Currently, you will find the weekly newsletter under the BLOG section at SIMPLEVISOR.COM (Just log in with your current credentials.)

As we finish fixing a few bugs, we will have a site update in the next few days and the newsletter will have its own section under COMMENTARY.

Portfolio Trade Alert For 12-16-21

Trade Alert For Equity & ETF Models Only

With the Fed meeting now behind us, and just options expiration left on Friday, we are using the weakness from the last couple of trading days to fill out the rest of our portfolio for the Santa Claus rally into year-end.

As such we are making 2-key adjustments. First, we are adding slightly to our equity holdings mostly by adding to our S&P 500 index trading position. Secondly, we are rebalancing our bond portfolio to lower volatility and increase yield as we head into 2022.

Equity Portfolio

Sell 100% of GSY (Short-Duration Bond Portfolio)

Add 6% of TFLO (Floating Treasury Bonds)

Increase IEF (Intermediate Treasury Bonds) to 4% of the portfolio.

Increase Preferred ETF (PFF) to 10% of the portfolio

Reduce Apple (AAPL) by 0.5% to take profits.

Add 0.5% to Adobe (ADBE) on earnings-related weakness this morning.

Add 1% of Asana (ASAN) to the portfolio following its recent correction.

Add 2% of the portfolio to the S&P 500 Index ETF (SPY) bringing the trading position to 7%.

ETF Portfolio

Sell 100% of GSY (Short-Duration Bond Portfolio)

Add 10% of TFLO (Floating Treasury Bonds)

Increase IEF (Intermediate Treasury Bonds) to 4% of the portfolio.

Increase Preferred ETF (PFF) to 10% of the portfolio

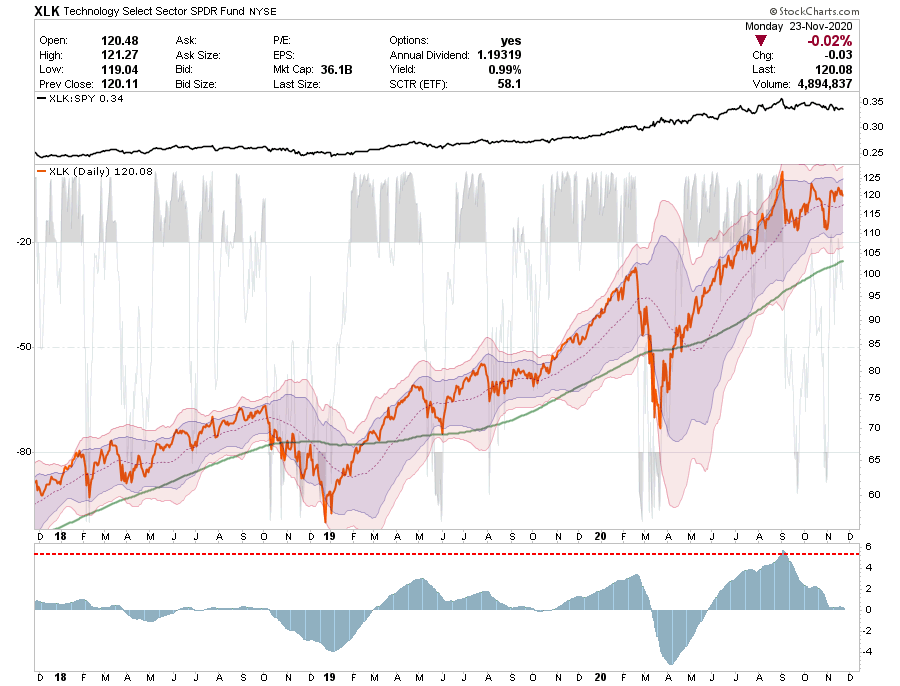

Add 1% to Technology Select ETF (XLK) bringing total weight to 14%

Add 2% of the portfolio the S&P 500 Index ETF (SPY) bringing the trading position to 7%.

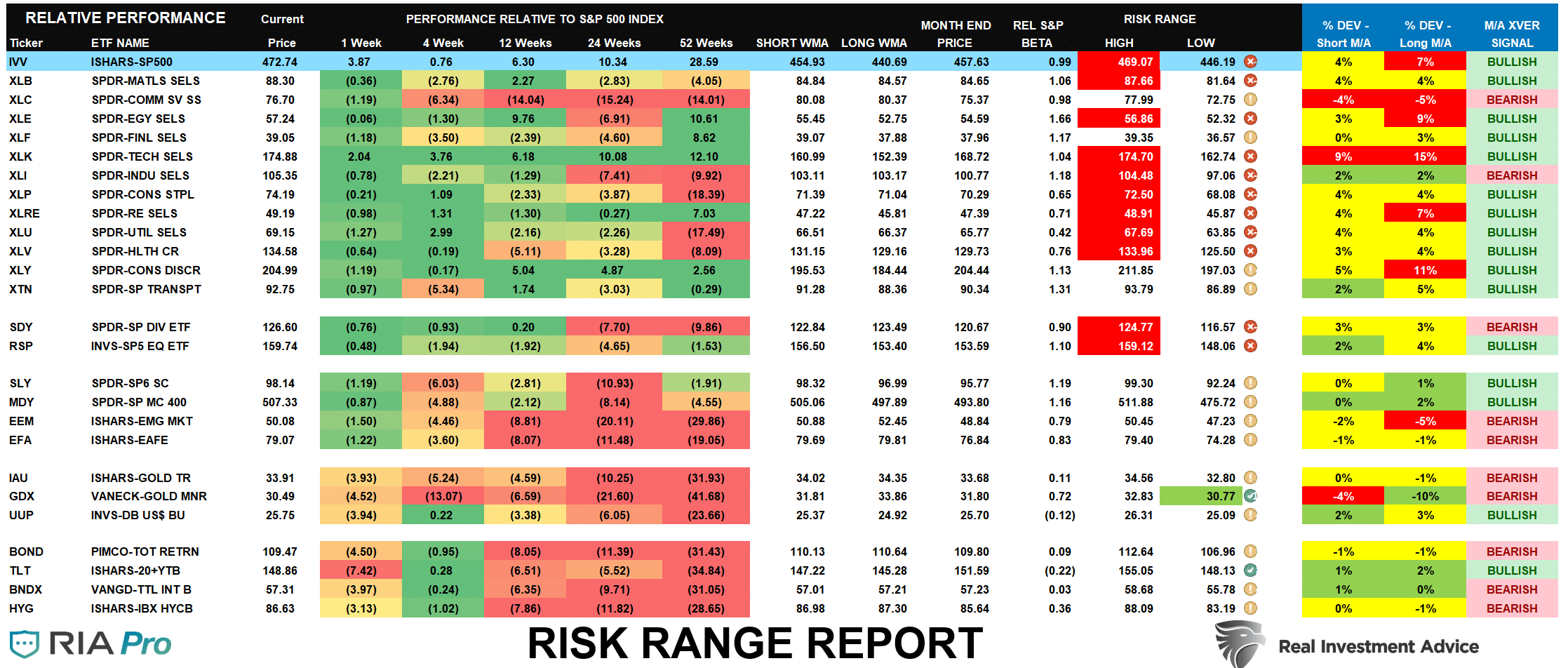

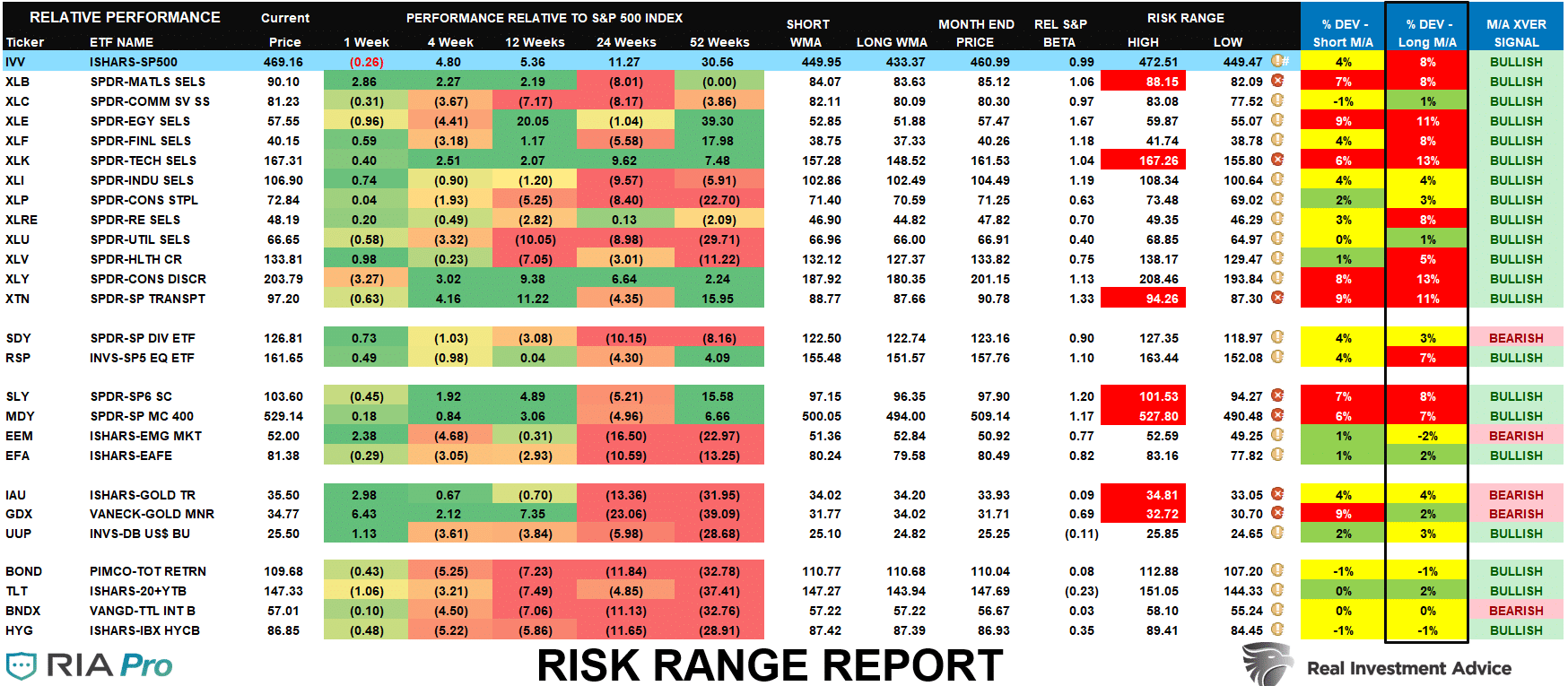

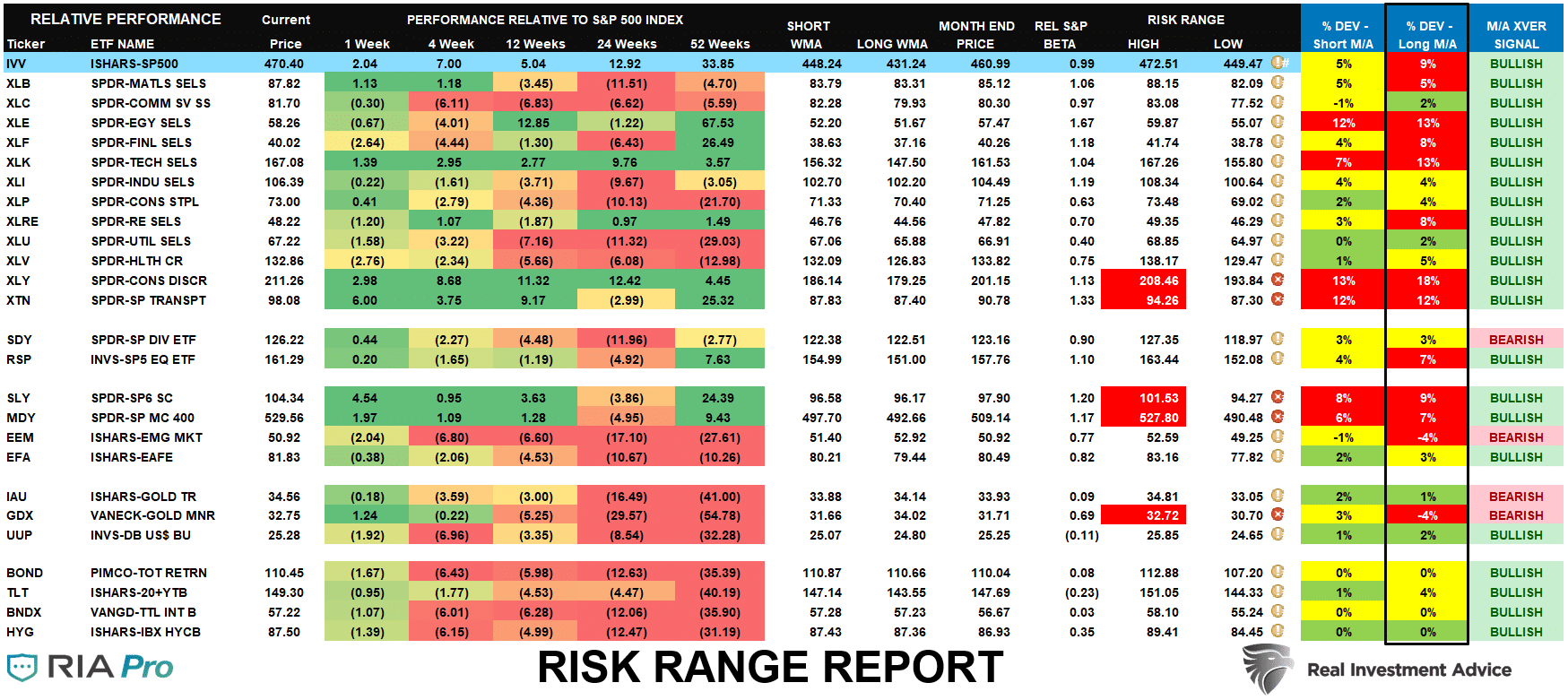

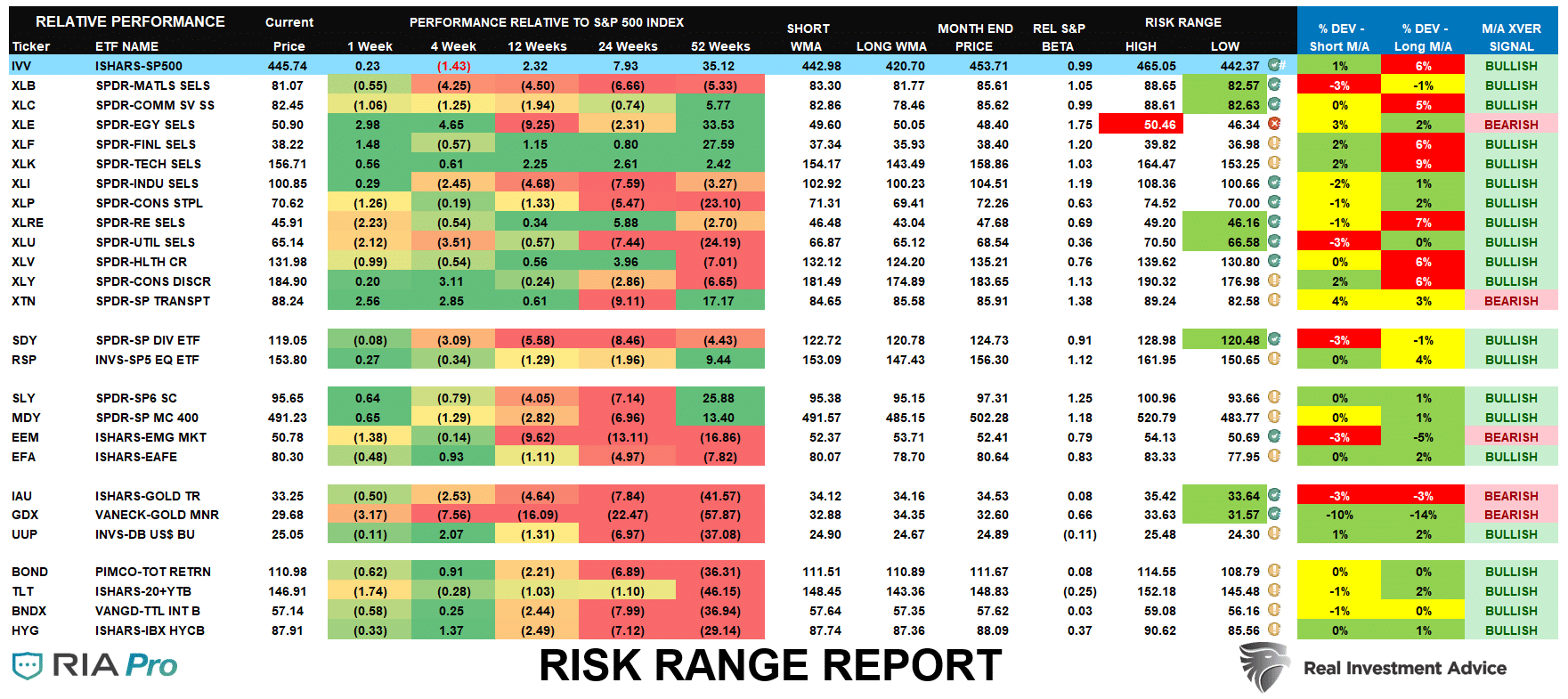

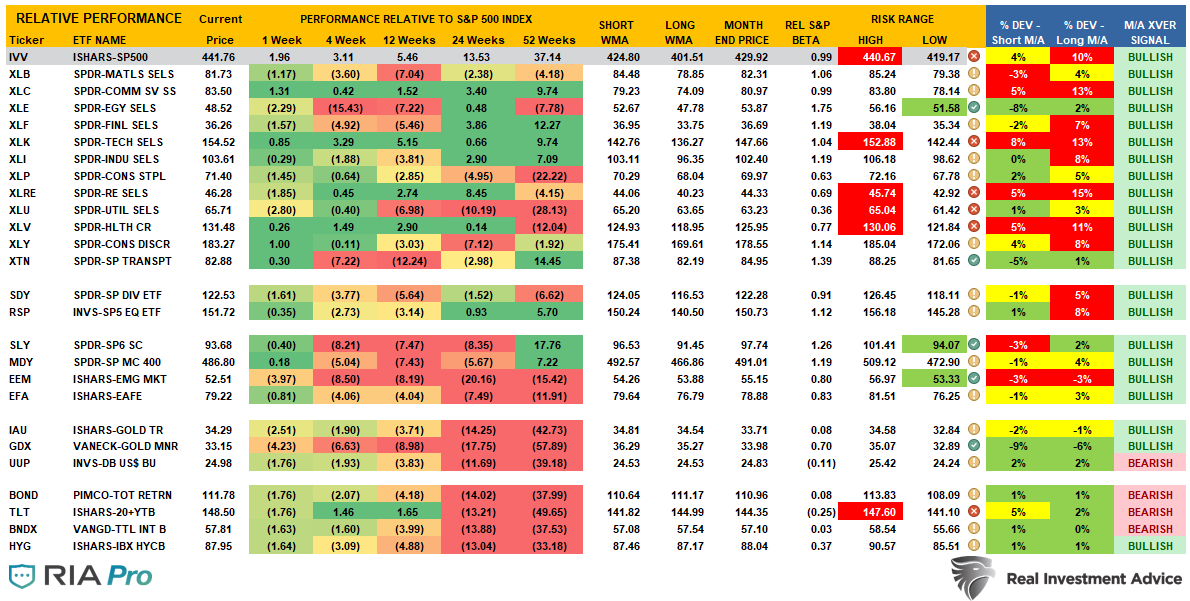

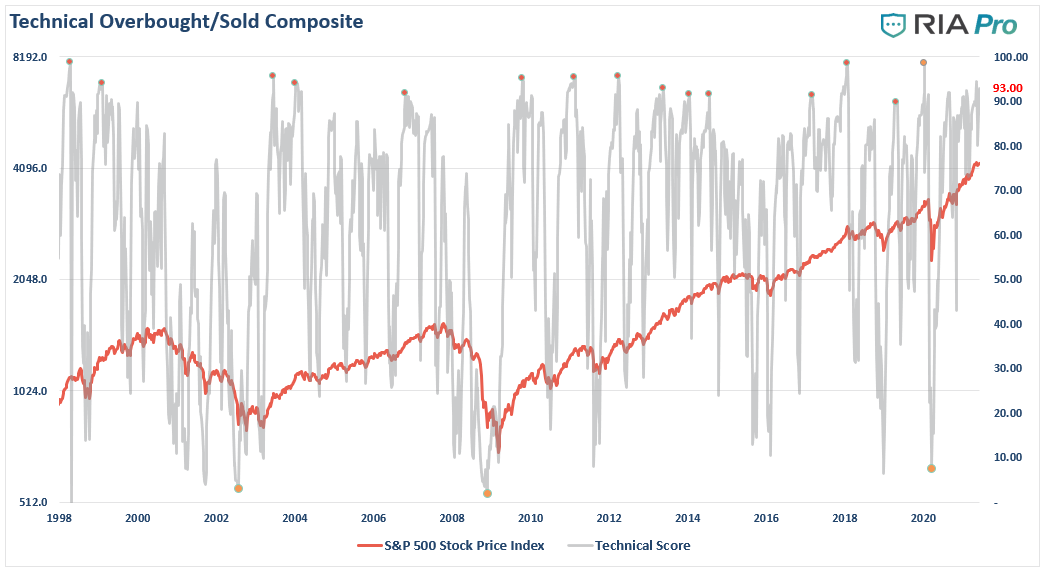

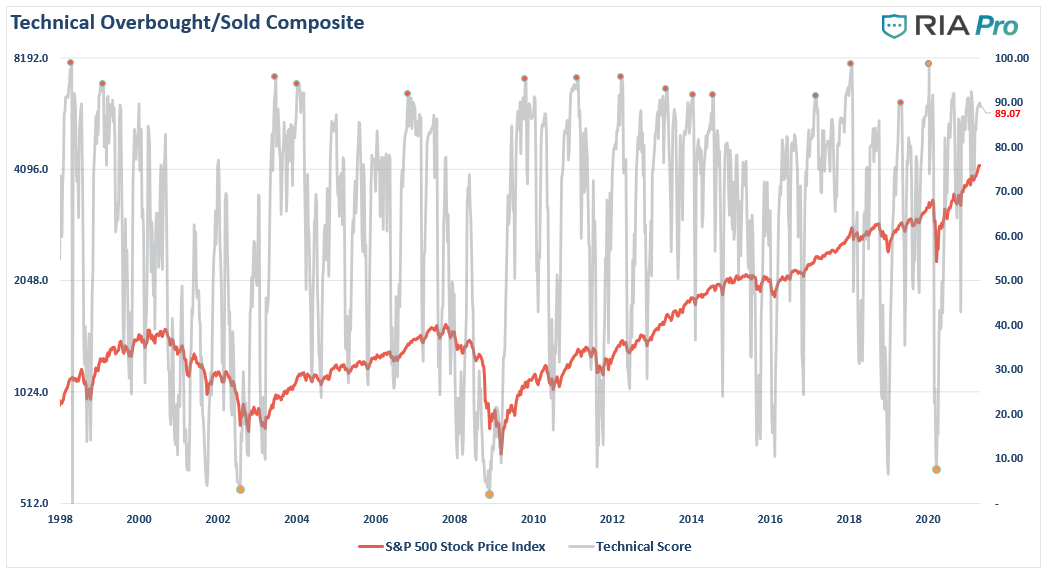

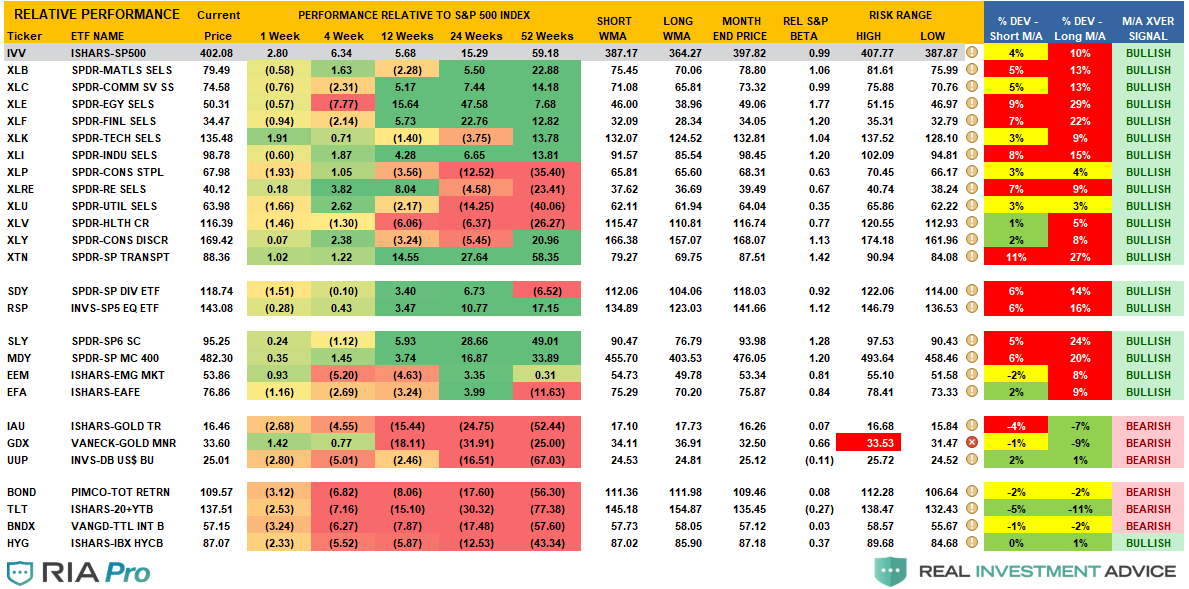

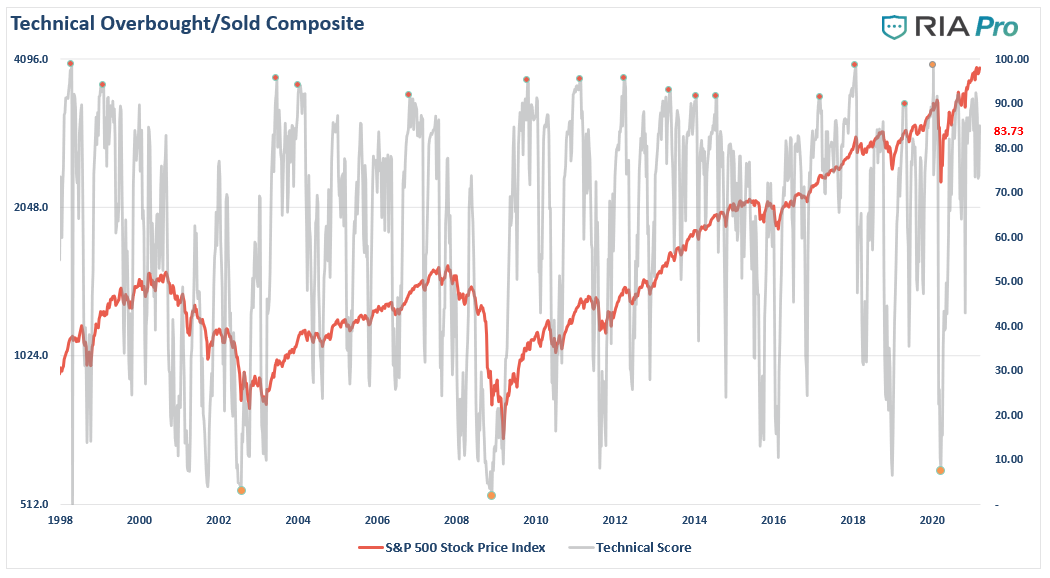

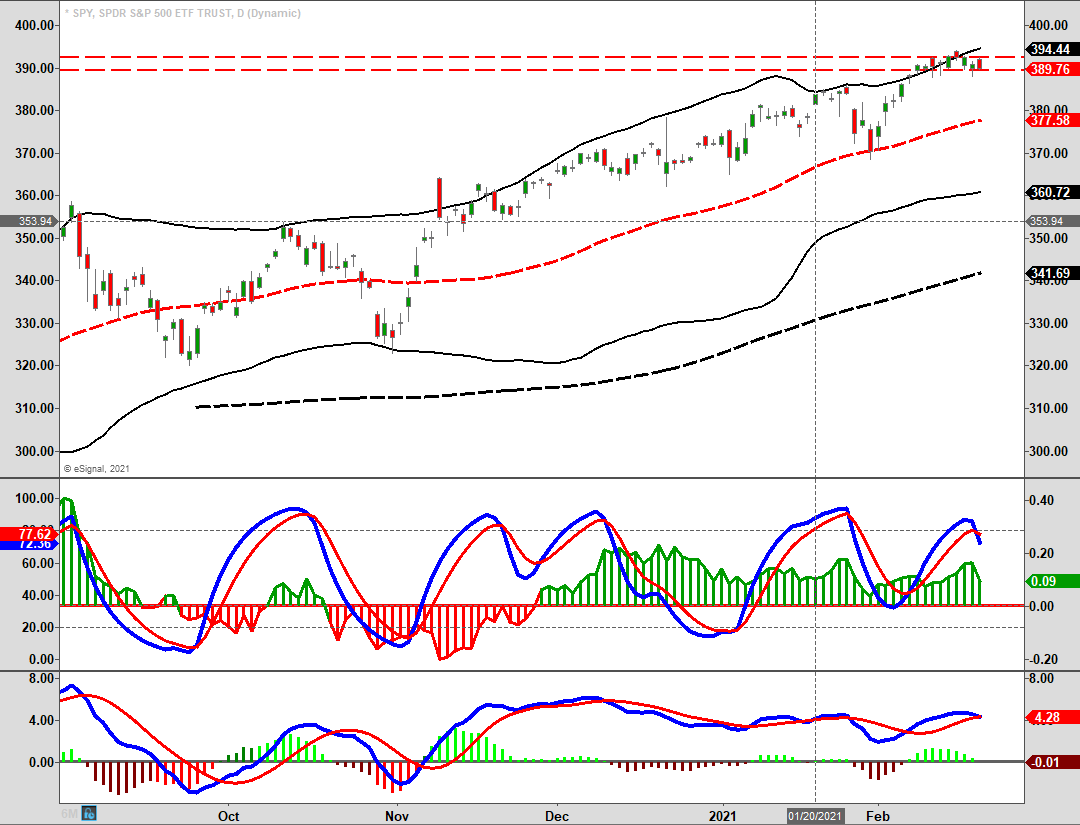

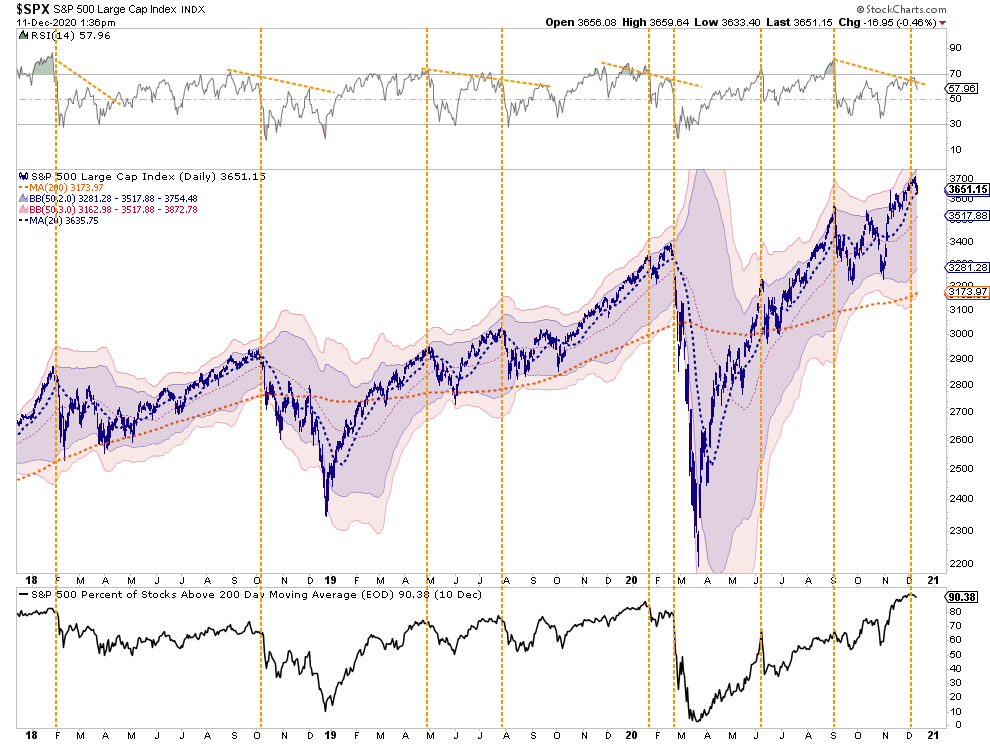

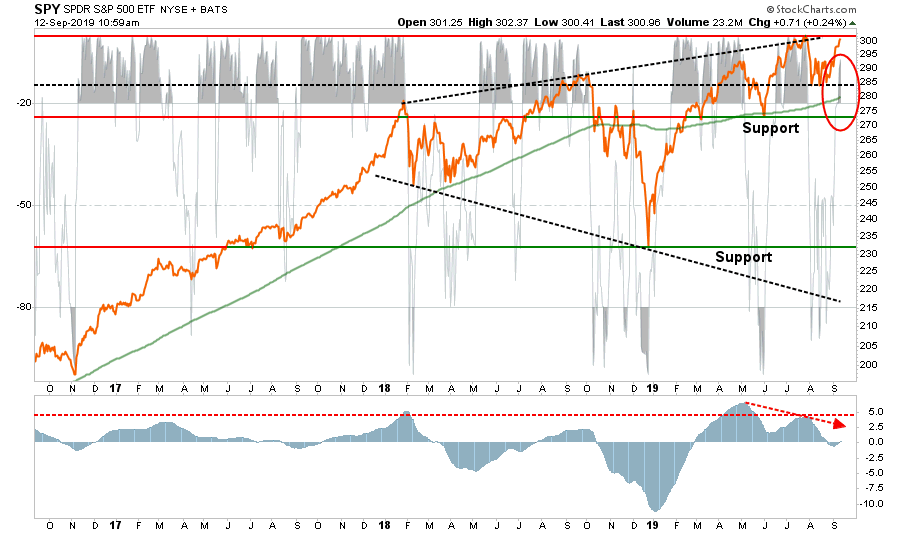

Risk/Reward Range Suggests Short-Term Correction Possible.

Portfolio Trade Alert For 12-10-21

NOTE: Trading alerts are moving to SimpleVisor.com entirely starting January 1st, 2022.

Trade Alert For Both Equity & ETF Models

As noted previously, we will continue to use weakness in the market to add additional exposure to the portfolio in preparation for the year-end rally. Today, we are adding 3% of the portfolio into the equity allocation sleeve.

With the exception of the addition of 1% to our SPY trading position, we are adding to our existing core holdings in both models after recent corrective action. We do expect we could see some additional market weakness next week heading into December options expiration. We will continue using dips to add exposure accordingly.

Equity Model

Increase Netflix (NFLX) by 0.5% of the total portfolio. Model weight is now 2.5%

Add 0.5% to Adobe (ADBE) bringing total portfolio weight to 2.5%.

Ford (F) gets increased by 0.5% to a total weight of 3%.

Costco (COST) also gets increased by 0.5% to a total weight of 3%.

Add 1% to the SPY trading position bringing the total weight to 5%.

ETF Model

Add 1% to LIT (Lithium ETF) bringing portfolio weight back to 3%.

Increase XLK (Technology ETF) by 1% bringing total portfolio weight to 13.5%

Add 1% to the SPY trading position bringing the total weight to 5%

Portfolio Trade Alert For 12-07-21

*** Portfolio Trading Alert *** – Equity Model Only

As noted in this past weekend’s newsletter, we started adding to our equity exposure in the portfolio due to the short-term oversold condition in the market. Furthermore, our “money flow” indicator is about to flip to positive registering a buy signal for the market. (This indicator is in the last stages of development and will be deployed soon for your use.)

After previously taking profits when the “weak sell” signaled was triggered, we are now adding back to those positions now that they have suffered sizable corrections. We are also maintaining our SPY trading position for now as well, which increases our equity exposure to target model weights.

Equity Portfolio

Increase Nvidia (NVDA) to 2% of the portfolio

Same also for AMD (AMD), increase to 2% of the portfolio

Add 1% to Microsoft (MSFT) increasing portfolio weight to 3.5%

Also, add 1% to Marathon OIl (MRO) bring total portfolio weight to 2%.

Increase Raytheon Technologies (RTX) to 2% of the portfolio.

Lastly, add 1% to Albamarle (ALB) bringing the total weight back to 4% of the portfolio.

We added 2% of SPY to the sector and equity models late this afternoon. We are taking advantage of today’s sell-off to add to our position. The market is holding support at the 100-dma and is deeply oversold. We suspect we will see a tradeable rally into next week.

Add 2% of the portfolio in SPY to the current holdings. (Position size increases to 4%)

Over the last couple of weeks, we discussed the potential for some corrective action in the first two weeks of December as mutual funds distribute their annual gains. That selling came a bit sooner than expected, but our previous reduction in equity exposure and hedging reduced our overall volatility. With the deeply oversold condition now present, and the seasonal tendency for a year-end rally, we are now starting to increase our risk exposure accordingly.

We are nibbling at some beaten-up oil stocks, adding a broad market trading position, and continuing to clean up laggards. Over the next week or so, we will look to increase allocations in Healthcare, Technology, Energy, and Financials primarily. Although we will pick up opportunities wherever we find them.

Equity Model

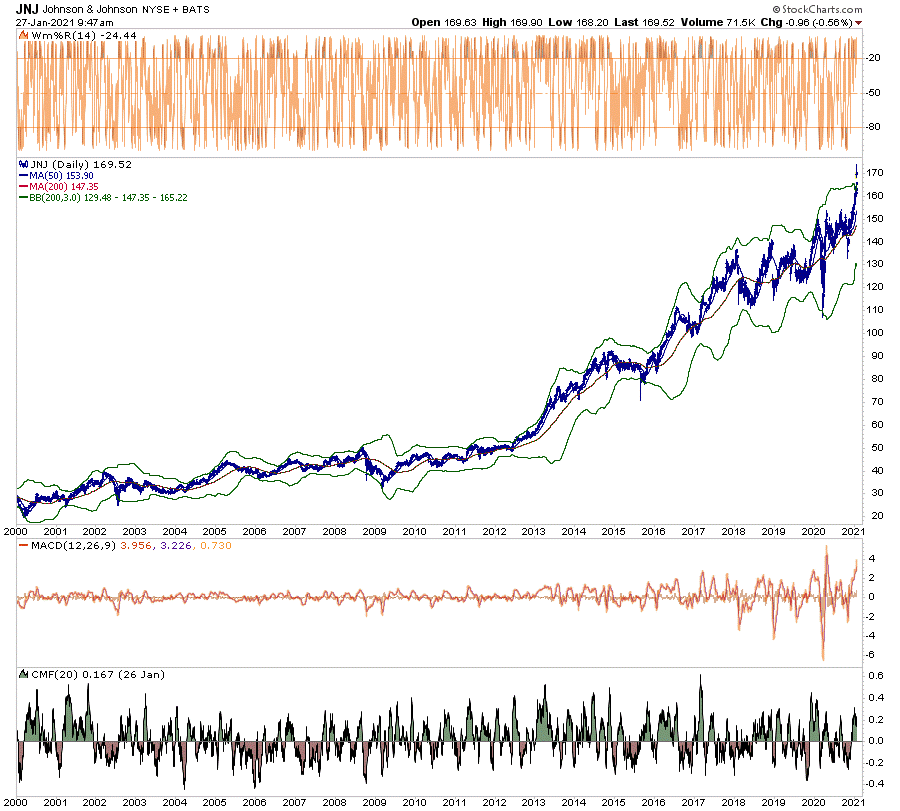

Sell 100% of Johnson and Johnson (JNJ)

Increase XOM to target a weight of 2% of the portfolio.

Initiate a 1% position in MRO (Marathon Petroleum)

Add a 2% trading position in SPY in the portfolio.

ETF Model

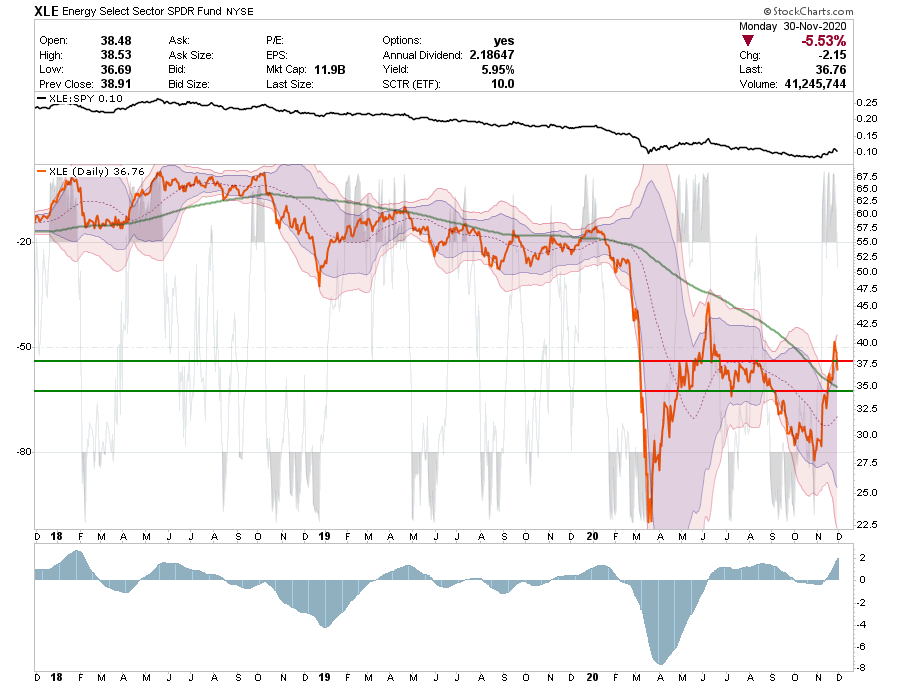

Add 1% to XLE bringing the total position weight to 3% of the portfolio.

Add a 2% trading position in SPY in the portfolio.

*** Portfolio Trading Alert *** – Equity Model Only

We sold Verizon (VZ) in the equity model this morning for tax-loss harvesting. We have a lot of gains to offset this year from profit-taking. While we like Verizon fundamentally, particularly the 4% yield, we think it could continue to trade weaker over the next couple of weeks as mutual funds and professional managers do the same. We will likely buy it back in a month as it should benefit from the infrastructure bill and a potential shift to value next year.

We previously put on a small volatility hedge in light of the record number of call options outstanding. At that time we said we would close out that hedge when those options expired. This more we sold the entire hedge of VXX at a small loss. Given that next week is Thanksgiving, and trading volumes will be exceptionally light, we are leaving the portfolios with a heavier weighting of cash to offset risk.

Equity & ETF Models

Sell 100% of the Volatility Index (VXX)

November 17, 2021

*** Portfolio Trade Alert *** Equity Model

This morning news hit that Amazon (AMZN) would not be accepting Visa (V) credit cards issued in the U.K. That news sent the stock immediately lower this morning violating all of our stop-loss levels. While we still have a small gain in the stock, we are selling the remaining shares in our portfolio. We are looking for a replacement in the space and are evaluating some candidates to add.

*** Portfolio Trade Alert *** Equity and ETF Models

Over the last week, we have discussed reducing equity risk slightly by raising cash and adding hedges. As we head into options expiration week, the Thanksgiving holiday, and mutual fund distribution season, we are looking to become a little more defensive by raising cash levels.

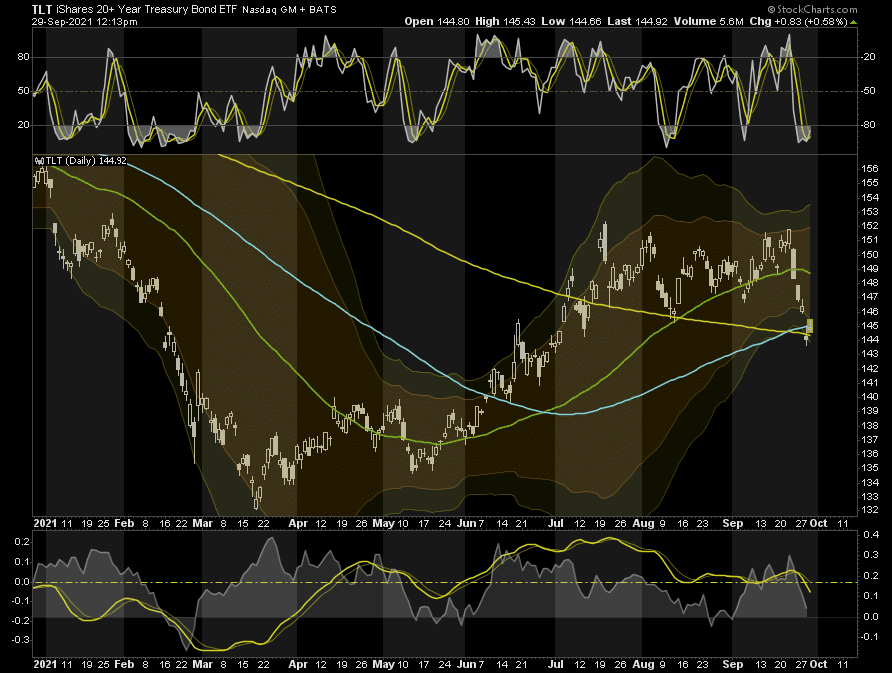

Currently, our bonds have gotten extremely overbought short term, so we are trimming our duration back a bit by reducing TLT. We are still fully in the camp that rates will fall next year as the economy slows, so we will use a pullback in bond prices to increase our exposure.

On the equity side of the allocation, we are just reducing our position sizes in some stocks or sectors that are more extremely overbought and triggering short-term sell signals.

Equity Model

Trim TLT from 8% to 6%

Reduce PFF from 10% to 7.5%

Reduce MSFT from 2.5% to 2% of the portfolio.

Taking profits in AMD from 2.5% to 1.75%

Trimming ABBV from 4% to 3.5%

Reducing ABT from 2% to 1.5%

For a second time, we are reducing NVDA from 2% to 1.75%

As noted earlier this week, with the market back to extreme overbought and extended levels, and individual names making outsized moves, we are taking some small profits out of our most egregiously extended positions.

In the equity model, we are reducing CVS Health (CVS) from 3.5% of the portfolio to 3%.

Equity Model

Reduce CVS from 3.5% to 3.0% of the portfolio.

November 2, 2021

*** Portfolio Trade Alert *** Equity & ETF Models

The market is now back to extreme overbought and extended levels. As such, we are now taking some small profits out of our most egregiously extended positions.

In the equity model, we are taking some profits in F, NVDA, ALB, and NFLX back to model weights. We are also selling all of SBUX after it violated our stop levels.

In the sector model, we are reducing LIT by 0.5% as it is overbought like ALB. We remain decently overweight in the basic materials sector.

With the market entering a “melt-up” phase on earnings exuberance, we are adding to our VXX position today to hedge against the currently overbought conditions. With the Fed meeting next week, there is a risk of a short-term sell-off if the Fed appears more hawkish than expected.

Both Models

Add 1% of the portfolio to VXX increasing size to 3% of the portfolio.

October 27, 2021

*** Portfolio Trade Alert *** Equity & ETF Models

This morning we trimmed back on both of our energy exposures (XOM and XLE) back to model weights. The recent run took the positions out of tolerance relative to the portfolio.

We also added a 2% position in VXX (Volatility Index) which has become very suppressed lately. Given the overbought condition of the market, we are looking for a small risk hedge heading into the Fed meeting next week.

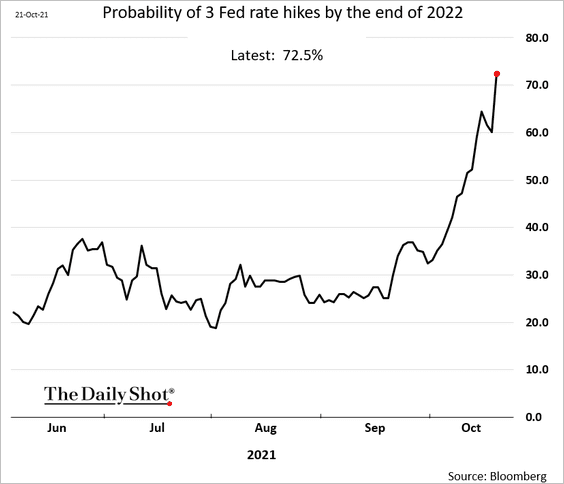

This morning we sold 100% of SHY which is under pressure as the market gets more aggressive about pricing in future interest rate hikes. As shown, there is currently a 100% chance the Fed will hike rates twice in 2022, and a 70% chance of three rate hikes.

When the Fed gets more aggressive about rate hikes, the long end of the curve will fall. Therefore, as the 10-year moves toward 1.8-2%, we will become more aggressive buyers of duration. For the meantime, we will leave the money in cash and over the next week or so decide how to deploy it within the fixed income sector.

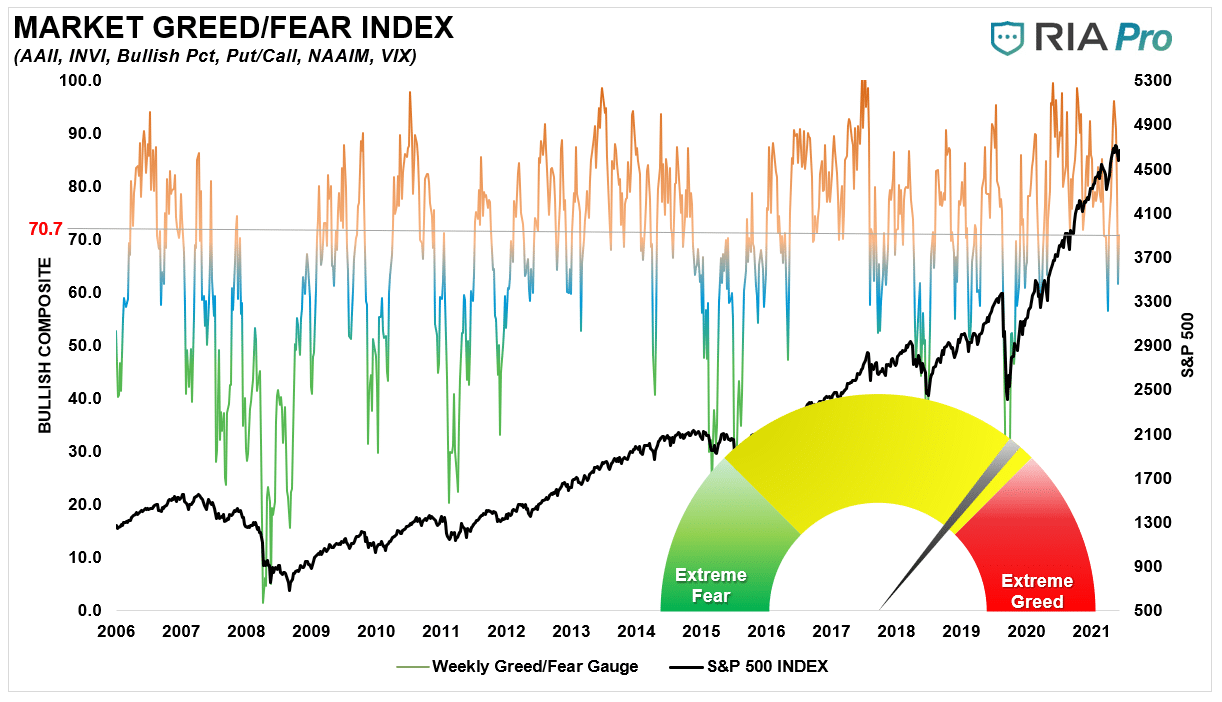

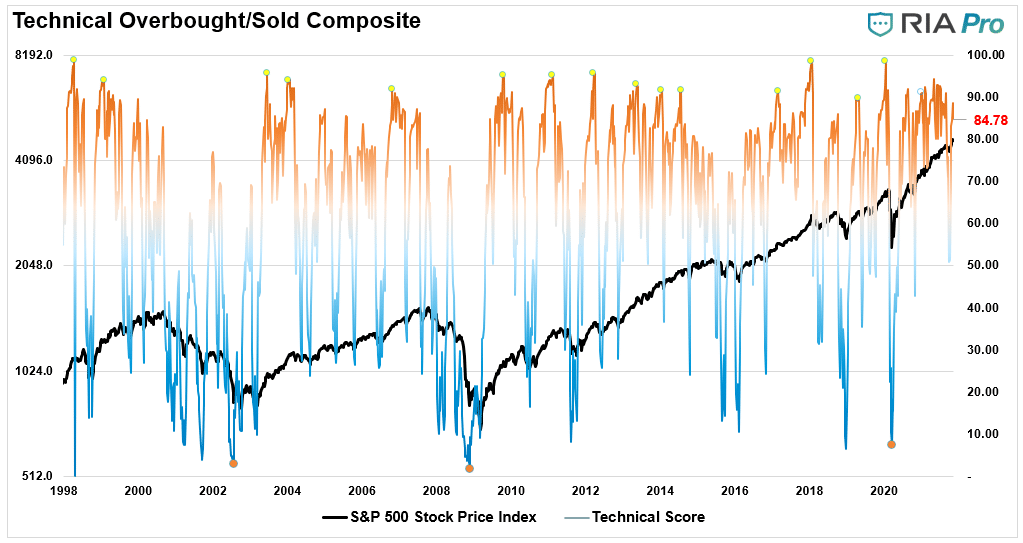

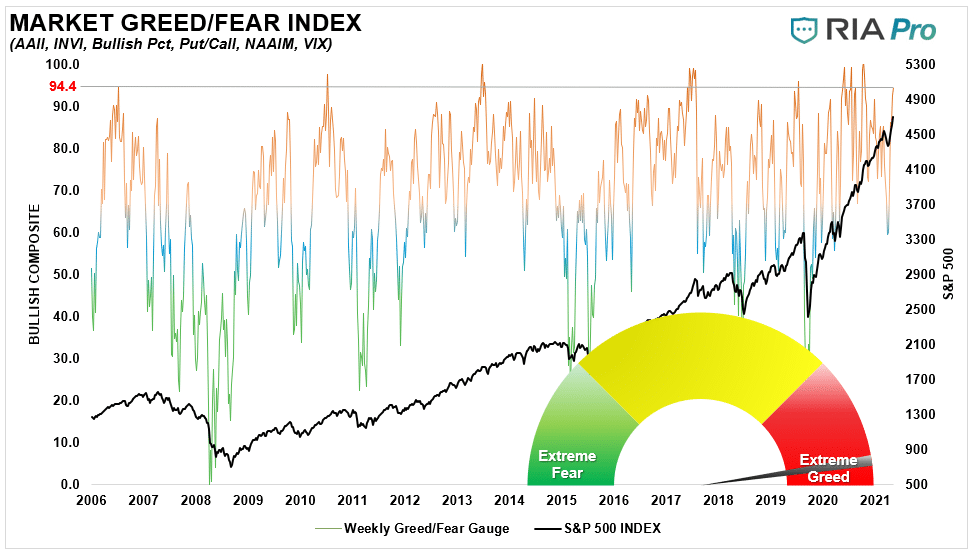

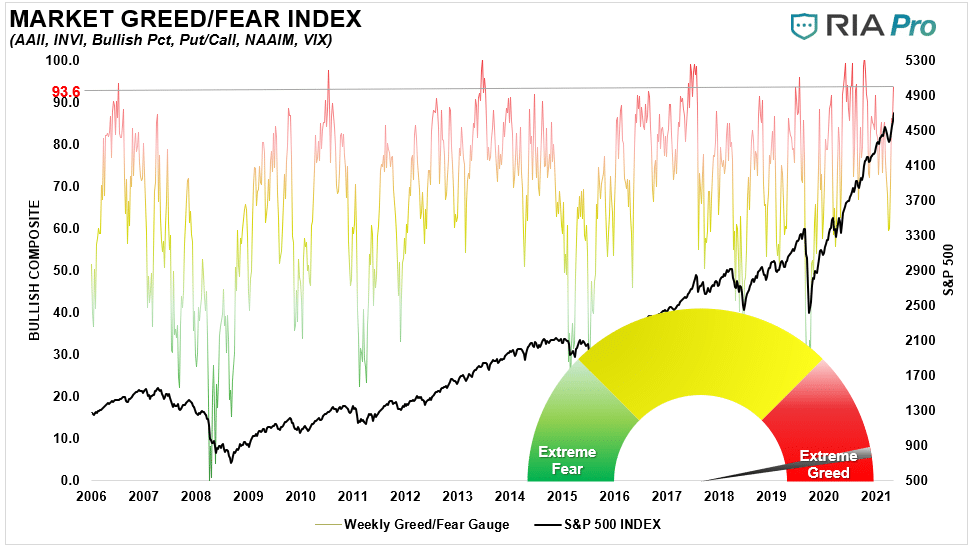

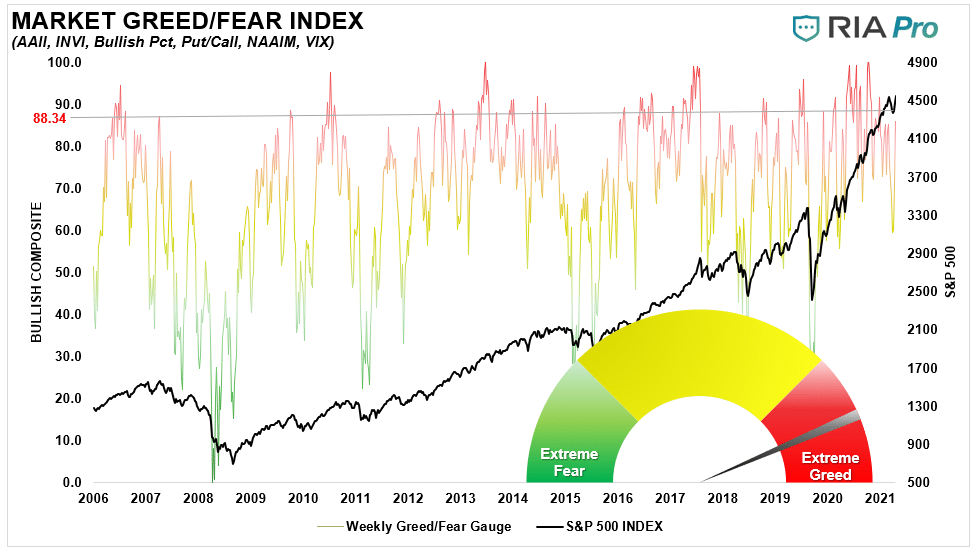

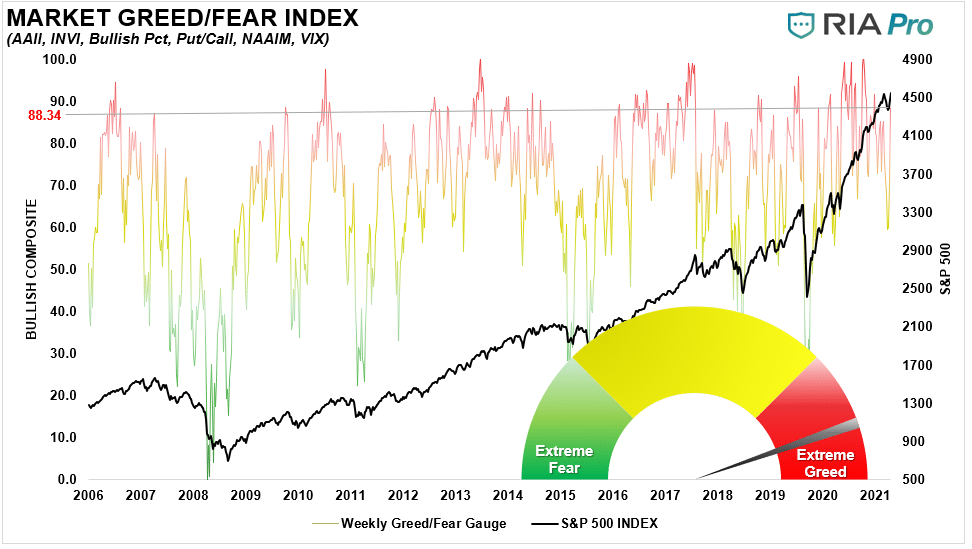

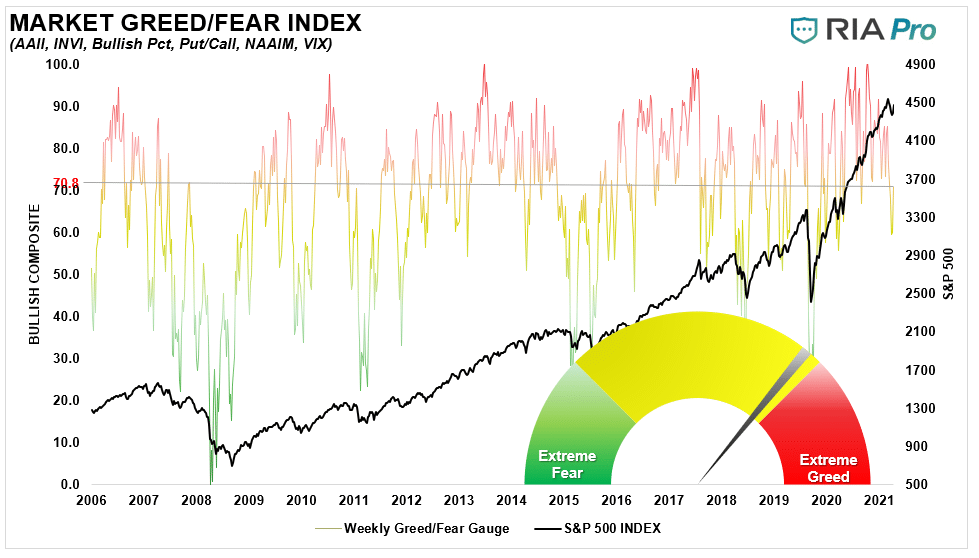

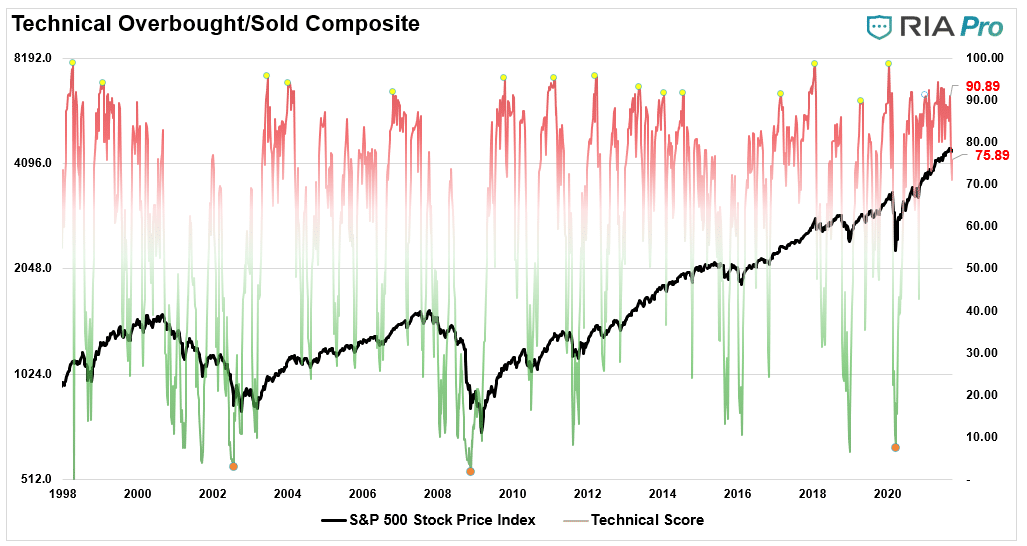

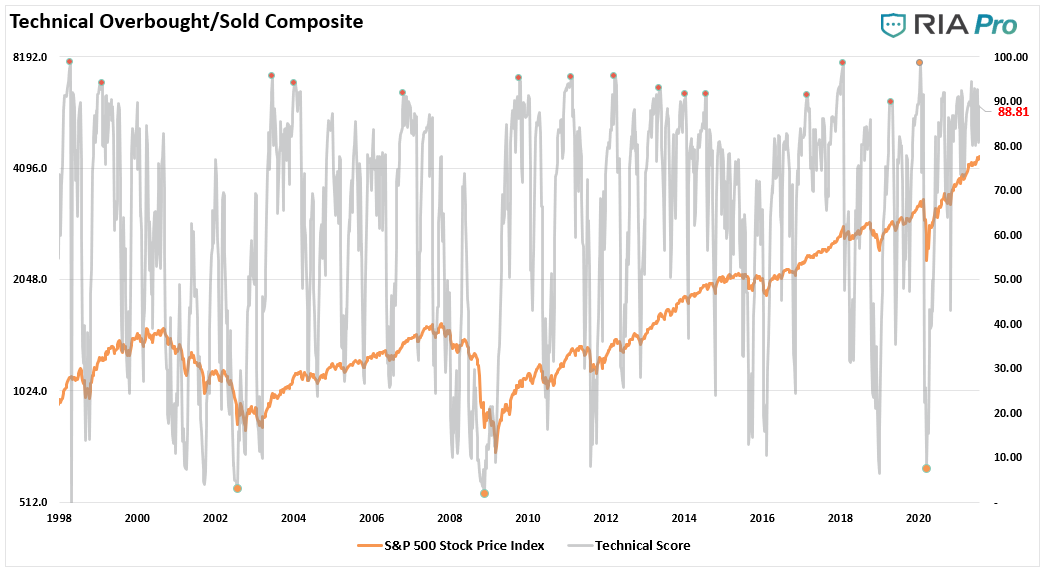

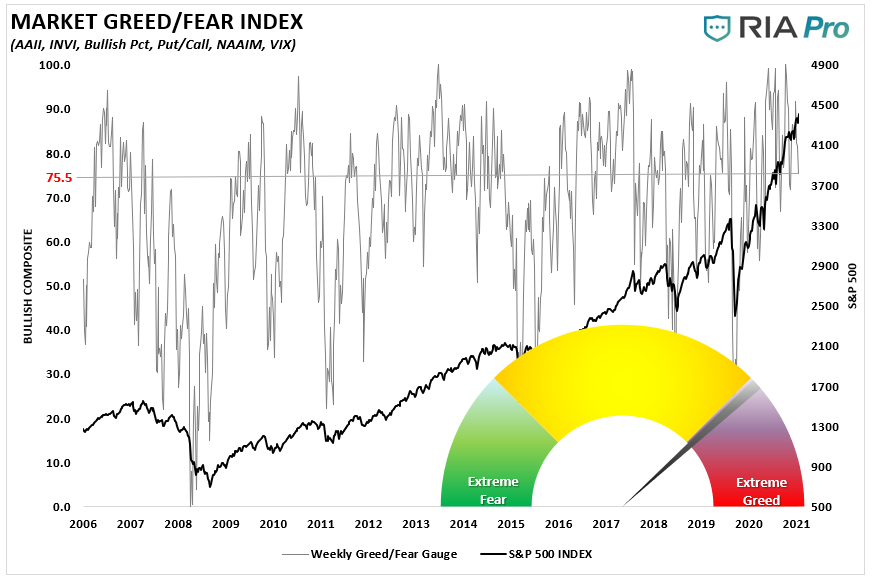

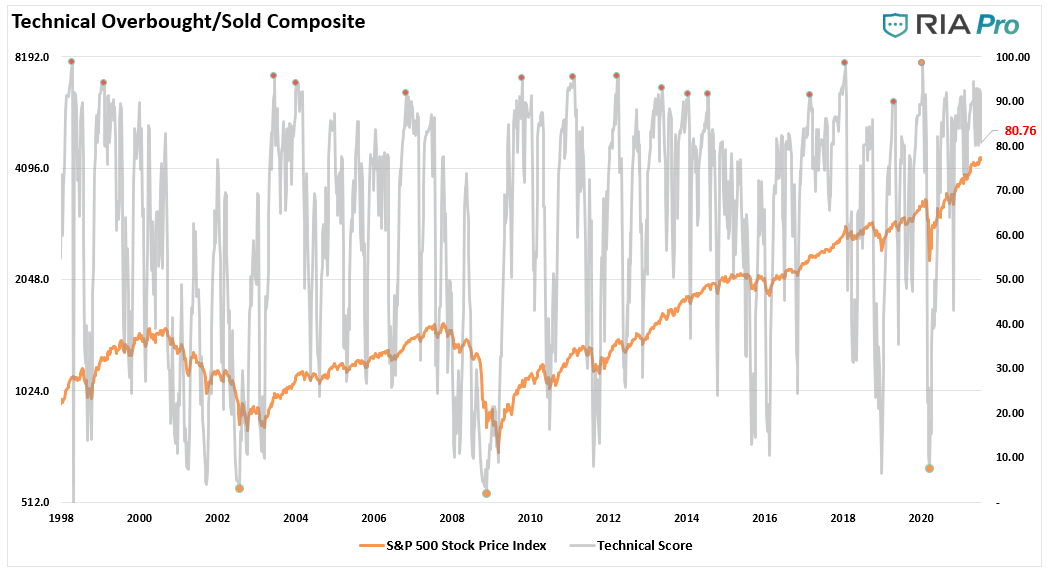

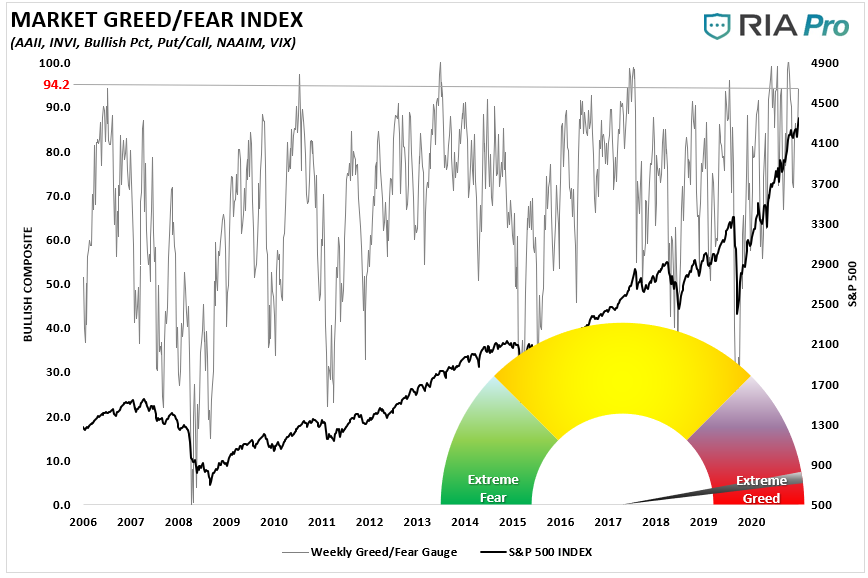

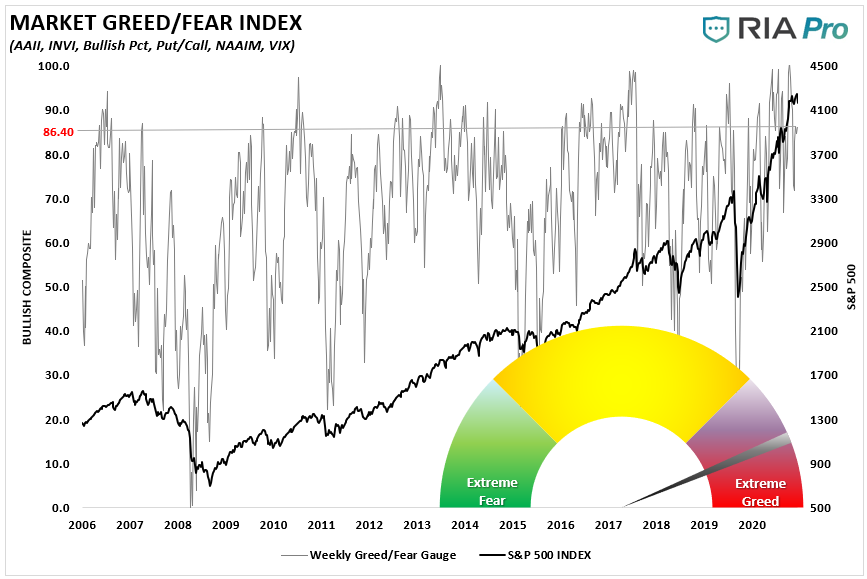

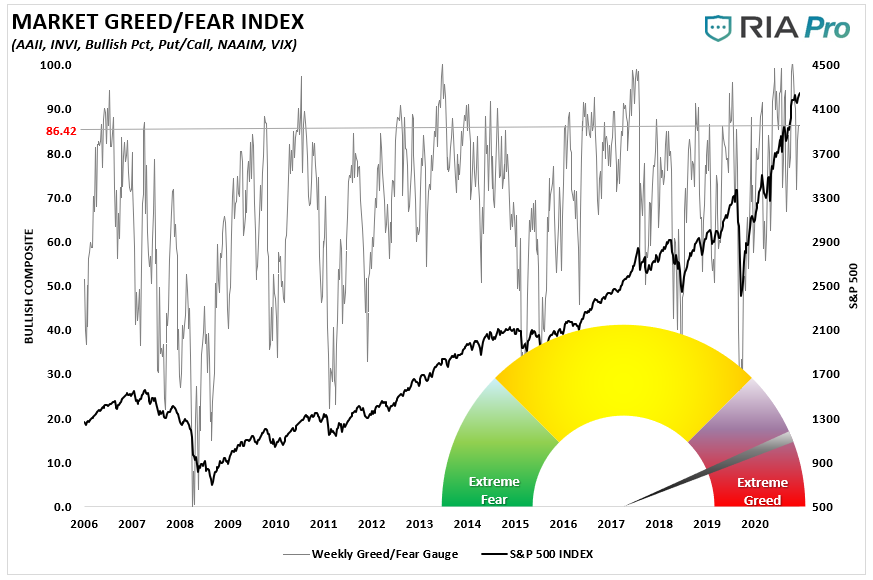

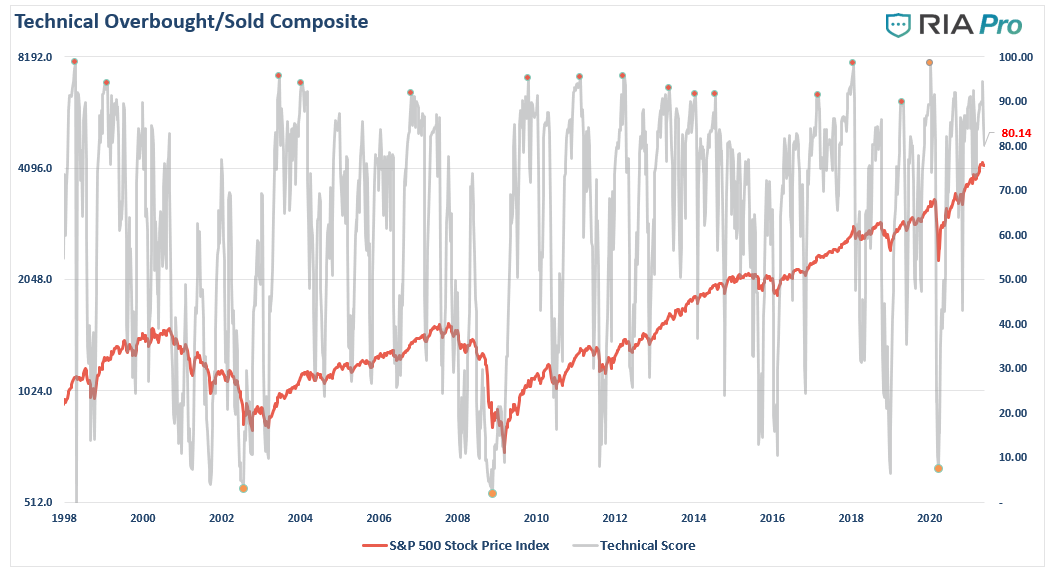

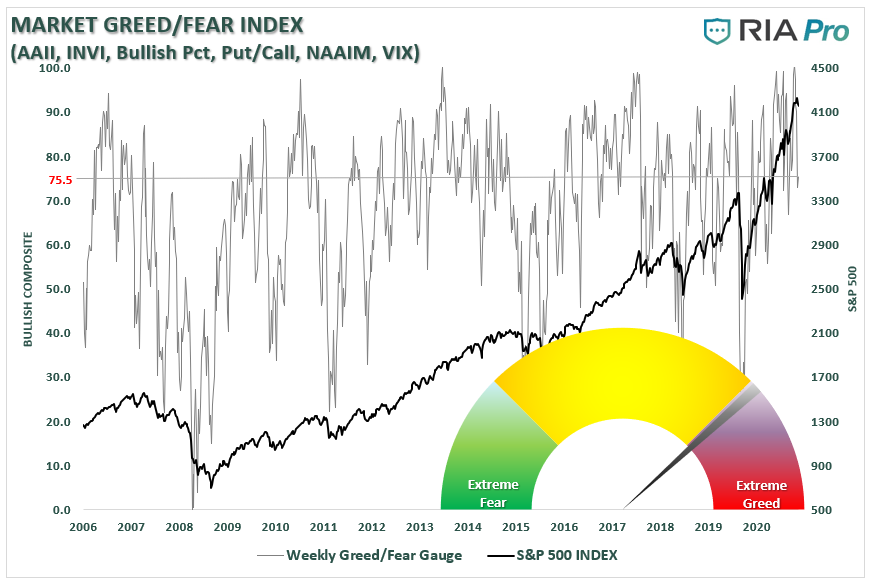

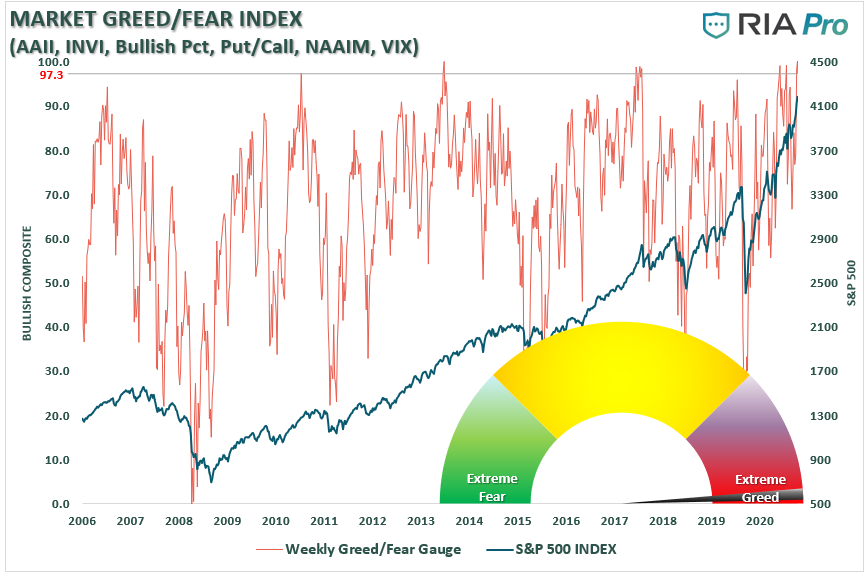

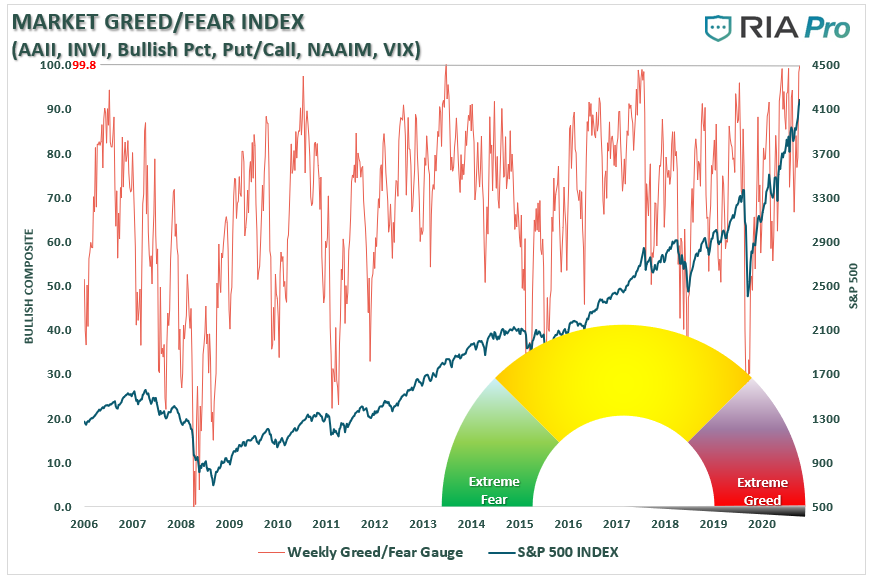

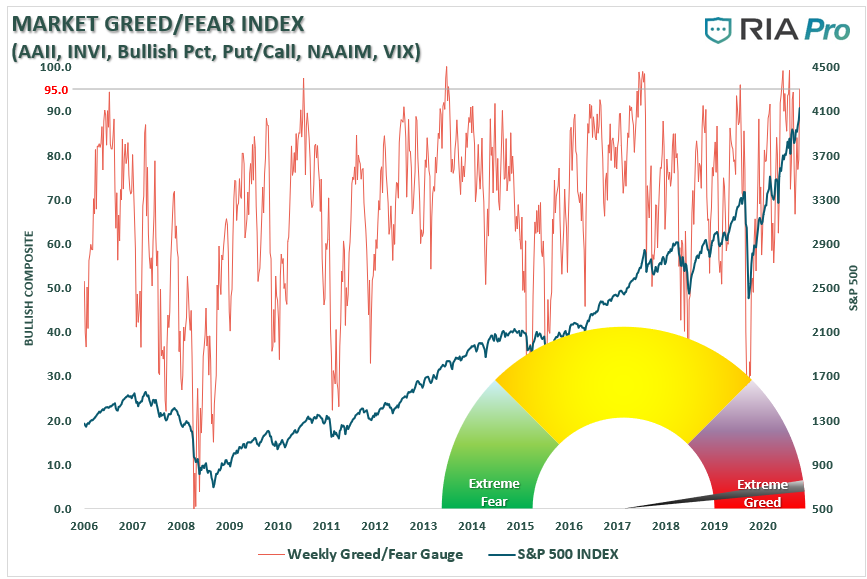

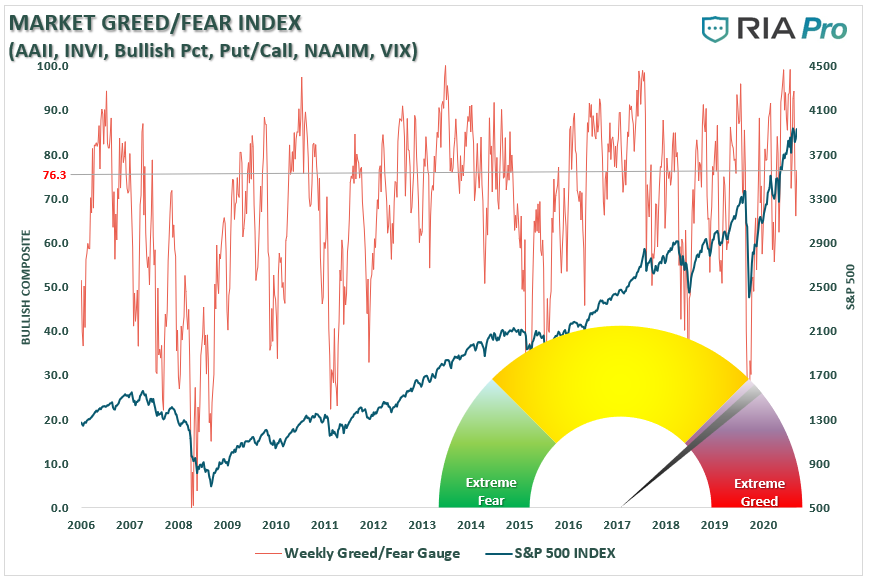

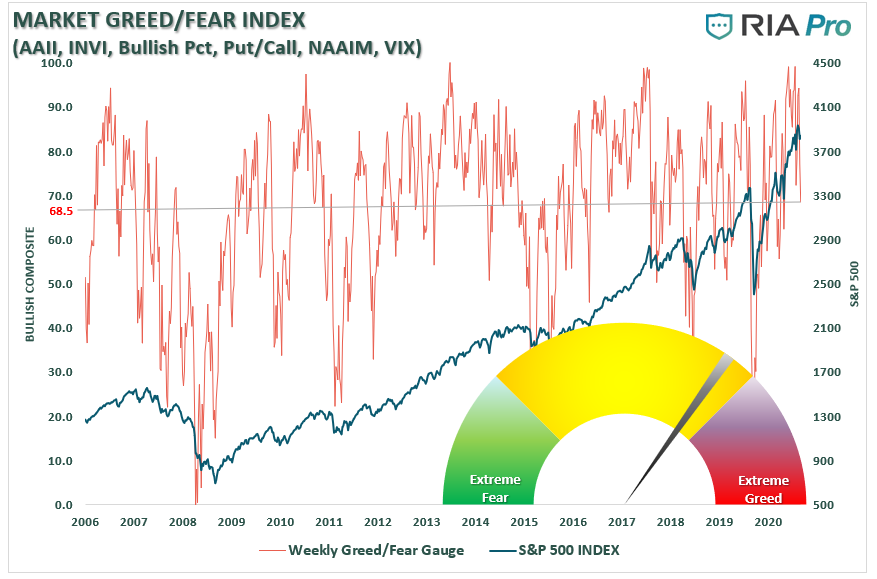

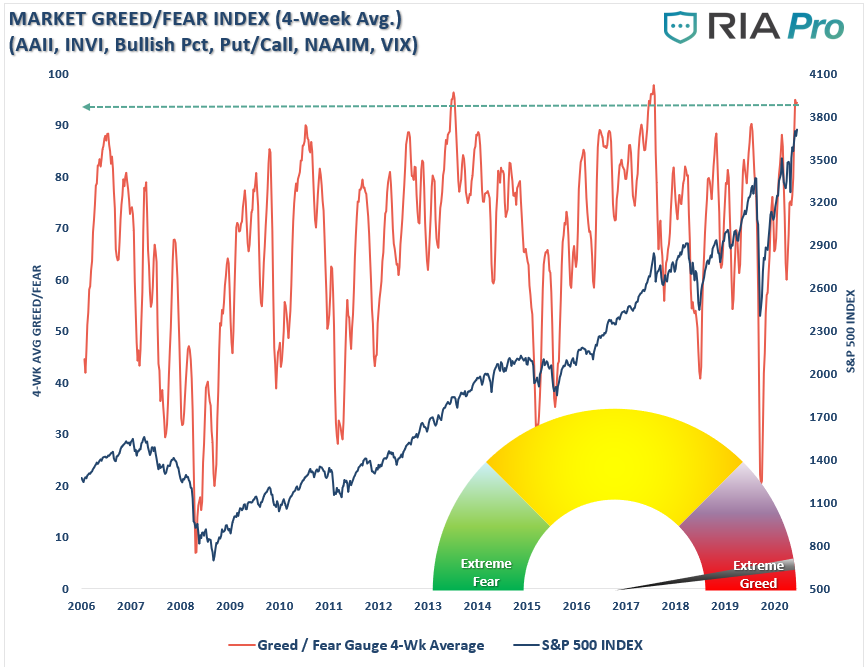

Fear / Greed Model Rising But Not Yet Back To Greed

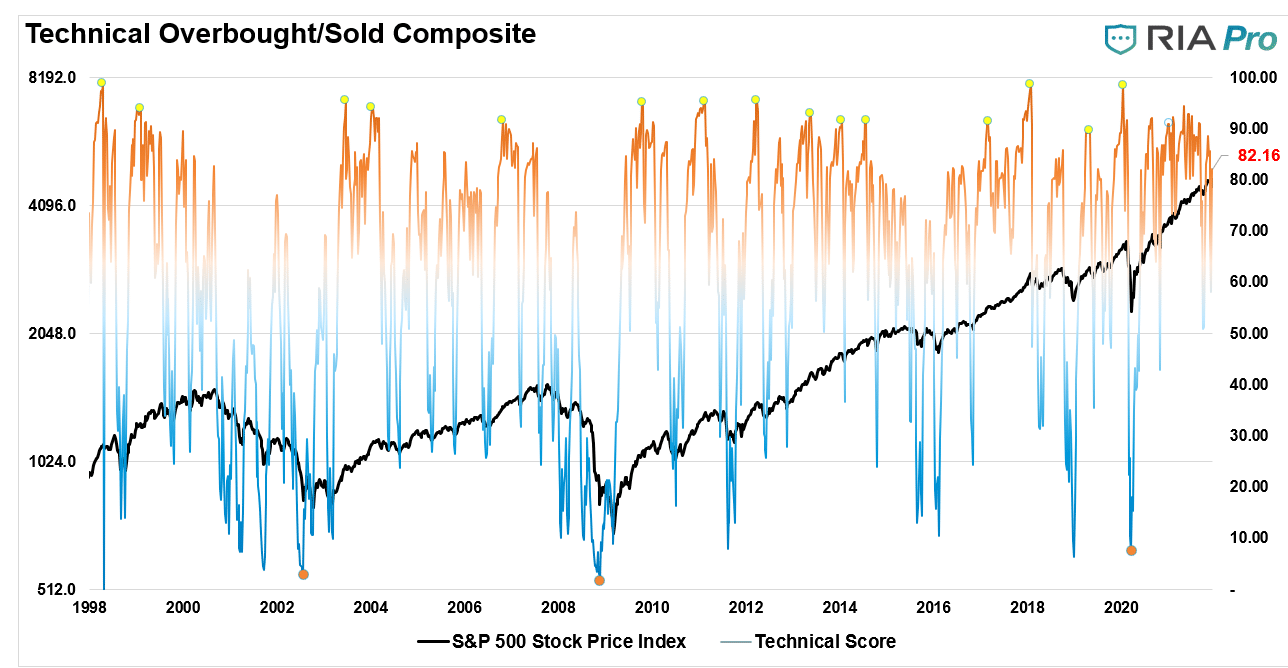

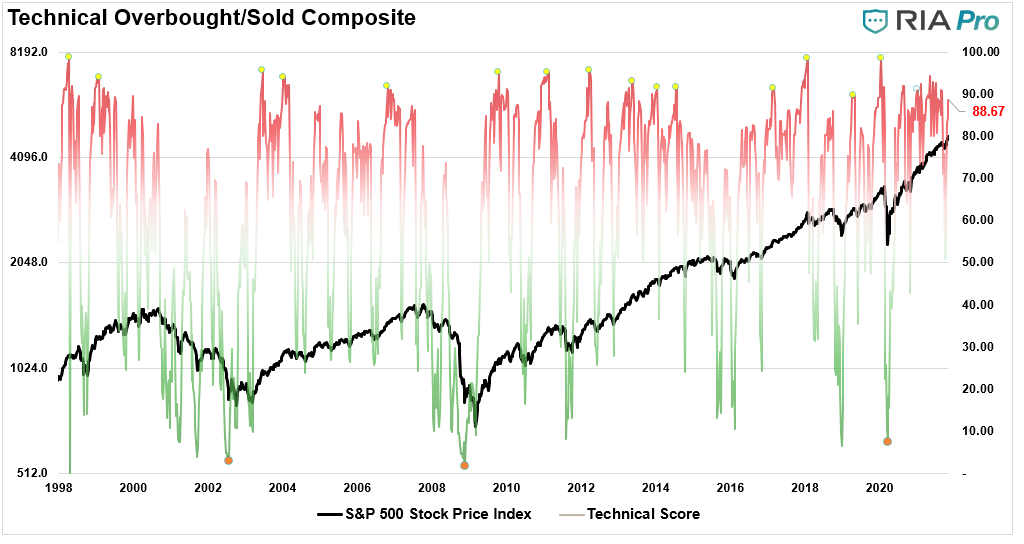

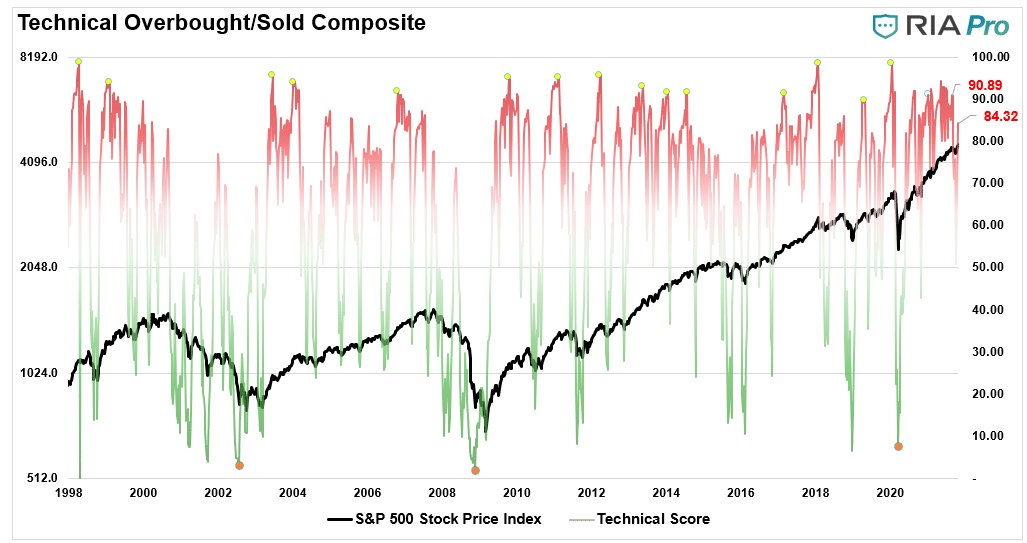

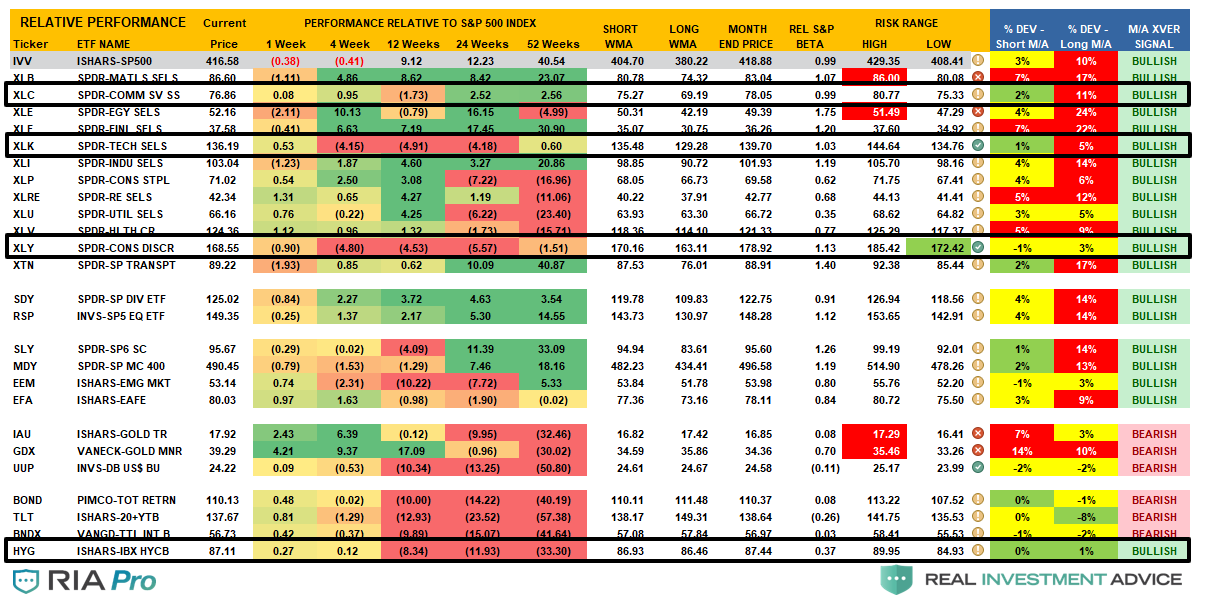

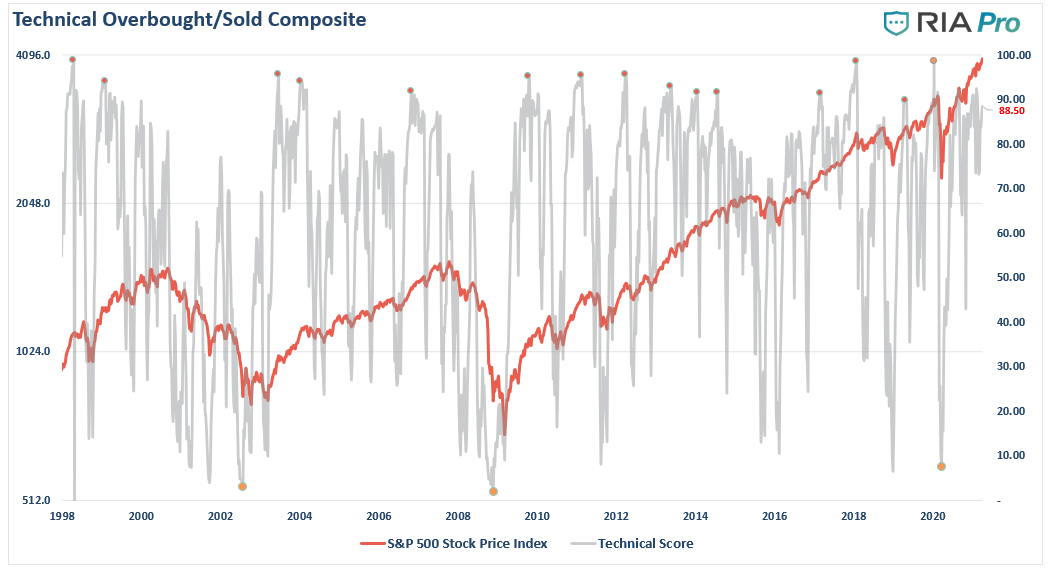

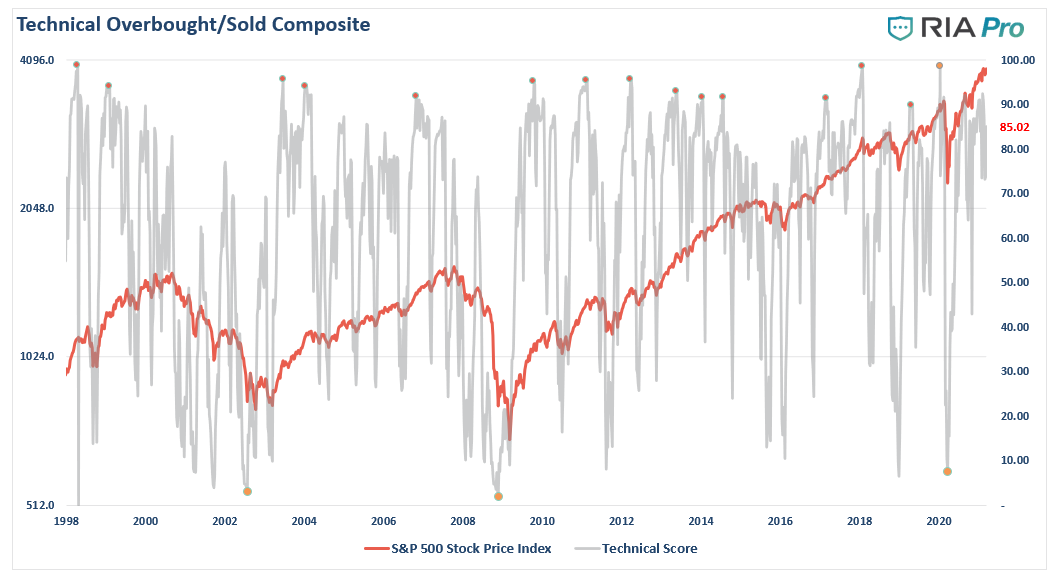

Risk / Reward Ranges Show Market Back To Short-Term Overbought

October 14, 2021

*** Portfolio Trade Alert *** Equity & ETF Models

As we kick off earnings season in earnest we are increasing our technology exposure where we have been underweight previously. In the equity model, we are adding 1% to our current holdings of ADBE and initiating a 2% position in AMD due to its breakout above its recent downtrend.

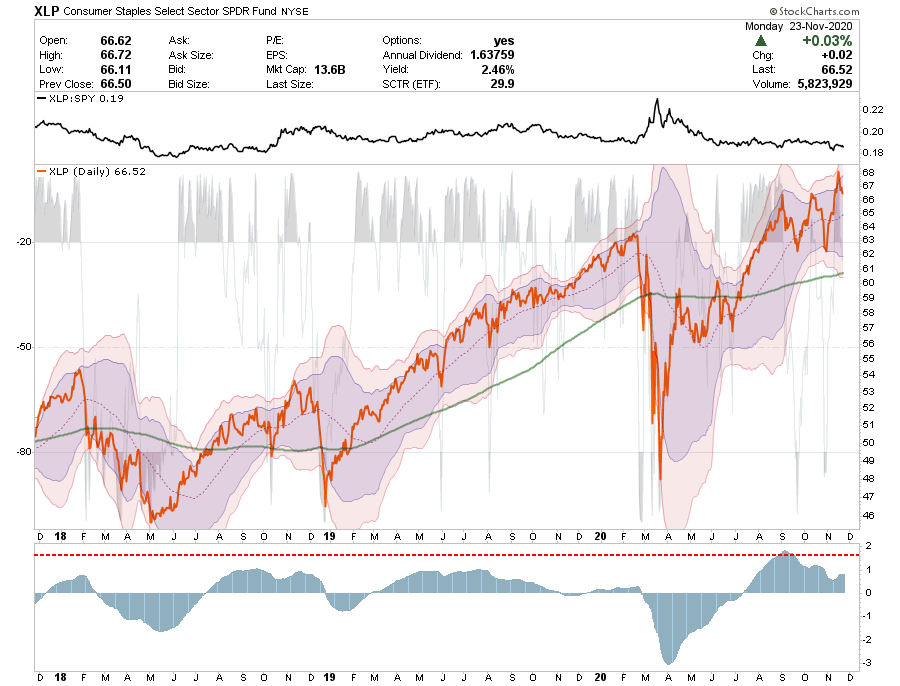

We added 1% of XLP to the sector model. It is turning up on a buy signal from a very oversold condition. The inflationary impulse is likely to fade or at least take a break, arguing for sectors like staples, technology, and healthcare should begin to perform better.

ETF Model

Add 1% of the portfolio to XLP increasing weight to 5% of the portfolio.

October 7, 2021

*** Portfolio Trade Alert *** Equity Model Only

This morning we added 1% to COST and PG. We also bought a new 1% position in WM. All three have nice technical setups. COST and PG are staples and we were underweight staples in the equity model. WM allows us to increase exposure to industrials without taking on China’s risk, as many industrials have.

Equity Model

Add 1% to COST bringing the total weight to 2.5% of the portfolio.

Adding 1% to PG bringing the total weight to 2% of the portfolio.

Initiating a 1% position in WM.

October 6, 2021

*** Portfolio Trade Alert *** Equity & ETF Models

We just reduced our exposure in both portfolios slightly in part because of recent volatility and what we view as a poor risk/reward skew.

In the Equity model, we sold the entire position in UPS. It broke through key technical support and is trading poorly. FDX recently had poor earnings and UPS will likely follow suit when they report on October 26th. We also sold the entire stake of IYT in the ETF model as well.

We also cut JNJ to 1.5% from 2.5%. It has also broken through key technical support, but we like the fundamental story longer-term. We will look for an opportunity to add back into the position once it strengthens technically.

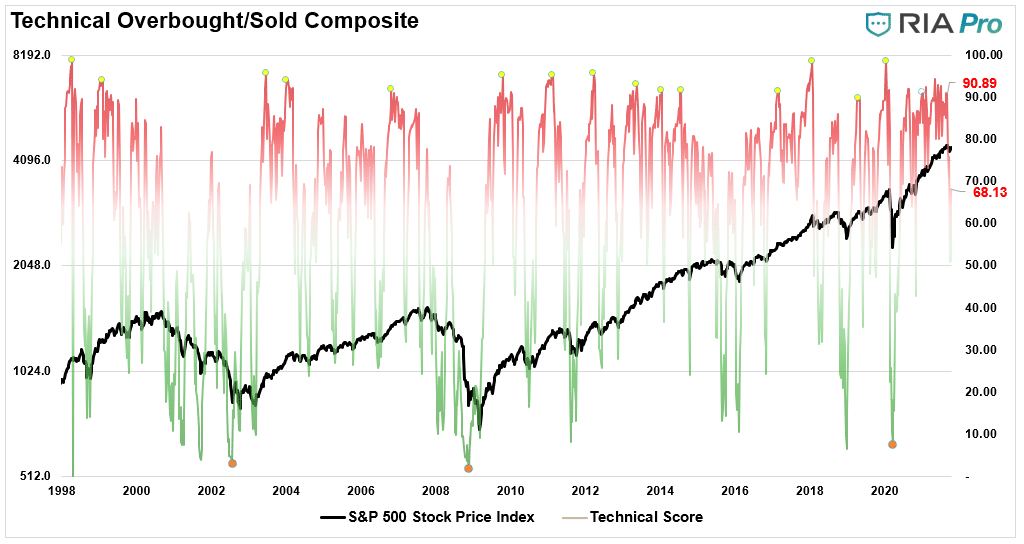

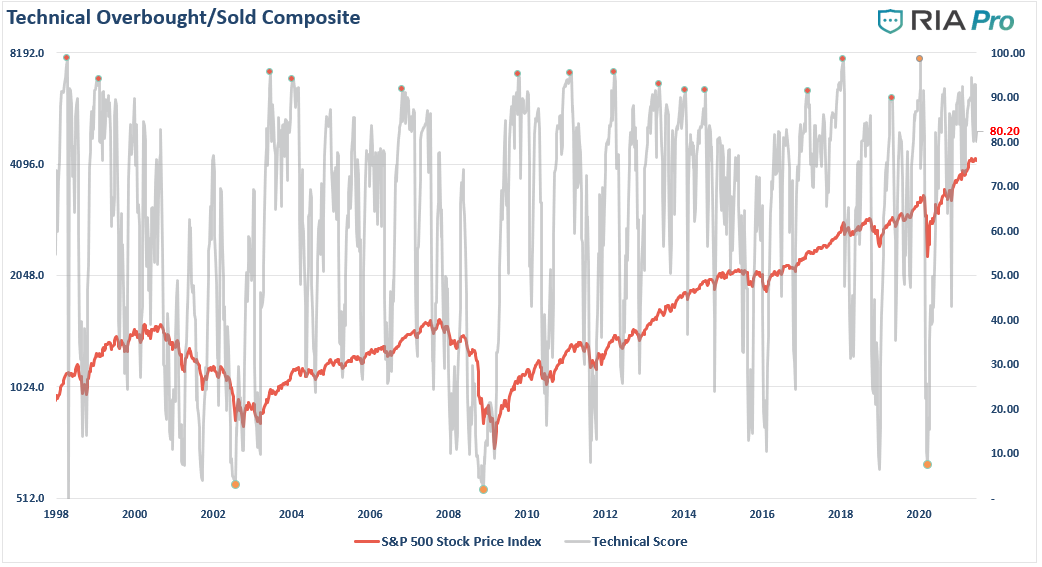

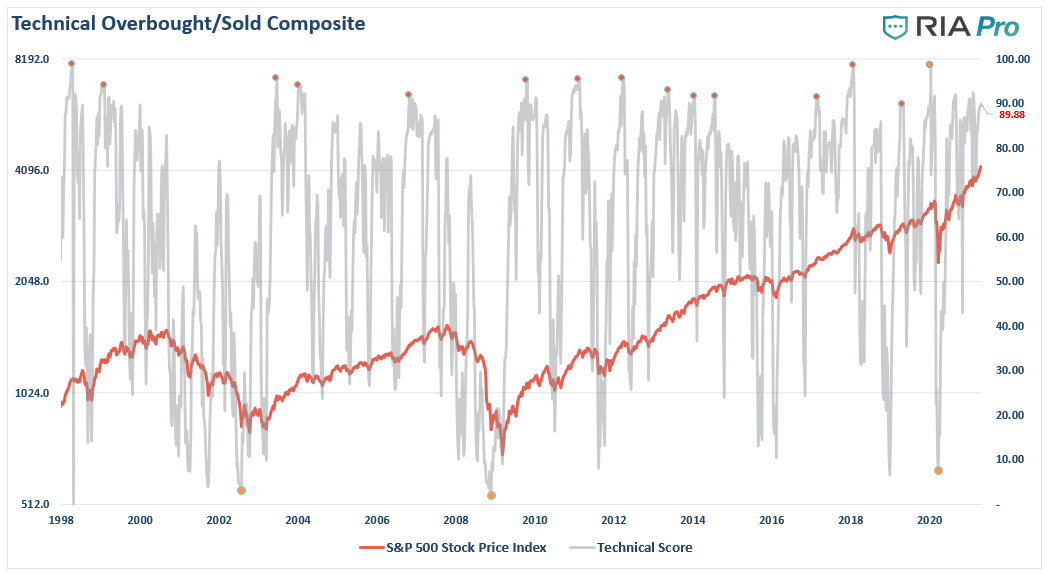

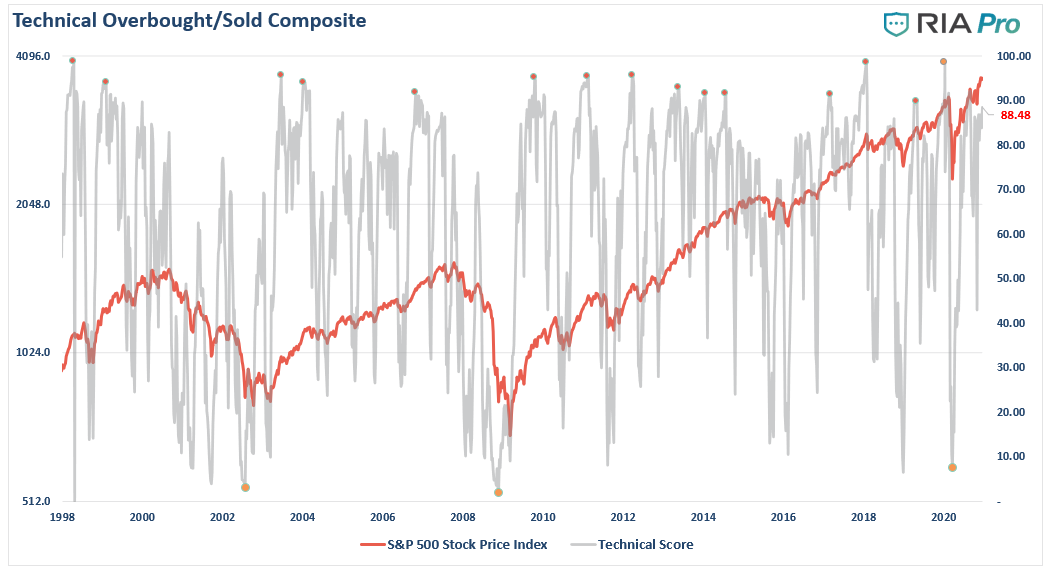

Technical Gauge Drops Into “Buy Territory” For A Bull Trend

Allocation Model Also Moves Into “Buy Zone” For A Bull Market.

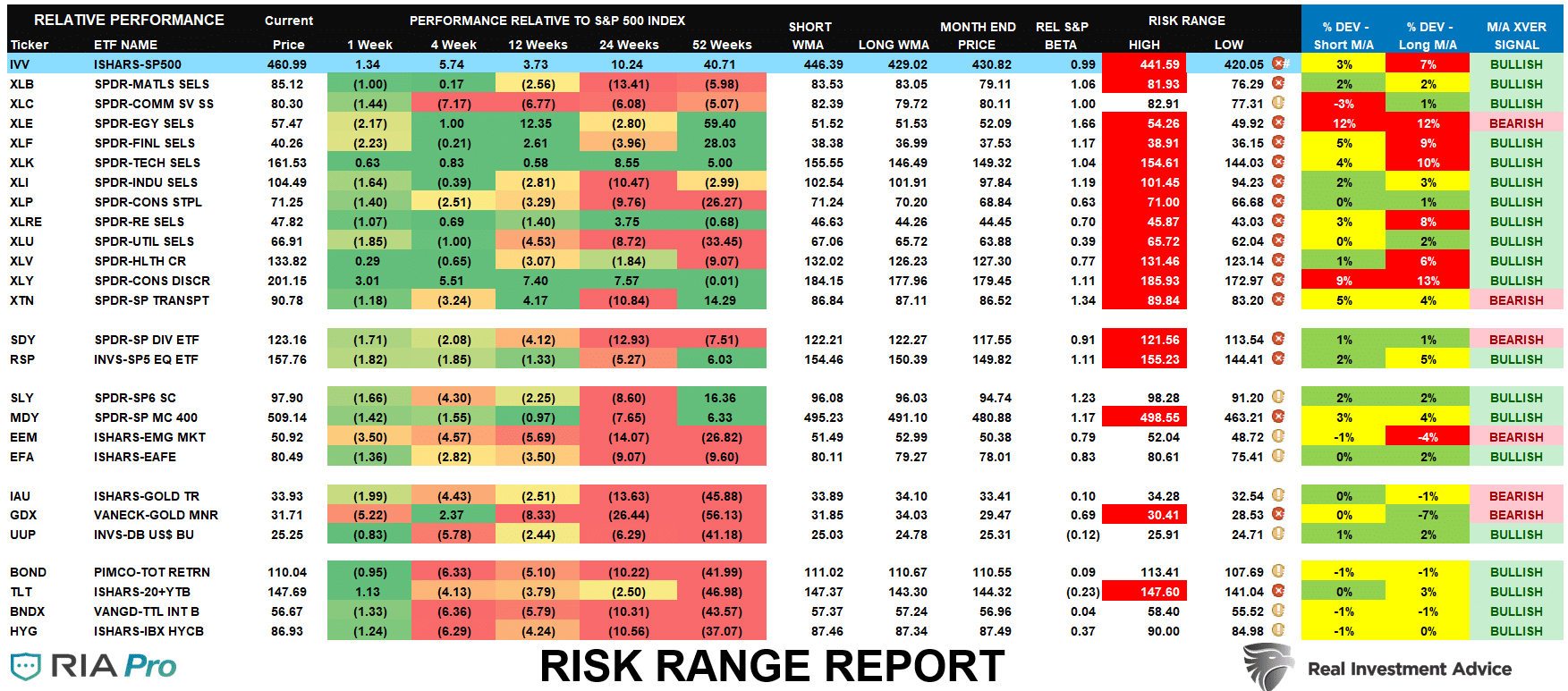

Risk / Reward Ranges Reset For New Month – Most Excesses Reversed

September 29, 2021

*** Portfolio Trading Alert *** Equity and ETF Models

As noted in this morning’s Daily Commentary, the recent spike in interest rates has given us a decent opportunity to add to our longer-duration bond portfolios. We have an article coming out on Friday discussing the history of “debt ceiling” debates and the outcome for bonds. With bonds bouncing off support at the 200-dma and oversold, such has historically provided a decent entry point to add exposure.

Equity & ETF Models

Add 1% to both IEF and TLT respectively.

September 27, 2021

*** Portfolio Trading Alert *** Equity and ETF Models

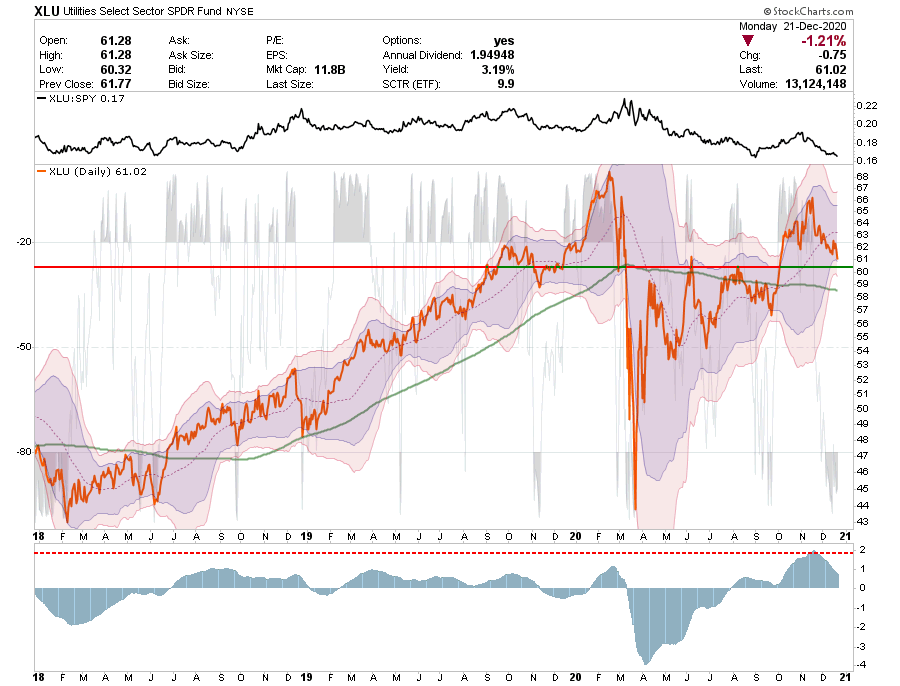

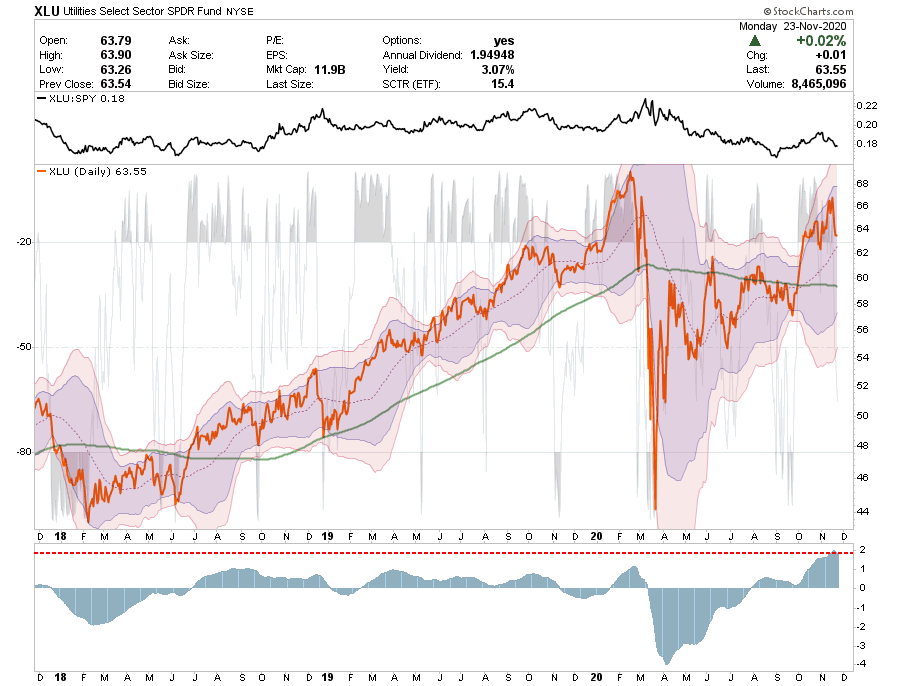

As noted in this morning’s Daily Commentary, with the market triggering its “money-flow” buy signal, we are continuing to increase our exposure in both models. This morning we added a bit more to our Utility exposure which increases our overall portfolio dividend yield and gives us a bit of defensive positioning. We also increased our stakes in energy and financials.

Equity Model

Add 1% to DUK, XOM and JPM bringing total portfolio weight to 2% each.

ETF Model

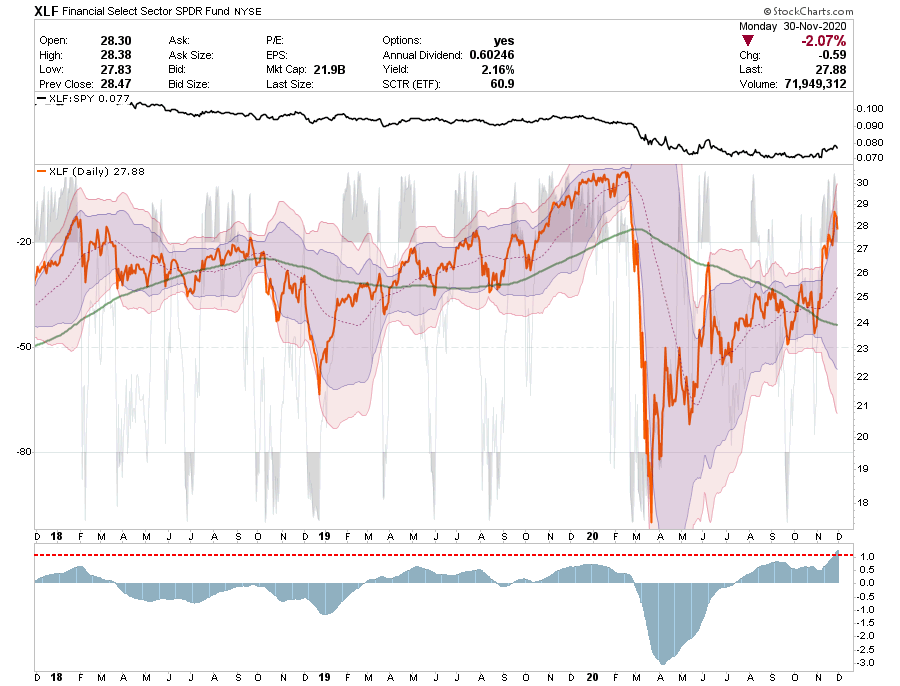

Add 1% to the current holdings of XLE, XLU, and XLF

The Federal Reserve did exactly as expected yesterday and threaded the needle well on putting “taper on the table” and assuring markets the “punch bowl” wasn’t being taken away just yet.

“There has been a great deal of handwringing by some market participants over the potential market implications of the Fed’s eventual tapering of asset purchases, and a great deal of ink spilled on the topic too. But at the risk of merely contributing to the latter, we hope to assuage those who worry about the former.

In sum, we think that the tapering of Fed asset purchases (likely a $10 billion reduction in U.S. Treasury purchases and a $5 billion reduction in agency mortgages per month) is likely to have minimal market impact at this stage. This is partly because the Fed has done a decent job of telegraphing when tapering is likely to begin (most market participants believe the announcement will come this year), but more importantly it’s because the asset purchase reductions are likely to be trivial when seen in the context of how large the fixed income markets are today, and how overwhelming the demand for income has become.” – Rick Rieder, BlackRock’s CIO of Global Fixed Income

With stocks deeply oversold on a short-term basis, as noted yesterday, and the threat of “taper” largely baked into the recent decline, there is a decent entry point for traders to add exposure near term. As noted, the 50-dma is the only real challenge ahead but will likely be resolved today.

Equity Model:

Add 1% to GS and MSFT bring exposure to 2% each.

Add 1% to GOOG bring model exposure to 3%. (It is 4% in equity portfolio due to price of shares.)

ETF Model

Add 1% to XLF bringing exposure to 3%

Add 2% to XLK bringing exposure to 10.5%.

September 21, 2021

After finally getting a bit of a sell-off to work off the overbought condition, we are beginning to look for opportunities to increase equity exposures in portfolios as we head into year-end.

As Sentiment Trader noted today:

“The broad market is in an environment known as ‘No Man’s Land.’ That means we have a few oversold short-term indicators with several intermediate to long-term indicators that are deteriorating but above a level that creates a fat pitch situation.

Remember the following:

“The markets do whatever they have to do to frustrate the most people.”

There are many more reasons to be bullish than bearish at the moment.

Global liquidity flows remain extremely strong.

October through November are historically strong especially when markets are up 15% or more in the first half of the year.

Interest rates remain low, and even if the Fed does announce taper, it will be minimal by year-end.

Volatility has spiked up recently providing the bulls some fresh “fuel”

Sentiment is negative and AAII sentiment is bearish.

With this backdrop we are beginning to add exposure to portfolios starting with defensive positioning first, to hedge against short-term volatility, and then we will move into more momentum names as markets improve.

Risk / Reward Ranges (Reset For Beginning Of Month)

Technical Gauge Pushing Higher

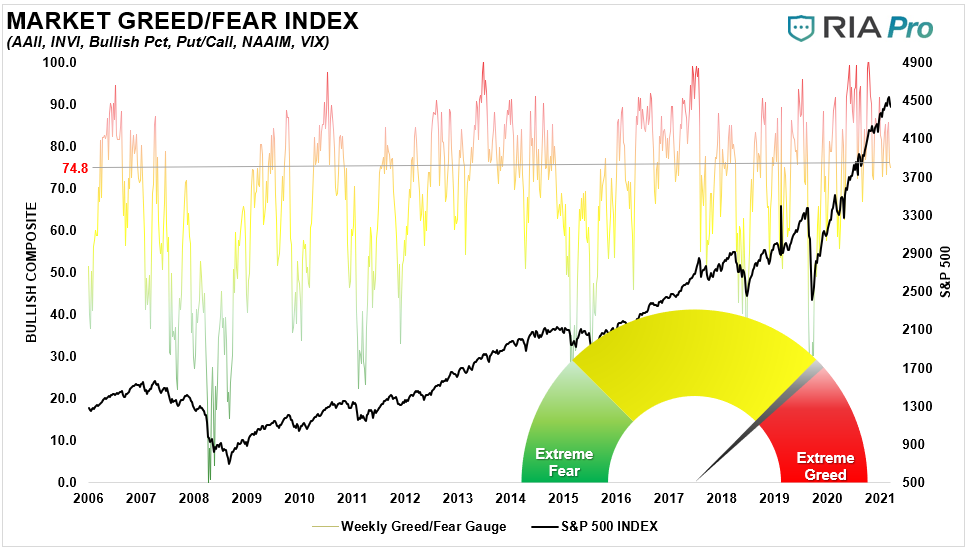

Fear / Greed Index Rising

September 2, 2021

*** Portfolio Trade Update *** Equity & ETF Model

We added 1% to TLT bringing it to 7% in both models. Technically it looks ready to break higher and has good support directly below with the 50/200 dma’s.

We added 1% ABBV to the equity model. The sharp decline yesterday seems overdone and provides us an opportunity to add.

In the equity model, we took profits on WOOF, selling the entire position. We may revisit it in the future as we like its fundamentals but currently, price action remains very weak.

We also sold our 1% of FANG and replaced it with 1% of XOM. We did this to reduce volatility and align the beta of our energy holdings with the beta of XLE. FANG was a great buy but much more volatile than the sector and market. Also, XOM carries a 3+% yield which increases our dividend payout for the portfolio.

We remain wary of this market. Internals continue to deteriorate, volume remains weak, and technicals are stretched. Therefore, we continue to keep “tweaking” the portfolio to give us relative but reduce our overall risk exposure as well.

This morning we added 1% TLT and 2.5% IEF to both models. We sold GSY down to 2.5% to make room. Our WAVG duration is now 4.5 versus 5.9 for our benchmark. Such is due to today’s commentary:

“The graph below is 30-year UST yields with its 50 and 200 dma’s. The vertical lines highlight the last five times, 30 year yields have witnessed its 50 dma falling below its 200 dma, also known as a “death cross.” In 3 of the last 4 death cross instances yields fell appreciably and reached record lows. The only time they didn’t was in 2017 (red vertical line). At that time yields consolidated to negate the death cross. As shown, on Monday 30-year yields witnessed a death cross.”

Risk / Reward Ranges Show Overbought In Technology

Technical Gauge Remains Elevated

Allocation Levels Remain Greedy

August 13, 2021

*** Portfolio Trading Alert *** – Equity Model Only

This morning we added 1% of AAPL and 2% WOOF (Petco) to the equity model. AAPL looks strong from a technical perspective despite the overall market showing signs of technical weakness. WOOF is also strong technically and relatively cheap fundamentally. They report earnings next week on August 19th.(Hopefully, it’s not a dog!!)

Equity Model

Add 1% of the portfolio to AAPL increasing position size to 3.5%

Deviations from long-term means are getting extreme again. Suggests a correction in leading sectors likely.

Fear / Greed Allocation Increased

August 5, 2021

*** Portfolio Trading Update *** Equity & ETF Model

This morning we reduced our exposure slightly as our indicators are starting to turn back down. We also think, with the Fed constantly yammering about tapering QE, the market struggle to move much higher limiting upside. It’s also worth reminding you we are now in the weakest 3-months of the year. We are reducing our financial sector exposure slightly as the yield curve continues to flatten which will hurt their profit margins.

Equity Model

Sell 100% AMLP

Reduce JPM and GS by 1% of the portfolio each.

ETF Model

Sell 100% of AMLP

Reduce XLF by 1% of the portfolio

This morning DUK reported GAAP EPS of $0.96, which missed expectations of $1.08. However, adjusted EPS of $1.15 beat expectations of $1.11. Revenue for the second quarter was $5.76B, which fell just short of the consensus of $6.26B. Management confirmed guidance for FY21 adjusted EPS of $5.00-$5.30 and an adjusted EPS growth rate of 5%-7% through 2025. The adjusted EPS guidance, at the midpoint, falls slightly below the consensus of $5.19. Regarding the future of DUK, the CEO Lynn Good commented, “Moving forward, we’re leading the most ambitious clean energy transition in North America while providing safe, reliable and affordable energy solutions to our customers and communities across the Southeast and Midwest, enabled by our scope and scale”. We hold a 1% position in the Equity Model.

ALB reported earnings for the second quarter yesterday after the close. GAAP EPS of $3.62 demolished the consensus estimate of $0.85. Revenue came in at $773.9M, which disappointed in comparison to expectations of $787.7M. Although aggregate sales growth was lackluster, lithium sales increased 13% YoY in connection to increased order volume under long-term agreements. Pointing to a positive outlook for lithium sales, management raised guidance for FY21 adjusted EPS to $3.35-$3.70, bringing the midpoint in line with analyst expectations. Guidance for FY21 sales was set at $3.2B-$3.3B, with the midpoint again measuring in line with estimates. The stock is up roughly 5.5% this morning following the earnings results and upbeat guidance. We hold a 2.5% position in the Equity Model.

August 4, 2021

This morning CVS reported GAAP EPS of $2.10, which smashed expectations of $1.71. Revenue was $72.6B in the second quarter versus the consensus of $70.3B. The earnings beat was driven by a combination of sales growth and QoQ operating margin improvement. In addition to the strong results, management raised guidance for FY21 GAAP EPS to $6.35-$6.45 from $6.24-$6.36 previously. Adjusted EPS guidance was also revised upward to $7.70-$7.80, which tops the current consensus of $7.67. We hold a 3.5% position in the Equity Model.

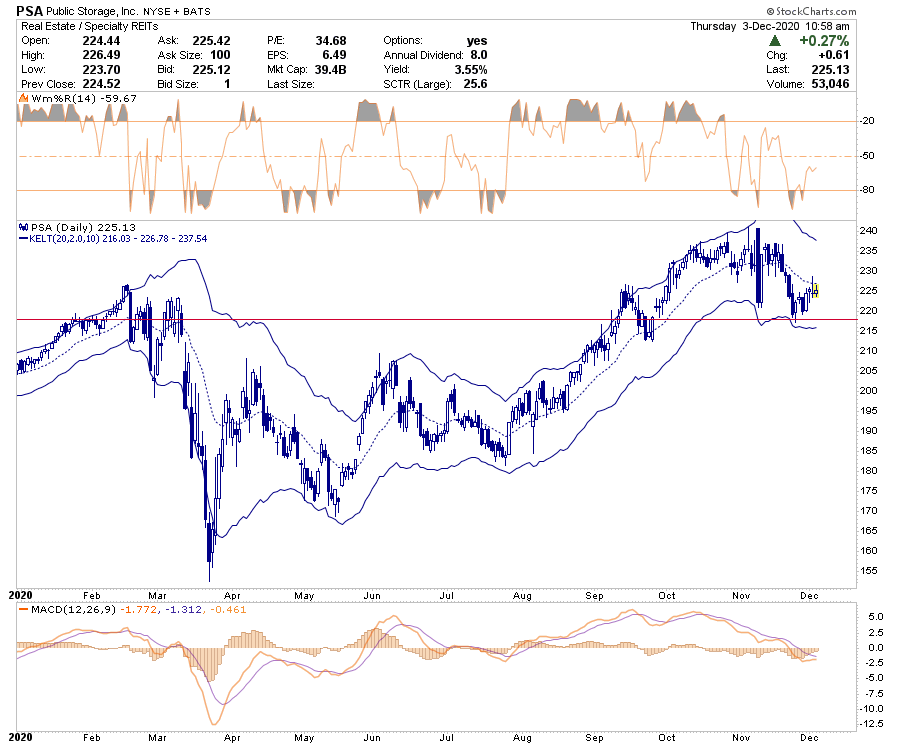

Yesterday after the close, PSA reported core FFO per share for the second quarter of $3.15, which beat the consensus of $2.94. Revenue was $829.3M compared to expectations of $805M. Same store net operating income increased by 20.8% during the quarter, driven an increase of 10.8% in same store revenues and a 15.9% decrease in same store operating costs. Management raised guidance for full-year 2021 core FFO per share to $11.90-$12.30 from $11.35-$11.75 previously, which is about 2% above consensus at the midpoint. Guidance was also raised for FY21 same-store net operating growth to 9.4%-11.9% from 4.8%-7.3% previously. We hold a 1% position in the Equity Model.

August 3, 2021

Yesterday FANG reported GAAP EPS of $1.71, which missed expectations of $2.19. Revenue topped expectations however, coming in at $1.68B versus the consensus of $1.33B. FANG increased its annual dividend by 12.5% to $1.80 per share and continued right sizing its balance sheet by paying down debt during the quarter. Management slightly raised guidance for full-year 2021 production to 363-370 MBOE/d, an increase of 3.2% at the midpoint. Citing an artificial lack of supply in the global oil market, FANG believes maintaining operational discipline is the right strategy moving forward. As CEO Travis Stice put it, “We still believe the best path to long term value creation for stockholders today is achieved through flat oil production, lower costs and return of Free Cash Flow”. We hold a 1% position in the Equity Model.

Technical Guage Remains Elevated Suggesting More Correction Is Possible

Risk / Reward Ranges Show Some Extreme Elevations.

Fear / Greed Allocation Gauge Remains High As Retail Investors Pile In.

PG reported GAAP EPS of $1.13 versus expectations of $1.07. Revenue of $18.96B (+3.9% YoY) beat the consensus of $18.38B. Organic sales growth was 4% while total sales growth was 7% for PG’s FY21. Management guided to FY22 sales growth of 2%-4% YoY, all of which is expected to be organic. Management guided to FY22 GAAP EPS growth of 6%-9%, while core EPS growth is expected to be 3%-6%.

The market is showing a positive reaction to the earnings release and detailed FY22 guidance. The stock is up roughly 3% this morning. We hold a 1% position in the Equity Model.

ABBV reported GAAP EPS of $0.42, far short of expectations of $1.65 for the second quarter. With such a large miss on a GAAP basis it’s worth noting that adjusted EPS of $3.11 beat the estimate of $3.03. Revenue of $13.96B beat expectations of $13.64B. Management lowered FY21 guidance for GAAP EPS by 17% at the midpoint to a range of $6.04-$6.14. However, management raised FY21 guidance for adjusted EPS to a range of $12.52-$12.62. The midpoint is essential inline with the consensus of $12.58. ABBV is down roughly 1.5% this morning following the less than desirable results and guidance. We hold a 3% position in the Equity Model.

July 29, 2021

AMZN reported GAAP EPS of $15.12, easily topping the consensus of $12.32. Revenue missed estimates however, coming in at $113.1B compared to expectations of $115.1B. Operating income similarly disappointed at $7.7B vs. expectations of $7.8B. AMZN expects net sales in Q3 between $106-112B, roughly 8% below the current consensus. Management guided to Q3 operating income between $2.5B-$6B, in contrast with the $6.2B seen in Q3 of 2020. The stock is down 5% in after-hours trading following the disappointing results and guidance. We hold a 3% position in the Equity Model.

We are continuing to increase the duration of our bond portfolio in increments when we get pullbacks to support on 10-year Treasury Rates. This morning we added 1.5% to our position in TLT in both models, bringing it to 5%. We reduced our position in SHY to 7.5% to make room for the additional exposure in the fixed income sleeve.

We also initiated a 2% position in NVDA in the Equity Model. Both models are now around 50% equity exposure.

Equity Model

Initiate at 2% position in NVDA

Add 1.5% of the portfolio into TLT

ETF Model

Add 1.5% of the portfolio into TLT

July 28, 2021

F reported GAAP EPS of $0.14, which smashed expectations of $0.09. Automotive revenue also surprised to the upside at $24.1B versus the consensus of $22.8B. The strong results come after F previously commented on the likelihood of the global chip shortage impacting production during the quarter. F took advantage of strong demand by decreasing incentives and prioritizing a favorable mix of vehicles, which ultimately helped the company beat expectations. Management boosted its FY21 guidance for adjusted operating earnings by roughly $3.5B to the range of $9B-$10B. We hold a 3% position in the Equity Model.

*** Portfolio Trading Alert *** – AeonViZion

After an upbeat earnings report from Alphabet, GOOG was added to the AeonViZion to comprise 27.7% of the model. GOOG continues to create sustained growth in cloud space with a revenue of 4.6 billion, an increase of 54.4% year-over-year. In addition, Alphabet continued to dominate the digital ad space and racked up $50.4 billion in revenue, an increase of 69% year-over-year.

AeonViZion Model

Initiate at 27.7% position in GOOG

July 27, 2021

MSFT reported non-GAAP EPS of $2.17, which beat expectations of $1.92 for the quarter. Similarly, revenue of $46.2B beat expectations of $44.3B. Weaker than expected growth in Azure revenue and a decline in Xbox sales appear to be weighing on the stock despite having beat revenue and earnings estimates. MSFT is trading 2.7% lower in the after-hours session. We hold a 1.5% position in the Equity Model.

V reported GAAP EPS of $1.18 versus the consensus estimate of $1.35. Revenue of $6.1B topped expectations of $5.86B. Payments volume grew 34% versus the year-ago quarter, which was significantly higher than the consensus of 26.2%. We hold a 1% position in the Equity Model.

GOOG reported GAAP EPS of $27.26 compared to expectations of $19.27. Revenue for the second quarter was $61.9B, which smashed expectations of $56.1B. According to the CEO, Sundar Pichai, the strong quarterly revenue was driven by increased online activity from consumers and strength in advertising spend. Assisted by revenue growth, GOOG’s operating margin improved to 31% from 17% in the second quarter of 2021. We hold a 1.5% position in the Equity Model.

AAPL reported GAAP EPS of $1.30, which easily beat expectations of $1.01. This came on the back of revenue of $81.4B versus the consensus of $73.5B. AAPL saw record quarterly revenue in each of its geographic segments and double-digit growth in each product category. iPhone sales surprised the most within the product categories, coming in 14.5% above market expectations. We hold a 2.5% position in the Equity Model.

SBUX reported GAAP EPS of $0.97 versus the consensus of $0.77. Revenue of $7.5B also beat expectations of $7.3B on comparable sales growth of 73%. Management raised its guidance for full year 2021 GAAP EPS to $2.97-$3.02 from the previous range of $2.65-$2.75. SBUX is trading down 3.3% post market despite reporting strong results and lifting guidance. We hold a 1% position in the Equity Model.

UPS reported GAAP EPS of $3.05, which beat the consensus estimate of $2.80. Revenue of $23.4B was slightly above expectations of $23.2B during the quarter. The results are positive, however, management offered guidance for FY21 operating margin of 12.7% which was below market expectations of 14%. UPS is currently trading down roughly 8.5% this morning as a result. We hold a 2% position in the Equity Model.

RTX reported GAAP EPS of $0.69 versus expectations of $0.79 for the second quarter. Revenue came in at $15.9B for the quarter, which beat the consensus of $15.4B. RTX achieved $185M of incremental cost synergies resulting from the 2020 merger. Citing a strong focus on integration execution, management raised its guidance for merger related cost synergies by $200M to $1.5B. Management also raised full-year 2021 guidance for adjusted EPS to $3.85-$4.00, which represents an increase of 9.2% at the midpoint. RTX is trading roughly 3.7% higher this morning after the release. We hold a 1.5% position in the Equity Model.

This morning we added 1% DUK to the equity model bringing the exposure to Utilities to 2%. This action aligns the Equity Model with the ETF Model in terms of Utility exposures.

Buy 1% of the portfolio in DUK

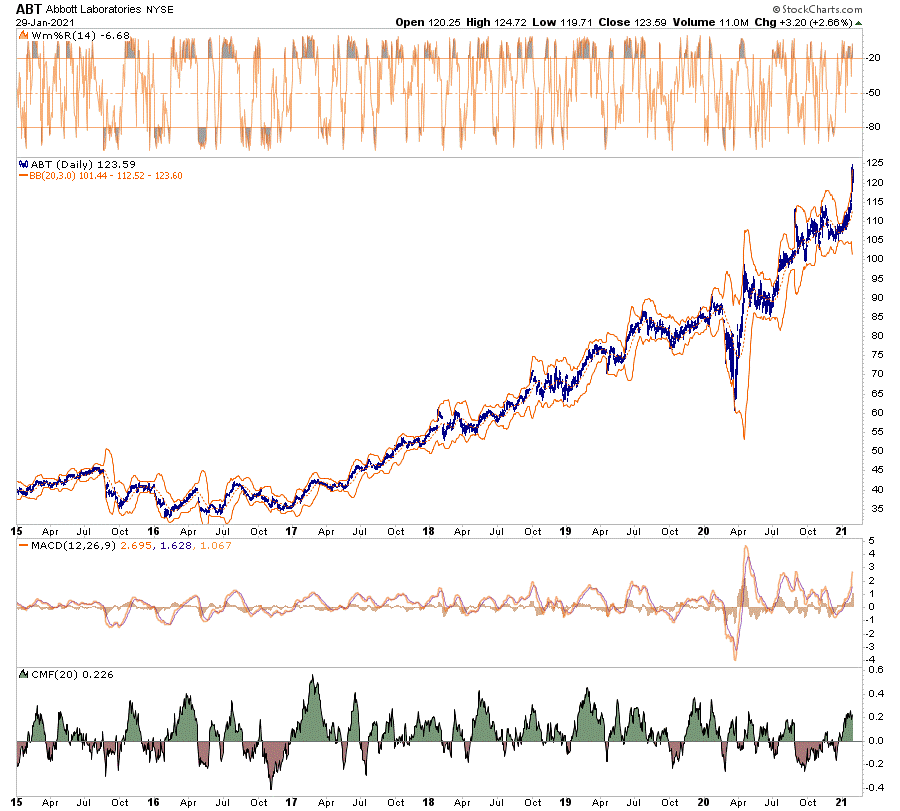

ABT reported Q2 GAAP EPS in line with expectations of $0.66. Quarterly revenue was $10.2B, which beat the consensus of $9.7B. Excluding COVID-19 testing, organic sales grew 11.3% versus the second quarter of 2019. ABT maintained its guidance for full-year 2021 GAAP EPS of $2.75-$2.95. Despite the positive results, the stock is down 2.3% this morning. We hold a 2% position in ABT in the Equity Model.

We are adding to our existing TLT (20-year Treasury Bond) holding today to increase our exposure on this recent pullback in rates. With economic growth likely to have peaked, we feel there is more downside pressure on yields to come by year-end. Given we are very underweight our benchmark in bonds, the minor addition of duration moves us in the right direction.

Equity & ETF Models

Increase TLT from 2.5% of the portfolio to 3.5%.

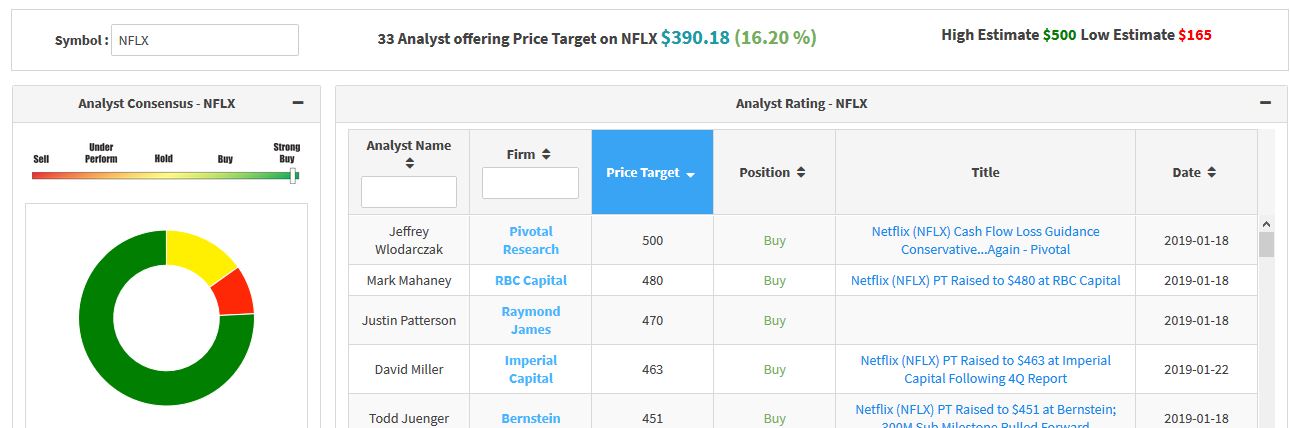

Netflix (NFLX) missed on earnings ($2.97 vs $3.16) last night but beat slightly on revenues. They also reported mixed news on subscriber growth. Paid subscribers increased by 1.54m versus expectations for 1.12m. However, third-quarter expectations for the change in paid subscribers was +3.5m versus expectations for +5.86m. NFLX is trading down a little more than 1% in pre-market trading. We own NFLX in our Equity Model.

This morning we are reducing exposure slightly in portfolios particularly in the Nasdaq-related areas which is extremely overbought relative to the S&P 500 index. As has been the case with our actions as of late, we continue to tweak exposures to reduce overall risk while still maintaining our core positions.

Equity Model

Reduce ADBE by 1% of the portfolio

Sell 1% of AAPL as it has run well ahead of earnings.

Reduce UPS by 1% of the portfolio

Sell down AMLP from 3.5% to 2% of the portfolio.

ETF Model

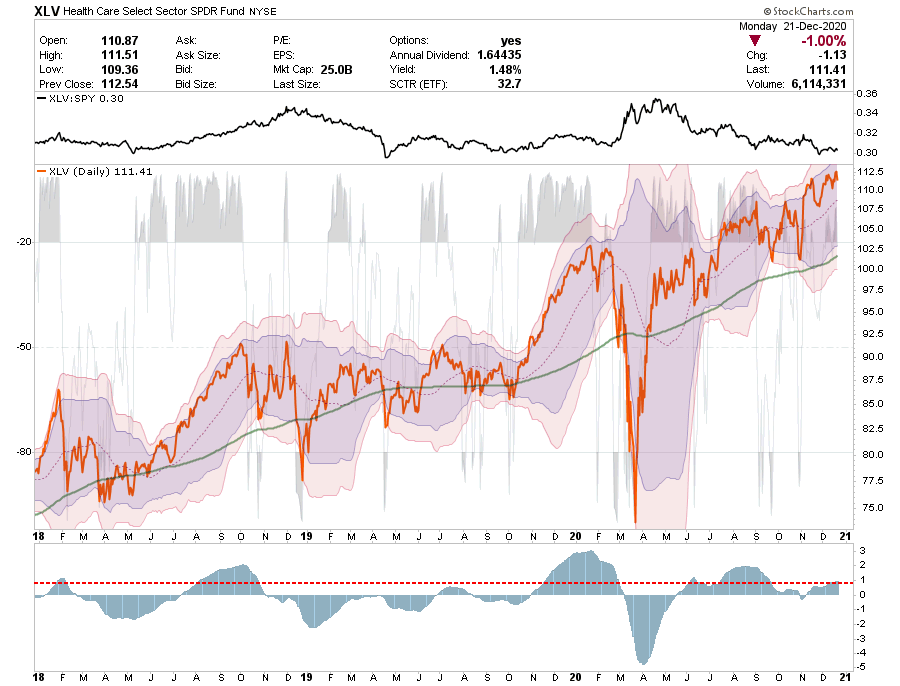

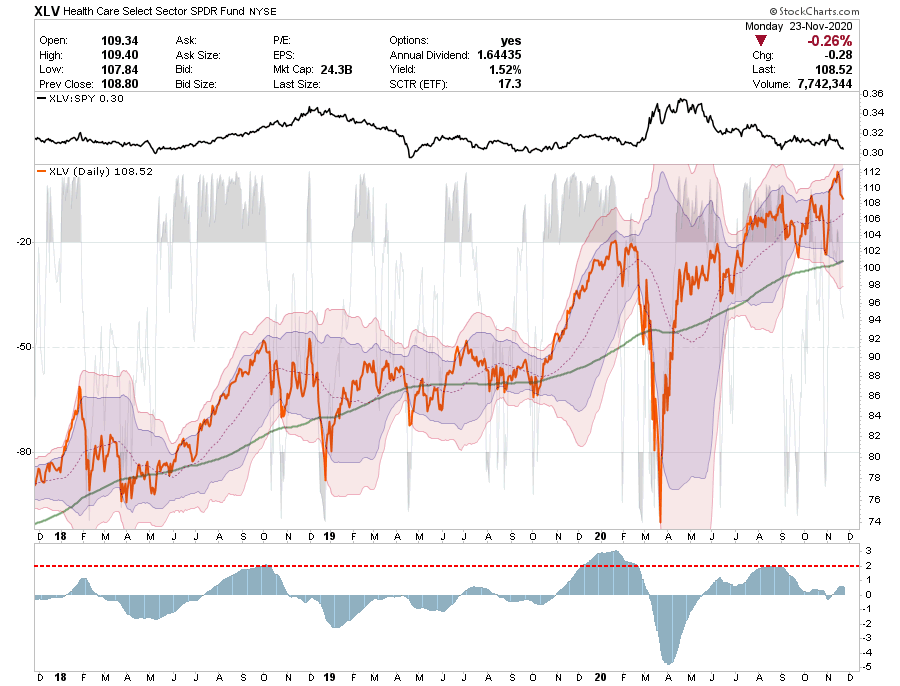

Reduce XLV by 1% of the portfolio.

Reduce XLK by 1% of the portfolio.

*** Portfolio Trading Alert *** – AeonViZion

This morning BABA was added to AeonViZion to compromise 12.8% of the model. Although BABA currently has bearish signs in technicals and negative Chinese sentiment. The market continues to discount the stock and is currently trading at a Forward P/E ratio of 22.82 while the rest of the industry trades on average Forward P/E ratio of 60.16. In addition, the Chinese tech conglomerate posted 64% year-over-year in Q4.

AeonViZion Model

Initiate at 12.8% position in BABA

July 19, 2021

***Portfolio Trading Update *** AeonViZion

NEW MODEL – The AeonViZion model is tailored toward aggressive or young investors willing and able to take on more risk. The model reflects a Gen-Z viewpoint that looks for high growth opportunities with a long-term perspective. Disruptive innovation, emerging sectors, and new technologies are the focal points of the model, while maintaining exposure to established companies.

Risk Reward Ranges – Real Estate and Utilities Very Overbought

Fear Greed Gauge Mostly Unchanged For The Week – Still Elevated

Technical Gauge Declines A Bit As Market Advance Slows

July 13, 2021

JPM and GS both released earnings results for the 2nd quarter this morning. We hold a 2% position in each stock in the Equity Model.

JPM reported GAAP EPS of $3.78, which easily beat expectations of $3.18. These results came on revenue of $30.5B, which topped expectations of $29.7B. The EPS was boosted by $0.75 from a net credit benefit of $2.3B due to the release of loan loss reserves, which accumulated earlier in the pandemic but have since been largely unnecessary. This compares to a net credit benefit of $4.2B in the first quarter of 2021. Finally, JPM reduced its FY21 guidance for Net Interest Income to $52.5B from its previous outlook of $55B.

GS reported GAAP EPS of $15.02 versus expectations of $9.95. Revenue of $15.4B, which beat expectations of $12.2B, was driven by record Asset Management revenue and the 2nd highest quarterly Investment Banking revenue to date for GS. Furthermore, the Investment Banking backlog ended the 2nd quarter at a record level. Prior to the strong results, the Board announced on July 12th that it is increasing the quarterly dividend by 60% to $2.00 per share, payable September 29, 2021.

July 12, 2021

*** Portfolio Trading Alert *** – ETF Model

This morning we took some profits in LIT in the sector model as it is overbought and replaced it with XLB which is oversold. Both trades were for .5%. The trade will slightly reduce net exposure as LIT was overallocated and XLB slightly under-allocated versus the model.

In the equity model, we sold NXPI as it performed poorly versus the tech sector and its weakening from a technical perspective. As we discussed this morning the tech sector is overbought as well.

In the sector model, we reduced XLY and XLV by 1% each to reduce exposure to overweight sectors that are overbought.

Given the plunge in yields, there is something not “quite right” with the market. We are taking our DIA trading position off for now at a very small loss to reduce our overall equity exposure. If the current sell off begins to gain some traction we will take further risk reduction actions.

Equity & ETF Model

Sell 100% of DIA

July 7, 2021

*** Portfolio Trading Alert *** – Dynamic Model (Beta Test Termination)

This morning we are liquidating the entire Dynamic Model portfolio. The portfolio algorithm we have been testing has not been operating to the degree that we are searching for. Some of the performance issues are derived from the current “breadth problem” of the market, the other has been the rather rapid rotations with the internals. The algorithm did not compensate adequately for the current environment.

Therefore, we are liquidating the entire model portfolio and will rebuild and relaunch the model by the end of the summer. If you have been tracking the Dynamic model, switch over to the Equity model for now as holdings are not too dissimilar.

We are reducing ADBE back to its original portfolio weight of 2% after a nice run lately that took the holding back to more extreme overbought conditions.

We are increasing AMLP to 2% of the portfolio in the ETF Sector model on the dip this morning to balance our Energy exposure and increase portfolio yield.

Equity Model

Reduce ADBE to 2% of the portfolio.

ETF Model

Increase AMLP to 2% of the portfolio.

*** Portfolio Trading Alert *** Dynamic Models (Beta Test Model)

This morning we are making a couple of changes to the portfolio model at the open.

We are reducing CVS by 50% due to the technical failure at the 50-dma. We like the position going forward but the failure suggests we could see some lower prices to rebuild the position into.

KNX just has not performed well. We took profits previously at higher prices, but we are going to sell the rest of the position today and remove a laggard from the portfolio.

We are light on industrial exposure so we are adding a 3% position in Raytheon Technologies (RTX) which is about to trigger a fairly oversold money-flow buy signal.

With the Biden Administration potentially passing an infrastructure bill in the next couple of months that will fund 5g expansion, we are adding a 3% weight in VZ. Like RTX, it too is in an oversold position and on support and close to a buy signal with a 4% yield.

Dynamic Models

Initiate a 3% position of the portfolio in VZ and RTX.

This morning we sold 1.5% of XOM and replaced it with 1.5% of AMLP in the equity model. We are picking up extra dividends and the technical backdrop looks better on AMLP than XOM.

We added 7.5% of GSY to both portfolios this morning. The purpose is to sop up extra cash and improve our yield in the fixed income portfolio until we decide to increase our duration.

Equity & ETF Models

Initiate a 7.5% position in GSY

June 28, 2021

*** Portfolio Trading Alert *** All Models

This morning we added a 5% trading position in DIA (Dow ETF) in all models. Our cash flow indicators signal an upward trend and historically the first two weeks of July are good for the markets. Beyond mid-July the market tends to consolidate or dip into the fall months, so we added a trading position now versus adding to individual holdings as it may likely be a short-term position.

In our beta testing model (Dynamic) we are adding some financials given the clearance of the stress test last week, and the recent sell-off.

With the markets holding the 50-dma and firming up a bit, we are increasing equity exposure in areas where money flow “buy signals” are triggering. We were underweight discretionary holdings in the Equity and ETF models so those weights were brought up.

In the Dynamic Model we added the same holdings is in the Equity model but also increased exposure to UPS for the transport sector.

Overall, the money flow “sell” signal for the overall market remains in place with a confirming MACD sell signal. While the market is hitting an all-time high, such is not unusual given past cycles. A correction is still possible while the sell signal is in place, so we continue to maintain a slightly higher level of cash currently.

*** Portfolio Trading Update *** Dynamic Model (Beta Portfolio)

The Dynamic Model, that we launched in January has had a bumpy start with the model algorithm getting whipsawed a good bit by the Nasdaq selloff in February and March, and then the rotational trade over the last month or so. However, we are honing in on the model allocation and should have a functional model in place by the end of the year.

Trades

Initiate a 3% position of the portfolio in KHC, ADSK, and UNH.

*** Portfolio Trade Alert *** Dynamic Model (Beta Test Portfolio)

We continue working on getting this model balanced correctly, and are making some additional rebalancing changes this morning. We also got stopped out of our GOLD and SLV trades.

Initiate a 1.5% position in AVGO

Sell 100% of SLV

Sell 100% of JPM

Sell 100% of GOLD

Initiate a 1.5% position in AMAT

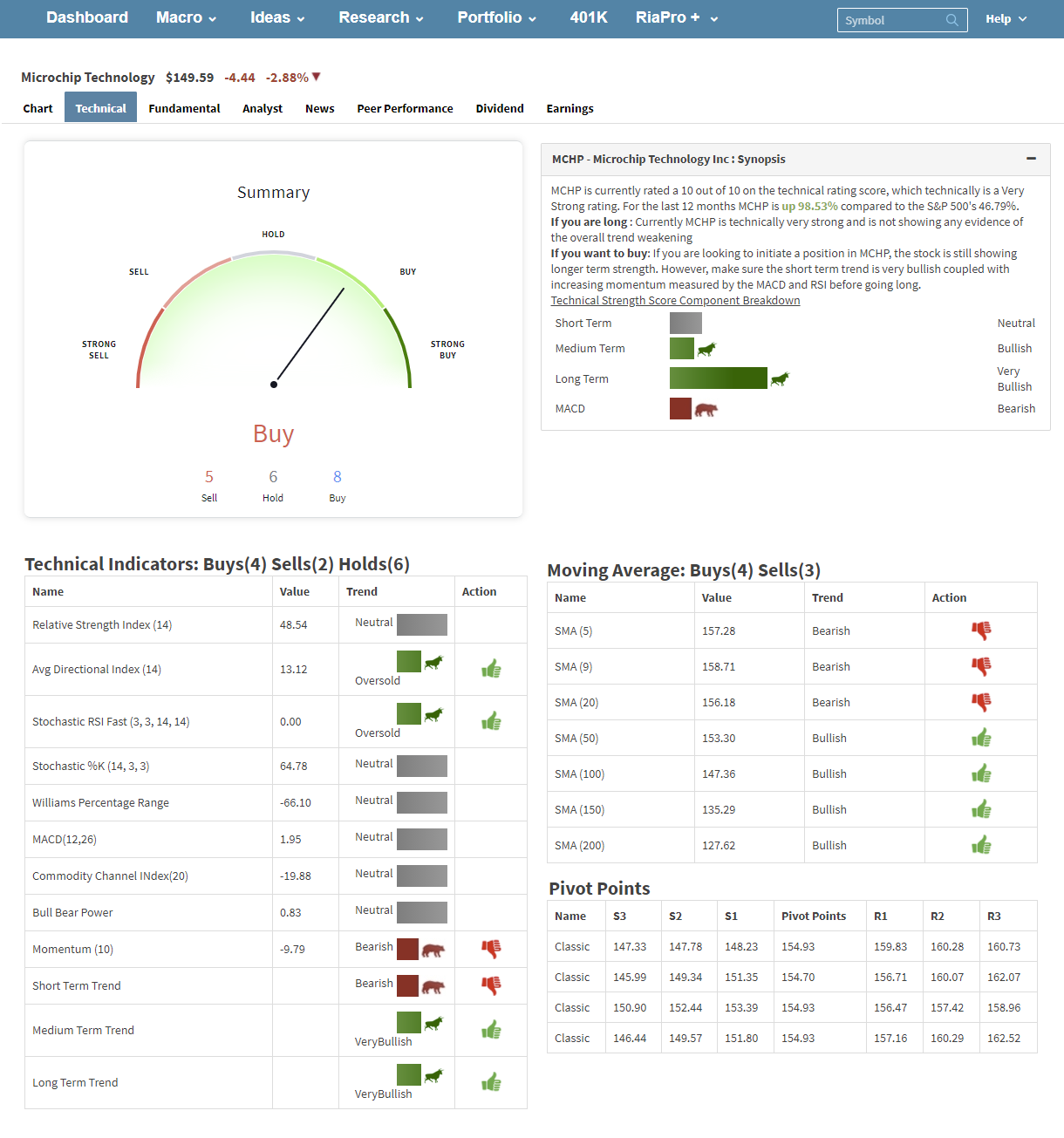

Sell 100% of MCHP

Add 1.5% to OSTK

Add 1.5% to QRVO

Reduce FANG, XOM, MRO, and KMI by 50% each.

Add 1.5% to CVS

Sell 100% of TPR

Note: There was an error in the transaction report on FANG. On 6/10/21 we sold 18 shares of FANG at $87.245 but the system did not report the transaction. We caught the error in today’s rebalance.

*** Portfolio Trade Alert *** Equity & ETF Models

We are rebalancing exposures in the Equity and ETF models slightly this morning.

This morning we adjusted our models to reduce commodity risk. in the Equity model, we sold all of KMI (1.5%), and we were stopped out of GOLD (2%). We added 1% of CVS which is turning on a nice buy signal and in a sector we like. In the Sector model, we sold 1% each of AMLP and XLE. Our equity exposure is just north of 50%.

As discussed over the last few weeks in our weekly newsletter, we are coming upon the confluence of daily and weekly signals turning negative for a wide swath of sectors, stocks, and broad indexes. As such, we are reducing our net exposure by 3.5% to 53% in both models. At the same time, we are adding to a few sectors/stocks that have positive technical outlooks.

Equity Model:

AAPL – reduce position by 1/2% of the portfolio.

ABBV – increase the position by 1% of the portfolio.

ADBE – reduce position by 1/2% of the portfolio.

ALB – reduce position by 1 and 1/2% of the portfolio.

FANG – reduce position by 1/2% of the portfolio.

CVS – increase the position by 1/2% of the portfolio.

GOLD – increase by +1 of the portfolio.

JNJ – increase the position by 1/2% of the portfolio.

MSFT – reduce the position by 1/2% of the portfolio.

PSA – reduce the position by 1/2% of the portfolio.

RTX – reduce the position by 1/2% of the portfolio.

UNP – sell 100% of the position.

UPS – increase the position by 1% of the portfolio.

V – reduce the position by 1/2% of the portfolio

Sector Model:

XLV – increase the position by 2% of the portfolio.

XLK – reduce the position by 2.5% of the portfolio

LIT – reduce the position by 1% of the portfolio

IYT – reduce the position by 1/2% of the portfolio

XLB – reduce the position by 1/2% of the portfolio

XLE – reduce the position by 1/2% of the portfolio

XLF – reduce the position by 1% of the portfolio

XLI – reduce the position by 1/2% of the portfolio

XLU – increase the position by 1% of the portfolio

Dynamic Model

JPM – reduce the position by 1/2% of the portfolio.

XOM – reduce the position by 1/2% of the portfolio.

MRO – reduce the position by 1/2% of the portfolio.

SLV – initiate a 2% position of the portfolio.

KNX – sell 50% of the position.

JNJ – increase position by 1/2% of the portfolio.

ALB – reduce by 1% of the portfolio.

GOLD – initiate a 2% position of the portfolio.

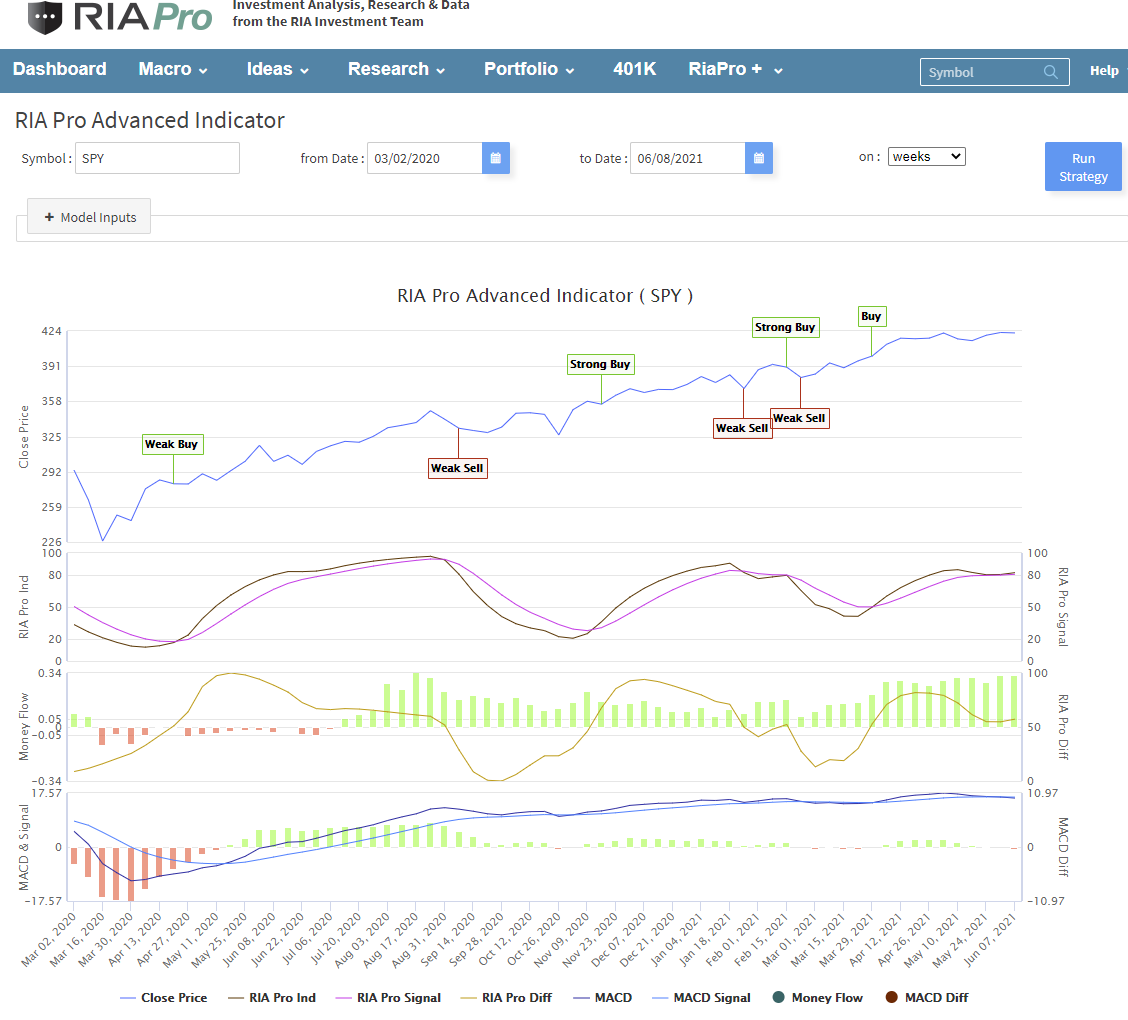

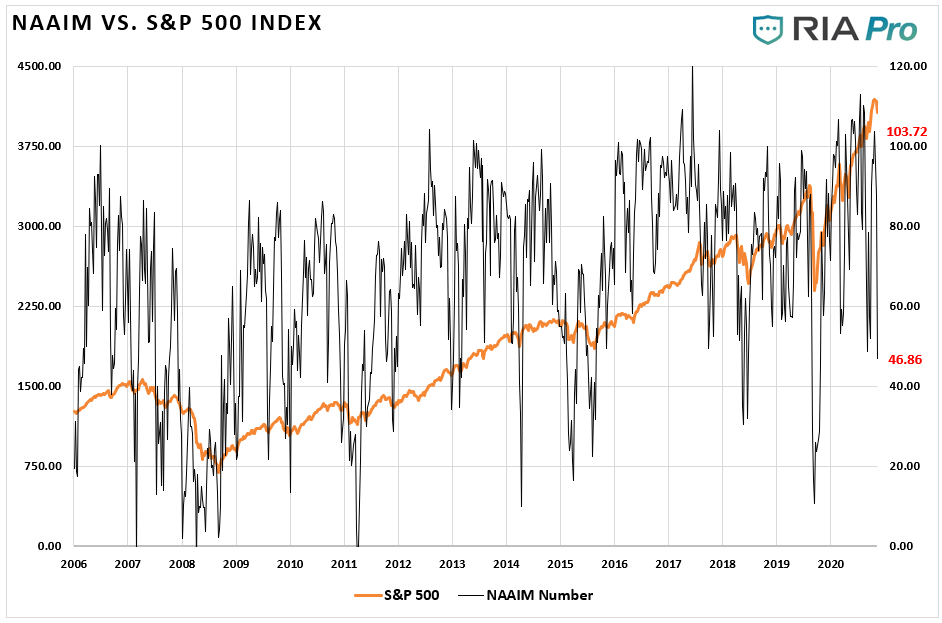

Money Flow Signal

I have been getting many emails lately about how to gain access to our proprietary money flow indicator that Mike and I use to manage our client portfolios.

We hear you and it is coming.

We have 2-huge projects underway currently with our programmers.

A complete website redesign to improve the look, feel speed, and efficiency of the site.

Integration with Interactive Brokers so that you can have access to multiple models on the site and have them automatically traded for you. OR, you can manage your own portfolio and have full reporting on the site.

We have many more features we are adding to the site as well from curated stock lists, to portfolio model management and model backtesting.

AND YES….We are currently working on the RIA PRO Money Flow indicator that you will have access to once we get all the bugs worked out of the coding. Here is a snapshot of where we are currently.

Click to enlarge

Thank you for your patience and for using our service. We are constantly working to improve the site into a “must-have” tool for investors.

Your comments, criticisms, and suggestions are ALWAYS welcome.

We closed out the remainder of our QQQ position as our indicators are now aligning for the next sell signal. We should begin to see technology underperform relative to the broad index over the next couple of weeks.

With our “money flow” buy signal now getting fairly elevated we trimmed off another 1% of our QQQ position this morning in both models. We will likely exit the entire position by the end of the week.

In the Equity model, we also reduce Ford (F) by 1.5% (down to 2% of the portfolio) to take profits after a strong price surge last week.

*** Portfolio Trade Update *** – Dynamic Model (Beta Test) Only

We recently added exposure for the “money flow” buy signal which worked well. However, that signal is now beginning to get extended in some stocks and oversold in others. Therefore, we are rebalancing the model by selling/trimming overbought stocks and adding to oversold positions.

(NOTE: I had a trade error and bought SWKS rather than selling. I have corrected that error.)

Full Portfolio Rebalance

FANG – Add 1% to the position

MRO – Add 1% to the position

AMZN – Sell 50% of the position

NEE – Sell 50% of the position

QRVO – Reduce portfolio position by 50%

GOOG – Reduce portfolio position by 50%

SWKS – Sell 100% of the position

MCHP – Sell 50% of the position

AAPL – Reduce by 50%

MSFT – Reduce by 50%

ETSY – Sell 100% of the position

ALB – Add 1% of the portfolio to the position

SQ – Sell 100% of the position

ABBV – Add 1% of the portfolio to the position

BRK.B – Add 1.5% of the portfolio to the position

WMT – Sell 100% of the position

CRM – Sell 100% of the position

TPR – Add 1.5 % of the portfolio to the position

KNX – Add 1% of the portfolio to the position

KMI – Add 1.5% of the portfolio to the position

XOM – Add 1.5% of the portfolio to the position

NFLX – Sell 50% of the position

ADBE – Sell 50% of the position

PG – Sell 50% of the position

JPM – Add 1% of the portfolio to the position

OSTK – Sell 50% of the position

May 27, 2021

COST reported GAAP EPS of $2.75, which topped the consensus estimate of $2.34. Revenue of $45.3B beat expectations of $43.8B, while membership fees increased 11% YoY, coming in 3.1% above the consensus estimate. We currently hold a 1.5% position in COST in our equity model.

This morning we reduced our 4% QQQ position in both models by 1% to 3% of portfolio. The technical signals that led us to buy are getting extended, so we are just taking some profits. When our signals begin to suggest a “sell signal” is approaching we will remove the rest of the position.

We are also adding 2% AMLP in both models as it technically looks strong and we think inflationary stocks will have decent relative outperformance in the coming days. This is a trade for a near-term bump in inflationary pressures and picking up an 8% dividend yield at the same time.

The buy signals on the Dow and S&P are not as extended as the NASDAQ.

Equity & ETF Models

Reduce the 4% position in QQQ to 3% of the portfolio.

Click the link above to add TPA Daily Reports and Long/Short trading ideas to your subscription.

REASONS TO BE CAUTIOUS. MITIGATING FACTORS. SIGNALS TO WATCH FOR REAL PROBLEMS.

Since March 23, 2020, the U.S. stock market has enjoyed a consistent rally. The S&P500 is up 87% since the Covid-19 March 2020 panic low. Many investors, money managers, strategists and analysts are rightfully concerned about the rally’s longevity and the levels of equity prices. Examining the measures TPA has used for over a decade, TPA is also concerned. At the same time, TPA is mindful that many mitigating factors are supporting the current rally. Some of these factors are historic. In this report, TPA will examine why clients are justified to be cautious, while acknowledging the factors that have and do support stock prices. Finally, TPA will provide signposts that clients should monitor to determine when the likelihood of a sell-off will increase.

Caution

Historically high valuations

Bubble characteristics

The level of margin used by stock investors is at a historic high

Mitigating factors

Reduced number of shares for investors to buy

FED activities

Fiscal stimulus

Low rates

What to watch for that things are changing

FED tapering or tightening

House price declines

Sustained weakening in consumer demand

Technicals.

Sustained risk-off signals

50 DMA’s of the major indexes starting to decline

Earnings announcement show negative price bias

Junk Bond Risk premium widening

May 26, 2021

Amazon (AMZN) has reached an agreement to acquire MGM for $8.45B. The move will strengthen the positioning of Prime Video versus competitors in the ongoing “streaming wars.” AMZN will receive a catalog of more than 4,000 movies and 17,000 TV shows from the acquisition.

Ford (F) is trading higher this morning as they reaffirmed their commitment to electric vehicles (EV). Further, they intend to hit long-term operating margin goals, despite the ramped-up EV production and R&D expenses.

“The company said during an investor day on Tuesday it will spend $30 billion on electric vehicle development — including battery development — by 2025. Previously, the auto giant said it would spend $22 billion on its EV ambitions by 2023. The company anticipates that 40% of its global vehicle volume will be fully electric by 2030 fueled by new models of the electric Mustang Mach-E and F-150“- Yahoo Finance

May 24, 2021

Feature Upgrade – Reminder

In case you missed it, we have now put a full technical overview under the RESEARCH / CHARTS tab. The new charting system now allows you to save your technical setups and has a wide range of indicators to choose from – so customize your layouts the way you like them. Then click the TECHNICAL TAB to see a full technical review of the stock you are looking at.

Technical Gauge (Now live under the Macro/Market Internals Link)

Fear/Greed Gauge (Also Live)

Risk / Reward Ranges – XLK, XLC, and XLY now in buy territory.

May 20, 2021

*** Portfolio Trading Update *** Equity Model (Updated)

We added 1% to Ford (F) increasing our total position to 3%. The stock broke out of its previous downtrend and pushed above the 50-dma. We expect that at some point, the company will re-establish its dividend which will help total returns in the future. For now, it is a trading position until that transition occurs.

Equity & ETF Models

Add 1% of the portfolio into F increasing total weighting to 3%.

May 19, 2021

*** Portfolio Trading Update *** Equity & ETF Model

In both models we added 2.5% of TLT and 1% QQQ, bringing QQQ up to 4%. We are adding TLT in part for technical reasons as it’s very close to its 200 dma and getting ready to turn up on a money signal. Further, it may provide a little insurance if the recent downtrend in equities continues.

Equity & ETF Models

Initiate a 2.5% position in TLT

Add 1% of the portfolio into QQQ increasing total weighting to 4%.

May 18, 2021

*** Portfolio Trading Update *** Equity Model Only

We trimmed back CVS to model weight into the market close today (2% of the portfolio) after a big move higher. We still like the position longer-term on a fundamental basis but it needs a correction to add to the position.

Note: The full history of the Technical Gauge and Fear Greed Gauge is now under Macro/Market Internals. We are working to have them overlaid against the S&P 500 index.

Technical Gauge Is Still High But Has Declined

Fear/Greed Gauge Is Back Into The “Neutral Zone”

Risk/Range Analysis Shows Technology & Discretionary As Opportunistic

May 14, 2021

*** Portfolio Trading Update *** Dynamic Model (Beta Test)

The Dynamic Model, launched in January, is still in beta testing.

We are closing out the rest of our position in LEN after a huge run and starting to see relative weakness in pricing.

Dynamic Model

Sell 100% of LEN

May 13, 2021

*** Portfolio Trading Update *** Equity & ETF Model

We are continuing to build a trading position in QQQ for an approaching “buy signal” on our “money flow” indicator. After our initial add of 2% of the portfolio, we are increasing the position by another 1% bringing the total portfolio weight to 3%.

Equity & ETF Models

Add 1% of the portfolio to the existing position in QQQ

May 12, 2021

*** NEW FEATURE UPDATE ***

Every week in the newsletter we publish the FEAR / GREED Gauge and our TECHNICAL GAUGE

We have gotten a lot of requests for the history of gauges. We have now published them under the MACRO tab along with our other market indicators.

We will be adding a comparison to the S&P here soon, but we wanted to let you know these two charts are now available.

Click to enlarge images

Menu

Guages

*** Portfolio Trading Update *** Dynamic Model (Beta)

Reminder note:

The Dynamic Model, launched in January, is still in beta testing. We are working through the modeling of the portfolio methodology. We should have the model finished by the end of this year as we work through various market dynamics and weightings.

Currently, the performance of the model is not working as expected due to the shift in inflation, and economic, expectations. As such, we are tweaking the model to compensate. However, it will take a few months before that alignment to the benchmark is complete.

Dynamic Model

Taking profits in CVS and reducing the position from 3% to 2% of the portfolio.

In today’s 3 Minutes on Markets & Money we discussed that the NASDAQ is relatively oversold versus the S&P and DJIA.

The graph below helps provide some risk levels on the NASDAQ (QQQ). Since the market rout last March, QQQ has fallen below its 50-day moving average three times. The second graph shows its deviation from the 200-day ma. It is still about 10% above the average. As discussed, the NASDAQ is over-sold on a short-term basis but not a long-term basis. There is a potential opportunity here but it entails a good eye on risk management.

We are going to build into a position of QQQ over the next several trading days looking for a relative pickup in performance relative to the S&P 500. We are starting with a 2% position in QQQ and will add to it if we get further weakness.

Equity & ETF Model

Initiate a 2% trading position in QQQ

May 10, 2021

*** Portfolio Trading Update *** All Models

We are taking some profits in the Equity and ETF Models in more grossly extended positions. In the Equity model, we are paring back to model weights of 2% in UPS and ALB back to 4% of the portfolio. In the ETF model, we reduced IYT (Transportation) back to model weight as well.

In the Dynamic model, we added to FANG and initiated a new position in MRO as we continue to rebalance that portfolio as well.

Fear/Greed Gauge Still Elevated But Off Of Recent Highs

Risk/Reward Ranges Not Optimal – But Technology Has Worked Off Extremes

May 7, 2021

*** Portfolio Trade Update *** Dynamic Model

With our “money flows” on some of the technology names getting very oversold, we are adding some exposure back to holdings that we previously sold at higher levels. We are also adding a bit more to basic materials with an addition of Linde (LIN).

*** Portfolio Trade Update *** All Models (Update)

In the Equity and ETF models we are adding to our “inflation” plays by adding a starter position to Barrick Gold (GOLD) in the equity portfolio and adding to Industrials (XLI) in the ETF Model.

In the Dynamic Model, after a selling half our stake in SQ at higher prices, we are adding back to our holdings. We are also adding back to ALB with the recent selloff taking our position size back to 3%.

Equity Model

Initiate a 1% “Starting” position in GOLD

ETF Model

Increase XLI from 2% to 3% of the portfolio.

Dynamic Model

Increase SQ from 1.5% to 3% of the portfolio.

Increase ALB to 3% of the portfolio.

May 5, 2021

ALB reported GAAP EPS of $0.84 compared to the consensus estimate of $0.80 per share. Revenue came in above consensus at $829.3M versus expectations of $757.1M. Despite beating top and bottom-line estimates, the stock is currently trading 2.5% lower post-market. Management’s decision to leave fiscal year 2021 guidance unchanged appears to be weighing on the stock.

May 4, 2021

CVS reported GAAP EPS of $1.68, which beat expectations of $1.33. Revenue also beat expectations, coming in at $69.1B versus the consensus of $68.35B. In addition to the positive figures, CVS raised full-year guidance for GAAP EPS to $6.24 to $6.36 from $6.06 to $6.22. This represents an increase of 2.6% at the midpoint as well as a tightening in the range of guidance. The stock is currently up 2.8% pre-market.

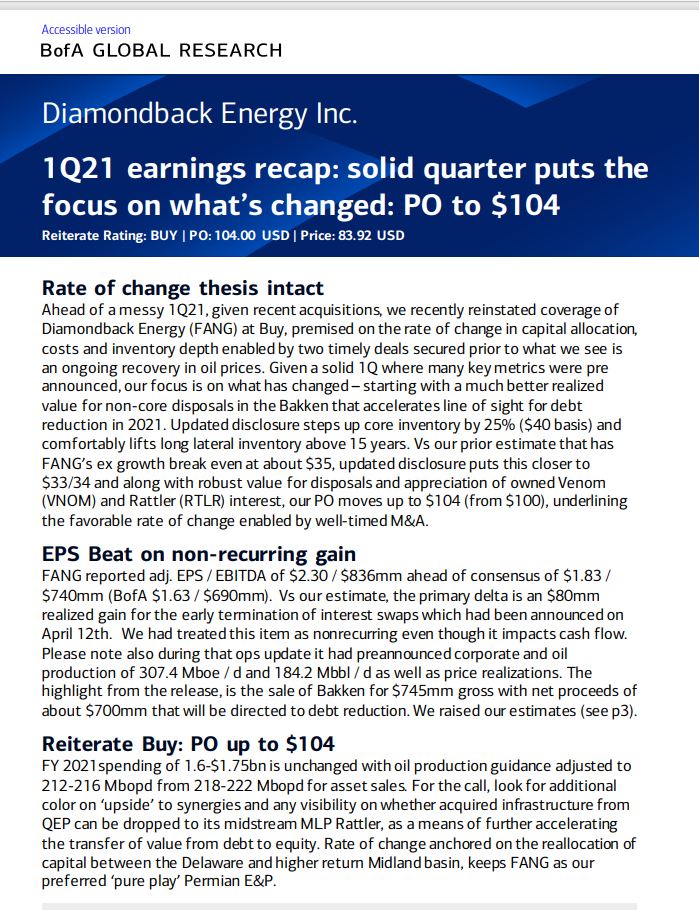

Yesterday we reported FANG fell short on EPS estimates but beat revenue expectations. The paragraphs below from Bank of America provide a nice summary of FANG’s earnings report and their rationale for slightly increasing the price target to $104 from $100 per share.

May 3, 2021

FANG reported GAAP EPS of $1.33, which missed the consensus estimate of $1.89. Conversely, revenue of $1.2B beat expectations of $1.02B. Today FANG announced the divestiture of three of its non-core operating assets for total consideration of $832M, which will help the company accelerate its debt reduction program and continue strengthening its balance sheet.

*** Portfolio Trade Update *** Dynamic Model

Diamond Back Energy (FANG) is going to report earnings this week and we expect a substantial beat of earnings. With a fairly close stop-loss, and the MACD about to register a buy signal, the risk-reward is favorable.

We were stopped out of PINS and PLTR after selling 50% of the positions a couple of weeks ago.

With the breakout of the consolidation of ABBV, we are adding a 3% weight to the portfolio. The same for WMT which just broke out of a downtrend from previous all-time highs.

After taking profits previously in CVS, JNJ and PG, we are increasing those positions back to size for the next “buy signal.”

Buy 1.5% of FANG with a stop-loss at $73.50

Selling 100% of PINS and PLTR – violations of stop-loss after previous 50% sells.

Initiate a 3% position in ABBV

Initiate a 3% position in WMT

Increase JNJ, CVS, and PG from 1.5% of the portfolio to 3%.

Risk / Reward Ranges Reset For May – Long-Term Deviations Unsustainable.

*** Portfolio Trade Update *** All Models

In the Equity and ETF Models, we are reducing Real Estate just a “smidge” to take profits in a sector that has gotten extremely overbought. In the Dynamic Model, we sharply reduced equity exposure with the previous sell signal. With the next “buy signal” approaching, we are looking to add to fundamentally strong stocks that got hit recently during earnings announcements, and are holding near support levels.

We are also initiating two new positions in the Dynamic of KNX (Knight Transportation) and OSTK (Overstock.com). With the demand for freight very high, we like the transportation sector and have no previous exposure. Overstock is an interesting play because if they sell off their “retail” business, we can acquire their “blockchain” business essentially for free. We are starting with 1/2 positions and will add to accordingly.

Equity Model

Reduce PSA from 2% to 1.5% of the portfolio.

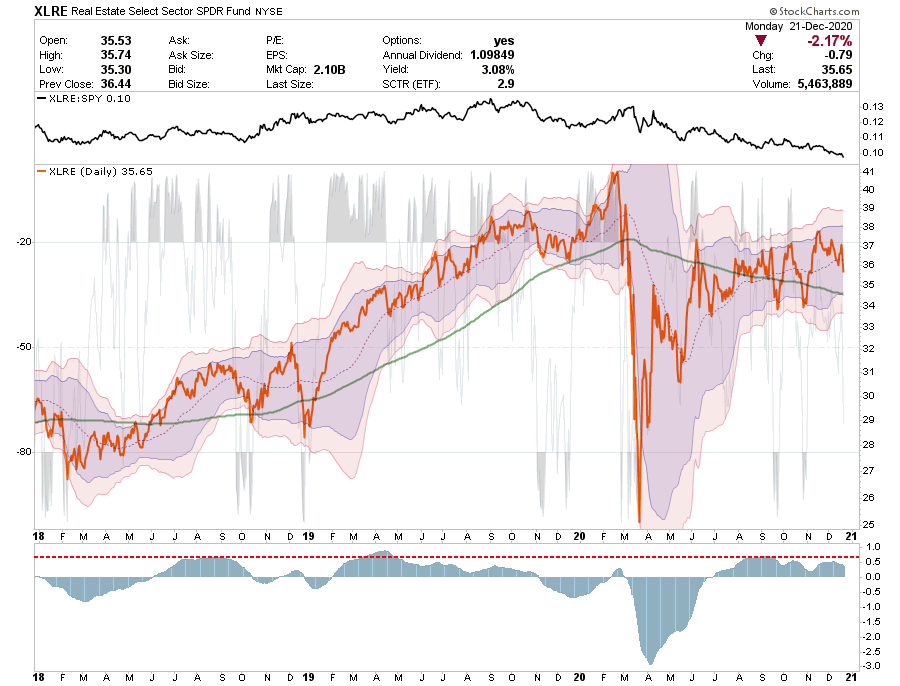

ETF Model

Reduce XLRE from 3% to 2%.

Dynamic Model

Initiate a 1.5% position in OSTK

Initiate a 1.5% position in KNX

Increase NFLX from 1.5 to 3% of the portfolio.

Increase JPM from 1.5% to 3% of the portfolio.

ABBV reported GAAP EPS of $1.99, which easily beat expectations of $1.47. Revenue of $13B came in slightly above the consensus estimate of $12.8B. Management has raised guidance for full-year 2021 EPS to $7.27-$7.47 from $6.69-$6.89, an increase of 8.5% at the midpoint.

XOM reported GAAP EPS of $0.64 for the first quarter of 2021, which beat expectations of $0.57. Revenue also beat expectations, coming in at $59.2B versus the consensus of $56.5B. The positive results were driven by a combination of higher commodity prices and XOM’s focus on structural cost reduction.

April 30, 2021

*** Portfolio Trade Update *** All Models

In the Equity and ETF Models, we are reducing Real Estate just a “smidge” to take profits in a sector that has gotten extremely overbought. In the Dynamic Model, we sharply reduced equity exposure with the previous sell signal. With the next “buy signal” approaching, we are looking to add to fundamentally strong stocks that got hit recently during earnings announcements, and are holding near support levels.

We are also initiating two new positions in the Dynamic of KNX (Knight Transportation) and OSTK (Overstock.com). With the demand for freight very high, we like the transportation sector and have no previous exposure. Overstock is an interesting play because if they sell off their “retail” business, we can acquire their “blockchain” business essentially for free. We are starting with 1/2 positions and will add to accordingly.

Equity Model

Reduce PSA from 2% to 1.5% of the portfolio.

ETF Model

Reduce XLRE from 3% to 2%.

Dynamic Model

Initiate a 1.5% position in OSTK

Initiate a 1.5% position in KNX

Increase NFLX from 1.5 to 3% of the portfolio.

Increase JPM from 1.5% to 3% of the portfolio.

ABBV reported GAAP EPS of $1.99, which easily beat expectations of $1.47. Revenue of $13B came in slightly above the consensus estimate of $12.8B. Management has raised guidance for full-year 2021 EPS to $7.27-$7.47 from $6.69-$6.89, an increase of 8.5% at the midpoint.

XOM reported GAAP EPS of $0.64 for the first quarter of 2021, which beat expectations of $0.57. Revenue also beat expectations, coming in at $59.2B versus the consensus of $56.5B. The positive results were driven by a combination of higher commodity prices and XOM’s focus on structural cost reduction.

April 29, 2021

AMZN reported first quarter GAAP EPS of $15.79 as compared to the consensus estimate of $9.61. Revenue of $108.5B (+43.7% YoY) came in well above expectations of $104.6B. For the second quarter of 2021, AMZN has set guidance for revenue of $110-$116B, or 24-30% growth YoY. The stock is currently trading 4.7% higher in the post-market session based on the strong results.

April 28, 2021

PSA reported core FFO of $2.82 per diluted common share, which beat expectations of $2.71 per share. Revenue of $647.8M missed the consensus estimate of $759.3M. PSA saw same-store revenue growth of 3.4% YoY. The company acquired ezStorage for $1.8B during the quarter, which the CEO- Joe Russell, referred to as “one of the highest quality self-storage portfolios in the United States”.

AAPL reported GAAP EPS of $1.40, which easily beat the consensus estimate of $0.98. Revenue of $89.6B beat the consensus estimate of $77.3B. Further, revenue beat expectations in each major product category. In addition to the positive top and bottom-line data, AAPL raised its dividend to $0.22 per share (+7%).

F reported GAAP EPS of $0.81 for the first quarter of 2021, which smashed the consensus estimate of $0.18. Automotive revenue also came in above expectations, measuring $33.6B versus expectations of $32.2B.

Despite the strong results, the stock is down 2.9% in the post-market session. John Lawler, CFO, commented that the semiconductor shortage facing the auto maker will likely get worse before it gets better- due to a fire that occurred in March at supplier plant in Japan. The company expects the shortage to bottom out in the second quarter and improve throughout the rest of the year, but now expects to lose up to 50% of its planned second quarter production.

April 27, 2021

V reported GAAP EPS of $1.38, which beat the consensus estimate of $1.28. Revenue came in at $5.7B (-2.6% YoY), finishing slightly above expectations of $5.56B. Payments volume increased 11% YoY, while total processed transactions increased 8% YoY. Conversely, cross-border total volume decreased 11% YoY.

MSFT reported GAAP EPS of $2.03 versus expectations of $1.77. Revenue of $41.7B (+19.1% YoY) beat the consensus estimate of $40.85B.

GOOG reported GAAP EPS of $26.29, which beat the consensus estimate of $15.67. Revenue of $55.3B (+34.4% YoY) came in well above expectations of $51.7B.

RTX reported GAAP EPS of $0.51, which missed the mark by $0.30. Revenue of $15.3B was slightly below expectations of $15.4B. With first quarter sales and adjusted EPS coming in above management’s expectations, RTX has boosted the low end of its 2021 guidance for sales and adjusted EPS.

UPS reported impressive first quarter results this morning. GAAP EPS of $5.47 beat expectations of $1.68, while revenue of $22.9B similarly beat expectations of $20.7B. Average daily volume increased by 14.3% YoY. Of note, $2.70 of the EPS was driven by a reduction in the pension liability arising from re-measurement required under the ARPA. The stock is currently up 7.2% in pre-market trading.

April 26, 2021

NXPI reported first quarter GAAP EPS of $1.25, which beat expectations of $1.21. Revenue also beat expectations, coming in at $2.6B versus the consensus of $2.5B.

*** Portfolio Trade Alert ***

Both Equity and ETF Models

We are selling 100% of our gold position in IAU. We bought it for a trade and it looks as if that move has been completed. Taking the small gain and will re-evaluate the position for another opportunity.

KMI released its earnings data yesterday after the market close. GAAP EPS of $0.62 smashed market expectations of $0.23, and revenue of $5.2B ended up much higher than expectations of $3B. A driving factor behind the stellar results was the winter storm that hit Texas in February. Even though KMI recognized that benefit as temporary, the firm raised its quarterly dividend by 2.9% to $0.27 per share.

April 21, 2021

NEE reported earnings for the first quarter of 2021 this morning. GAAP EPS of $0.84 beat expectations of $0.55 per share, while revenue of $3.7B missed expectations of $4.9B. Management has guided to adjusted EPS between $2.40 and $2.54 for fiscal year 2021 with 6% to 8% growth in adjusted EPS in 2022 and 2023.

VZ reported GAAP EPS of $1.27 compared to expectations of $1.28, a slight miss. Revenue for the first quarter was $32.9B (+4.0% YoY), which beat estimates by $440M. VZ saw wireless post-paid net adds of -170k versus expectations of +82k for the quarter.

April 20, 2021

NFLX reported GAAP EPS of $3.75, which beat expectations by $0.78. The firm reported revenue of $7.2B for the first quarter of 2021, which came in $20M above the average estimate. Looking beyond the positive top and bottom-line figures, paid net additions for the quarter were 4M versus Management’s guidance of 6M. NFLX is currently trading almost 10% lower in the post-market session.

*** New Feature ***

(You may need to log out and log back in to see the new Technical Analysis)

We have added a new Technical Overview under RESEARCH/CHARTS which provides buy/sell analysis based on a range of technical indicators.

Click Image To Enlarge

ABT reported GAAP EPS of $1.00, which beat the average estimate by $0.09. However, revenue of $10.5B missed analyst estimates by $170M. Organic revenue growth was 32.9% YoY including COVID-19 testing related effects, and 5.7% YoY excluding COVID-19 testing related effects.

JNJ reported GAAP EPS of $2.32, which beat the average estimate by $0.22. Similarly, revenue of $22.3B beat analyst estimates by $280M. The positive results were led by above market growth of the Pharmaceutical business and continued recovery in Medical Devices, according to the CEO, Alex Gorsky.

PG reported GAAP EPS of $1.26, which beat by $0.07. Revenue also beat estimates, coming in at $18.1B versus the expectation of $17.95B. Organic sales growth increased 4% YoY; 2% of this was driven by increased prices and 2% by positive product mix.

April 19, 2021

*** Portfolio Trade Update ***

As noted in this past weekend’s newsletter, our “money flow” buy signal is very extended and is starting to roll over. As such we are now beginning to cut exposure in portfolios and raise cash levels. We are preparing to add a short-S&P 500 index position once the “sell signal” engages.

We removed half of our 5% SPY position in both models this afternoon, bringing them both down to 2.5%. Our money flow models will turn bearish over the next day or two and we decided to take some profits.

April 14, 2021

*** Trading Update – Dynamic Model ***

Taking some profits in LEN and SQ which have had big runs lately and are extremely overbought. Adding a position of MSTR with a stop at $675 to potentially trade against the Coinbase IPO. Technically signals are oversold and turning up so there is some upside to about $900 as long as current uptrend support holds.

Take Profits – reduce LEN to 1% of the portfolio.

Take Profits – reduce SQ to 3% of the portfolio.

Initiate 5% of MSTR with a stop at $675

JPM reported GAAP EPS of $4.50, which beat analyst estimates by $1.38 or 44%. Revenue came in at $32.3B, 6.6% above the average estimate of $30.3B. The results were driven by a large decrease in loan loss reserves of $5.2B (contributing $1.28 to EPS).

GS reported GAAP EPS of $18.60, which came in 86% above analyst estimates. Revenue for the first quarter was $17.7B compared to estimates of $12.7B, a 39% surprise.

In both cases the strong results were driven by record Investment Banking, Trading, Asset Management revenues and a significant increase in Global Markets revenues. We hold 2% of each stock in our Equity Model.

Just prior to the initiation of the “money flow buy signal,” we added two leveraged index positions to the Dynamic Model. With the sharp rally, and with markets back to more extreme overbought conditions, we are taking those profits and reducing equity risk a bit.

Dynamic Model

Selling 100% of QLD and SSO

PORTFOLIO TRADING UPDATE – 04-06-21

We added 2.5% of IAU this morning in both models. Gold is setting up nicely on a technical and money flow basis with reliable stop-loss levels not far below. The trade also aligns with the thought that the market is looking beyond the next few months of strong economic data and questioning whether the reflation trade will still have legs come later summer and fall.

EQUITY & ETF MODELS

Initiate a 2.5% position in IAU / Stop-Loss is $16

NOTICE – SITE DATA ISSUE!

We are having a data issue this morning on numerous pages.

Please bear with us as we fix the problem.

PORTFOLIO TRADING UPDATE – 04-05-21

We sold TLT this morning in both portfolios. We had TLT on a tight leash and given strong economic data and money flows were rolling back over on TLT, we thought it best shorten-duration in portfolios back to previous levels. We are significantly underweight our benchmark weight in terms of bond duration at the current time.

Wishing you a very “Good Friday” and a Happy Easter.

As noted yesterday, we added to individual positions yesterday within portfolio models, and today we added our “trading index” positions to all models. As noted, with the quarter-end rebalancing behind us, and with April being one of the strongest performance months of the year within the seasonally strong cycle, we are upping exposure short-term to participate with a breakout to new highs.

Equity Model:

Reduced SHY to 10% of the portfolio

Added a 5% position in SPY

ETF Model

Reduced SHY to 10% of the portfolio

Added a 5% position in SPY

Dynamic Model

Added 3% TSLA

Added 1/2 position (3%) of SSO to the portfolio.

Added 1/2 position (3%) of QLD to the portfolio.

March 31, 2021

*** Portfolio Trading Update – All Models***

With our S&P 500 “money flow” models turning positive, along with money flows, we are adding exposure to portfolios for what tends to be a historically strong April period. We are doing this in two phases – adding individual positions today, and shortly, we will add trading index positions in SPY and QQQ.

Equity Model:

Increased ALB to 4% of the portfolio.

Initiated a 2% in NXPI

Initiated a 2% in F

Selling 100% of CRM

ETF Model

Added 1% to LIT increasing weight to 4%

Dynamic Model

Increased AAPL from 3% to 3.5% of the portfolio

Added to SQ increasing weight to 3.75% from 3%

Added to ALB increasing its weighting to 3.5% from 3%

While our S&P indicator is still in sell mode, energy and financials, are starting to turn up. They went into sell mode well before the broader market so are coming out sooner. As such, we added back to energy and financials.

Equity Model:

Added .5% to KMI, XOM, and FANG

Added .5% to GS and JPM

ETF Model

Added 1% to XLE and XLF

Dynamic Model

Added .5% to KMI and XOM

Added .5% to JPM

March 24, 2021

*** Portfolio Trading Update – Equity and Sector Models ***

With our models pointing to potential short-term turbulence in the equity markets and potential upside in bond prices (as discussed in Three Minutes on Markets), we increased our bond portfolio duration and equity hedge by swapping IEF for TLT. We also put extra cash to work by adding to our short-term bond position (SHY). We will redeploy SHY into stocks and or bonds when needed.

Equity and Sector Model:

Sold 6% IEF and Bought 6% TLT

Added 7% SHY

March 23, 2021

*** Portfolio Trading Update – All Models ***

With our daily “money flow” indicators very close to turning negative, with money flows negative as well, we are reducing equity risk across all models slightly.

Equity Model:

Selling 100% of MRO to reduce our overweight energy holdings.

Selling 100% of ZM reducing our exposure to communications and a sector laggard.

Initiating a 1% position in PG to add to our Consumer Staples (defensive) holdings.

Fear / Greed Gauge Remains Very Elevated Despite Recent Volatility

Technical Gauge Remains Overbought Currently

Risk/Ranges Suggest Market Still Not A Good Buy

March 18, 2021

*** Portfolio Trade Update – Dynamic Model ***

Portfolio Managers: Nick Lane/Lance Roberts

We are selling our entire stake of TSLA this morning. We bought it previously at support which failed. The recent rally ran back into our previous support and failed again. We simply had bad timing on this trade. We are closely evaluating all of our positions now and continue to raise cash.

Sell 100% of TSLA

March 16, 2021

*** Portfolio Trade Update – Equity, Sector and Dynamic Model ***

Portfolio Managers: Michael Lebowitz/Lance Roberts

After a nice run-up in the banks/financials, we are taking some profits.

Equity model- reduce GS and JPM from 2% to 1.5%

Sector model- reduce XLF from 4% to 3%

Dynamic model- reduce JPM from 3.5% to 2.5%

*** Portfolio Trade Update – Dynamic Model ***

Portfolio Managers: Nick Lane/Lance Roberts

We are initiating a 3% position in Tapestry (TPR) which is a high-end retailer of luxury goods. With stimulus checks coming in and the economy reopening there is potential upside for TPR.

Initiate a 3% position of TPR with a stop-loss at $40.

With our short-term money flow indicator turning positive yesterday we are adding exposure to all of our portfolios. Primarily, we are just bringing positions that recently sold-off back up to model weights but we are increasing sizing in APPL and MSFT to 3.5% of the portfolio and bringing ABT, ABBV, JNJ and CVS up to 2% each after reducing those positions previously. In the Dynamic Model which is very technology-heavy, we are adding a bit of industrial and healthcare exposure as well to broaden out the allocation model.

Equity Model

Increase allocation to AAPL and MSFT to 3.5% of the portfolio.

Bring NFLX and ZM up to 2% of the portfolio.

Add 0.5% weight to ABBV, ABT, JNJ, and CVS increasing total exposure to 2% each.

ETF Model

Increase XLV to 8% of the portfolio.

Increase XLK to 12.5% of the portfolio.

Dynamic Model(Still in beta testing)

Reduce BGSF from 5% to 3% of the portfolio.

Initiate a 3% position in JNJ, CSV, and BRK.B each in the portfolio.

March 9, 2021