In this issue of “Winter Is Coming. Is It Time For Value To Shine?”

- Market Is At Technical Extremes

- More Signs Of Exuberance

- Is There A Rotation To Value Coming.

- Winter Is Coming

- MacroView: March Was A Correction

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

We Need You To Manage Our Growth.

Are you a strong advisor who wants to grow your practice? We need partners we can work with to manage our lead flow. If you are ready to move your practice forward, we would love to talk.

Catch Up On What You Missed Last Week

Bulls Breakout To New Highs

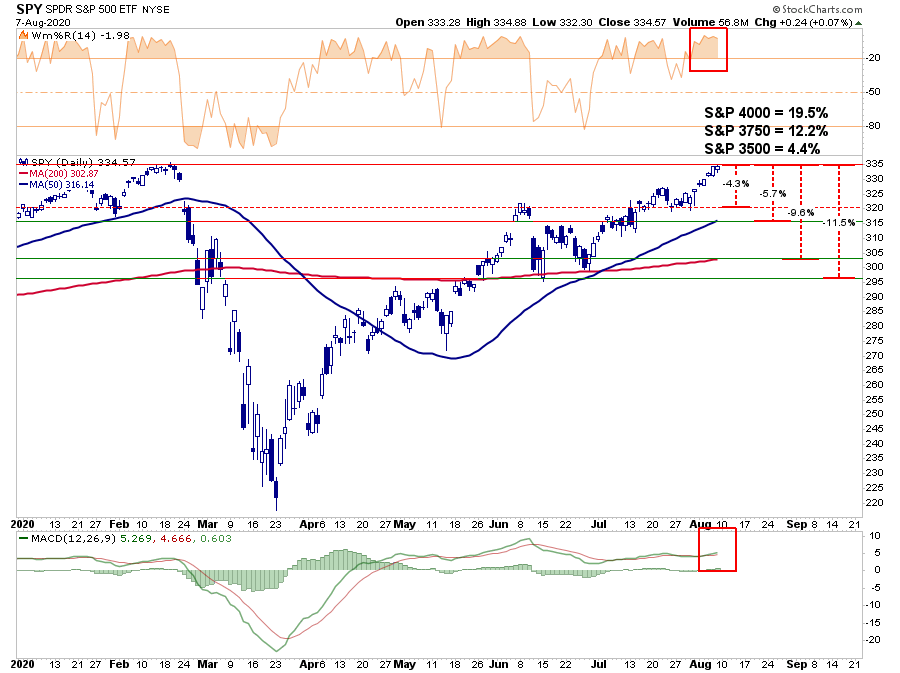

A couple of weeks ago, I wrote a wildly unpopular article laying out why, if the bulls could push the markets to new all-time highs, the next target would be 3750. With the market now at new all-time highs, and the bulls clearly in charge, is it “safe” for investors to become complacent? Maybe, not.

Technical analysis works well when there are defined “knowns” such as a previous top (resistance) or bottom (support) from which to build analysis. However, when markets break out to new highs, it pretty much becomes a “wild @$$ guess” or “WAG.”

However, we did previously attempt to establish some reasonable targets based on relative “risk/reward ranges,”

“With the markets closing just at all-time highs, we can only guess where the next market peak will be. Therefore, to gauge risk and reward ranges, we have set targets at 3500, 3750, and 4000 or 4.4%, 12.2%, and 19.5%, respectively.”

“Given there is no good measure to justify upside potential from a breakout to new highs, you can personally go through a lot of mental exercises. While there is certainly a potential the market could rally 19.9% to 4000, it is also just as reasonable the market could decline 22.2% test the March closing lows.

Just in case you think that can’t happen, just remember no one was expecting a 35% decline in March, either.”

We then delved into establishing a target using the well-established trendlines from the 2009 lows. Given these trendlines have held for over a decade, we can only reasonably assume they will hold in the future. Therefore, since the upper bullish trend line coincides with the February 2020 market peak and the polynomial trend line, 3750 is the next reasonable target.

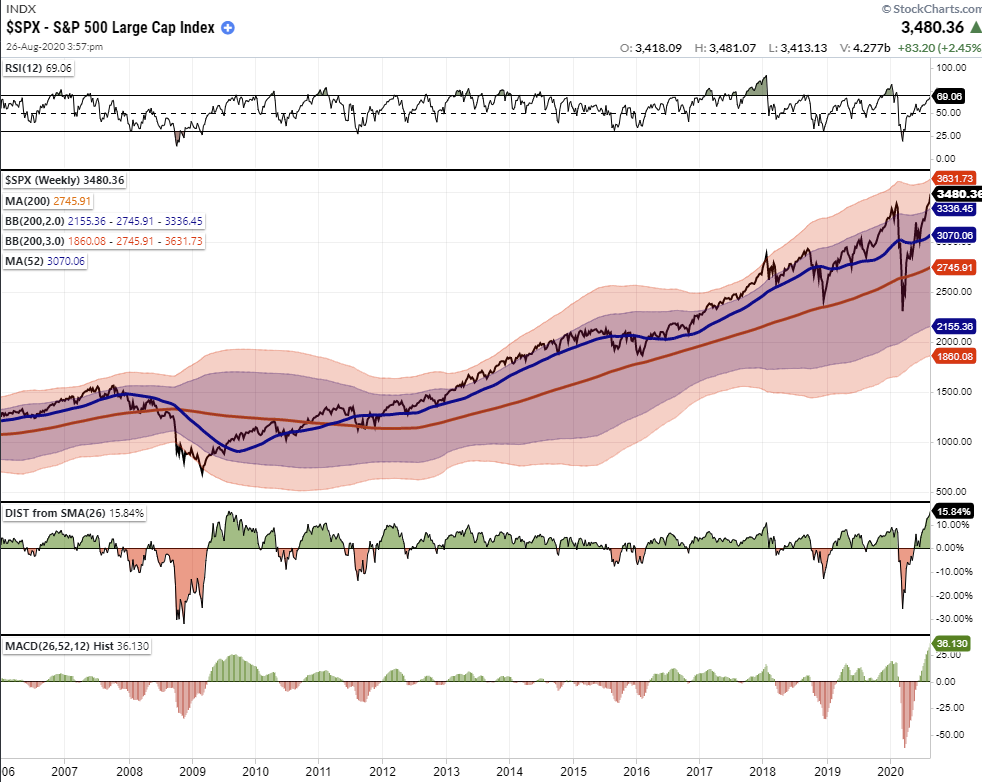

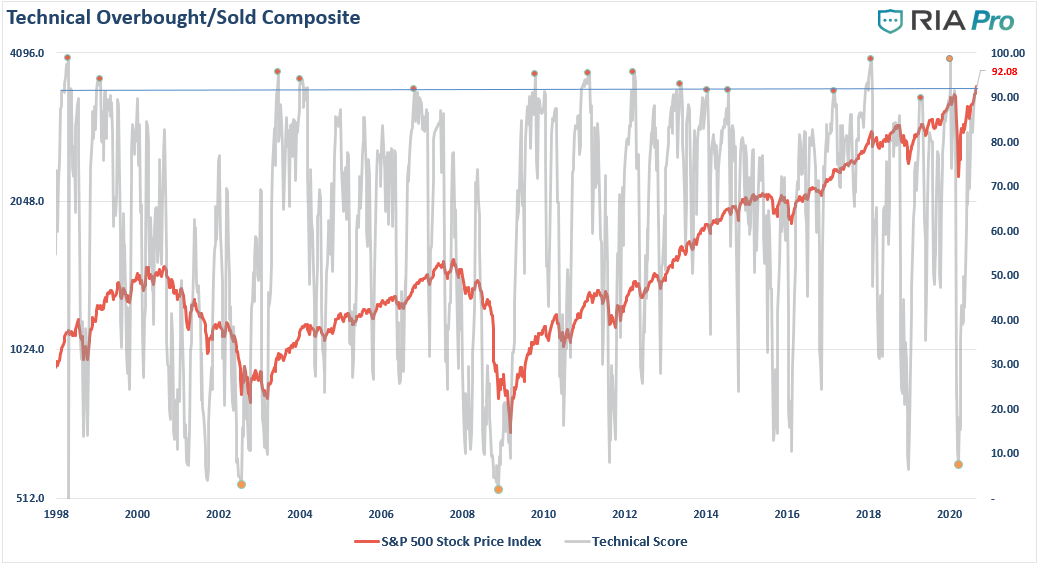

Markets At Technical Extremes

The markets currently are at historic market extremes. I explained this concept in much more detail in today’s #Macroview.

However, the most critical point of that article was the extreme deviation from long-term means. As noted, trend lines and moving averages tend to act as “gravity.” The further away the market moves from the trendline, the greater the pull becomes.

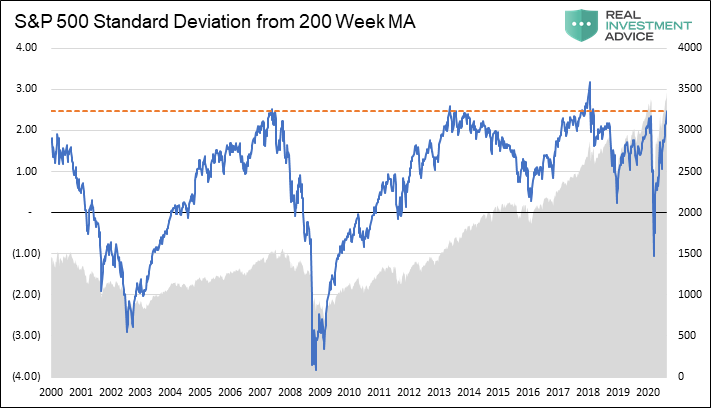

“Kyōki is the Japanese word for “insanity.” That was the word that came to mind when my co-portfolio manager, Michael Lebowitz, emailed me the following chart.”

“The chart is WEEKLY data, which smooths out some of the short-term volatility. What is displayed is the standard deviation of the market from its 200-WEEK (4-year) moving average.

Notably, each time of the 5-times previously, going back to 1999, where the market traded at 2-standard deviations or higher from the 4-year moving average, a reversion occurred. Those periods were 2000, 2007, 2014, 2018, February 2020, and now.”

It is remarkable given the economic devastation; the S&P 500 is trading at not only at record highs, but at near-record deviations of the 4-year moving average and MACD readings. Historically, such deviations resolve through a correction or a full-fledged bear market.

Such is just statistical evidence of more extreme positioning by investors in the short-term. As I discussed in “Revisiting Bob Farrell’s 10 Investing Rules”:

“Like a rubber band that has been stretched too far – it must be relaxed in order to be stretched again. This is exactly the same for stock prices that are anchored to their moving averages. Trends that get overextended in one direction, or another, always return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average.”

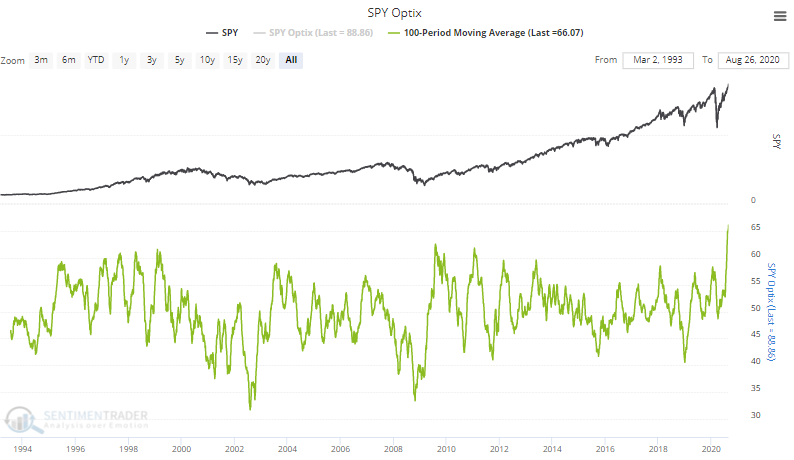

More Signs Of Exuberance

While prices are clearly at historic extremes on many levels, we continue to see more numerous indicators showing extreme signs of “exuberance” in the markets.

This tweet from Sentiment Trader summed it up best.

Speculative options trading reached the equivalent of 12% of NYSE volume last week.

Like some combustible combo of musical chairs, Russian roulette, and five finger fillet.

How many traders can dance upon the head of a pin? pic.twitter.com/nsCeyKH093

— SentimenTrader (@sentimentrader) August 29, 2020

As noted in the weekly charts above, the S&P is also trading at extreme levels above its shorter-term daily moving averages as well.

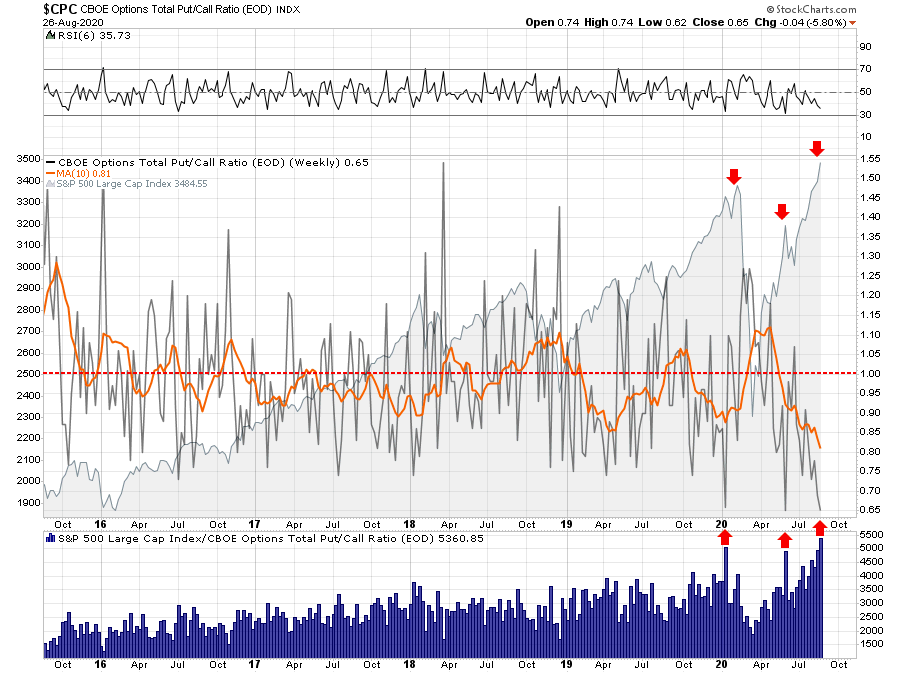

With “shorts” now at historically levels, market participants have given up hedging portfolios against a correction. Historically low put/call ratios have always coincided with short-term corrections or worse. It is one of the lowest levels since the peak of the market in 1999.

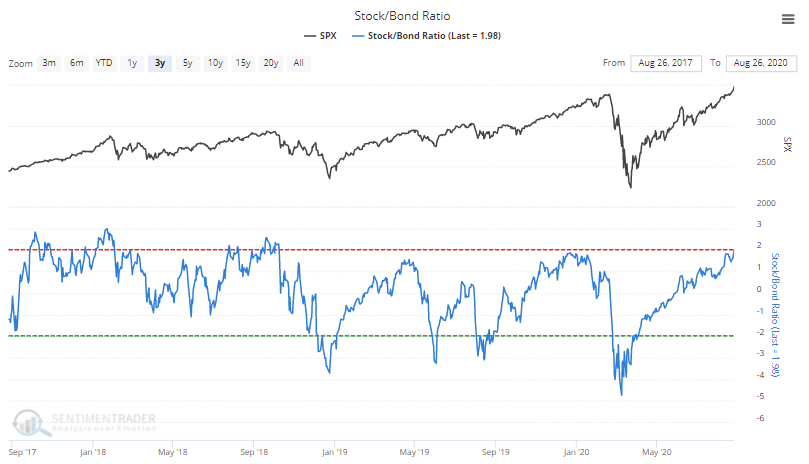

The stock/bond ratio has also reached levels more normally consistent with short-term market peaks and corrective actions.

The rise in the stock/bond ratio is not surprising, given the level of exuberance by retail investors.

None of this data means the market is about to crash.

What it does mean, as we discussed last week in “Winter Approaches,” is that a correction of 5-10% has become increasingly likely over the next few weeks to two months. While a 5-10% correction may not seem like much, it will feel much worse due to the high level of complacency by investors currently.

All of the data suggests that “Winter Is Coming.” Therefore, this is why we are adding “value” to our portfolios to prepare for colder weather.

Is There A Rotation To Value Coming

Why value?

As Michael Lebowitz, CFA previously noted:

“As a result of these behaviors, we have witnessed a divergence in what has historically spelled success for investors. Stronger companies with predictable income generation and solid balance sheets have grossly underperformed companies with unreliable earnings and over-burdened balance sheets. The prospect of majestic future growth has trumped dependable growth. Companies with little to no income and massive debts have been the winners.”

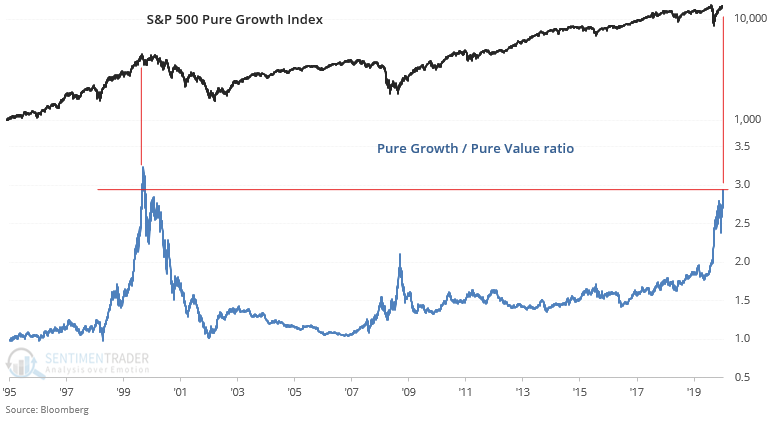

This underperformance of “value” relative to “growth” is not unique. What is unusual is the current duration and magnitude of that underperformance. Such underperformance was only seen previously in 1999-2000.

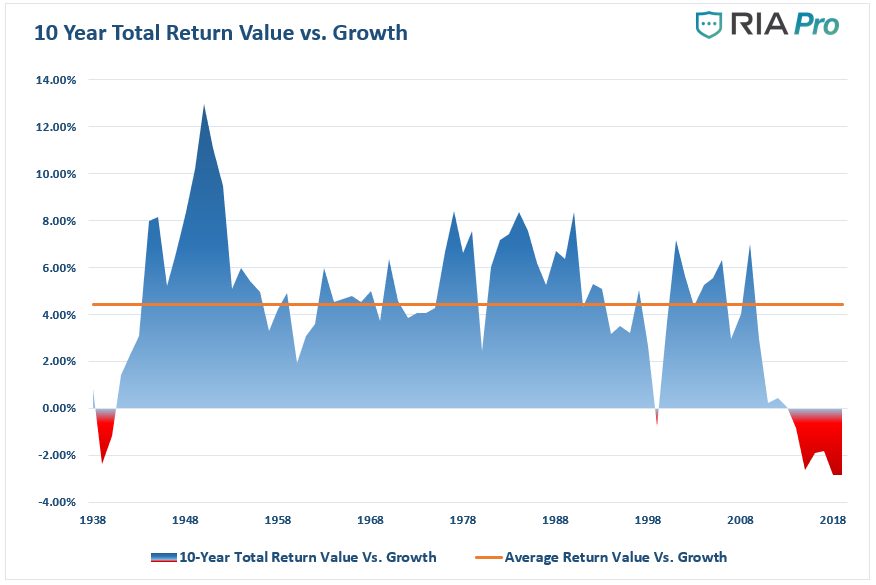

10-Year Total-Return Failure

The graph below charts ten-year annualized total returns (dividends included) for value stocks versus growth stocks. The most recent data point representing 2019, covering the years 2009 through 2019, stands at negative 2.86%. Such indicates value stocks have underperformed growth stocks by 2.86% on average in each of the last ten years.

The data for this analysis comes from Kenneth French and Dartmouth University.

There are two critical takeaways from the graph above:

- Over the last 90 years, value stocks have outperformed growth stocks by an average of 4.44% per year (orange line).

- There have only been eight ten-year periods over the last 90 years (total of 90 ten-year periods) when value stocks underperformed growth stocks. Two of these occurred during the Great Depression, and the other spanned the 1990s leading into the Tech bust of 2001. The other five are recent, representing the years 2014 through 2019.

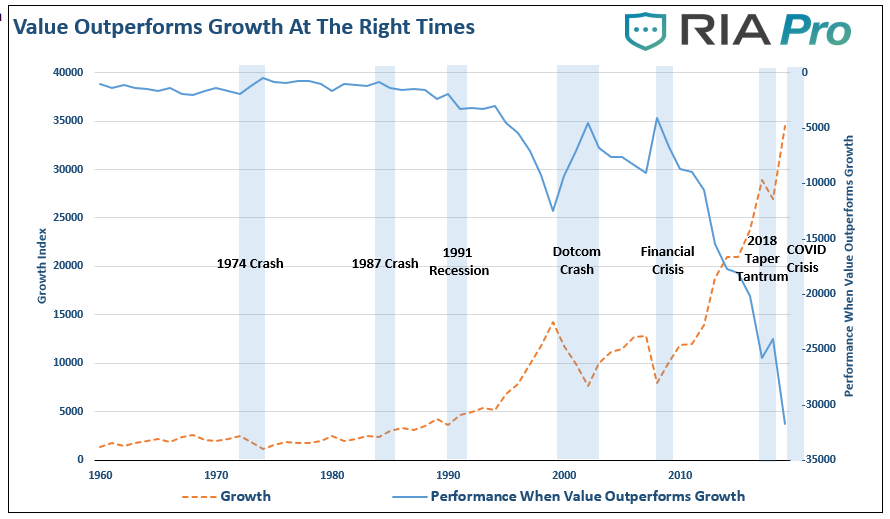

Mirror Opposites

The chart shows the difference in the performance of the “value vs. growth” index. The value and growth indices are each based on a $100 investment. While value investing always provides consistent returns, there are times when growth outperforms value. The periods when “value investing” has the most significant outperformance, as noted by the “blue shaded” areas, are notable.

The question is, what are the causes of this underperformance, and eventually, outperformance.

Reasons For Under-performance

As Research Affiliates noted:

“The Fama–French value factor, and value investing in general, has suffered an extraordinarily long 13.3 years of underperformance relative to the growth investing style. The current drawdown has been by far the longest as well as the largest since July 1963.

An investment strategy, style, or factor can suffer a period of underperformance for many reasons.

- First, the style may have been a product of data mining, only working during its backtest because of overfitting.

- Second, structural changes in the market could render the factor newly irrelevant.

- Third, the trade can get crowded, leading to distorted prices and low or negative expected returns.

- Fourth, recent performance may disappoint because the style or factor is becoming cheaper as it plumbs new lows in relative valuation.

- Finally, flagging performance might be a result of a left-tail outlier or pure bad luck.

If the first three reasons imply the style no longer works, and will not likely benefit investors in the future, the last two reasons have no such implications.

With today’s value vs. growth valuation gap at an extreme (the 100th percentile of historical relative valuations), it sets the stage for a potentially historic outperformance of value relative to growth over the coming decade.”

The reasons for underperformance are also the reasons for potential outperformance in the future. When something in the market ultimately goes “pear-shaped,” the return to value tends to be a swift event.

Such is the reason we are starting to add value to our portfolio. When “winter comes,” we have little doubt the value-growth relationship will revert to its long-term mean.

Our college recently penned a similar report for our RIAPro Subscribers:

(This is unlocked content usually reserved for RIAPro Subscribers. Try RISK-FREE for 30-days.)

Be Careful Declaring Value Dead

While the current market advance seems to be unstoppable, such was always what investors believed at every prior market peak in history. As Howard Marks once stated:

“Rule No. 1: Most things will prove to be cyclical.

Rule No. 2: Some of the most exceptional opportunities for gain and loss come when other people forget Rule No. 1.”

The realization that nothing lasts forever is crucial to long term investing. To “buy low,” one must have first “sold high.” Understanding that all things are cyclical suggests that after significant price increases, investments become more prone to declines than further advances.

The rotation from “growth” to “value” is inevitable. It will occur against a backdrop of devastation for the majority of investors quietly lulled into the extreme sense of complacency years of monetary interventions have provided.

As Research Affiliates concludes:

“Overall, relative valuations are in the far tail of the historical distribution. If, as history suggests, there is any tendency for mean reversion, the expected future returns for value are elevated by almost any definition.”

The only question is whether you will be the buyer of “value” when everyone else is selling “growth?”

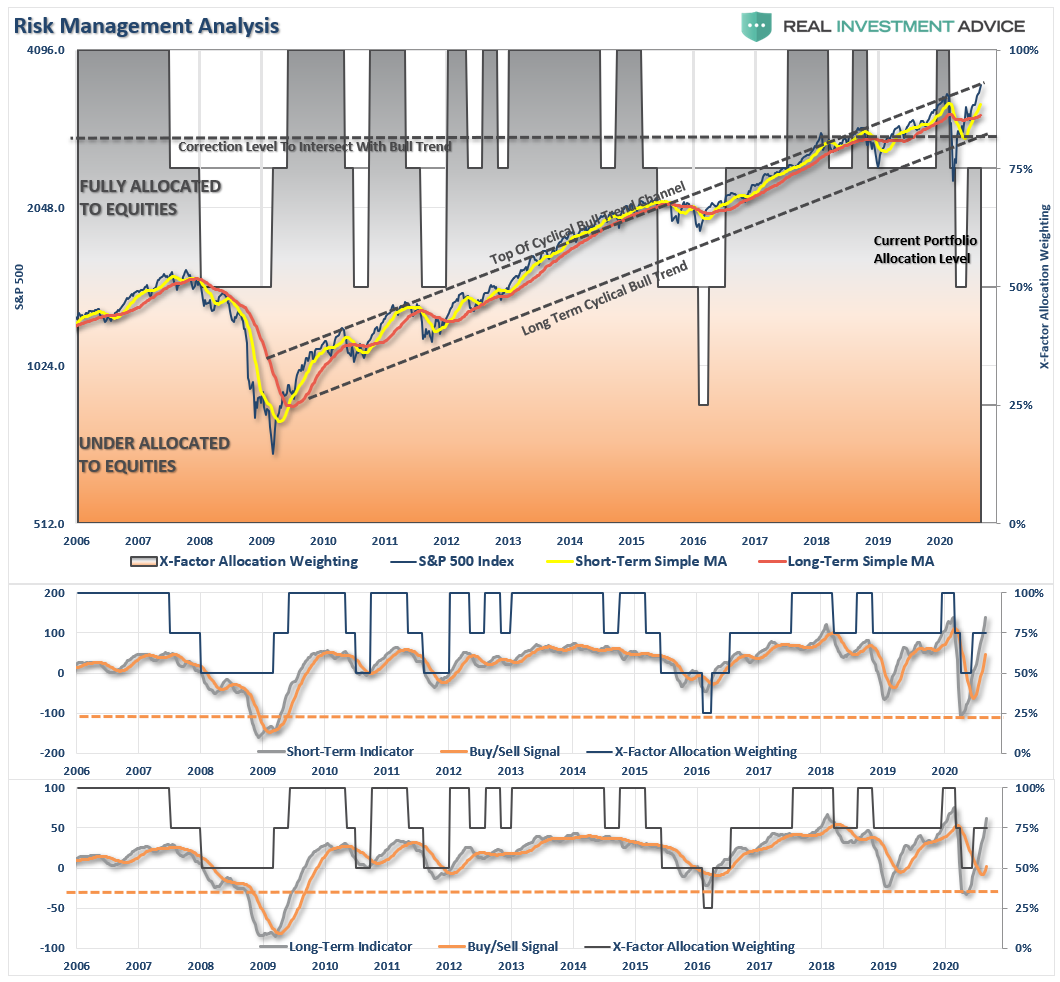

Portfolio Positioning

As we discussed last week in “Tending The Garden,” there is a good analogy between gardening and portfolio management. I put together a short video last week as a recap.

(We publish “3-Minutes” Monday-Thursday. Click here to subscribe to our YouTube channel for email notification of all of our video postings and live-streams.)

Such is where we are currently.

While we remain long-biased in our equity portfolios, we have begun to “harvest” some of our big winners (take profits), and do some “winter preparation” by adding to our defensive “value” oriented positions, and our risk hedges.

In the short-term, this will indeed provide some drag between our portfolio and the major market index. However, when the first “cold snap” washes across the markets, our preparation should protect our garden from “frostbite.”

We indeed remain “bullish” on the markets currently as momentum is still in play. However, just as any farmer is keenly aware of the signs “Winter” is approaching, we are just taking some precautionary actions. As noted last week:

“If you wait for the “blizzard” to hit, it will be too late to make much difference.”

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

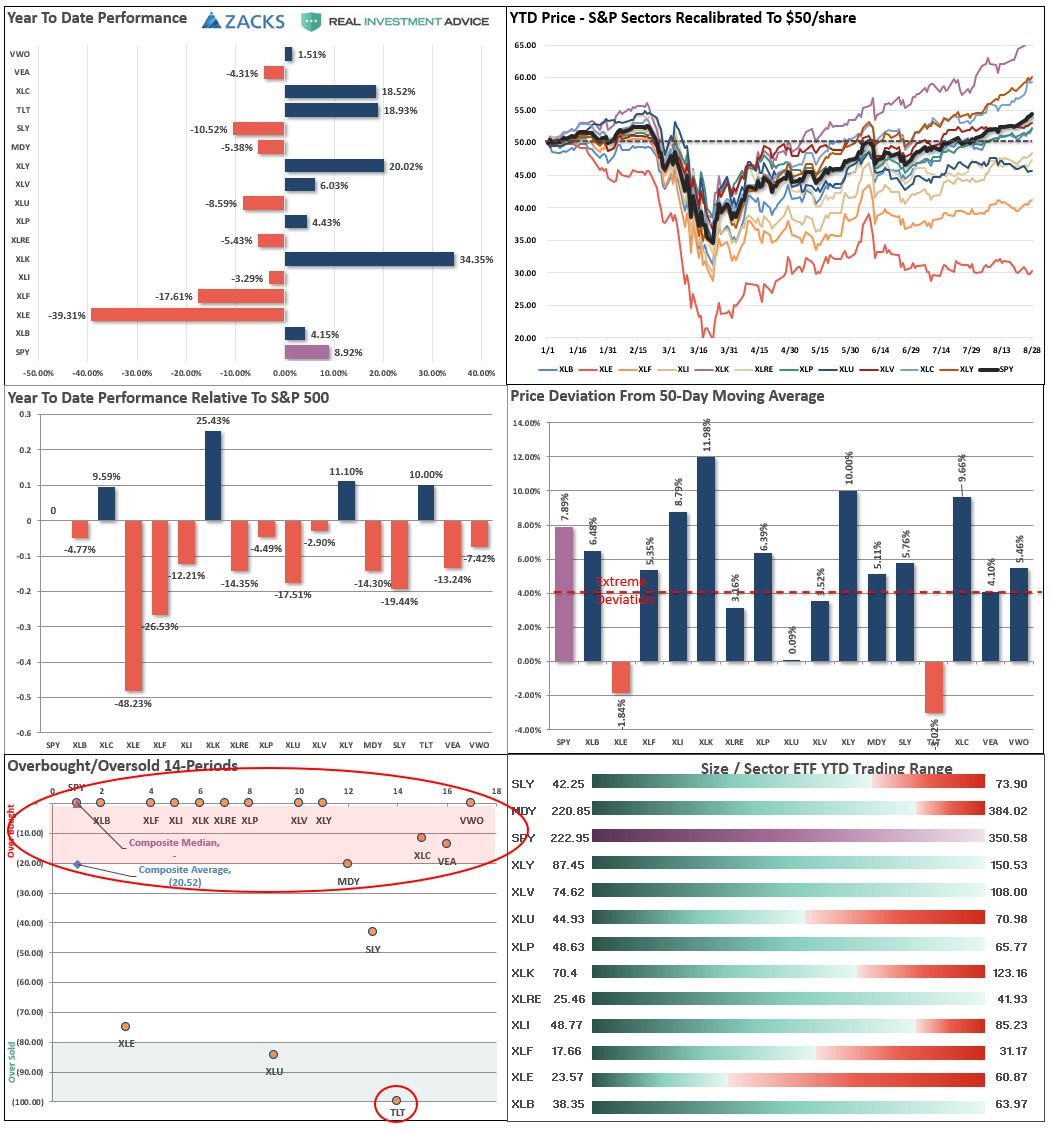

S&P 500 Tear Sheet

Performance Analysis

Technical Composite

Sector Model Analysis & Risk Ranges

How To Read.

- The table compares each sector and market to the S&P 500 index on relative performance.

- The “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market.

- The table shows the price deviation above and below the weekly moving averages.

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels.

Sector-by-Sector

Improving – Financials (XLF), and Industrials (XLI)

While Financials remain the improving quadrant, they are still vastly underperforming the market. Conversely, Industrials have broken above their 200-dma and are performing better. However, Industrials, like Financials, are very overbought and beginning to lag the overall market. We have taken profits twice now in Industrials and Transports.

Current Positions: XLI, IYT

Outperforming – Materials (XLB), and Discretionary (XLY)

Discretionary stocks have broken out to new highs and continue to perform well due primarily to AMZN. However, the sector is massively overbought, and a correction is will happen. Take profits, rebalance risk, and pay attention as economic weakness is beginning to resurface.

Current Positions: None

Weakening – Technology (XLK), and Communications (XLC)

Technology and Communications holdings have gone parabolic. We have previously taken profits, and late this past week, those sectors started to show more relative weakness. We have tight stops on our positions and are likely to reduce further soon. A correction is coming.

Current Position: XLK, XLC

Lagging – Energy (XLE), Healthcare (XLV), Utilities (XLU), Real Estate (XLRE), and Staples (XLP)

We have some minor holdings in two Energy-related names (XOM and CVX), which are holding support with a high dividend yield. However, the sector is underperforming for the time being, so we are not currently increasing exposure.

We continue to maintain our core defensive positions Healthcare, Staples, Utilities, and Real Estate. We are going to have to take profits in Staples soon, and are looking to add exposure to our defensive positions in Utilities and Real Estate for a market “risk-off” rotation.

Current Position: XLU, XLV, XLP

Market By Market

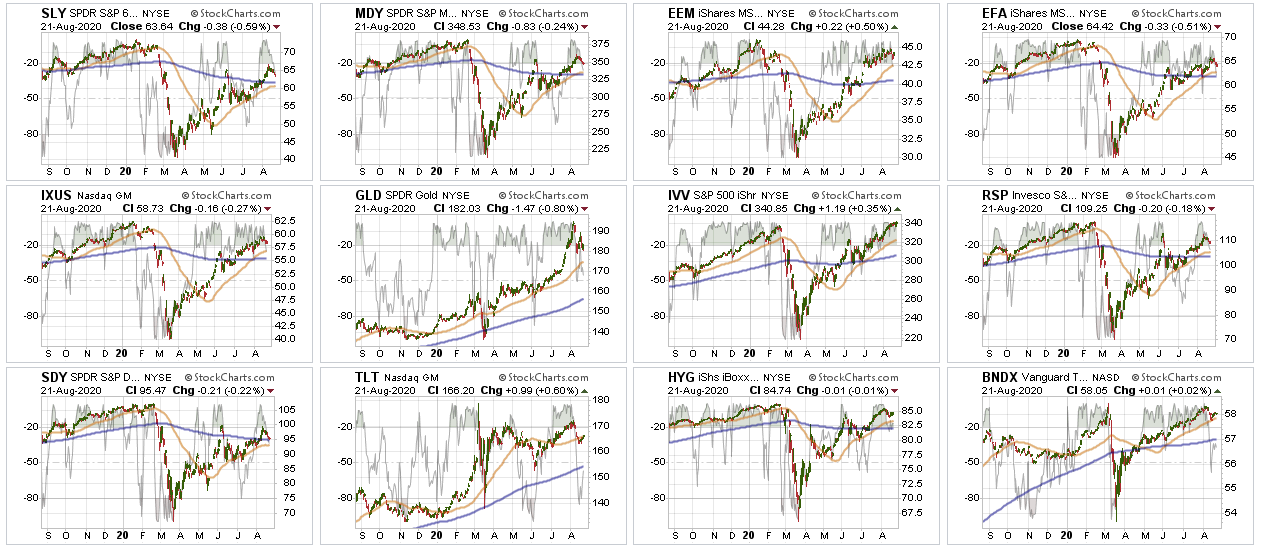

Small-Cap (SLY) and Mid Cap (MDY) – Both of these markets continue to underperform, and continued to struggle against the broader S&P and the mega-cap stock names. We suggested taking profits previously. If these markets can remain above critical support and work off the overbought condition, we may have a reasonable entry point to add exposure for a trade.

Current Position: None

Emerging, International (EEM) & Total International Markets (EFA)

Emerging and International Markets have performed better recently. We added a long-dollar hedge to our portfolios, which will weigh on international exposure. However, we will look to add international back to portfolios once the dollar reversal occurs.

Current Position: None

S&P 500 Index (Exposure/Trading Rentals) – We currently have no “core” holdings.

Current Position: None

Gold (GLD) – We added to our gold and gold miners position on Friday after we took profits previously. We are using Gold as a potential market hedge that should protect against a market decline. The Dollar is extremely oversold; we continue to hold our small UUP position to hedge downside risk in Gold.

Current Position: IAU, GDX, UUP

Bonds (TLT) –

We continue to hold our bond holdings as a hedge against market risk. However, those positions got oversold recently and should see a rebound in bond prices in the next two weeks. (Lower rates.)

Current Positions: TLT, MBB, & AGG

Portfolio / Client Update

As discussed last week, we are currently making changes to portfolios to become a bit more defensive. We have been adding “value” to the portfolio both for relative “safety” and “dividend yield.” As noted in this week’s newsletter, the deviations from long-term means are at extreme levels.

Over the next several weeks, or even a couple of months, the markets can certainly extend the current deviations from the long-term averages even further. But that is the nature of every bull market mania throughout history.

As Vitaliy Katsenelson once wrote:

“Our goal is to win a war, and to do that we may need to lose a few battles in the interim. Yes, we want to make money, but it is even more important not to lose it.”

In the short-term, we are willing to take some underperformance to hedge against a more significant decline. We have had requests to get more aggressive, and we will. We don’t want to get swept up into the mania and jeopardize your capital.

Unfortunately, most investors have very little understanding of the dynamics of markets and how prices are “ultimately bound by the laws of physics.” While prices can certainly seem to defy the law of gravity in the short-term, the subsequent reversion from extremes has repeatedly led to catastrophic losses for investors who disregard the risk.

In the market, there is no such thing as “bulls” or “bears.” For us, there is only ensuring your ability to reach your long-term goals.

If we lose too many soldiers trying to win a short-term battle, we will ultimately lose the war.

Portfolio Changes

In the equity model, we recently added a new value position in VIAC. This week, our analyst Nick Lane has provided updated analysis supporting our purchase.

As we have been discussing lately, we are making subtle changes to the portfolio to rebalance the risk profile to a more defensive allocation. With markets overbought, we are holding a bit of extra cash and, after taking profits previously, used the pullback in metals to add to Gold and Goldminers on Friday.

Equity & ETF Portfolios:

- Buy 1.00% IAU from 3.00% to 4.00%

- Buy 1.00% GDX from 1.00% to 2.00%

We continue to look for opportunities to abate risk, add return either in appreciation or income, and protect capital.

Please don’t hesitate to contact us if you have any questions or concerns.

Lance Roberts

CIO

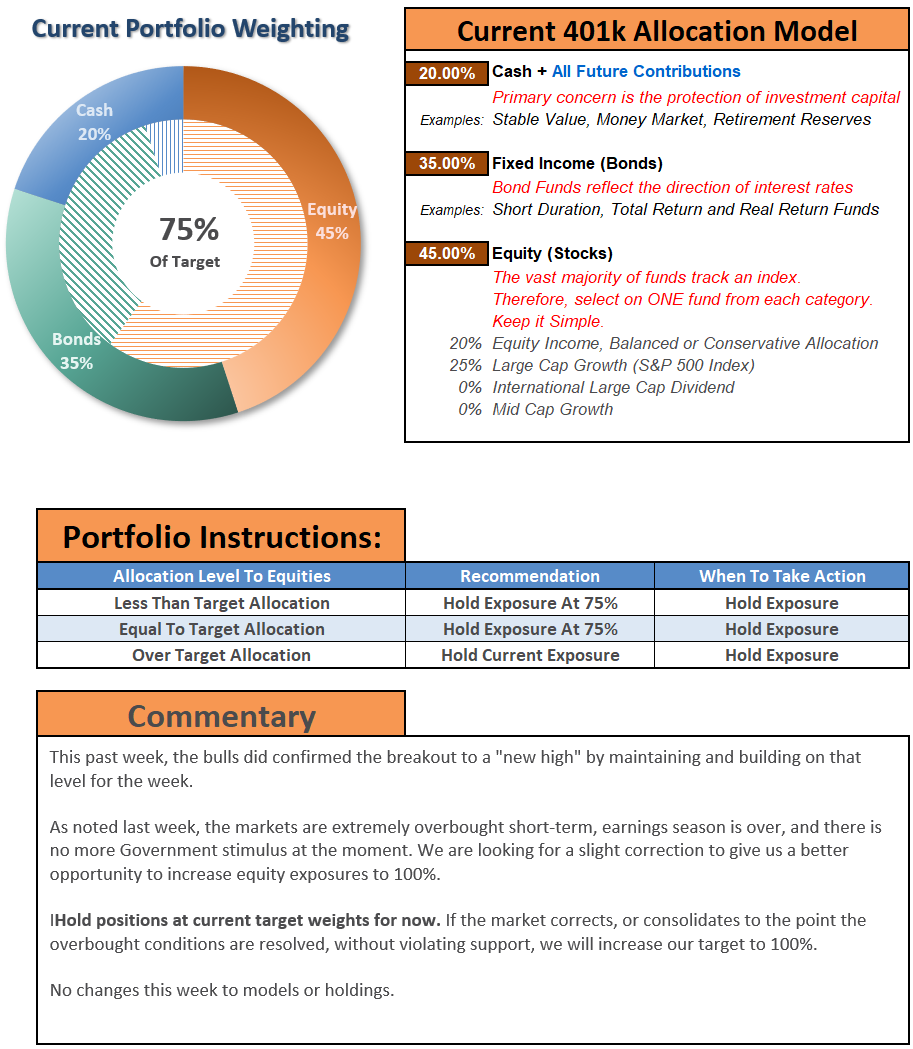

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert; do not hesitate to contact me

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free), you have access to our live 401k plan manager.

Compare your current 401k allocation, to our recommendation for your company-specific plan as well as our on 401k model allocation.

You can also track performance, estimate future values based on your savings and expected returns, and dig down into your sector and market allocations.

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read