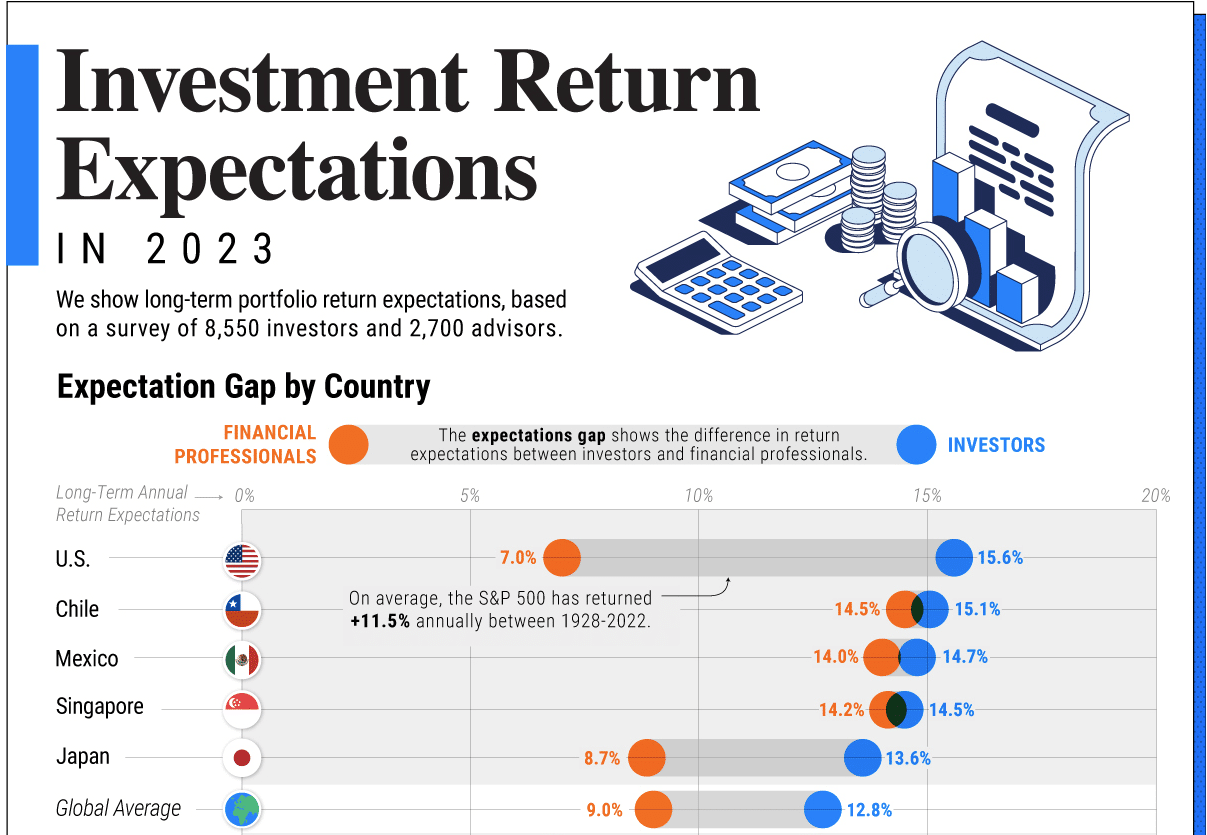

A stunning post from VisualCapitalist showed a poll of 8550 investors and 2700 advisors and the gap between the two of future portfolio return expectations. The poll was global; however, I will focus on this post’s domestic portfolio return expectations.

Note the gap between investors’ and advisors’ portfolio return expectations in the U.S. is the widest of any country. However, as we will discuss, that gap is unsurprising given the outsized returns relative to long-term historical portfolio returns since the “Financial Crisis.”

However, here is the most apparent problem with which advisors are more correctly aligned. It is a true statement that over the very long term, stocks have returned roughly 6% from capital appreciation and 4% from dividends on a nominal basis. However, since inflation has averaged approximately 2.3% over the same period, real returns are closer to 8% annually.

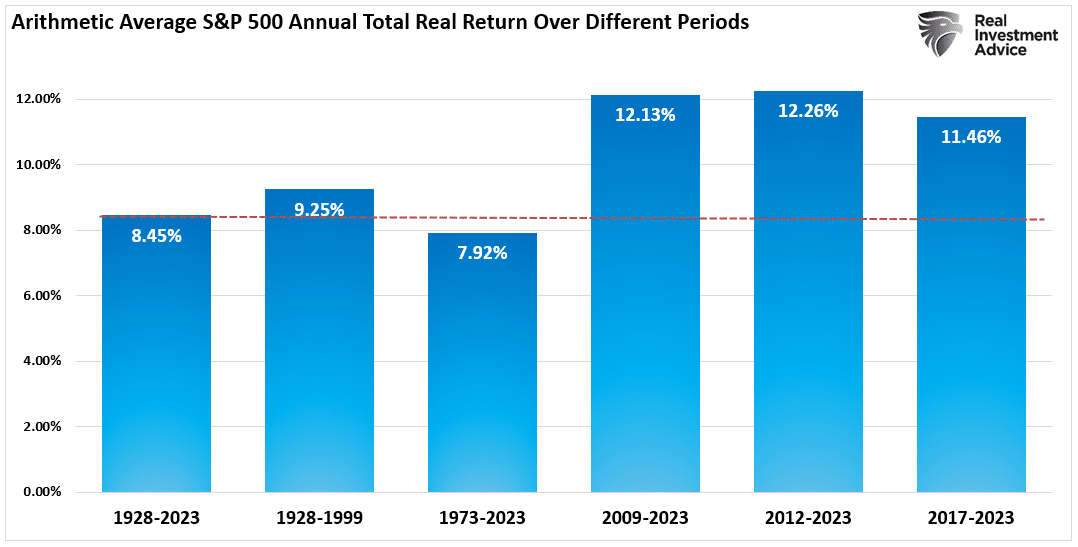

That is shown with the red dashed line in the chart below. The chart shows the average annual inflation-adjusted total returns (dividends included) since 1928. I used the total return data from Aswath Damodaran, a Stern School of Business professor at New York University. The chart shows that from 1928 to 2023, the market returned 8.45% after inflation. However, after the financial crisis in 2008, returns jumped by nearly four percentage points for the various periods.

After over a decade, many investors have become complacent in expecting elevated portfolio returns from the financial markets. However, can those expectations continue to be met in the future?

Can Future Portfolio Returns Replicate The Past

We must understand what drove those returns to gauge whether future portfolio return rates can replicate the past.

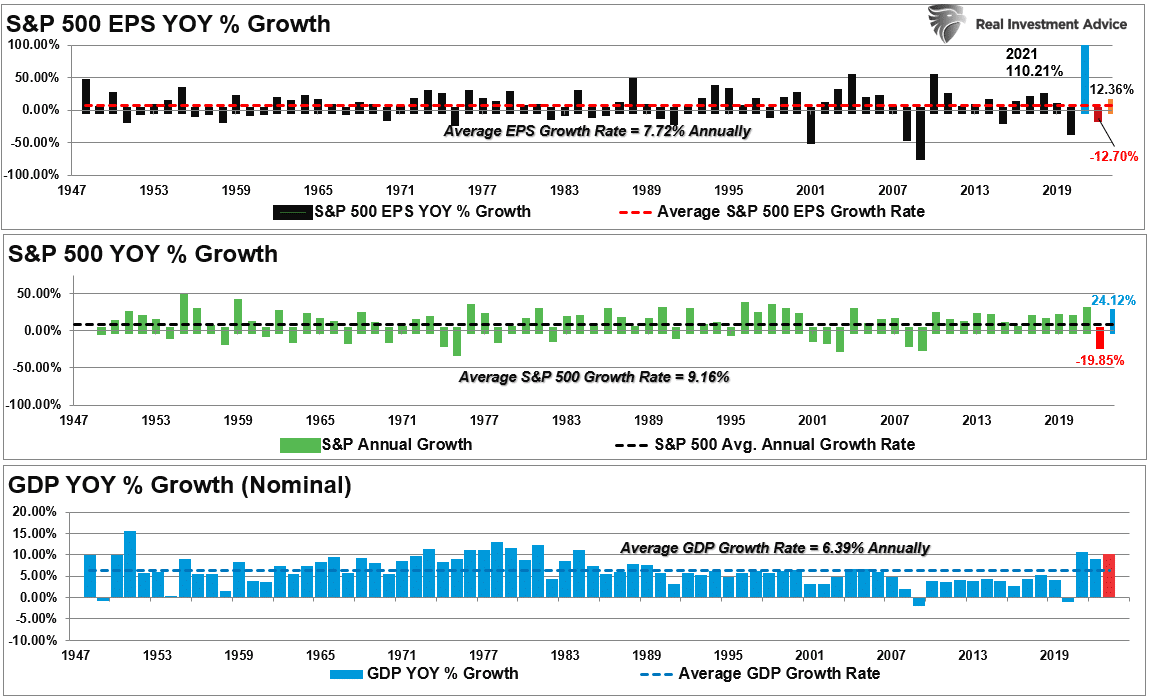

Over the long term, there is an apparent relationship between the stock market and the economy. Such is because it is economic activity that creates corporate revenues and earnings. As such, stocks can not indefinitely grow faster than the economy over long periods. When stocks deviate from the underlying economy, the eventual resolution is lower stock prices. Over time, there is a close relationship between the economy, earnings, and asset prices. For example, the chart below compares the three from 1947 through 2023.

Since 1947, earnings per share have grown at 7.72%, while the economy has expanded by 6.39% annually. That close relationship in growth rates is logical, given the significant role that consumer spending has in the GDP equation.

The slight difference is due to periods where earnings can grow faster than the economy when coming out of recession. However, while nominal stock prices have averaged 9.16%, reversions to actual economic growth eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports.

So, if the economic and earnings relationship is true, what explains the market disconnect from underlying economic activity over the last decade? In other words, what was the driver of portfolio returns over the last decade, if all else is equal? Two differences in the previous 13 years didn’t exist before 2008.

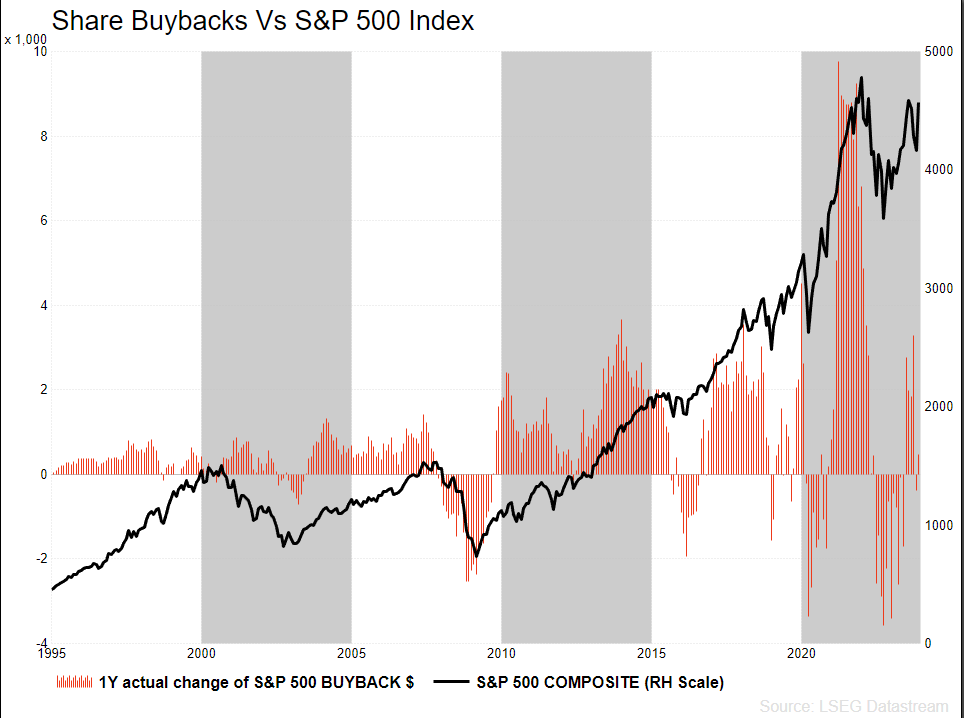

The first is corporate stock buybacks. While corporate share repurchases are not new, the egregious use of buybacks to boost earnings per share accelerated post-2008. As discussed previously:

“In a previous Wall Street Journal study, 93% of the respondents point to “influence on stock price” and “outside pressure” as reasons for manipulating earnings figures. Such is why stock buybacks have continued to rise in recent years. Following the “pandemic shutdown,” they skyrocketed.”

As discussed in that article, since 2008, share buybacks have accounted for nearly 40% of the market’s return/

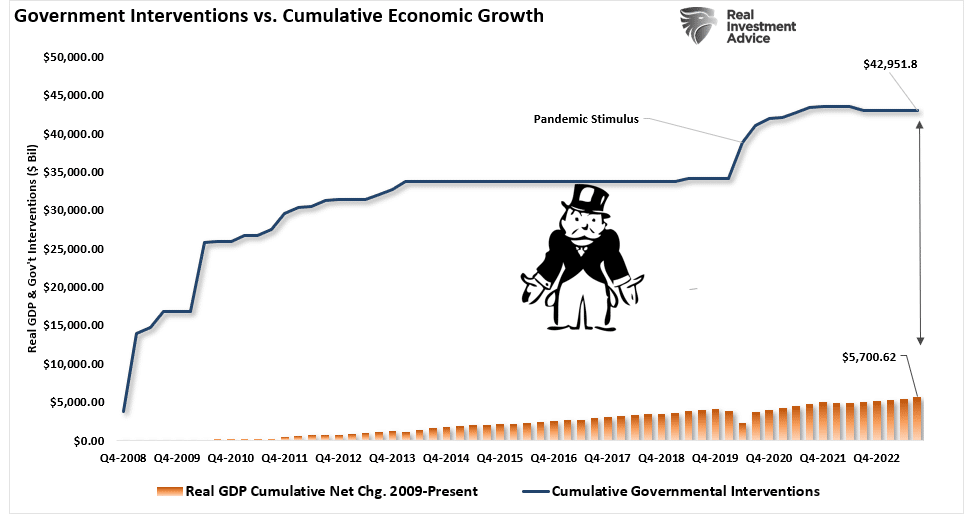

The second is monetary and fiscal interventions, unprecedented since the financial crisis.

As discussed in “The Markets Are Frontrunning The Fed.” the psychological change is a function of more than a decade of fiscal and monetary interventions that have separated the financial markets from economic fundamentals. Since 2007, the Federal Reserve and the Government have continuously injected roughly $43 Trillion in liquidity into the financial system and the economy to support growth.

That support entered the financial system, lifting asset prices and boosting consumer confidence to support economic growth.

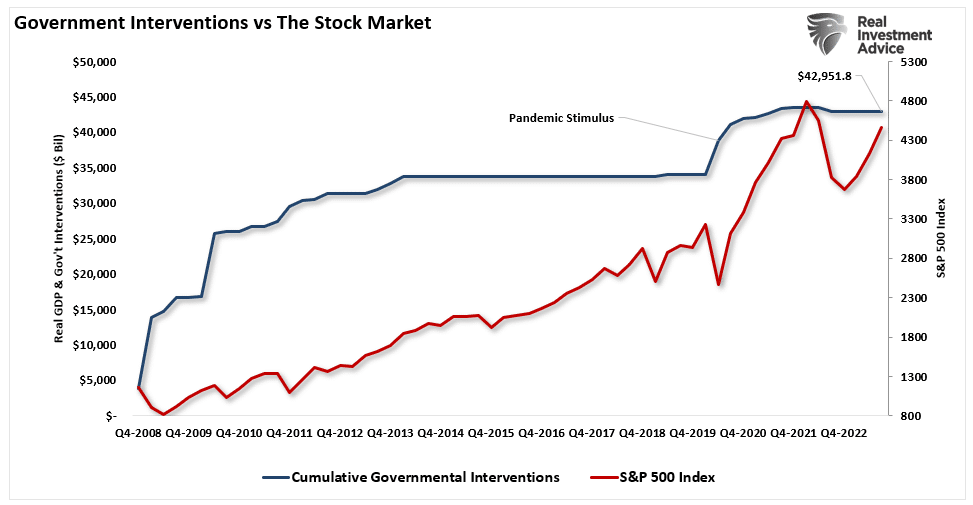

The high correlation between these interventions and the financial markets is evident. The only outlier was the period during the Financial Crisis as the Fed launched the first round of Quantitative Easing or Q.E. What followed was multiple Government bailouts, support for the housing and financial markets, zero interest rates, and eventually direct checks to households in 2020.

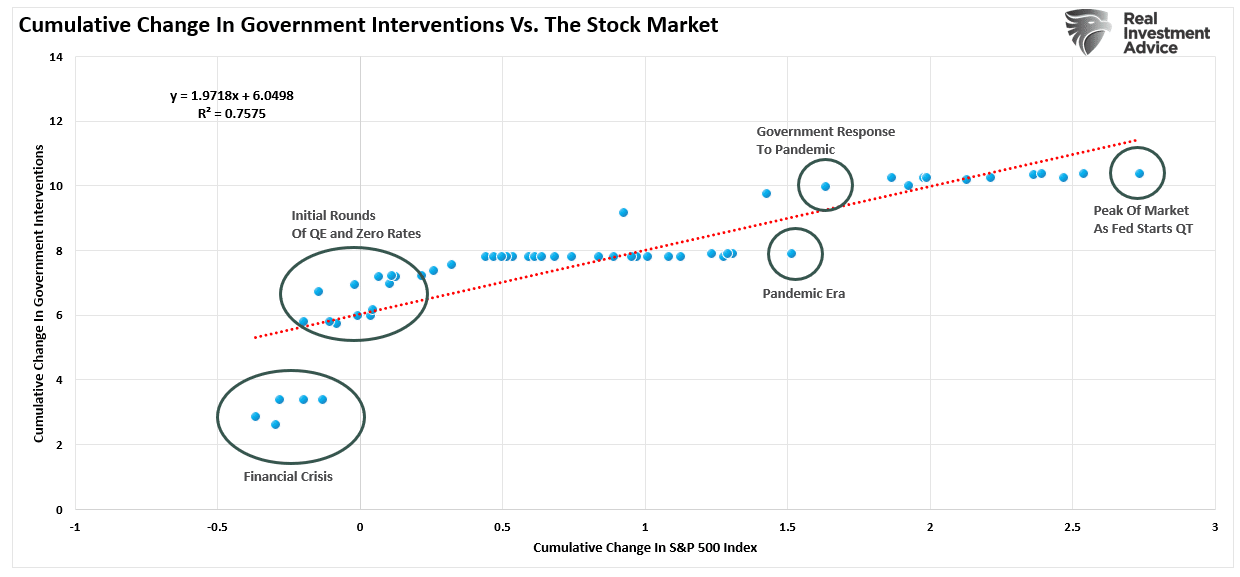

Given the repeated history of financial interventions over the last 13 years, it is unsurprising that investors now expect outsized portfolio returns in the future.

The only problem with that assumption is the ability of the Government and the Federal Reserve to repeat the massive monetary interventions seen since the Financial Crisis.

The Decade Will Likely Be Very Different Than The Last

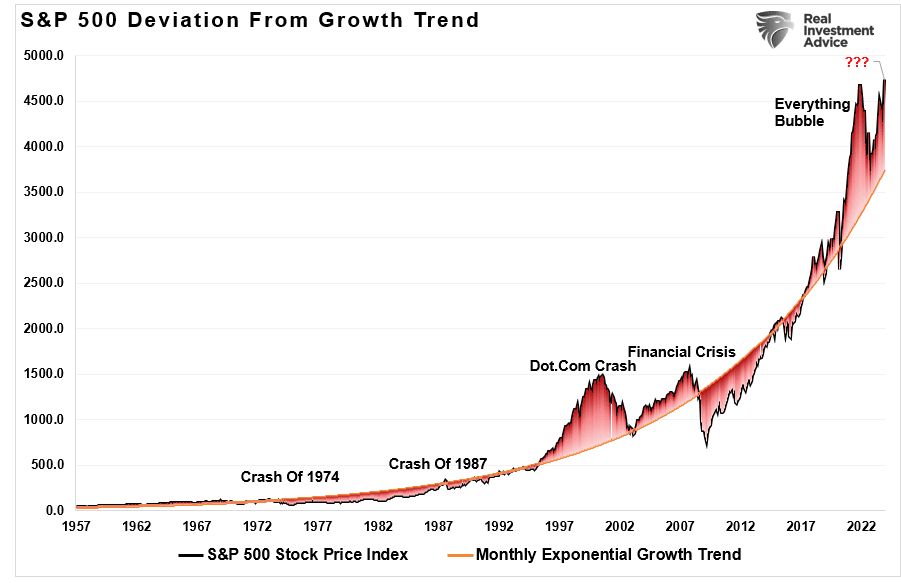

During the last decade, those fiscal and monetary inputs fostered history’s most significant asset bubble. In 2020, the pandemic started the needed reversal of those excesses but was cut short by massive monetary and fiscal interventions. The current deviation of the market from the long-term exponential growth trend is once again pushing record levels.

Unsurprisingly, since economic and revenue growth trailed the explosion in asset prices, valuations also deviated from long-term exponential growth trends.

Over the next decade, the ability to replicate nearly $5 of interventions for each $1 of economic growth seems much less probable. Of course, one must also consider the drag on future returns from the excessive debt accumulated since the financial crisis.

That debt’s sustainability depends on low-interest rates, which can only exist in a low-growth, low-inflation environment. Low inflation and a slow-growth economy do not support excess portfolio return rates.

As Jeremy Grantham noted:

“All 2-sigma equity bubbles in developed countries have broken back to trend. But before they did, a handful went on to become superbubbles of 3-sigma or greater: in the U.S. in 1929 and 2000 and in Japan in 1989. There were also superbubbles in housing in the U.S. in 2006 and Japan in 1989. All five of these superbubbles corrected all the way back to trend with much greater and longer pain than average.

Today in the U.S. we are in the fourth superbubble of the last hundred years.”

The deviation from long-term growth trends is unsustainable. Repeated financial interventions by the Federal Reserve caused such. Therefore, unless the Federal Reverse is committed to a never-ending program of zero interest rates and quantitative easing, the eventual reversion of returns to their long-term means is inevitable.

Such will result in profit margins and earnings returning to levels that align with actual economic activity.

It is hard to fathom how forward return rates will not be disappointing compared to the last decade. However, those excess returns were the result of a monetary illusion. The consequence of dispelling that illusion will be challenging for investors.

Will this mean investors make NO money over the decade? No. It means that returns will likely be substantially lower than investors have witnessed over the last decade.

But then again, getting average returns may be “feel” very disappointing to many.