3-Market Risks In 2022

The 3-market risks for 2022 are probably not what you think. However, before we get into that, I want to wish you and your families a very Merry Christmas.

As we wrap up 2021, such will mark our 21st year of publishing the weekly newsletter. It has been amazing to watch it grow from a few readers into a global audience. Over the years, we have reported on bull markets, crushing bear markets, financial crises, and economic events, both good and bad.

It has been a privilege, or rather an honor, to continue to share my thoughts with you over all these years. I hope you have found it informative and helpful. As we enter into 2022, I remain hopeful we can continue to share our thoughts for another 20-years.

Thank you again for your loyal readership,

“May the peace and joy that Christmas brings always be with you all year long.”

3-Market Risks In 2022

This week’s newsletter is in a simple format for quick reading. We will return with the regular newsletter in January.

While many issues can impact markets, here are the 3-market risks that we think are the most important.

As Jeffrey Kleintop recently noted:

“Rather, [these risks] are often hiding in plain sight. As goes one of my favorite quotes often attributed to Mark Twain: “It ain’t what you don’t know that gets you in trouble, it’s what you know for sure that just ain’t so.” Risk appears when there is a very high degree of confidence among market participants in a specific outcome that doesn’t pan out.

That is correct. While we disagree on the issues that we think could disrupt the “bull market” in 2022, we do agree that “risk” comes from the disappointment of what was previously “priced” into the market. The repricing of the market to align with “reality” tends to catch investors by surprise.

In this case, the 3-market risks are simply the reversal of previously supportive forces of stock prices. If these forces remain supportive, then markets should continue their bullish advance. However, for whatever reason, should those supports reverse, then logically weaker markets should follow. Such was a point I discussed with Charles Payne on Fox Business this week.

So, what are the 3-Market Risks we see in 2022?

A Reversal Of Monetary Policy

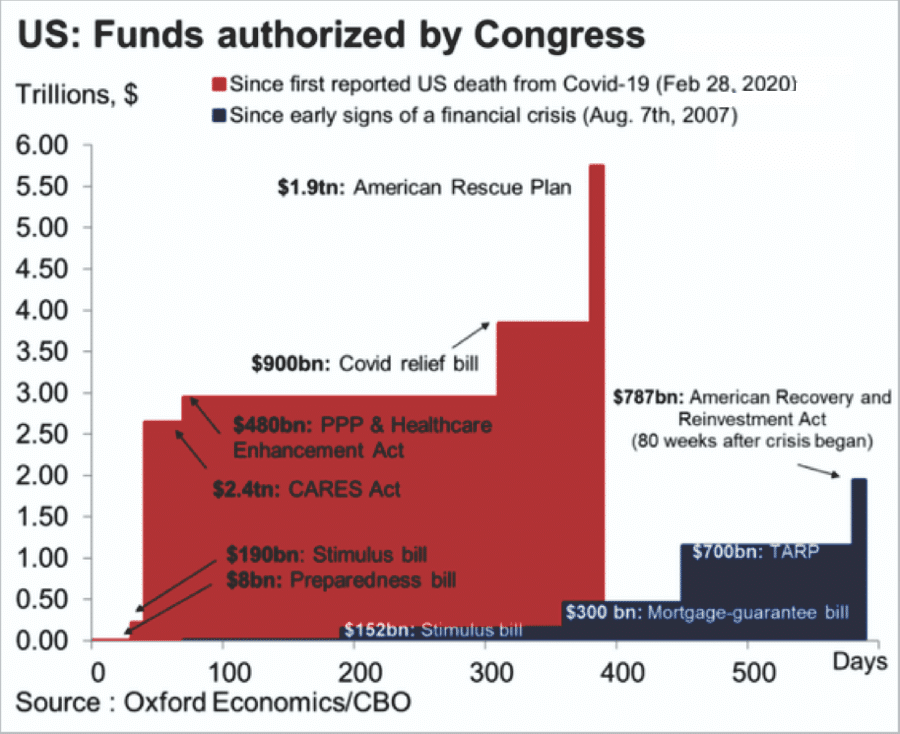

Over the last couple of years, the Federal Government engaged in a tsunami of monetary policies that flooded the financial system. However, the scale of these monetary interventions dwarfed those seen post the financial crisis.

An essential difference between the monetary injection in 2008 and 2020 was the direct checks sent to households. These direct deposits created an enormous demand “pull-forward” on an unprepared supply chain. Not surprisingly, inflation became a problem because it took about 9-months for increases in money supply to hit the economy.

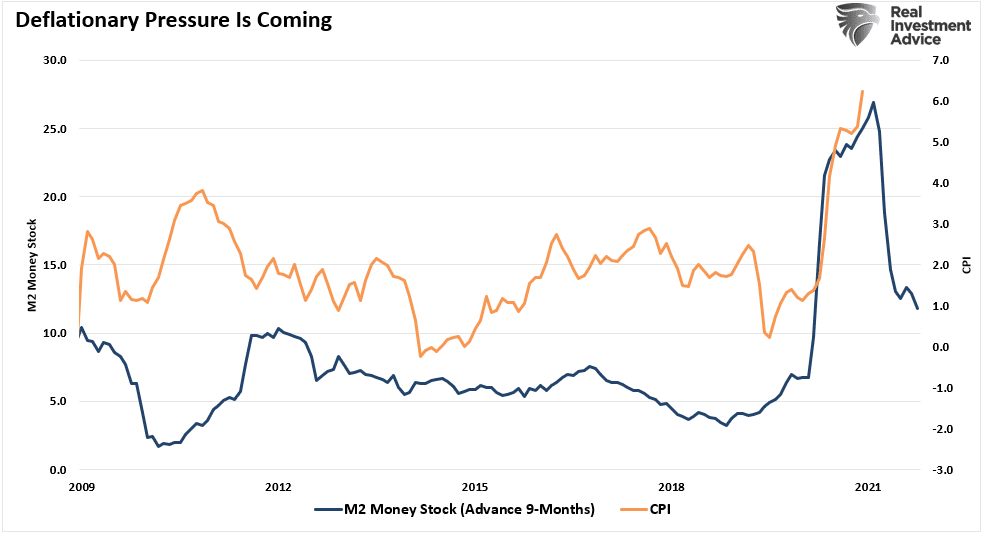

However, with the majority of the monetary impulses fading, 2022 will likely be a year where we could see deflationary pressures return. Unfortunately, the return of deflation may come precisely when the Federal Reserve plans to hike interest rates.

Don’t dismiss that last point lightly. The Fed is hiking interest rates to quell inflationary pressures, which will, by definition, lead to slower economic growth. As Larry Summers previously stated:

“There is a chance that macroeconomic stimulus on a scale closer to World War II levels will set off inflationary pressures of a kind not seen in a generation. I worry that containing an inflationary outbreak without triggering a recession could be even more difficult now than in the past.”

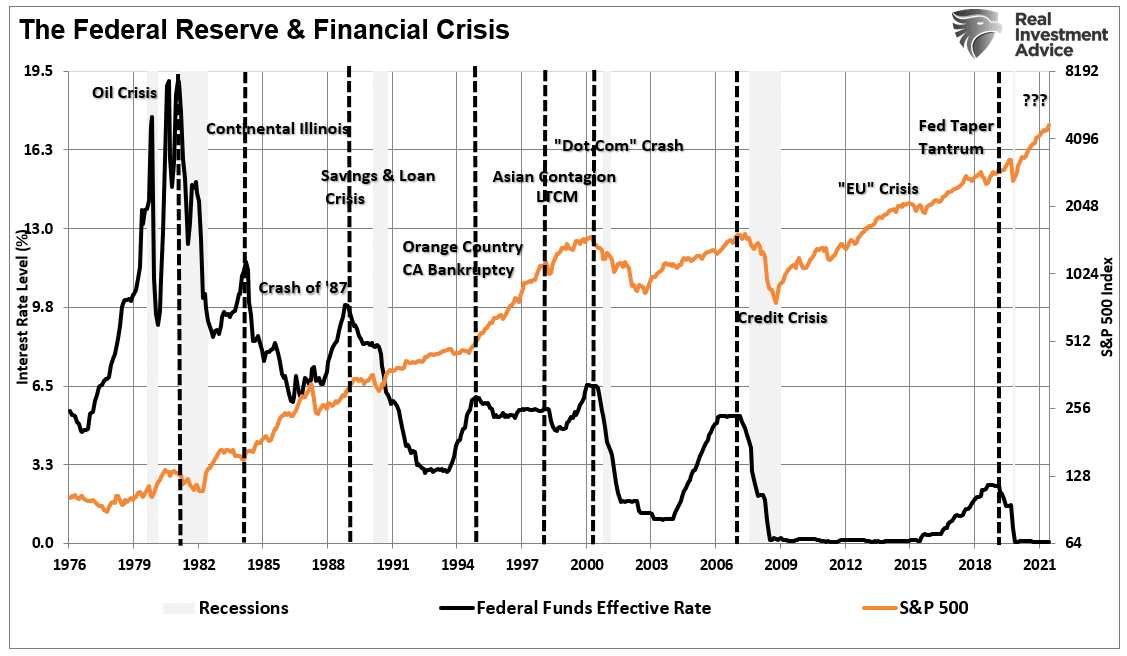

He is correct. The Fed is notorious for mismanaging economic cycles. Despite repeated hopes for a “soft landing,” they have never achieved such an outcome. Instead, their history, as noted previously, is one of creating booms and busts.

The risk is not the initial rate hike, the second, or even the third for stocks. It is the point where the increase in rates causes something to break either in the economy, credit markets, or a change in bullish psychology. Secondly, without exception, rate-hiking campaigns led to a negative outcome.

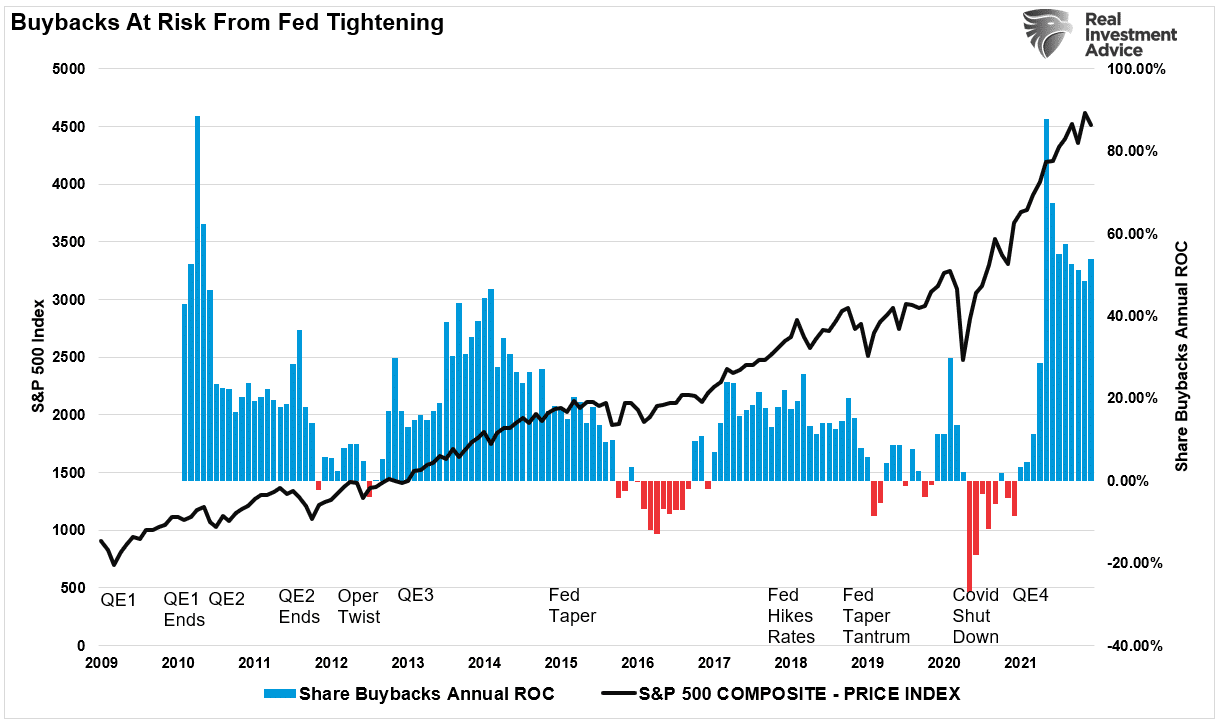

Liquidity Flows Reverse

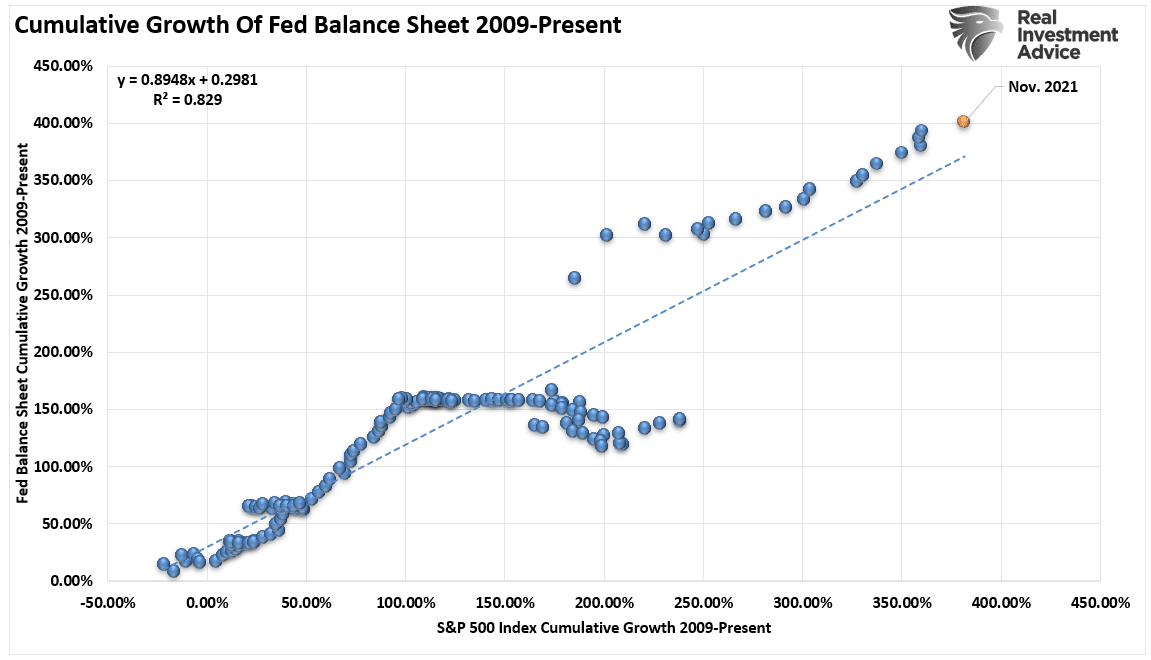

It has not been just fiscal policy that inflated asset prices over the last couple of years, but monetary policy as well. The Fed’s repeated interventions of “quantitative easing” and “zero-interest-rate policy (Z.I.R.P.)” fostered an appetite for speculative risk-taking in the markets. Moreover, as we have shown previously, there is a high correlation between the Fed’s balance sheet expansion and increases in asset prices.

Whether that correlation is due to the direct transfer of liquidity into the financial markets or just a “psychological” one, the link between the Fed’s actions and speculative risk-taking is unarguable.

However, it has not been just the Fed’s monetary policy supporting higher asset prices, but also corporate share repurchases and a record flow of foreign liquidity into U.S. markets to chase returns.

“The return of buybacks is a big antidote to market scares over the withdrawal of Federal Reserve monetary stimulus and the emergence of a new Covid-19 variant. – Bloomberg

While the surge in buybacks may temporarily ease concerns over the withdrawal of monetary support, such will likely not last. Historically, the reversal of Fed policy to a tighter regime slows stock buybacks and tempers stock market returns.

Secondly, the flood of capital into global equity funds could also slow. With less accommodative monetary policy, risk appetites could reverse. It is unlikely the pace of equity inflows can continue at the current clip in a weaker economic and market environment.

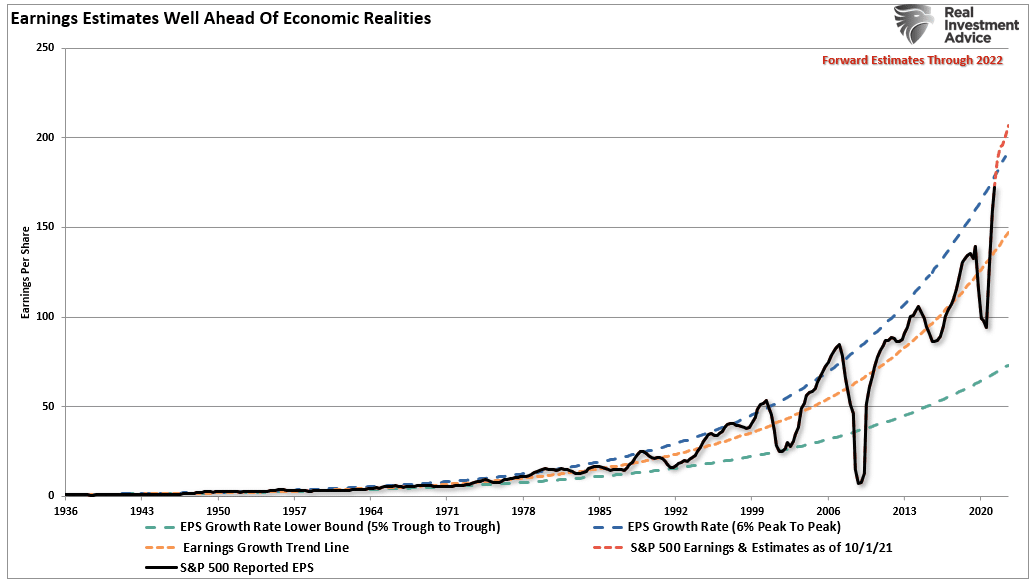

Earnings Disappointment

Lastly, of our 3-market risks in 2022, we think a disappointment in earnings is likely. But, as is always the case in a bull market, analysts are exceedingly optimistic in their estimates.

Analysts increased their earnings estimates despite the Fed tightening monetary policy, potentially weaker economic growth, less liquidity, and tougher annual comparisons. As shown, analysts’ estimates currently exceed the historical 6% exponential growth trend that contained earnings growth since 1950.

While there is certainly a possibility the analysts could be correct, history suggests otherwise.

“The biggest problem with Wall Street, both today and in the past, is the consistent disregard of the possibilities for unexpected, random events. In a 2010 study, by the McKinsey Group, they found that analysts have been persistently overly optimistic for 25 years. During the 25-year time frame, Wall Street analysts pegged earnings growth at 10-12% a year when in reality earnings grew at 6% which, as we have discussed in the past, is the growth rate of the economy.

This is why using forward earnings estimates as a valuation metric is so incredibly flawed – as the estimates are always overly optimistic roughly 33% on average.” – The Problem With Wall Street Forecasts

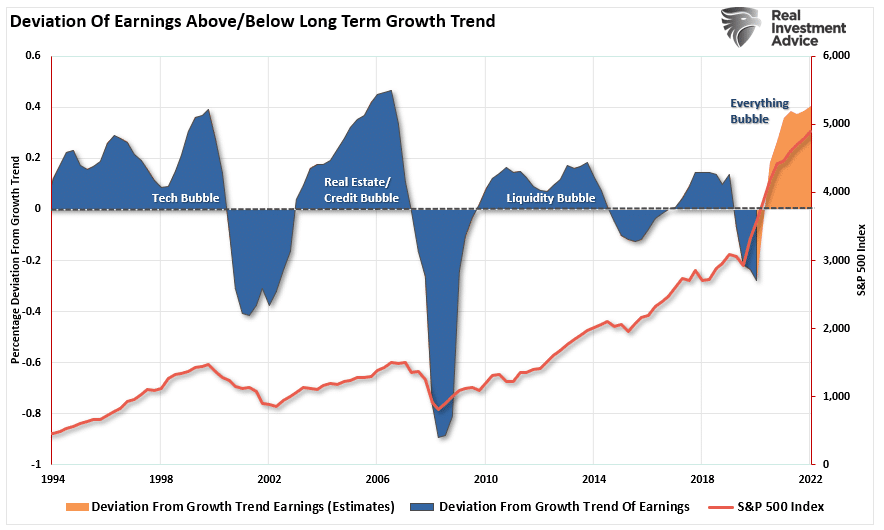

There are currently only two periods with similar deviations above the long-term earnings growth trend – the “Financial Crisis” and the “Dot.com” bubble.

Be Optimistic – Just Don’t Be Blinded By It

As we enter into 2022, we should temper our optimism.

- As noted, tighter monetary policy, and high valuations.

- Less liquidity globally as Central Banks slow accommodation.

- Less liquidity in the economy the previous monetary injections fade.

- Higher inflation reduces consumption

- Weaker economic growth

- Weak consumer confidence due to inflation

- Flattening yield curve

- Weaker earnings growth

- Profit margin compression

- Weaker year-over-year comparisons of most economic data.

I am sure I have forgotten a couple of things. However, the point is that many of the tailwinds that rationalized overpaying for assets since March of 2020 will now become headwinds.

However, the 3-market risks of a reversal of buybacks, liquidity, and earnings growth are the ones we are watching closely. This is because the reversal of liquidity impacts every facet of the economy and markets, and earnings are the “bullish support” for overvaluation.

As is always the case, the event that changes the “bullish psychology” is always unknown. However, the eventual market reversion is almost always a function of changes in liquidity or a contraction in earnings.

So, as we head into 2022, it is acceptable to remain optimistic. However, it is more important not to be “blinded by optimism.”

Merry Christmas & Happy New Year

Lance Roberts, CIO