In this issue of “Bulls Buy Stocks, As Fed Starts To Talk Taper.“

- Market Review And Update

- Fed Starts To Talk Taper

- Risk Is Elevated

- Portfolio Positioning

- #MacroView: NFIB Data Says It’s Only A Recovery

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

Market Review & Update

After another rough start to the week, the bulls finally showed up and flipped our “money flow” indicators back to a buy signal. As we stated last week:

“Well, that follow-through failed to occur.Not only did the “buy signal” not trigger, but the market also broke down through the previous consolidation range. As I said, it did not work out as planned. The last exposure we took on is now pressuring the portfolio momentarily, but we should benefit from the turn if we are correct.”

With markets deeply oversold on a short-term basis and with signals at levels that generally precede short-term rallies, the rally on Thursday and Friday was not unexpected. Notably, the S&P 500 held support at the 50-dma and rallied back into the previous trading range. Importantly, we have been focusing on the Nasdaq and building an index trading position over the last few trading days for a rotation from the “reflation” trade back to the “growth” trade.

On Wednesday, the Nasdaq triggered its short-term “buy signal,” which will likely provide some relative outperformance over the S&P 500. It will be important for the Nasdaq to hold above the 50-dma into next week. If we do get some follow-through, the Nasdaq should get a confirming MACD buy signal as well (bottom panel).

As noted last week, the following statement remains very important:

“We will hold exposures at current levels for now. However, instead of looking for a more extended rally into mid-summer, we suspect this rally will be fairly short-lived.”

We do expect a counter-trend rally due to the liquidations occurring by institutional investors over the previous few weeks. Over the last few weeks, we continue to build the case of a deeper (5-10%) correction by mid-summer.

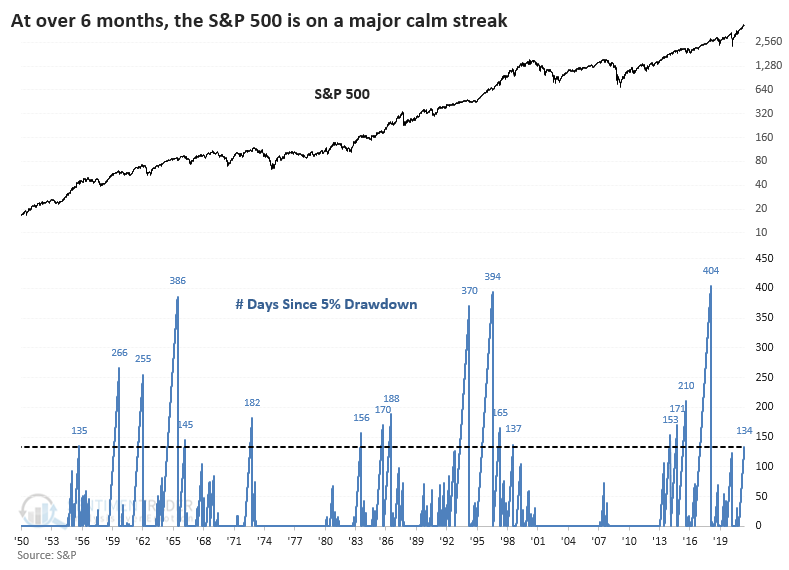

A Long Time

That view has not changed, particularly given the length of time without one. As noted recently by Sentiment Trader:

“The S&P 500 has gone 134 trading days without even a 5% pullback from a high. That’s among the longest streaks since 1928, and preceded choppy medium-term returns before momentum tended to resume.”

While we are adding exposure, we are not getting overly aggressive. The risk of a more significant drawdown outweighs the reward longer-term, but we are willing to trade short-term opportunities.

For more discussion and detail on why this is a 3-4 week trade, watch Thursday’s “3-Minutes” video.

Fed Starts To Talk Taper

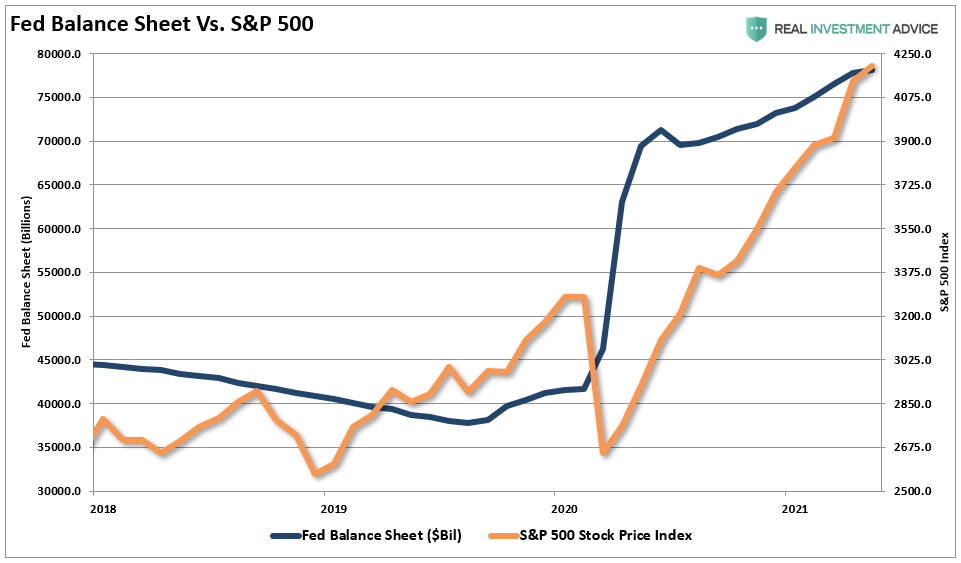

The general premise of “bullish investors” is that as long as the Fed is pumping money into the markets, you have to “buy stocks.” As we discussed in “The Market Will Reach 4500,” that has been the right call.

“The correlation between the Fed’s monetary interventions and the stock market is evident. The increase in the Fed’s balance sheet remains in near lockstep with the stock market’s climb.”

Of course, you should also not the period of somewhat volatile and ZERO return from 2018 through March 2020, as the Fed tapered their balance sheet.

The Fed currently purchases $120 billion a month in Treasury and Mortgage Back securities, which has inflated both an equity and housing bubble. However, given the rapid economic recovery and rising inflationary pressures, the Fed is now setting the table for the “T” word. The following are two excerpts from the recent Fed minutes.

“A number of participants suggested that if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.”

Such is important because they also realize they are responsible for elevated asset valuations.

“Regarding asset valuations, several participants noted that risk appetite in capital markets was elevated, as equity valuations had risen further, IPO activity remained high, and risk spreads on corporate bonds were at the bottom of their historical distribution.”

Let’s focus on the last sentence.

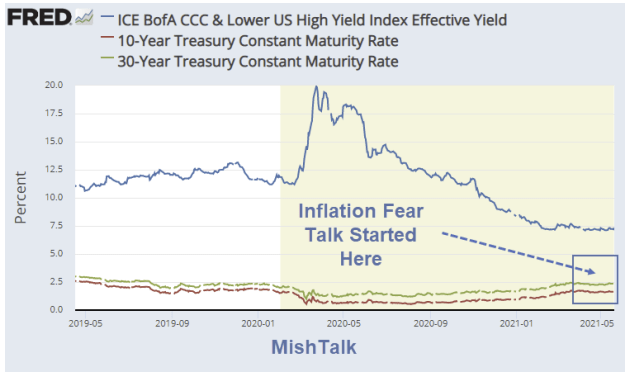

Risk Is Elevated

The most considerable risk to the “equity markets” is always a “credit-related event.” When credit stops flowing, for any reason, the resulting liquidation spreads across every market as the scramble for safety begins.

Mish Shedlock had an excellent note out on this issue this week.

“‘When I look at CCC’s rallying so hard — even if the default rates are at the low end of historical average — your chances of making money over the long run aren’t great. You’d be lucky to break even.’ – John Hussman”

Of course, CCC-rated bonds are just one step above bonds that are already in default. Yet, as Mike notes, there is “no fear” of default from bonds that historically have a very high propensity to default.

With the Fed likely on the verge of tapering, interest rates rising, and economic growth slowing later in the year, the risk of a credit-related event has increased markedly. While the media is busy focusing on “inflation,” which “will be transitory,” the credit market is the “monster under the bed.”

“I do believe fear is on the horizon. But it is not fear of inflation. Rather it is fear of paying too much for junk bonds, too much for stocks, and too much for cryptos, most of the latter will be worthless.

Writers, no doubt, will blame it on fear of inflation. That’s the excuse of the day instead of blaming the Fed with help from Congress for another huge set of bubbles.” – Mish Shedlock

Such is why understanding where you are in the current cycle is so crucial to long-term outcomes. Crashes matter and they matter a lot.

The next crash will be caused by the Fed once again. The only question is when.

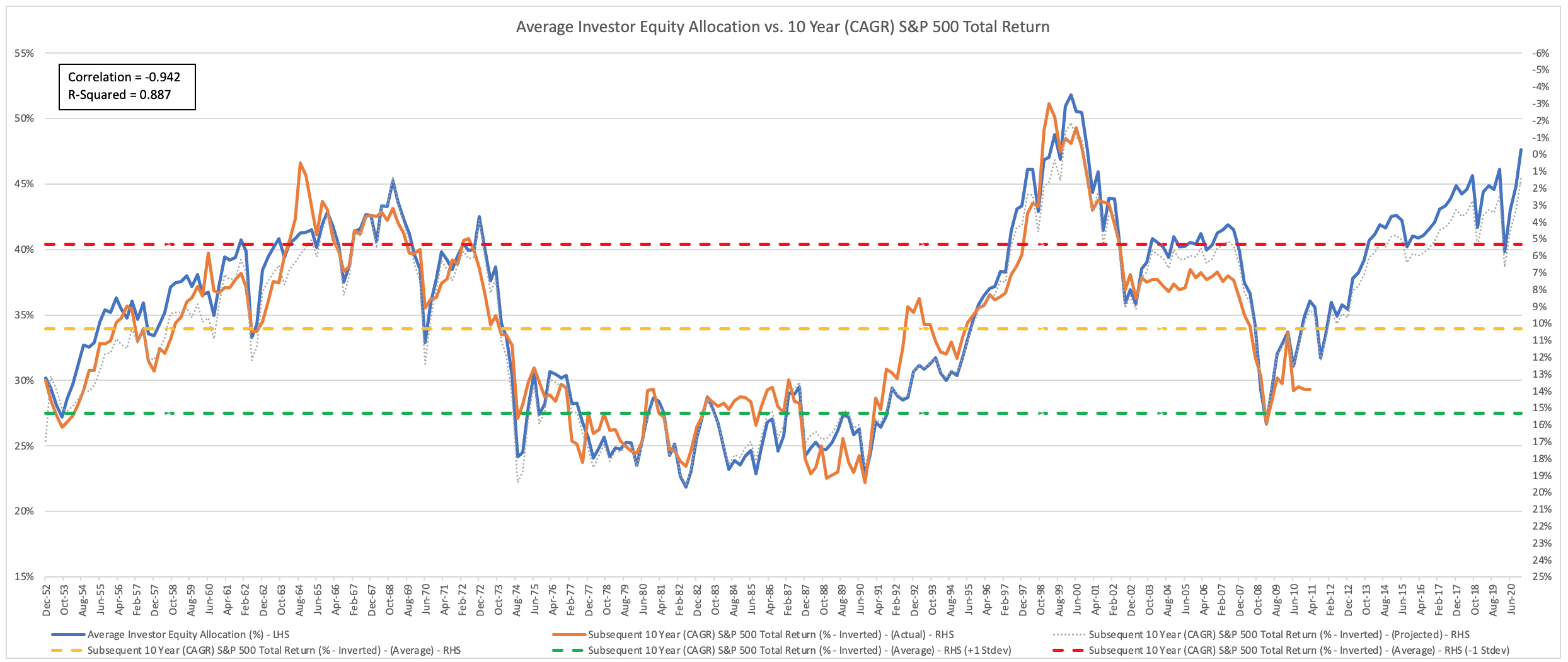

It Matters When You Start

My colleague, CEO of Armor ETF’s, emailed me recently a vital point.

“There are two critical points that investors fail to understand: 1) it matters when you start and 2) losses matter because they take time to recoup the loss.

When it comes to investing, time can be your biggest enemy or your biggest beneficiary depending upon where you are (i.e. 20-year-old beginning investing journey vs. 60-year-old looking to retire in the next 5-10 years).” – Jim Colquitt

The chart below shows forward 10-year total forward returns versus starting equity allocation levels. The returns (CAGR) for the next 10-years should be around 0% (note the r-squared).

He is correct.

Let me explain. (The following is an excerpt from an upcoming article.)

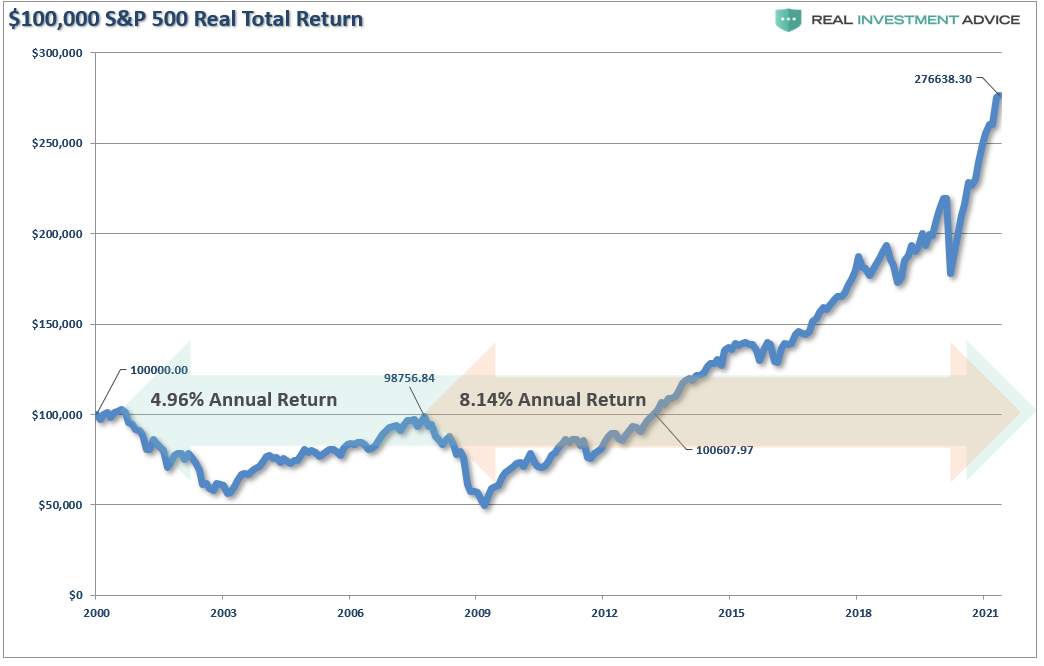

Crashes Matter

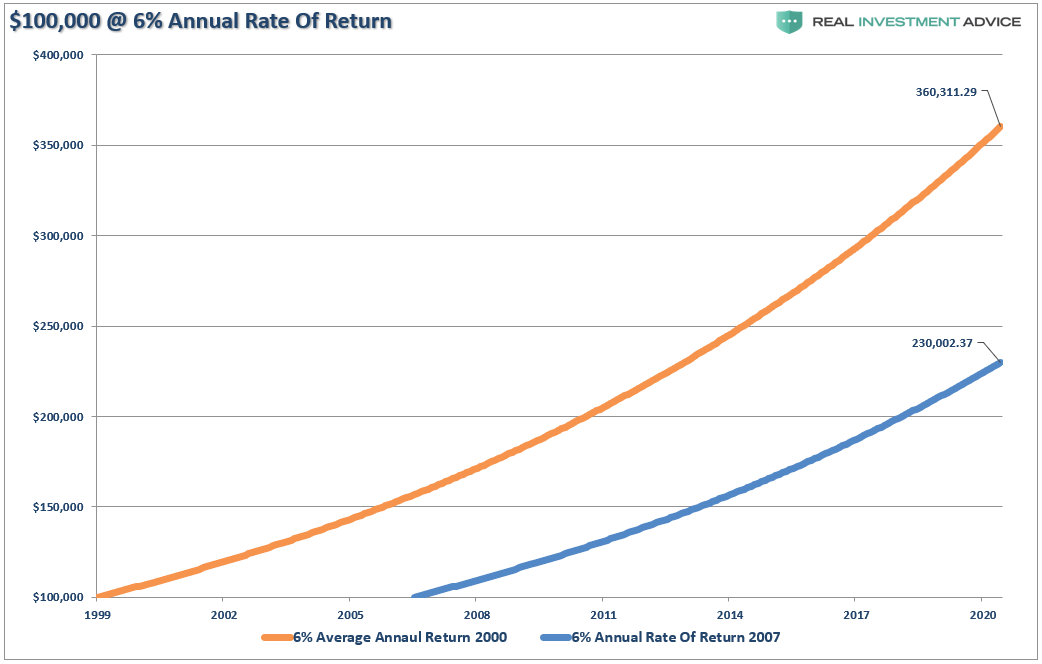

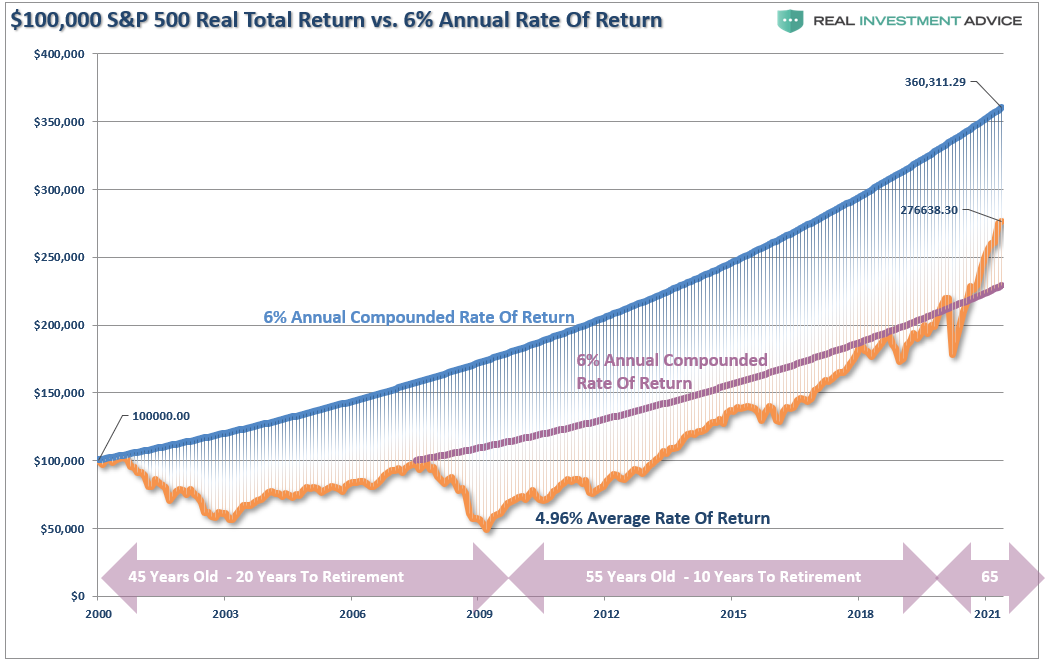

Financial advisors regularly tell clients that since the market grew 6% annually since 1900. Therefore, that is what returns will be in the future. The chart below shows $100,000 invested at 6% annually from 2000 or 2007.

Unfortunately, it didn’t work out that way.

During the past 20-years, the annual return for stocks has been just 4.96% annualized. Since the peak of 2007, returns have annualized roughly 8.14%. Over the next decade, current valuations suggest average returns will return to 2% or less.

For boomers who start in 2000, whose financial plans assume high return rates to offset a savings shortfall, they are now well short of their retirement goals. For those who started in 2007 they finally got back on track this year. The question is can they keep it?

Unfortunately, investment returns are far worse, as a vast majority of the fully invested individuals in 2007 sold out of the market by the end of 2008. It took years before they returned to the market. As such, actual returns are vastly different than what the index suggests.

Here is the sequence of events by age:

- 30’s: In 1980, the “baby boomer” generation is working, saving, and investing during the ’80-’90s bull market.

- 50’s: From 2000 to 2002, the “Dot.Com” crash cuts investments by 50%.

- 53-57: From 2003-2007, the market grows savings back to breakeven.

- 57-58: The 2008 “Financial Crisis” wipes out 100% of the gains of the previous bull market and resets savings values back to 1995 levels.

- 58-63: From 2009-2013, financial markets rose, growing savings back to levels seen in 2000.

- 63-71: In 2021, investors finally made some progress towards their retirement goals.

Today, for most individuals heading into retirement, the importance of “mean-reverting events” should not be dismissed.

Portfolio Update

We made few changes to the portfolio, except for adding to our QQQ index trading position. While we seek to take advantage of a short-term oversold condition, we remain focused on long-term risk.

Such brings up some essential investment guidelines as we head into the unknown.

- Investing is not a competition. There are no prizes for winning but there are severe penalties for losing.

- Emotions have no place in investing.You are generally better off doing the opposite of what you “feel” you should be doing.

- The ONLY investments that you can “buy and hold” are those that provide an income stream with a return of principal function.

- Market valuations (except at extremes) are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading. Knowing what type of investor you are determines the basis of your strategy.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

The one lesson you should have learned in 2020?

“The unexpected outcome occurs more often than you expect.”

Remember, it doesn’t matter if you underperform the index on the way up. The key is not “outperforming” the index on the way down.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

S&P 500 Tear Sheet

Performance Analysis

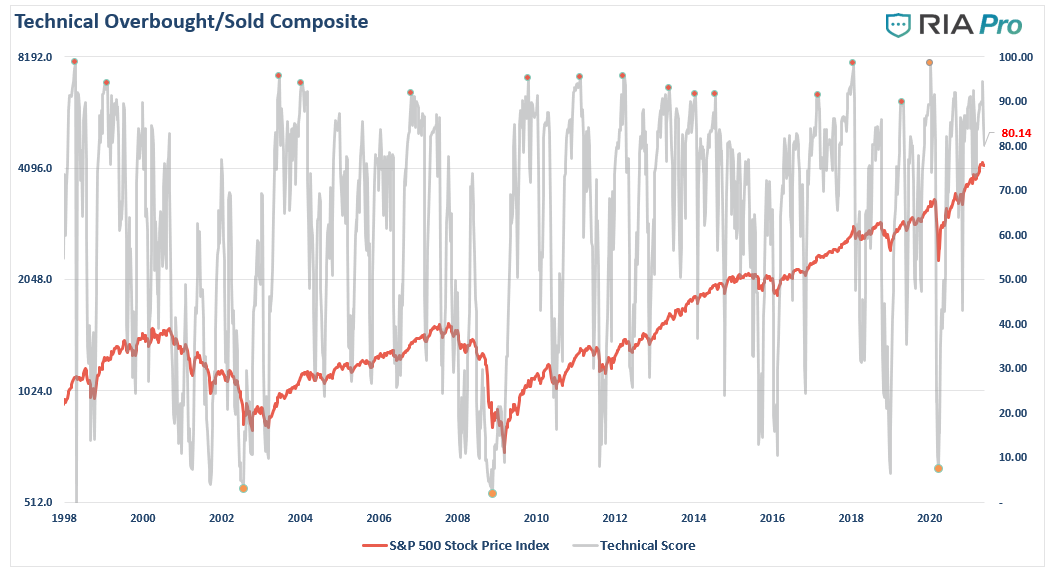

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” is oversold. The current reading is 84.70 out of a possible 100.

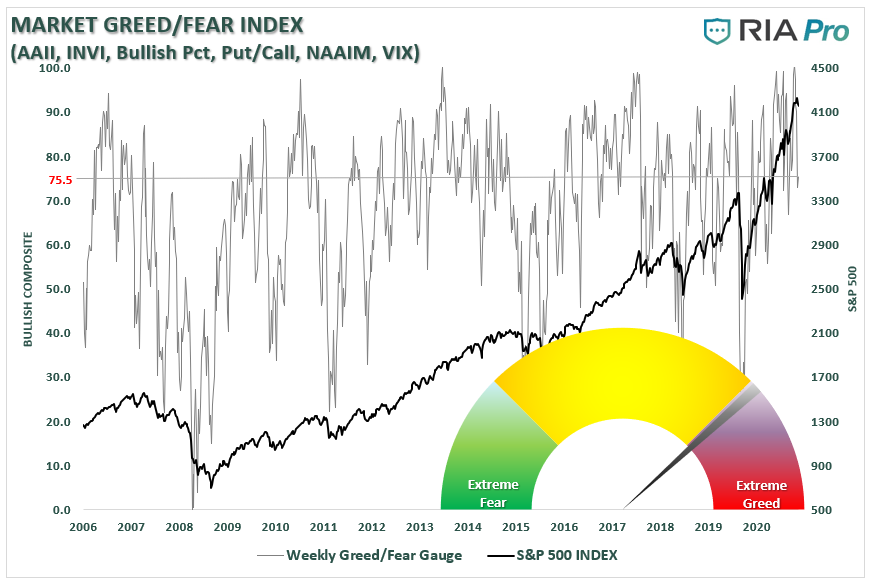

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 75.5 out of a possible 100.

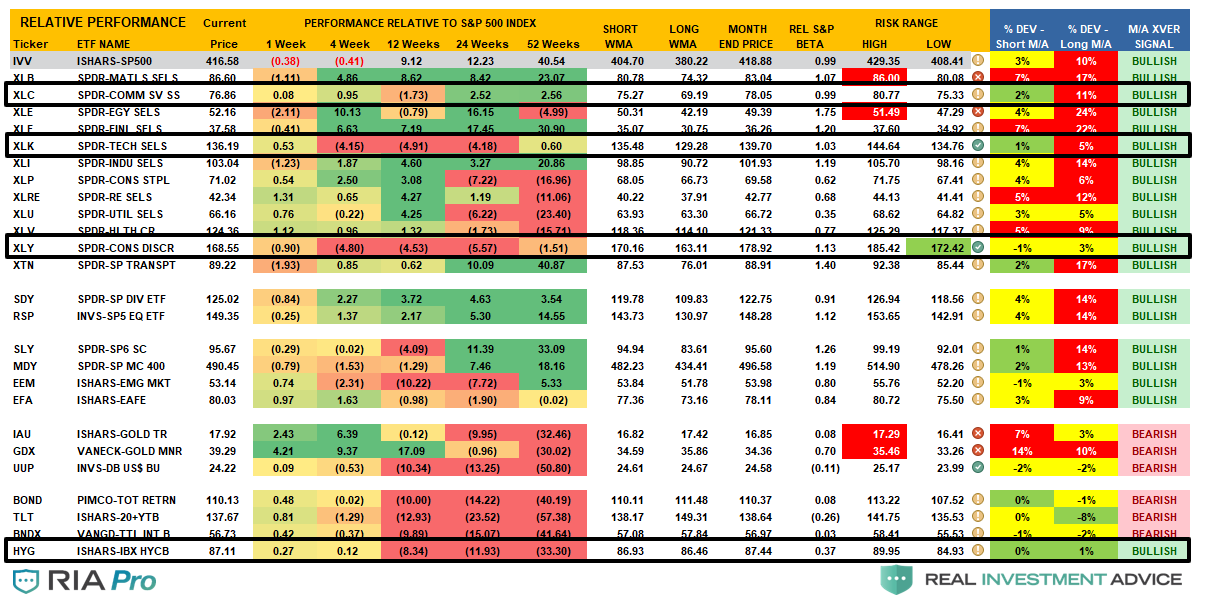

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market.

- Table shows the price deviation above and below the weekly moving averages.

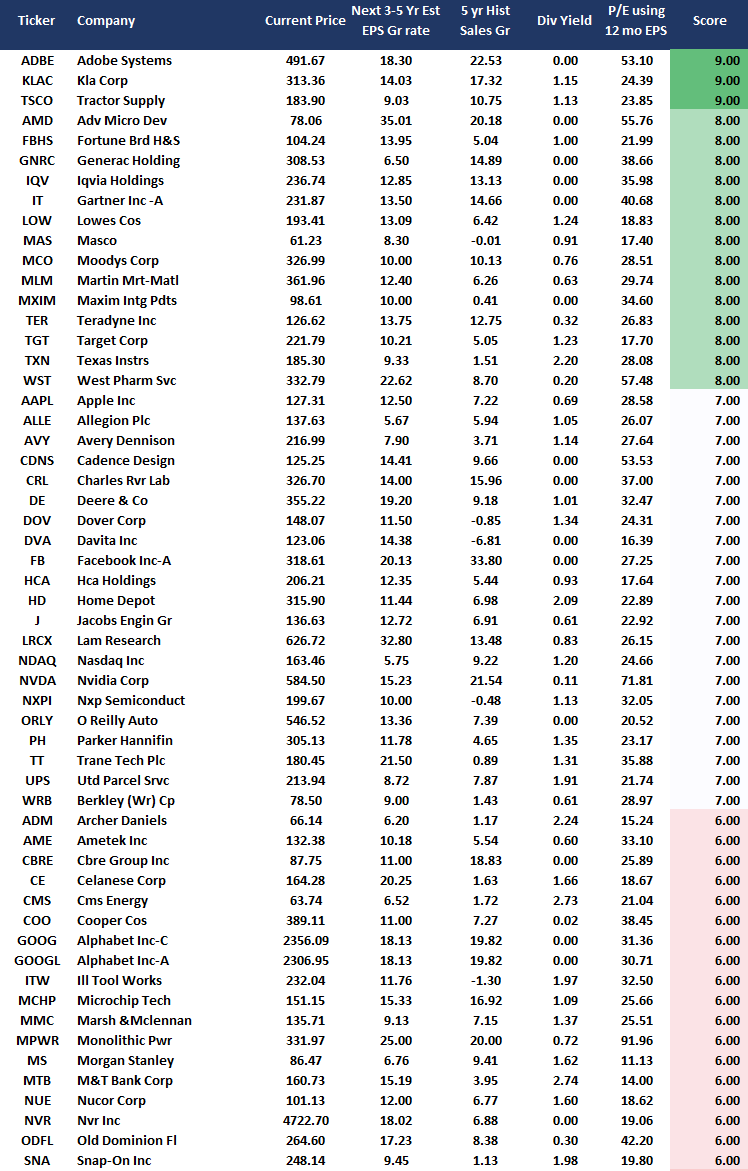

Weekly Stock Screens

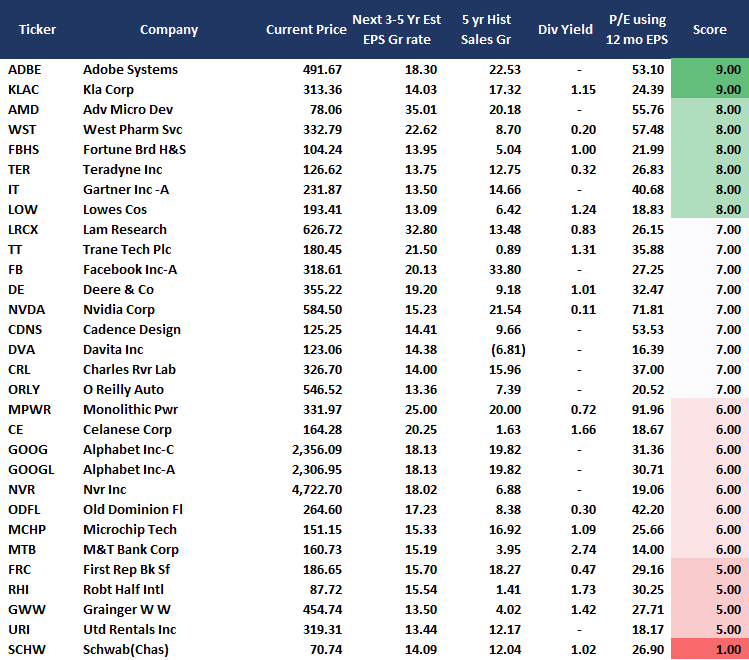

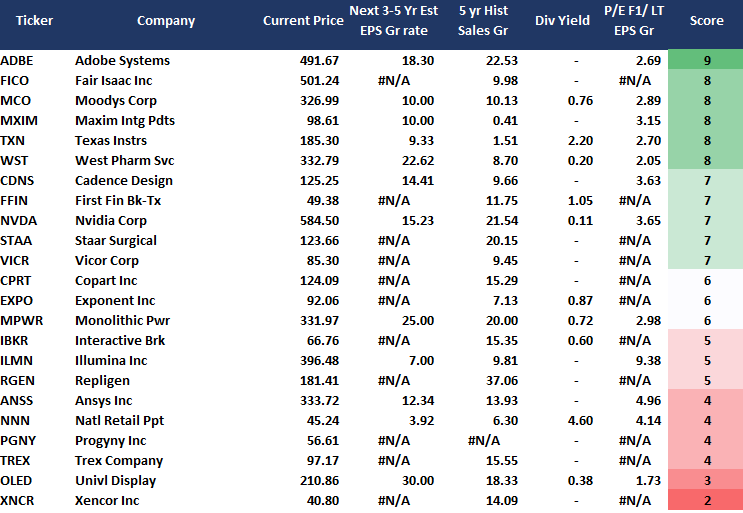

Currently, there are four different stock screens for you to review. The first is S&P 500 based companies with a “Growth” focus, the second is a “Value” screen on the entire universe of stocks, and the last are stocks that are “Technically” strong and breaking above their respective 50-dma.

We have provided the yield of each security and a Piotroski Score ranking to help you find fundamentally strong companies on each screen. (For more on the Piotroski Score – read this report.)

S&P 500 Growth Screen

Low P/B, High-Value Score, High Dividend Screen

Fundamental Growth Screen

Aggressive Growth Strategy

Portfolio / Client Update

We discussed that our “money-flow” indicators were back to more oversold levels during the last couple of weeks. Such suggested the recent bout of selling was likely concluding. Therefore, we have slowly added an index trading position (QQQ) to portfolios for a trading opportunity over the next few weeks.

However, it is essential to note this is just a “short-term” trade, and we will be selling the position once the money-flow indicators return to the top of their historical ranges. At that juncture will also look to reduce overall exposure to the portfolio as we expect to see a peak in economic and earnings growth.

Furthermore, let me repeat from last week:

“Nonetheless, we continue to make minor tweaks to portfolios to adjust allocations and rebalance risks. Our short-term concern is the Fed “panics” and makes a mistake that shocks the market. It won’t be the first time it has happened and is always unexpected.”

With the Fed now discussing the potential of “tapering” asset purchases in the future, such will be the start of the “clock ticking.” However, that is a concern for later.

In the meantime, we continue with our game plan and continue to focus on risk controls.

Portfolio Changes

During the past week, we made minor changes to portfolios. We post all trades in real-time at RIAPRO.NET.

*** Trading Update – Equity and Sector Models ***

“We added 1% to Ford (F) increasing our total position to 3%. The stock broke out of its previous downtrend and pushed above the 50-dma. We expect that at some point, the company will re-establish its dividend which will help total returns in the future. For now, it is a trading position until that transition occurs.” – 05/20/21

Equity & ETF Models

- Add 1% of the portfolio into F increasing total weighting to 3%.

“In both models we added 2.5% of TLT and 1% QQQ, bringing QQQ up to 4%. We are adding TLT in part for technical reasons as it’s very close to its 200 dma and getting ready to turn up on a money signal. Further, it may provide a little insurance if the recent downtrend in equities continues.” – 05/19/21

Equity & ETF Models

- Initiate a 2.5% position in TLT

- Add 1% of the portfolio into QQQ, increasing total weighting to 4%.

“We trimmed back CVS to model weight into the market close today (2% of the portfolio) after a big move higher. We still like the position longer-term on a fundamental basis but it needs a correction to add to the position.” – 05/18/21

Equity Model

- Reduce CVS to 2% of the portfolio

As always, our short-term concern remains the protection of your portfolio. We have shifted our focus from the election back to the economic recovery and where we go from here.

Lance Roberts

CIO

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert, do not hesitate to contact me.

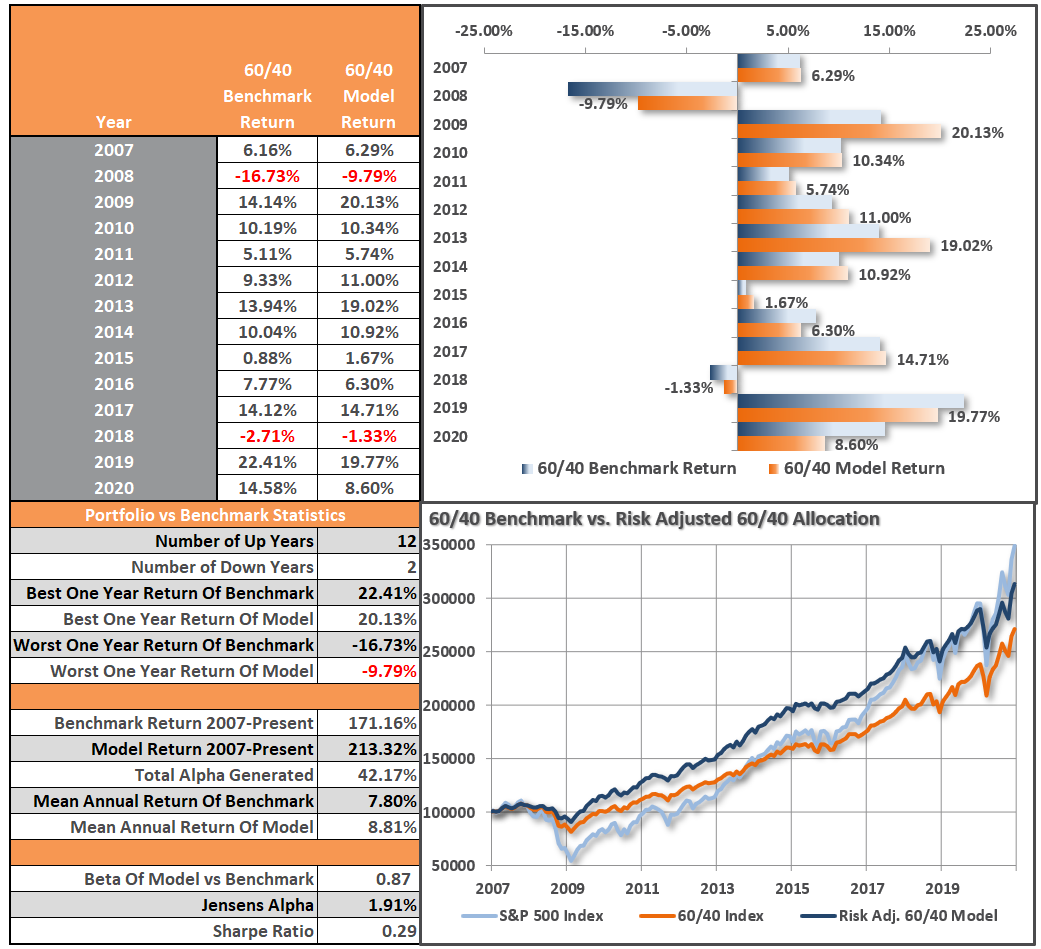

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

Have a great week!

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read