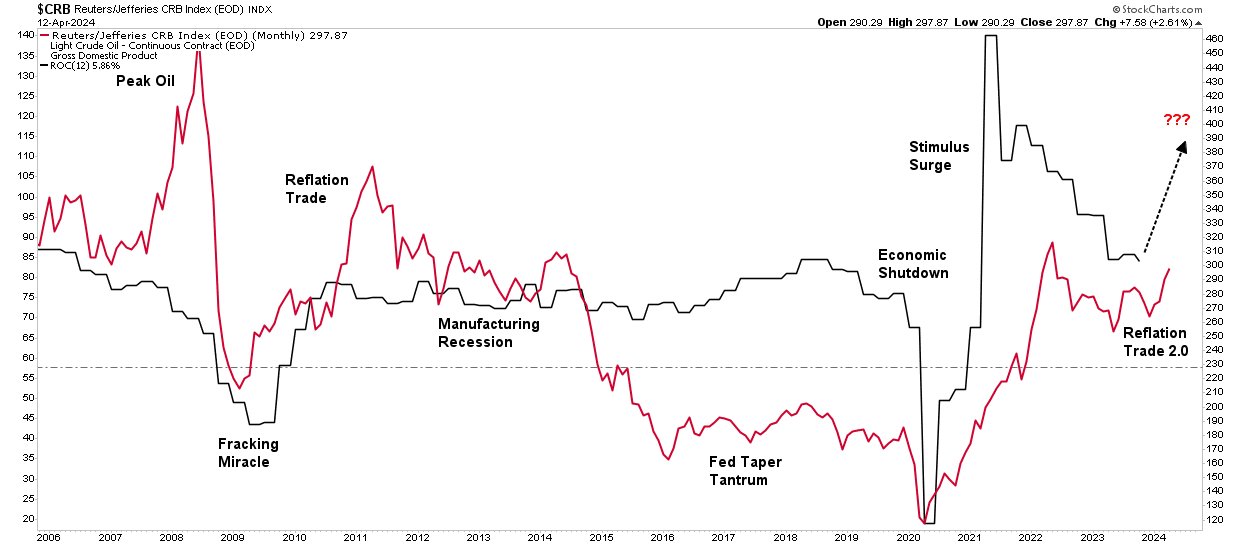

Reflation Trade Is The New Bullish Narrative

Economic “reflation” is becoming the next bullish narrative as equity valuation increases continue to outpace earnings gains, at least according to Gold Sachs and Tony Pasquariello.

“If GS is correct on the big calls, the macro backdrop is set to remain friendly: the US economy should continue to grow nicely above trend — picking up speed as the year moves along — with three adjustment rates cuts along the way. to not obscure the moral of that story: the Fed is set to ease policy … into an upswing. while Fedspeak this week had a somewhat hawkish bent, the house view for 2024 remains intact.”

Interest rates, gold, and commodity prices have increased in the past few months. Unsurprisingly, the bullish narrative to support that rise has gained traction. Interestingly, this “reflation” narrative tends to resurface by Wall Street whenever there is a need to explain the surge in commodity prices. Notably, the last time Wall Street focused on the reflation trade was in 2009, as noted by the WSJ:

“The most talked-about investing strategy these days isn’t stuffing money in a mattress, it’s the reflation trade — the bet that the world economy will rebound, driving up interest rates and commodities prices.”

While that “reflation trade” lasted for about two years, it quickly failed as economic growth returned to 2%-ish growth along with inflation and interest rates. As shown, oil and commodity prices have a very high correlation. The critical reason is that higher oil prices reduce economic demand. As consumption falls, so does the demand for commodities in general. Therefore, if commodity prices are to “reflate,” as shown, such will depend on more robust economic activity.

As such. The reflation trade hinges on a global resurgence of economic activity, usually associated with economies recovering from a recessionary period. However, the U.S. never experienced a recession. As discussed in “Deficit Spending,” despite numerous recessionary signals, like the inverted yield curve, manufacturing data, and leading economic indicators, the economy avoided recession due to massive governmental spending. To wit:

“One explanation for this has been the surge in Federal expenditures since the end of 2022 stemming from the Inflation Reduction and CHIPs Acts. The second reason is that GDP was so grossly elevated from the $5 Trillion in previous fiscal policies that the lag effect is taking longer than historical norms to resolve.”

While economists focus on the “reflation trade,” we must answer whether the support for more substantial economic growth exists. This is the sole determining factor in whether the “reflation trade” can continue.

Is Reflation Already Behind Us?

Interest rates and inflation have ticked up recently, driving investors into gold and commodities. However, the surge in precious metals and commodities is more of a function of speculative exuberance rather than an economic resurgence. As discussed in “Speculative Warnings,”

“In other words, the stock market frenzy to “buy anything that is going up” has spread from just a handful of stocks related to artificial intelligence to gold and digital currencies.“

Notably, the gold, commodities, and interest rate surge corresponded with more robust economic growth beginning in the third quarter of last year. That uptick in economic growth defied economists’ expectations of a recession. Such was because of the massive flood of monetary support from Government spending programs. However, that monetary impulse is now reversing.

As far as the “reflation trade” is concerned, as that monetary impulse recedes, so will economic growth, as shown. Even if the economy continues to grow at 2-2.5% annualized each quarter, the annual rate of change in growth will continue to slow.

Importantly, this assumes that the Government will keep “spending like drunken sailors” over that same period. However, if they don’t, the economic growth rate will slow even more quickly without increasing monetary spending.

It is important to remember that increasing debts and deficits do not elicit stronger long-term economic growth. As debt levels rise, economic growth rates will slow as money diverts from productive investment into debt service.

That reality should be unsurprising, as this is not the first time the Government has gone “all in” on a reflation trade. As noted above, following the Financial Crisis, the Government intervened with HAMP, HARP, TARP, and a host of other spending programs to “reflate” the economy.

Let’s review what happened with interest rates, inflation, and gold and commodity trade.

Past May Be Prologue

As noted in 2009, following the “Financial Crisis” and recession, the Government and the Federal Reserve engaged in various monetary and fiscal supports to repair the economy. While the economy initially recovered from the recessionary lows, inflation, economic growth, and interest rates remained subdued despite ongoing interventions.

That is because debt and artificially low interest rates lead to malinvestment, which acts as a wealth transfer mechanism from the middle class to the wealthy. However, that activity erodes economic activity, leading to suppressed inflation and a surging wealth gap.

During that same period, commodities and precious metals rose initially as the “reflation expectation” was widespread. However, debt-driven realities quickly undermined that assessment and those investments languished relative to equities, as the flood of liquidity and low rates made equities far more attractive to investment.

While the relative performance of precious metals and commodities has picked up in recent months, this is more likely a function of “irrational exuberance” in the financial markets. As discussed previously, the surge in speculative investment activity is not uncommon to markets, and currently, many asset classes are becoming highly correlated.

However, while there is a compelling narrative around gold and precious metals from an investment perspective, those chasing that trade have had many years of terrible underperformance. While this time could be different, the “reflation narrative” will most likely fall prey to the realities of excessive debt, which will pressure Governments to cut rates once again.

If the past is potentially prologue, likely, the bullish narrative of “reflation” may once again find future disappointment. Such is particularly the case as the economics of debt and poor policy choices continue to erode the middle class further.

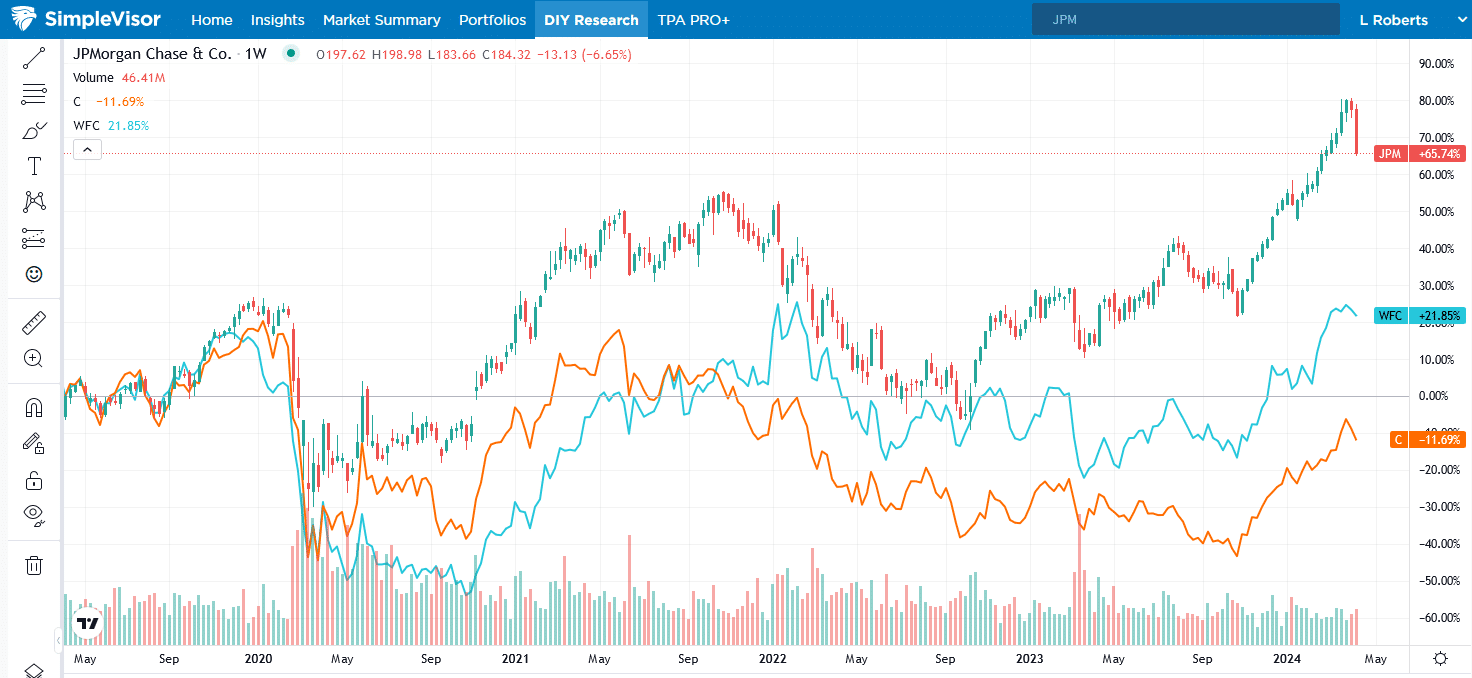

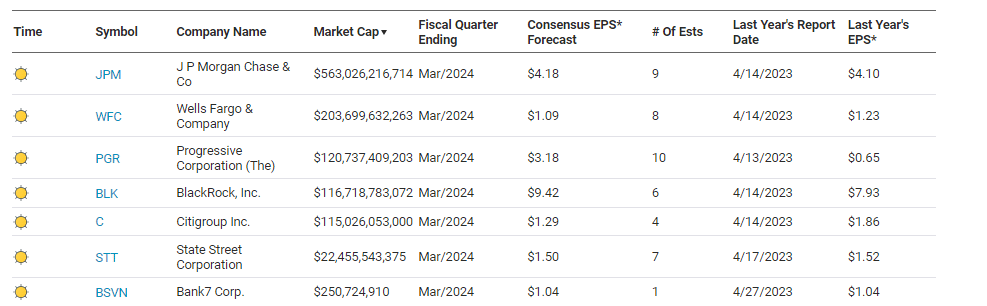

Bank Earnings Paint A Mixed Economic Picture

From a macroeconomic perspective, Friday’s bank earnings reports provide two important pieces of information. As we detail below, their profit margins are shrinking, and their economic outlook remains favorable.