Fed Tightening “Sooner & Faster” Sends Stocks Rallying?

In this 01-28-22 issue of “Fed Tightening ‘Sooner & Faster’ Sends Stocks Rallying?”

- Fed To Tighten Sooner & Faster

- Bearish Sentiment Getting Really Bearish

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Is It Time To Get Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Market Review & Update

It was a busy week with a lot of market volatility. So let’s start with a recap from last week.

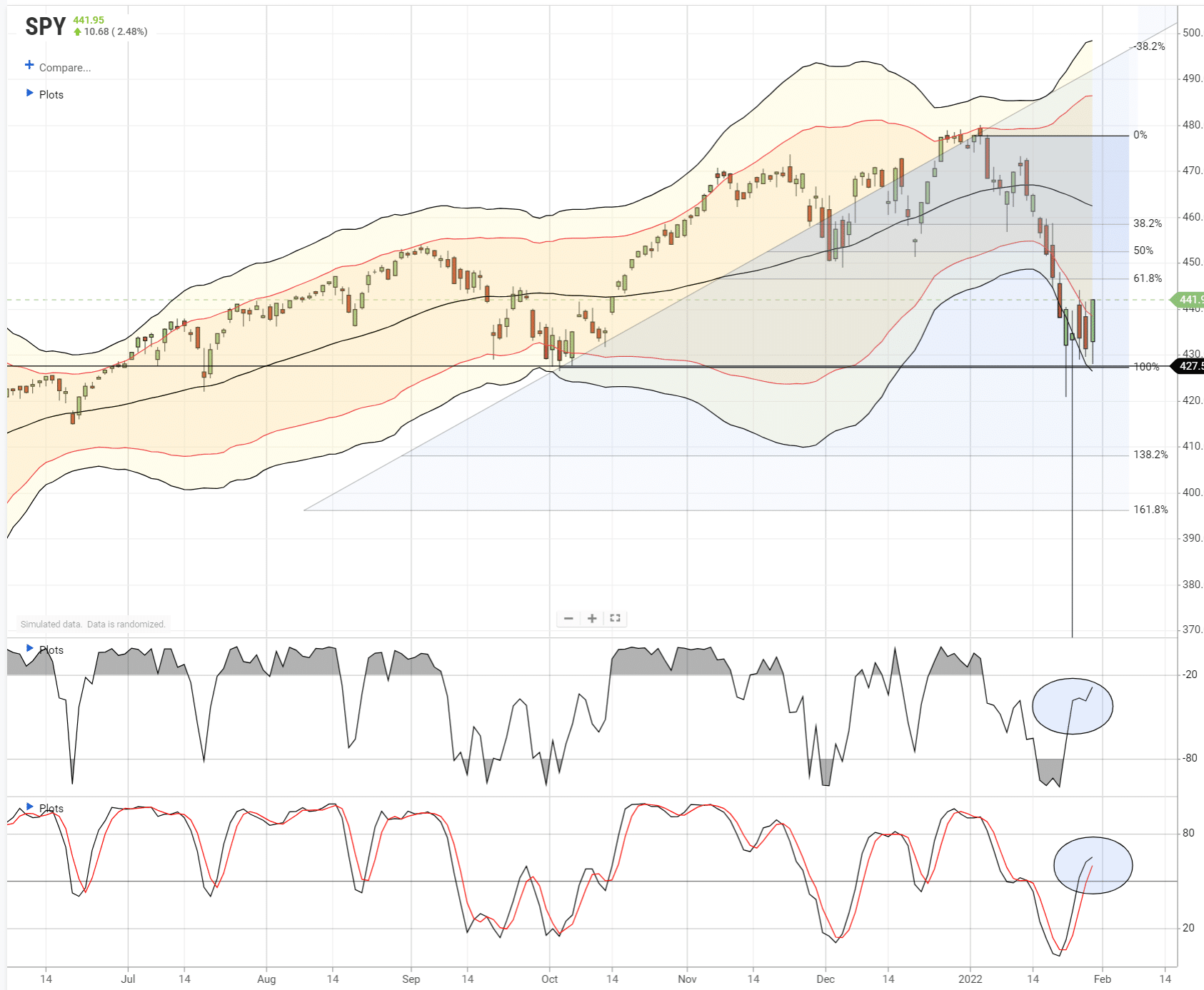

“This past week, retail investors began to panic sell as “meme” stocks fell apart. Previous favorites became an anathema from AMC to Gamestop to Pelton and Netflix. The selling pressure took the S&P 500 below its trendline support, deep into oversold territory, and well into 3-standard deviations below the mean.”

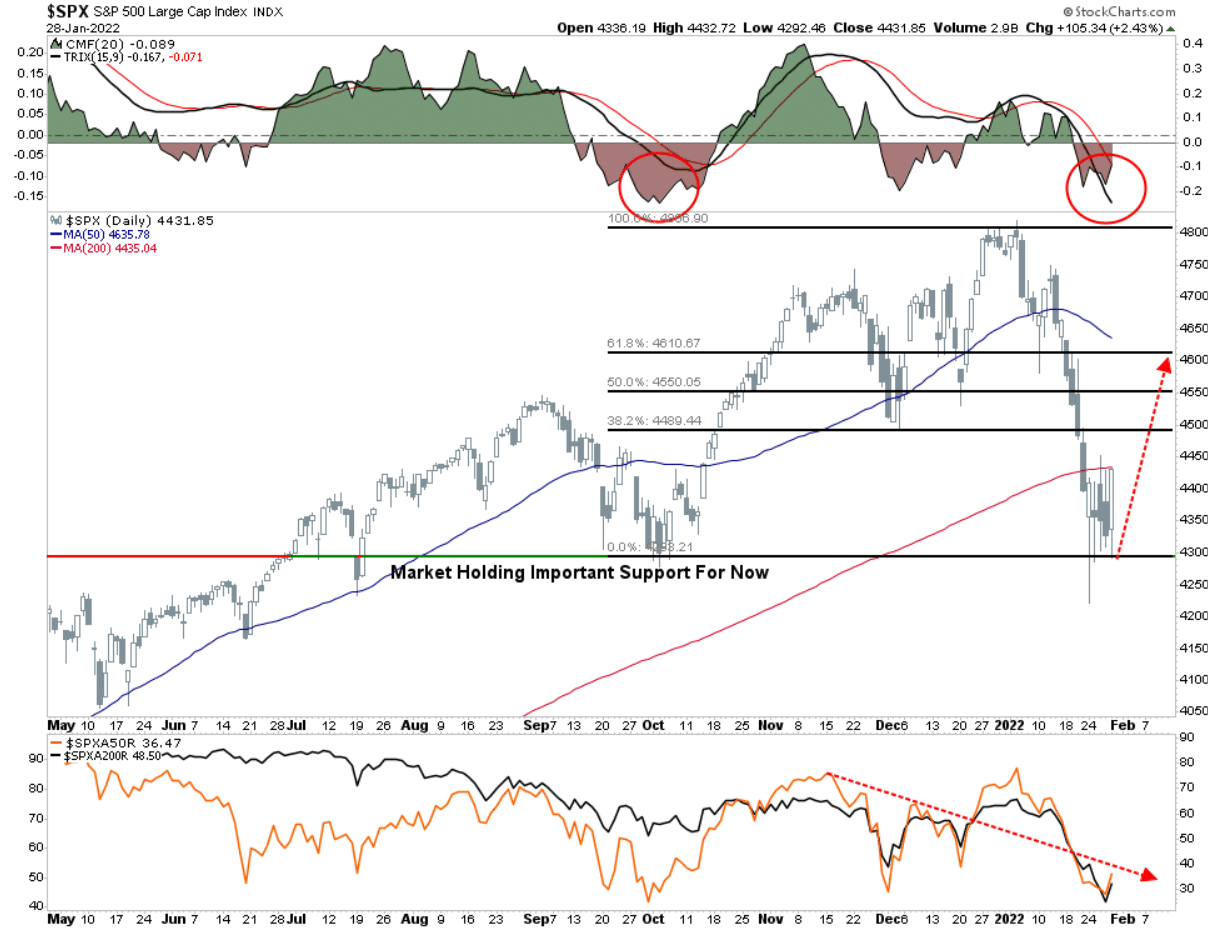

Despite the Fed tightening rhetoric, the market ended the week positively, erasing the week’s losses. The markets do look to be stabilizing, as shown below, and are holding the October lows. That 100% Fibonacci retracement, and multiple rally attempts, triggered a short-term buy signal. All of this is short-term bullish.

While a reflexive rally is very likely, we are starting to use that rally to leg into a short-market hedge and reduce overall equity risk. (We will discuss the reflex rally more in a moment.) We are also looking to tilt our portfolio a bit more to the value sector. However, we are also maintaining some of our major “growth” stocks which are now profoundly oversold and will benefit from a rise of disinflationary pressures later this year.

For a discussion on our disinflationary/market views watch the Fox Business with Charles Payne interview.

The relatively sharp drop in the market to start 2022 has undoubtedly shaken up many previously over-bullish investors. However, while we are not forecasting a 50% market crash, as the Fed tightens policy, we expect more of these outsized swings this year as the market comes to grips with a Fed removing monetary accommodation.

Fed To Tighten “Sooner & Faster”

Such was what we saw on Wednesday as the Fed spooked investors with just a tiny change in their language.

This week’s pickup in volatility accelerated on Wednesday, with markets up more than 2% going into the FOMC announcement. However, such was short-lived as Jerome Powell said the Fed would remove assets from their balance sheet “sooner and faster” markets plunged.

The S&P was up 95 points as Powell kicked off his press conference. However, by the time he spoke his final words, it was down nearly 40 points. While markets had “priced in” the Fed’s previous commitment to tighten monetary accommodation, it certainly seems the term “sooner and faster” was not.

Notably, he ended the conference by stating that “asset prices do not represent a threat to financial stability.” Given that “financial stability” is a crucial concern of the Fed, Powell essentially lowered the “Fed put,” or where the Fed will restart QE, to a market level much lower than previously thought.

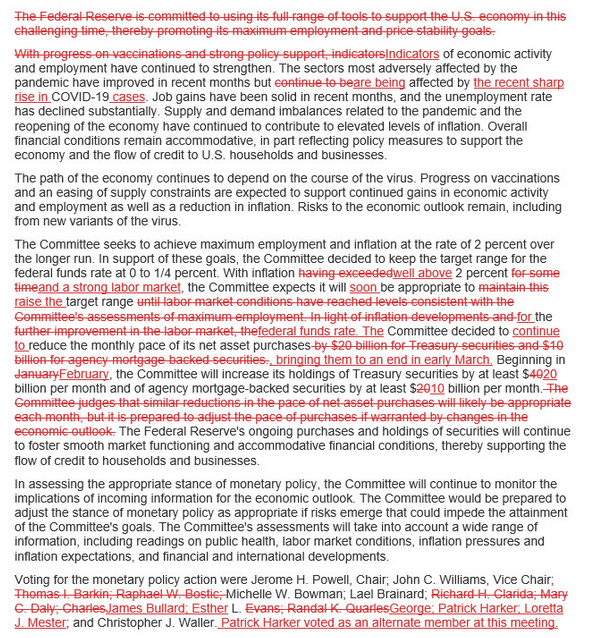

The redlined statement below, courtesy of Zero Hedge, shows the changes from the last FOMC policy statement to the current statement.

In a nutshell, the Fed tightening will start by ending QE in early March, and it “will soon be appropriate to raise the target range for the Federal Funds rate.” Based on the words they removed regarding employment, we can assume they believe employment is at their goal of maximum employment. As such, policy changes will remain focused on inflation.

Powell’s Big Lie

“Asset prices do not represent a threat to financial stability.” – Jerome Powell

The Fed is bluffing when they suggest asset prices are NOT a threat to financial stability. In truth, the Fed focuses entirely on the markets as they are dependent on “stability” to keep the financial “house of cards” from collapsing.

“With the entirety of the financial ecosystem more heavily levered than ever, the “instability of stability” is the most significant risk.

The ‘stability/instability paradox’ assumes all players are rational and implies avoidance of destruction. In other words, all players will act rationally, and no one will push ‘the big red button.’

The Fed is highly dependent on this assumption. After more than 12-years of the most unprecedented monetary policy program in U.S. history, they are attempting to navigate the risks built up in the system.“

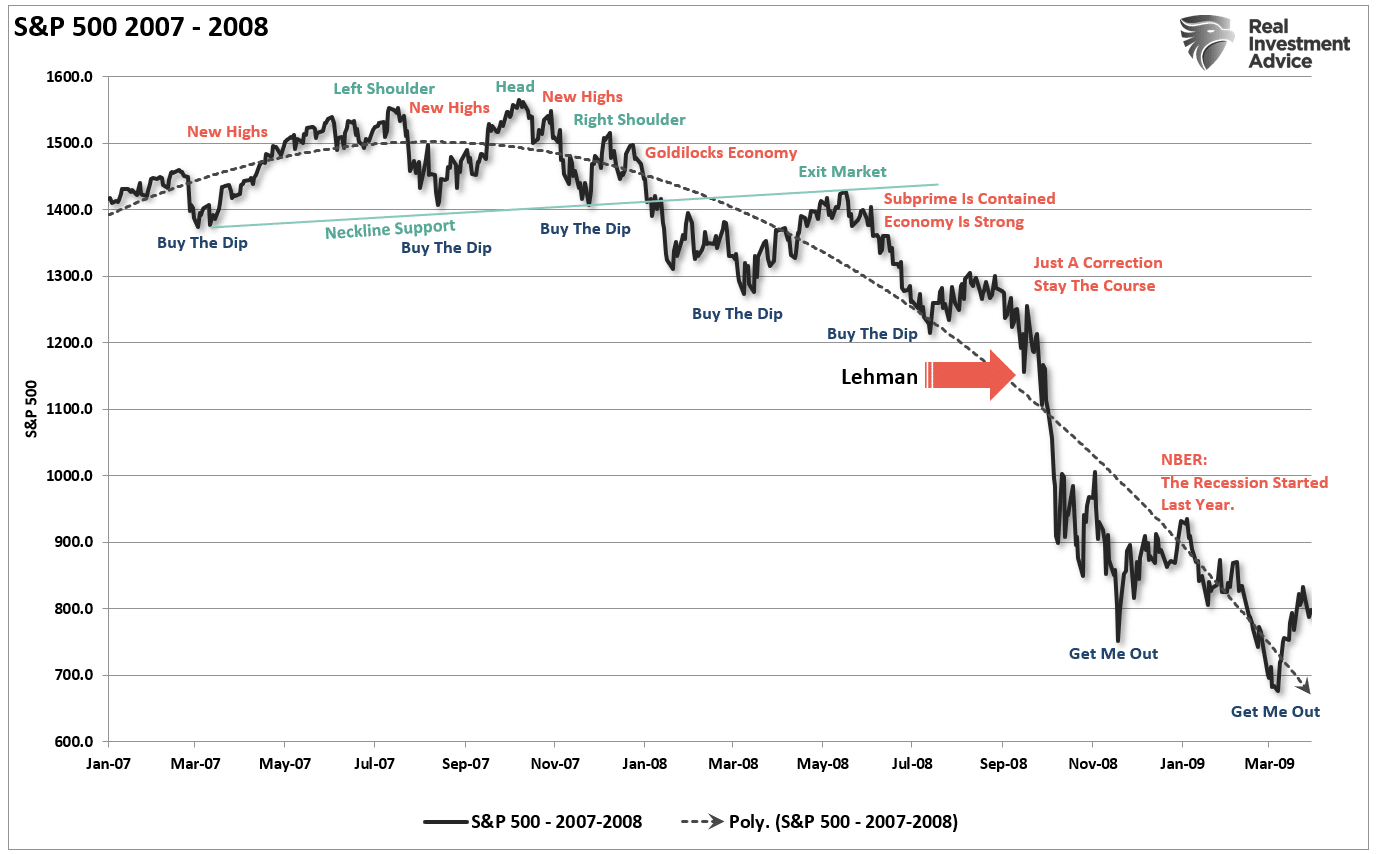

The problem, as shown below, is that throughout history, when the Fed tightens policy, someone inevitability pushes the “big red button.” However, throughout history, the Fed’s actions repeatedly led to adverse outcomes as investors eventually panicked.

- In the early 70’s it was the “Nifty Fifty” stocks,

- Then Mexican and Argentine bonds a few years after that

- “Portfolio Insurance” was the “thing” in the mid -80’s

- Dot.com anything was a great investment in 1999

- Real estate has been a boom/bust cycle roughly every other decade, but 2007 was a doozy

- Today, it’s real estate, GAMA, debt, credit, private equity, SPAC’s, IPO’s, “Meme” stocks…or rather…”everything.”

“If easy money is the bedrock of valuations and the Fed is getting ready to shift the bedrock, investors best pay attention to market forecasts and how the Fed ultimately acts.“ – Michael Lebowitz

With the Fed now tightening policy “sooner and faster,” the only question is how long before something breaks?

This Week’s MacroView

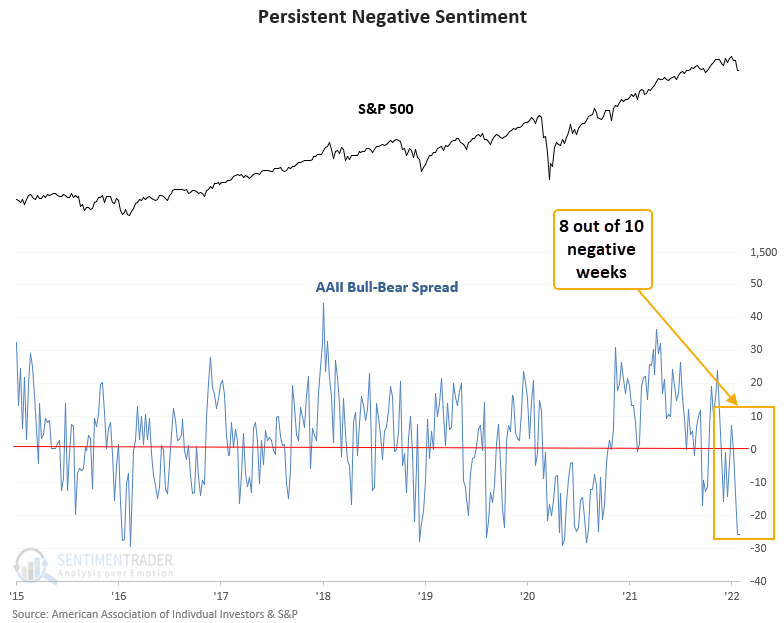

Bearish Sentiment Getting Really Bearish

It is certainly easy to be very “bearish” short-term. However, it is essential to remember that there can be rather vicious rallies, even during “bear markets.” A review of the 2008 “bear market” is a good example.

Of course, what drives the vicious counter-trend rallies is the washout of sellers, as represented by very negative sentiment. Sentiment Trader recently showed such is now present in the market.

The AAII sentiment survey can be used as a contrary indicator to identify an environment where sentiment has become too pessimistic on the future direction of stocks. When opinions become too bearish, stocks tend to rally. – Sentiment Trader

“Dumb Money” traders have proven themselves to be bad at market timing over history. They get bullish after a market rally and bearish after a market fall. By the time most of them catch on to a trend, it’s too late – the trend is about to reverse. It tells us how confident we should be in selling the market. Examples of some Dumb Money indicators include the equity-only put/call ratio, the flow into and out of the Rydex series of index mutual funds, and small speculators in equity index futures contracts. Because the “dumb money” follows trends, they are usually correct during the meat of the trend but wrong at the extremes. – Sentiment Trader

While such does NOT mean the current corrective period is over, it does suggest we are likely to see a reflexive rally that we can use to rebalance equity risk in portfolios.

Signs That Selling May Not Be Done Yet

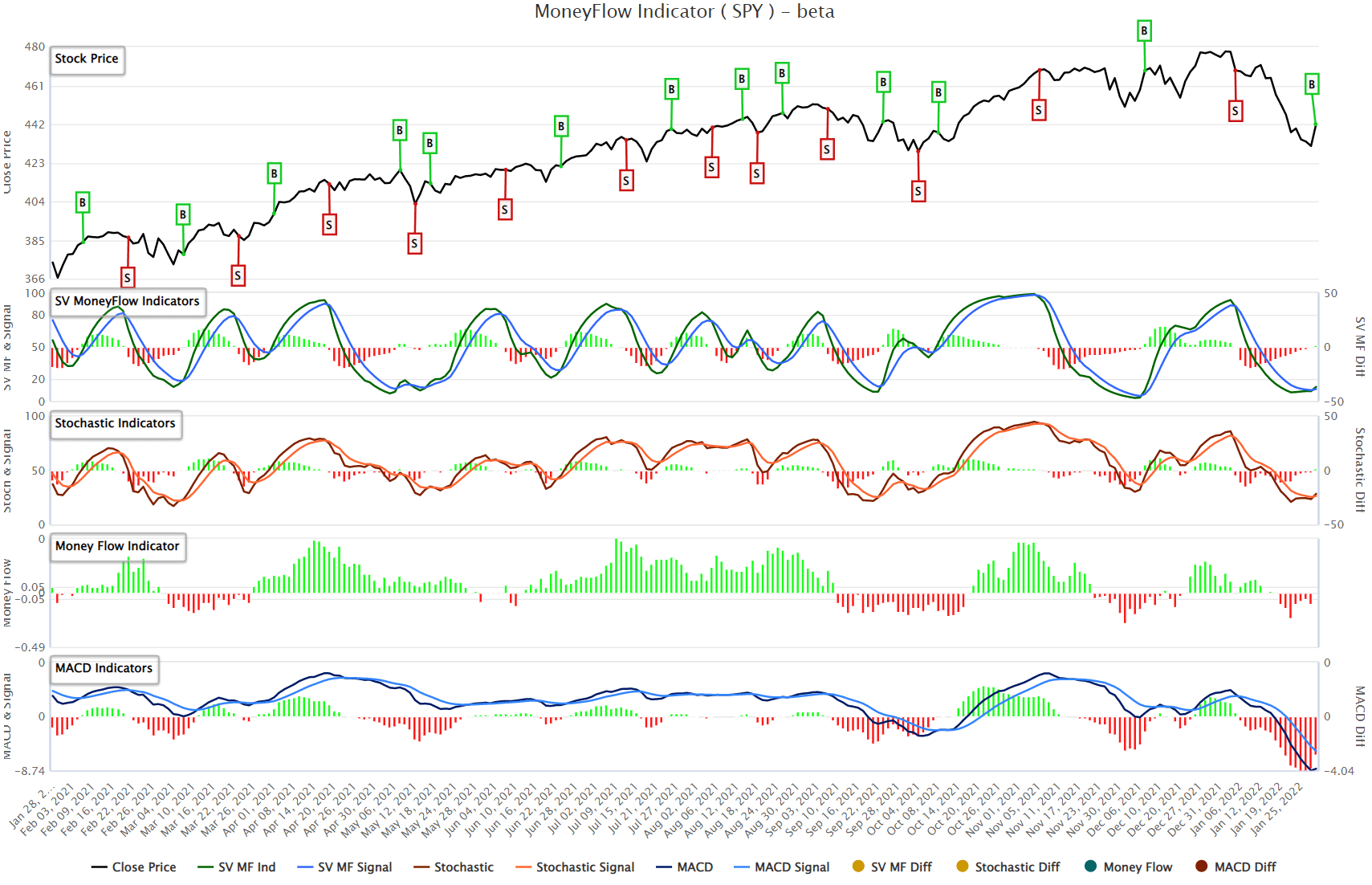

One of the reasons we feel like rallies will be “sellable rallies,” at least for now, is that breadth remains very weak.

As shown below, our Simplevisor Money Flow analysis chart is at extreme oversold levels. Such usually provides a sustainable rally, particularly when the indicator is at extreme lows and triggering a “buy” signal.

As shown below, the market continues to hold very crucial support. However, as noted, the internal breath of the market remains very weak. The good news is that such levels of more extreme oversold conditions of money flows and negative breadth provide fuel for a bounce. However, when it comes, that bounce is likely limited to a 50% to 61.8% retracement of the recent decline.

The fall in the market’s advance/decline line suggests weak participation but with the market at more extreme oversold levels, a retracement rally is likely.

This analysis continues to suggest any rally that occurs will likely:

- Fail at a lower high / resistance level; and,

- The subsequent decline will potentially retest or break recent lows.

We base that assumption on things remaining “status quo” with the Fed’s current stance on tightening monetary policy. However, if the Fed softens its stance or reverses course entirely, this analysis will change.

The crucial point is to understand the risk we are currently dealing with, but not over-react and allow emotions to interfere with prudent decision-making.

Portfolio Update

The bounce on Friday confirms our thesis of a short-term washout. However, it is too early to say with certainty that the recent lows were “the bottom.” However, as noted, we are beginning to search for opportunities in strong companies with excellent fundamentals and strong positioning in the economy. Therefore, while we reduced our equity exposure some last week, we remain positioned for a bounce.

Again, we are looking for a short-term rally that we can trade into. So, we are not yet ready to commit to long-term purchases but rather trading opportunities in beaten-up assets.

My colleague Doug Kass confirmed our thoughts this week on searching for opportunities.

“January has been an unmitigated disaster for many and since price does change sentiment (h/t The Divine Ms M), investor sentiment has dropped like a stone along with plummeting stocks – a prerequisite to stocks reaching attractive levels.

Essentially what we have been expecting (Fed tightening, etc.) is now occurring and with it brought a dramatic decline in stock prices. There was nothing really very new that came out of Powell’s statement on Wednesday, and the market has already begun to discount the well-anticipated Fed pivot.

As well, many companies, post EPS releases, will shortly have a window to repurchase their own shares. Remember, the flows from corporate buybacks were the largest source of stock demand over the last 12 months.

Most importantly, as noted previously, the upside reward vs. downside risk has improved and there is a growing list of attractive stocks.”

We agree. The most challenging thing for an investor to do is buy when everyone else is selling. However, that is precisely when the best trades ultimately get made.

Undoubtedly, it is hard to “buy when there is blood in the streets.”

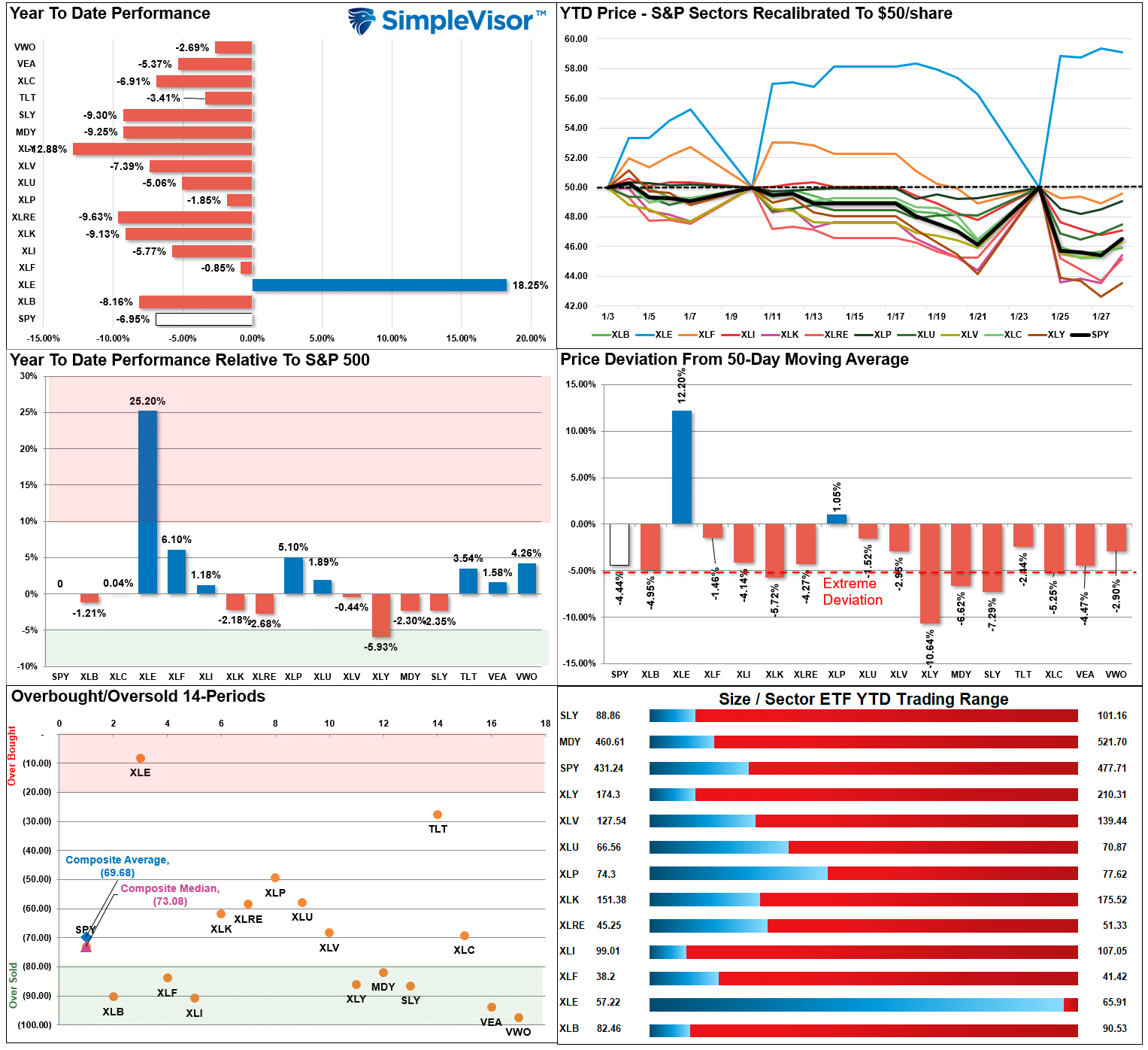

Market & Sector Analysis

S&P 500 Tear Sheet

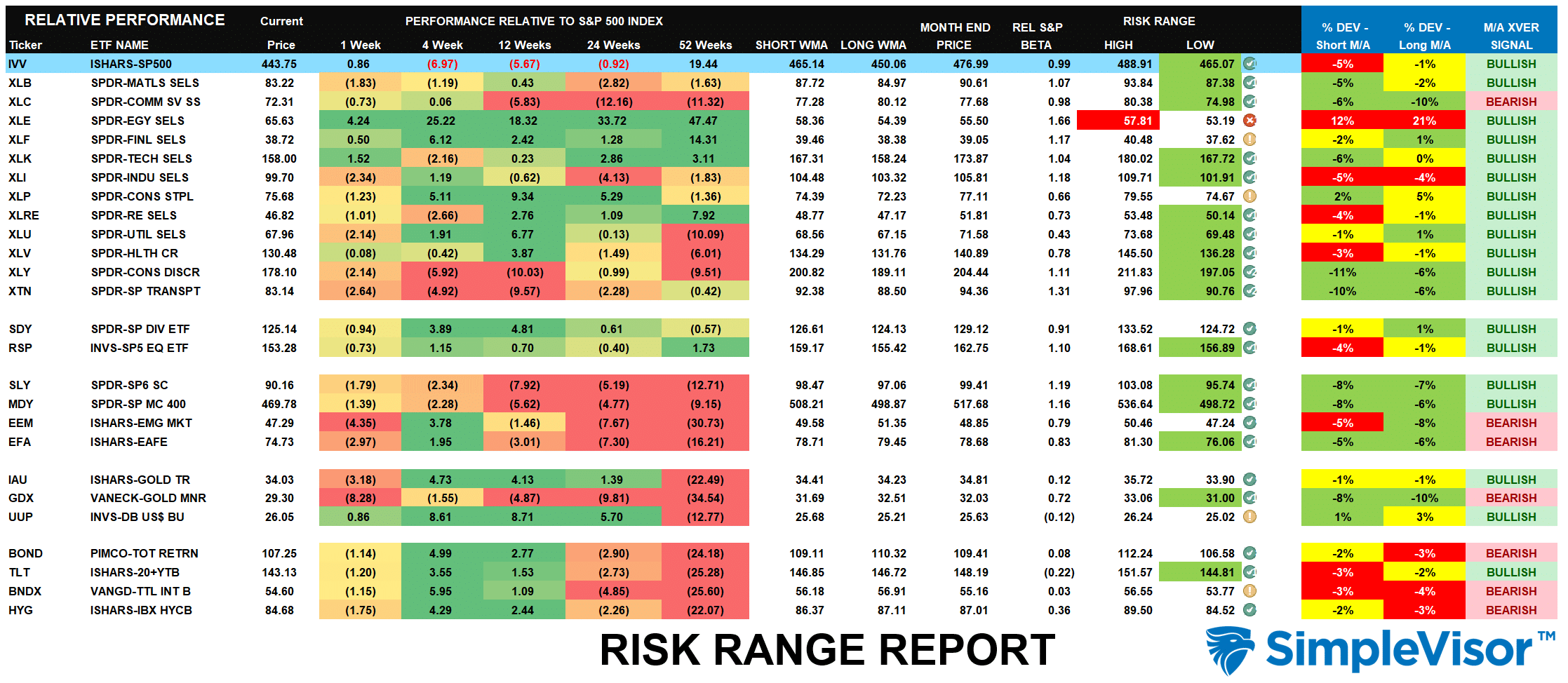

Relative Performance Analysis

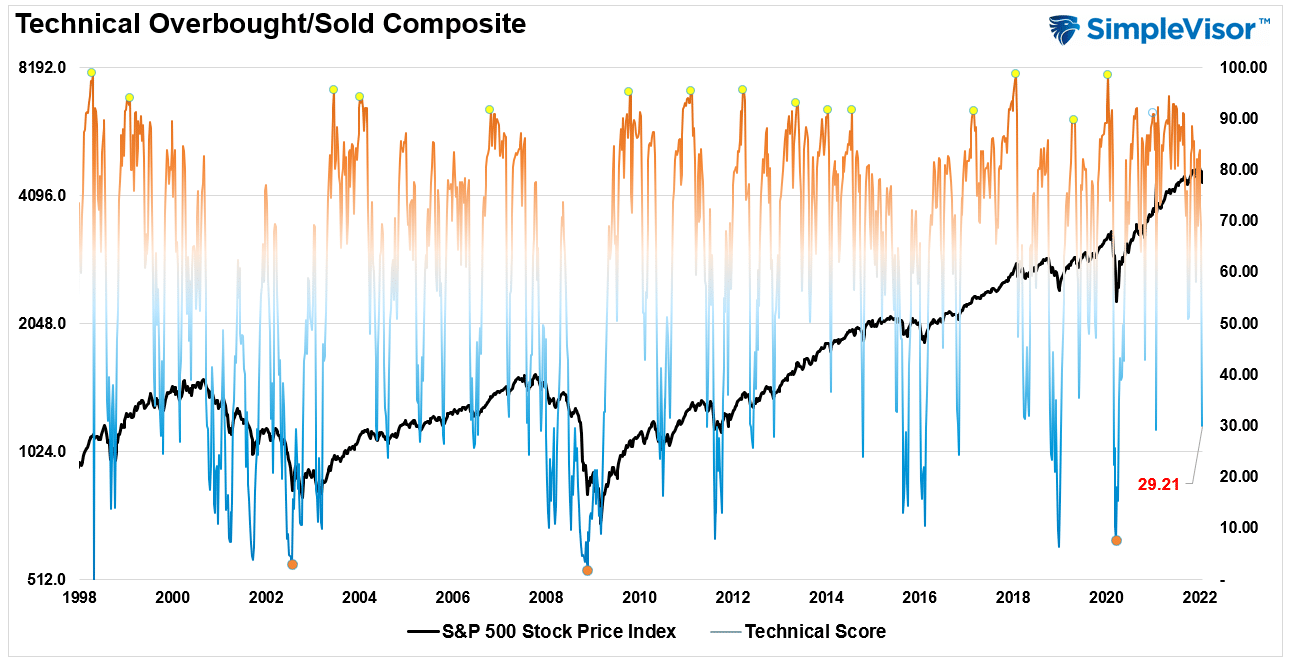

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 29.21 out of a possible 100.

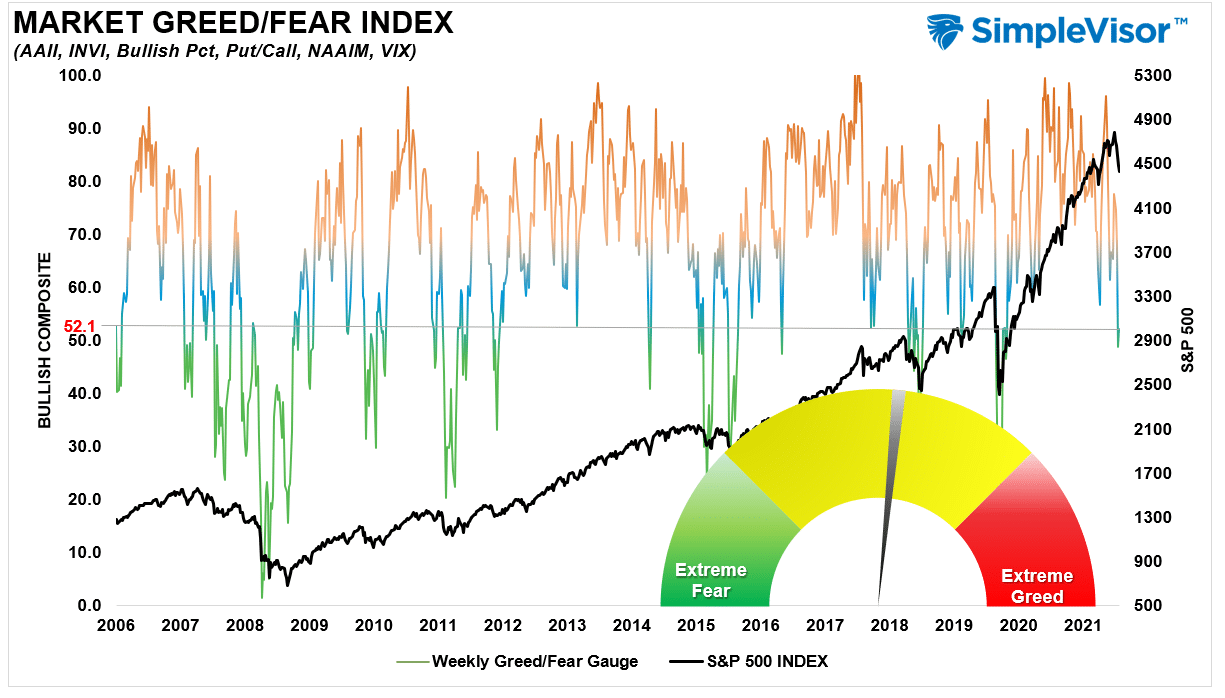

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 52.1 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is on under the Dashboard/Sentiment tab at SimpleVisor

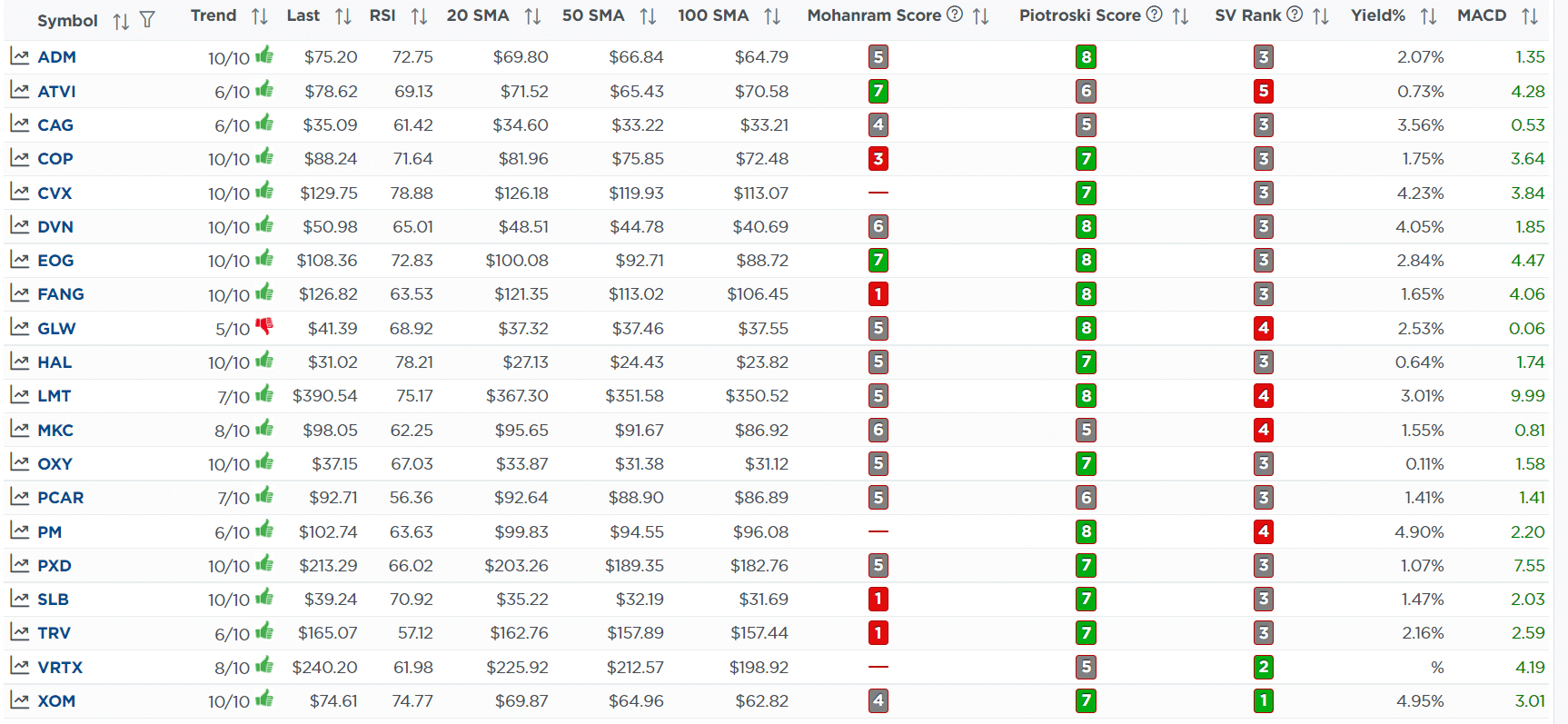

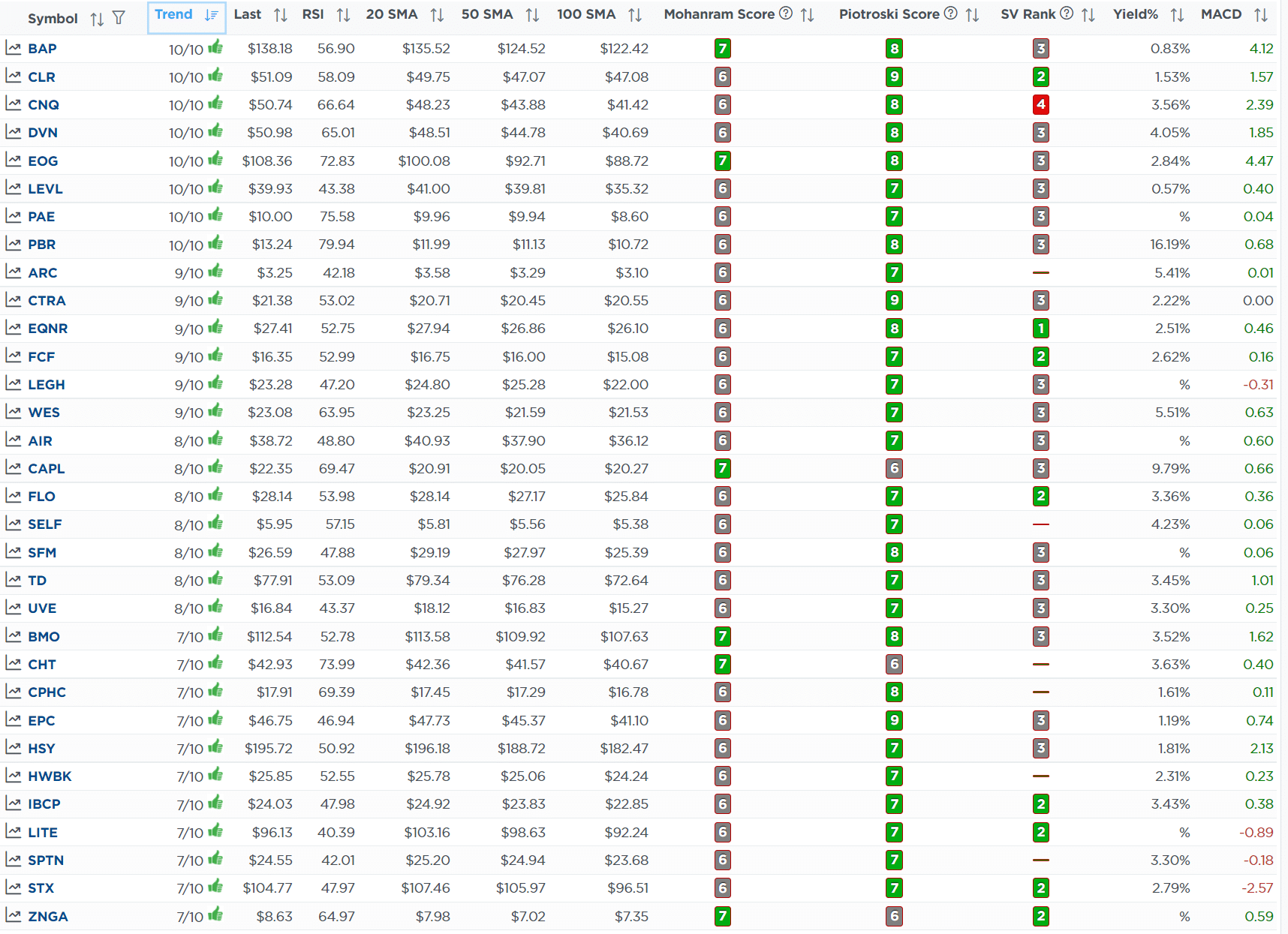

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

There were two sets of trades this week.

January 24th

“We added a QQQ trade for a technical oversold bounce in the market and tried to give it a bit of room for a bounce, but such is not to be the case heading into the Fed meeting. We suspect the Fed will begin to back peddle on their hawkish stance, but we will wait for the bounce to manifest and we will buy back into it at that point. There is a very high probability we are getting stopped out at the bottom of this selloff.” – 01/24/22

Equity Model

- Sell 100% of QQQ

- Sell 100% of ASAN and the rest of NFLX (We sold half previous to the earnings miss)

ETF Model

- Sell 100% of QQQ

January 28th

“This morning we are executing a few “clean up” trades as the market attempts an oversold rally. With the dollar rallying, and deflationary pressures showing up in the economic data, we are starting to trim some of our commodity trades to take in some gains.

The market gyrations are working off the deeply oversold condition we had previously. We suspect that we will get a rally of 4-6% over the next couple of weeks as we progress through earnings. However, that rally will likely fail at resistance. As such we are trimming our PFF holdings and adding a short S&P 500 position incrementally into the rally.

As the market rallies, we will continue to add to the short and reduce our long equity exposures as needed. IF the market breaks above resistance and regains a bullish trend, we will remove the short and add back to our equity holdings.” – 01/28/22

Equity Model

- Reduce Marathon Oil (MRO) to 1% of the portfolio

- Reduce Exxon Mobil (XOM) to model weight of 2% of the portfolio.

- PFF gets reduced by 2% of the portfolio.

- Add 1% of the portfolio to SH

ETF Model

- Reduce XLE from 4% of the portfolio to 3%.

- PFF gets reduced by 2% of the portfolio.

- Add 1% of the portfolio to SH

Lance Roberts, CIO

Have a great week!