In this issue of “Market Rallies On Powell’s Easy Money Promise.”

- Market Review And Update

- Powell’s “Easy Money” Promise

- Stock Buybacks Gone Wild

- Portfolio Positioning

- #MacroView: Could A Transaction Tax Be A Good Thing?

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

RIA Advisors Can Now Manage Your 401k Plan

Too many choices? Unsure of what funds to select? Need a strategy to protect your retirement plan from a market downturn?

RIA Advisors can now manage your 401k plan for you. It’s quick, simple, and transparent. In just a few minutes, we can get you in the “right lane” for retirement.

Catch Up On What You Missed Last Week

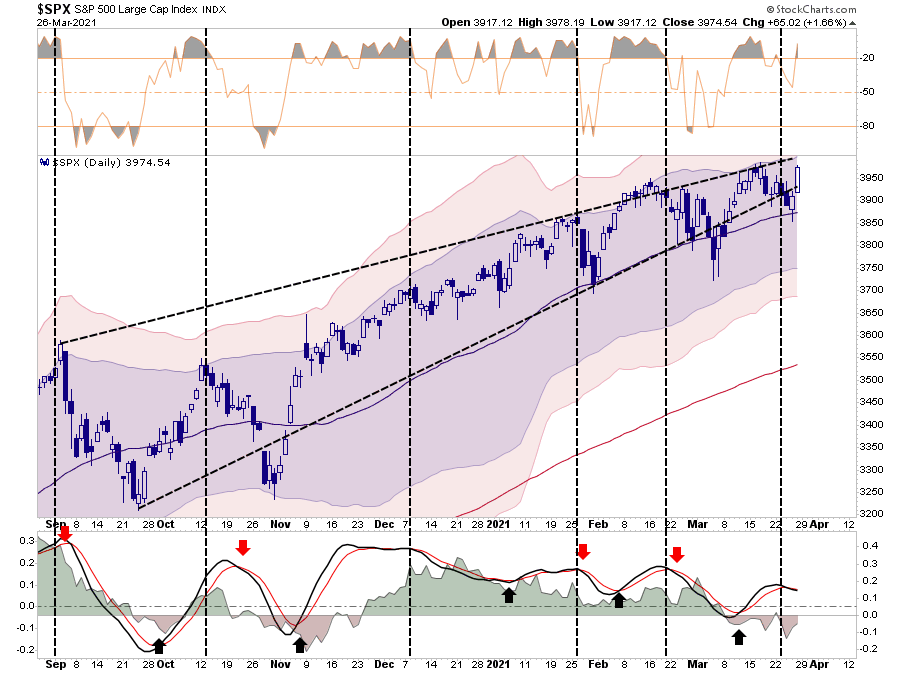

Market Review & Update

I could almost repeat last week’s market update.

“Over the past week, the market didn’t make a lot of headway, as price rises were limited while intraday dips got repeatedly bought. Such is what we would expect with the ‘money flow’ indicators we have discussed over the last several weeks back on “sell signals.” (Importantly, note that Friday’s early morning decline held the uptrend line from the October lows.)”

This week was much the same story, with stocks slopping around all week. However, on Friday, a late afternoon buying surge sent the market back to all-time highs. Again, as noted, stocks haven’t made a lot of headway since the February peak despite a lot of volatility. But Powell’s promise of continue “easy money” certainly didn’t hurt.

As discussed last week, the “sell signal” triggering on a short-term basis coincides with our concerns of quarter-end rebalancing for pension funds. We discuss the confluence of the long- and short-term indicators and the market’s potential outcome in Thursday’s “3-minutes” video.

I think we saw a good bit of that rebalancing this past week and are likely close to its conclusion. As noted, the positive weekly money flows keep downside risk somewhat mitigated for now. As seen over the last two weeks, dips continue to be bought despite overall price weakness. We also see relatively rapid rotations between the defensive and offensive market sectors. As stated previously, such suggests rallies may remain limited until the subsequent “buy signals” are triggered.

I suspect we may have some additional quarter-end rebalancing risk early next week. However, buying on Thursday and Friday next week, as second-quarter positioning gets underway, would not be surprising.

As such, hold positions early next week and look for weaknesses to add to exposures as needed.

The Dollar’s Silent Action

Over the last couple of months, we repeatedly discussed the market’s ongoing rise, particularly the “value” rotation, depended on continuing dollar weakness.

The recent rotation to value has been primarily a function of a “weaker dollar,” which boosts commodities. As noted, if economic growth does strengthen, leading to higher rates will attract foreign inflows into the dollar for a higher yield. Such also undermines corporate profitability, given that roughly 40% of corporate profits are from abroad.

The dollar has been gaining strength this year on expectations of more robust economic growth. A break above the 200-dma could accelerate buying as shorts begin to cover their positions.

The risk not factored into the current “value” trade is the inflation and interest rate increase due to the massive amounts of stimulus. However, that stimulus will quickly flow through the system, leaving consumers tapped by higher inflation and rates eroding disposable income.

In other words, the “value trade” could be just a fleeting as the “economic recovery” itself.

We are firm believers in “value investing.” However, after years of artificial interventions, accounting gimmicks, share buybacks, and massive balance sheet leveraging, there is little “real” value in the markets currently.

Given that the markets have not been allowed to reset, speculators are now simply chasing the next “momentum” trade called “value.”

Powell’s “Easy Money” Promise

Last week, we discussed Powell’s latest change to monetary policy, or rather, lack thereof.

“The U.S. economy is heading for its strongest growth in nearly 40 years, the Federal Reserve said on Wednesday, and central bank policymakers are pledging to keep their foot on the gas despite an expected surge of inflation.” – Reuters

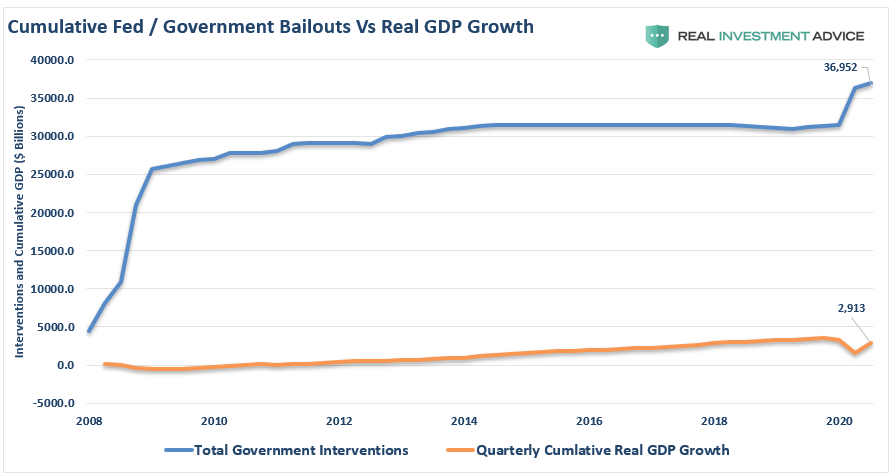

In other words, despite the Fed’s mandate of maximum employment and price stability, the Fed is opting to let things run ‘hot’ for some time to ensure that growth is ‘sticky.'” That stance makes some sense, given the economy still requires massive liquidity support more than a decade after the financial crisis. As discussed previously in ‘Forever Stimulus:’

‘What this equates to is more than $12 of liquidity for each $1 of economic growth.'”

The question that financial markets wanted answering was just how much of a decline in asset prices the Fed will tolerate before providing reassurance.

It only took a 3% clip off of all-time highs before there was a scramble by Fed members to assuage market concerns. My colleague, Mish Shedlock, put together an excellent summary:

“Easy Money” Quotes

- On Thursday, Fed Chair Jerome Powell said even with the economy rebounding faster than expected, any change in monetary policy would happen “very, very gradually over time and with great transparency. Only when the economy has all but fully recovered.”

- Fed Vice Chair Richard Clarida said the central bank would stay in the game until the recovery is “well and truly complete.”

- Fed Governor Lael Brainard promised “resolute patience.”

- San Francisco Fed President Mary Daly said the central bank would show at least “a healthy dose” of patience. ”We are not going to take this punch bowl away.”

- Richmond Fed President Thomas Barkin said that the United States might well see economic growth remain above trend for several years given the amount of pent-up demand. Nonetheless, “What matters is what outcomes we get. I will see where we go and am not trying to overthink the date (of any policy change). I am trying to think about the outcome.”

Not surprisingly, the Fed is very cautious about the financial markets due to its inherent impact on consumer confidence. However, at this juncture, with rates at zero, stimulus checks in the mail, and QE running $120 billion per month, verbal support is all they can do currently.

As Mish concludes:

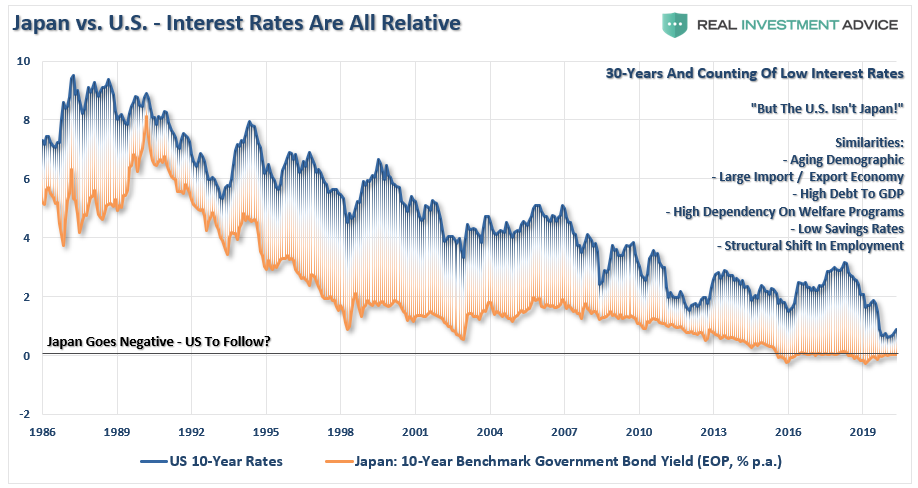

“The Fed’s 2% inflation target is monetary insanity. Full speed ahead with the stimulus in search of inflation that would be visible to anyone who was not wearing groupthink blinders. Japan has tried what the Fed is doing now for over a decade, with no results.”

Japanification

He is correct. The Fed’s “inflation policy” will likely backfire on them badly. As discussed previously in “Japanification:”

“The U.S., like Japan, is caught in an ongoing ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments, and risk begins to outweigh the potential return.”

As my colleague Doug Kass noted, Japan is a template of the fragility of global economic growth.

“The bigger picture takeaway the fact that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.”

I agree with Doug, as does the data, that while financial engineering props up asset prices, it does nothing for an economy over the medium to longer-term. It actually has negative consequences.

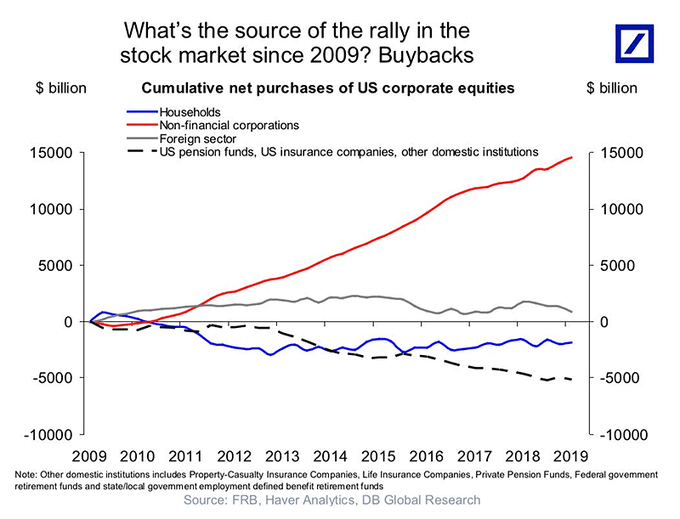

Stock Buybacks Gone Wild

Two weeks ago, I addressed the “Money On The Sidelines” myth stating:

“No, this is not the ‘cash on the sidelines’ argument which I debunked previously. Following the pandemic, corporations drew down credit lines and hoarded cash due to economic uncertainty. Now, with expectations of recovery, corporations are once again beginning to deploy that cash.”

As I stated then, while the mainstream media hope is all this cash will be flowing back into the economy, the reality is that it will primarily go to stock buybacks. Again, while not necessarily bad, it is the “least best” use of the company’s cash. Instead of expanding production, increasing sales, acquiring competitors, or making capital investments, the money gets used for a one-time boost to earnings on a per-share basis.

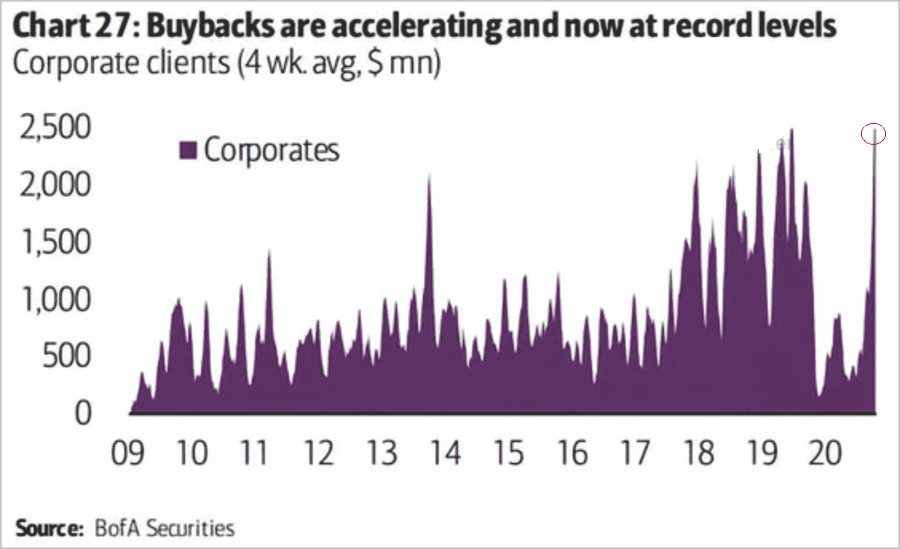

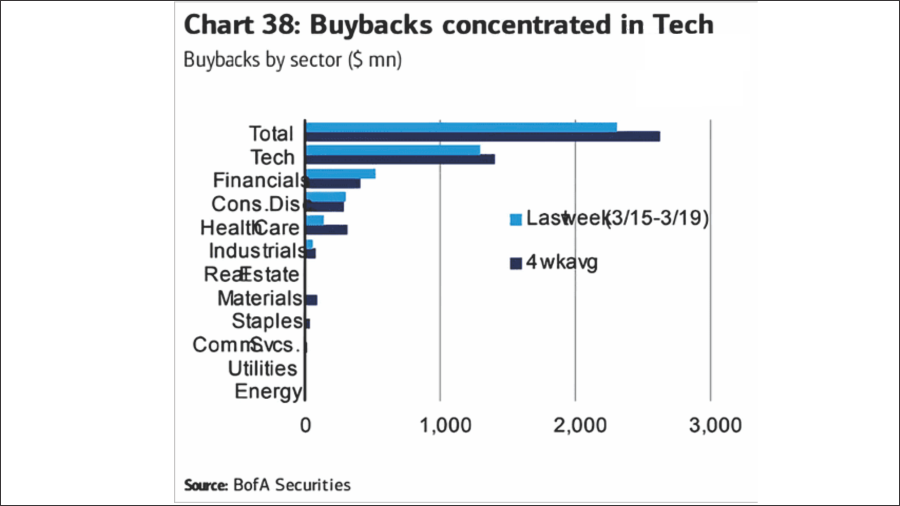

This past week, share buybacks hit a new record.

Not surprisingly, the most prominent players in buybacks are the ones that need to subsidize their earnings the most to beat estimates; technology and financials.

Net Purchases

While share buybacks primarily are for the benefit of corporate insiders “cashing out,” it does have the effect of supporting asset prices as well. As I discussed in 2019, when stocks were hitting records amid record share repurchases:

“What is clear, is that the misuse, and abuse, of share buybacks to manipulate earnings and reward insiders has become problematic. As John Authers recently pointed out:

‘For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.’

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.”

I bring this up for two reasons:

- The buybacks ARE SUPPORTIVE of asset prices in the short-term; and,

- We just had to “bailout” these companies because they couldn’t weather an economic downturn as they have spent years piling into debt and buying back shares.

While Janet Yellen is okay with the buybacks, as she thinks the banks are healthier now, why doesn’t anyone ask the question:

“If banks are so healthy, why do they need a constant monetary stimulus to remain in business and a bailout every time the economy declines?”

It doesn’t sound very healthy to me.

Portfolio Update

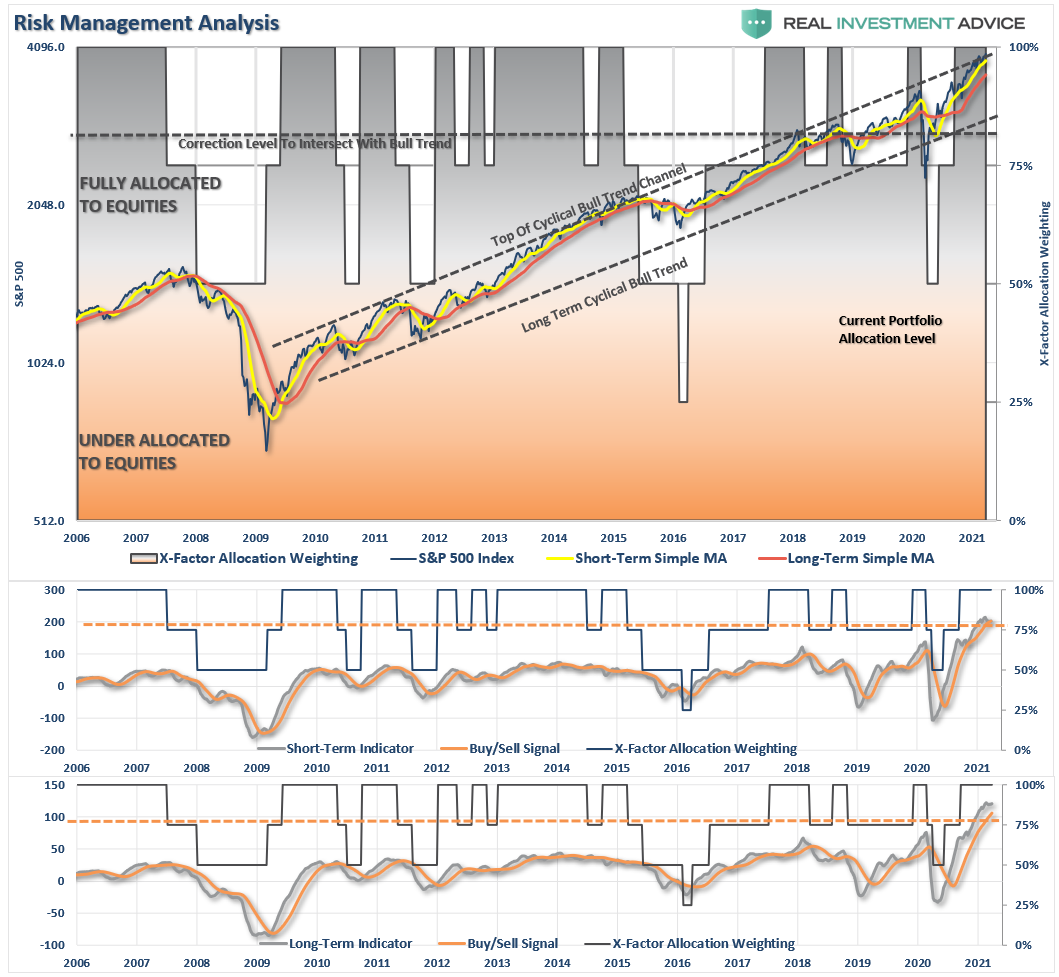

As noted above, with the “money flow” indicators now negative on both a daily and weekly basis, we are currently holding much higher levels of cash. Last week, we also added a bit of “duration” to our bond portfolio by stepping into TLT to add a hedge against a potential pickup in volatility short-term.

With the market now about 1/3rd of the way through the correction cycle, there is limited downside risk currently as we remain in the year’s seasonally strong period. However, such doesn’t mean we can’t have a lot of volatility in the meantime.

We remain wary of the rise in yields, and ultimately the dollar, which remains the key to the current market cycle. As discussed last week, the “value trade,” which had become excessively overbought, corrected in earnest this past week. While we may see some “bottom-fishing” in the short-term, there is still substantially more room for a correction given the extension from long-term means.

Our more significant concern over the next quarter is the extremely high net positioning of institutions in the markets. Historically, when “everyone is in the pool,” outcomes have not been all that pleasant. While we continue to remain allocated toward equity risk currently, we do it with a constant eye on the risk. We suspect that we could see a fairly substantial correction during the summer.

But that is a story we will discuss when we get there.

Continue to manage risk until we start to see “buy signals” across our indicators once again.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

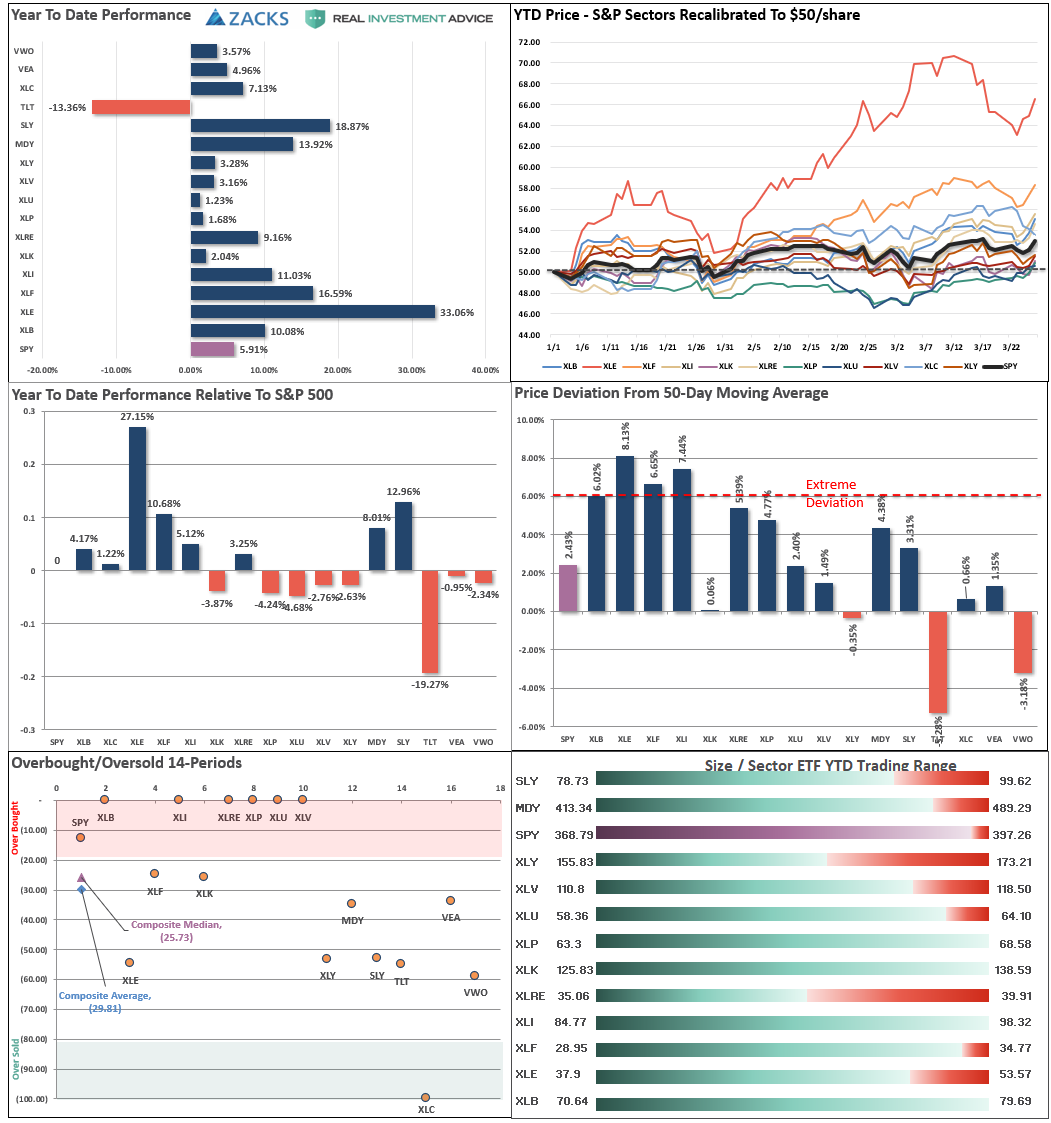

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

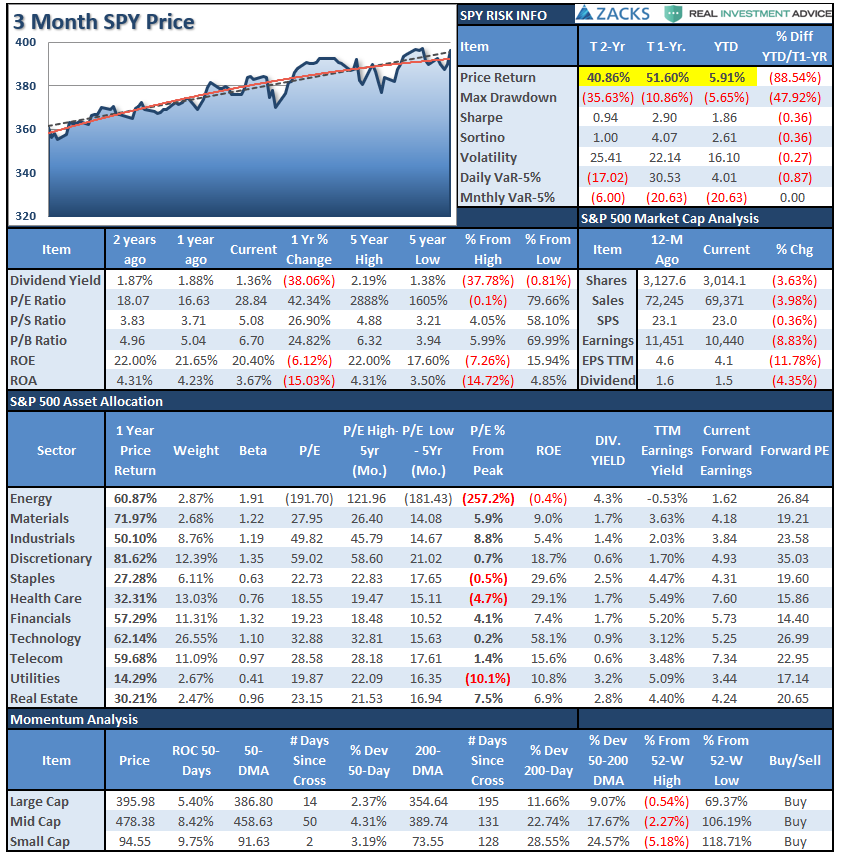

S&P 500 Tear Sheet

Performance Analysis

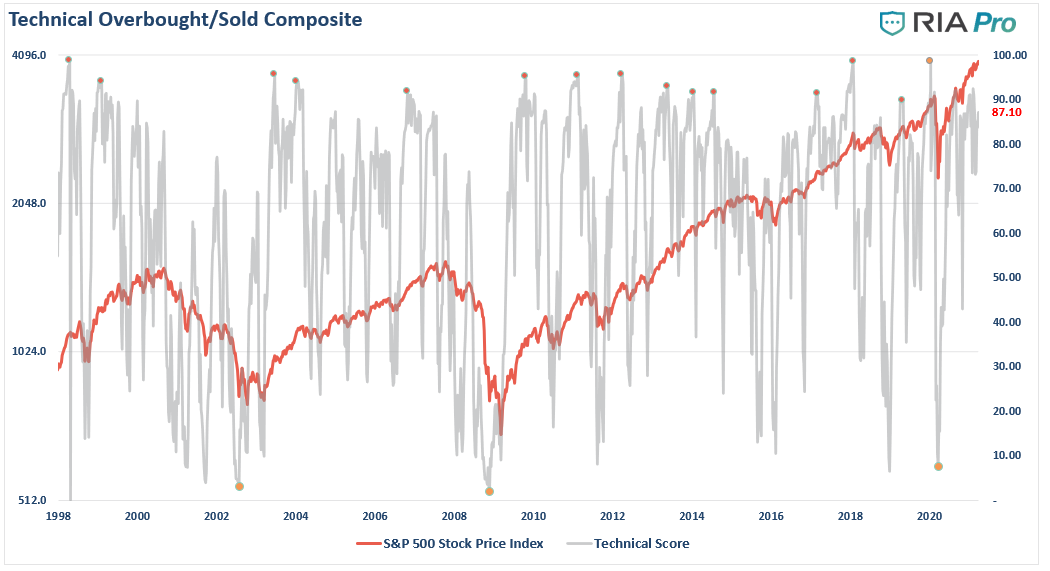

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” is oversold. The current reading is 87.10 out of a possible 100.

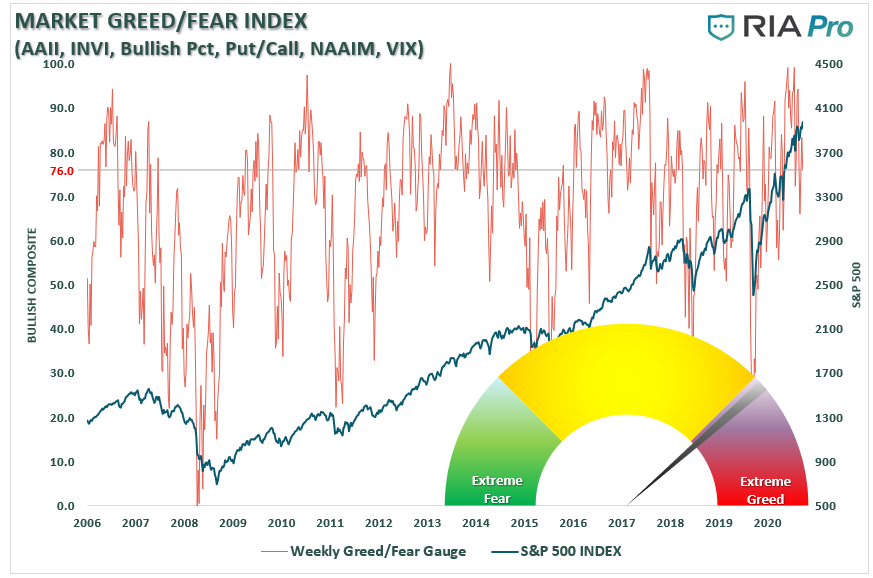

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 76.3 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market.

- Table shows the price deviation above and below the weekly moving averages.

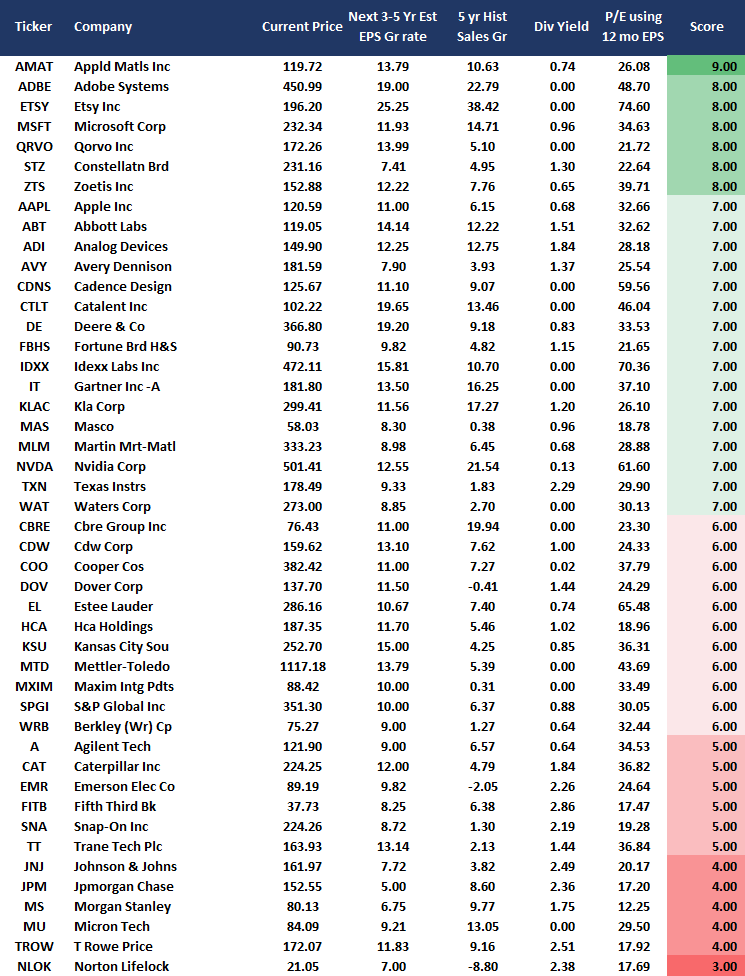

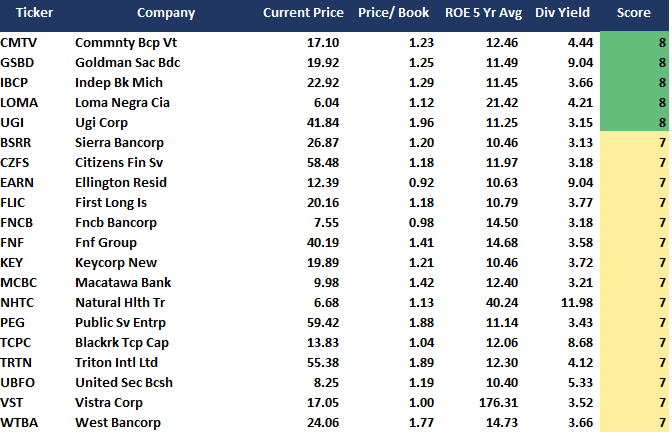

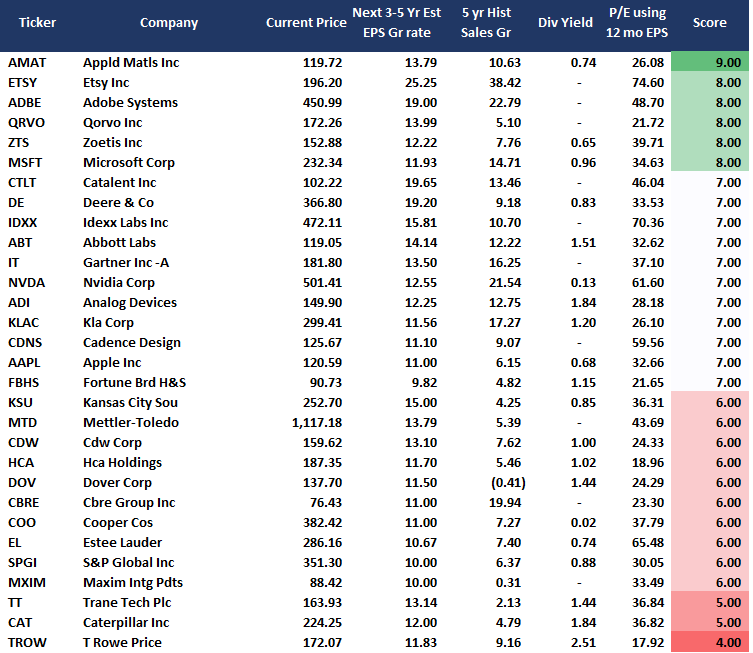

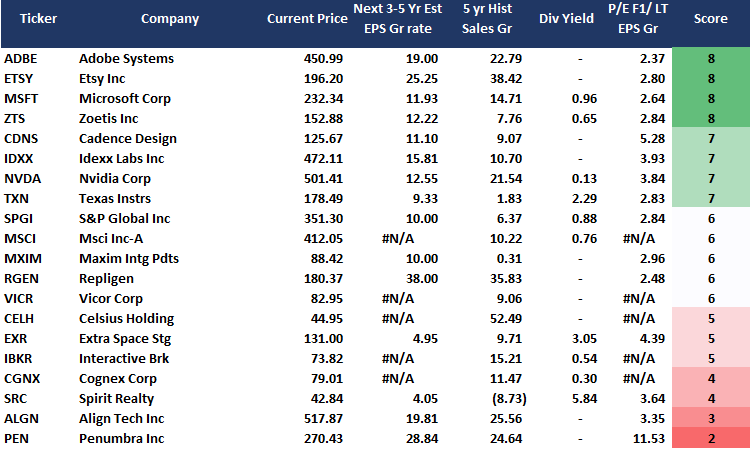

Weekly Stock Screens

Currently, there are four different stock screens for you to review. The first is S&P 500 based companies with a “Growth” focus, the second is a “Value” screen on the entire universe of stocks, and the last are stocks that are “Technically” strong and breaking above their respective 50-dma.

We have provided the yield of each security and a Piotroski Score ranking to help you find fundamentally strong companies on each screen. (For more on the Piotroski Score – read this report.)

S&P 500 Growth Screen

Low P/B, High-Value Score, High Dividend Screen

NEW! Fundamental Growth Screen

Aggressive Growth Strategy

Portfolio / Client Update

Repeating from last week, the market “indigestion” continues. However, the difference is our indicators have flipped to “sell signals.” As such, we have seen more downward pressure on prices, and the rotation between sectors and markets has been vicious. Such does not make our job very easy.

The good news is that markets continue to hold critical support, and investors keep stepping in to buy beaten-down stocks. We have raised cash across portfolios and will use the opportunity over the next two weeks to add to positions that have pulled back and held support successfully.

Our longer-term indicators are still negative, which continue to apply downside pressure and limit upside. We should be getting to a point in the next two weeks where we will see those indicators begin to reverse back to a “buy signal.” That reversal will carry markets into early summer, where we think a more significant correction awaits as earnings and economic growth hit their peaks for this cycle.

As noted below, with yields having reached our target “buy” zone, we did add some additional exposures back to portfolios to further hedge equity risk. We used some of our cash holdings to pick up bond exposures which should help offset equity volatility in the near term.

As always, we continue watching our indicators closely. However, support at the 50-dma continues to hold, which negates some downside risk in the short-term.

Portfolio Changes

During the past week, we made minor changes to portfolios. We post all trades in real-time at RIAPRO.NET.

** Equity / ETF Portfolio – Trade Update ***

“While our S&P indicator is still in sell mode, energy and financials, are starting to turn up. They went into sell mode well before the broader market so are coming out sooner. As such, we added back to energy and financials.” – 03/26/21

Equity Model:

- Added .5% to KMI, XOM, and FANG

- Added .5% to GS and JPM

ETF Model

- Added 1% to XLE and XLF

“With our models pointing to potential short-term turbulence in the equity markets and potential upside in bond prices (as discussed in Three Minutes on Markets), we increased our bond portfolio duration and equity hedge by swapping IEF for TLT. We also put extra cash to work by adding to our short-term bond position (SHY). We will redeploy SHY into stocks and or bonds when needed.” – 03/24/21

Equity and Sector Model:

- Sold 6% IEF and Bought 6% TLT

- Added 7% SHY

“With our daily “money flow” indicators very close to turning negative, with money flows negative as well, we are reducing equity risk across all models slightly.” – 03/23/21

Equity Model:

- Selling 100% of MRO to reduce our overweight energy holdings.

- Selling 100% of ZM, reducing our exposure to communications and a sector laggard.

- Initiating a 1% position in PG to add to our Consumer Staples (defensive) holdings.

ETF Model:

- Reduce XLE to 2% of the portfolio

As always, our short-term concern remains the protection of your portfolio. We have now shifted our focus from the election back to the economic recovery and where we go from here.

Lance Roberts

CIO

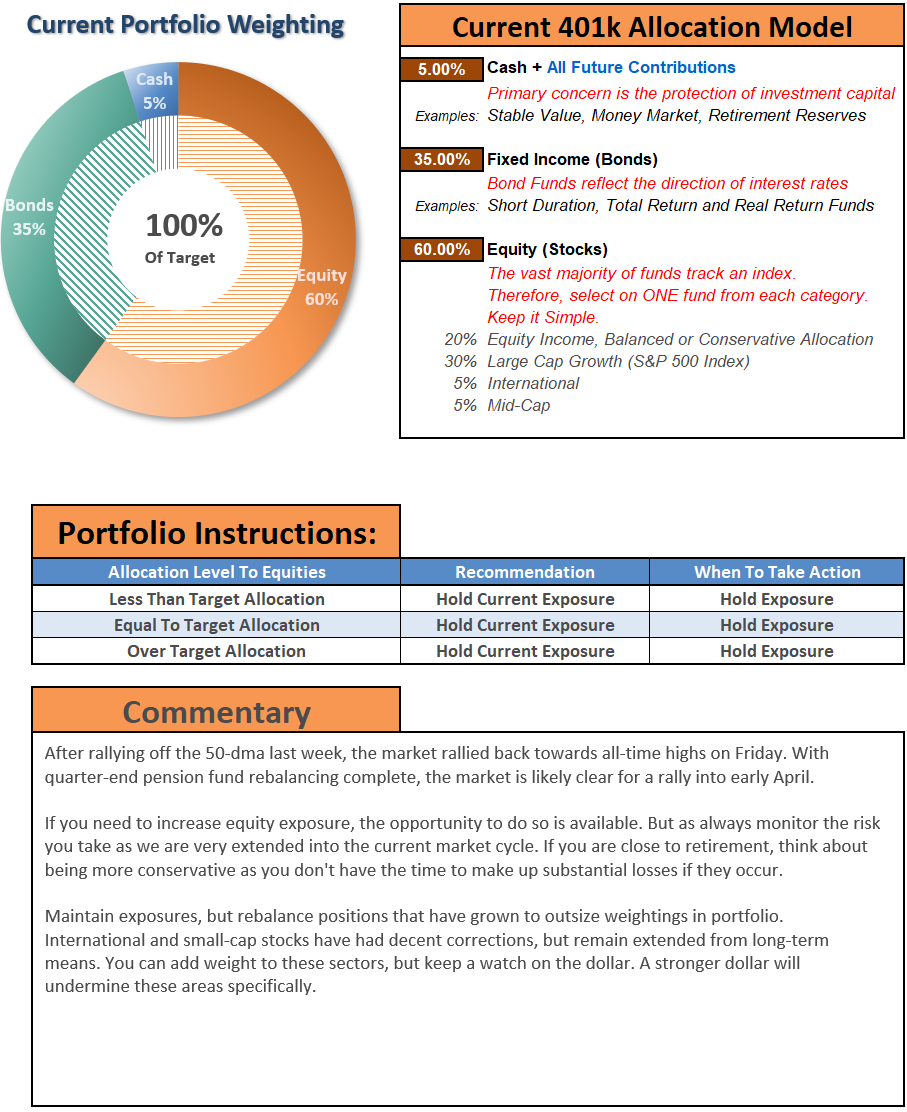

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert, do not hesitate to contact me.

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read