The interest rate surge sent stocks tumbling in the worst day since March. The ongoing “debt ceiling debate,” the specter of a government shutdown, and potential of a “technical default,” sent interest rates higher as bond traders positioned for the worse. Treasury Secretary Janet Yellen has warned Congress that the debt limit must be raised or suspended by Oct. 18.

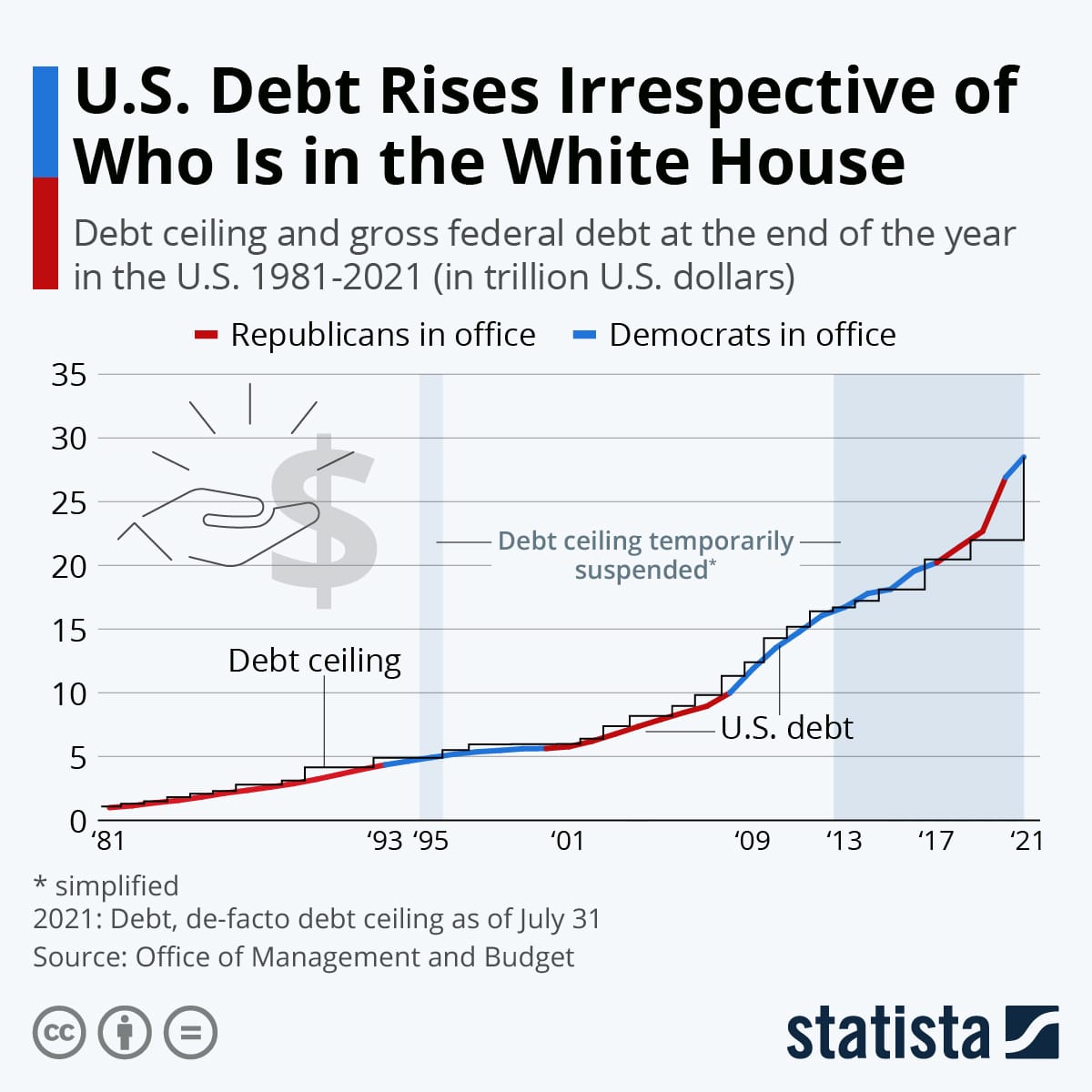

“The U.S. has seen three Republican and three Democratic administrations since the 1980s, but no matter who is in the White House, U.S. debt has been rising steadily throughout the years, also expanding the debt ceiling in the process.“

While almost nobody expects Uncle Sam will stop paying his bills, Washington’s highly partisan atmosphere is enough to give investors a serious gut check, especially because technology and growth-sensitive stocks are sensitive to rising rates.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended September 24 (4.9% during prior month)

- 10:00 a.m. ET: Pending home sales, month-over-month, August (1.3% expected, -1.8% in July)

Earnings

- No notable reports scheduled for release

Politics

- President Biden canceled a trip to Chicago today to work the phones to try and salvage his economic agenda. The bipartisan infrastructure bill and the multitrillion dollar reconciliation package hang in the balance.

- On Capitol Hill, less than 48 hours away from a government shutdown, lawmakers remain gridlocked after key moderate Senator Joe Manchin (D-WV) says he’s made “no commitments” on a reconciliation package, which is leading to what some are terming a liberals revolt over the plan from U.S. House of Representatives Speaker of the House Nancy Pelosi to vote on the separate infrastructure bill this week.

- Also today, in Pittsburgh, is the inaugural meeting of the U.S.-E.U. Trade and Technology Council, chaired on the U.S. side by Commerce Secretary Gina Raimondo and other members of Biden’s cabinet. The council will talk about “expanding and deepening transatlantic trade.”

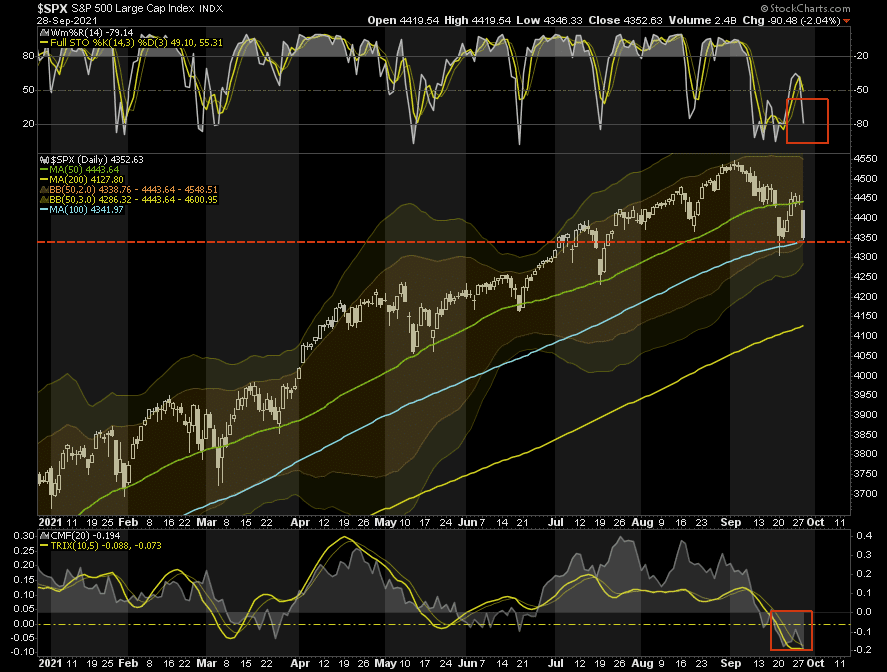

No Safe Place To Hide

The good news is that stocks are back to very oversold on a short-term basis. The bad news is the market failed support at the 50-dma and is now looking to retest the 100-dma. If the market fails the 100-dma there is another decent leg of downside risks to the market in the short-term.

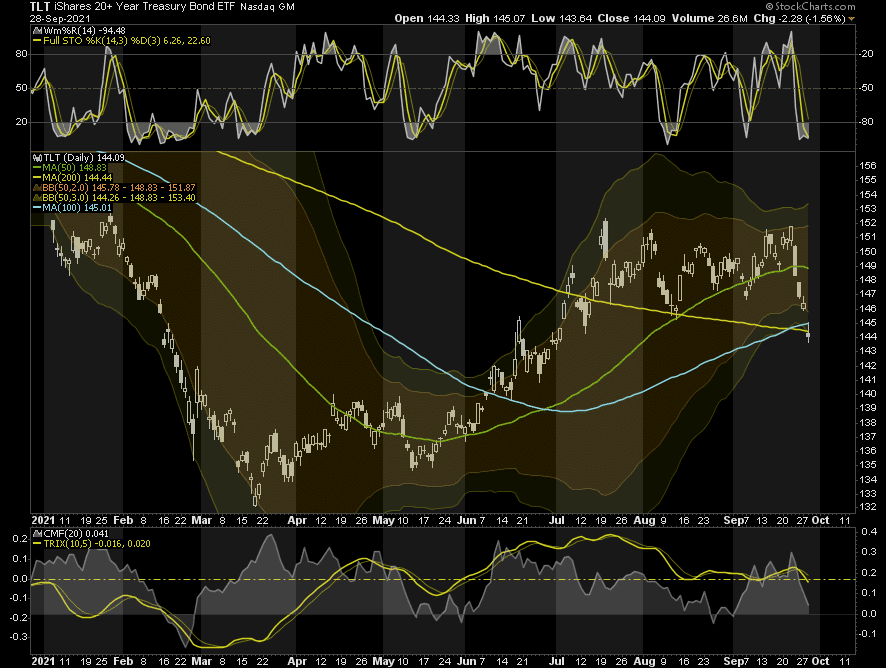

Unfortunately, bonds are helping the matter currently as the area usually hedging off the risk of a market decline is getting hit as well.

At the moment there is no safe place to hide. However, the market should resolve itself as soon as the debt ceiling is lifted and bonds recalibrate for the new issuance. Like stocks, bonds are deeply oversold, and as we discuss below, there is likely a very good bond buying opportunity approaching.

How To Spot Bond Buying Opportunities

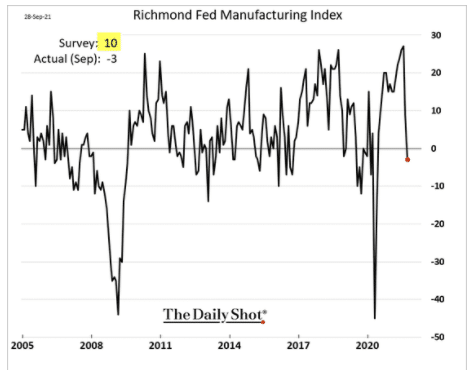

Richmond Fed Points to Contraction

The Richmond Fed Manufacturing Index now points to economic contraction at -3 versus estimates of 10 and a prior month reading of 9. The regional index is at its lowest level since May 2020. While most sub-indexes fell, the good news is that employment is still expanding. Yesterday, the Dallas Manufacturing Index fell from 9 to 4.6 but remains in expansion mode. The ISM National Manufacturing Index will be released on Friday. Expectations are for a minor decline but keeping it well within an expansionary mode.

Ford on a Roll

Per CNBC: “Ford (F) – Ford is accelerating its push into electric vehicles, with plans for a new U.S. assembly plant and three battery factories. Ford and South Korean partner SK Innovation will invest more than $11 billion in the project. Ford shares rose 3.3% in premarket trading.” We hold a 3% in F in the 60/40 Equity Model.

Hawks are Fleeing The Fed

Dallas Fed President Kaplan is following Boston Fed’s Rosengren in retiring from the Fed. The announcements come in the wake of disclosures about their active trading activity. Both members were hawkish and outspoken about their desire to taper QE and ultimately raise rates.

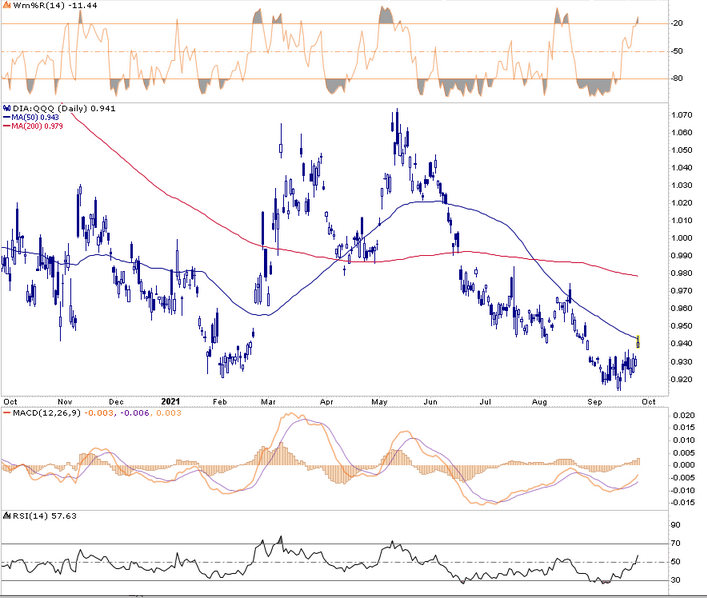

Dow or NASDAQ?

In the aftermath of the last Fed meeting, value and cyclical stocks are edging out growth stocks. Given the recent jump in yields and outperformance of energy, materials, and industrials, the market may be voicing concern the Fed is late to stop inflation. We recently boosted allocations to cyclical and value sectors as their respective technical setups are enticing and the possible reflation rotation may be back on.

To help us track a reflation rotation we can use the ratio of the more value-centric Dow Jones to the growth-led NASDAQ. The graph below shows the recent uptick in Dow versus the NASDAQ. Also, note that the MACD of the ratio is turning up and the RSI is above 50. If the reflation trade is on again, the relative upside of the Dow and value/cyclical sectors can be very rewarding. From February to June of 2021, during the last inflation scare, the Dow beat the NASDAQ by about 15%.

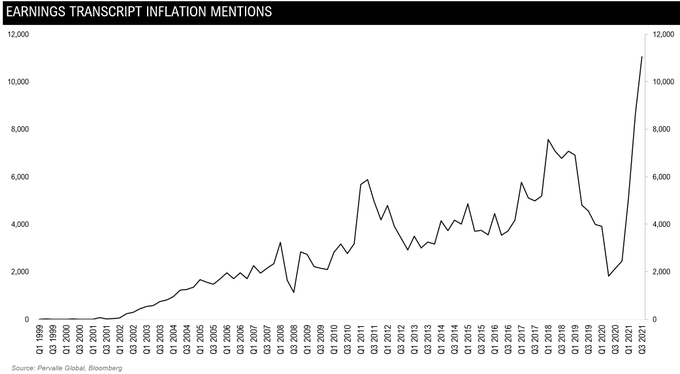

Inflation on the Mind

The graph below from Teddy Vallee shows that inflation concerns are top of mind in corporate earnings outlooks. In a couple of weeks, corporations will start announcing quarterly earnings. We suspect many companies will highlight how they are handling margin pressures due to higher wages and input costs. For companies that can push through said costs to consumers, the outlook should be better than for those that can’t.

Also Read