In this 11-05-21 issue of “Did The Fed Just Set The Stock Market Up For A Crash.”

- Market Pushes Higher As Speculation Increases

- The Fed’s Third Mandate Takes Priority

- Weaker Economic Growth Coming

- Portfolio Positioning

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Is It Time To Get Help With Your Investing Strategy?

Whether it is complete financial, insurance, and estate planning, to a risk-managed portfolio management strategy to grow and protect your savings, whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

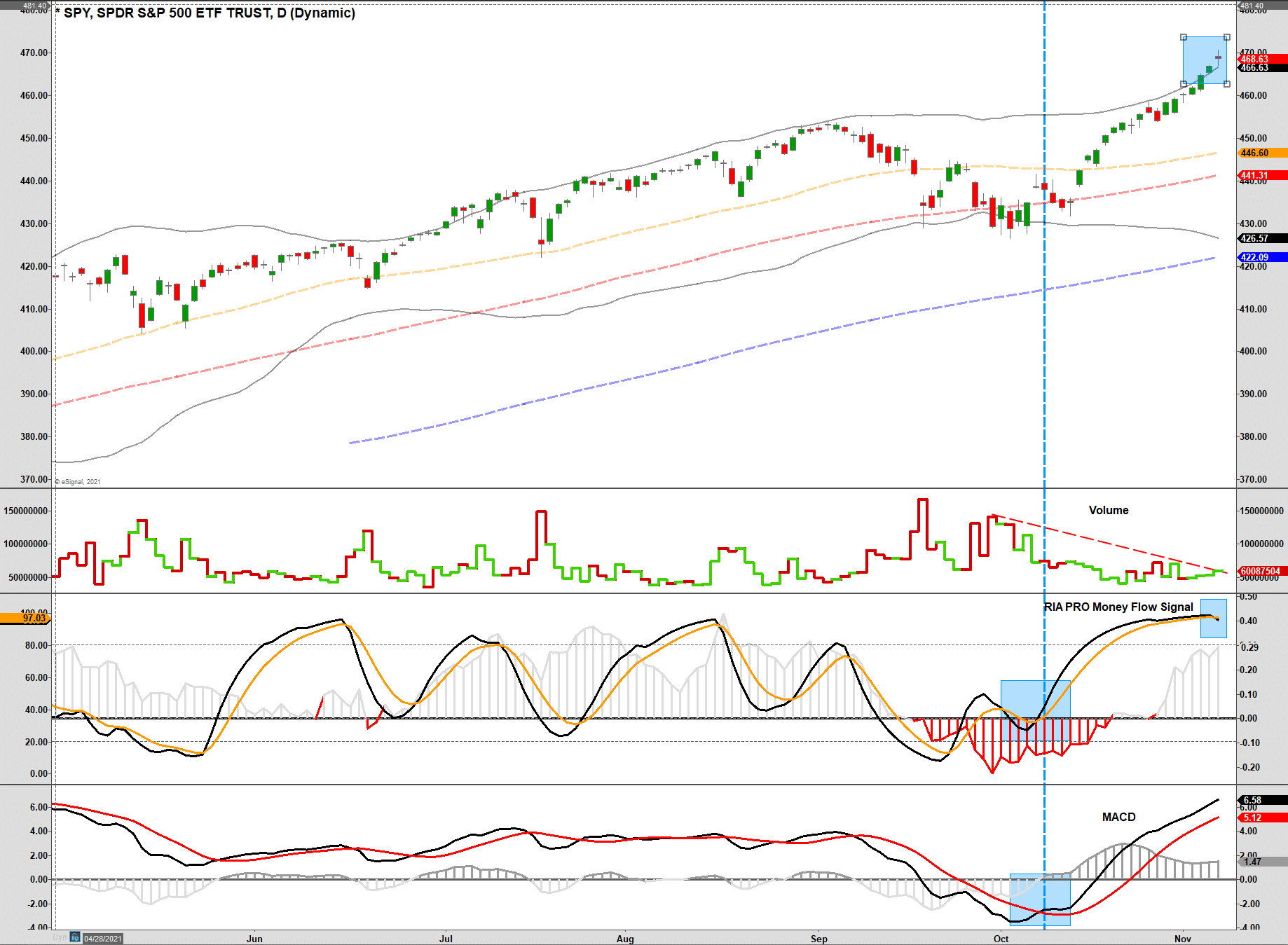

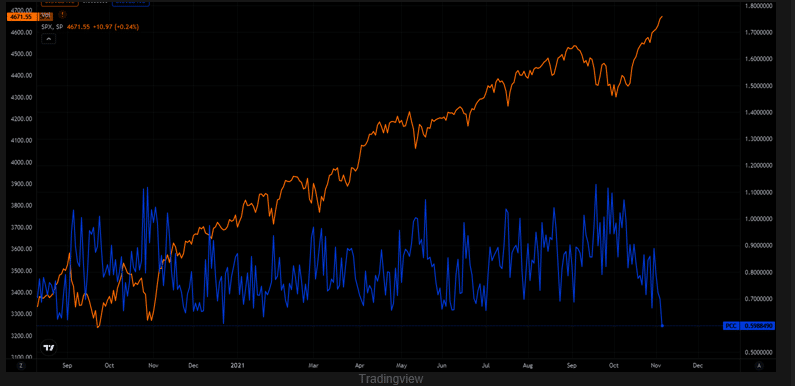

Market Back To Extreme Overbought

As noted last week, the more significant concern remains the underlying technical condition of the market. While the rally has been impressive, rising to all-time highs, the market is now back to more extreme overbought levels.

Furthermore, our “money flow buy signal” is near a peak and slightly triggered a “sell signal.” However, with the MACD still positive, the signal suggests a consolidation rather than correction. However, a confirming MACD often aligns with short-term corrections at a minimum. Therefore we will watch that signal closely. Also, this entire rally from the recent lows has been on very weak volume, which suggests a lack of commitment.

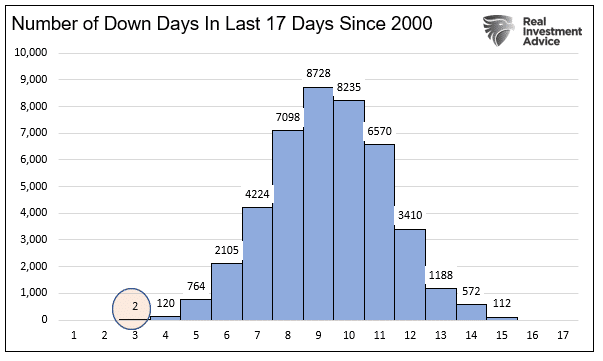

Currently, the bulls control the market as we are in the middle of a “buying stampede.” Historically, buying stampedes last on average between 7 and 12 days. Logically, buying stampedes always get followed by selling stampedes of similar lengths. However, there are times these stampedes can last much longer than expected.

We are currently in one of those longer-term periods. As shown below, the S&P 500 has only been down in 2 of the last 18 days. How unusual is that? In the previous 20-years of the S&P 500, the number of times the market accomplished such a feat was precisely ZERO.

Of course, that stampede gets driven by exuberance.

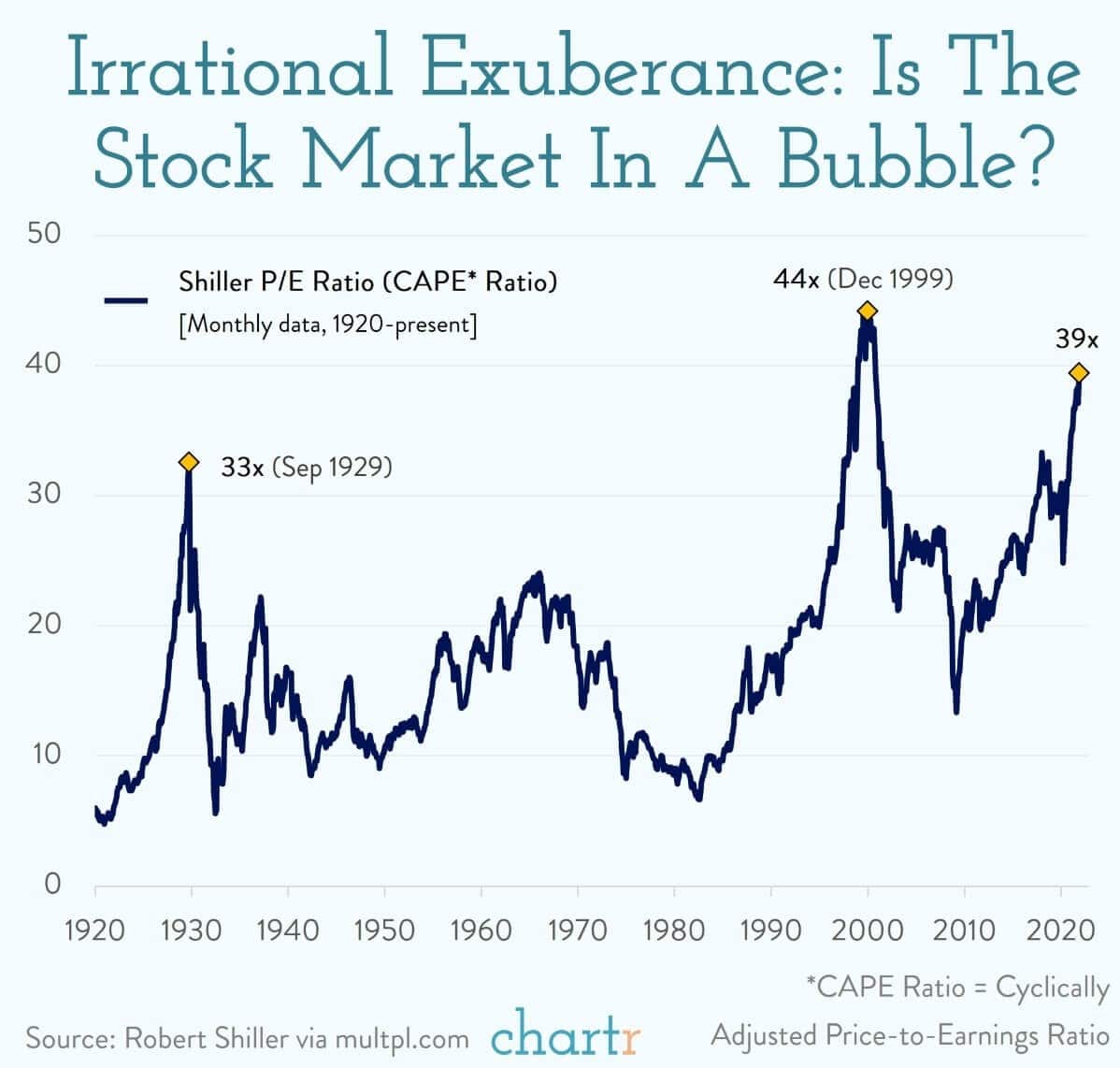

Irrational Exuberance

In our daily market commentary (click the banner below to subscribe for FREE morning delivery), we quoted a piece of analysis from Chartr.com. To wit:

“Every week it feels like we get a new headline about financial markets doing something unusual. Just this week we’ve had:“

- A “squid game” crypto token falling 99.99% in a few minutes.

- Tesla adding hundreds of billions of dollars in value over a deal with Hertz that hasn’t even been signed.

- US stock markets hitting fresh all-time-highs.

“All of which begs the question: are we in a bubble?”

So where are we now?

The latest CAPE ratio for the S&P 500 Index is 38x. That’s pretty close to the all-time record, which was 44x back in 2000. For those with a short memory, that was just before the dotcom bubble burst and stock markets (particularly tech) crashed hard.”

As we have noted previously, valuations, by themselves, are a terrible timing metric. However, they tell us a great deal about expected future returns and current market psychology.

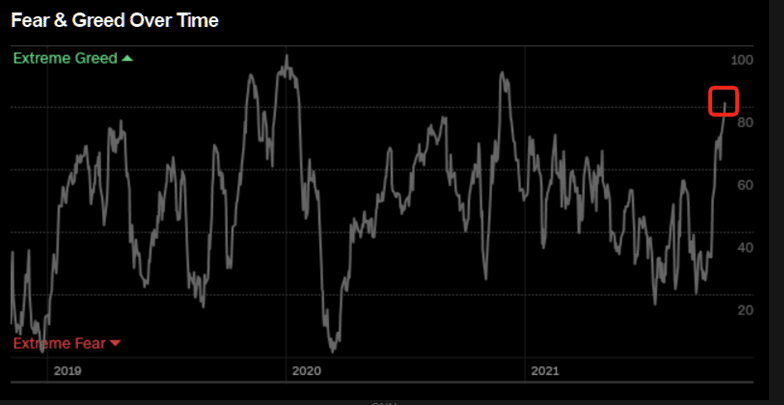

When it comes to “irrational exuberance,” there are other indicators better at revealing speculation in the markets that have preceded a stock market crash.

The CNN Fear/Greed index is now at extreme greed territory.

Furthermore, the demand for protection against a stock market crash (put options) fell to new lows.

Historically, such periods of “speculative” activity led to a minimum of short-term stock market corrections, but a crash is not beyond the realm of possibilities.

As noted above, with the market extremely overbought, speculative activity surging, and conviction weak, taking some actions to rebalance and manage risk is warranted.

However, for now, investors have “no fear” as they believe the Fed will continue to remain accommodative.

The Fed’s Third Mandate Takes Priority

My co-portfolio manager, Michael Lebowitz, made an important observation on Thursday.

“Jerome Powell made it clear the Fed is in no hurry to raise interest rates. ‘We don’t think it’s time yet to raise interest rates. There is still ground to cover to reach maximum employment, both in terms of employment and in terms of participation.’ The Fed’s reason is the employment picture is not back to pre-pandemic levels.

In our mind, there is plenty of evidence such as the outsize quits rate, rising wages, and the record number of job openings that scream the labor market is very healthy. Does Mr. Powell disagree with our assessment, or is there more to the Fed’s policy stance?

We believe he answered the question at Wednesday’s press conference. Per Jerome Powell:

‘The Fed’s policy actions have been guided by our mandate to promote maximum employment and stable prices for the American people along with our responsibilities to promote the stability of the financial system.‘”

The last sentence is the most important.

According to the Federal Reserve’s Congressional authorization, the Fed has only TWO mandates: price stability (inflation) and full employment.

The third mandate is a self-imposed mandate from Ben Bernanke, who was the Fed Chairman in 2010:

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

Fed Opts To Keep Markets Elevated

Jerome Powell ignored surging inflationary pressures and a robust job market in favor of supporting asset prices. With valuations surging, speculative activity rising, and investors heavily leveraged, the Fed faces a difficult choice.

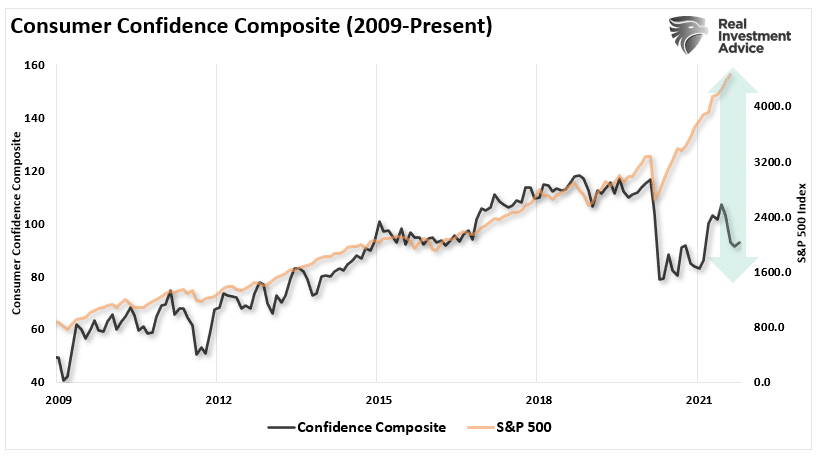

There is already a decoupling of markets from consumer confidence. A stock market crash would further devastate confidence pushing the economy into recession. That is the risk the Fed cannot afford.

However, while the Fed remains focused on keeping markets elevated, inflation poses a significant risk.

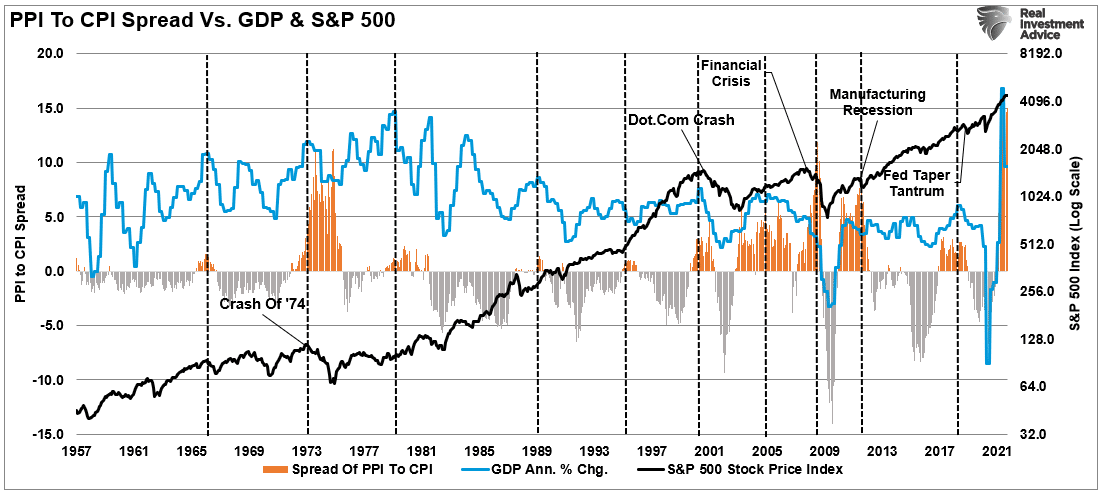

Currently, with PPI at the highest spread to CPI in history, it suggests producers can’t pass on costs to customers. Such equates to weaker profit margins and earnings in the future. However, if they elect to pass those costs onto consumers, such will raise living costs well above wages.

As Michael concluded:

“‘Promoting the stability of the financial system’ seems to be an unofficial mandate. Might the Fed be dragging their feet to reduce crisis-driven policy because they fear a stock market crash? More specifically, can extreme stock valuations be justified without an overly aggressive Fed?

The latest Fed meeting makes it increasingly clear that monetary policy changes are more a function of the asset markets and not the Fed’s congressionally stated mandates.”

Ignoring the inflation risk is likely unwise. Previous spikes in the inflation spread aligned with weaker economic growth, stock market contractions, or crashes.

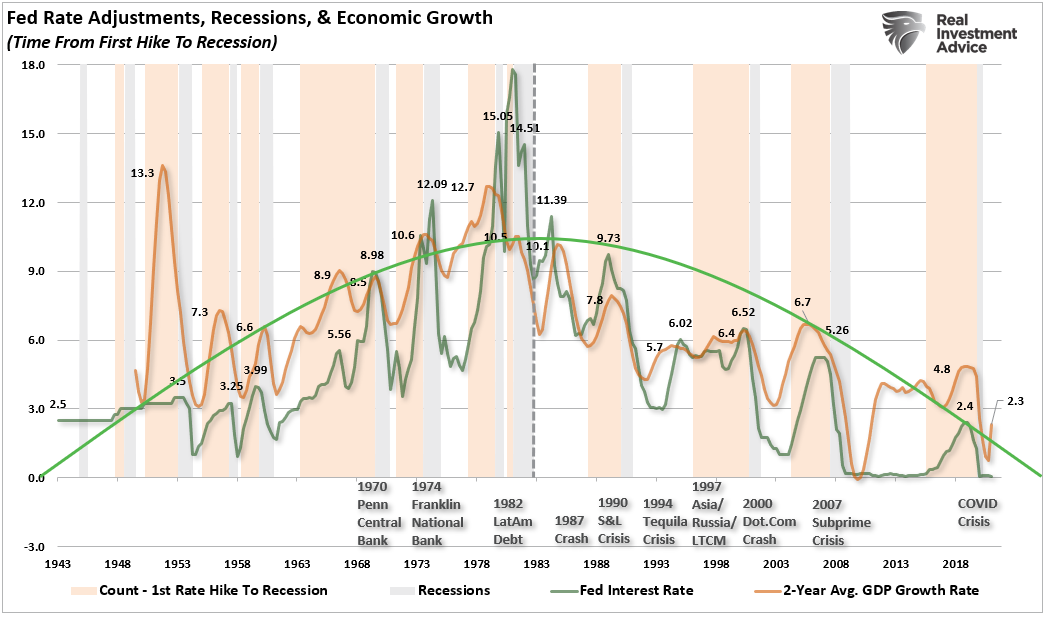

While the Fed should be tapering monetary policy and hiking rates to prepare for the next recessionary downturn, they will opt to keep asset prices inflating. However, just as in the past, opting to keep monetary policy too loose for too long eventually triggers a more significant crisis.

In Case You Missed It

Weaker Economic Growth Coming

While the Fed is busy supporting the equity markets, overvaluations, and speculative activity, the bond market has a different message. As discussed this past week, our expectation of weaker economic growth in 2022 is coming to fruition.

“The history of stock market crashes due to the Fed’s monetary intervention schemes is evident. Not just over the last decade, but since the Fed became ‘active’ in 1980.”

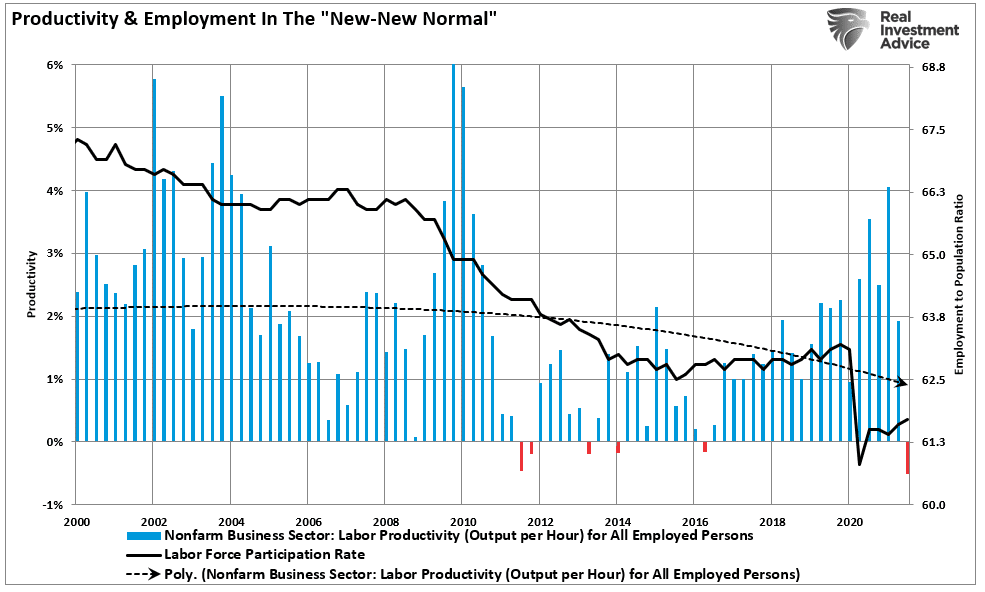

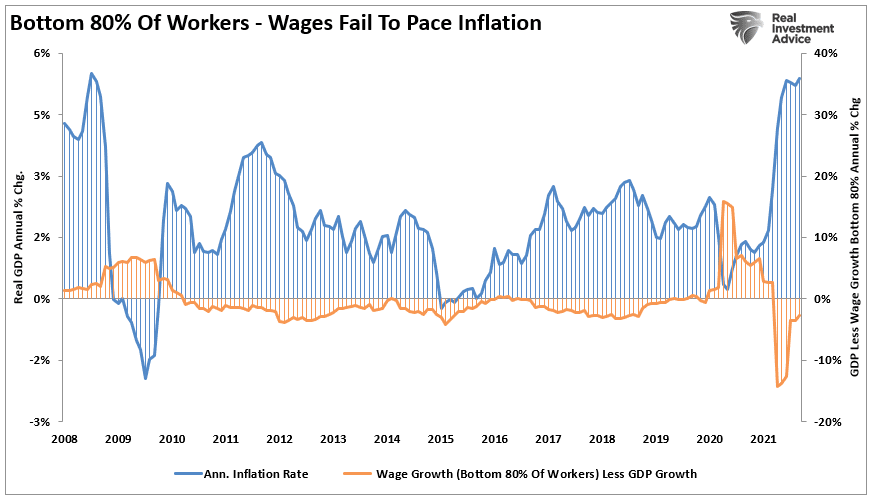

More evidence continues to support that view, as noted by the sharp drop in productivity despite jobless claims falling back to pre-pandemic levels. Thus, while the Fed hopes for “full employment,” such remains a function of “math” as the labor force shrinks.

More importantly, “real wages” are not keeping up with the inflationary surge.

Such will inevitably weigh on consumption which will weaken economic growth.

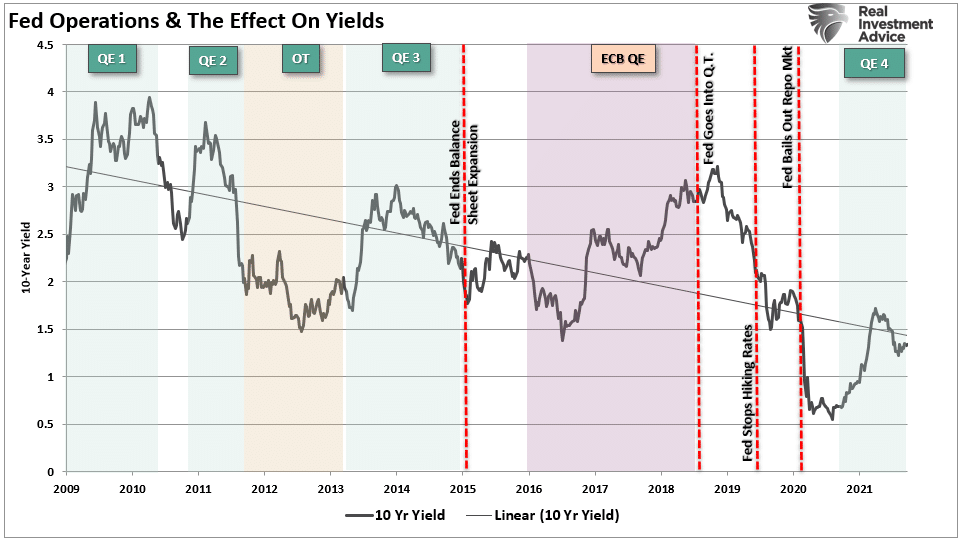

Lower Bond Yields On The Way

Are there currently risks to the bond market that investors should be concerned about near term? Yes. The current spike in inflation will likely last longer than expected due to the break of supply lines. Furthermore, rates tend to rise when the Fed begins to discuss “tapering” their bond purchases as they are doing now.

However, both of these issues will resolve themselves going forward. Eventually, the supply chain disruption will mend, and inflation will decline as supply comes back online.

More importantly, when the Fed does begin the process of “tapering” their bond purchases, yields historically fall as investors’ “risk-preference” shifts from “risk-on” to “risk-off.”

As if always the case with investing, timing, as they say, is everything.

Such is why, particularly with the Fed set to hike rates in 2022, we are looking for our next opportunity to add duration to our bond portfolios. Moreover, with the equity market grossly overvalued, we suspect that bonds will provide a chunk of our capital gains over the next couple of years.

There is little upside to the equity market given current valuations, slowing earnings growth, a weaker economy, and less liquidity. However, whenever the next recession approaches, yields will once again likely approach zero.

Got bonds?

Portfolio Update

The following is worth repeating:

“While anything is possible in the near term, complacency has returned to the market very quickly. However, there are numerous reasons to remain mindful of the risks.

- Earnings and profit growth estimates are too high

- Stagflation is becoming more prevalent (weak economic growth and rising inflation)

- Inflation indexes are continuing to rise

- Economic data is surprising to the downside

- Supply chain issues are more persistent than originally believed.

- Inventory problems continue unabated

- Valuations are high by all measures

- Interest rates are rising

“Furthermore, as noted above, there is limited upside as the annual rate of change in the market declines.”

As I mentioned several times this week on the RealInvestmentShow broadcast, we have started the process of reducing portfolio risk by rebalancing positions that have become grossly extended.

Let me be clear. We took profits; we did not sell the entirety of our position. Therefore, our portfolio allocations are near fully invested. However, our cash position is growing as the market becomes more aggressively extended.

I make this clarification for two reasons.

- Many assume that when I say we are adjusting for risk, that equals selling everyting and going to cash; and,

- Risk management is about small moves.

An old axiom is that football is a “game of inches.” The same holds in portfolio management. Trying to throw a “hail mary” on every down will likely wind up costing you the game. Sure, you could potentially get lucky, but eventually, luck runs out.

As Jim Cramer noted last week when discussing taking profits:

“Bulls get fat, pigs get fat, but hogs get slaughtered.”

It’s another old Wall Street axiom that often gets ignored but probably shouldn’t be.

Have a great weekend.

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

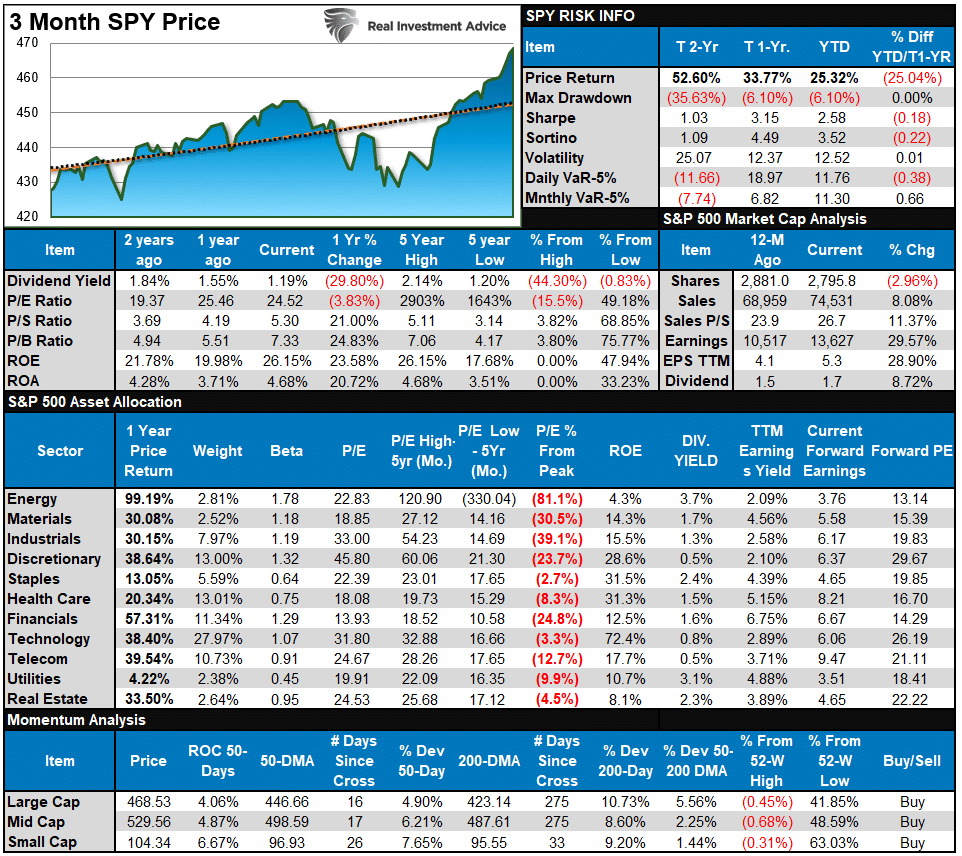

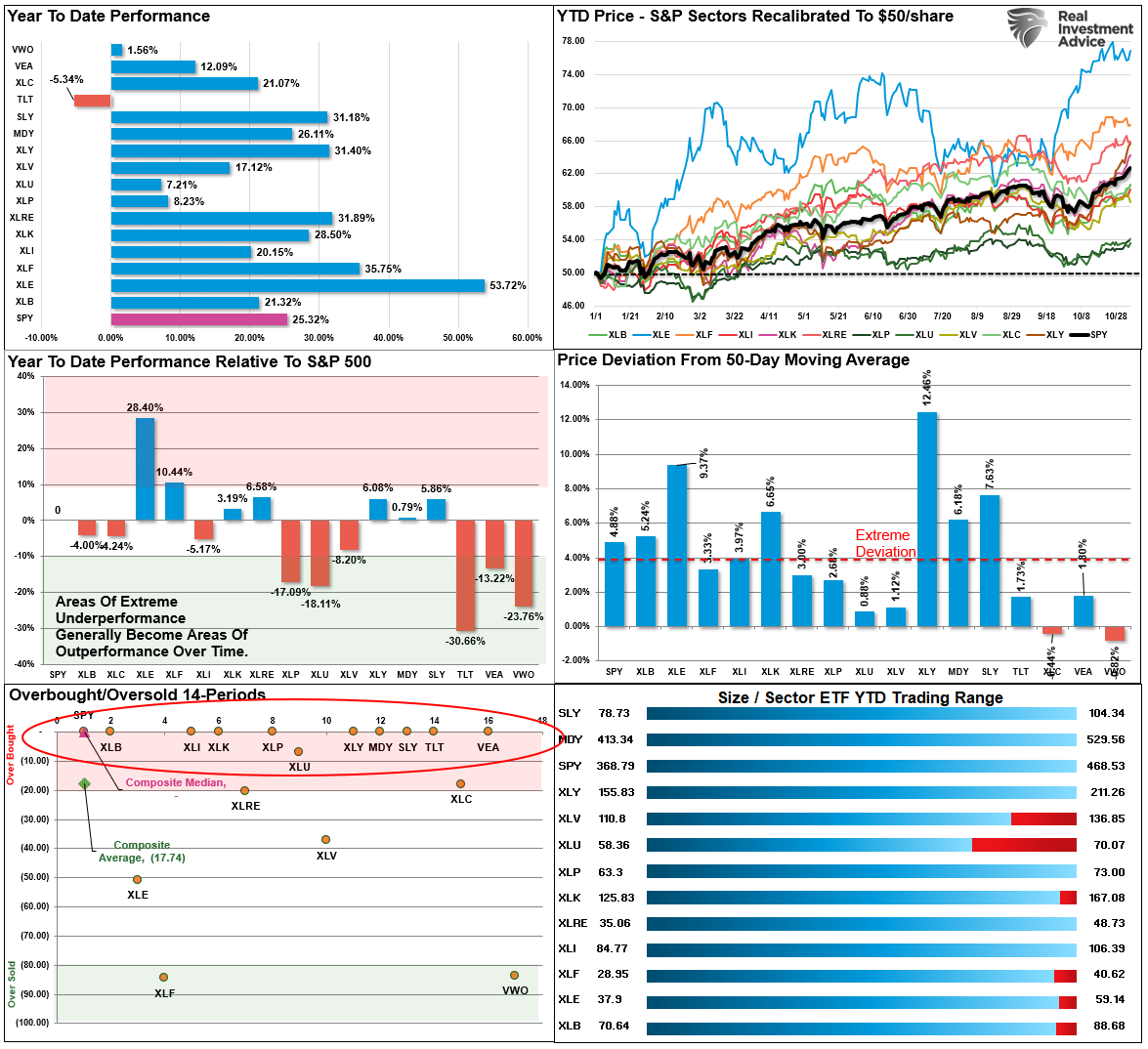

S&P 500 Tear Sheet

Performance Analysis

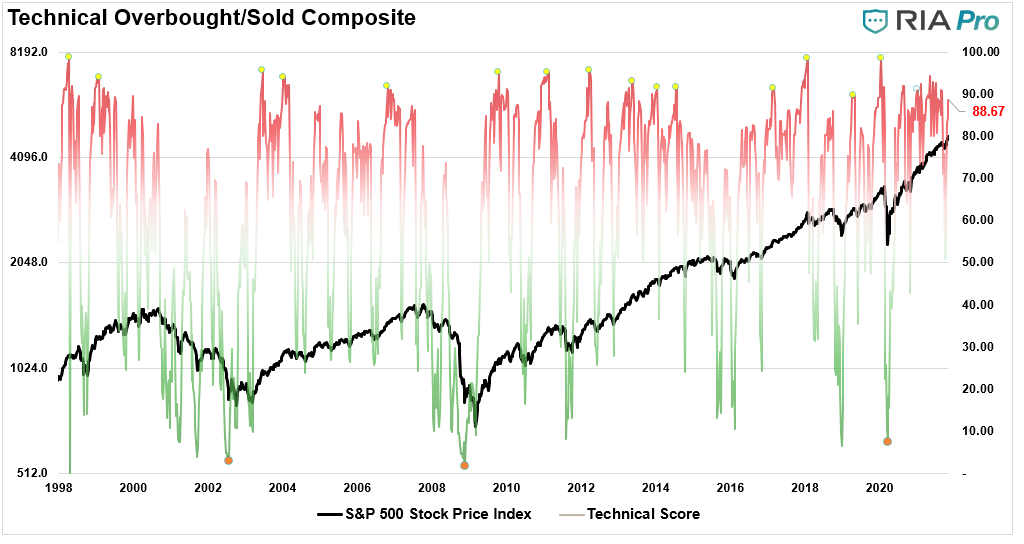

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 88.67 out of a possible 100.

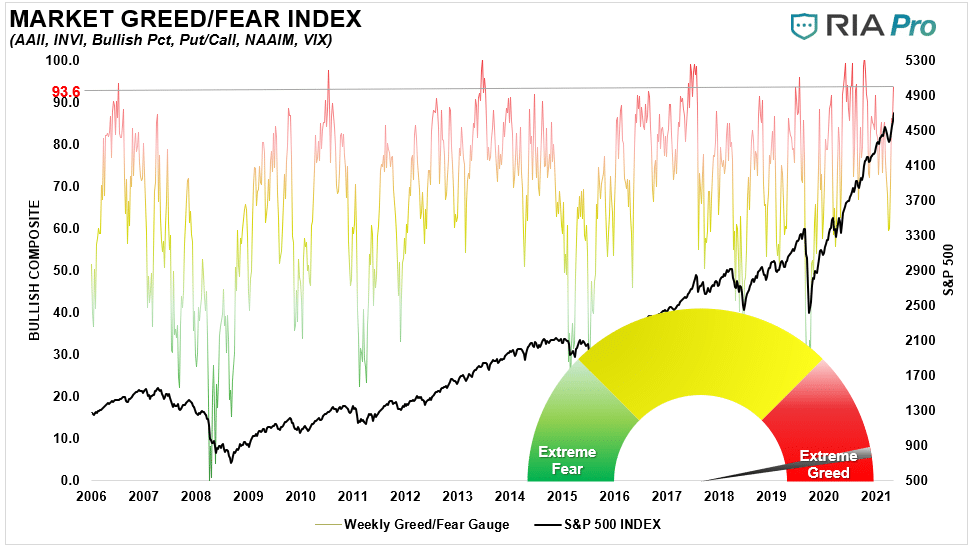

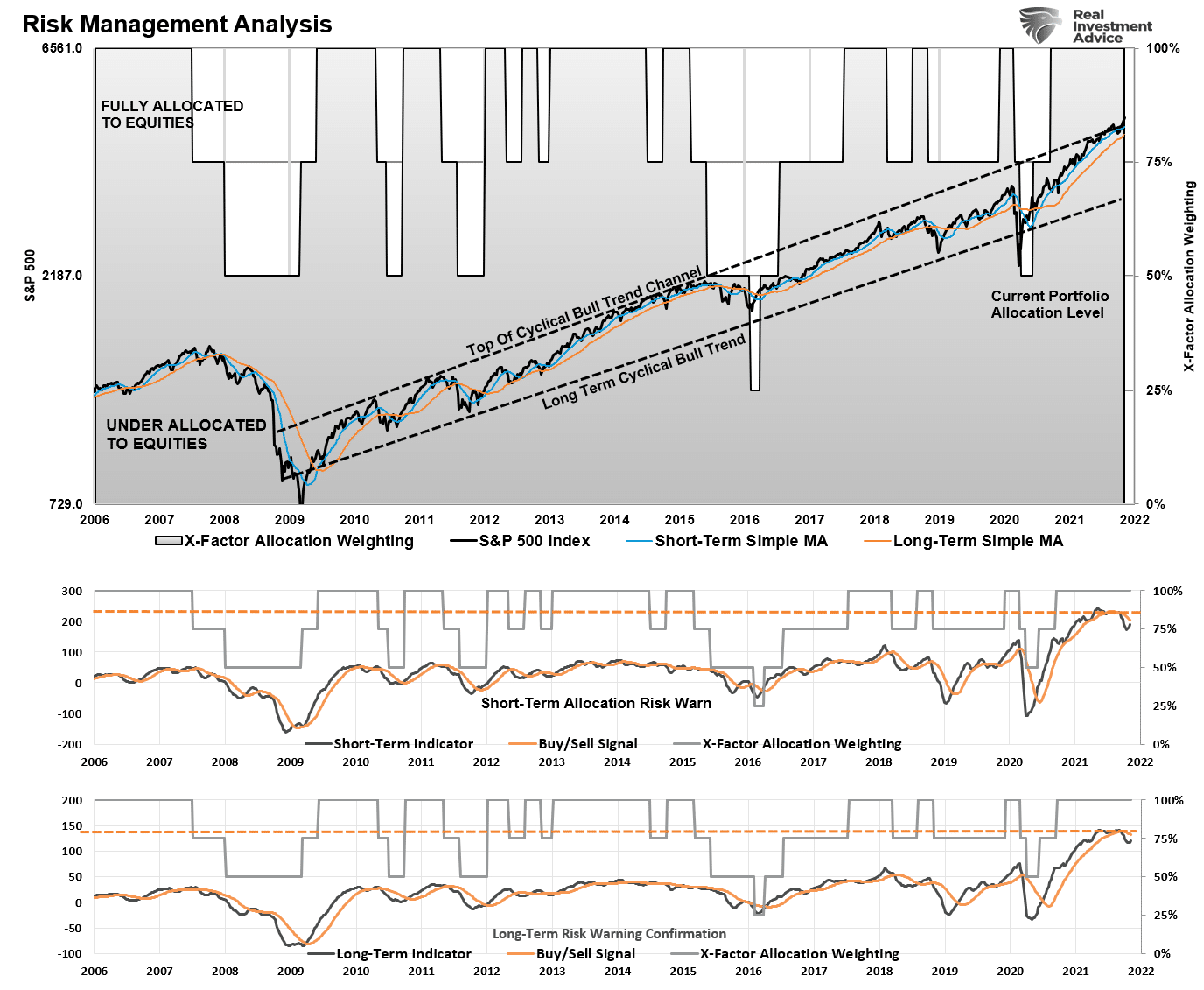

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 93.6 out of a possible 100.

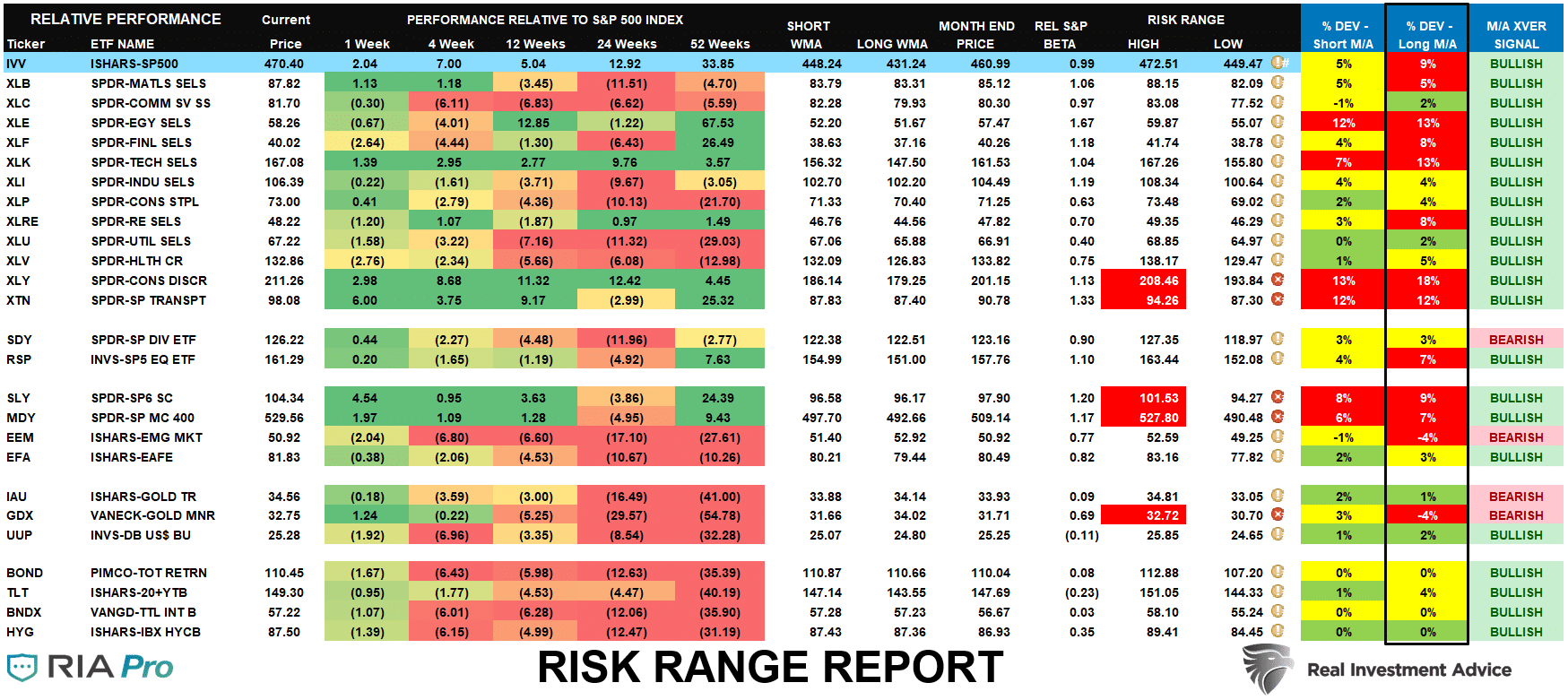

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

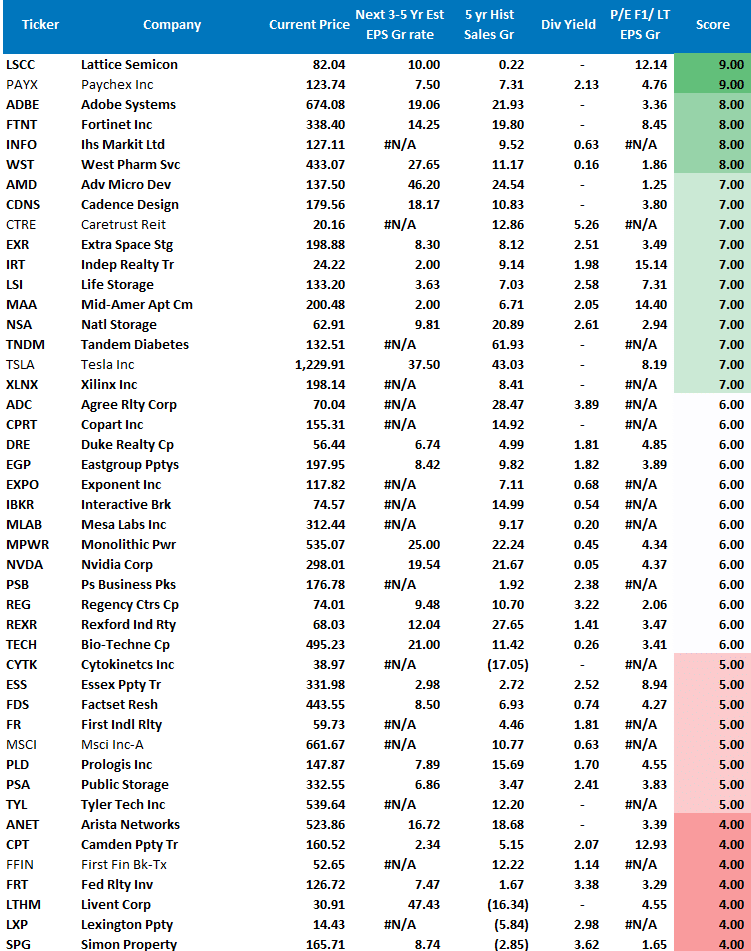

Weekly Stock Screens

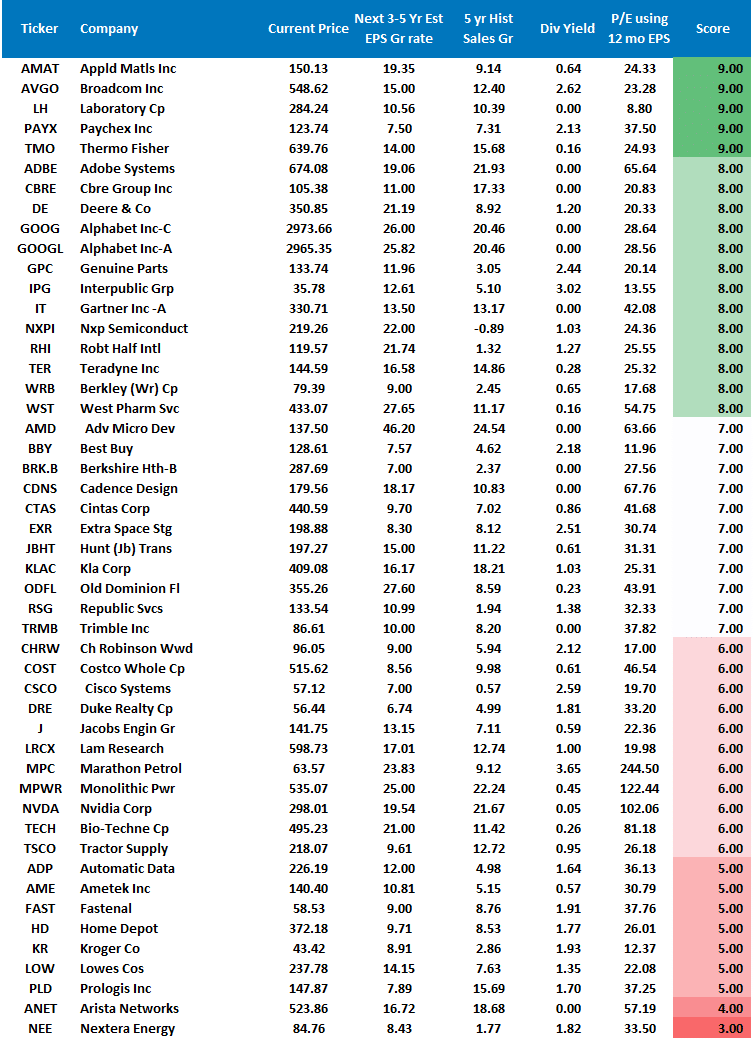

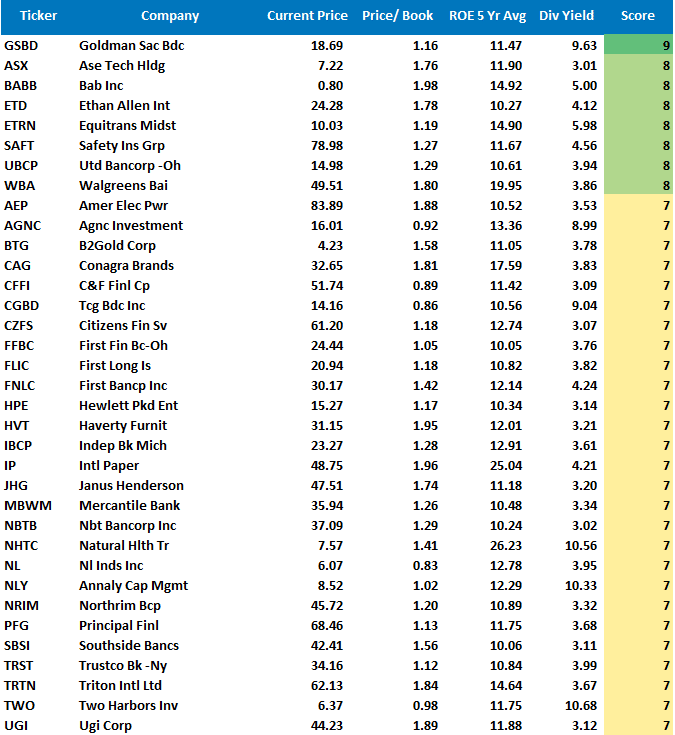

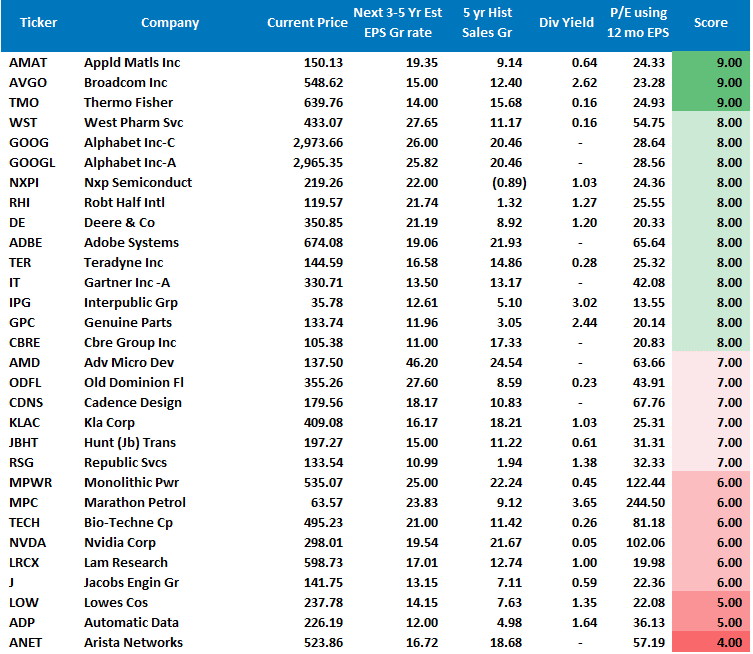

Currently, there are four different stock screens for you to review. The first is S&P 500 based companies with a “Growth” focus, the second is a “Value” screen on the entire universe of stocks, and the last are stocks that are “Technically” strong and breaking above their respective 50-dma.

We have provided the yield of each security and a Piotroski Score ranking to help you find fundamentally strong companies on each screen. (For more on the Piotroski Score – read this report.)

S&P 500 Growth Screen

Low P/B, High-Value Score, High Dividend Screen

Fundamental Growth Screen

Aggressive Growth Strategy

Portfolio / Client Update

It has been a stellar few weeks in the market. The speculative frenzy quickly returned to the market, and the fear of a correction has “gone with the wind.” However, as noted, the market is now back into more extreme overbought levels. Therefore, we have started taking profits in egregiously overbought positions.

As noted last week, there was not much to do in portfolios this week. However, several stocks did exceptionally well (NVDA, F, AMD, CVS, and AMZN), which boosted the whole portfolio. These were also some of the stocks we did reduce slightly to rebalance back to our risk management sizes.

We also are continuing to watch interest rates closely. While the Fed did proceed with their balance sheet taper announcement, they avoided discussing rate hikes. That will change as we move into 2022. Both of these actions will slow economic growth leading to a decline in yields. As a result, we patiently wait for another “buy point” to further increase our bond holdings’ duration.

Again, while it may seem counter-intuitive at the moment, the current bout of inflation will turn into deflation next year as liquidity gets drained from the system. Therefore, we continue to manage the deflationary side of our portfolio closely.

As noted, while there seems to be minimal risk in the market, don’t be misled. There are numerous risks we are watching that could lead us to reverse course rapidly. Our job remains to protect your capital first and foremost, but we want to capture gains when we can.

Portfolio Changes

During the past week, we made minor changes to portfolios. In addition, we post all trades in real-time at RIAPRO.NET.

*** Trading Update – Equity and Sector Models ***

“As noted earlier this week, with the market back to extreme overbought and extended levels, and individual names making outsized moves, we are taking some small profits out of our most egregiously extended positions.

In the equity model, we are reducing CVS Health (CVS) from 3.5% of the portfolio to 3%.” – 11/04/21

Equity Model

- Reduce CVS from 3.5% to 3.0% of the portfolio.

“The market is now back to extreme overbought and extended levels. As such, we are now taking some small profits out of our most egregiously extended positions.

In the equity model, we are taking some profits in F, NVDA, ALB, and NFLX back to model weights. We are also selling all of SBUX after it violated our stop levels.

In the sector model, we are reducing LIT by 0.5% as it is overbought like ALB. We remain decently overweight in the basic materials sector.” – 11/02/21

Equity Model

- Reduce to model weight F, NVDA, ALB, and NFLX

- Sell 100% of SBUX

ETF Model

- Reduce LIT by 0.5% of the portfolio weight.

As always, our short-term concern remains the protection of your portfolio. Accordingly, we remain focused on the differentials between underlying fundamentals and market over-valuations.

Lance Roberts, CIO

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

Attention: The 401k plan manager will no longer appear in the newsletter in the next couple of weeks. However, the link to the website will remain for your convenience. Be sure to bookmark it in your browser.

Commentary

The bull market continued again this week, pushing into more extreme overbought territory. While there is little reason to be concerned about a more significant correction at this juncture, a period of weakness would not be surprising. With the mutual fund distribution season approaching, such could weigh on the markets in the first two weeks of December. However, such would set the market up for the traditional “Santa Claus” rally.

Therefore, if you have taken no action over the last couple of weeks, we suggest rebalancing your holdings and reducing portfolio risk. Most likely, your equity exposure is above target allocations, with bonds under-allocated. In the short term, we suggest maintaining exposures in plan portfolios but continue putting new contributions back into cash or stable value holdings for now.

While we have not removed international, emerging, small and mid-cap funds from the allocation model, we suggest avoiding these areas for now and moving those allocations to domestic large-cap.

If you are close to retirement or are concerned about a pickup in volatility, there is nothing wrong with being underweight equities. However, there is likely not a lot of upside in markets heading into next year.

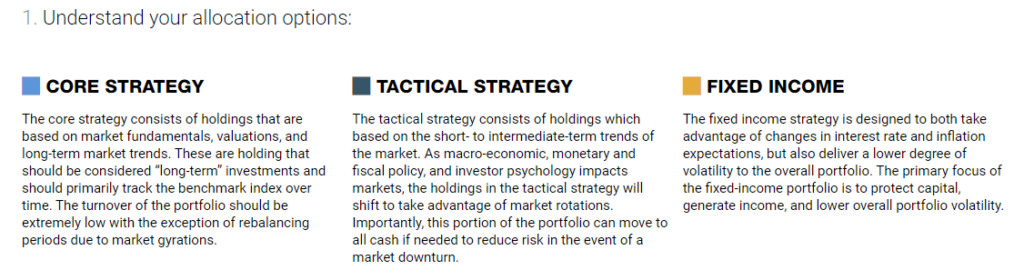

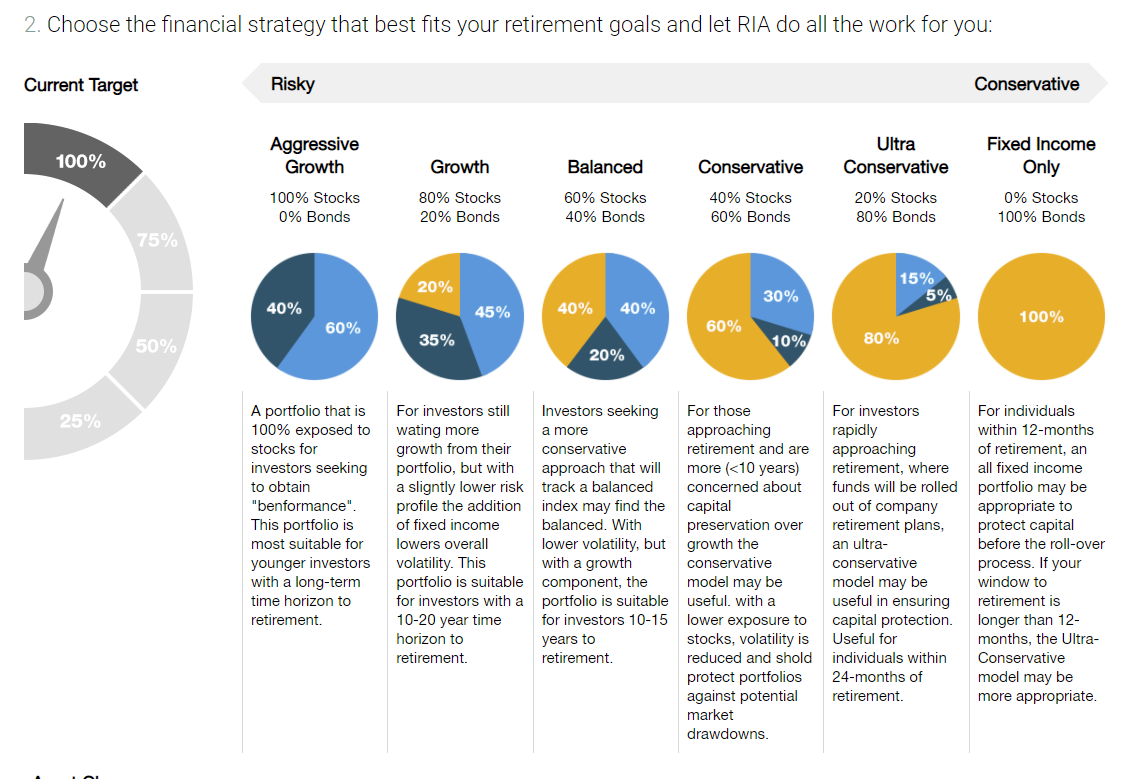

Model Descriptions

Choose The Model That FIts Your Goals

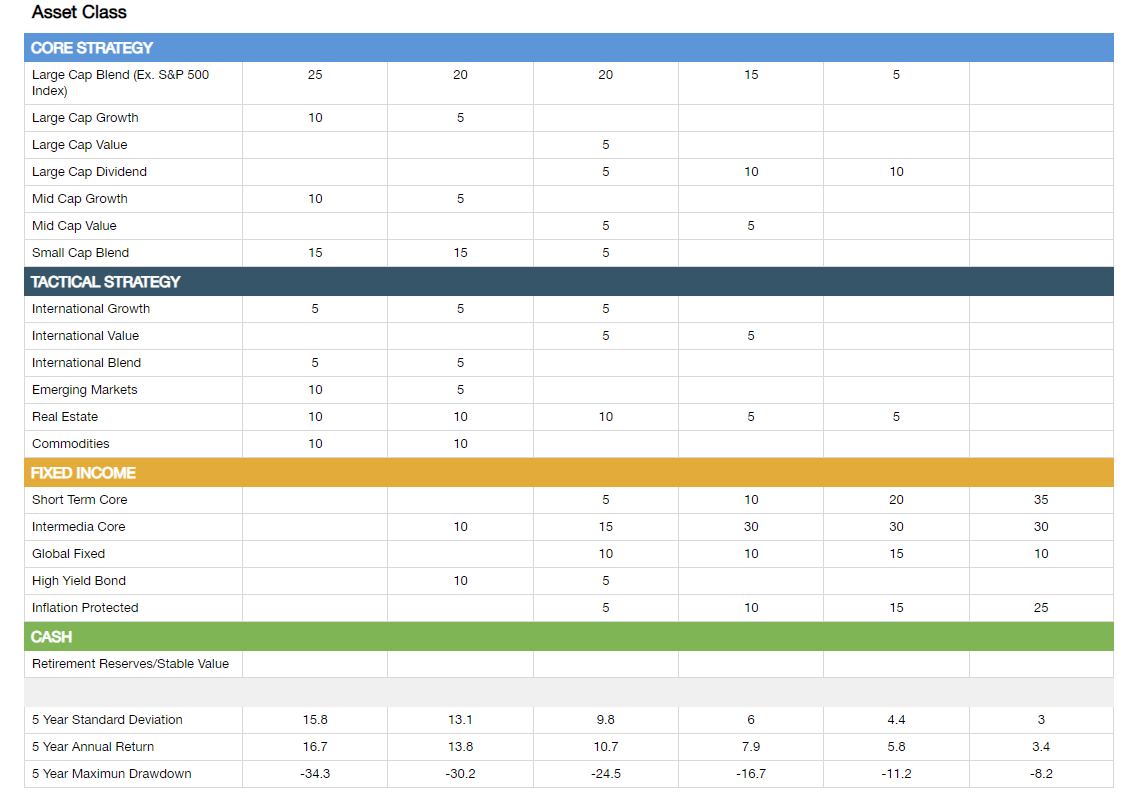

Model Allocations

If you need help after reading the alert, do not hesitate to contact me.

Or, let us manage it for you automatically.

401k Model Performance Analysis

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

Have a great week!

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read