In this 10-15-21 issue of “Bulls Regain Control Of The Market As Fed Taper Looms.”

- Market Rallies As Earnings Season Kicks Off

- FOMC Minutes Confirm Fed Taper Coming

- Navigating Uncertainty

- Portfolio Positioning

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Is It Time To Get Help With Your Investing Strategy?

Whether it is complete financial, insurance, and estate planning, to a risk-managed portfolio management strategy to grow and protect your savings, whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Market Rallies As Earnings Season Kicks Off

Two weeks ago, we laid out the case for why we started increasing our equity exposure in portfolios.

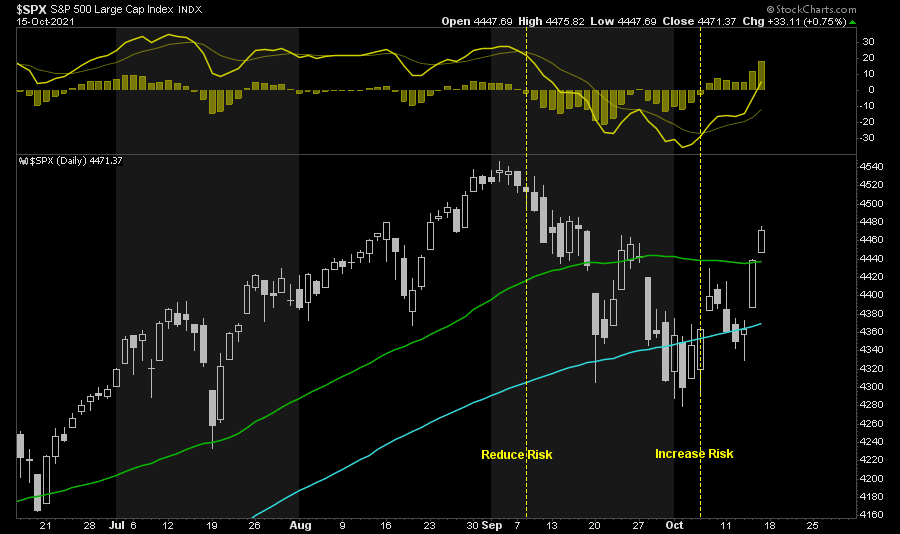

“It is worth noting there are two primary support levels for the S&P. The previous July lows (red dashed line) and the 200-dma. Any meaningful decline occurring in October will most likely be an excellent buying opportunity particularly when the MACD buy signal gets triggered.

The rally back above the 100-dma on Friday was strong and sets up a retest of the 50-dma. If the market can cross that barrier we will trigger the seasonal MACD buy signal suggesting the bull market remains intact for now.“

Chart updated through Friday.

While the market started the week a bit sloppily, the bulls charged back on Thursday as earnings season officially got underway. With the market crossing above significant resistance at the 50-dma and turning both seasonal “buy signals” confirmed, it appears a push for previous highs is possible.

Correction Is Over For Now

After nearly a month of selling pressure, the rally over the last couple of days came on cue and supported our recommendation to increase exposure to equities. As noted by Barron’s:

“Market sentiment is getting more buoyant. Thursday, the S&P 500 saw its largest gain since March 5, according to Instinet. The percent of stocks on the index that rose, 95%, was the highest since June 21. Friday, about 90% of components were positive. Instinet sees a high likelihood that the index will reach 4.570 fairly soon, for a more than 2% gain.”

Two factors are driving the rebound. Earnings, so far, are coming in above estimates. Such isn’t surprising as analysts suppressed estimates going into reporting season. Secondly, bond yields declined.

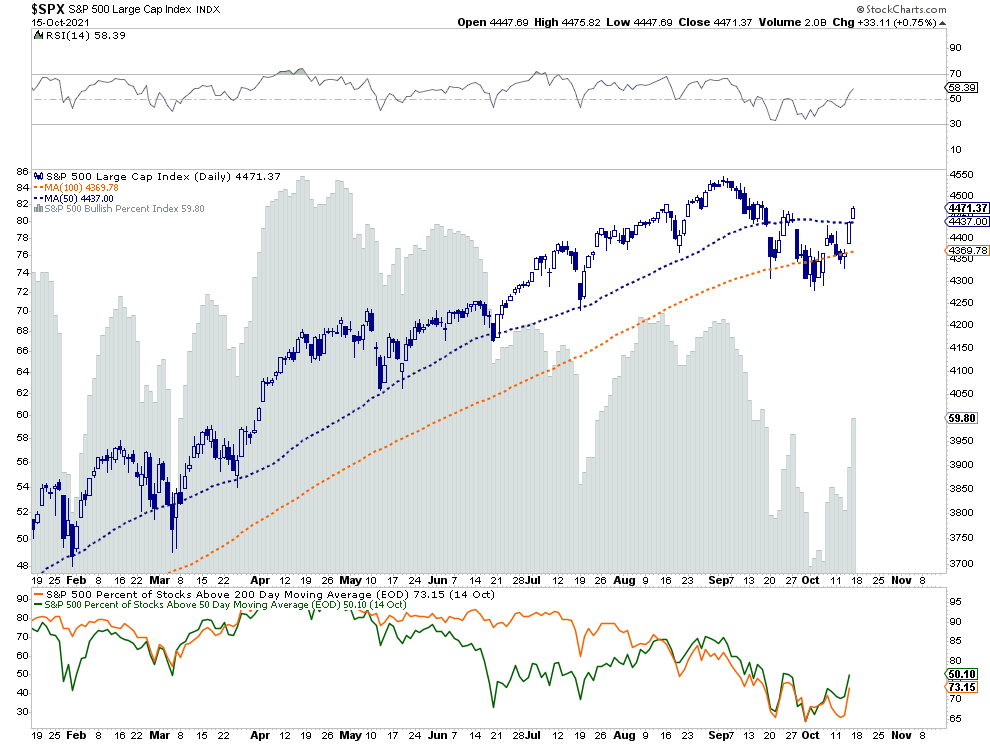

However, there are still reasons to remain cautious near term. As shown below, the internals of the market, while improved slightly, remain negatively diverged. The number of stocks above respective 50- and 200-dma remains low, the bullish percent index remains weak, and relative strength declines.

Furthermore, most companies haven’t reported earnings yet, and macroeconomic challenges still exist. So far, large banks beat estimates on reduced loan loss reserves, but they don’t deal with supply-chain limitations. We are about to see earnings from companies directly impacted by, and don’t benefit from, higher inflation, labor costs, and supply line disruptions.

Technically, If the current rally is going to push back to all-time highs, the market’s underlying strength must begin to improve markedly over the next couple of weeks. If not, the current rally will likely fail sooner than later. Furthermore, the odds of a correction increase as the Fed begins to reduce monetary accommodation.

FOMC Minutes Confirms Taper Is Coming

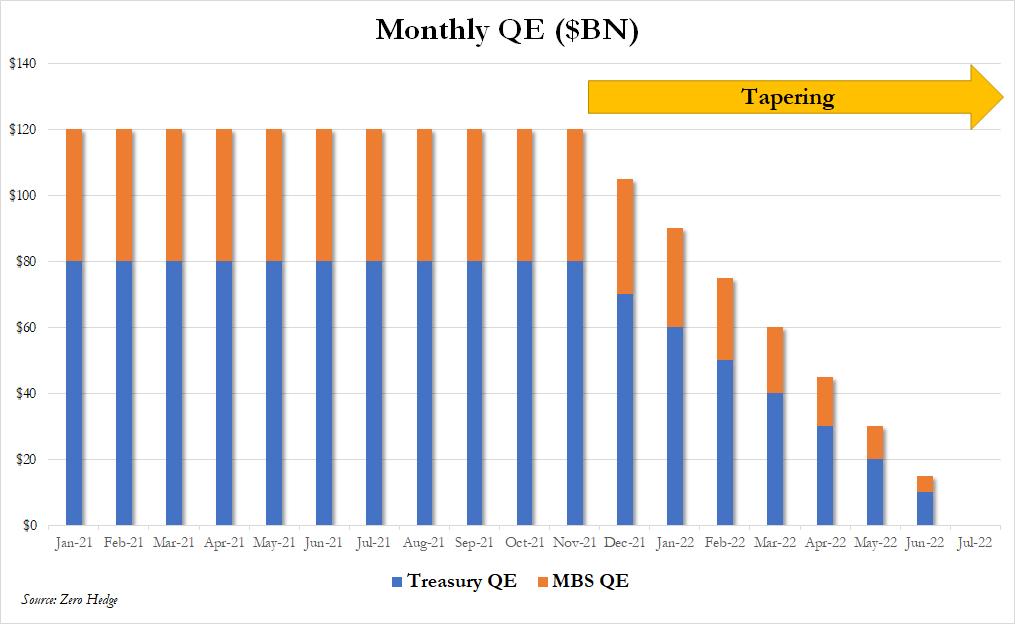

In the most recent release of the Federal Reserve’s FOMC minutes, the much anticipated “taper” of bond-buying programs got confirmed. To wit:

“The illustrative tapering path was designed to be simple to communicate and entailed a gradual reduction in the pace of net asset purchases that, if begun later this year, would lead the Federal Reserve to end purchases around the middle of next year.

The path featured monthly reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities (MBS). Participants generally commented that the illustrative path provided a straightforward and appropriate template that policymakers might follow, and a couple of participants observed that giving advance notice to the general public of a plan along these lines may reduce the risk of an adverse market reaction to a moderation in asset purchases.“

While the Fed did not explicitly discuss rate hikes, as noted in our Daily Commentary, the futures market has already priced in two rate hikes next year.

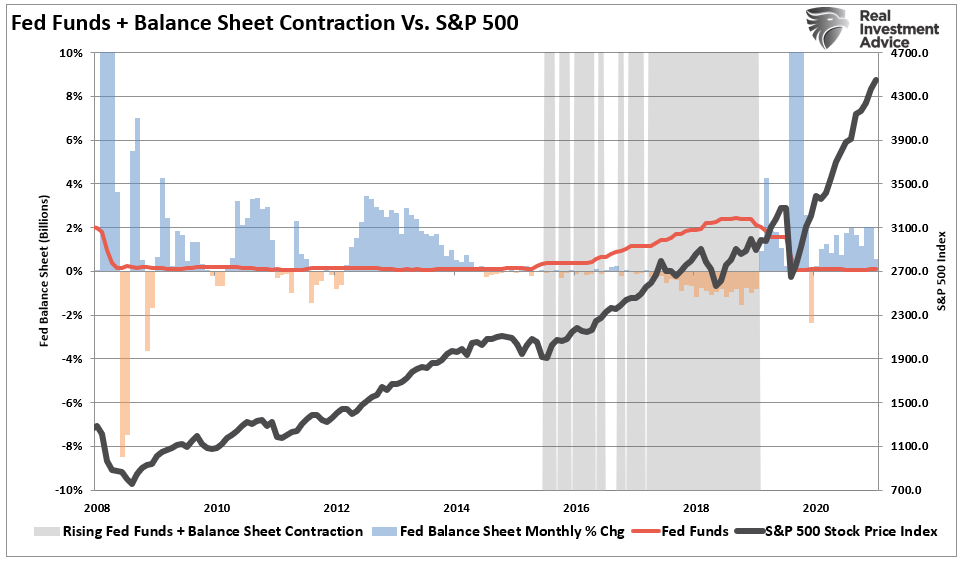

Between reducing bond purchases and lifting overnight rates, the risk to investors is more than evident. As we noted in “3-Things That Will Trigger The Next Bear Market:”

“The risk of a market correction rises further when the Fed is both tapering its balance sheet and increasing the overnight lending rate.

What we now know, after more than a decade of experience, is that when the Fed starts to slow or drain its monetary liquidity, the clock starts ticking to the next corrective cycle.”

The problem for the Fed is that while they suggest they will “adjust” based on incoming data, they may well get trapped between surging inflation and a recessionary economy.

Inflation: Transient Or Persistant

As noted, the risk to the Fed is getting trapped by inflation. The hope has been that current inflationary pressures from the economic shutdown would be “temporary” or “transient” and resolved as the economy reopened. However, nearly 18-months later, with the economy booming, employment running hot, and more job openings than unemployed persons, the disruptions remain. Notably, prices are surging, particularly in the areas that affect households the most.

If inflation is running ‘hot” and employment is full, the Fed should remove monetary accommodation and hike interest rates. However, with economic growth weak, financial stability dependent on monetary interventions, and record numbers of near-bankrupt companies dependent on low-interest-rate debt, a reversal of accommodation could be disastrous.

The hope was inflation would be transient and monetary accommodations could continue unfettered. Now, as noted by St. Louis President James Bullard, this year’s surge in inflation may well persist amid a strong U.S. economy and tight labor market.

“While I do think there is some probability that this will naturally dissipate over the next six months, I wouldn’t say that’s such a strong case that we can count on it,” Bullard said Thursday during a virtual discussion hosted by the Euro 50 Group.

“I would put 50% probability on the dissipation story and 50% probability on the persistent story.”

As Michael Lebowitz noted this week:

“If demand stays high, and supply lines and production remain fractured, inflation will continue to run hot. If such occurs, CEOs may decide not to invest in new production facilities where ‘persistent’ inflation becomes more likely.

Primarily, ‘persistent’ is not ‘transitory.’ Nor is persistent in the Fed’s forecast. Persistent inflation requires the Fed to take detrimental actions to investors.

Given the oddities of the current environment, and our fiscal leaders’ carelessness, it is something we must consider.”

In Case You Missed It

Both Bulls And Bears Have Valid Views

Given the potential for a “policy mistake” and our cautionary views, the following email question currently sums up many investors’ views.

“I really am not sure what to do. Should I raise more cash and be defensive with inflationary pressures rising, and the Fed set to taper. Or, should I just stay invested given the market seems to be doing okay?”

For investors, they have gotten caught between logical views.

From the bullish perspective:

- The market just completed a much-needed 5% correction.

- Short-term conditions are oversold.

- Bullish sentiment is largely negative.

- Earnings season should be supportive.

- Stock buybacks are running at a record pace.

- The seasonally strong period of the year tends to be positive for stocks.

However, those views get countered by the bearish perspective discussed last week.

- Valuations remain elevated.

- Inflation is proving to be sticker than expected.

- The Fed confirmed they will likely move forward with “tapering” their balance sheet purchases in November.

- Economic growth continues to wane.

- Technical underpinnings remain weak.

- Corporate profit margins will shrink due to inflationary pressures.

- Earnings estimates will get downwardly revised keeping valuations elevated.

- Liquidity continues to contract on a global scale

- Consumer confidence continues to slide.

Given this backdrop, it is understandable why investors are finding reasons “not” to invest. However, as stated previously, avoiding crashes and downturns can be as costly to investment outcomes as the downturn itself.

Navigating Uncertainty In Your Portfolio

As noted above, the market has not done anything technically wrong. Longer-term, the bullish trend remains intact, the recent correction worked off much of the overbought condition, and investor sentiment is negative enough to support a short-term rally.

However, while we think a rally is likely near-term, there is considerable risk to the market as we head into 2022. Such is why we stated last week:

“If you didn’t like the recent decline, you have too much risk in your portfolio. We suggest using any rally to the 50-dma next week to reduce risk and rebalance your portfolio accordingly.“

So here are some guidelines to follow.

- Move slowly. There is no rush in making dramatic changes.

- If you are over-weight equities, DO NOT try and fully adjust your portfolio to your target allocation in one move. Think logically above where you want to be and use the rally to adjust to that level.

- Begin by selling laggards and losers.

- Add to sectors, or positions, that are performing with, or outperforming the broader market.

- Move “stop-loss” levels up to recent lows for each position. Managing a portfolio without “stop-loss” levels is foolish.

- Be prepared to sell into the rally and reduce overall portfolio risk. Not every trade will always be a winner. But keeping a loser will make you a loser of both capital and opportunity.

- If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.

While we remain optimistic about the markets, we are also taking precautionary steps to tighten up stops, add non-correlated assets, raise some cash, and hedge risk opportunistically on any rally.

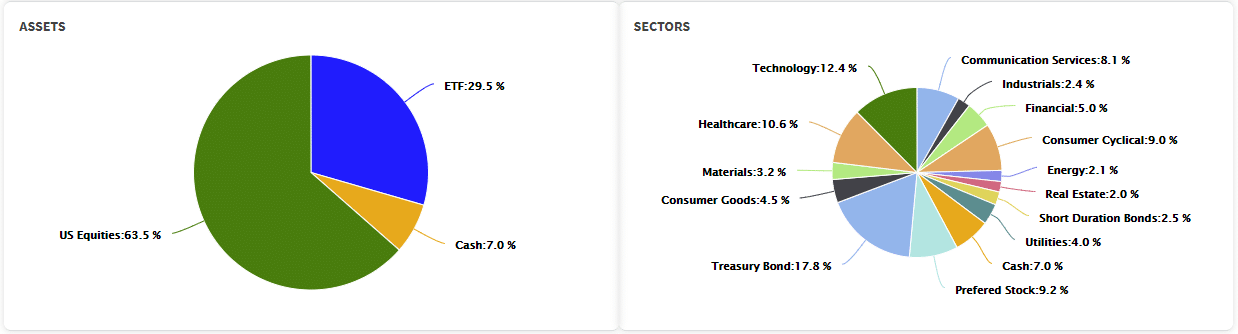

Portfolio Update

As we head into the heart of earnings seasons, we slightly increased our exposure to technology stocks while maintaining the balance of our allocations. After making additions to equities over the last couple of weeks, we are nearly fully exposed to equities, slightly overweight cash, and a tad underweight target duration in our bond holdings.

While our positioning is bullish, we remain very concerned about the market over several months. Historically, stagflationary environments do not mix well with financial markets. Such is because the combination of inflationary pressures and weaker economic growth erodes profit margins and earnings.

Furthermore, expectations heading into 2022 remain exceptionally optimistic, which leaves much room for disappointment. With liquidity getting drained, the Fed reducing monetary accommodation, and two rate hikes scheduled next year, the risk to investors remains elevated.

So, why aren’t we sitting in cash? Because our job is to take advantage of markets when a reasonable risk/reward opportunity presents itself, like now. However, we do understand there is a significant risk. Or, as Seth Klarman from Baupost Capital once stated:

“Can we say when it will end? No. Can we say that it will end? Yes. And when it ends and the trend reverses, here is what we can say for sure. Few will be ready. Few will be prepared.”

We are not in the “prediction business.”

We are in the “risk management business.”

For now, we are giving the market the benefit of the doubt. However, we are keeping our positioning on a very short leash. With valuations still elevated, the technical deterioration of the market remains a primary concern.

Have a great weekend.

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

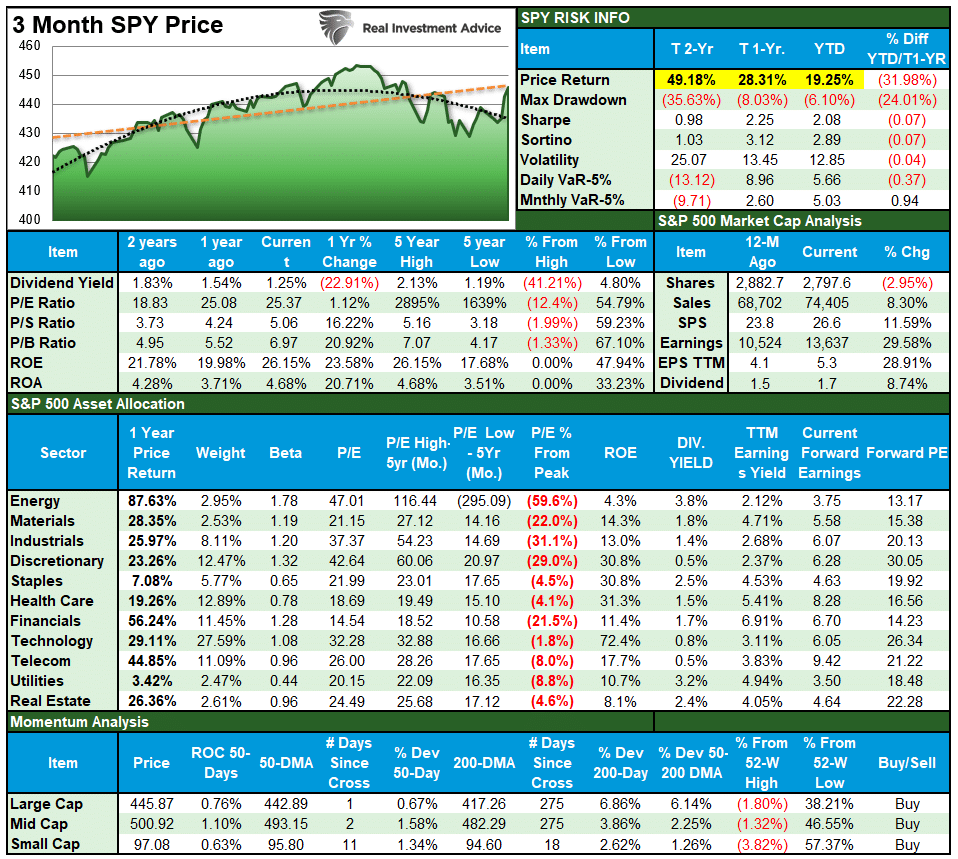

S&P 500 Tear Sheet

Performance Analysis

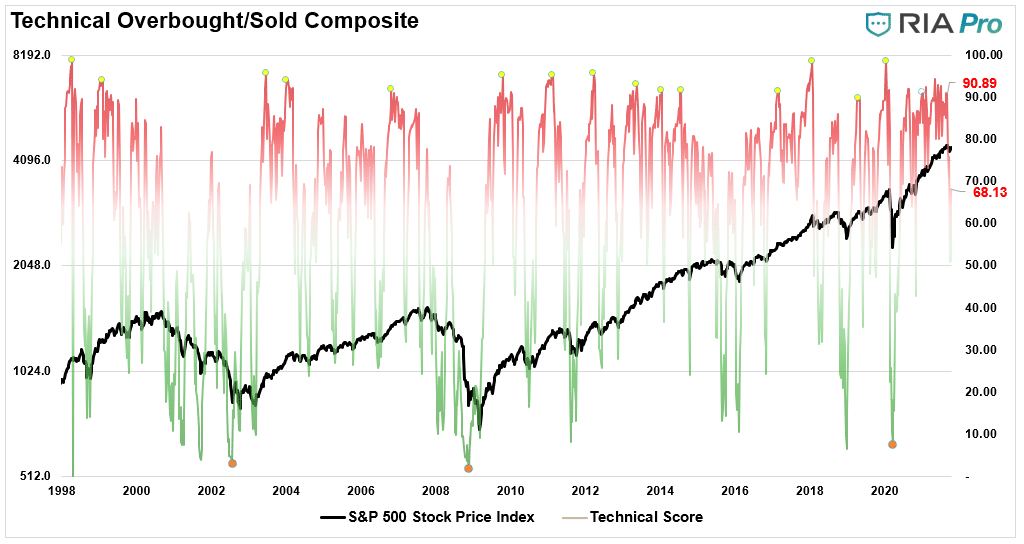

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 68.13 out of a possible 100.

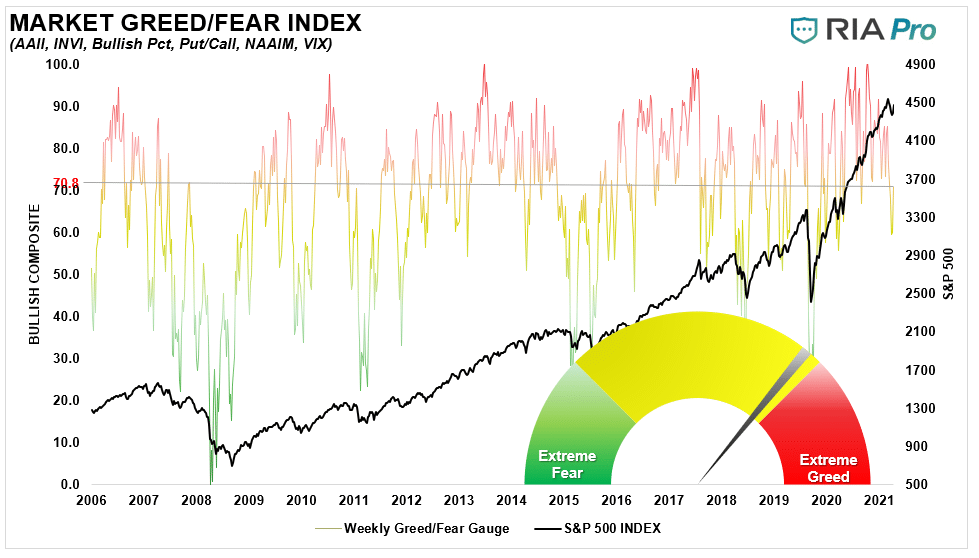

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 70.8 out of a possible 100.

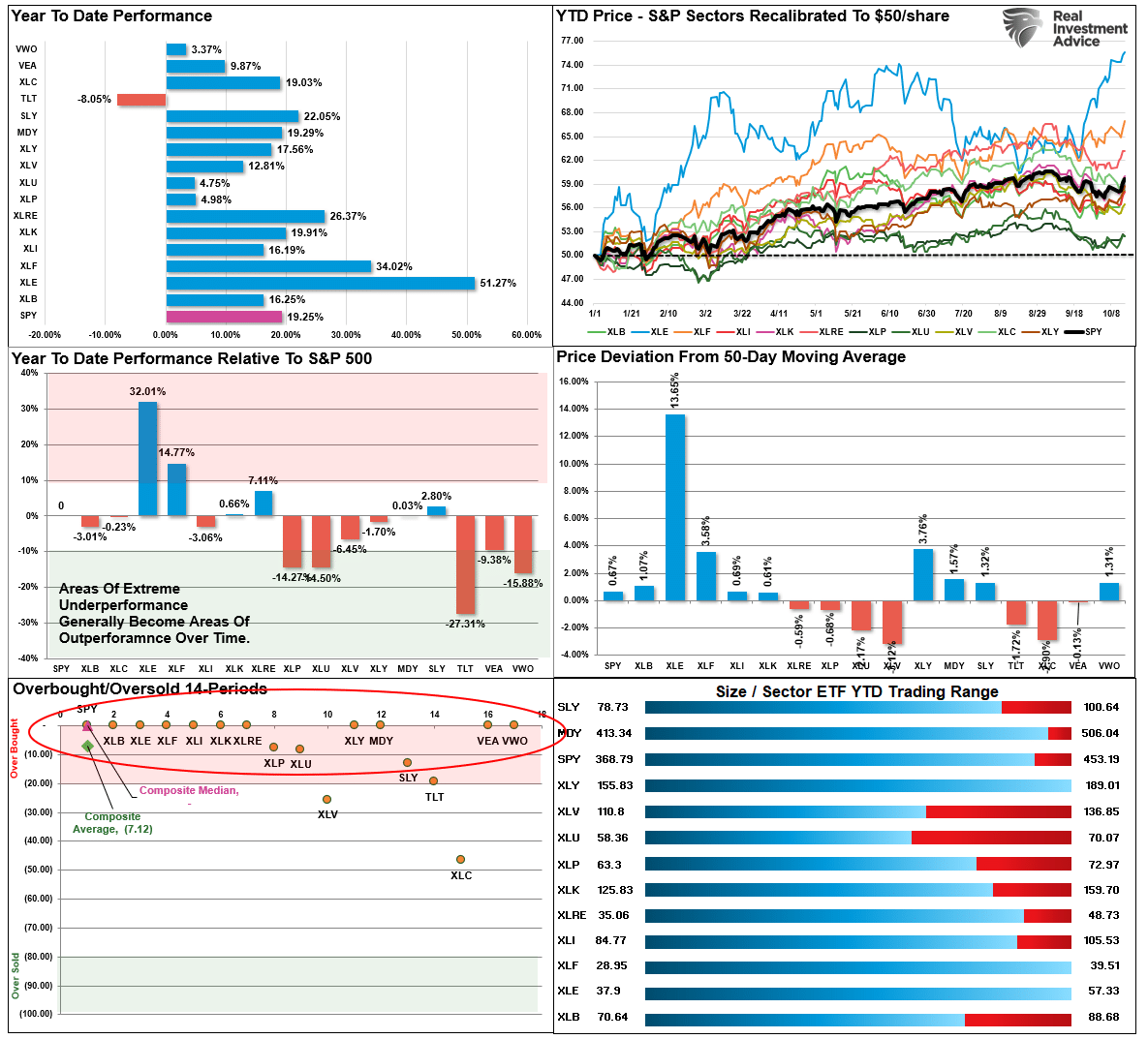

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

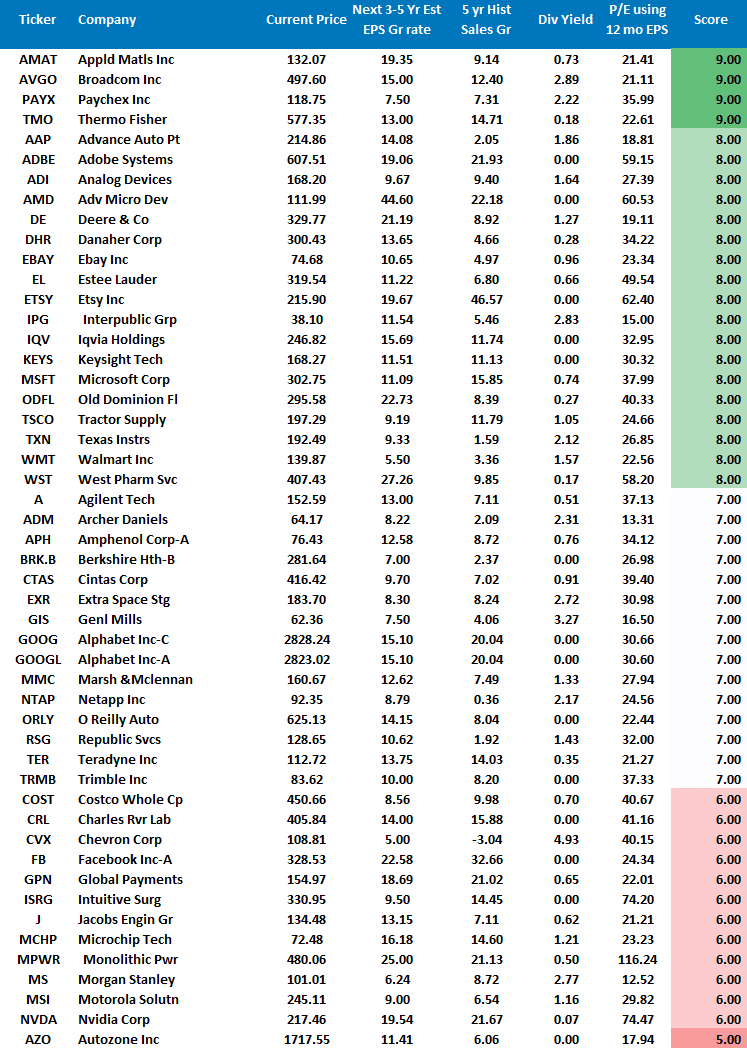

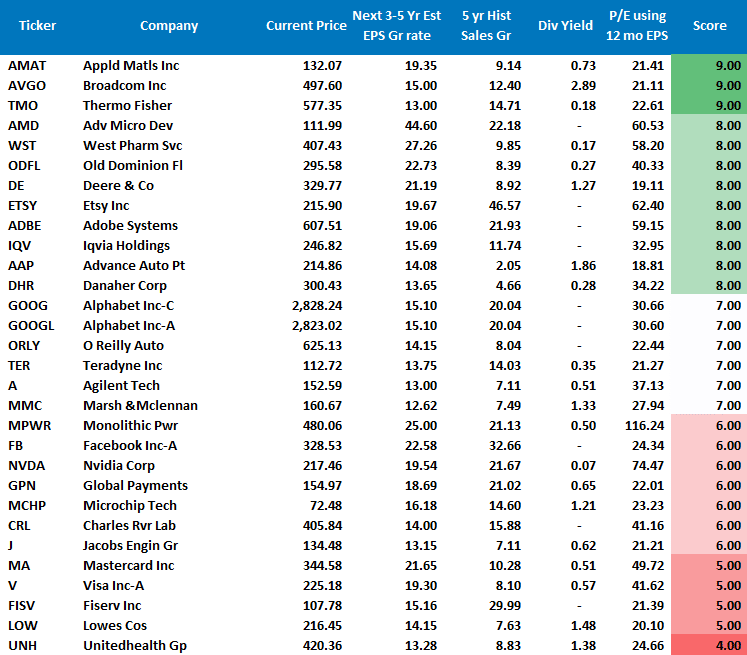

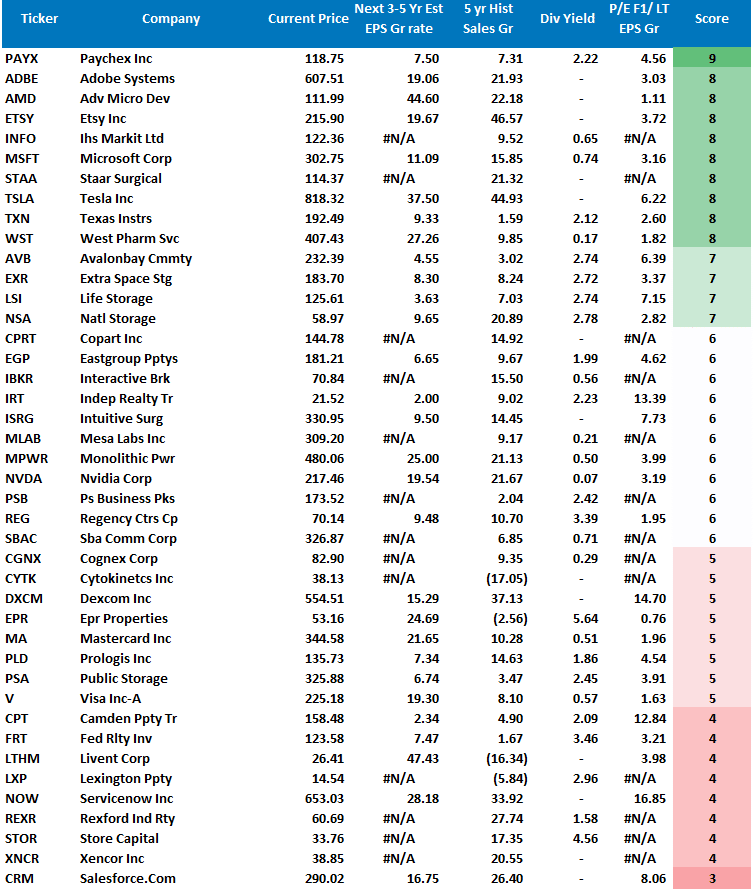

Weekly Stock Screens

Currently, there are four different stock screens for you to review. The first is S&P 500 based companies with a “Growth” focus, the second is a “Value” screen on the entire universe of stocks, and the last are stocks that are “Technically” strong and breaking above their respective 50-dma.

We have provided the yield of each security and a Piotroski Score ranking to help you find fundamentally strong companies on each screen. (For more on the Piotroski Score – read this report.)

S&P 500 Growth Screen

Low P/B, High-Value Score, High Dividend Screen

Fundamental Growth Screen

Aggressive Growth Strategy

Portfolio / Client Update

As noted last week,

“The markets finally appeared to have bottomed this week as the debt ceiling debate got resolved until December. But, while the pressure was relieved somewhat, there is still risk heading into the end of the year.”

Such remains the case this week. While the market started weakly, it successfully retested and held the 100-dma. Such bolsters our case, with both MACD signals confirming that the “seasonally strong” period has begun. While such does not eradicate any downside risk, it does reduce the risk of a significant correction near-term.

As noted below, we continued adding to our equity exposure this week and are currently carrying nearly full allocations. While such leaves us a little uncomfortable given the Fed, valuations, and a stagflationary environment, we think the short-term benefits offset the risk.

We are watching our positions closely and have moved stops up to recent lows for all positions.

Furthermore, after increasing the duration of our bond portfolio, the recent uptick in rates provides another entry point to lengthen our duration once again. If there is a risk-off event in the market, yields will drop to 1% or less providing a nice bump in appreciation in our bond portfolio. In the meantime, we are collecting a bit of income while holding the hedge.

For now, there seems to be minimal risk in the market. However, don’t be misled. There are numerous risks we are watching that could lead us to reverse course rapidly. Our job remains to protect your capital first and foremost, but we want to capture gains when we can.

Portfolio Changes

During the past week, we made minor changes to portfolios. In addition, we post all trades in real-time at RIAPRO.NET.

*** Trading Update – Equity and Sector Models ***

“As we kick off earnings season in earnest we are increasing our technology exposure where we have been underweight previously. In the equity model, we are adding 1% to our current holdings of ADBE and initiating a 2% position in AMD due to its breakout above its recent downtrend.

In the ETF model, we are adding 3% to XLK.” – 10/14/21

Equity Model

- Add 1% to ADBE bringing the total weight to 2.5%

- Initiating a 2% position in AMD.

ETF Model

- Add 3% to XLK bringing total weight to 13.5%

As always, our short-term concern remains the protection of your portfolio. Accordingly, we remain focused on the differentials between underlying fundamentals and market over-valuations.

Lance Roberts, CIO

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

Attention: The 401k plan manager will no longer appear in the newsletter in the next couple of weeks. However, the link to the website will remain for your convenience. Be sure to bookmark it in your browser.

Commentary

As noted last week, the market finally bounced solidly off of support and broke above the overhead resistance at the 100-dma and the 50-dma. The triggering of the underlying MACD “buy signals” suggests we have entered into the seasonally strong period of the year.

However, our weekly signals continue to suggest some caution despite the current short-term bullish improvements. There are currently several essential catalysts that could derail the market rally over the next couple of months, the most prominent of which is the Fed.

In the short term, we suggest maintaining exposures in plan portfolios and putting stored cash back to work in your selected allocation model. While we have not removed international, emerging, small and mid-cap funds from the allocation model, we suggest avoiding these areas for now and moving those allocations to domestic large-cap.

If you are close to retirement or are concerned about a pickup in volatility, there is nothing wrong with being underweight equities. However, there is likely not a lot of upside in markets heading into next year.

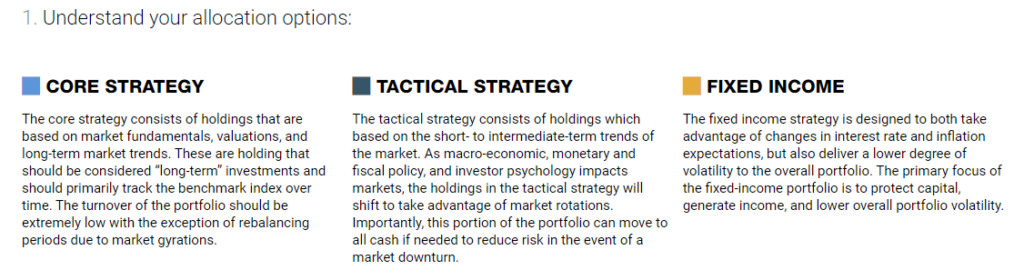

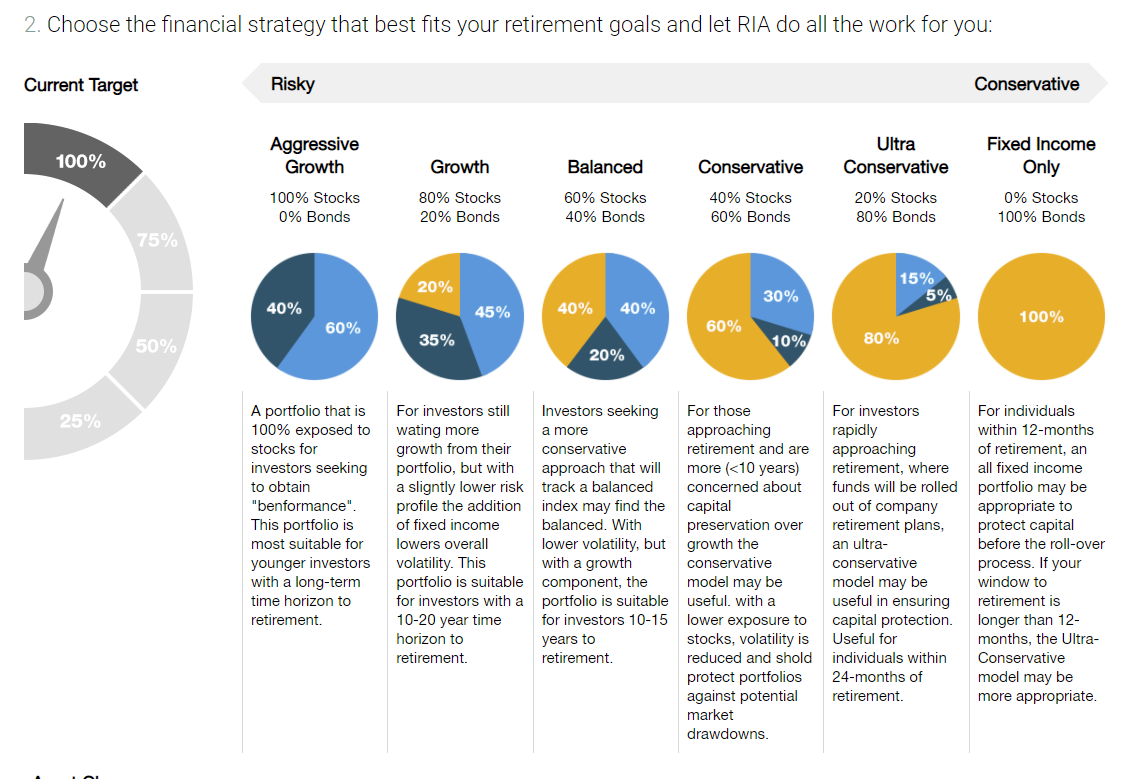

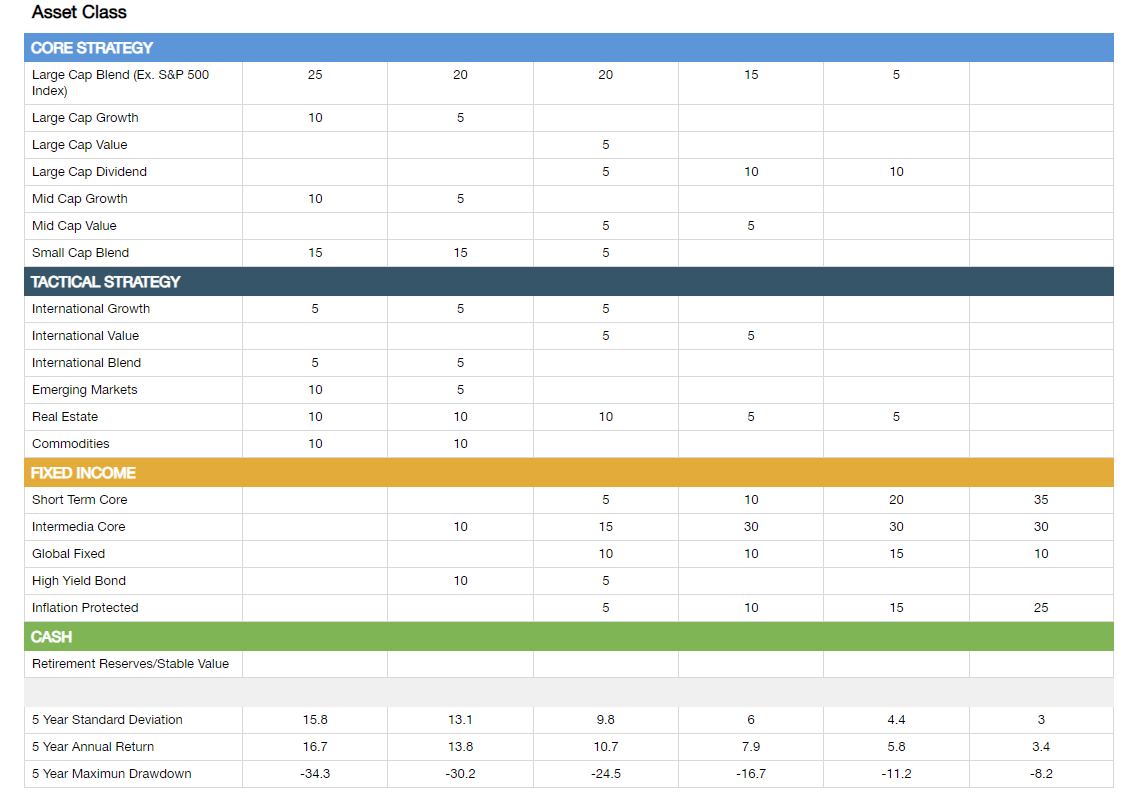

Model Descriptions

Choose The Model That FIts Your Goals

Model Allocations

If you need help after reading the alert, do not hesitate to contact me.

Or, let us manage it for you automatically.

401k Model Performance Analysis

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

Have a great week!

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read