Despite The Fed, The Bond Market Is Hiking Rates 02-26-21

In this issue of “Despite The Fed, The Bond Market Is Hiking Rates.”

- Market Review And Update

- Bond Market Is Hiking Rates

- Why Higher Rates Are A Real Problem

- Portfolio Positioning

- #MacroView: Why Stimulus Doesn’t Lead To Organic Growth

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

RIA Advisors Can Now Manage Your 401k Plan

Too many choices? Unsure of what funds to select? Need a strategy to protect your retirement plan from a market downturn?

RIA Advisors can now manage your 401k plan for you. It’s quick, simple, and transparent. In just a few minutes, we can get you in the “right lane” for retirement.

Catch Up On What You Missed Last Week

Market Review & Update

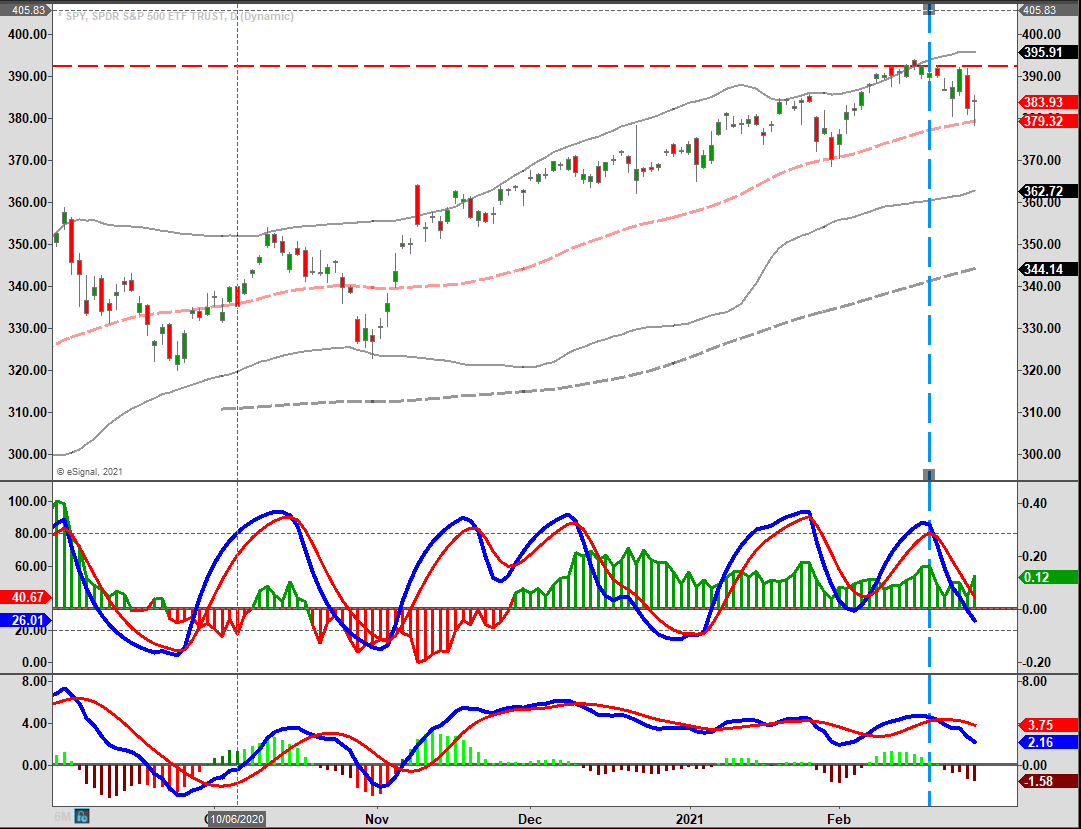

Last week, we discussed that the market was likely starting to adjust for higher rates. As we stated, historically, there is little room for error as higher rates undermine one of the critical “bullish supports” that low rates justify high valuations.

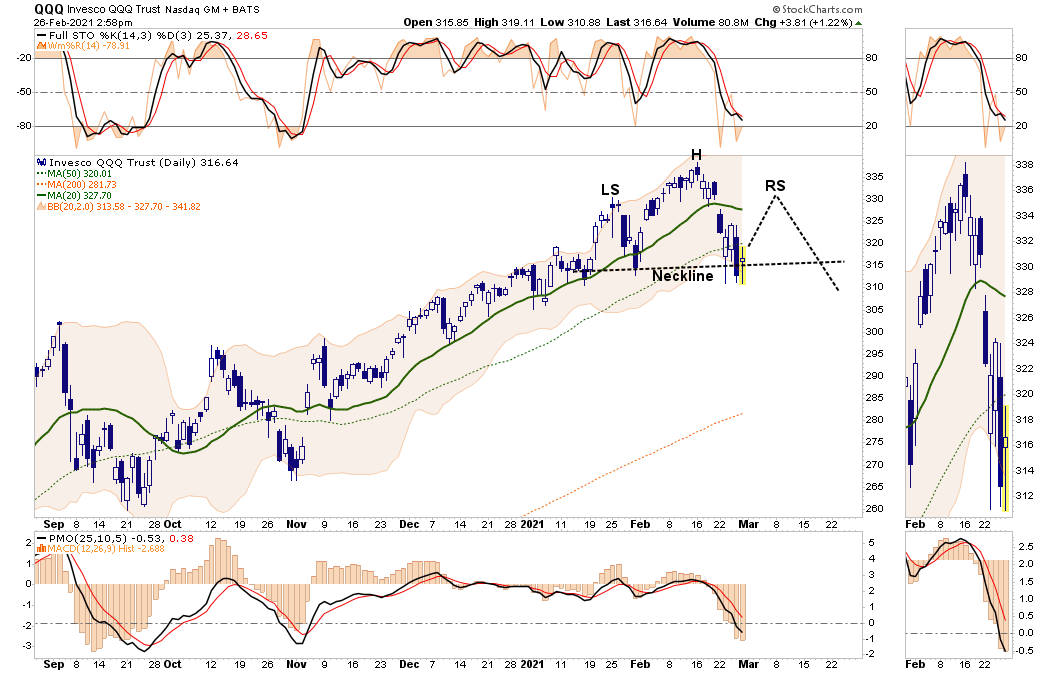

This past week, rates jumped higher, putting a further pause in the stock rally for now. As we stated over the last few weeks, the upside remains limited with the money-flow sell signal still intact. (The vertical dashed blue line denotes when the signals initially triggered.)

Thursday morning before the market opened, I discussed the two areas we watch very closely: the 10-year treasury rate and the volatility index. Both were on extremely oversold signals, and if they turned higher, such would suggest a continued correction in the market. That turned out to indeed be the case.

https://www.youtube.com/watch?v=ZAhmyJgyFkU

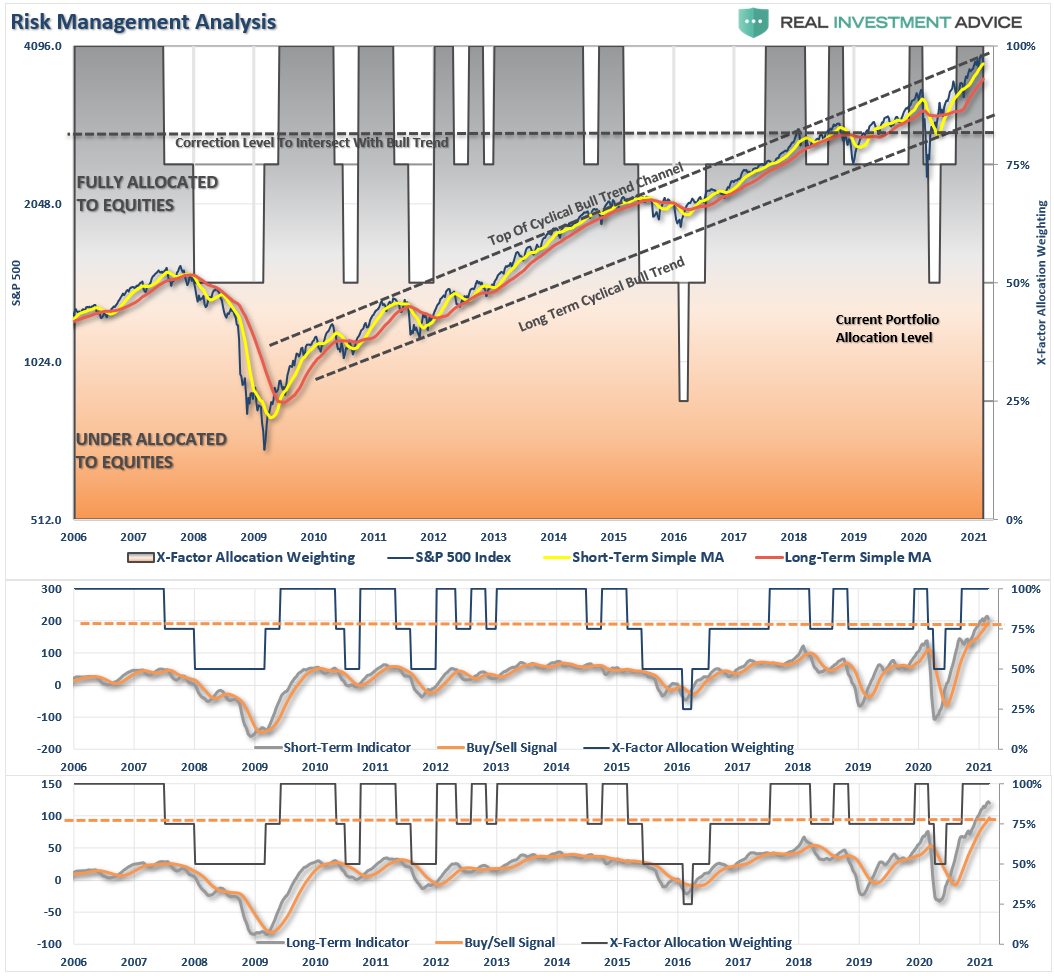

Currently, as shown above, the money flows remain positive, but “sell signals” are firmly intact. Such suggests downward pressure on prices currently.

We do expect that market will likely muster a short-term oversold rally next week. However, the risk of a continued correction in March is likely if money flows deteriorate further. It is advisable to use any rallies to reduce equity risk and rebalance allocations accordingly.

We continue to suggest some caution. Despite media claims to the contrary, higher interest rates will matter, as we will discuss next. More importantly, they tend to matter a lot.

The Fed Is Walking Into A Trap

We sent the following market commentary out to our RIAPRO subscribers yesterday morning:

- Jim Bullard: “The rise in bond yields is a good sign so far.”

- Esther George “LONG-TERM YIELD RISE DOESN’T WARRANT MONETARY RESPONSE”

- R. Bostic: FED DOESN’T NEED TO RESPOND TO YIELDS AT THIS POINT

Jerome Powell, Jim Bullard, Esther George, Raphael Bostic, and other Fed members are steadfast in their determination to use an excessive amount of monetary stimulus to promote inflation and growth. The reflationary trade and the weak dollar over the last few months are confirmation that investors believe the Fed is making headway toward its goals.

The problem is that bond investors also believe they are making progress. On Tuesday and Wednesday, Jerome Powell said that he is not concerned about inflation and will keep the monetary pedal to the metal in no uncertain terms. The quotes above are all excellent reasons for bond investors to keep selling.

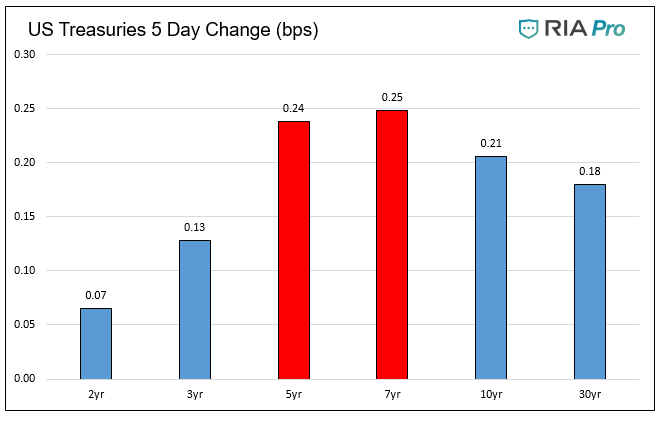

Selling in the bond market became problematic this week as yields in the economically sensitive 5-and 7-year sectors rose precipitously. Previously, it was 10- and 30-year bonds taking the brunt of selling activity. The shorter, intermediate sectors largely determine mortgage, corporate, and auto borrowing rates.

They steer economic activity.

While the Fed is running accommodative monetary policy, the market is increasingly imposing tighter financial conditions.

The Fed has a choice. They can watch yields rise to the detriment of economic growth, or they can walk back monetary policy. Doing so requires tapering QE and raising rates. Either action will pose problems for overvalued equity markets based on a tailwind of easy monetary policy.

To put it bluntly, the Fed is walking into a trap where at some point, they will get forced into deciding between rescuing the bond market or the stock market.

Why Higher Rates Are A Problem

It is essential to understand the impact of rates on a heavily leveraged economy.

1) Economic growth is still dependent on massive levels of monetary interventions. An increase in rates curtails growth as rising borrowing costs slows consumption.

2) The Federal Reserve runs the world’s largest hedge fund with over $7.5-Trillion in assets. Long Term Capital Mgmt., which managed only $100 billion, nearly derailed the economy when rising rates caused its collapse. The Fed is 75x that size.

3) Rising interest rates will immediately slow the housing market. People buy payments, not houses, and rising rates mean higher payments.

4) An increase in interest rates means higher borrowing costs which lowers profit margins for corporations.

5) One of the main bullish arguments over the last 11-years remains stocks are cheap based on low interest rates. That will change very quickly.

6) The negative impact on the massive derivatives market could lead to another credit crisis as rate-spread derivatives go bust.

7) As rates increase, so do the variable rate interest payments on credit cards. With the consumer already impacted by stagnant wages, under-employment, and high costs of living; a rise in debt payments would further curtail disposable incomes. Such would lead to a contraction in spending and rising defaults. (Which are already happening as we speak)

8) Rising defaults on the debt will negatively impact banks that are still not adequately capitalized and still burdened by massive levels of bad debt.

9) Commodities, which are sensitive to the direction and strength of the global economy, will revert as economic growth slows.

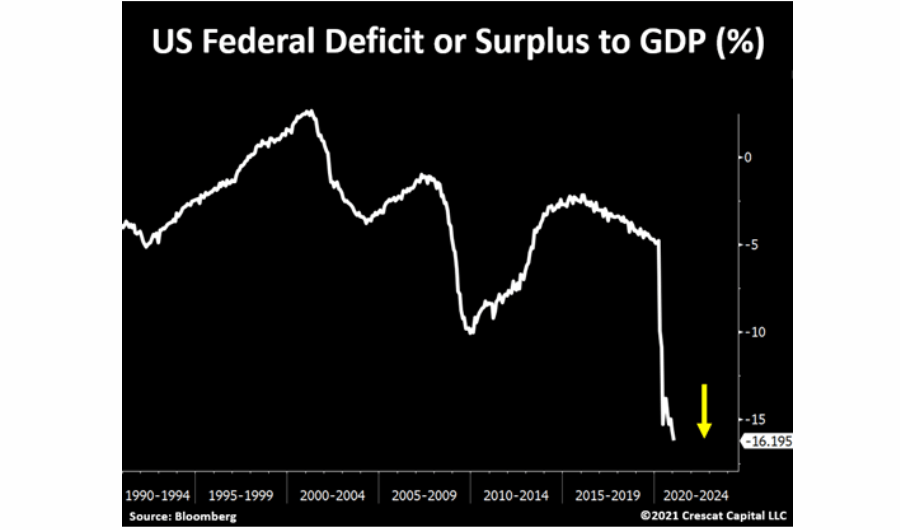

10) The deficit/GDP ratio will surge as borrowing costs rise sharply. The many forecasts for lower future deficits will crumble as new estimates begin to propel higher.

I could go on, but you get the idea.

Putting It In Pictures

The ramifications of rising interest rates apply to every aspect of the economy.

As rates rise, so do rates on credit card payments, auto loans, business loans, capital expenditures, leases, etc., while corporate profitability gets reduced.

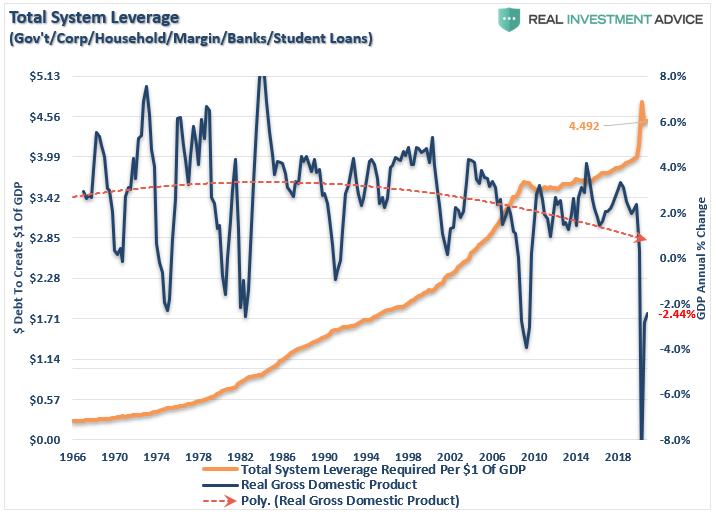

Currently, the economy requires almost $4.50 in debt to manufacture $1.00 of economic growth. Given the dependence on debt to fund growth, higher interest rates would be inherently destructive.

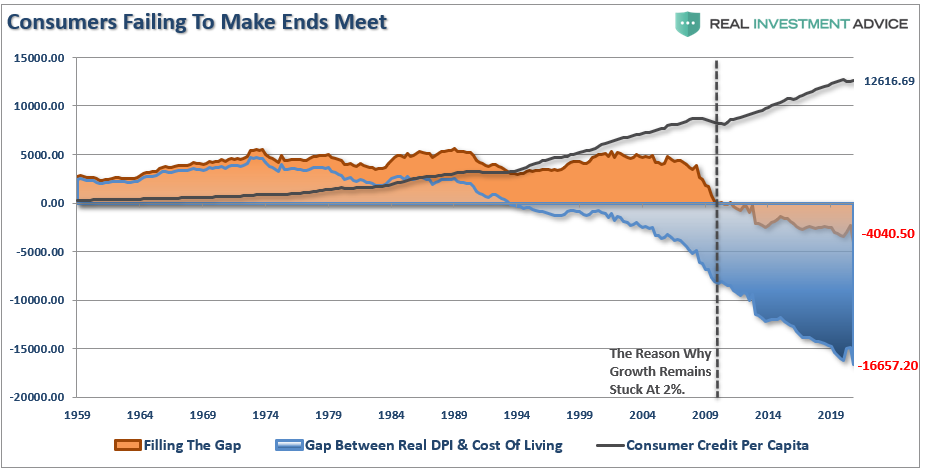

More importantly, consumers have sunk themselves deeper into debt as well. Currently, the gap between wages and the costs of supporting the required “standard of living” is at a record. With a requirement of over $16,000 in debt to maintain living standards, there is little ability to absorb higher rates before it drastically curbs consumption.

The annual deficit of over $4000 to make up the gap between the cost of living and current incomes increases debt loads on consumers. Higher interest rates will further absorb discretionary incomes into debt service.

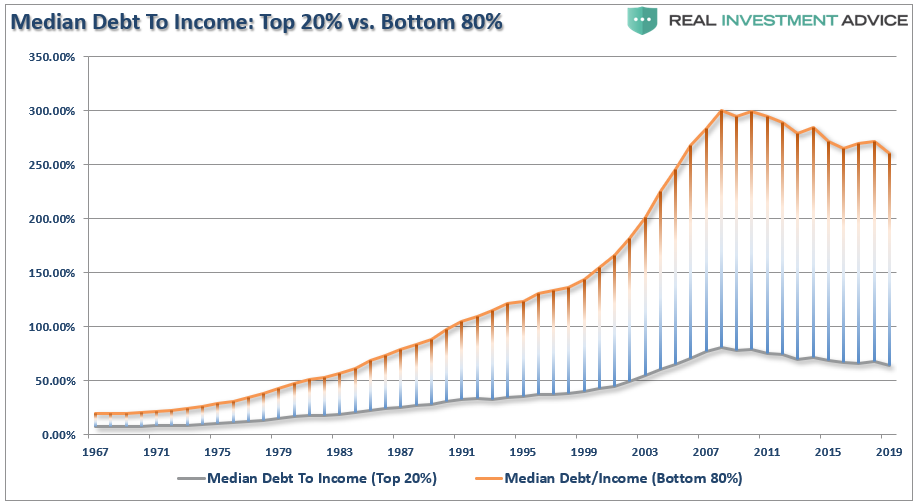

“But what about those charts that show the average American has deleveraged themselves? “

The vast majority of the deleveraging only occurred in the top 20% of income earners, which you would expect. It is hard to suggest that a family barely making ends meet before the pandemic crisis suddenly found excess cash flow to pay off debt.

Interest rates matter. When rates hit a point where consumers and businesses can’t justify further indebtedness, a credit-driven economy slows down.

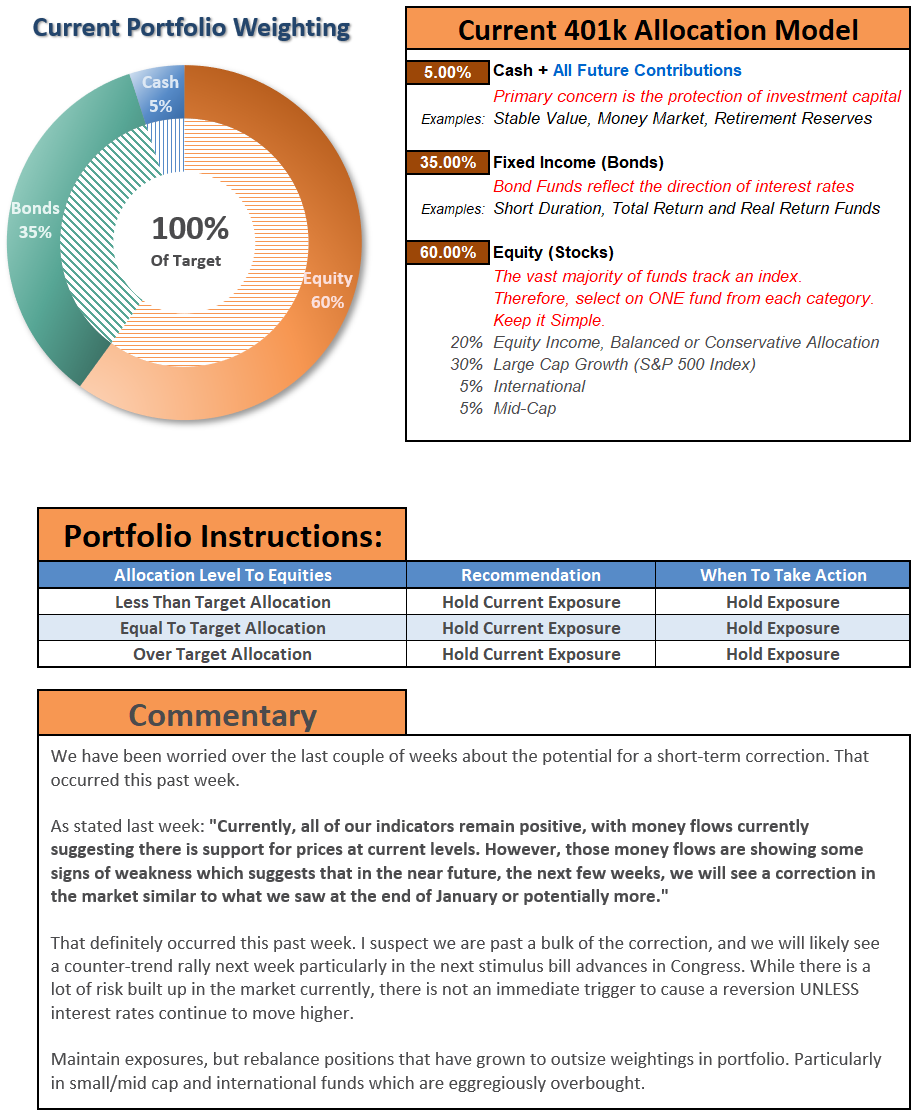

Portfolio Update

As noted last week, we raised cash levels in portfolios over the last couple of weeks. Notably, we had sharply reduced our bond portfolios’ duration by shifting treasuries to short-term bonds and selling mortgage-backed securities. That shift helped hedge portfolios a lot of the last few days.

We remain fairly allocated to equities at the moment, but we will likely start using counter-trend rallies to reduce risk further if the markets don’t begin firming up next week. After this week’s selloff, the market is getting fairly oversold, so a counter-trend bounce would not surprise us.

As we discussed with our RIAPRO Subscribers, some defined “bearish” patterns continue to form on the S&P 500, Nasdaq (shown below), Emerging, and International markets.

There is much commentary about the rotation to “reflation” sectors like industrials, materials, energy, etc., which will benefit from a reopening economic surge. While we already own these sectors, it is essential to remember very little “value” in the market.

We will likely see a boost in economic growth this year. However, that growth has already gotten well priced into the market at every level. Valuations are extreme across every market. Such places the market at risk of disappointment if expectations fall short.

If history is any guide, it is highly likely we will be disappointed as we move further into the year.

What To Do Now

While this past week was rough, particularly for more aggressively allocated models, it is crucial not to let short-term psychological pressures derail your investment discipline.

As we have discussed previously, “risk happens fast.” As such, it is essential not to react emotionally to a sell-off.

Instead, fall back on your investment discipline and strategy.

- Is the premise of why you bought a position previously still intact?

- Has anything fundamentally changed for the company?

- Review the positioning of your portfolio relative to the benchmark? Are you out of tolerance in your allocations?

- Review your positions. Are they out of tolerance relative to your sizing rules?

Last but not least, keep your portfolio management process as simplistic as possible.

- Trim Winning Positions back to their original portfolio weightings. (ie. Take profits)

- Sell Those Positions That Aren’t Working. If they don’t rally with the market during a bounce, they will decline more when the market sells off again.

- Move Trailing Stop Losses Up to new levels.

- Review Your Portfolio Allocation Relative To Your Risk Tolerance. If you have an aggressive allocation to equities at this point of the market cycle, you may want to try and recall how you felt during 2008. Raise cash levels and increase fixed income accordingly to reduce relative market exposure.

Nobody ever went broke taking profits.

While keeping your capital intact is hard, making up lost capital is even harder.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

Discover All You Are Missing At RIAPRO.NET

This is what our RIAPRO.NET subscribers are reading right now! Risk-Free For 30-Day Trial.

- Sector & Market Analysis

- Technical Gauge

- Fear/Greed Positioning Gauge

- Sector Rotation Analysis (Risk/Reward Ranges)

- Stock Screens (Growth, Value, Technical)

- Client Portfolio Updates

- Live 401k Plan Manager

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert, do not hesitate to contact me.

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

If you have any questions or comments, feel free to contact me.