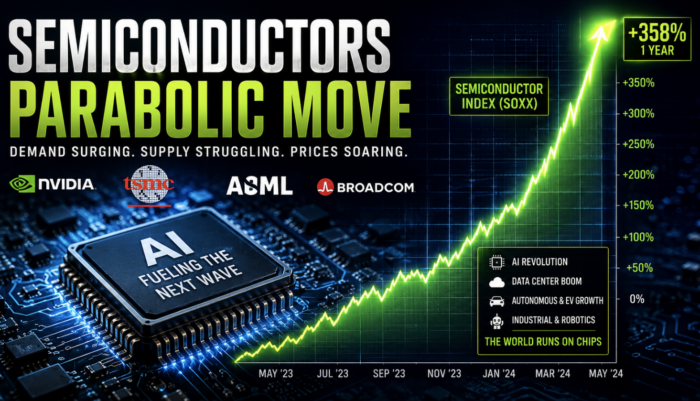

The parabolic semiconductor rally crossed a line this week. SOXX, the iShares Semiconductor ETF,...

Upcoming Event

Candid Coffee: Financial Organization

May 16, 2026 at 8:00 am - 9:00 am

FILTERS

-

Most Searched Terms

Commodity Supercycle: The Enemy Of The Bull Thesis (Part 1)

A funny thing about bull markets is that investors develop a very short memory about the previous...

Gold Bugs Faulty Thesis: M2 and Inflation

Gold bugs often claim that when more dollars are in circulation, each dollar buys less; prices...

Market Correction Risk: Why Summer 2026 Looks Risky

Collapsing breadth. Stretched positioning. The worst seasonal window of the year. The worst year of...

A Robot Economy: Who Gets Rich, Who Gets Left Behind

A funny thing about bull markets is that investors develop a very short memory about the previous...

BDCs: Not All Yield Is Created Equal

Gated funds, collateral fraud, and auto-sector defaults are giving investors in private credit...

Hormuz: Why Markets Are Shrugging Off The Oil Shock

As of this writing, the Strait of Hormuz remains effectively closed since February 28. Roughly 20%...

Government Debt: Not What The Doom Crowd Thinks It Is

A funny thing about bull markets is that investors develop a very short memory about the previous...

GFC 2.0 Or False Alarm Part 2

In Part One, we explored how leverage and derivatives turned subprime mortgages into a crisis that...

Market Lesson: Why Panic Is A Costly Mistake

The Iran shock erased 18% from valuations and fully recovered in two weeks. Investors who panicked...

BLS Jobs Report Is Broken. Is There A Better Measure?

A funny thing about bull markets is that investors develop a very short memory about the previous...

Will Private Credit Cause The Next Financial Crisis?

Believe it or not, it’s been 18 years since the Global Financial Crisis (GFC). Despite many...

Inside You’ll Find:

- The Money-Savvy Guide to Maximum Retirement Income

- Investment & Planning Rules for Financial Success

- The Real Investment Advice Investing Manifesto

- The Savvy Financial Advice Survival Guide

- Much more!

Financial Survival Guides

Real Investment Advice offers a series of in-house financial survival guides to help you navigate the markets and achieve your financial life benchmarks.

Get this guide and many others by signing up below!