Retail Sales Data Suggests A Strong Consumer Or Does It

The latest retail sales data suggests a robust consumer, leading economists to become even more optimistic about more robust economic growth this year. To wit:

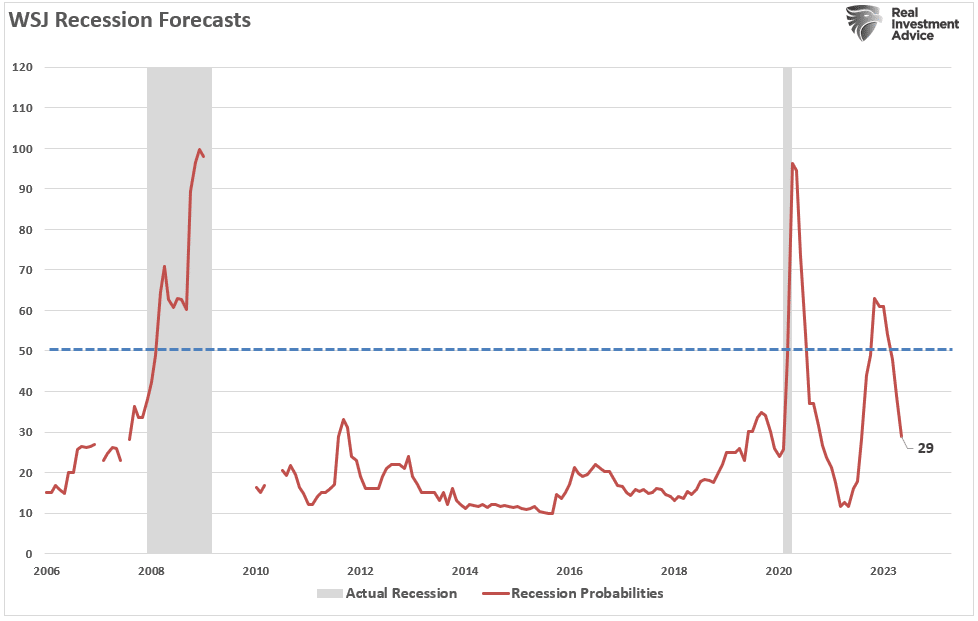

“It has been two years since forecasters felt this good about the economic outlook. In the latest quarterly survey by The Wall Street Journal, business and academic economists lowered the chances of a recession within the next year to 29% from 39% in the January survey. That was the lowest probability since April 2022, when the chances of a recession were set at 28%.

Economists don’t think the economy will get even close to a recession. In January, they, on average, forecast sub-1% growth in each of the first three quarters of this year. Now, they expect growth to bottom out this year at an inflation-adjusted 1.4% in the third quarter.” – WSJ

According to the March retail sales data, consumer spending added “fuel” to economists’ exuberance about this year.

Rising inflation in March didn’t deter consumers, who continued shopping at a more rapid pace than anticipated, the Commerce Department reported Monday. Retail sales increased 0.7% for the month, considerably faster than the Dow Jones consensus forecast for a 0.3% rise though below the upwardly revised 0.9% in February, according to Census Bureau data that is adjusted for seasonality but not for inflation.” – CNBC

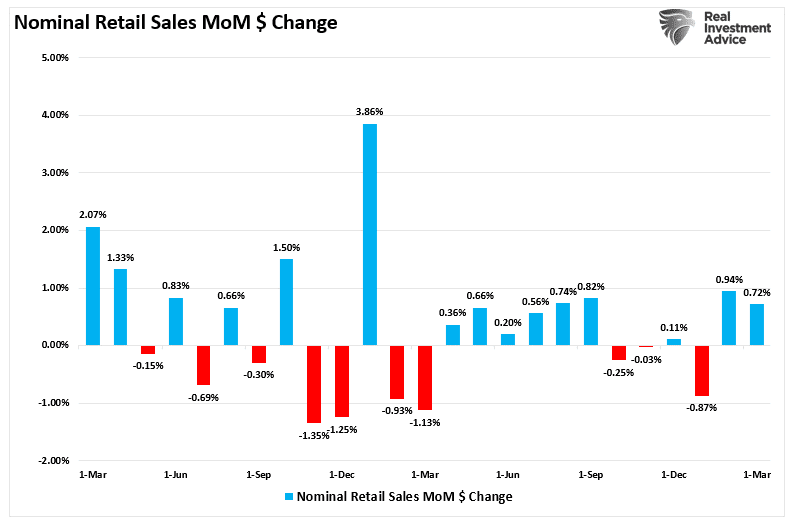

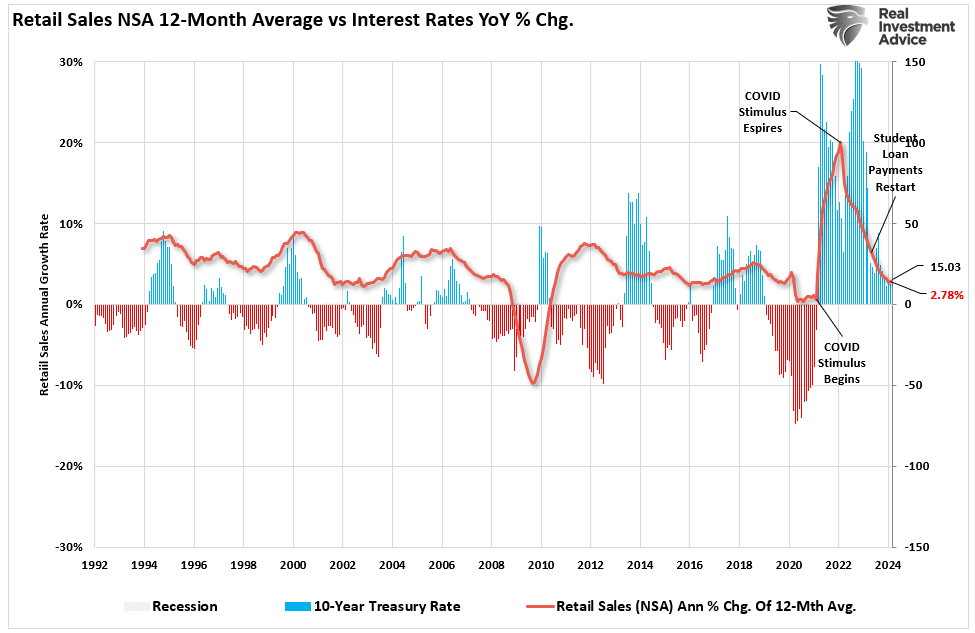

The chart below shows the monthly change in the retail sales data over the last two years.

While mainstream economists trumpeted the strength of the consumer, the March retail sales data had some interesting points worth noting.

First, retail sales data was extraordinarily weak from October to January, the traditionally strongest shopping months of the year. That period included Halloween, Thanksgiving, Christmas, and NYear’sr’s. So, to some degree, the strength of spending over the last two months is unsurprising as, eventually, consumers need to buy goods or services previously postponed.

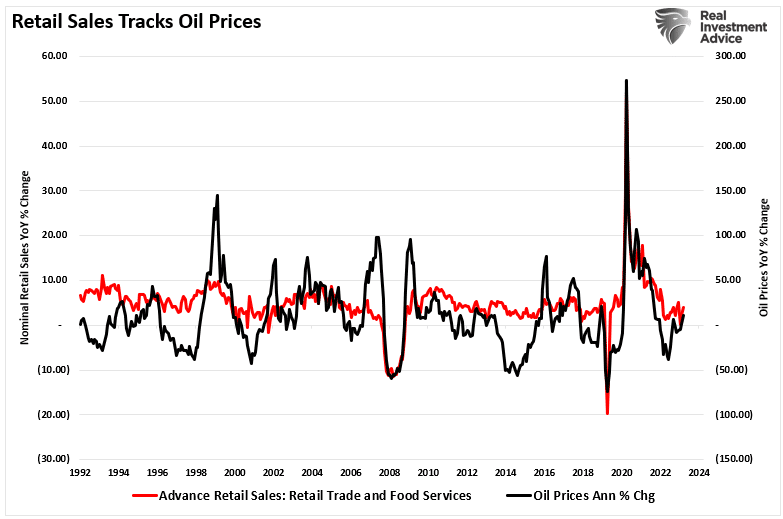

Secondly, while the March retail sales data was strong, it was weaker than February. However, March contained two significant spending periods, Spring Break and Easter, which generally don’t occur. Since Spring Break and Easter are considerable travel and shopping periods, it is unsurprising that the retail sales data increased with oil prices rising. As shown below, there is a very high correlation between nominal retail sales and oil prices.

Paying More For The Same Amount

Economists often overlook another important point about the retail sales data. As noted above, the March retail sales report was NOT adjusted for inflation. Furthermore, the report is in nominal “dollar volume” and not the amount of goods or services sold. Oil and gasoline prices are an excellent example of the issue with the retail sales data.

Let’s assume you own a car with 18-gallon fuel tank. Your daily activities are mostly going to work, going to the grocery store, eating out, having entertainment, etc. As such, you consume one tank of gas each week. Here is the math:

Week 1: 18-gallons of gas @ $3/gallon = $54.

That week, the store adds $54 to the monthly retail sales total for selling 18 gallons of gasoline. However, the price will increase to $4 per gallon next week.

Week 2: 18-gallons of gas @ $4/gallon = $72.

Here is the question.

While the retail sales data increased by $18 in week two, did the consumer purchase more gasoline? In other words, if the economy’s strength is ultimately measured by how much we produce (gross domestic product), then does spending more for the same amount of goods or services equate to a stronger economy?

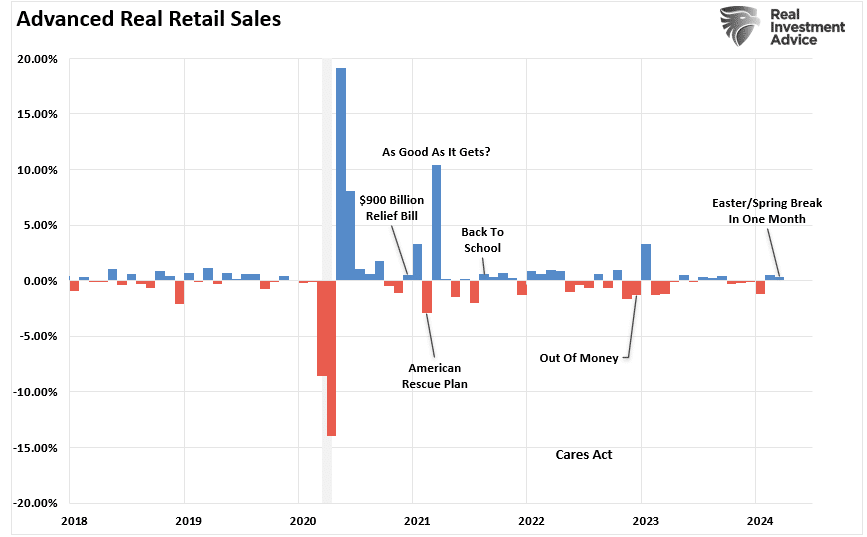

The picture is quite different if we adjust the nominal retail sales data for inflation. Again, it is unsurprising that even on an inflation-adjusted basis, retail sales rose in February after declining for four months previously. However, with March containing Spring Break and Easter, the data suggests a weaker consumer that headlines tout.

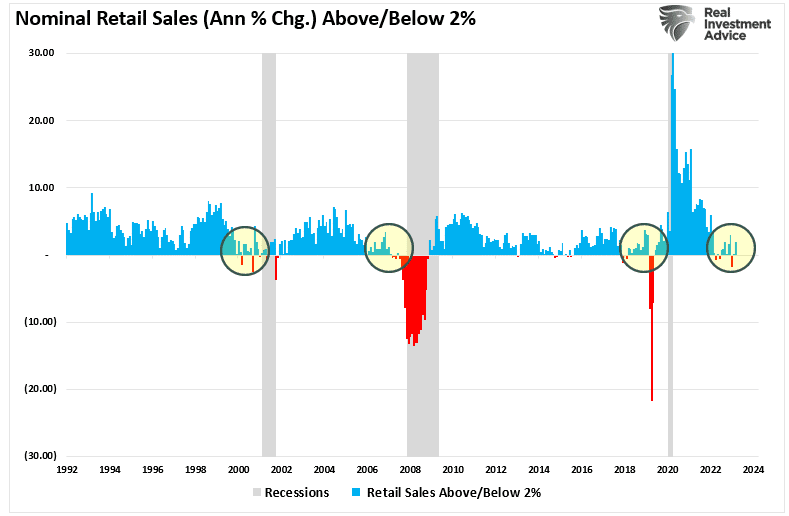

It is worth noting that retail sales data is not very useful in determining whether the economy is nearing a recession. As shown below, an annual growth rate of 2% has been a good marker for economic growth. As such, retail sales should grow at roughly 2% annually as well, given that personal consumption expenditures comprise approximately 70% of the economic equation. However, other than 2007, retail sales did not clarify economic strength.

In other words, spending more for the same amount of goods and services is not a sign of economic strength.

Economic Forecasts Tend To Be Erroneous

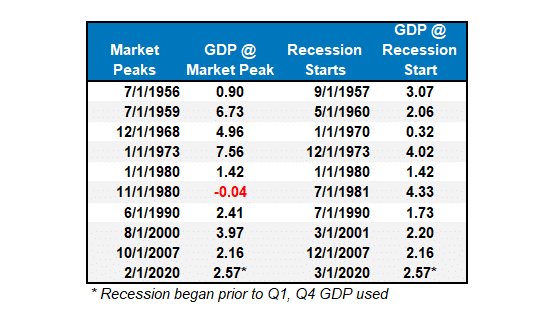

Furthermore, while the recent nominal sales data was robust, it is crucial to remember the economic data has a significant lag. Each of the dates below shows the economy’s growth rate immediately before the onset of a recession. You will note in the table that in 7 of the last 10 recessions, real GDP growth was running at 2% or above. In other words, according to the media, there was NO indication of a recession. But the next month, one began.

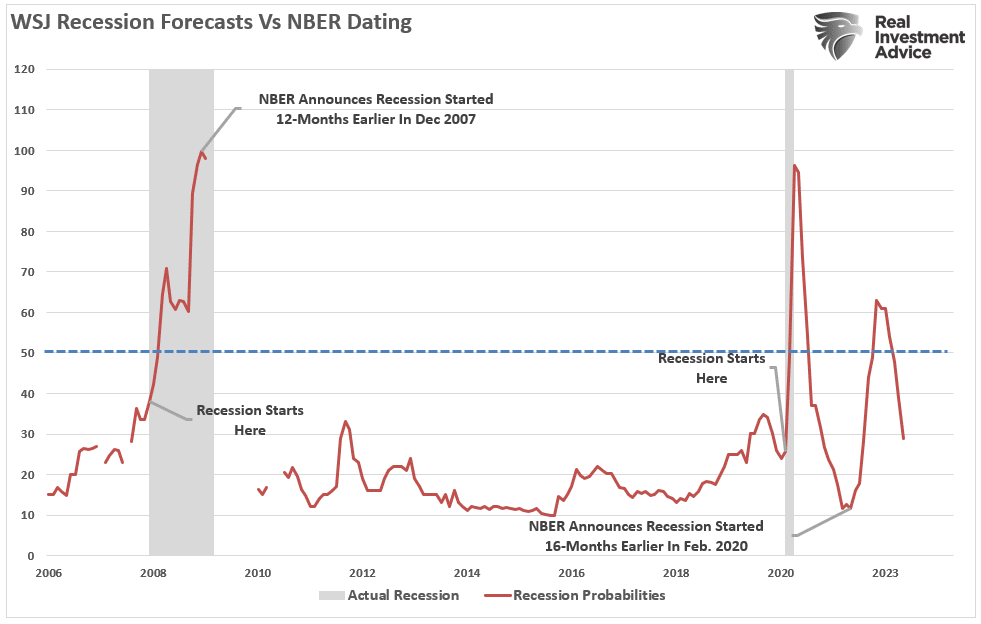

Crucially, I am not saying a recession is starting next month. However, I suggest that relying heavily on one month’s retail sales data to claim the economy avoided a recession is not likely ideal. Let’s revisit that chart of the WSJ economic forecast. I have added two notations: the start and end of recessions and when the NBER officially dated that period. As shown in both previous recessions, WSJ economists had a very low probability of the economy entering a recession just before it occurred.

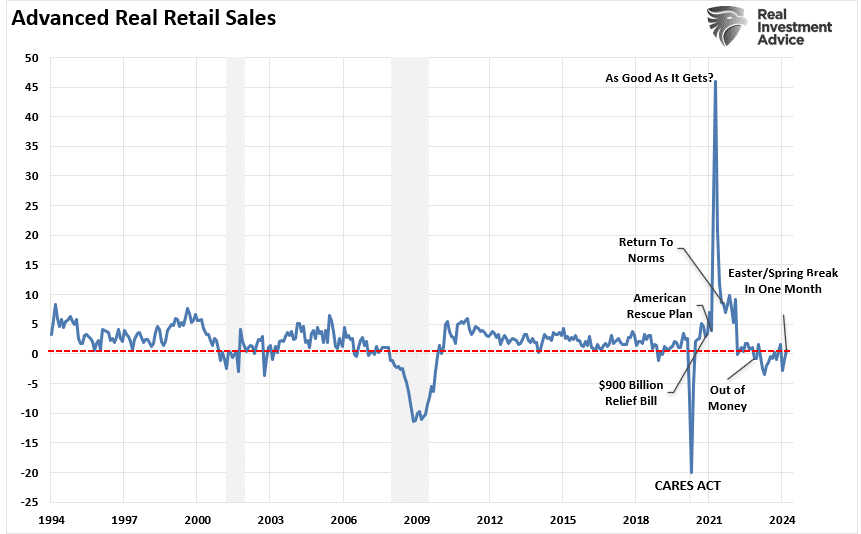

The reality is that on an inflation-adjusted basis, the retail sales data suggests the consumer remains weak. While spending more to buy the same amount of goods or services may look good on paper, the average household has less money to spend elsewhere. As shown, the annual rate of change in real retail sales is near some of the lowest levels outside of a recession.

Lastly, consumer credit supporting retail sales will become more problematic with rising interest rates. Higher interest rates tend to reduce the average growth rate of retail sales data.

Our advice is to remain cautious about economic exuberance. Those forecasts are often disappointing.

Just A Correction, Or Is The Bull Market Over?

Is this just a correction after a strong bullish advance from November, or is the bull market ending? If you read some of the headlines, you would suspect the latter. As noted by MarketWatch last week:

“For the first time since early November 2023, less than 30% of S&P 500 stocks are trading above their 50-day moving average — a clear indicator of the current poor market’s breadth. This significant drop from the 85% observed in late March and 92% at the beginning of January highlights a dramatic reversal in market dynamics.

The 50-day moving average is often seen as a barometer for the short-term health of stocks. Falling below this level en masse suggests that a broad swath of the market is facing downward pressure. This shift comes amid escalating geopolitical tensions in the Middle East and renewed concerns over inflation, which have collectively nudged traders towards a more guarded stance in April.”

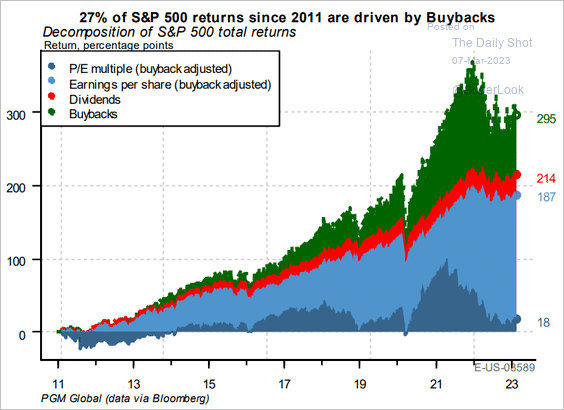

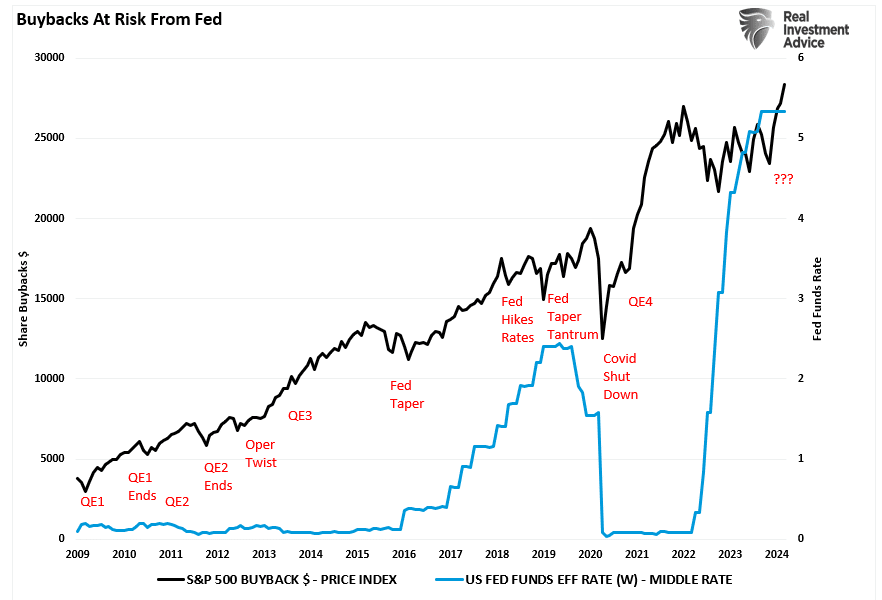

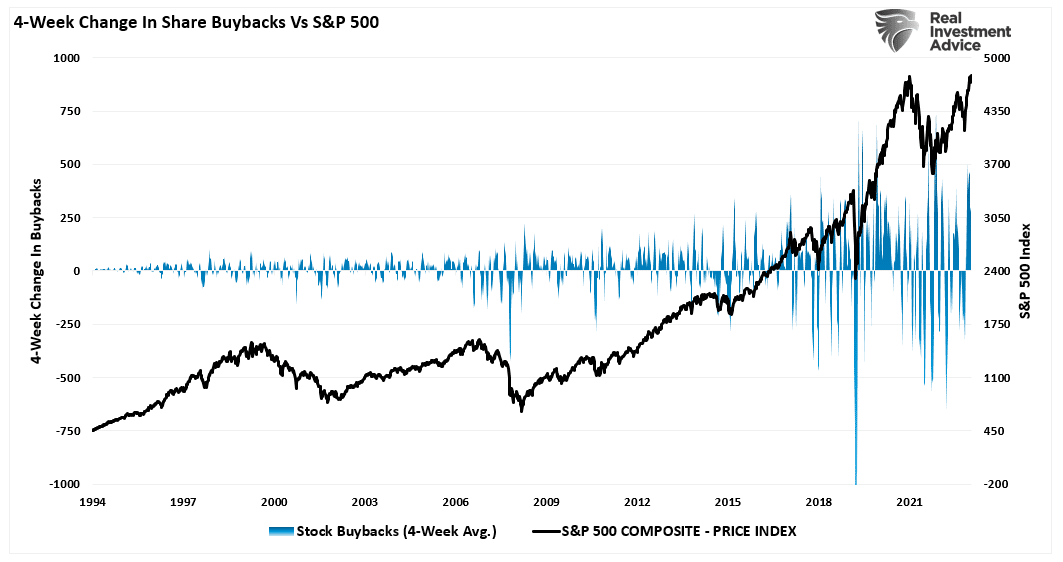

Of course, there are many “reasons” lately for the drop in stock prices. Geopolitical stress between Israel and Iran and hotter-than-expected inflation data that paused Fed rate cuts brought sellers into the market. However, none of this is shocking, as we previously noted in “Blackout Of Buybacks:”

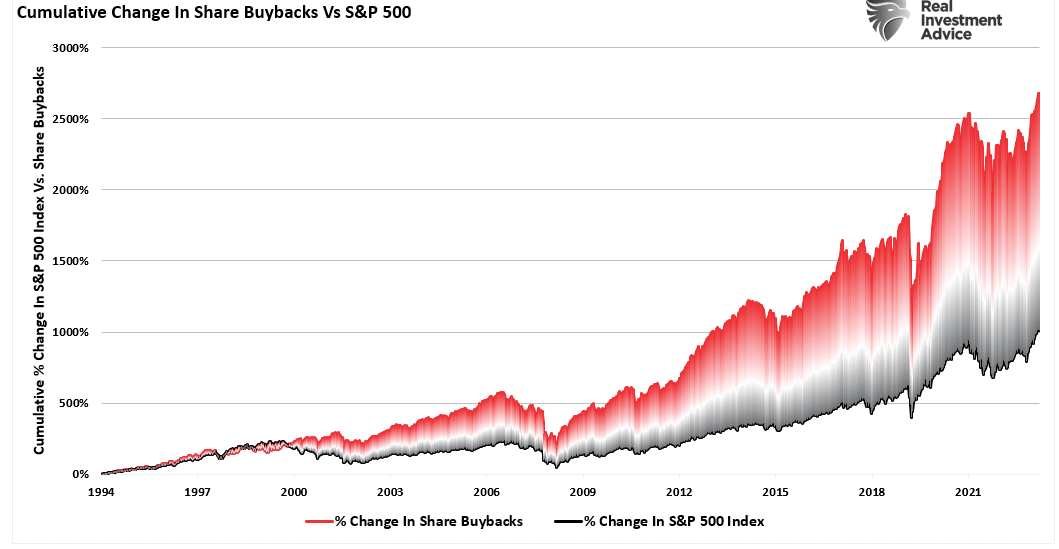

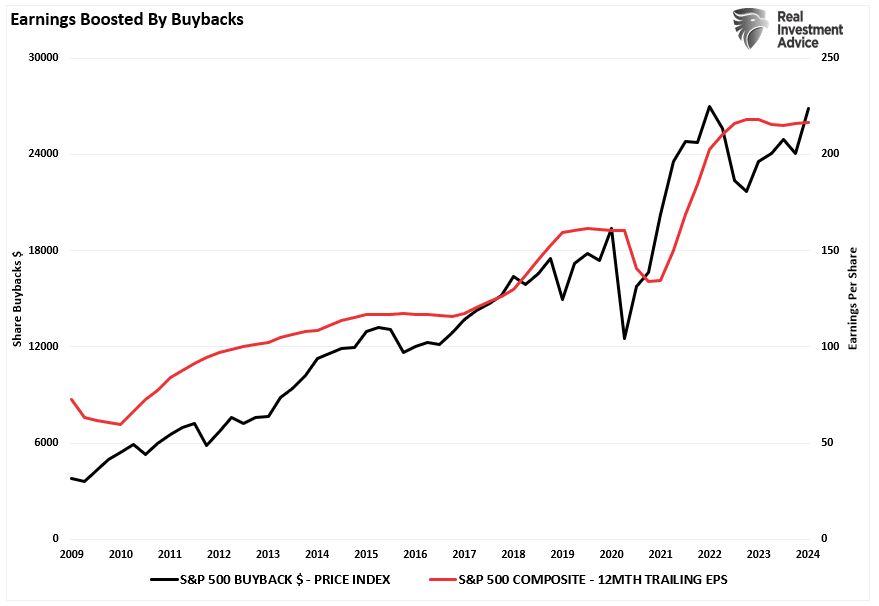

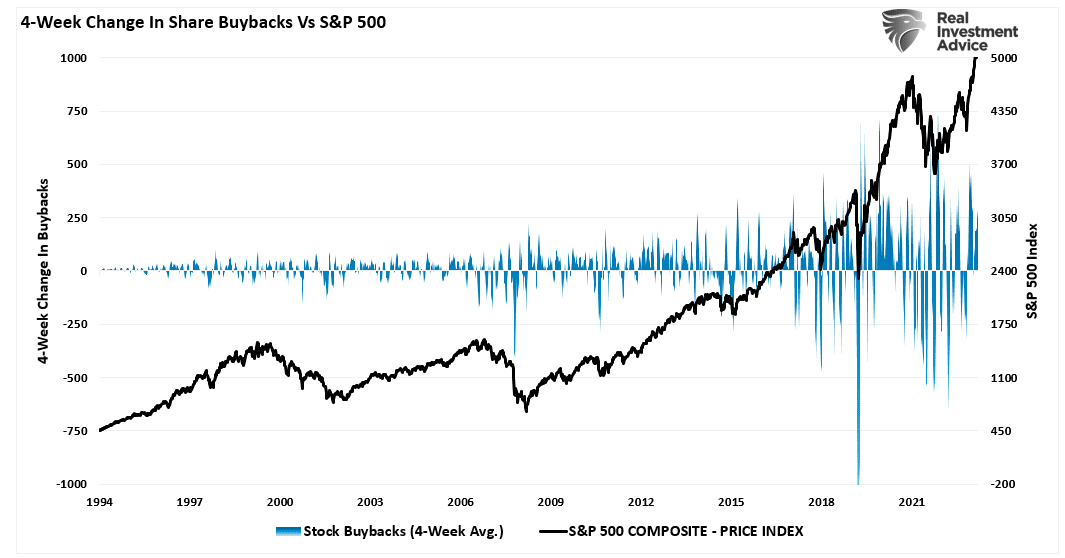

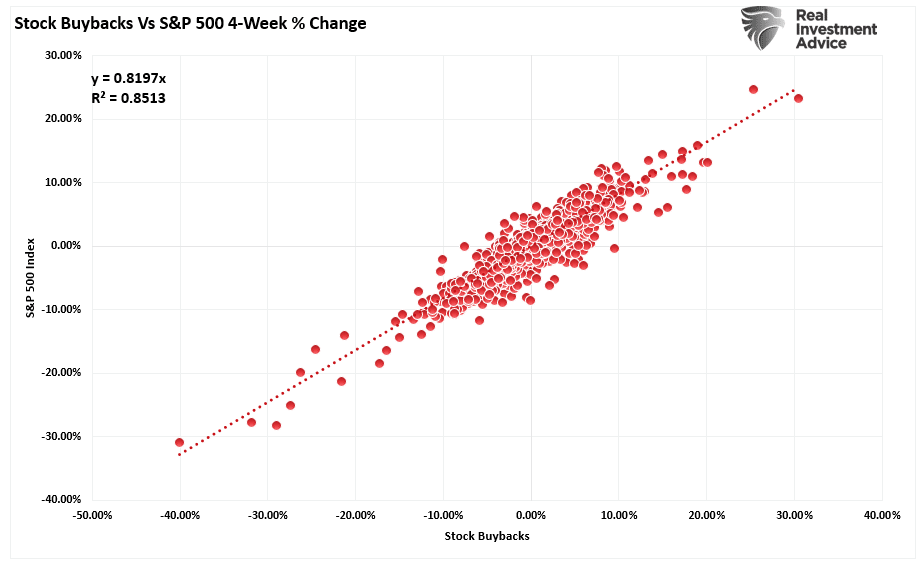

“Notably, since 2009, and accelerating starting in 2012, the percentage change in buybacks has far outstripped the increase in asset prices. As we will discuss, it is more than just a casual correlation, and the upcoming blackout window may be more critical to the rally than many think.” – March 19, 2024

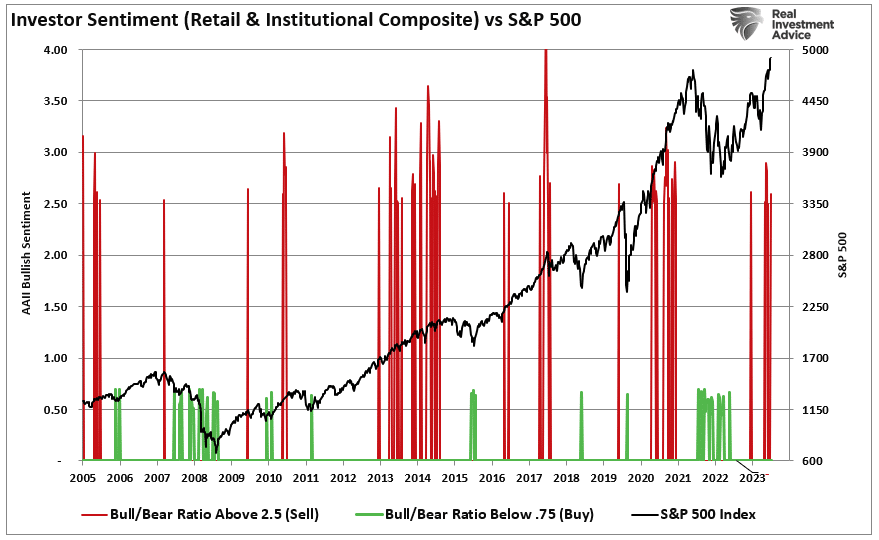

Furthermore, the “blackout” of corporate buybacks coincided with an aggressively bullish investor sentiment. As we noted in that same article:

“Investor sentiment is once again very bullish. Historically, when retail investor sentiment is exceedingly bullish combined with low volatility, such has generally corresponded to short-term market peaks.”

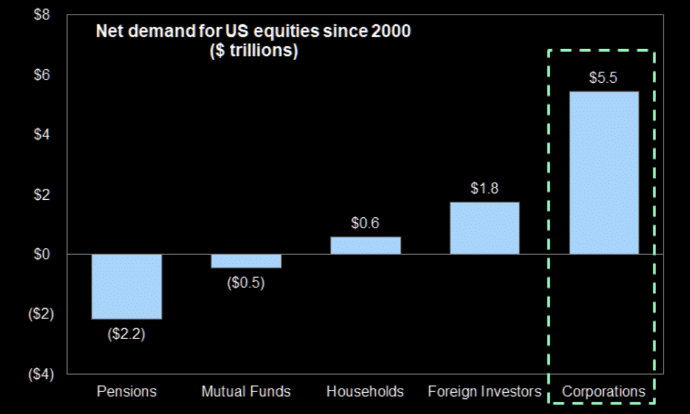

We will return to this chart momentarily, but given that corporate share buybacks have accounted for roughly 100% of net equity purchases over the last two decades, the blackout period combined with aggressive bullish sentiment was the recipe for a decline in asset prices.

Here is the math of net flows if you don’t believe the chart:

Pensions and Mutual Funds = (-$2.7 Trillion)

Households and Foreign Investors = +$2.4 Trillion

Sub Total = (-$0.3 T)

Corporations (Buybacks) = $5.5T

Net Total = $5.2 Trillion = Or 100% of all equities purchased

Such is crucial to understand as we head into the rest of the year. It will determine whether this is just a correction within a bullish trend or something more significant.

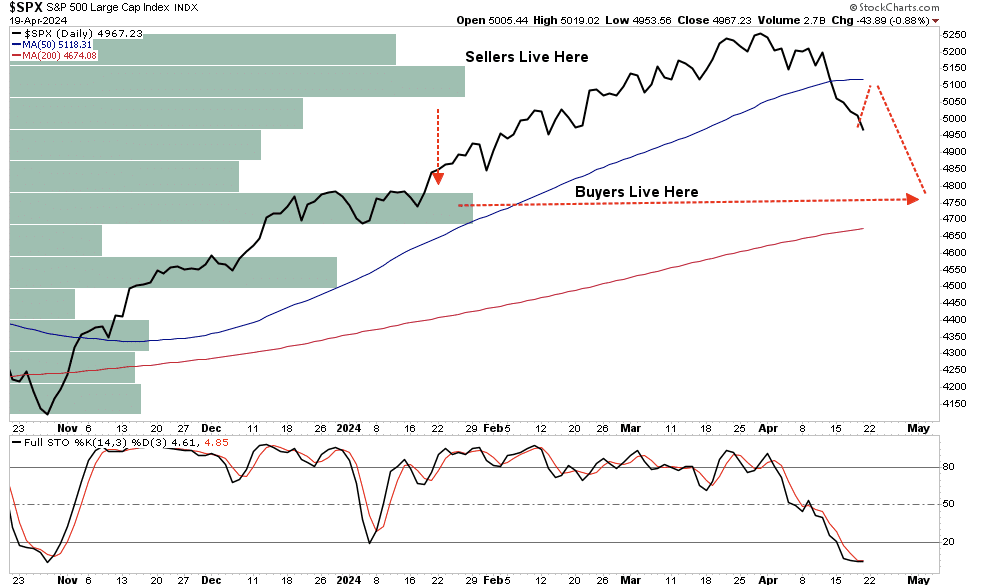

Buyers Live Lower

In “No Cash On The Sidelines,” we discussed the importance of understanding that “market prices” are set by the demand and supply between buyers and sellers. To wit:

“As noted above, the stock market is always a function of buyers and sellers, each negotiating to make a transaction. While there is a buyer for every seller, the question is always at “what price?”

In the current bull market, few people are willing to sell, so buyers must keep bidding up prices to attract a seller to make a transaction. As long as this remains the case and exuberance exceeds logic, buyers will continue to pay higher prices to get into the positions they want to own.

Such is the very definition of the “greater fool” theory.

However, at some point, for whatever reason, this dynamic will change. Buyers will become more scarce as they refuse to pay a higher price. When sellers realize the change, they will rush to sell to a diminishing pool of buyers. Eventually, sellers will begin to “panic sell” as buyers evaporate and prices plunge.”

In other words, “Sellers live higher. Buyers live lower.“

We can see where the buyers and sellers “live” in the following chart, which shows where the highest volume occurred.

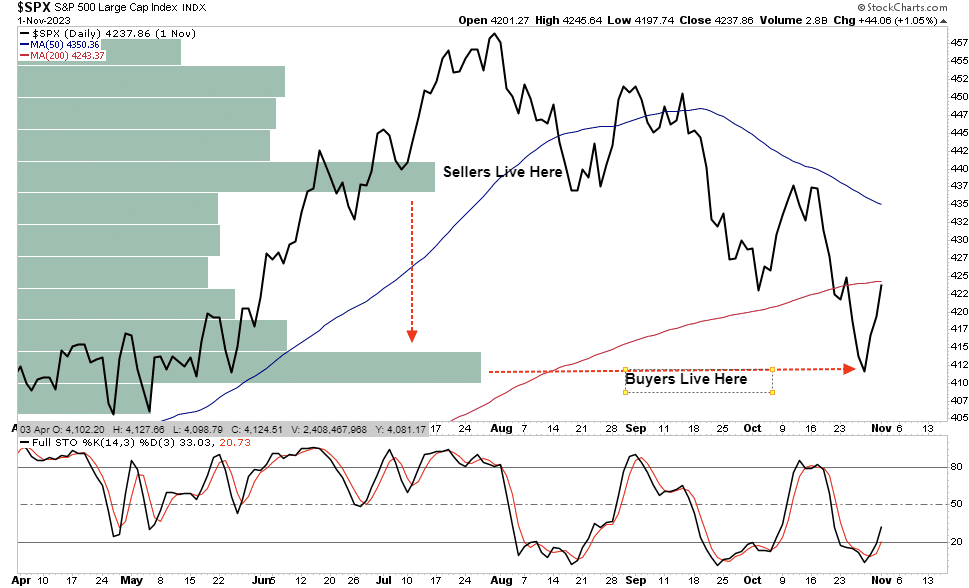

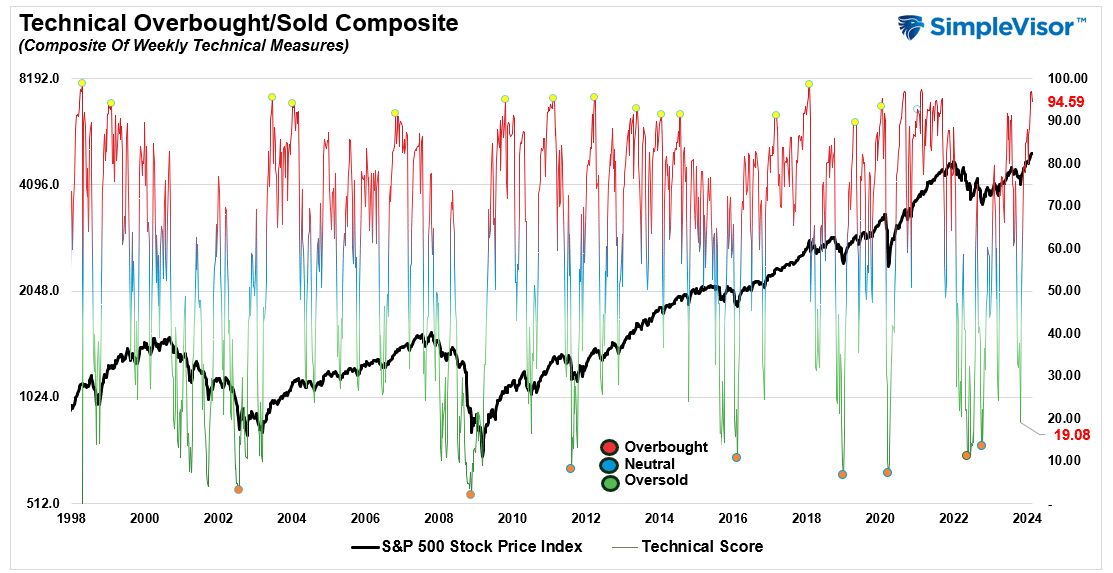

This current correction is becoming increasingly oversold (bottom panel), which suggests a bounce is likely toward the previous support of the 50-DMA. For comparison, we can look at last year’s market correction. As noted, the bullish rally into July peaked late that month. As the market corrected, it bounced from oversold conditions, allowing investors to reduce risk and hedge portfolios. The markets will likely present investors with that opportunity soon.

Then, like today, many investors began to believe it wasn’t just a correction but something much more. However, the reality was that the “buyers lived lower.” Buyers stepped in as prices approached the October lows, coinciding with the return of corporate share buybacks.

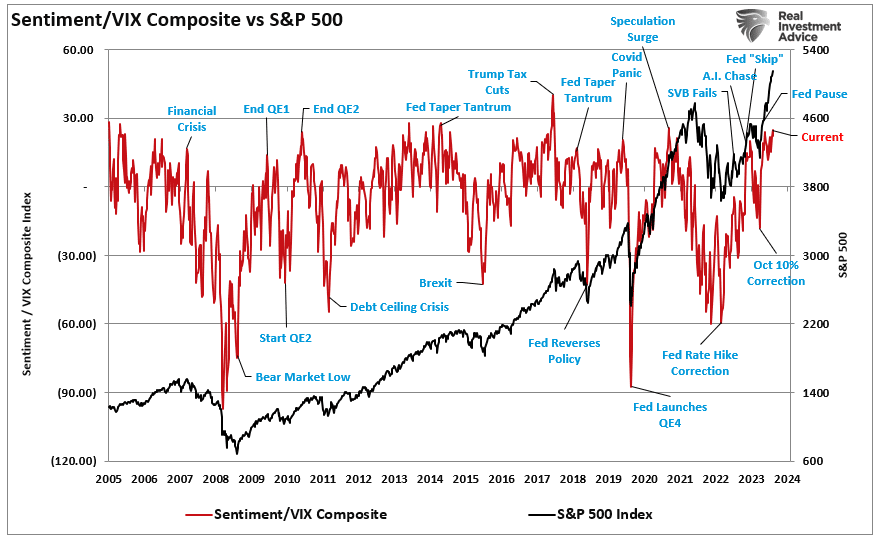

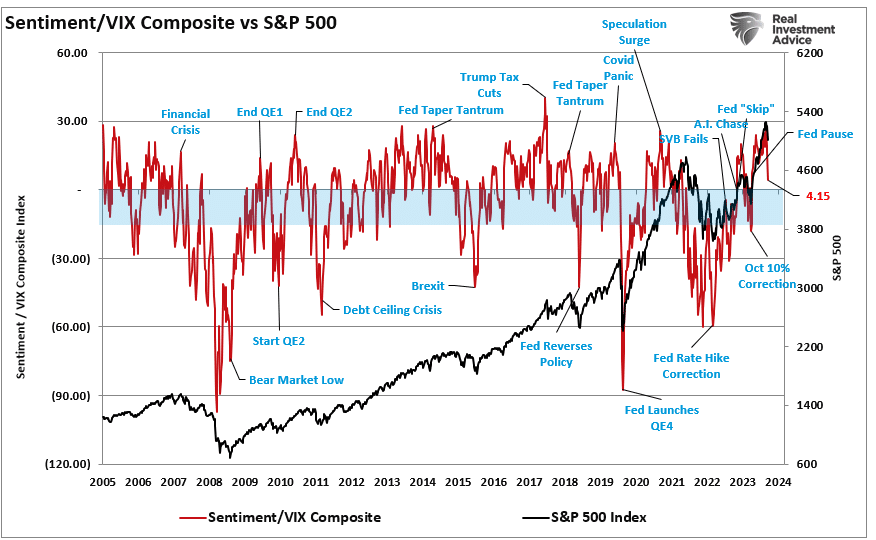

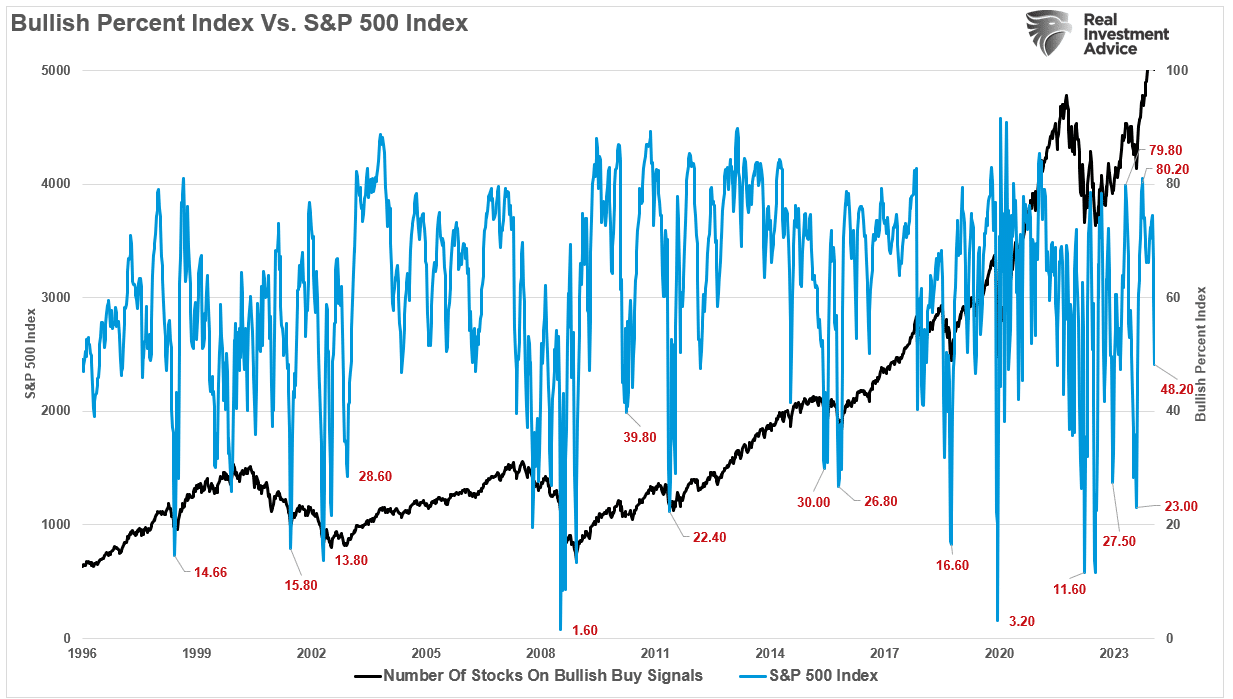

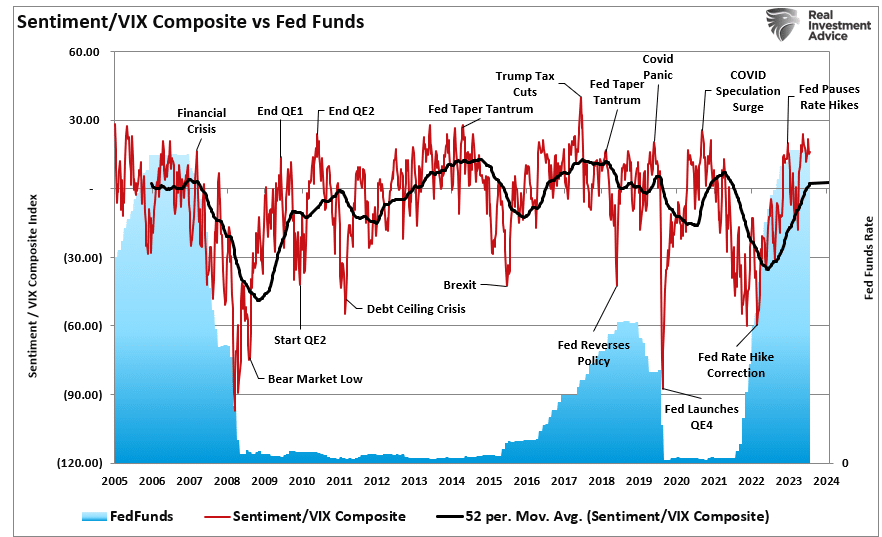

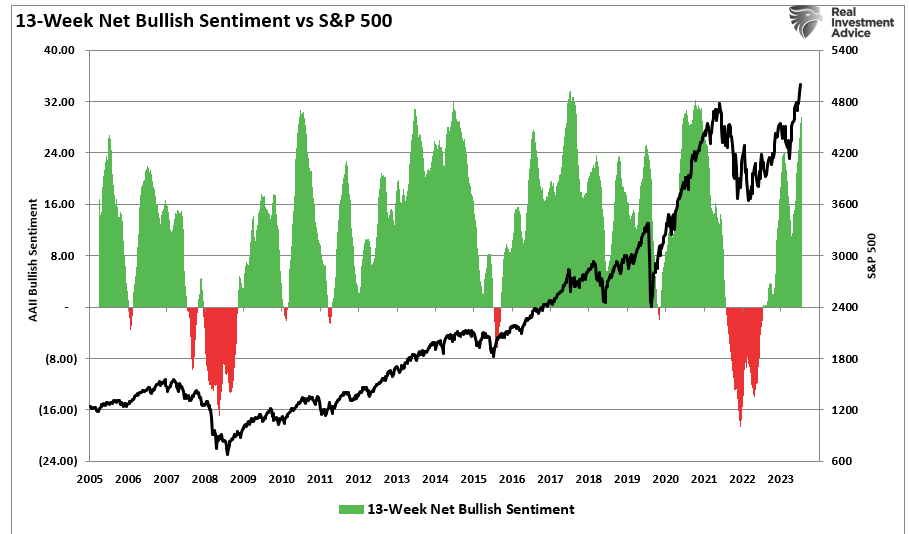

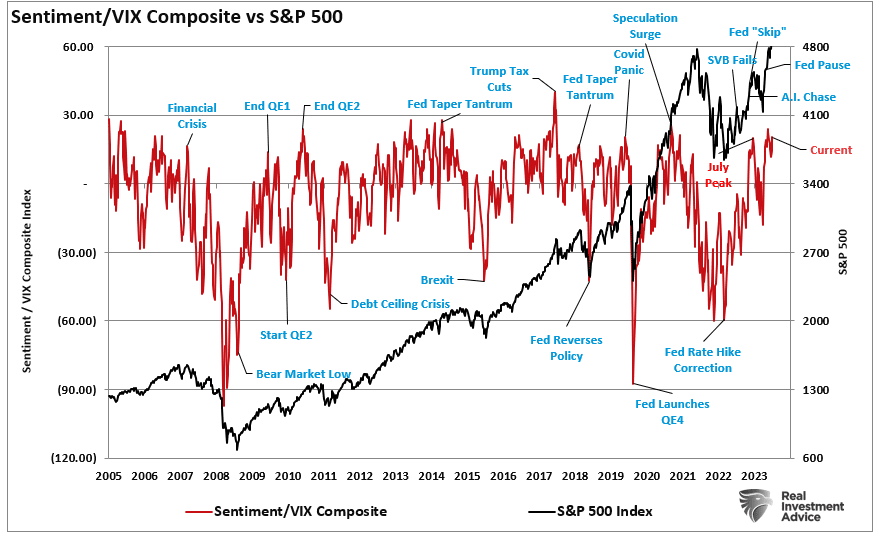

Sentiment Is Reversing Quickly

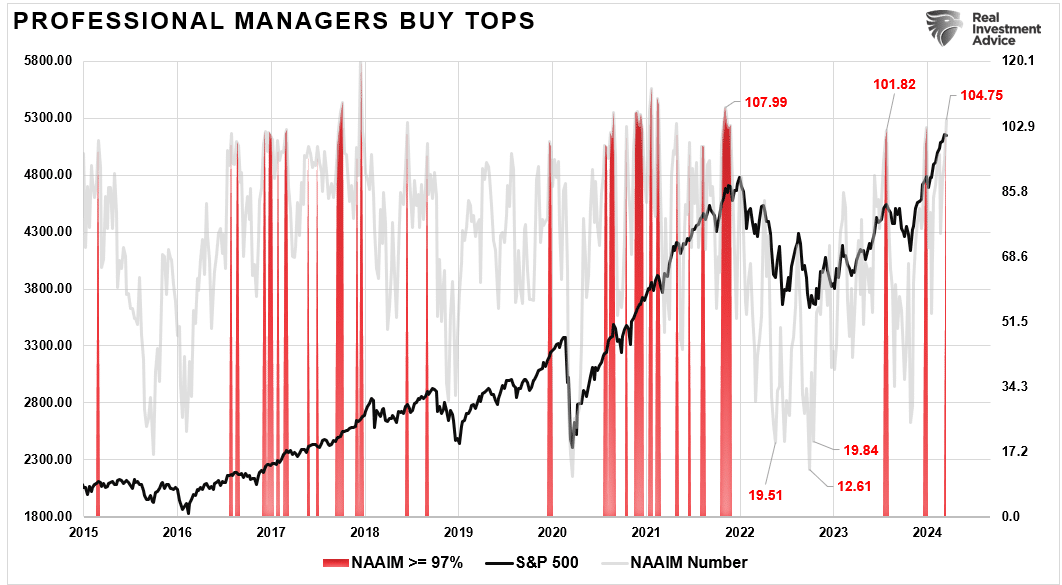

As I said, we need to revisit the sentiment chart above. Investors’ more frothy, bullish sentiment is reversing quickly on many fronts. The chart below, the same as above, is the composite net bullish sentiment index of retail and professional investors divided by the volatility index (VIX). If this is just a market correction, the index tends to bottom between zero (0) and negative (20). With a current reading of 4.15, down from 25.99 just two weeks ago, bullish sentiment has significantly reversed.

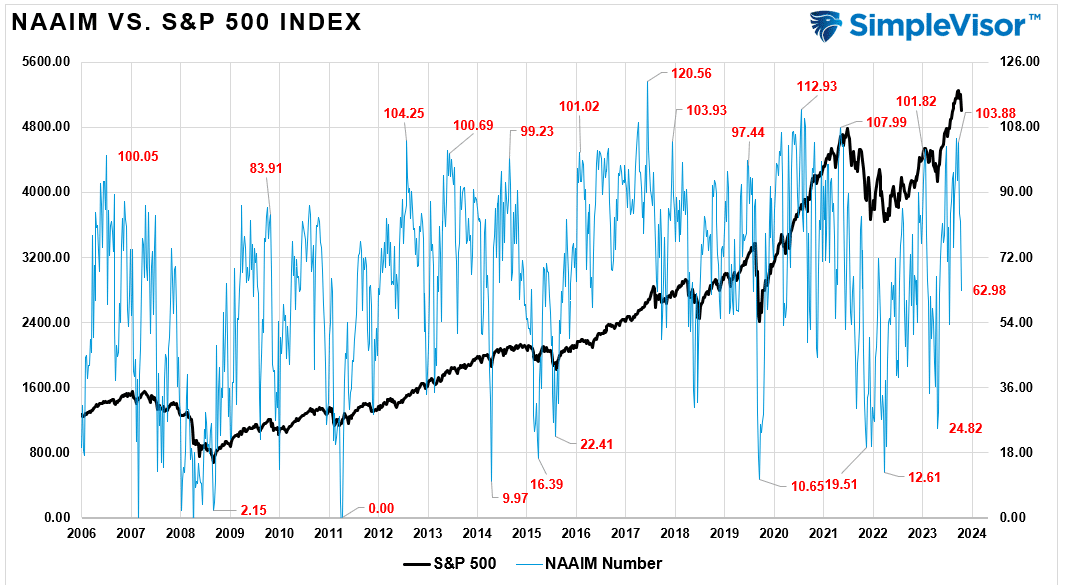

Notably, professional investor allocations to equities recently peaked at 103.88%, which has collapsed in just two weeks to just 62.98% exposure. (Professional investors are notorious for buying market peaks.)

Also, the number of stocks on bullish “buy signals” has dropped from 80.2 to 48.2.

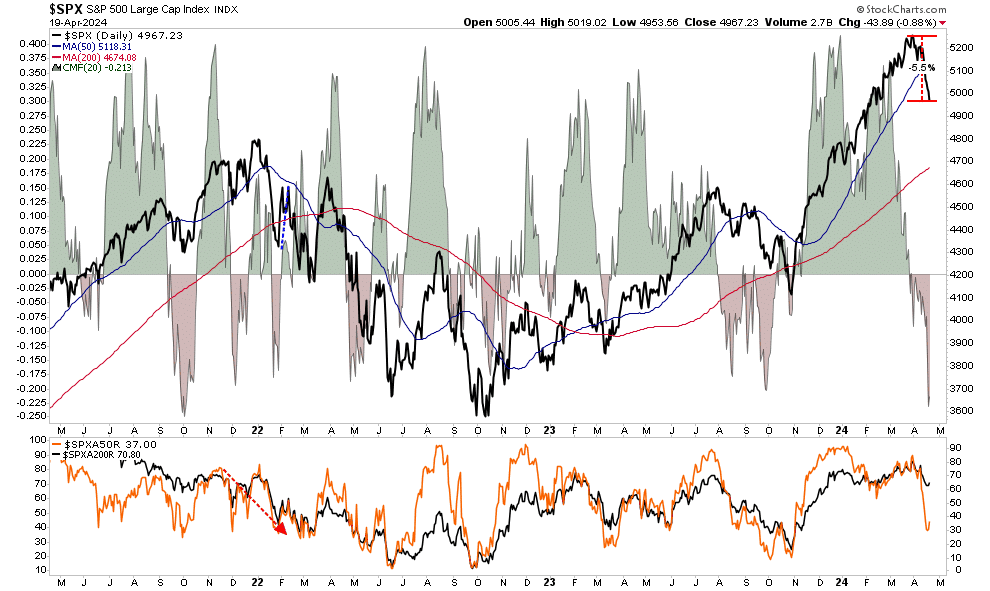

Furthermore, the number of stocks trading above the 50-DMA has fallen from over 80% to 37%, with money flows hitting levels lower than previous market bottom lows. Notably, with just a 5.5% correction from the recent peak (as of last Friday), much of the work of clearing the previous overbought conditions is completed.

Given the significant reversal in sentiment and short-term oversold conditions, we highly suspect the markets will provide a reflexive rally soon. However, with the number of bullish investors who got “trapped” in the selloff, any rallies will likely be met with further selling.

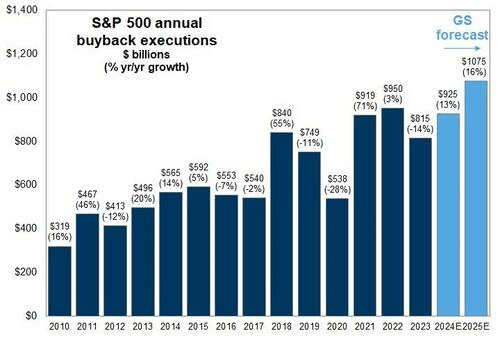

However, despite the current “panic” in the media headlines, this is likely just a correction within an ongoing bullish market. Such is particularly the case given that corporate share buybacks will resume in May, providing critical support for the markets heading into summer.

With that said, this correction, when complete, likely won’t be the last we see this year. Market history suggests we could see another “bumpy ride” heading into what many expect will be a somewhat contentious election.

But that is an article we will write when we get there.

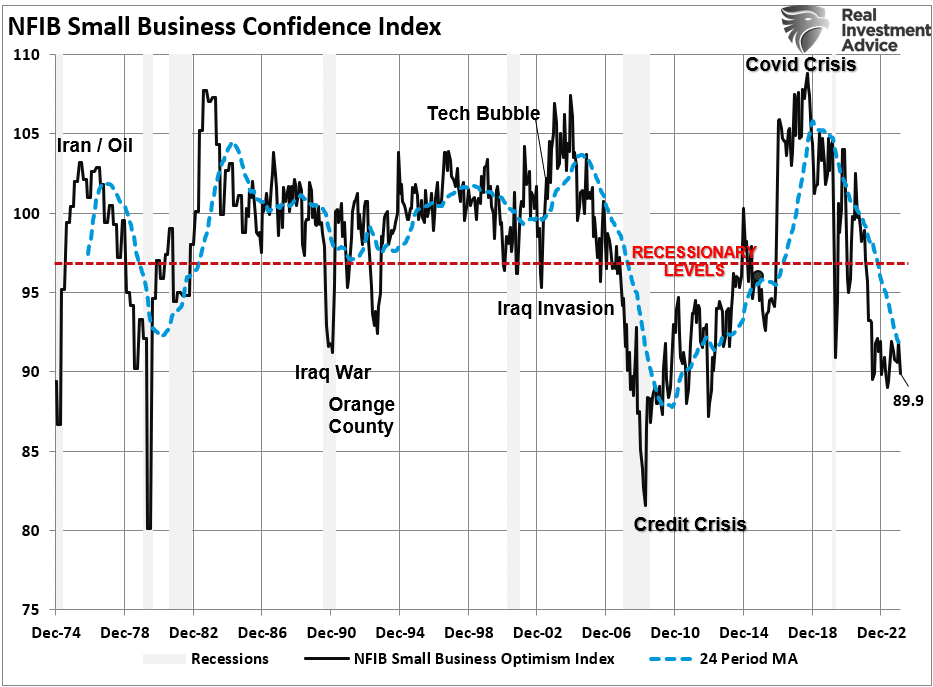

Economic Warning From The NFIB

The latest National Federation of Independent Business (NFIB) survey was an economic warning that departed widely from more robust governmental reports. Ina recent analysis of small businesses, we discussed the importance those business owners play in the economy.

“It is crucial to understand that small and mid-sized businesses comprise a substantial percentage of the U.S. economy. Roughly 60% of all companies in the U.S. have less than ten employees.

Small businesses drive the economy, employment, and wages. Therefore, the NFIB’s statements are highly relevant to the economy’s current state compared to the headline economic data from Government sources.”

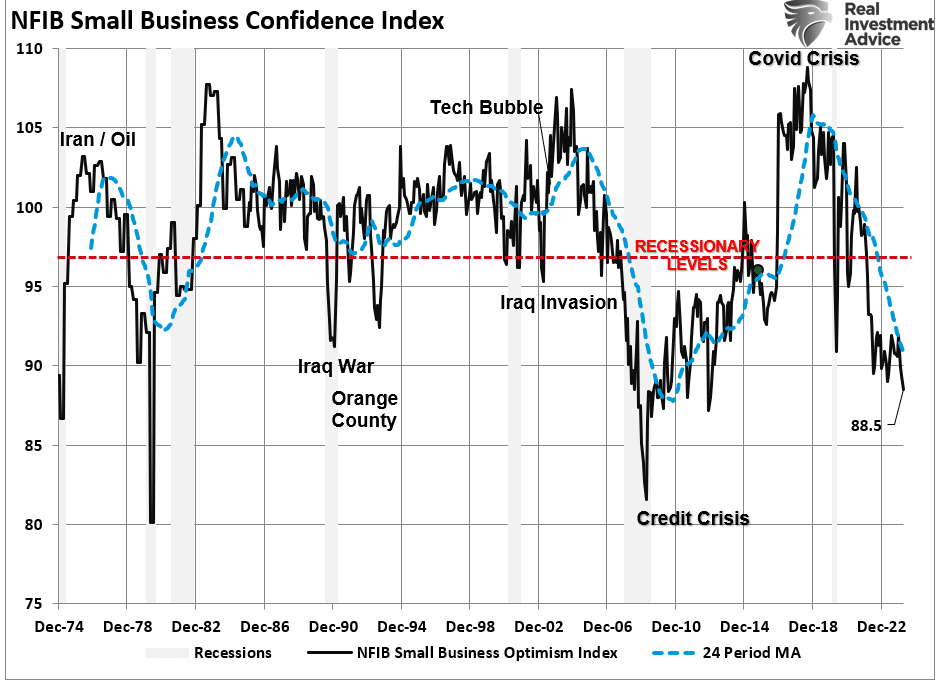

While recent government data on economic growth and employment remain robust, the NFIB small business confidence survey declined in its latest reading. Not only did it fall to the lowest level in 11 years, but, as far as an economic warning goes, it remained at levels historically associated with a recessionary economy.

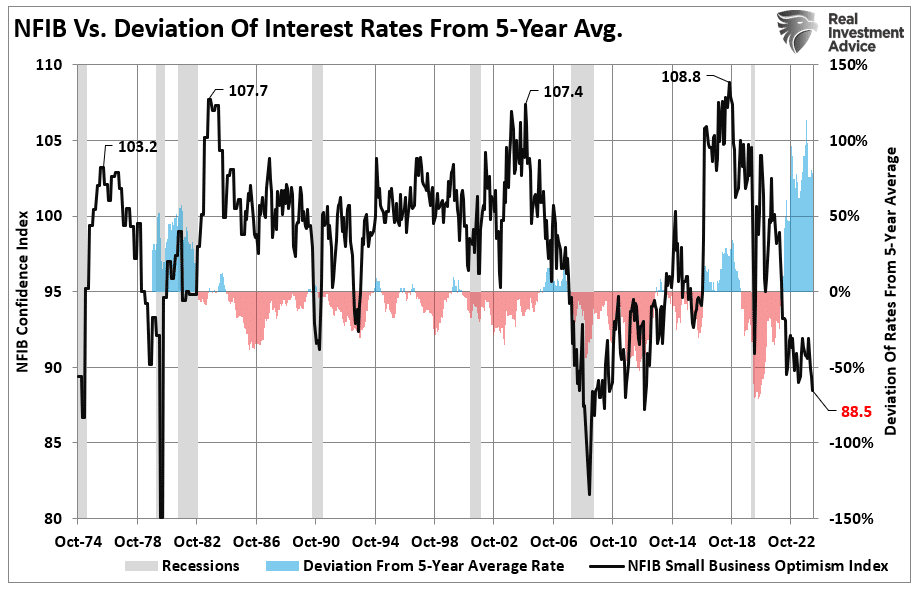

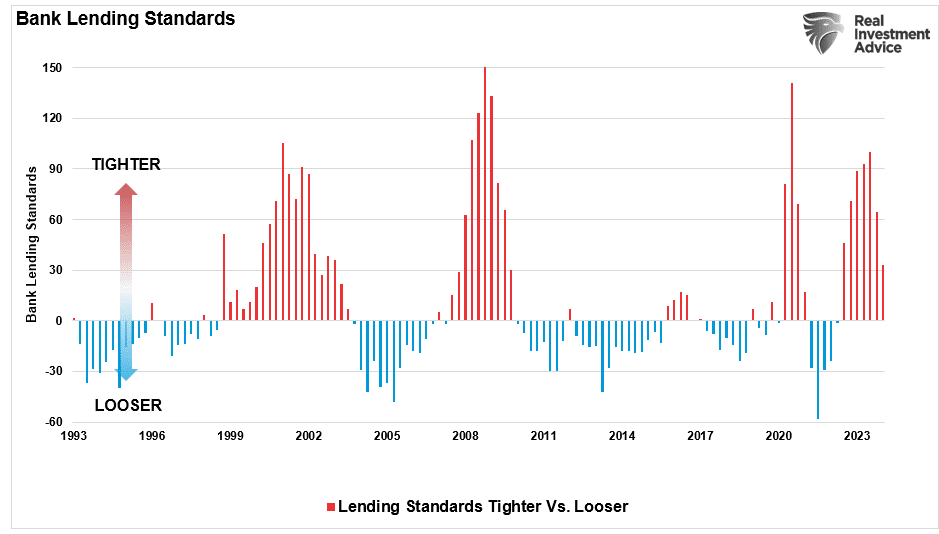

The decline in confidence should be unsurprising given the largest deviation of interest rates from their 5-year average since 1975. Higher borrowing costs impede business growth for small businesses, as they don’t have access to the bond market like major companies.

Therefore, as the economy slows and interest rates rise, small business owners turn to their local banks for operating loans. However, higher rates and tighter lending standards make access to capital more difficult.

Of course, given that capital is the lifeblood of any business, decisions on hiring, capital expenditures, and expansion hang in the balance.

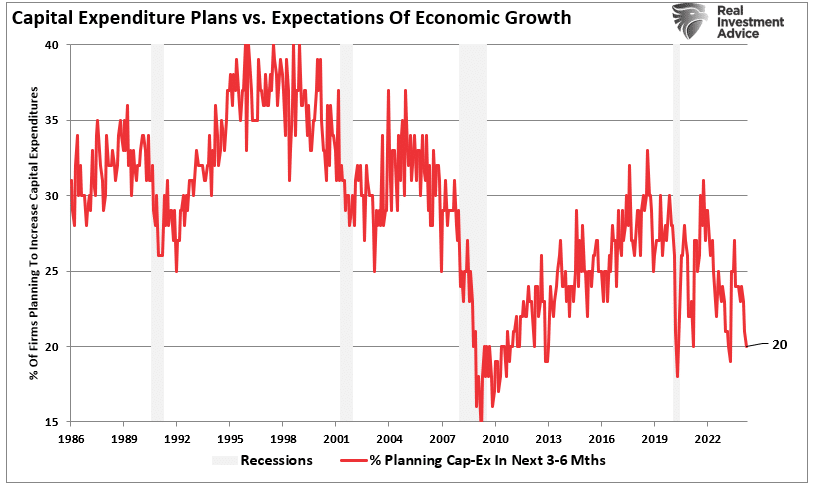

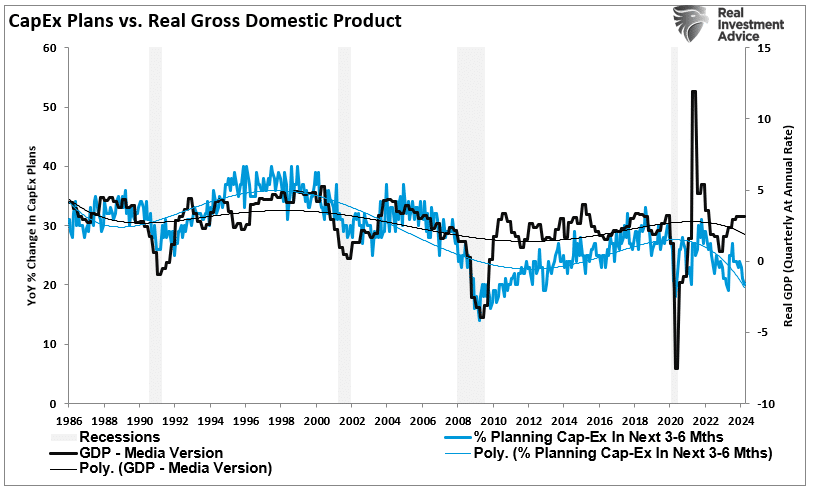

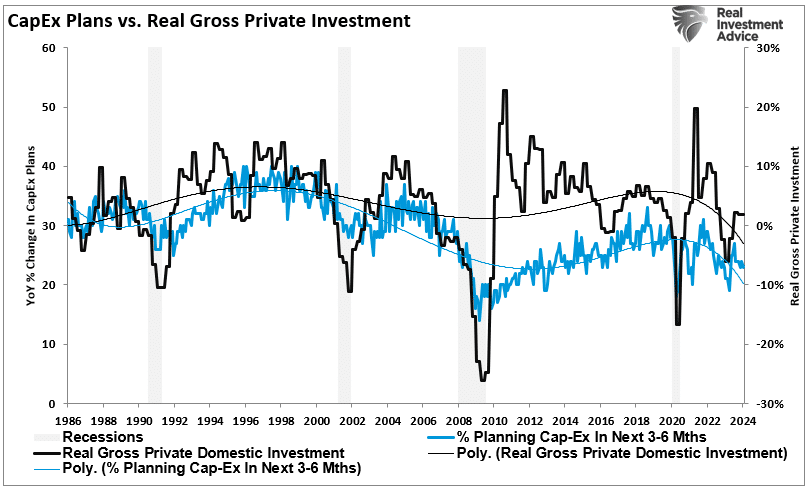

Economic Warning – Capital Expenditures

It should be unsurprising that if the economy were expanding as quickly as headline data suggests, business owners would be expending capital to increase capacity to meet rising demand. However, in the most recent NFIB report, the percentage of business owners planning capital expenditures over the 3-6 months dropped to the lowest level since the pandemic-driven shutdown.

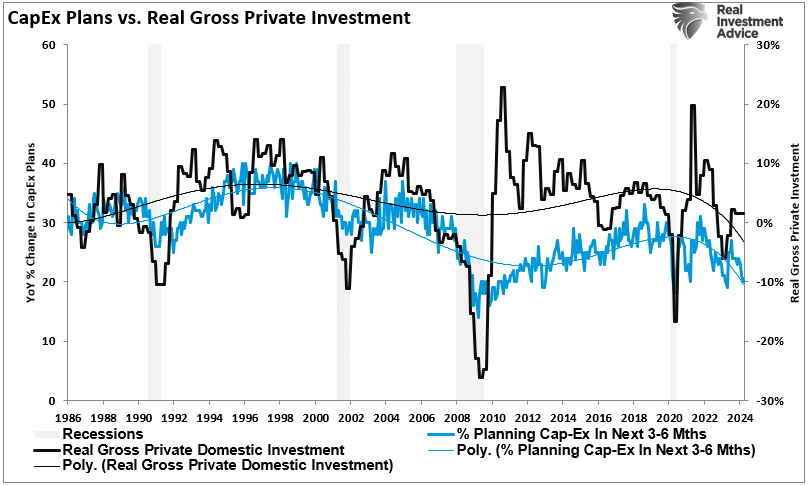

Again, given that small businesses comprise about 50% of the economy, there is more than just a casual relationship between their capital expenditure plans (CapEx) and real gross private investment, which is part of the GDP equation.

In other words, if small businesses cut back on CapEx, this will eventually translate into slower rates of private investment and, ultimately, economic growth in coming quarters.

As shown, the correlation between small business CapEx plans and economic growth should not be dismissed. While mainstream economists are becoming increasingly optimistic about an “economic reflation,” the economic warning between real GDP and CapEx suggests caution.

Of course, if small businesses are unwilling to increase CapEx, it is because there is a lack of demand to justify those expenditures. Therefore, if CapEx is falling, we should expect economic warnings from employment and sales.

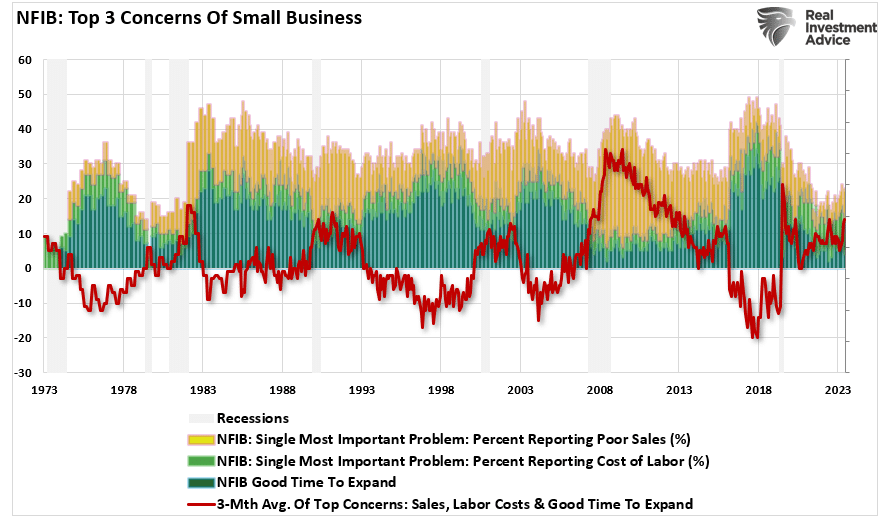

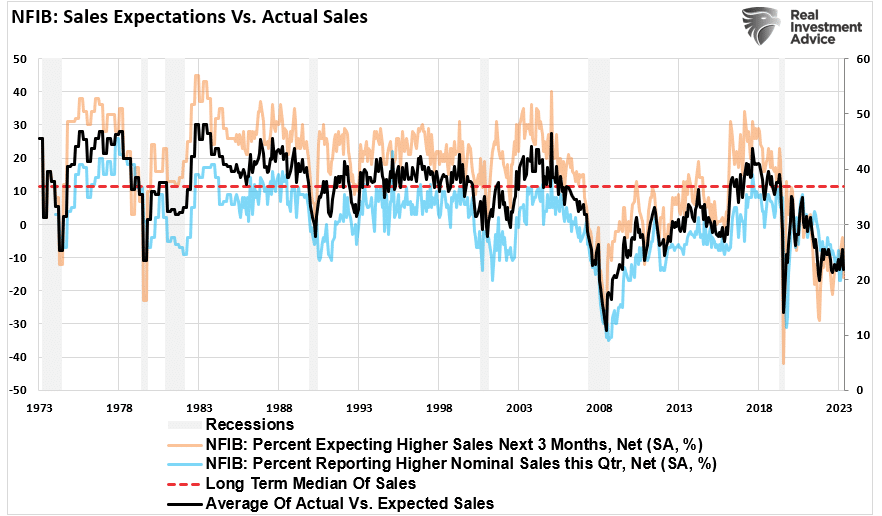

Something Amiss With Sales

Many reasons feed into a small business owner’s decision NOT to invest in their business. As noted above, tighter bank lending standards and increased borrowing costs certainly weigh on that decision. However, if “business is booming,” business owners will find the capital needed to meet increased demand. However, looking deeper into the NFIB data, we find rising concerns about the “demand” side of the equation.

The NFIB publishes several data points from the survey concerning the “concerns” small business owners have. These cover many concerns, from government regulations to taxes, labor costs, sales, and other concerns confronting business owners. When it comes to the “demand” side of the equation, there are three crucial categories:

Poor sales (demand),

Cost of labor (the most significant expense to any business), and

Is it a “Good time to expand?”(Capex)

In the chart below, I have inverted “Good time to expand,” so it correlates with rising concerns about the cost of labor and poor sales. What should be obvious is that the average of these concerns escalates as economic growth weakens (recessionary periods) and falls during economic recoveries. Currently, these rising concerns should provide an economic warning to economists.

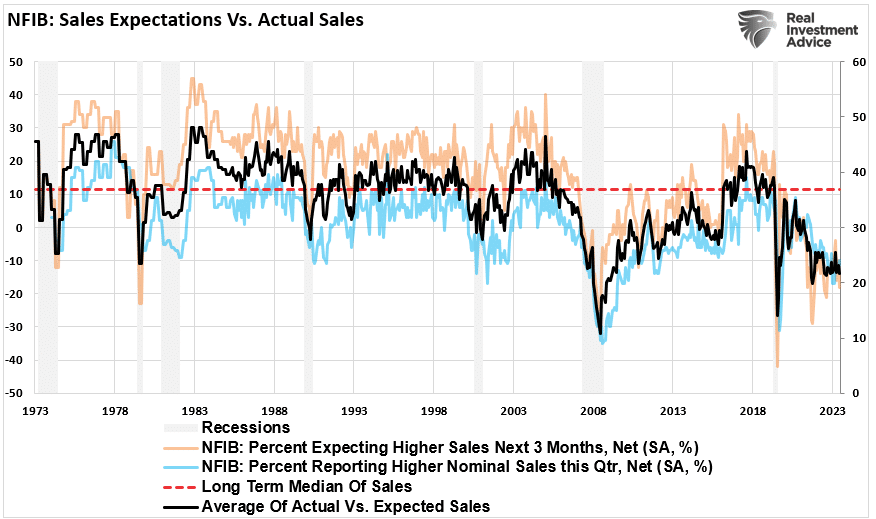

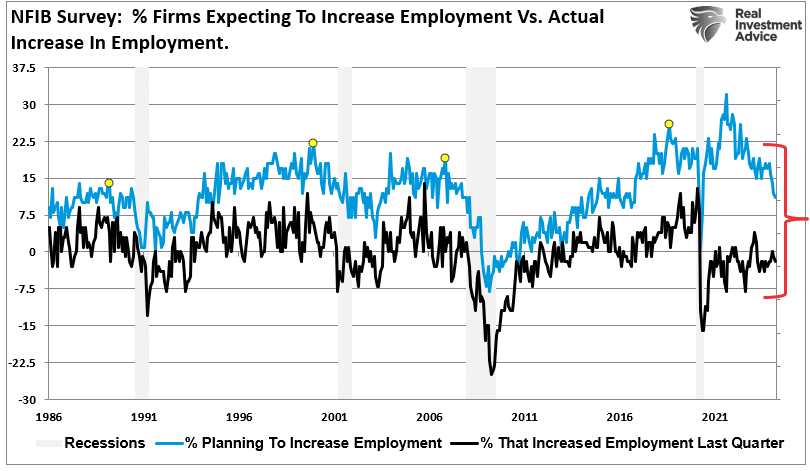

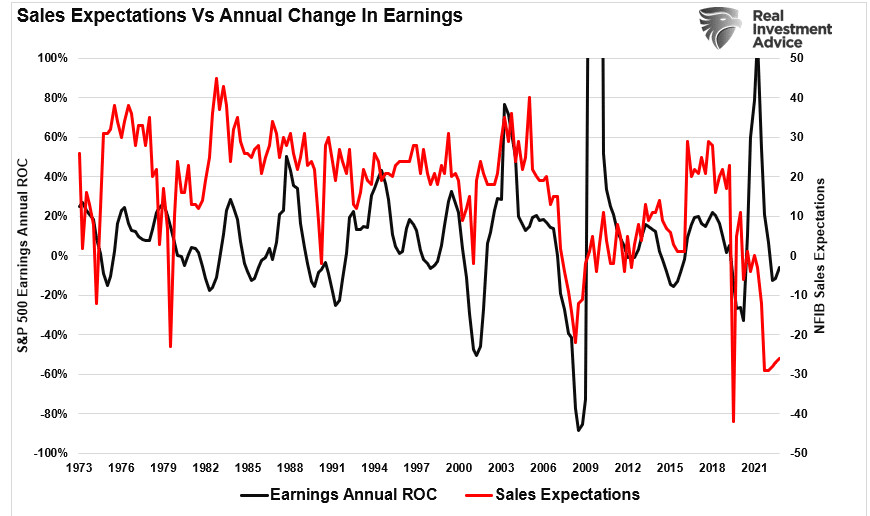

Examining sales and employment figures can help us understand why business owners remain pessimistic about the overall economy. The chart below shows the NFIB members’ sales expectations over the next quarter compared to the previous quarter. The black line is the average of both with a long-term median.

Unsurprisingly, business owners are always optimistic that sales will improve in the next quarter. However, actual sales tend to fall short of those expectations. The two have a very high correlation, which is why the average of both provides valuable information. Sales expectations and actual sales are well below levels typically witnessed during recessions. With sales (demand) weak, there is little need to increase production (supply) substantially.

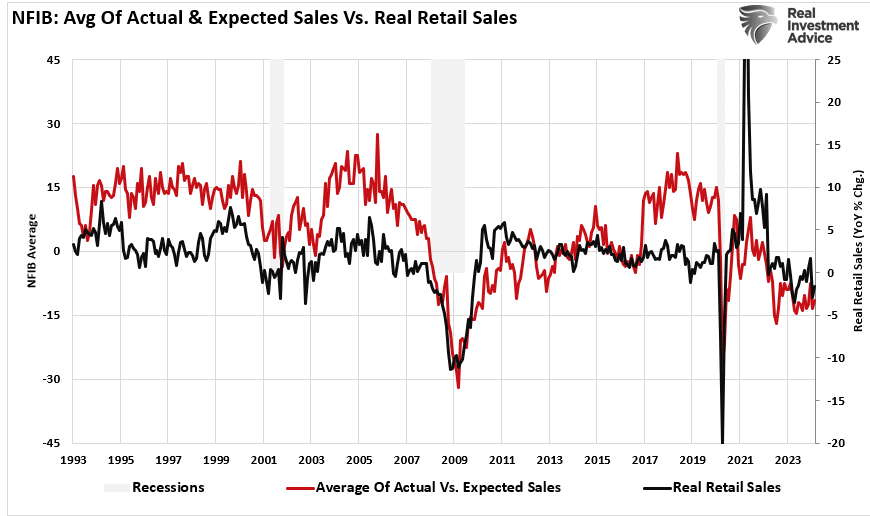

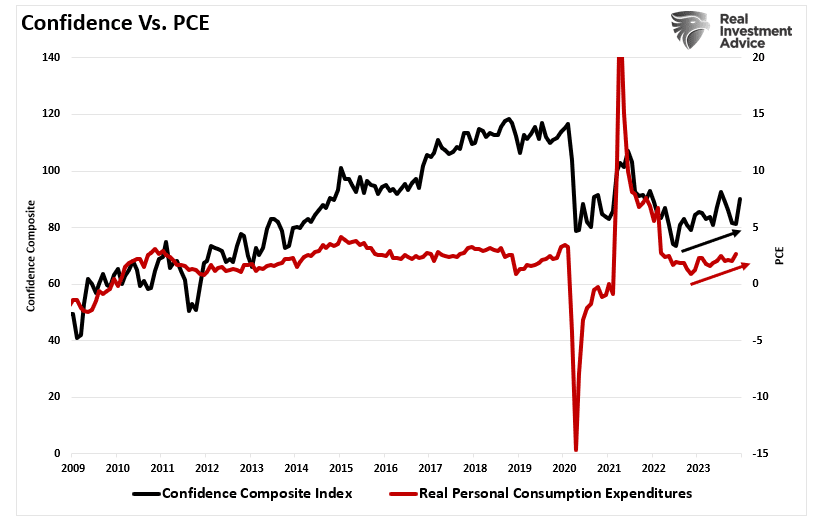

Here is the economic warning to pay attention to. Real retail sales comprise about 40% of personal consumption expenditures (PCE), roughly 70% of the economic growth rate. The decline in the average of actual and expected sales of small businesses suggests weaker retail sales and, by extension, a slower economic growth rate.

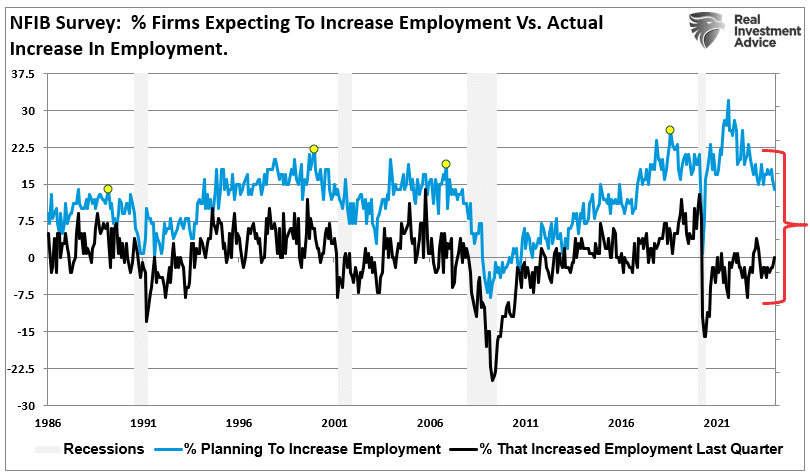

EmploymentWarning

The demand side of the economic equation is crucially important. If the demand for a business owner’s products or services declines, there is little need to increase employment. Therefore, if economic growth was as robust as headlines suggest, why are small businesses’ plans to increase employment declining sharply?

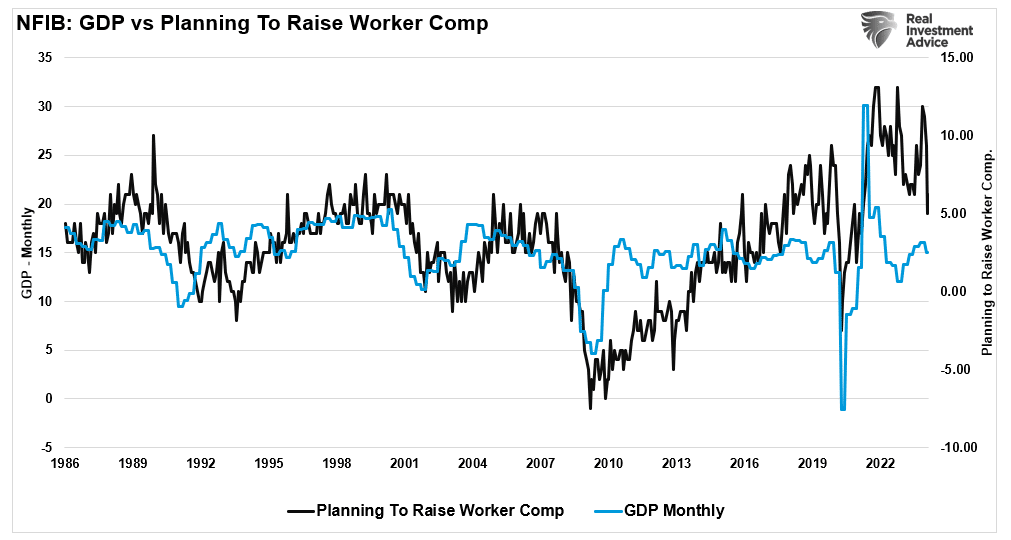

Furthermore, when demand falls, business owners look to cut operating costs to protect profitability. While cutting future employment is part of that equation, so are plans to raise worker compensation.

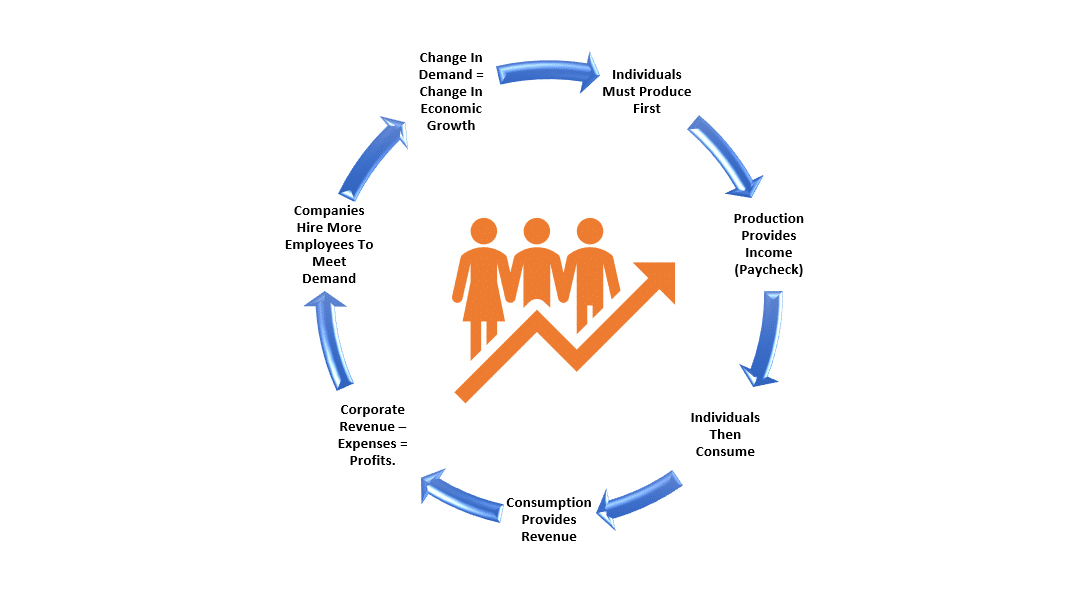

The last chart is crucial. The U.S. is a consumption-based economy. However, consumers can not consume without producing something first. Production must come first to generate the income needed for that consumption. The cycle is displayed below.

As employees receive fewer compensation increases (raises, bonuses, etc.) amid rising living costs, they cut consumption, which translates into slower economic growth rates. In turn, business owners cut employment and compensation further. It is a virtual spiral that historically ends in recession.

While this time could certainly be different, the economic warnings from the NFIB survey should not be dismissed. The data could explain why the Fed is adamant about cutting rates.

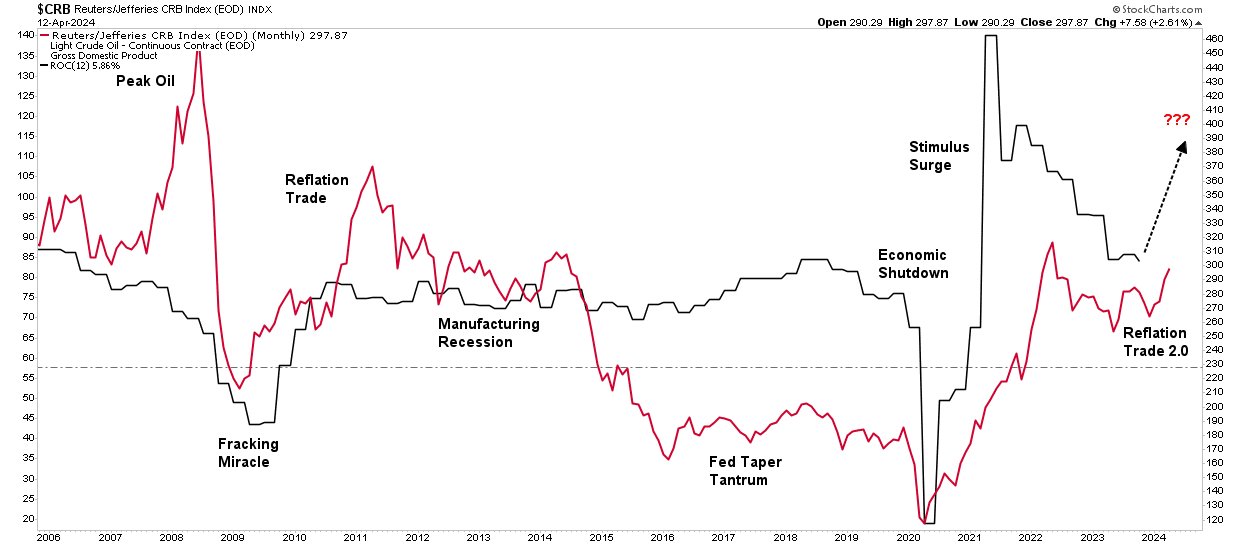

Reflation Trade Is The New Bullish Narrative

Economic “reflation” is becoming the next bullish narrative as equity valuation increases continue to outpace earnings gains, at least according to Gold Sachs and Tony Pasquariello.

“If GS is correct on the big calls, the macro backdrop is set to remain friendly: the US economy should continue to grow nicely above trend — picking up speed as the year moves along — with three adjustment rates cuts along the way. to not obscure the moral of that story: the Fed is set to ease policy … into an upswing. while Fedspeak this week had a somewhat hawkish bent, the house view for 2024 remains intact.”

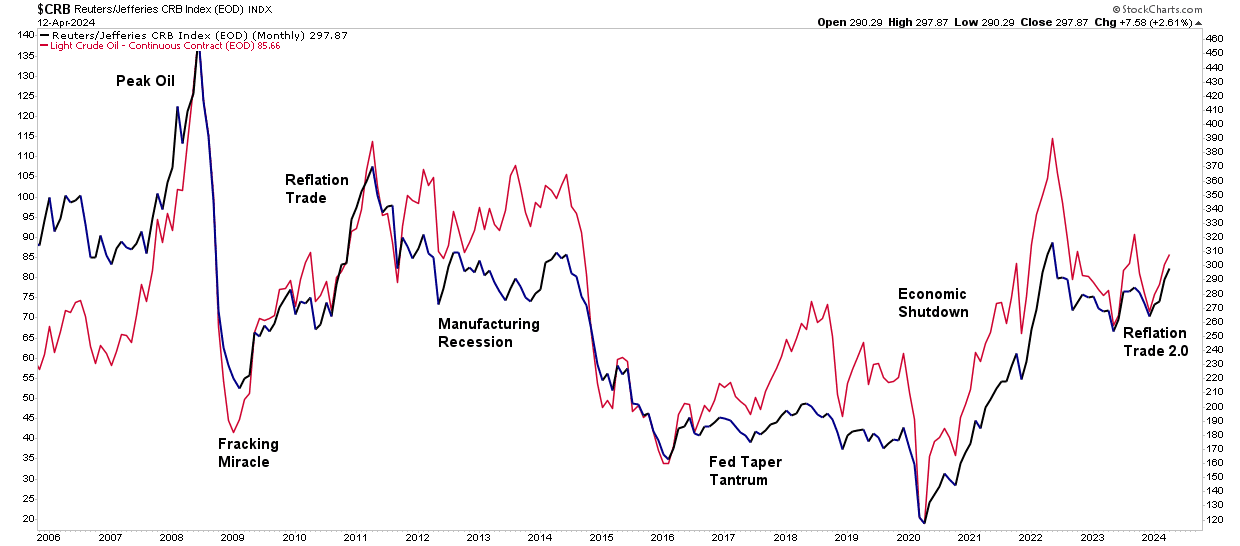

Interest rates, gold, and commodity prices have increased in the past few months. Unsurprisingly, the bullish narrative to support that rise has gained traction. Interestingly, this “reflation” narrative tends to resurface by Wall Street whenever there is a need to explain the surge in commodity prices. Notably, the last time Wall Street focused on the reflation trade was in 2009, as noted by the WSJ:

“The most talked-about investing strategy these days isn’t stuffing money in a mattress, it’s the reflation trade — the bet that the world economy will rebound, driving up interest rates and commodities prices.”

While that “reflation trade” lasted for about two years, it quickly failed as economic growth returned to 2%-ish growth along with inflation and interest rates. As shown, oil and commodity prices have a very high correlation. The critical reason is that higher oil prices reduce economic demand. As consumption falls, so does the demand for commodities in general. Therefore, if commodity prices are to “reflate,” as shown, such will depend on more robust economic activity.

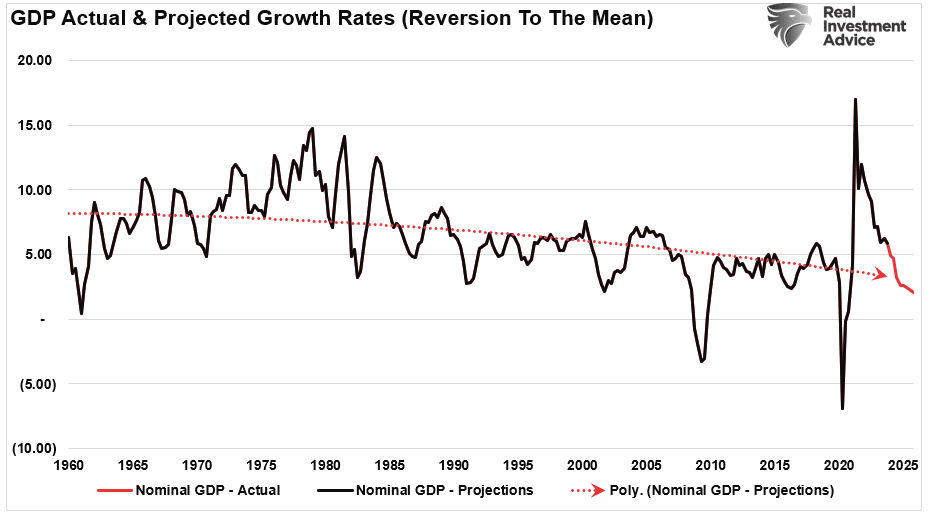

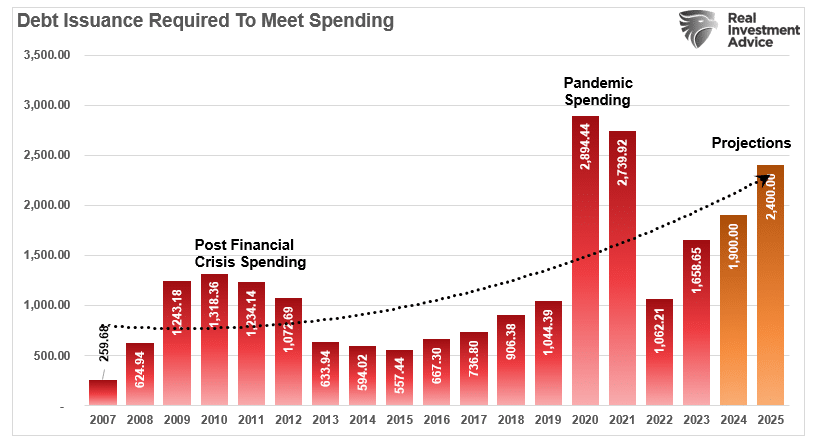

As such. The reflation trade hinges on a global resurgence of economic activity, usually associated with economies recovering from a recessionary period. However, the U.S. never experienced a recession. As discussed in “Deficit Spending,” despite numerous recessionary signals, like the inverted yield curve, manufacturing data, and leading economic indicators, the economy avoided recession due to massive governmental spending. To wit:

“One explanation for this has been the surge in Federal expenditures since the end of 2022 stemming from the Inflation Reduction and CHIPs Acts. The second reason is that GDP was so grossly elevated from the $5 Trillion in previous fiscal policies that the lag effect is taking longer than historical norms to resolve.”

While economists focus on the “reflation trade,” we must answer whether the support for more substantial economic growth exists. This is the sole determining factor in whether the “reflation trade” can continue.

Is Reflation Already Behind Us?

Interest rates and inflation have ticked up recently, driving investors into gold and commodities. However, the surge in precious metals and commodities is more of a function of speculative exuberance rather than an economic resurgence. As discussed in “Speculative Warnings,”

“In other words, the stock market frenzy to “buy anything that is going up” has spread from just a handful of stocks related to artificial intelligence to gold and digital currencies.“

Notably, the gold, commodities, and interest rate surge corresponded with more robust economic growth beginning in the third quarter of last year. That uptick in economic growth defied economists’ expectations of a recession. Such was because of the massive flood of monetary support from Government spending programs. However, that monetary impulse is now reversing.

As far as the “reflation trade” is concerned, as that monetary impulse recedes, so will economic growth, as shown. Even if the economy continues to grow at 2-2.5% annualized each quarter, the annual rate of change in growth will continue to slow.

Importantly, this assumes that the Government will keep “spending like drunken sailors” over that same period. However, if they don’t, the economic growth rate will slow even more quickly without increasing monetary spending.

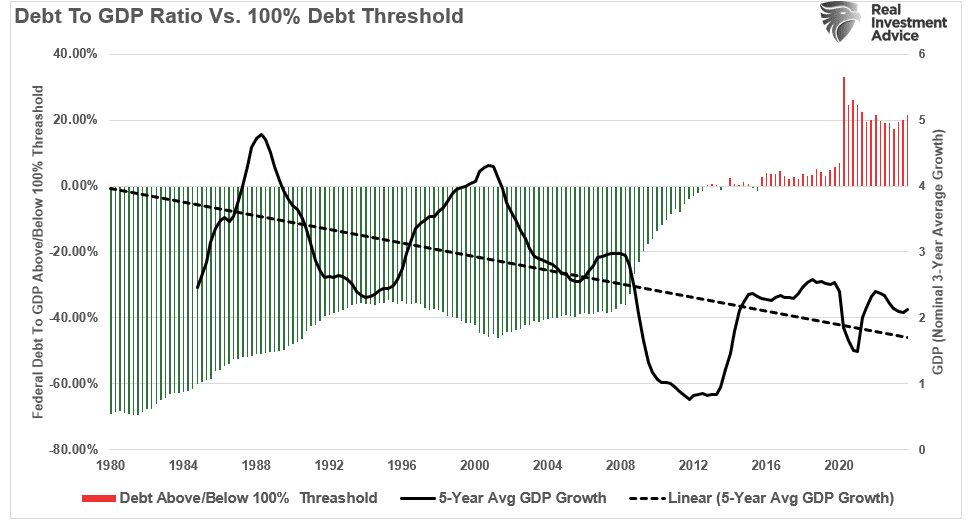

It is important to remember that increasing debts and deficits do not elicit stronger long-term economic growth. As debt levels rise, economic growth rates will slow as money diverts from productive investment into debt service.

That reality should be unsurprising, as this is not the first time the Government has gone “all in” on a reflation trade. As noted above, following the Financial Crisis, the Government intervened with HAMP, HARP, TARP, and a host of other spending programs to “reflate” the economy.

Let’s review what happened with interest rates, inflation, and gold and commodity trade.

Past May Be Prologue

As noted in 2009, following the “Financial Crisis” and recession, the Government and the Federal Reserve engaged in various monetary and fiscal supports to repair the economy. While the economy initially recovered from the recessionary lows, inflation, economic growth, and interest rates remained subdued despite ongoing interventions.

That is because debt and artificially low interest rates lead to malinvestment, which acts as a wealth transfer mechanism from the middle class to the wealthy. However, that activity erodes economic activity, leading to suppressed inflation and a surging wealth gap.

During that same period, commodities and precious metals rose initially as the “reflation expectation” was widespread. However, debt-driven realities quickly undermined that assessment and those investments languished relative to equities, as the flood of liquidity and low rates made equities far more attractive to investment.

While the relative performance of precious metals and commodities has picked up in recent months, this is more likely a function of “irrational exuberance” in the financial markets. As discussed previously, the surge in speculative investment activity is not uncommon to markets, and currently, many asset classes are becoming highly correlated.

However, while there is a compelling narrative around gold and precious metals from an investment perspective, those chasing that trade have had many years of terrible underperformance. While this time could be different, the “reflation narrative” will most likely fall prey to the realities of excessive debt, which will pressure Governments to cut rates once again.

If the past is potentially prologue, likely, the bullish narrative of “reflation” may once again find future disappointment. Such is particularly the case as the economics of debt and poor policy choices continue to erode the middle class further.

Immigration And Its Impact On Employment

Is immigration why employment reports from the Bureau of Labor Statistics (BLS) continue defying mainstream economists’ estimates? Many are asking this question as the U.S. experiences a flood of immigrants across the southern border. Concurrently, many young college graduates continue to complain about the inability to receive a job offer. As noted recently by CNBC:

The job market looks solid on paper. According to government data, U.S. employers added 2.7 million people to their payrolls in 2023. Unemployment hit a 54-year low of 3.4% in January 2023 and ticked up just slightly to 3.7% by December.

But active job seekers say the labor market feels more difficult than ever. A 2023 survey from staffing agency Insight Global found that recently unemployed full-time workers had applied to an average of 30 jobs only to receive an average of four callbacks or responses.”

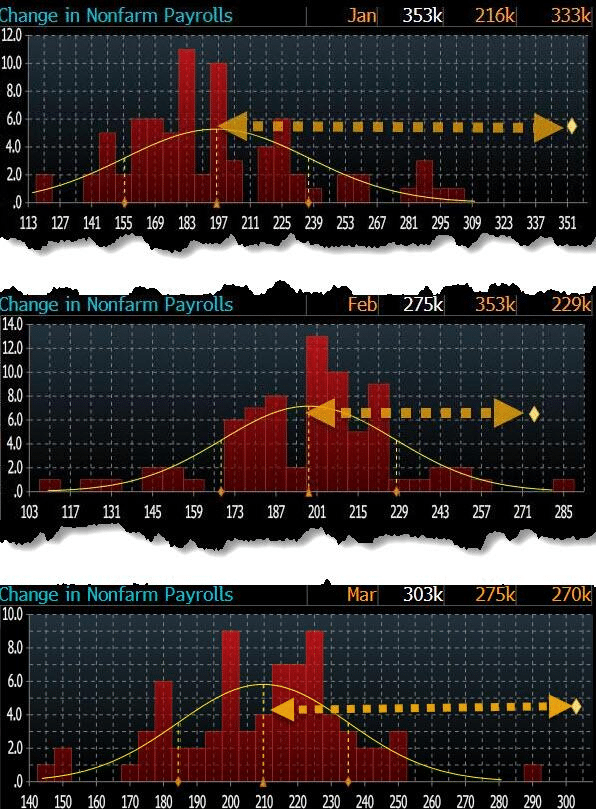

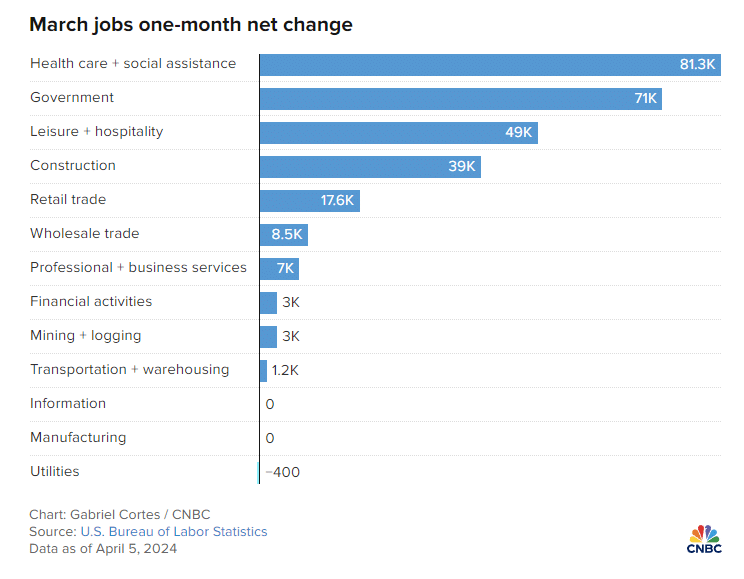

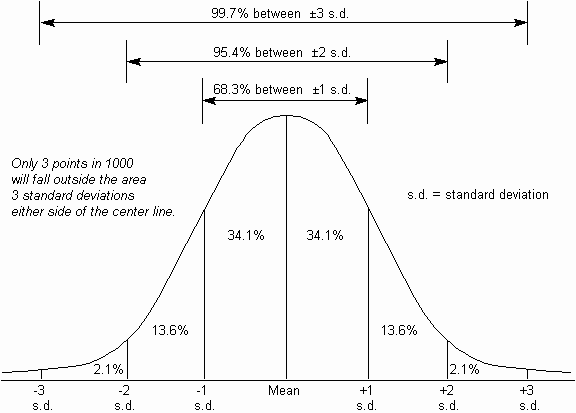

These stories are not unique. If you Google “Can’t find a job,” you will get many article links. Yet employment reports have been exceedingly strong for the past several months.In March, the U.S. economy added 303,000 jobs, exceeding every economist’s estimate by four standard deviations. In terms of statistics, a single four-standard deviation event should be rare. Three months in a row is a near statistical impossibility.

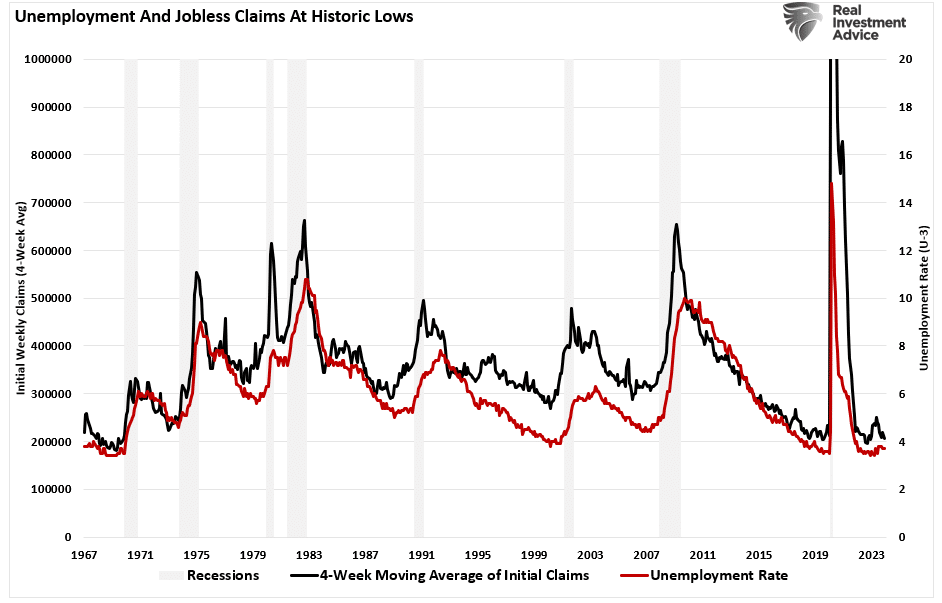

Despite weakness in manufacturing and services, with many companies recently announcing layoffs, we have near-record-low jobless claims and employment. According to official government data, the economy has rarely been more robust.

Such a situation begs an obvious question: How are college graduates struggling to find employment while the labor market remains so strong?

We may find the answer in immigration.

Immigrations Impact By The Numbers

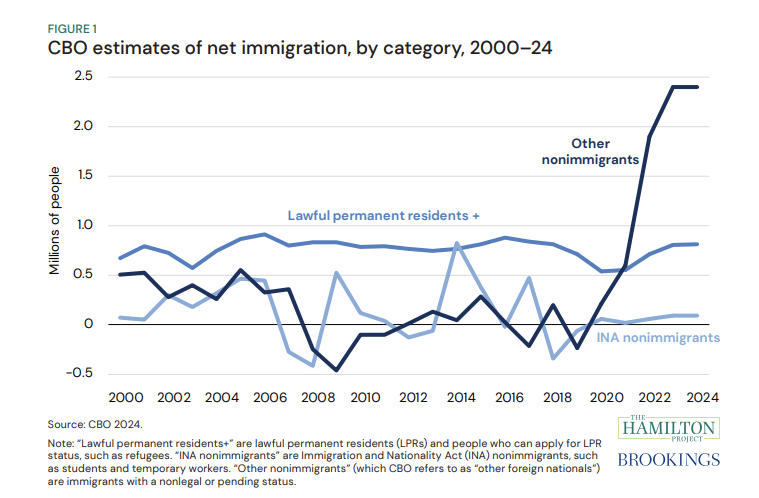

A recent study by Wendy Edelberg and Tara Watson at the Brookings Institution found that illegal immigrants in the country helped boost the labor market, steering the economy from a downturn. Data from the Congressional Budget Office shows a massive uptick of 2.4 million “other immigrants” who don’t fall into the category of lawful immigrants or those on temporary visas. The chart below shows how this figure has spiked from a level of less than 500,000 at the beginning of the 2020s.

The most significant change relative to the past stems from CBO’s other non-immigrant category, which includes immigrants with a nonlegal or pending status.

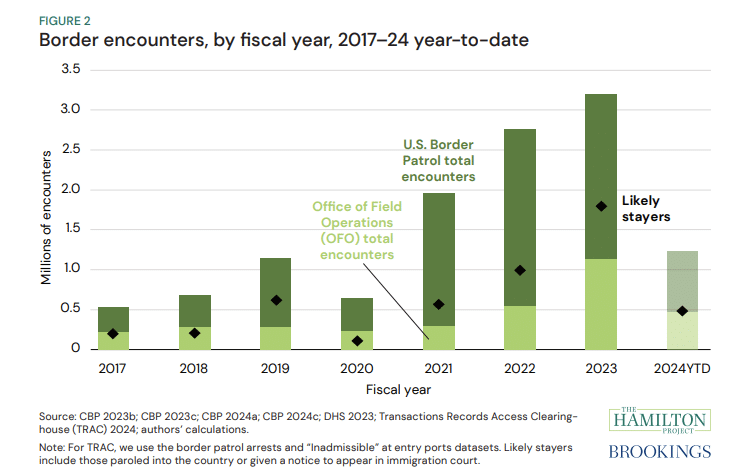

“We indicate our estimates of ‘likely stayers’ by diamonds in Figure 2. In FY 2023, almost a million people encountered at the border were given a ‘notice to appear,’ meaning they have permission to petition a court for asylum or other immigration relief. Most of these individuals are waiting in the U.S. for the asylum court queue, which has over a million case backlog. In addition, over 800,000 have been granted humanitarian parole (mostly immigrants from Ukraine, Haiti, Cuba, Nicaragua, and Venezuela). These 1.8 million ‘likely stayers’ in FY 2023 may or may not remain in the U.S. permanently, but most are currently living in the U.S. and participating in the economy. CBO estimates that there were 2 million such entries over the calendar year 2023, which is consistent with higher encounters at the end of the calendar year.”

According to the CBO’s estimates for 2023, the categories of lawful permanent resident migration, INA non-immigrant, and other non-immigrant equated to 3.3 million net entries. However, the number is likely much higher than estimates, subject to uncertainty about unencountered border crossings, visa overstays, and “got-aways.”

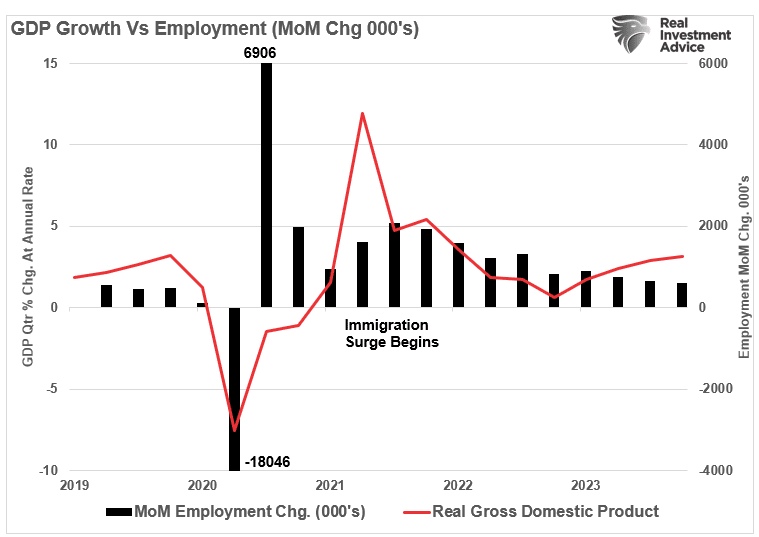

As such, this influx of immigrants has significantly added to payroll growth and has accounted for the uptick in economic growth starting in 2022. While the uptick in border encounters began in earnest in 2021, as the current Administration repealed previous border security actions, there is a “lag effect” of immigration on economic growth.

However, not all jobs are created equal.

Immigration’s Impact On Job Availability

Since 1980, the U.S. economy has shifted from a manufacturing-based economy to a service-oriented one. The reason is that the “cost of labor” in the U.S. to manufacture goods is too high. Domestic workers want high wages, benefits, paid vacations, personal time off, etc. On top of that are the numerous regulations on businesses from OSHA to Sarbanes-Oxley, FDA, EPA, and many others. All those additional costs are a factor in producing goods or services. Therefore, corporations must offshore production to countries with lower labor costs and higher production rates to manufacture goods competitively.

In other words, for U.S. consumers to “afford” the latest flat-screen television, iPhone, or computer, manufacturers must “export” inflation (the cost of labor and production) to import “deflation”(cheaper goods.) There is no better example of this than a previous interview with Greg Hays of Carrier Industries. Following the 2016 election, President Trump pushed for reshoring U.S. manufacturing. Carrier Industries was one of the first to respond. Mr. Hays discussed the reasoning for moving a plant from Mexico to Indiana.

“So what’s good about Mexico? We have a very talented workforce in Mexico. Wages are obviously significantly lower. About 80% lower on average. But absenteeism runs about 1%. Turnover runs about 2%. Very, very dedicated workforce.Which is much higher versus America. And I think that’s just part of these — the jobs, again, are not jobs on an assembly line that [Americans] really find all that attractive over the long term.“

The need to lower costs by finding cheaper and plentiful sources of labor continues. While employment continues to increase, the bulk of the jobs created are in areas with lower wages and skill requirements.

“The continued rebound of these jobs, along with strong months for sectors like construction, could be a sign that immigration is helping the labor market grow without putting too much upward pressure on wages.”

This is a crucial point. If there is strong employment growth, wages should increase commensurately as the demand for labor increases. However, that isn’t happening, as the cost of labor is suppressed by hiring workers willing to work for less compensation. In other words, the increase in illegal immigrants is lowering the “average” wage for Americans.

Nonetheless, in the last year, 50% of the labor force growth came from net immigration. The U.S. added 5.2 million jobs last year, which boosted economic growth without sparking inflationary pressures.

While immigration has positively impacted economic growth and disinflation, this story has a dark side.

FED CHAIR POWELL: Because, you know, immigrants come in, and they tend to work at a rate that is at or above that for non-immigrants. Immigrants who come to the country tend to be in the workforce at a slightly higher level than native Americans. But that’s primarily because of the age difference. They tend to skew younger.“

You should read that comment again carefully. As noted by Greg Hayes, immigrants tend to work harder and for less compensation than non-immigrants. That suppression of wages and increased productivity, which reduces the amount of required labor, boosts corporate profitability.

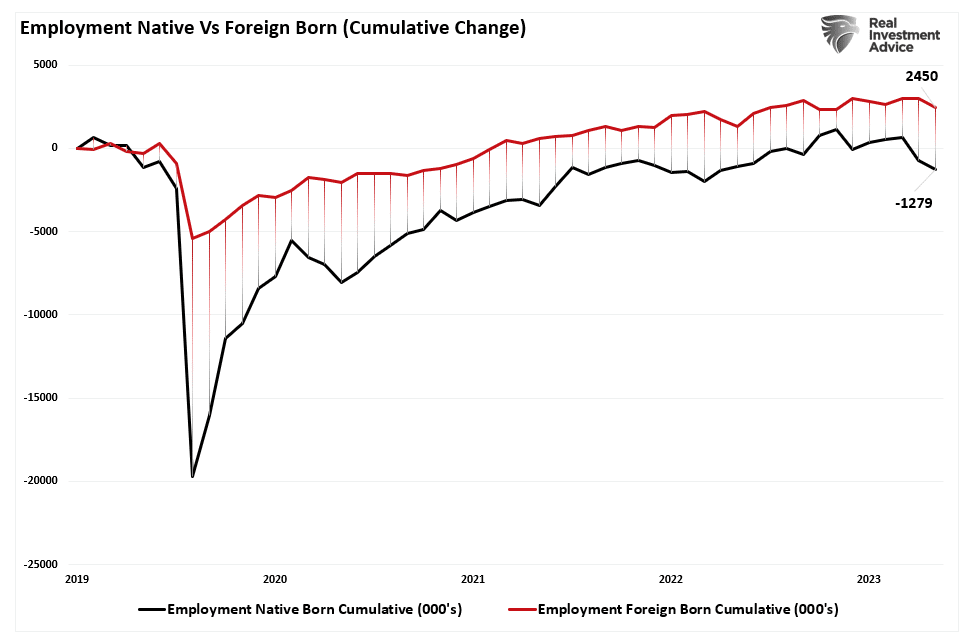

The move to hire cheaper labor should be unsurprising. Following the pandemic-related shutdown, corporations faced multiple threats to profitability from supply constraints, a shift to increased services, and a lack of labor. At the same time, mass immigration (both legal and illegal) provided a workforce willing to fill lower-wage paying jobs and work regardless of the shutdown. Since 2019, the cumulative employment change has favored foreign-born workers, who have gained almost 2.5 million jobs, while native-born workers have lost 1.3 million. Unsurprisingly, foreign-born workers also lost far fewer jobs during the pandemic shutdown.

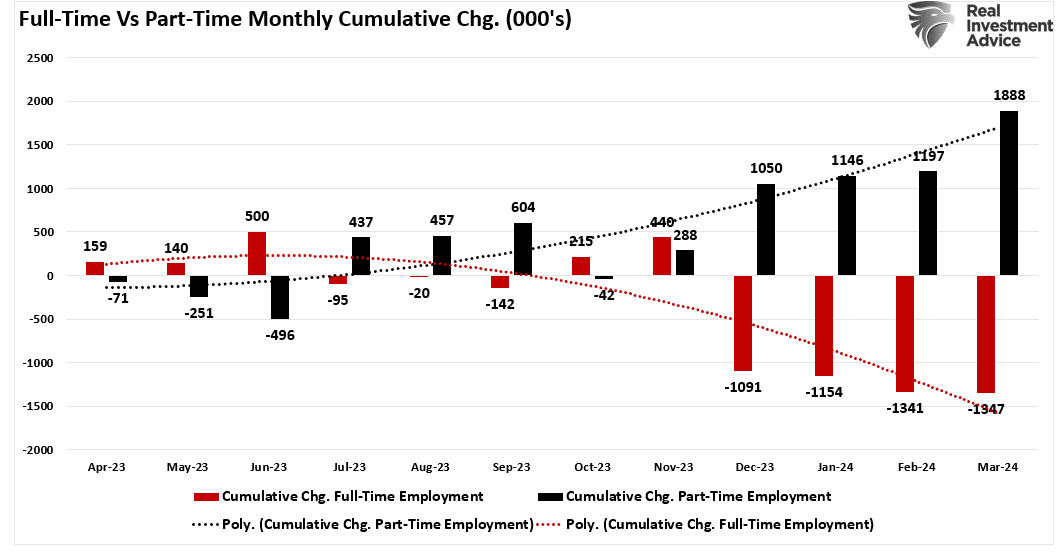

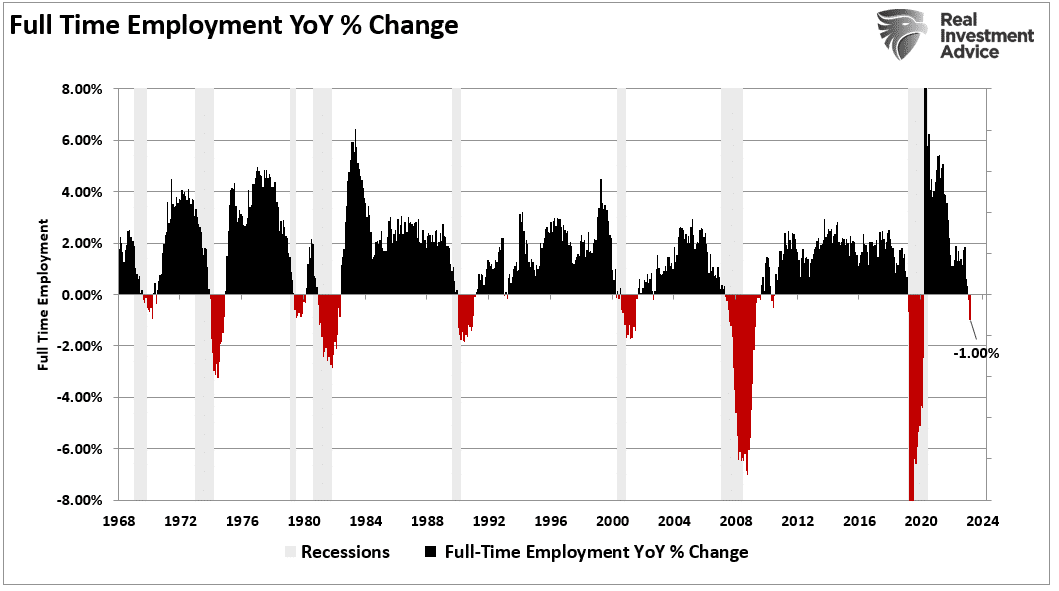

Given that the bulk of employment continues to be in lower-wage paying service jobs (i.e., restaurants, retail, leisure, and hospitality) such is why part-time jobs have dominated full-time in recent reports. Since last year, part-time jobs have risen by 1.8 million while full-time employment has declined by 1.35 million.

Not dismissing the implications of the shift to part-time employment is crucial.

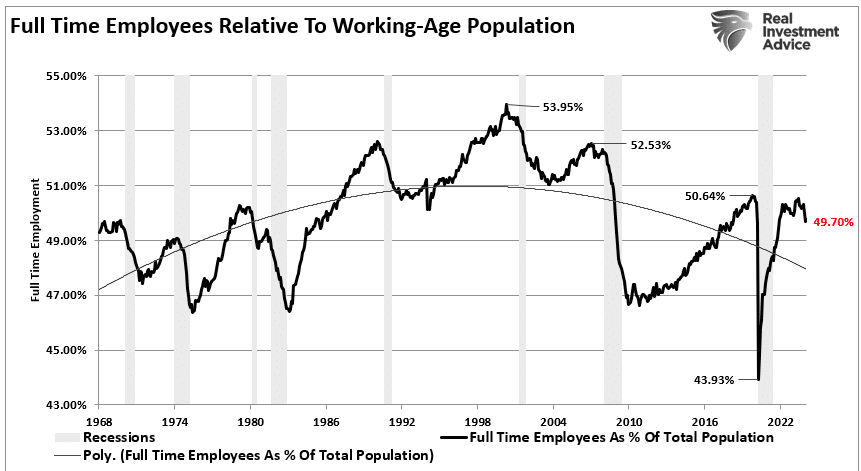

Personal consumption, what you and I spend daily, drives nearly 70% of economic growth in the U.S. Therefore, Americans require full-time employment to consume at an economically sustainable rate. Full-time jobs provide higher wages, benefits, and health insurance to support a family, whereas part-time jobs do not.

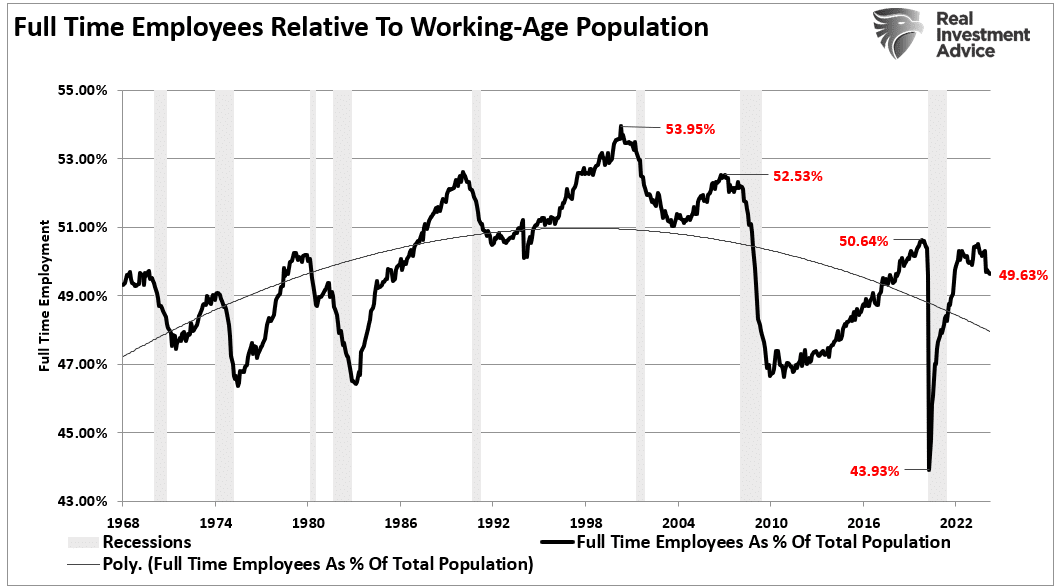

Notably, given the surge in immigration into the U.S. over the last few years, the all-important ratio of full-time employees relative to the population has dropped sharply. As noted, given that full-time employment provides the resources for excess consumption, that ratio should increase for the economy to continue growing strongly.

However, the reality is that the full-time employment rate is falling sharply. Historically, when the annual rate of change in full-time employment dropped below zero, the economy entered a recession.

While there is much debate over immigration, most of the arguments do not differentiate between legal and illegal immigration. There are certainly arguments that can be made on both sides. However, what is less debatable is the impact that immigration is having on employment and wages. Of course, as native-born workers continue to demand higher wages, benefits, and other tax-funded support, those costs must be passed on by the companies creating those products and services. At the same time, consumers are demanding lower prices.

That imbalance between input costs and selling price drives companies to aggressively seek options to reduce the highest cost to any business – labor.

Such is why full-time employment has declined since 2000 despite the surge in the Internet economy, robotics, and artificial intelligence. It is also why wage growth fails to grow fast enough to sustain the cost of living for the average American. These technological developments increased employee productivity, reducing the need for additional labor.

Unfortunately, college graduates expecting high-paying jobs will likely continue to find it increasingly frustrating. Such is particularly the case as “Artificial Intelligence” gains traction and displaces “white collar” work, further squeezing the demand for “native-born” workers.

Margin Debt Surges As Bulls Leverage Bets

In the most recent report from FINRA, margin debt levels have surged as bullish investors leverage their bets in the equity market. The increase in leverage is not surprising, as it represents increased risk-taking by investors in the stock market.

We previously discussed that valuations, in the short term, reflect investor optimism. In other words, as prices increase, investors rationalize why paying more for current earnings is rational.

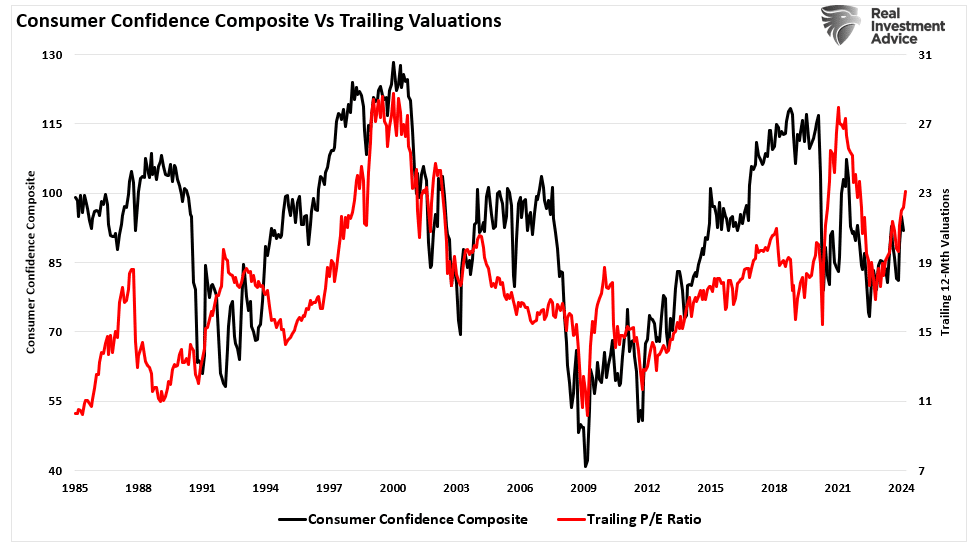

“Valuation metrics are just that – a measure of current valuation. More importantly, when valuation metrics are excessive, it is a better measure of ‘investor psychology’ and the manifestation of the ‘greater fool theory.’ As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations.”

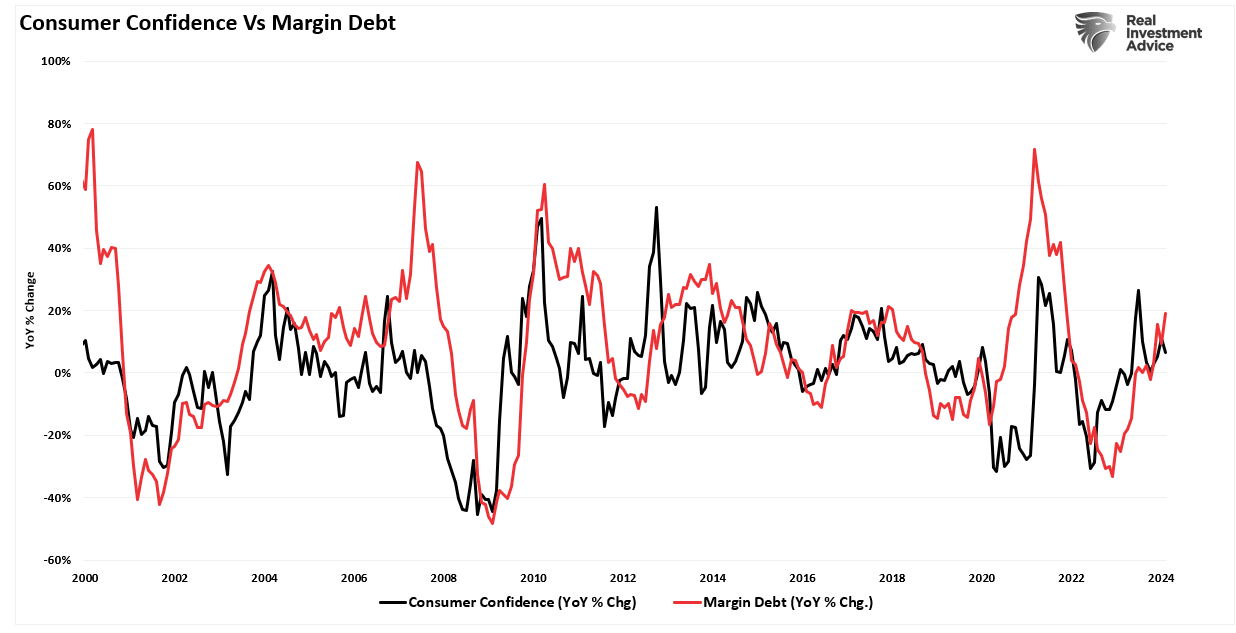

The same holds for margin debt. Unsurprisingly, as consumer confidence improves, so does the speculative demand for equities. As stock markets improve, the “fear of missing out” becomes more prevalent. Such boosts demand for equities, and as prices rise, investors take on more risk by adding leverage.

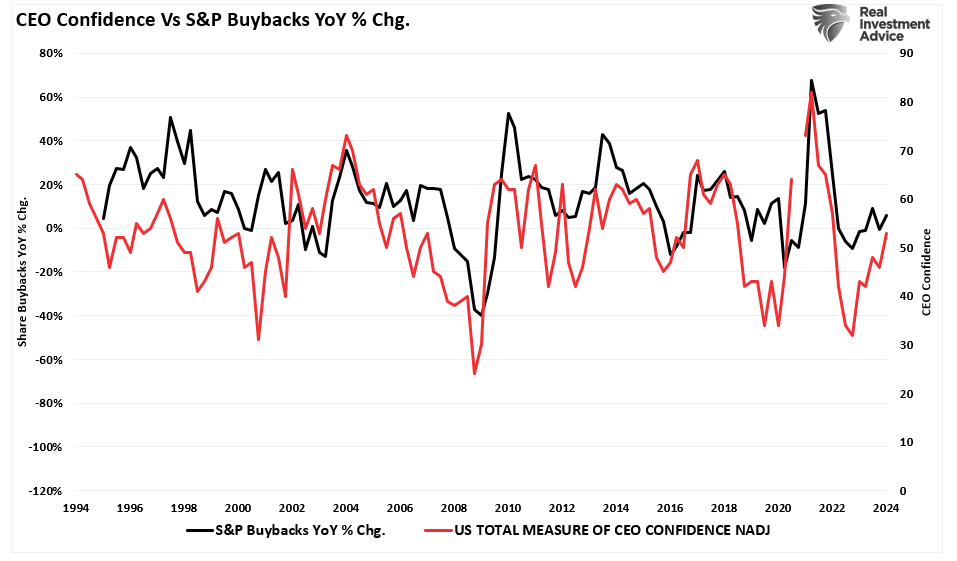

Adding to that exuberance is the increased demand for share repurchases, which has been a primary source of “buying” since 2000. As CEO confidence improves, a byproduct of increased consumer confidence, they increase the demand for share repurchases. As buybacks boost asset prices, investors take on more leverage and increase exposure as a virtual spiral develops.

However, should investors be afraid of rising margin debt?

A Byproduct Of Exuberance

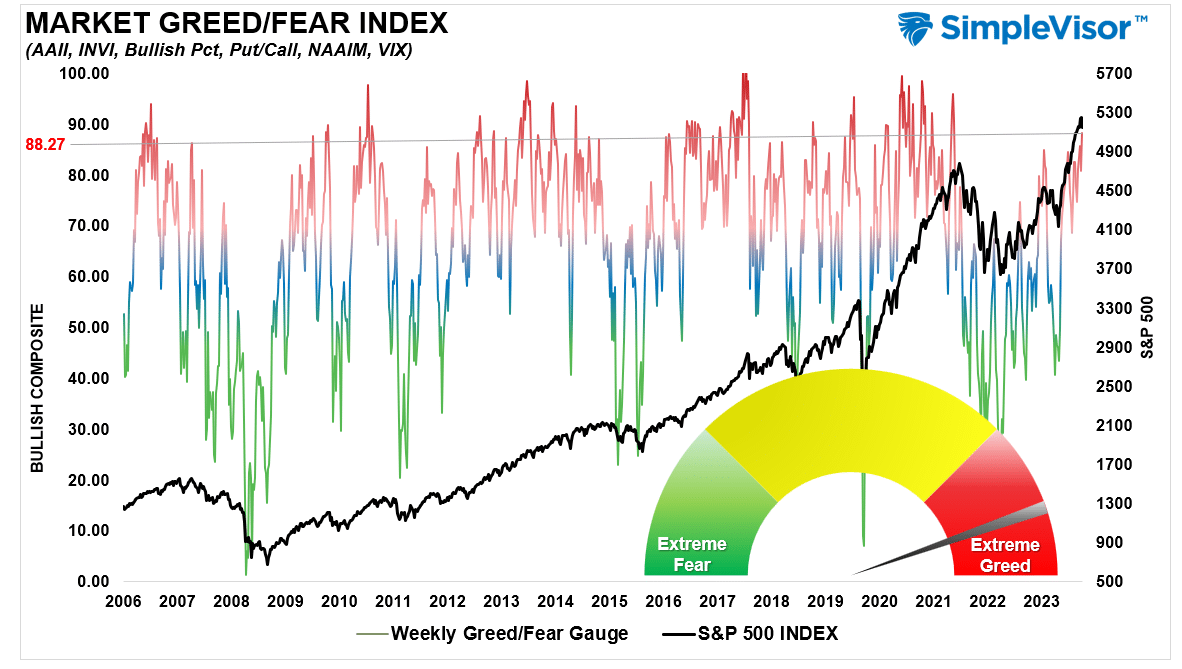

Before we dig further into what margin debt tells us, let’s begin with where we are currently. There is clear evidence that investors are once again highly exuberant. The “Fear Greed” index below differs from the CNN measure in that our model measures positioning in the market by how much professional and retail investors are exposed to equity risk. Currently, that exposure is at levels associated with investors being “all in” the equity “pool.”

As Howard Marks noted in a December 2020 Bloomberg interview:

“Fear of missing out has taken over from the fear of losing money. If people are risk-tolerant and afraid of being out of the market, they buy aggressively, in which case you can’t find any bargains. That’s where we are now. That’s what the Fed engineered by putting rates at zero…we are back to where we were a year ago—uncertainty, prospective returns that are even lower than they were a year ago, and higher asset prices than a year ago. People are back to having to take on more risk to get return. At Oaktree, we are back to a cautious approach. This is not the kind of environment in which you would be buying with both hands.

The prospective returns are low on everything.”

Of course, in 2021, that market continued its low volatility grind higher as investors took on increasing margin debt levels to chase higher equities. However, this is the crucial point about margin debt.

Margin debt is not a technical indicator for trading markets. What it represents is the amount of speculation occurring in the market. In other words, margin debt is the “gasoline,” which drives markets higher as the leverage provides for the additional purchasing power of assets. However, leverage also works in reverse, as it supplies the accelerant for more significant declines as lenders “force” the sale of assets to cover credit lines without regard to the borrower’s position.

The last sentence is the most important. The issue with margin debt is that the unwinding of leverage is NOT at the investor’s discretion. That process is at the discretion of the broker-dealers that extended that leverage in the first place. (In other words, if you don’t sell to cover, the broker-dealer will do it for you.) When lenders fear they may not recoup their credit lines, they force the borrower to put in more cash or sell assets to cover the debt. The problem is that “margin calls” generally happen simultaneously, as falling asset prices impact all lenders simultaneously.

Margin debt is NOT an issue – until it is.

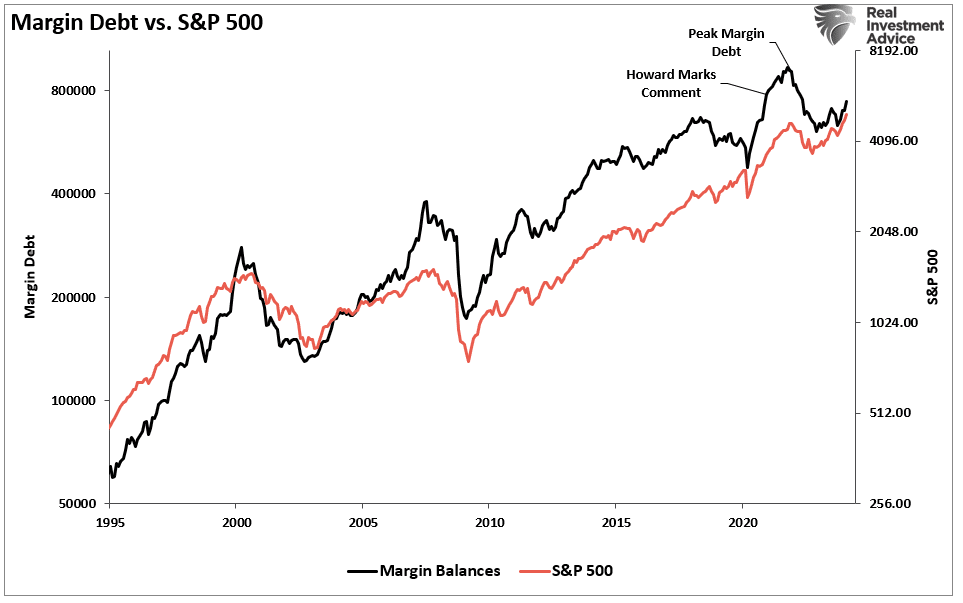

As shown, Howard was eventually right. In 2022, the decline wiped out all of the previous year’s gains and then some.

So, where are we currently?

Margin Debt Confirms The Exuberance

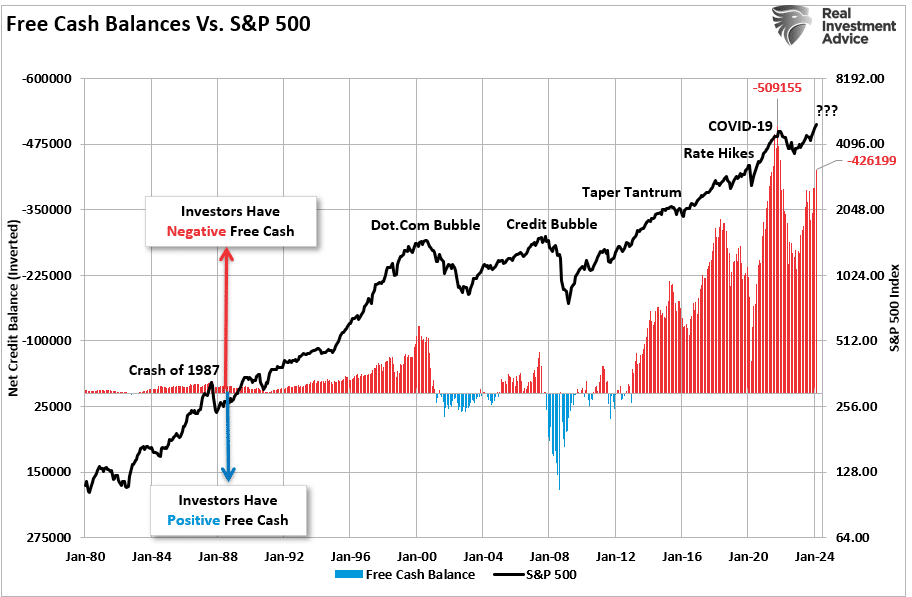

As noted, margin debt supports the advance when markets are rising and investors are taking on additional leverage to increase buying power. Therefore, the recent rise in margin debt is unsurprising as investor exuberance climbs. The chart shows the relationship between cash balances and the market. I have inverted free cash balances, so the relationship between increases in margin debt and the market is better represented. (Free cash balances are the difference between margin balances less cash and credit balances in margin accounts.)

Note that during the 1987 correction, the 2015-2016 “Brexit/Taper Tantrum,” the 2018 “Rate Hike Mistake,” and the “COVID Dip,” the market never broke its uptrend, AND cash balances never turned positive. Both a break of the rising bullish trend and positive free cash balances were the 2000 and 2008 bear market hallmarks. With negative cash balances shy of another all-time high, the next downturn could be another “correction.” However, if, or when, the long-term bullish trend is broken, the unwinding of margin debt will add “fuel to the fire.”

While the immediate response to this analysis will be, “But Lance, margin debt isn’t as high as it was previously,” there are many differences between today and 2021. The lack of stimulus payments, zero interest rates, and $120 billion in monthly “Quantitative Easing” are just a few. However, some glaring similarities exist, including the surge in negative cash balances and extreme deviations from long-term means.

In the short term, exuberance is infectious. The more the market rallies, the more risk investors want to take on. The issue with margin debt is that when an event eventually occurs, it creates a rush to liquidate holdings. Since margin debt is a function of the value of the underlying “collateral,” the forced sale of assets will reduce the value of the collateral. The decline in value then triggers further margin calls, triggering more selling, forcing more margin calls, and so forth.

Margin debt levels, like valuations, are not useful as a market-timing device. However, they are a valuable indicator of market exuberance.

While it may “feel” like the market “just won’t go down,” it is worth remembering Warren Buffett’s sage words.

“The market is a lot like sex, it feels best at the end.”

Investing Lessons From Your Mother

Your mother likely imparted valuable investing lessons you may not have known. With Mother’s Day approaching and bullish market exuberance present, such is an excellent time to revisit the investing lessons she taught me.

Personally, when I was growing up, my Mother had a saying, or an answer, for almost everything… as most mothers do. Every answer to the question “Why?” was immediately met with the most intellectual of answers:

“…because I said so”.

Seriously, my Mother was a resource of knowledge that has served me well over the years, and it wasn’t until late in life that I realized that she had taught me, unknowingly, valuable investing lessons to keep me safe.

So, by imparting her secrets to you, I may be violating some sacred ritual of motherhood knowledge, but I felt it was worth the risk of sharing the knowledge that has served me well.

1) Don’t Run With Sharp Objects!

It wasn’t hard to understand why she didn’t want me to run with scissors through the house – I think I did it early on to watch her panic. However, later in life, when I got my first apartment, I ran through the entire place with a pair of scissors, left the front door open with the air conditioning on, and turned every light on in the house.

That rebellion immediately stopped when I received my first electric bill.

Sometime in the mid-90s, the financial markets became a casino as the internet age ignited a whole generation of stock market gamblers who thought they were investors. There is a vast difference between investing and speculating; knowing the difference is critical to overall success.

A solid investment strategy combines defined goals, an accumulation schedule, allocation analysis, and, most importantly, a defined sell strategy and risk management plan.

Speculation is nothing more than gambling. If you are buying the latest hot stock, chasing stocks that have already moved 100% or more, or just putting money in the market because you think you “have to,” you are gambling.

The most important thing to understand about gambling is that success is a function of the probabilities and possibilities of winning or losing on each bet.

In the stock market, investors continue to play the possibilities instead of the probabilities. The trap comes with early success in speculative trading. Success breeds confidence, and confidence breeds ignorance. Most speculative traders tend to “blow themselves up” because of early success in their speculative investing habits.

When investing, remember that the odds of making a losing trade increase with the frequency of transactions. Just as running with a pair of scissors, do it often enough, and eventually, you could end up hurting yourself.

2) Look Both Ways Before You Cross The Street.

I grew up in a small town, so crossing the street wasn’t as dangerous as in the city. Nonetheless, she yanked me by the collar more than once as I started to bolt across the street, seemingly anxious to “find out what’s on the other side.” It is essential to understand that traffic does flow in two directions. If you only look in one direction, you will get hit sooner or later.

Many people want to classify themselves as a “Bull” or a “Bear.”The savvy investor doesn’t pick a side; he analyzes both sides to determine what the best course of action in the current market environment is most likely to be.

The problem with the proclamation of being a “bull” or a “bear” means that you are not analyzing the other side of the argument and that you become so confident in your position that you tend to forget that “the light at the end of the tunnel…just might be an oncoming train.”

It is an essential part of your analysis, before you invest in the financial markets, to determine not only “where” but also “when” to invest your assets.

3) Always Wear Clean Underwear

This was one of my favorite sayings from my Mother because I always wondered about the rationality of it. I always figured that even if you wore clean underwear before an accident, you’re still likely left without clean underwear following it.

The investing lesson is: “You are only wrong – if you stay wrong.“

However, being an intelligent investor means always being prepared in case of an accident. That means simply having a mechanism to protect you when you are wrong with an investment decision.

You will notice that I said “when you are wrong” in the previous paragraph. Many of your investment decisions will likely turn out wrong. However, cutting those wrong decisions short and letting your right decisions continue to work will make you profitable over time.

Any person who tells you about all the winning trades he has made in the market – is either lying or hasn’t blown up yet.

One of the two will be true – 100% of the time.

Understanding the “risk versus reward” trade-off of any investment is the beginning step to risk management in your portfolio. Knowing how to mitigate the risk of loss in your holdings is crucial to your long-term survivability in the financial markets.

4) If Everyone Jumped Off The Cliff – Would You Do It Too?

Every kid, at one point or another, has tried to convince their Mother to allow them to do something through “peer pressure.” I figured if she wouldn’t let me do what I wanted, she would bend to the will of the imaginary masses. She never did.

“Peer pressure” is one of the biggest mistakes investors repeatedly make. Chasing the latest “hot stocks” or “investment fads” that are already overvalued and are running up on speculative fervor always ends in disappointment.

Investors buy stocks that have moved significantly off their lows in the financial markets because they fear “missing out.”This is speculating, gambling, guessing, hoping, praying – anything but investing. Generally, when the media begins featuring a particular investment, individuals have already missed the major part of the move. By that point, the probability of a decline began to outweigh the possibility of further rewards.

The investing lesson is to be aware of the “herd mentality.” Historically, investors tend to run in the same direction until that direction falters. The “herd” then turns and runs in the opposite direction. This continues to the detriment of investors’ returns over long periods.

This is also generally why investors wind up buying high and selling low. To be a long-term successful investor, you must understand the “herd mentality” and use it to your benefit – getting out from in front of the herd before you are trampled.

So, before you chase a stock that has already moved 100% or more, figure out where the herd may move to next and “place your bets there.” This takes discipline, patience, and a lot of homework, but you will often be rewarded for your efforts.

5) Don’t Talk To Strangers

This is just good, solid advice all the way around. Turn on the television, any time of the day or night, and it is the “Stranger’s Parade of Malicious Intent.” I don’t know if it is just me or if the media only broadcasts news revealing human depravity’s depths. Still, sometimes, I wonder if we are not due for a planetary cleansing through divine intervention.

However, back to investing lessons, getting your stock tips from strangers is a sure way to lose money in the stock market. Your investing homework should NOT consist of a daily regimen of CNBC, followed by a dose of Grocer tips, capped off with a financial advisor’s sales pitch.

To succeed in the long run, you must understand investing principles and the catalysts to make that investment profitable. Remember, when you invest in a company, you buy a piece of it and its business plan. You are placing your hard-earned dollars into the belief that the individuals managing the company have your best interests at heart. The hope is they will operate in such a manner as to make your investment more valuable so that it may eventually be sold to someone else for a profit.

This also embodies the “Greater Fool Theory,” which states that someone will always be willing to buy an investment at an ever higher price. The investing lesson is that, in the end, someone is always left “holding the bag.” The trick is to ensure that it isn’t you.

Also, you must be aware of this when getting advice from the “One Minute Money Manager” crew on television. When an “expert” tells you about a company you should be buying, remember he already owns it and most likely will be the one selling his shares to you.

6) You Either Need To “Do It” (polite version) Or Get Off The Pot!

When I was growing up, I hated to do my homework, which is ironic since I now do more homework than I ever dreamed of in my younger days. Since I wouldn’t say I liked doing homework, school projects were rarely started until the night before they were due. I was the king of procrastination.

My Mom was always there to help, giving me a hand and an ear full of motherly advice, usually consisting of many “because I told you so…”

Interestingly, many investors tend to watch stocks for a very long period, never acting on their analysis but idly watching as their instinct proves correct and the stock rises in price.

The investor then feels that they missed his entry point and decides to wait, hoping the stock will go back down one more time so that he can get in. The stock continues to rise. The investor continues to watch, becoming more frustrated until he finally capitulates on his emotion and buys the investment near the top.

The investing lesson is to be aware of the dangers of procrastination. On the way up and down, procrastination is the precursor of emotional duress derived from the loss of opportunity or the destruction of capital.

However, if you do your homework and can build a case for the purchase, don’t procrastinate. If you miss your opportunity for the correct entry into the position – don’t chase it. Leave it alone, and come back another day when ole’ Bob Barker is telling you – “The Price Is Right.”

7) Don’t Play With It – You’ll Go Blind

Well…do I need to go into this one? All I know for sure is that I am not blind today. What I will never know for sure is whether she believed it or if it was just meant to scare the hell out of me.

However, kidding aside, the investing lesson is that when you invest in the financial markets, it is very easy to lose sight of your intentions in the first place. Getting caught up in the hype, getting sucked in by the emotions of fear and greed, and generally being confused by the multitude of options available can cause you to lose your focus.

Always return to the basic principle you started with. That goal was to grow your small pile of money into a much larger one.

Putting It All Together

My Dad once taught me a fundamental investing lesson as well: KISS: Keep It Simple Stupid.

This is one of the best investment lessons you will ever receive. Too many people try to outsmart the market to gain a small, fractional increase in return. Unfortunately, they take disproportionate risks, often leading to negative results. The simpler the strategy is, the better the returns tend to be. Why? There is better control over the portfolio.

Designing a KISS portfolio strategy will help ensure that you don’t get blinded by continually playing with your portfolio and losing sight of what your original goals were in the first place.

Decide what your objective is: Retirement, College, House, etc.

Define a time frame to achieve your goal.

Determine how much money you can “realistically” put toward your monthly goal.

Calculate the return needed to reach your goal based on your starting principal, the number of years to your goal, and your monthly contributions.

Break down your goal into achievable milestones. These milestones could be quarterly, semi-annual, or annual and will help ensure you are on track to meet your objective.

Select the appropriate asset mix that achieves your required results without taking on excess risk that could lead to more significant losses than planned.

Develop and implement a specific strategyto sell positions during random market events or unexpected market downturns.

If this is more than you know how to do – hire a professional who understands essential portfolio and risk management.

There is much more to managing your portfolio than just the principles we learned from our Mothers. However, this is a start in the right direction, and if you don’t believe me – just ask your Mother.

Market Corrections Matter More Than You Think

During running bull markets, much commentary is written on why this time is different and why investors should not worry about market corrections. One such piece was written recently by Fisher Investments. To wit:

“After the S&P 500’s 26% return last year and this year’s strong start, many investors are worried – understandably – that this bull run is getting ahead of itself.

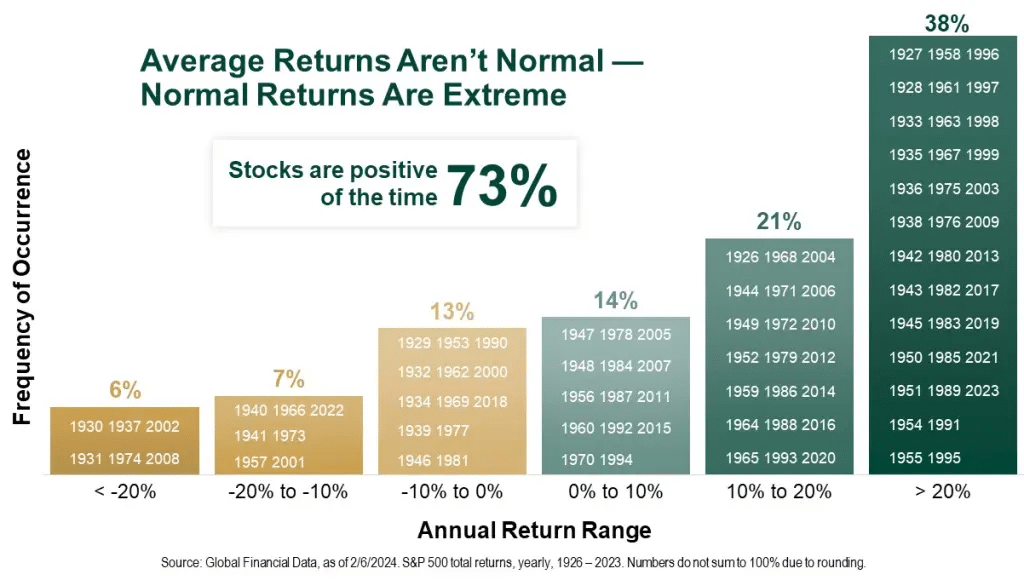

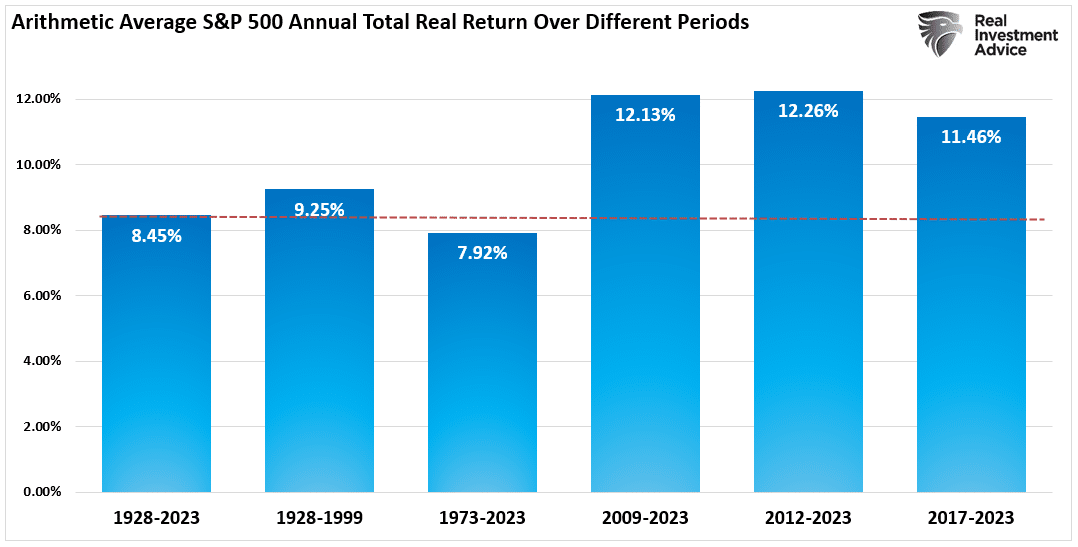

They shouldn’t. The strange-but-true fact is that, statistically speaking, average returns — which have amounted to about 10% a year over nearly a century of trading — aren’t normal in the stock market for any given year. A second, surprisingly pleasant fact is that so-called “extreme” returns are far closer to what we’d call normal — and they’re mostly on the positive side.”

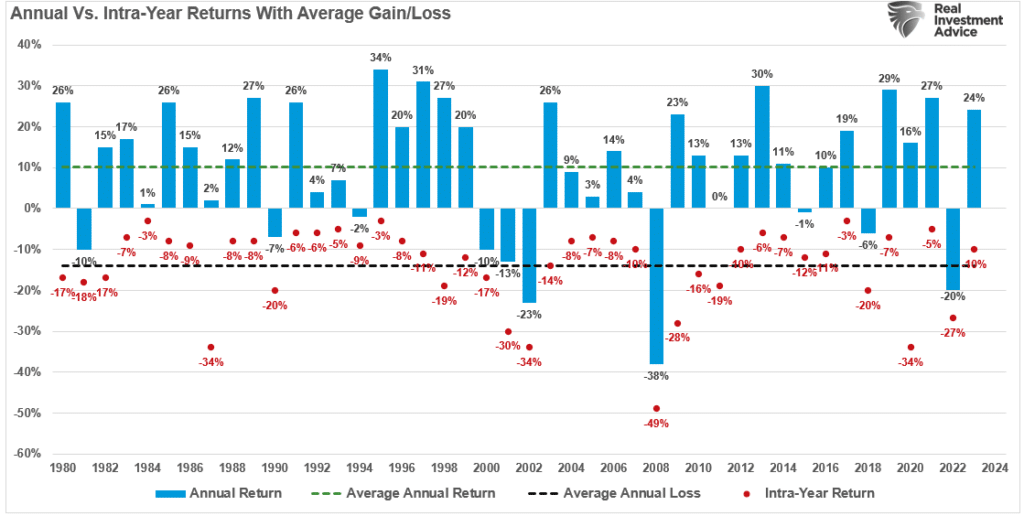

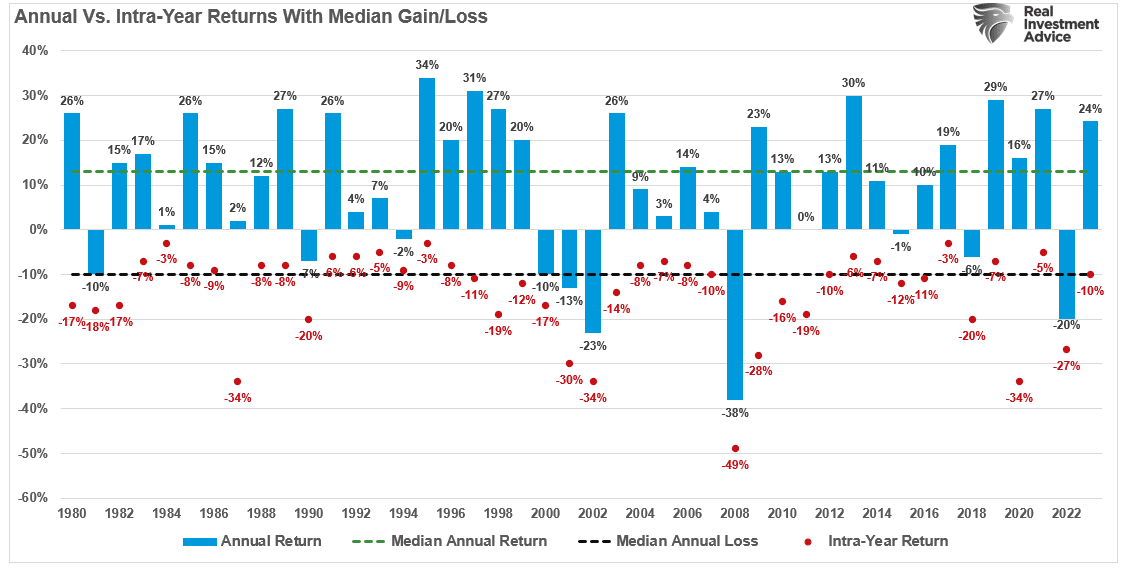

There are a lot of problems with that statement, which we will get into. However, there are some essential facts about markets that should be understood. First, indeed, stocks rise more often than they fall. Historically speaking, the stock market increases about 73% of the time. The other 27% of the time, market corrections are reversing the excesses of the previous advance. The table below shows the dispersion of returns over time.

However, fairly substantial corrections have not been uncommon in those positive return years. As shown in the table below, intra-year corrections, which average roughly 10%, are common.

There is little to be concerned about as 38% of the time, the market is cranking out greater than 20% returns versus just 6% of 20% or more market corrections. As Mr. Fisher notes:

“The upshot? Big returns simply aren’t the rarity that “too far, too fast” bears claim. In bull markets, they are more normal than not. Why? The roughly 10% long-term annual average includes bear markets. Strip out the bears and you’ll find that during the 14 S&P 500 bull markets before this one, stocks annualized 23%.“

The problem with Mr. Fisher’s statement is that he doesn’t understand the math behind market corrections. As we will explain, a significant difference exists between a 20% advance and a 20% market correction. Such is particularly the case if you are in or approaching retirement.

Market Corrections And The Function Of Math

Notice that the table above uses percentage returns. As noted, that is a deceptive take if you don’t examine the issue beyond a cursory glance.

For example, assume an arbitrary stock market index that trades at 1000 points. Over the next 12 months, the index will increase by 20%. The index value is now 1200 points.

During the next 12 months, the index declines by one of those rare outliers of 20%. The index doesn’t just give up its gain of 200 points.

1200 x (-20%) = 240 points = 960 points

The investor now has an unrealized capital loss.

Let’s take this example further and assume the index goes from 1000 to 8000.

1000 to 2000 = 100% return

From 1000 to 3000 = 200% return

The next 1000 to 4000 = 300% return

…

The final 1000 to 8000 = 700% return

No one would argue that a 700% return on their money wasn’t fantastic. However, let’s do some math:

10% loss equals an 800-point decline, nearly wiping out the last 1000-point advance.

20% market correction is 1600 points

30% decline erases 2400 points.

40% loss equals 3200 points or nearly 50% of all the gains.

50% decline is 4000 points.

The problem with using percentages to measure an advance is that there is an unlimited upside. However,you can only lose 100%.

A Graphic Example

That is the problem of percentages. We can also show this graphically.

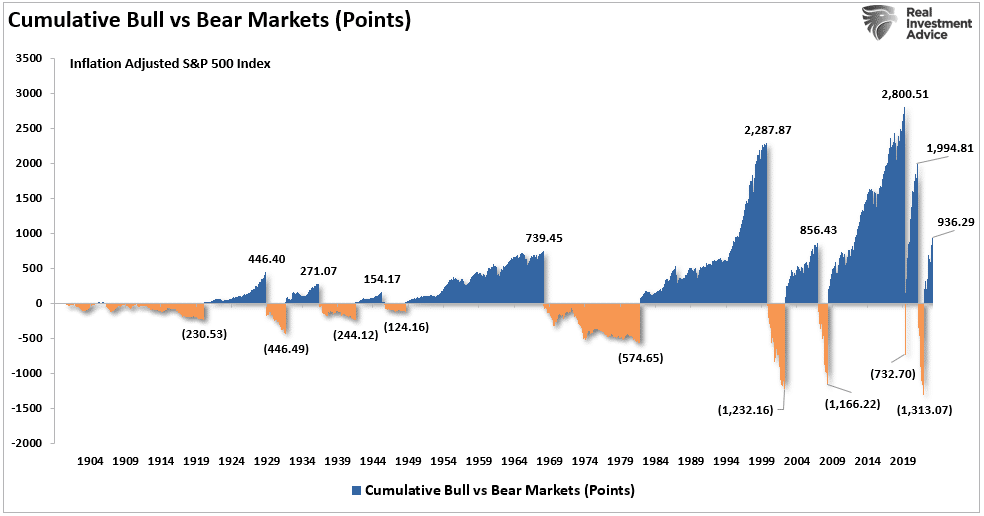

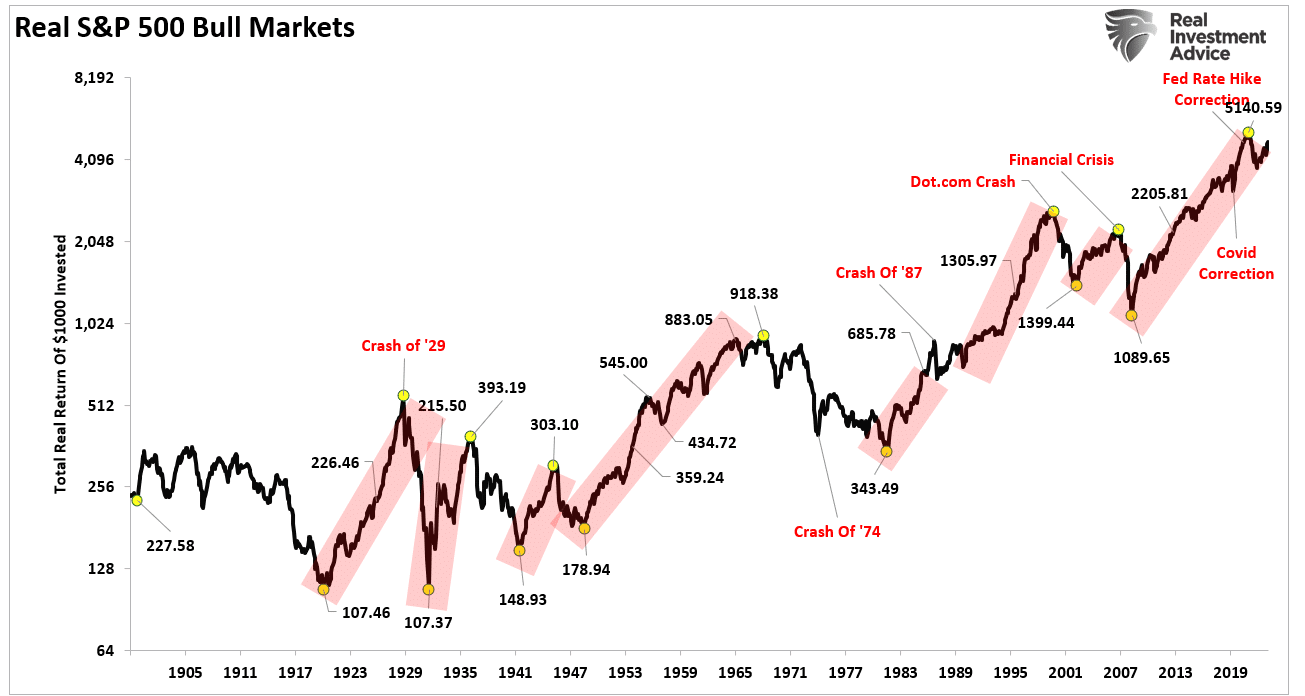

One of the charts often used by the “perma bulls” like Ken Fisher to coax individuals into not worrying about portfolio risk is measuring the cumulative advances and declines of the market in percentages. When presented this way, the bear market corrections are hardly noticeable. This chart is often used to convince individuals that bear markets don’t matter much over the long term.

However, as noted above, this presentation is very deceptive due to how math works. If we change from percentages to actual point changes, the devastation of market corrections becomes more evident. Historically, the subsequent declines wiped out huge chunks of the previous advances. Of course, at the bottom of these market corrections, investors generally sell due to the mounting losses’ psychological pressures.

This is why, after two of the most significant bull markets in history, most individuals have very little money invested in the financial markets.

Average And Actual Returns Are Not The Same

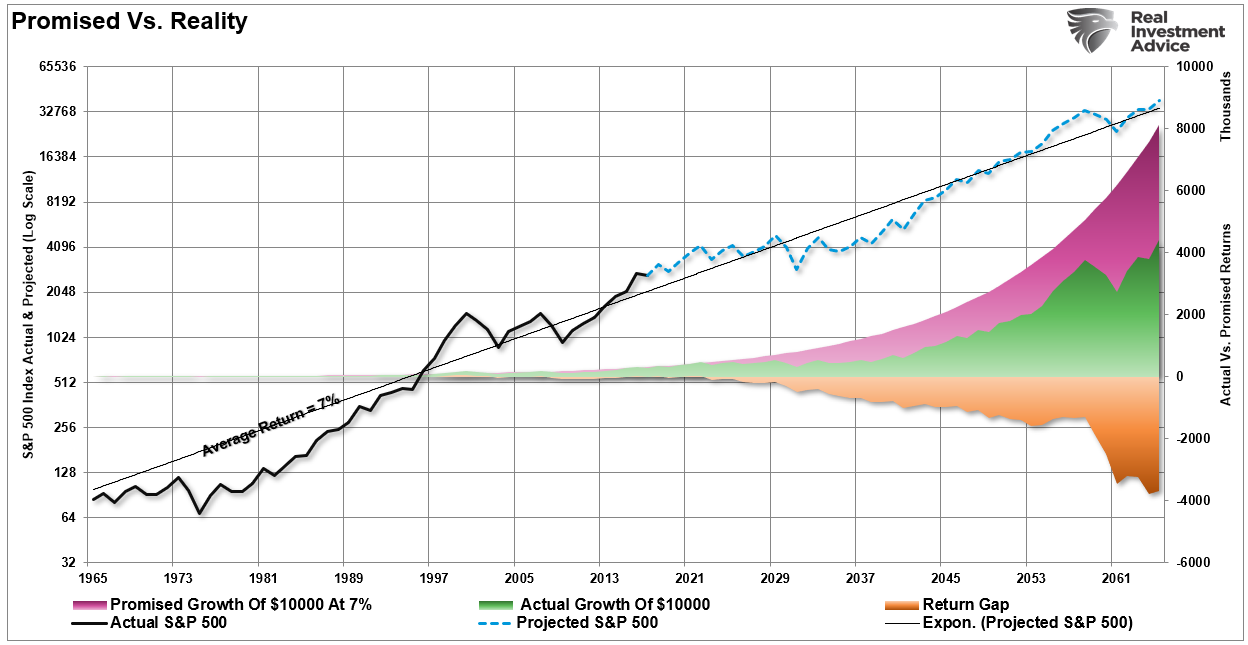

There is a massive difference between AVERAGE and ACTUAL returns on invested capital. Thus, in any given year, the impact of losses destroys the annualized “compounding” effect of money.

The chart below shows the difference between “actual” investment returns and “average” returns over time. See the problem? The purple-shaded area and the market price graph show “average” returns of 7% annually. However, the return gap in “actual returns,” due to periods of capital destruction, is quite significant.

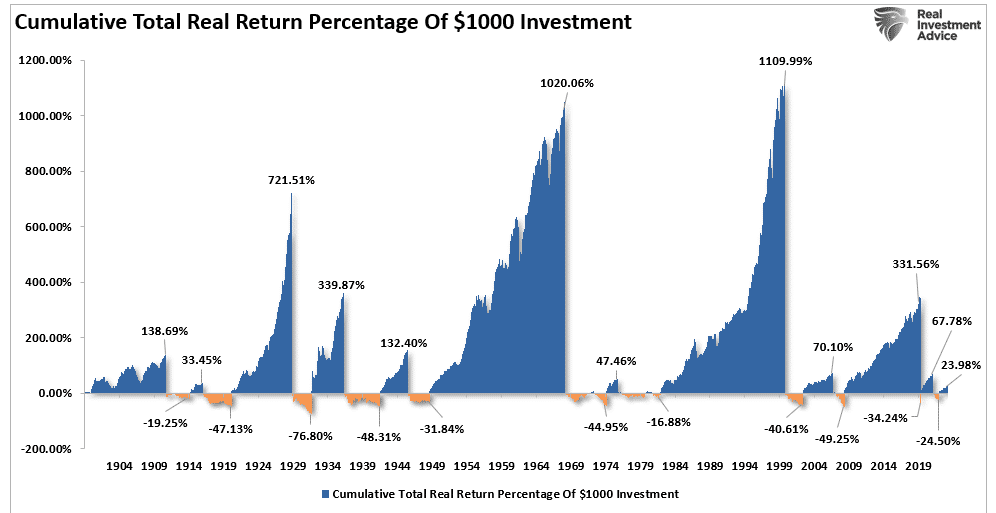

In the chart box below, I have taken a $1000 investment for each period and assumed the total return holding period until death. There are no withdrawals made. (Note: the periods from 1983 forward are still running as the investable life expectancy span is 40-plus years.)

The orange sloping line is the “promise” of 6% annualized compound returns. The black line represents what happened with invested capital from 35 years of age until death. At the bottom of each holding period, the bar chart shows the surplus, or shortfall, of the 6% annualized return goal.

At the point of death, the invested capital is short of the promised goal in every case except the current cycle starting in 2009. However, that cycle is yet to be complete, and the next significant downturn will likely reverse most, if not all, of those gains. Such is why using “compounded” or “average” rates of return in financial planning often leads to disappointment.

Three Key Considerations

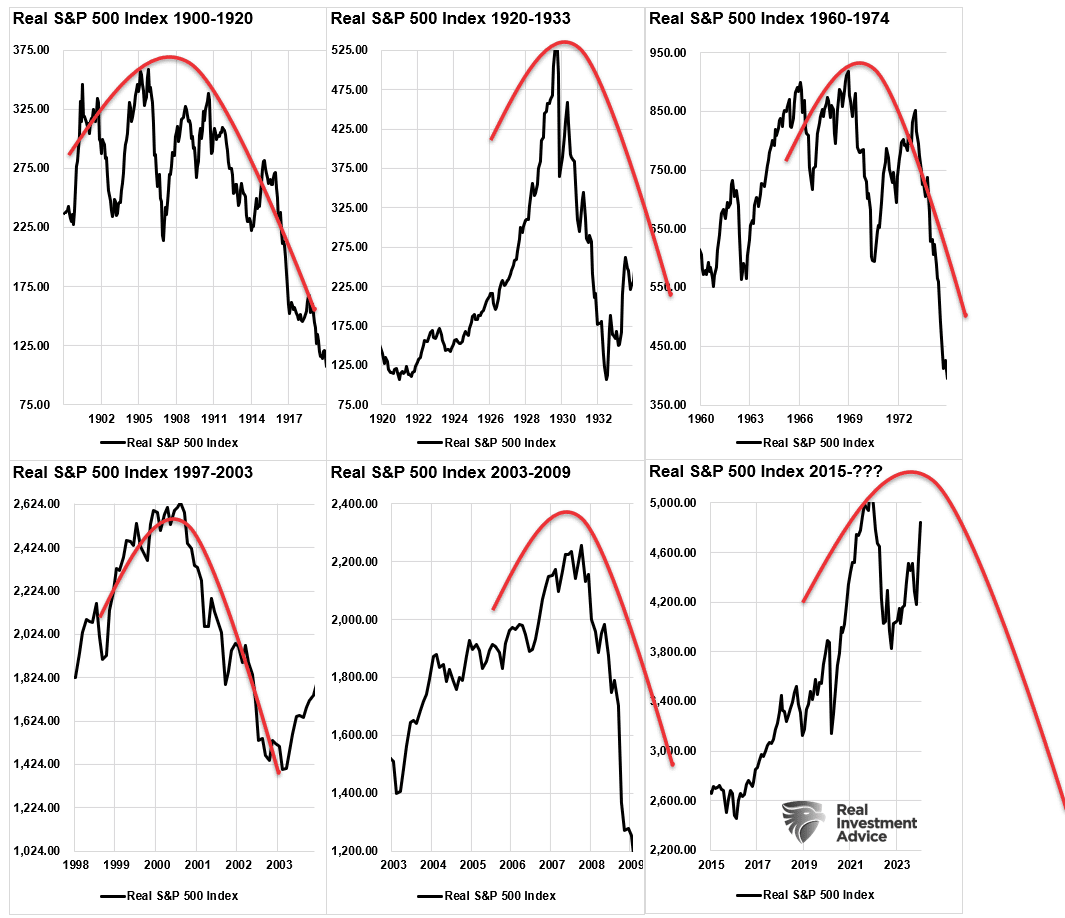

Over the next few months, the markets can extend the current deviations from the long-term mean even further. But that is the nature of every bull market peak and bubble throughout history as the seeming impervious advance lures the last stock market “holdouts” back into the markets.

As such, three key considerations exist for individuals currently invested in the stock market.

Time horizon (retirement age less starting age)

Valuations at the beginning of the investment period.

Rate of return required to achieve investment goals.

Suppose valuations are high at the beginning of the investment journey. In that case, if the time horizon is too short or the required rate of return is too high, the outcome of a “buy and hold” strategy will most likely disappoint expectations.

Mean reverting events expose the fallacies of “buy-and-hold” investment strategies. The “stock market” is NOT the same as a “high yield savings account,” and losses devastate retirement plans. (Ask any “boomer” who went through the dot.com crash or the financial crisis.”)

Therefore, during excessively high valuations, investors should consider opting for more “active” strategies with a goal of capital preservation.

As Vitaliy Katsenelson once wrote:

“Our goal is to win a war, and to do that we may need to lose a few battles in the interim. Yes, we want to make money, but it is even more important not to lose it.”

I agree with that statement, so we remain invested but hedged within our portfolios.

Unfortunately, most investors do not understand market dynamics and how prices are “ultimately bound by the laws of physics.” While prices can certainly seem to defy the law of gravity in the short term, the subsequent reversion from extremes has repeatedly led to catastrophic losses for investors who disregard the risk.

Just remember, in the market, there is no such thing as “bulls” or “bears.”

There are only those who “succeed” in reaching their investing goals and those who “fail.”

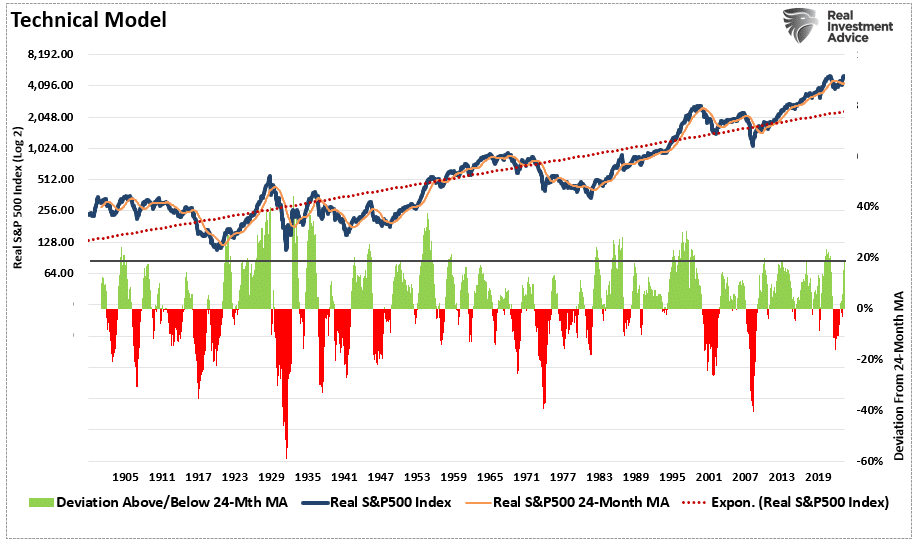

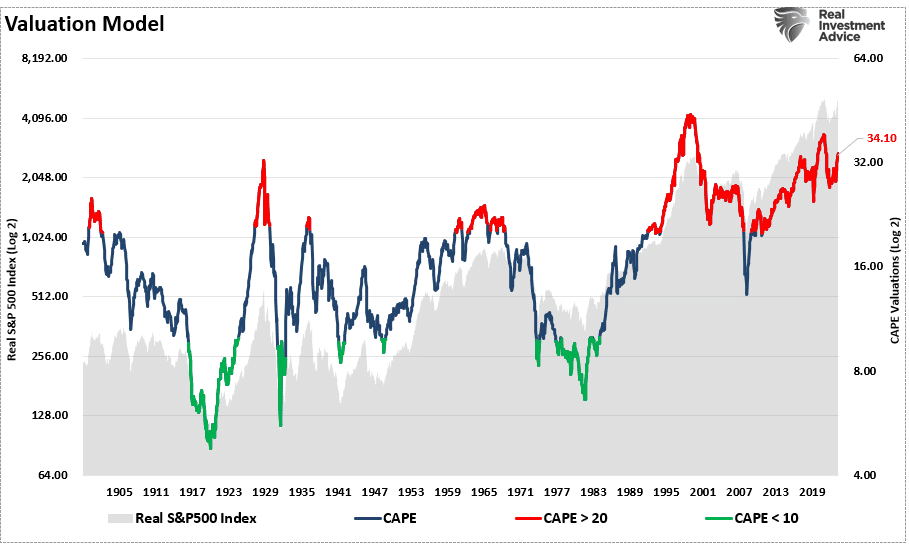

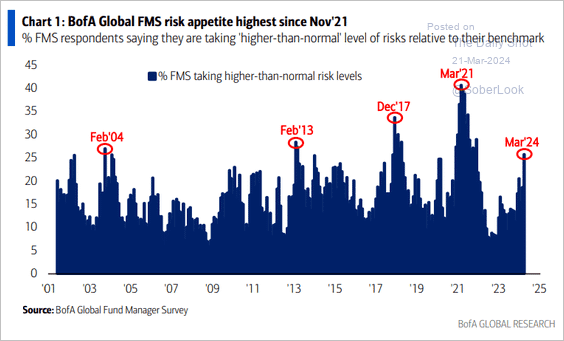

Technical Measures And Valuations. Does Any Of It Matter?

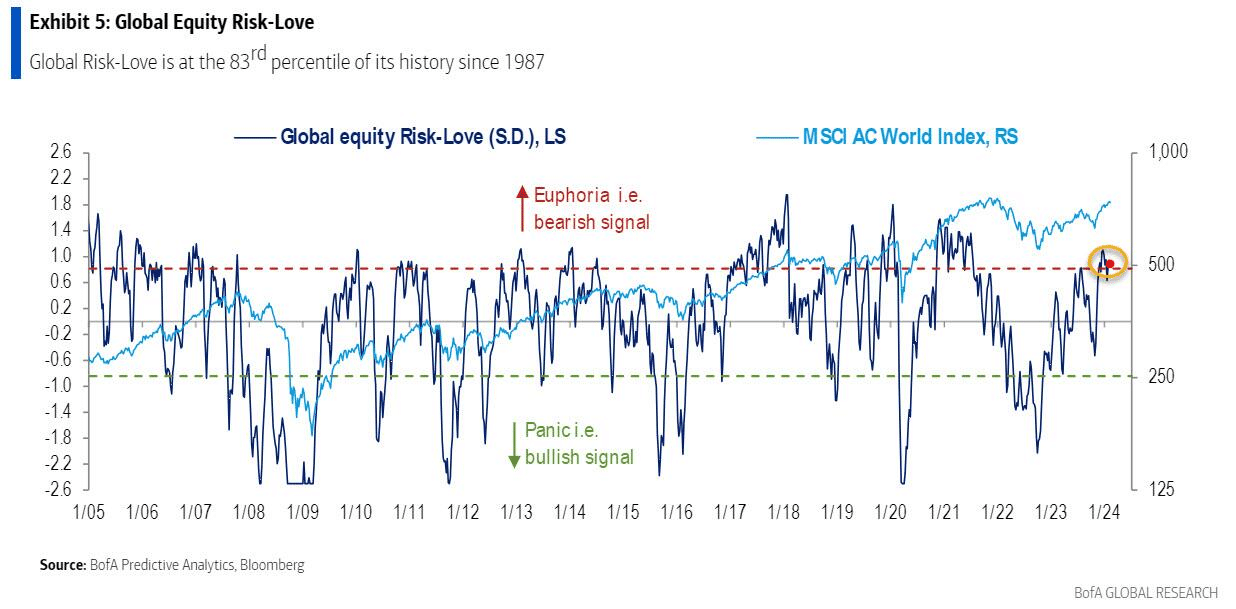

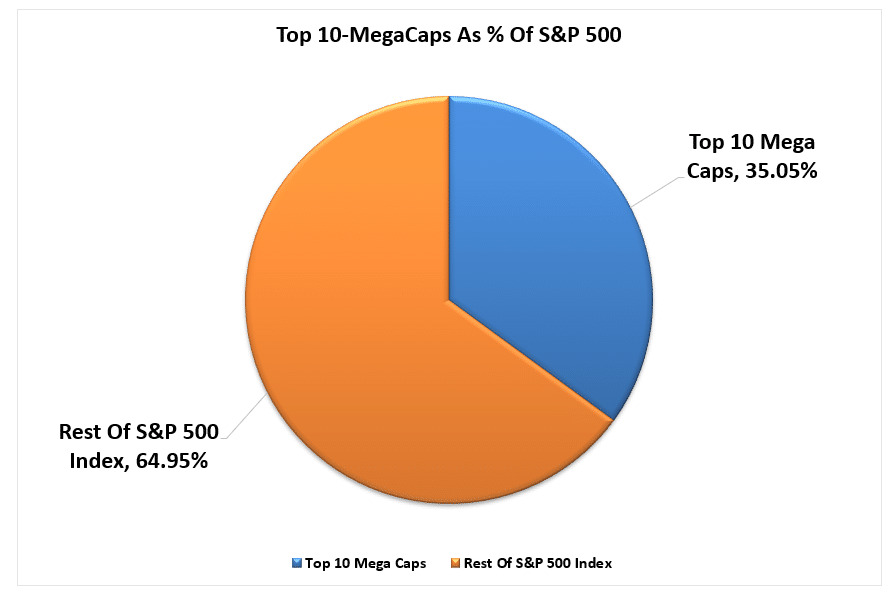

Technical measures and valuations all suggest the market is expensive, overbought, and exuberant. However, none of it seems to matter as investors pile into equities to chase risk assets higher. A recent BofA report shows that the increase in risk appetite has been the largest since March 2021.

Of course, as prices increase faster than underlying earnings growth, valuations also increase. However, as discussed in “Valuations Suggest Caution,” valuations are a better measure of psychology in the short term. To wit:

“Valuation metrics are just that – a measure of current valuation. More importantly, when valuation metrics are excessive, it is a better measure of ‘investor psychology’ and the manifestation of the ‘greater fool theory.’ As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations.”

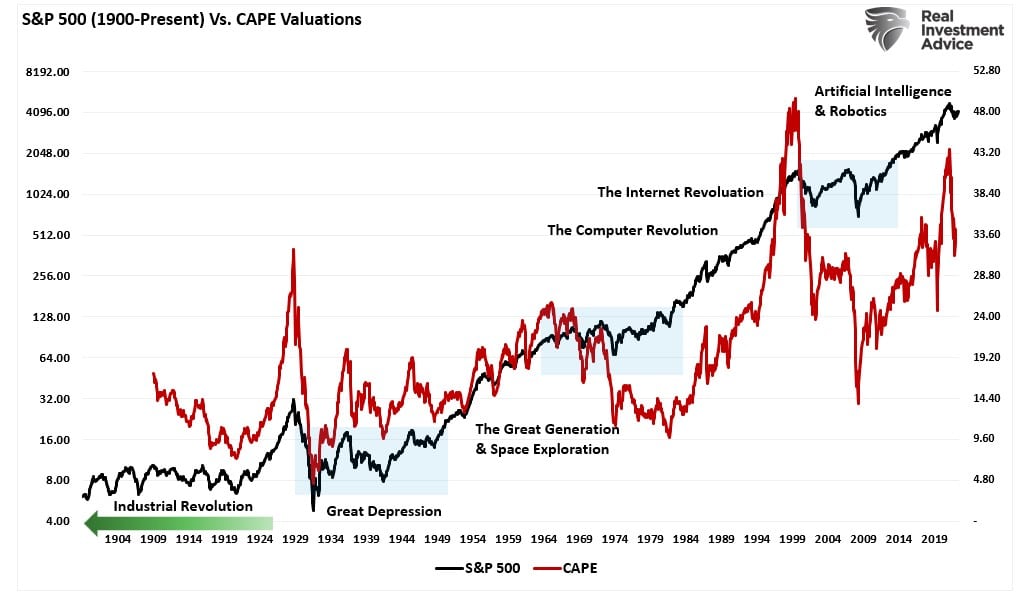

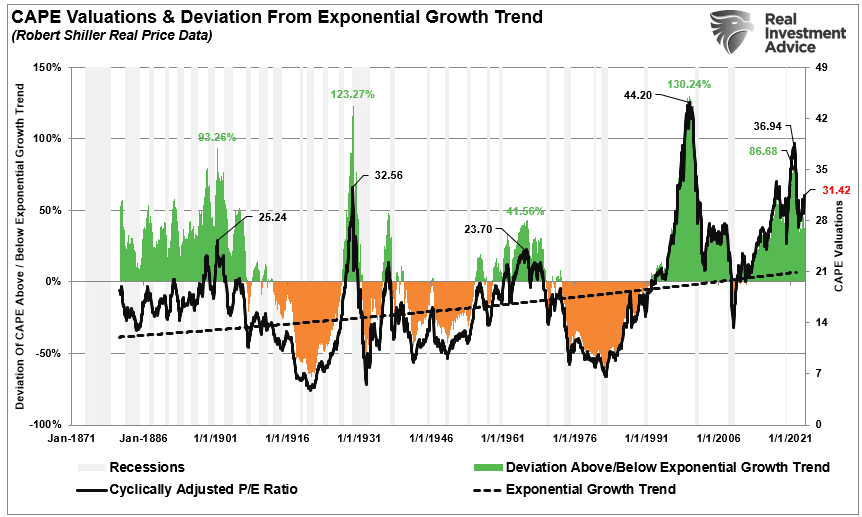

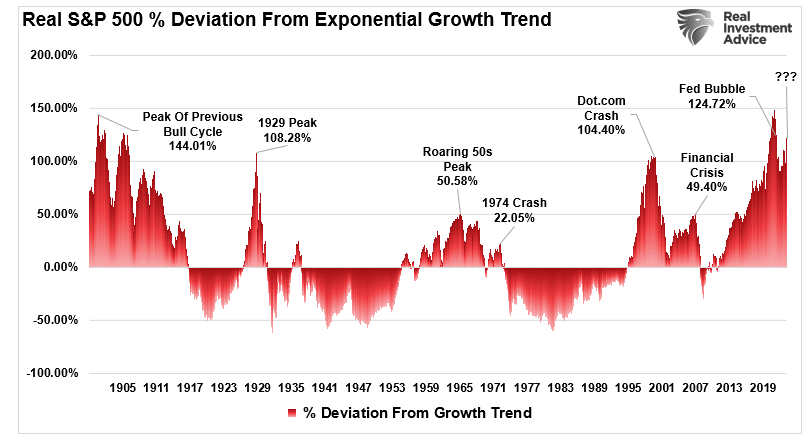

When investors are exuberant and willing to overpay for future earnings growth, valuations increase. The increase in valuations, also known as “multiple expansion,” is a crucial support for bull markets. As shown, the increase in multiples coincides with rising markets. Of course, the opposite, known as “multiple contractions,” is also true. With a current Shiller CAPE valuation multiple of 34x earnings, such suggests that investor confidence is elevated.

As noted, valuations are terrible market timing indicators and should not be used for such. While valuations provide the basis for calculating future returns, technical measures are more critical for managing near-term portfolio risk.

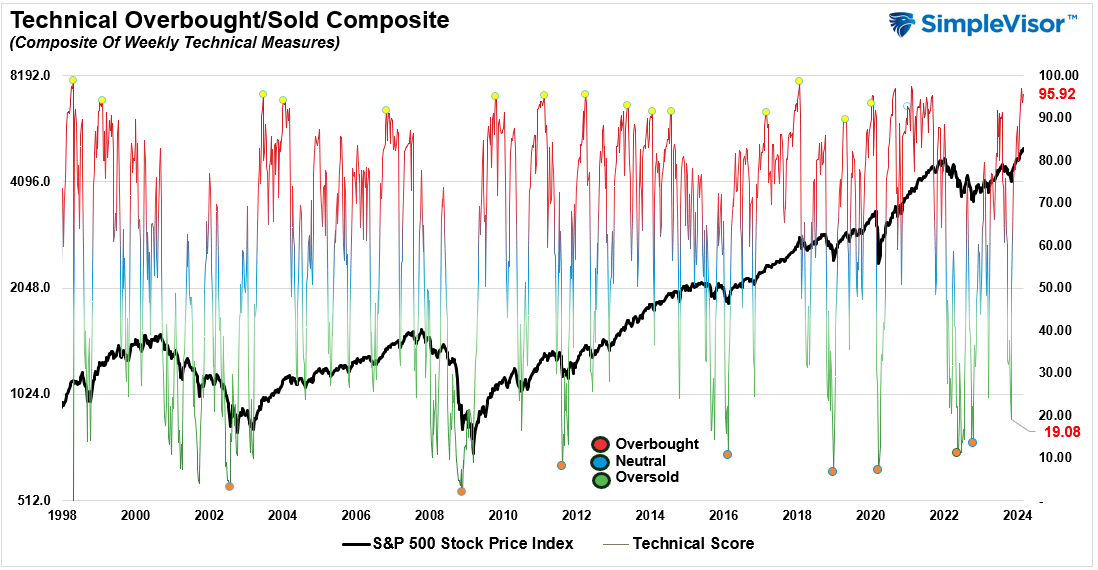

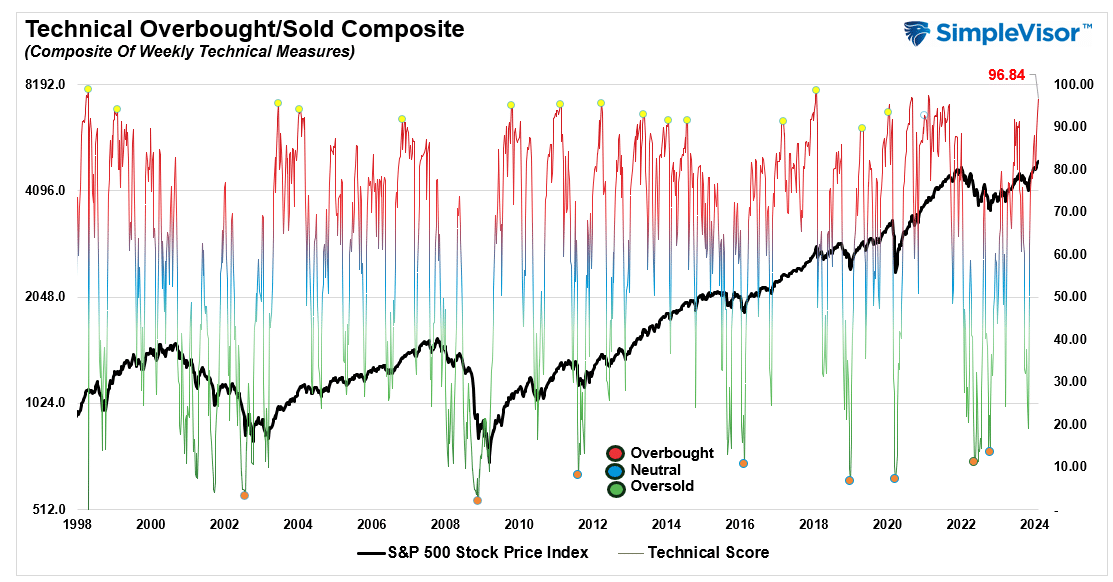

Technical Measures Are Getting Extreme

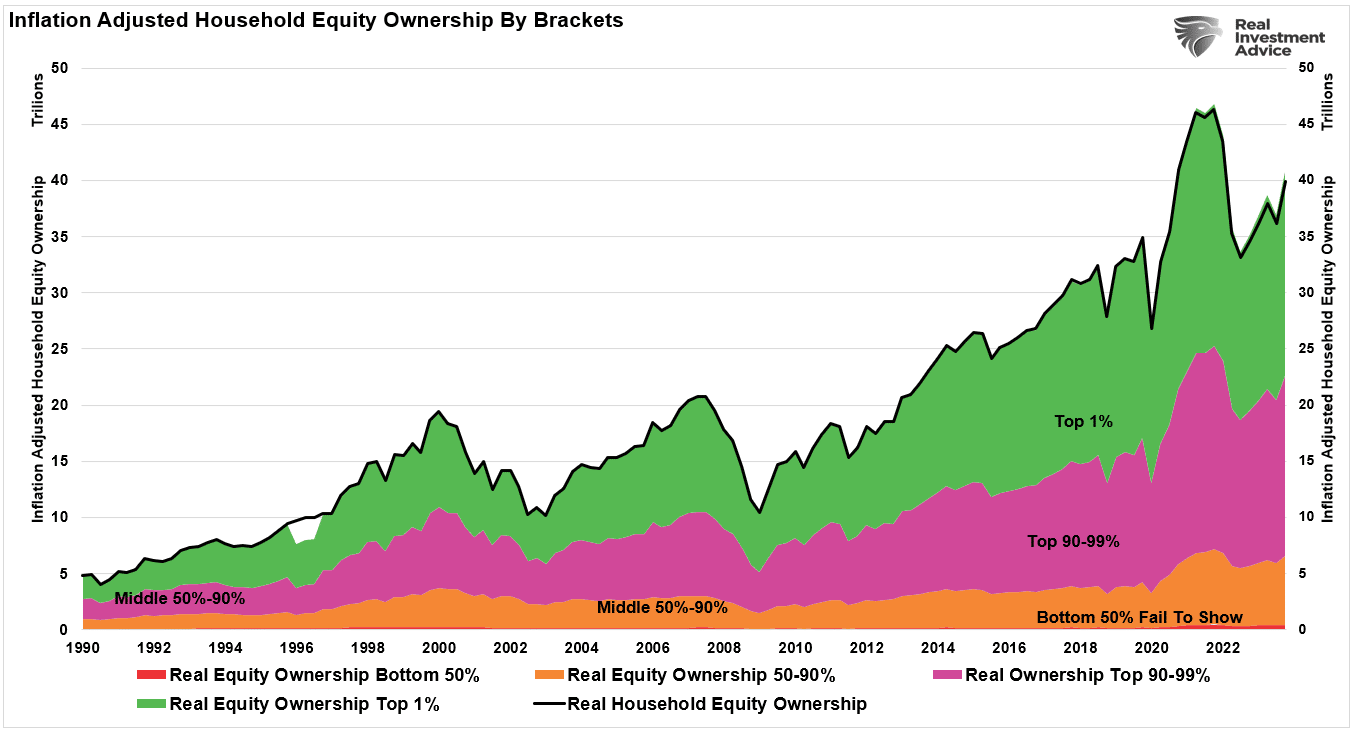

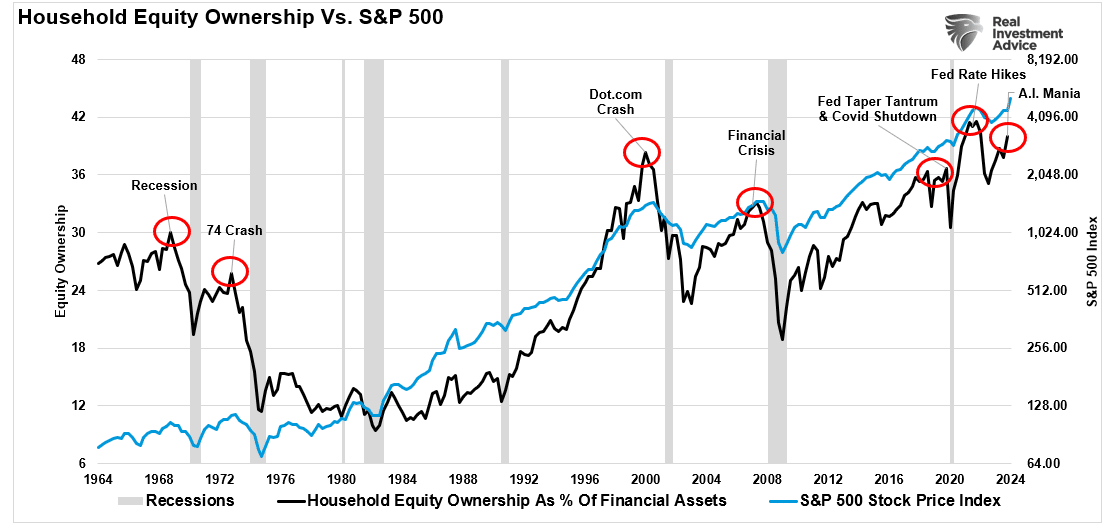

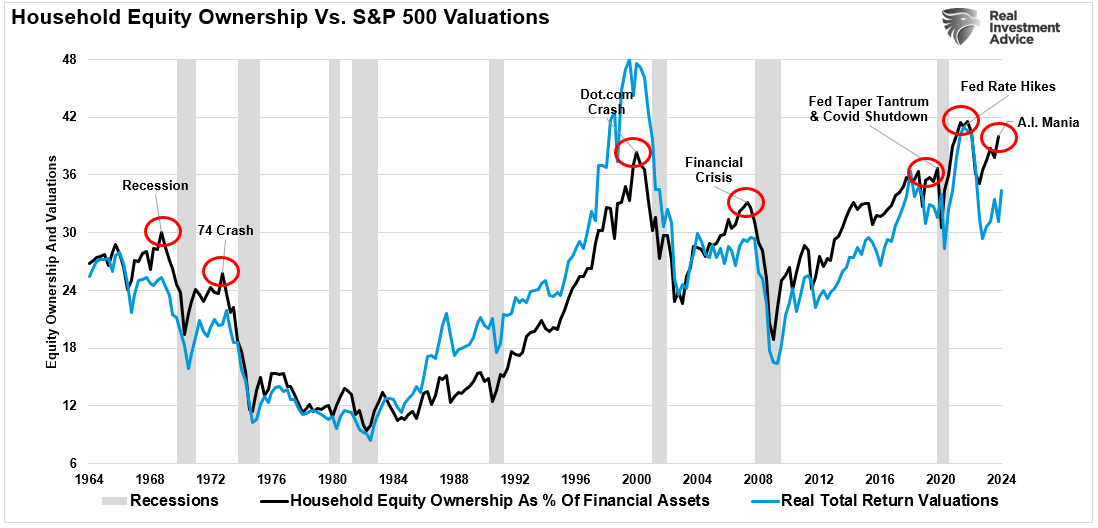

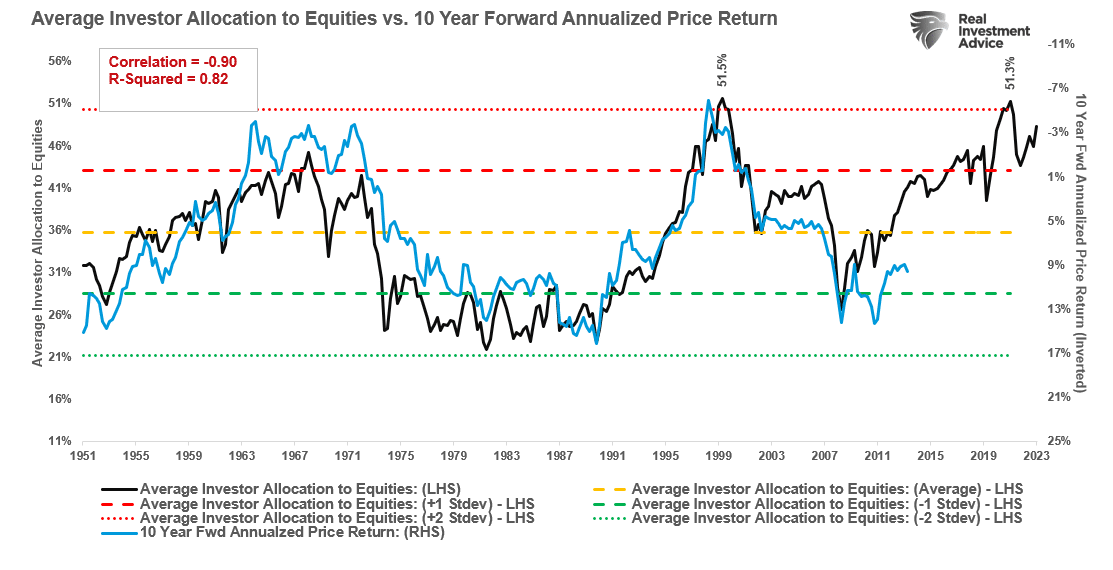

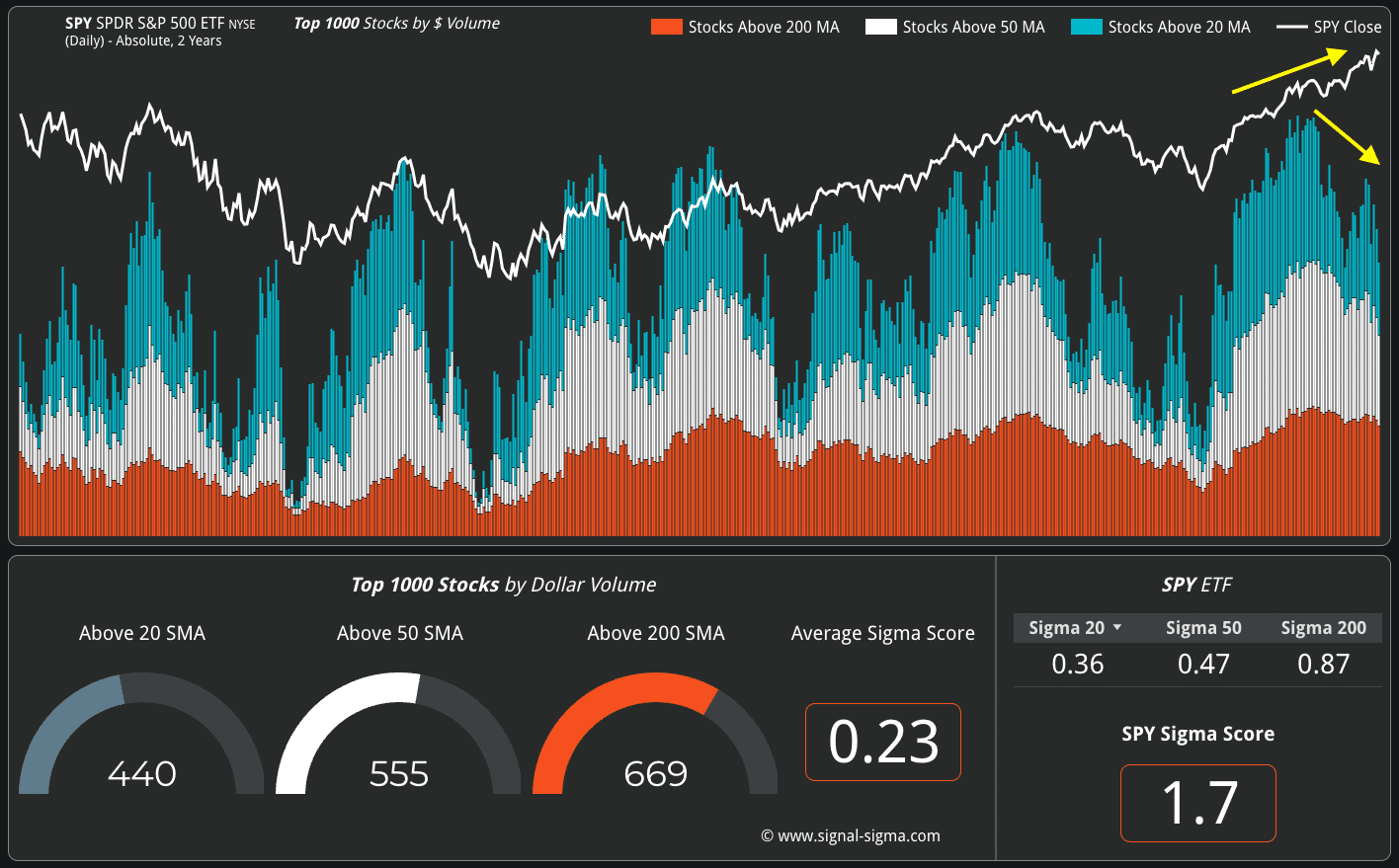

As noted, investors are again becoming exuberant over stock ownership. Such is vital to creating multiple expansions and fueling bull market advances. High valuations, bullish sentiment, and leverage are meaningless if the underlying equities are not owned. As discussed in “Household Equity Allocations,” the current levels of household equity ownership have reverted to near-record levels. Historically, such exuberance has been the mark of more important market cycle peaks.

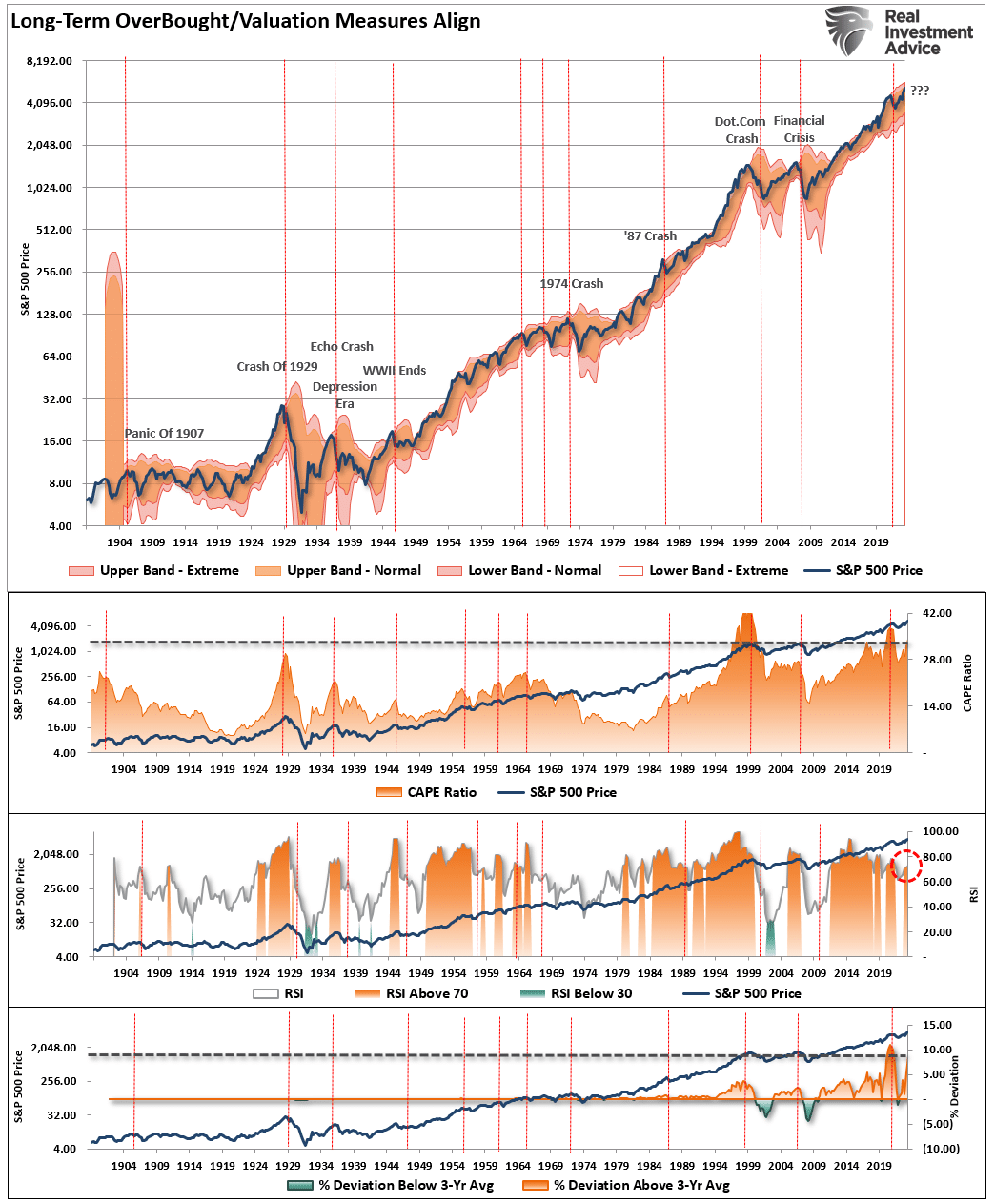

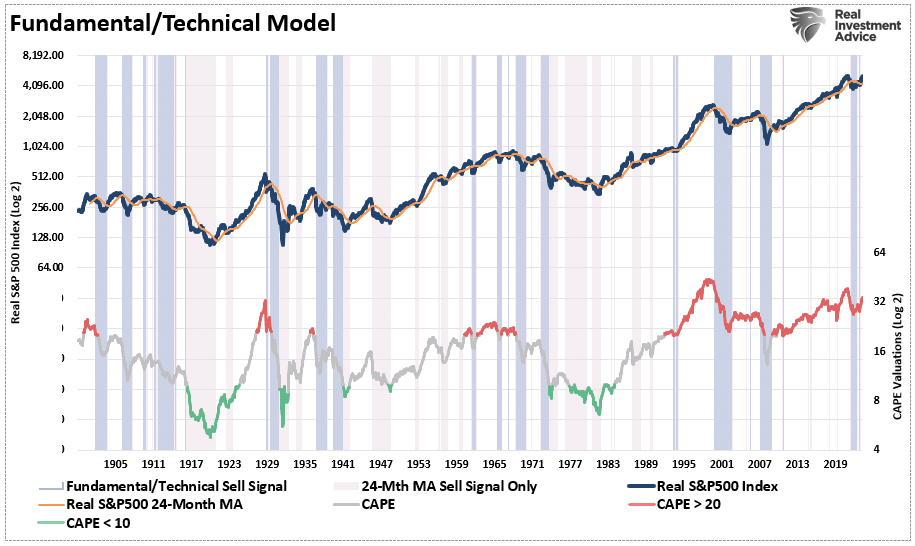

While household equity ownership is critical to expanding the bull market, the technical measures provide an understanding of when excesses are reached. One measure we focus on is the deviation of price from long-term means. The reason is that markets are bound to long-term means over time. For a “mean” or “average” to exist, prices must trade above and below that price over time. Therefore, we can determine when deviations are approaching more extreme levels by viewing past deviations. Currently, the deviation of the market from its underlying 2-year average is one of the largest in history. Notably, there have certainly been more significant deviations in the past, suggesting the current deviation from the mean can grow further. However, such deviations have crucially been a precursor to an eventual mean-reverting event.

The following analysis uses quarter data and evaluates the market using valuation and technical measures. From a long-term perspective, the market is trading at more extreme levels. The quarterly Relative Strength (RSI) measure is above 70, the deviation is close to a historical record, and the market trades nearly 3 standard deviations above its quarterly mean. As noted, while these valuation and technical measures can undoubtedly become more extreme, the ingredients for an eventual mean reverting event are present.

Of course, the inherent problem with long-term analysis is that while valuations and long-term technical measures are more extreme, they can remain that way for much longer than logic suggests. However, we can construct a valuation and technical measures model using the data above. As shown, the model triggered a “risk off” warning in early 2022 when high valuations collided with an extreme deviation of the market above the 24-month moving average. That signal was reversed in January 2023, as the market began to recover. While a new signal has not yet been triggered, the ingredients of valuations and deviations are present.

The Ingredients Are Missing A Catalyst

The problem with long-term technical measures and valuations is that they move slowly. Therefore, the general assumption is that if high valuations do not lead to an immediate market correction, the measure is flawed.

In the short term, “valuations” have little relevance to what positions you should buy or sell. It is only momentum, the direction of the price, that matters. Managing money, either “professionally” or “individually,” is a complicated process over the long term. It seems exceedingly easy in the short term, particularly amid a speculative mania. However, as with every bull market, a strongly advancing market forgives investors’ many investing mistakes. The ensuing bear market reveals them in the most brutal and unforgiving of outcomes.

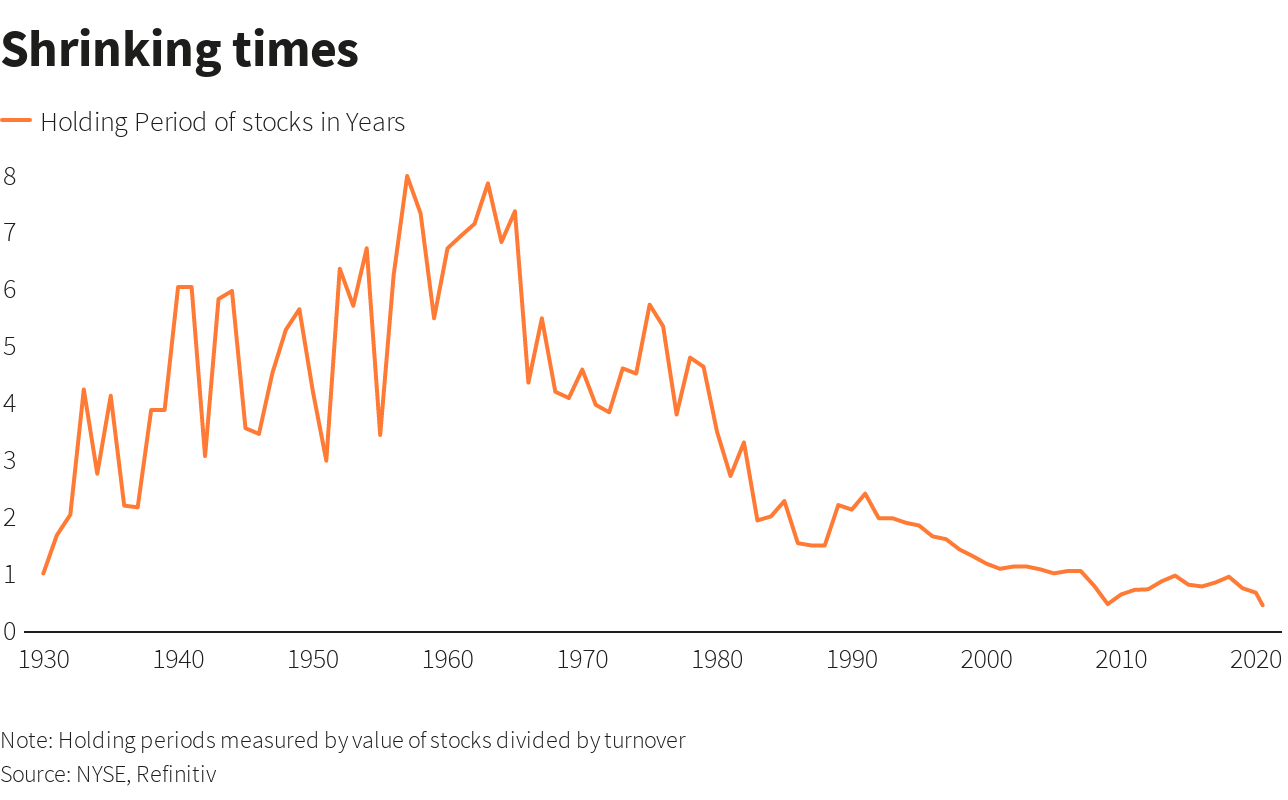

There is a clear advantage to providing risk managementto portfolios over time. The problem is that most individuals cannot manage their own money because of “short-termism.” As shown by shrinking holding periods.

While “short-termism” currently dominates the investor mindset, the ingredients for a reversion exist. However, that does not mean one will happen tomorrow, next month, or even this year.

Think about it this way. If I gave you a bunch of ingredients such as nitrogen, glycerol, sand, and shell, you would probably stick them in the garbage and think nothing of it. They are innocuous ingredients and pose little real danger by themselves. However, you make dynamite using a process to combine and bind them. However, even dynamite is safe as long as it is stored properly. Only when dynamite comes into contact with the appropriate catalyst does it become a problem.

“Mean reverting events,” bear markets, and financial crises result from a combined set of ingredients to which a catalyst ignites. Looking back through history, we find similar elements every time.

Like dynamite, the individual ingredients are relatively harmless but dangerous when combined.

Importantly, this particular formula remains supportive of higher asset prices in the short term. Of course, the more prices rise, the more optimistic investors become.

While the combination of ingredients is dangerous, they remain “inert” until exposed to the right catalyst.

What causes the next “liquidation cycle” is currently unknown. It is always an unexpected, exogenous event that triggers a “rush for the exits.”

Many believe that “bear markets” are now a relic of the past, given the massive support provided by Central Banks. Maybe that is the case. However, remembering that such beliefs were always present before more severe mean-reverting events is worth remembering.

To quote Irving Fisher in 1929, “Stocks are at a permanently high plateau.”

Retirement Crisis Faces Government And Corporate Pensions

It is long past the time that we face the fact that “Social Security” is facing a retirement crisis. In June 2022, we touched on this issue, discussing the stark realities confronting Social Security.

“The program’s payouts have exceeded revenue since 2010, but the recent past is nowhere near as grim as the future. According to the latest annual report by Social Security’s trustees, the gap between promised benefits and future payroll tax revenue has reached a staggering $59.8 trillion. That gap is $6.8 trillion larger than it was just one year earlier. The biggest driver of that move wasn’t Covid-19, but rather a lowering of expected fertility over the coming decades.” – Stark Realities

Note the last sentence.

When President Roosevelt first enacted social security in 1935, the intention was to serve as a safety net for older adults. However, at that time, life expectancy was roughly 60 years. Therefore, the expectation was that participants would not be drawing on social security for very long on an actuarial basis. Furthermore, according to the Social Security Administration, roughly 42 workers contributed to the funding pool for each welfare recipient in 1940.

Of course, given that politicians like to use government coffers to buy votes, additional amendments were added to Social Security to expand participation in the program. This included adding domestic labor in 1950 and widows and orphans in 1956. They lowered the retirement age to 62 in 1961 and increased benefits in 1972. Then politicians added more beneficiaries, from disabled people to immigrants, farmers, railroad workers, firefighters, ministers, federal, state, and local government employees, etc.

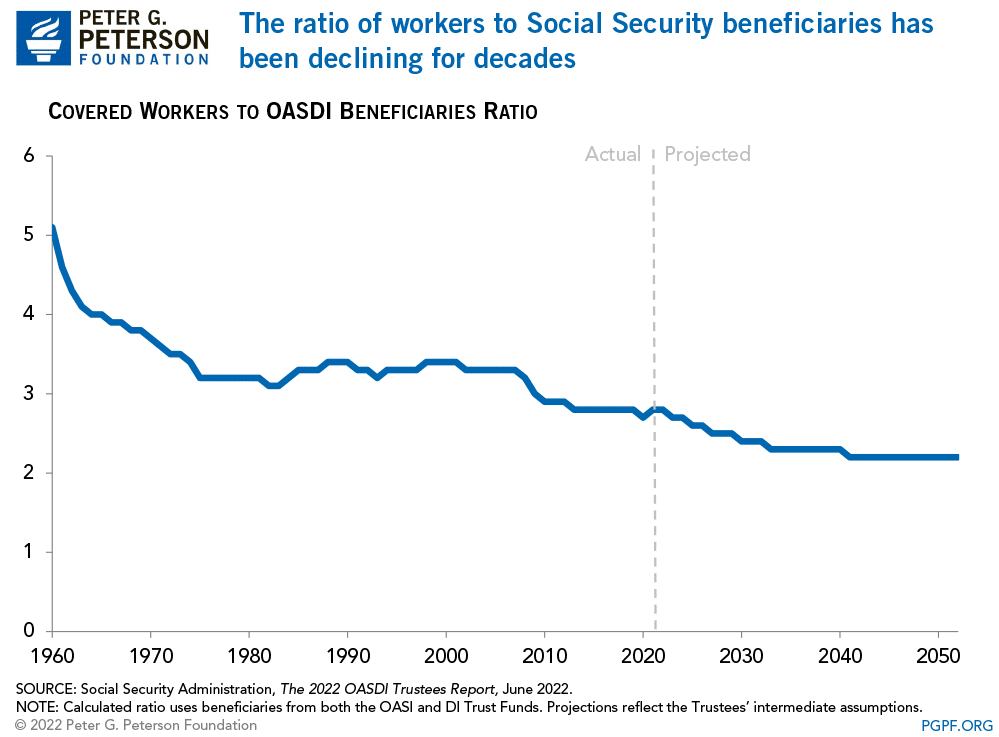

While politicians and voters continued adding more beneficiaries to the welfare program, workers steadily declined. Today, there are barely 2-workers for each beneficiary. As noted by the Peter G. Peterson Foundation:

“Social Security has been a cornerstone of economic security for almost 90 years, but the program is on unsound footing. Social Security’s combined trust funds are projected to be depleted by 2035 — just 13 years from now. A major contributor to the unsustainability of the current Social Security program is that the number of workers contributing to the program is growing more slowly than the number of beneficiaries receiving monthly payments. In 1960, there were 5.1 workers per beneficiary; that ratio has dropped to 2.8 today.”

As we will discuss, the collision of demographics and math is coming to the welfare system.

A Massive Shortfall

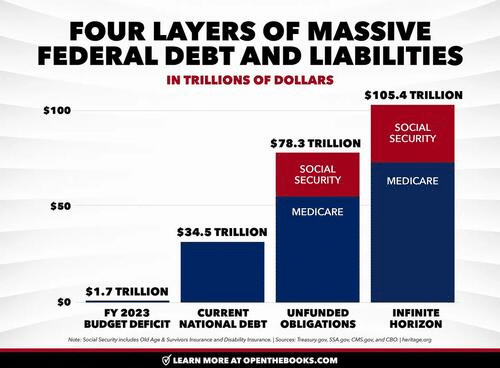

The new Financial Report of the United States Government (February 2024) estimates that the financial position of Social Security and Medicare are underfunded by roughly $175 Trillion. Treasury Secretary Janet Yellin signed the report, but the chart below details the problem.

The obvious problem is that the welfare system’s liabilities massively outweigh taxpayers’ ability to fund it. To put this into context, as of Q4-2023, the GDP of the United States was just $22.6 trillion. In that same period, total federal revenues were roughly $4.8 trillion. In other words, if we applied 100% of all federal revenues to Social Security and Medicare, it would take 36.5 years to fill the gap. Of course, that is assuming that nothing changes.

However, therein lies the actuarial problem.

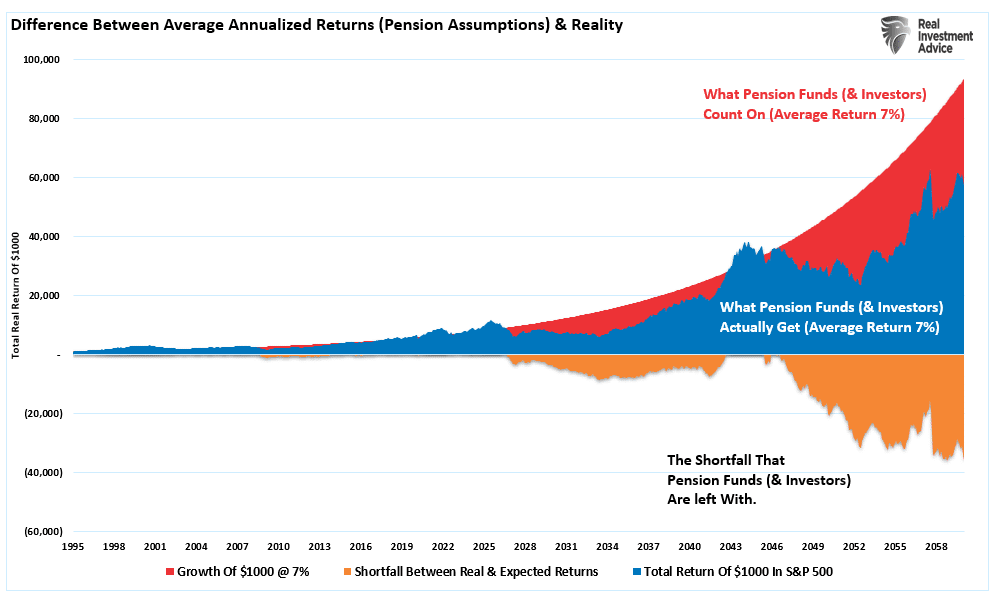

All pension plans, whether corporate or governmental, rely on certain assumptions to plan for future obligations. Corporate pensions, for example, rely on certain portfolio return assumptions to fund planned employee retirements. Most pension plans assume that portfolios will return 7% a year. However, a vast difference exists between “average returns” and “compound returns” as shown.

Social Security, Medicare, and corporate pension plans face a retirement crisis. A shortfall arises if contributions and returns don’t meet expectations or demand increases on the plans.

For example, given real-world return assumptions, pension funds SHOULD lower their return estimates to roughly 3-4% to potentially meet future obligations and maintain some solvency. However, they can’t make such reforms because “plan participants” won’t let them. Why? Because:

It would require a 30-40% increase in contributionsby plan participants they can not afford.

Given many plan participants will retire LONG before 2060, there isn’t enough time to solve the issues and;

Any bear market will further impede the pension plan’s ability to meet future obligations without cutting future benefits.

Social Security and Medicare face the same intractable problem. While there is ample warning from the Trustees that there are funding shortfalls to the plans, politicians refuse to make the needed changes and instead keep adding more participants to the rolls.

However, all current actuarial forecasts depend on a steady and predictable pace of age and retirement. But that is not what is currently happening.

A Retirement Crisis In The Making

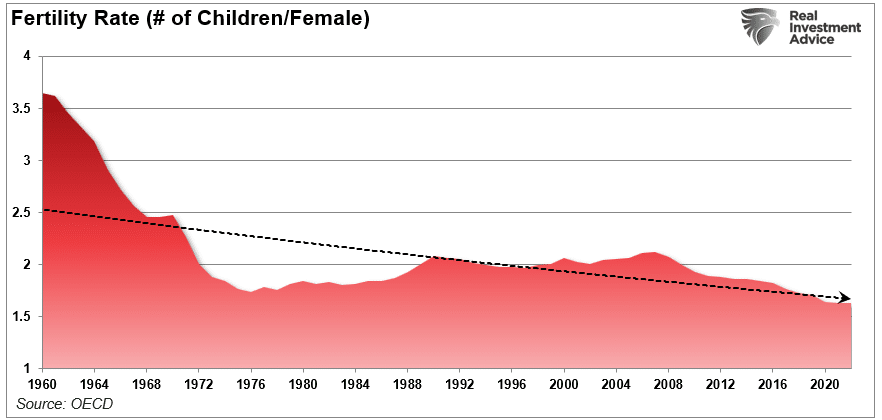

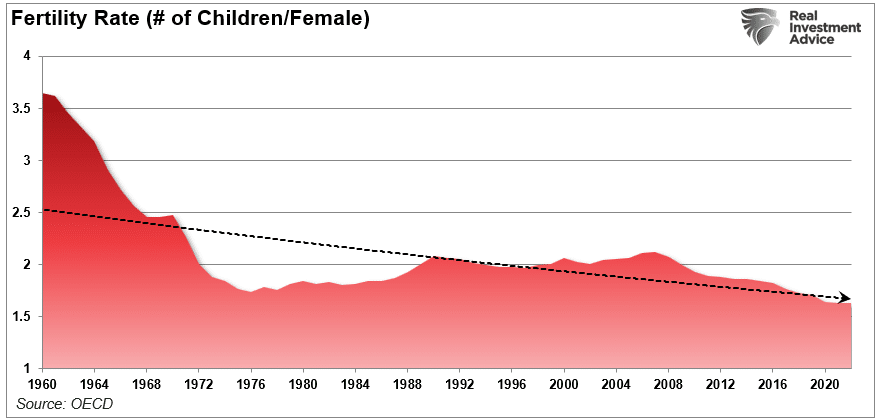

The single biggest threat that faces all pension plans is demographics. That single issue can not be fixed as it takes roughly 25 years to grow a taxpayer. So, even if we passed laws today that required all women of birthing age to have a minimum of 4 children over the next 5 years, we would not see any impact for nearly 30 years. However, the problem is running in reverse as fertility rates continue to decline.

Interestingly, researchers from the Center For Sexual Health at Indiana University put forth some hypotheses behind the decline in sexual activity:

Less alcohol consumption (not spending time in bars/restaurants)

More time on social media and playing video games

Lower wages lead to lower rates of romantic relationships

Non-heterosexual identities

The apparent problem with less sex and non-heterosexual identities is fewer births.

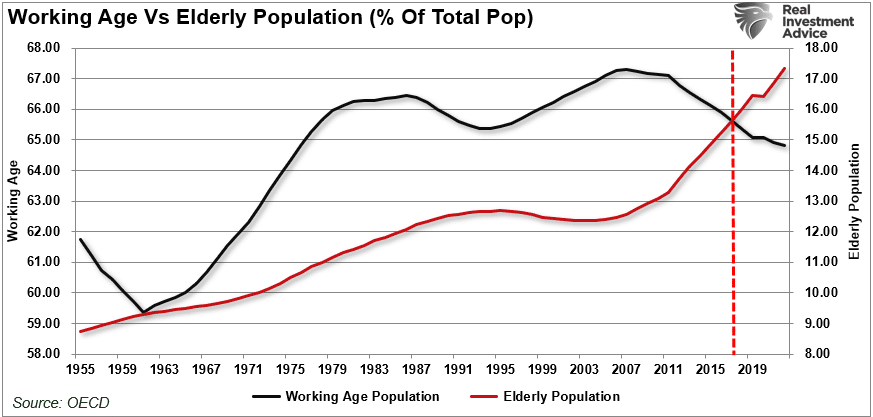

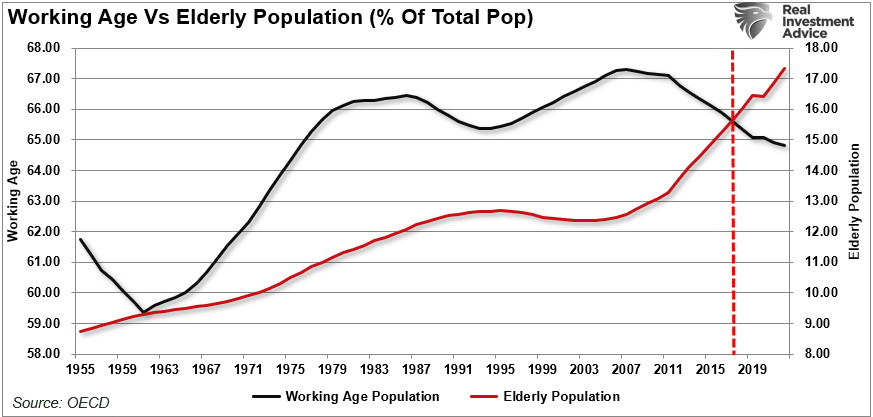

No matter how you calculate the numbers, the problem remains the same. Too many obligations and a demographic crisis. As noted by official OECD estimates, the aging of the population relative to the working-age population has already crossed the “point of no return.”

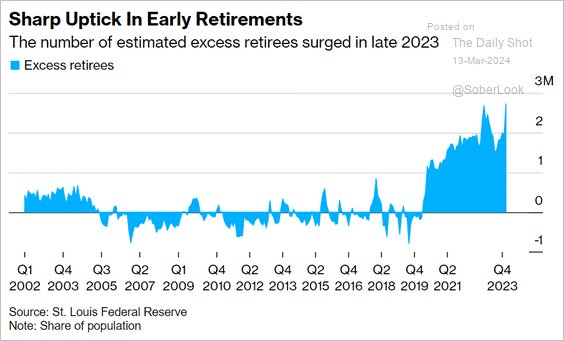

To compound that situation, there has been a surge in retirees significantly higher than estimates. As noted above, actuarial tables depend on an expected rate of retirees drawing from the system. If that number exceeds those estimates, a funding shortfall increases to provide the required benefits.

The decline in economic prosperity discussed previously is caused by excessive debt and declining income growth due to productivity increases. Furthermore, the shift from manufacturing to a service-based society will continue to lead to reduced taxable incomes.

This employment problem is critical.

By 2025, each married couple will pay Social Security retirement benefits for one retiree and their own family’s expenses. Therefore, taxes must rise, and other government services must be cut.

Back in 1966, each employee shouldered $555 of social benefits. Today, each employee has to support more than $18,000 in benefits. The trend is unsustainable unless wages or employment increases dramatically, and based on current trends, such seems unlikely.

The entire social support framework faces an inevitable conclusion where wishful thinking will not change that outcome. The question is whether elected leaders will make needed changes now or later when they are forced upon us.

For now, we continue to “Whistle past the graveyard” of a retirement crisis.

Blackout Of Buybacks Threatens Bullish Run