Key Takeaways Two weeks ago, after the S&P 500 logged its ninth consecutive weekly gain, we...

Upcoming Event

Beyond Protection: What Life Insurance Can Really Do

Jun 20, 2026 at 8:00 am - 9:00 am

Upcoming Event

Candid Coffee: Narrative Busters

Jul 18, 2026 at 8:00 am - 9:00 am

FILTERS

-

Most Searched Terms

The K-Shaped Economy: Why The Middle Class Moved Up.

A funny thing about bull markets is that investors develop a very short memory about the previous...

The IPO Boom: Where Will The Money Come From?

The media hype surrounding SpaceX’s upcoming mid-June initial public offering (IPO) is...

Equity Supply Surge: What Historically Comes Next

This past week, the market hit an all-time high. At the same time, Alphabet (GOOG) told investors...

Stronger Dollar Trade: The Most Unexpected Macro Bet (Part 2)

Wall Street has piled into the dollar debasement story; however, as is always the case, when...

Quantum Computing: Hype Or The Real Deal?

The word “quantum” is defined as “an amount,” with its Latin root meaning...

Risk Management For Retirees: When To Reduce Exposure

Last week, a viewer of the Morning Show emailed me about risk management for retirees. He asked the...

15 Investing Rules To Win The Long-Game

The rather “Pavlovian” response to Central Bank interventions has led investors into a false...

Dollar Dominance Remains Alive And Well (Part 1)

The dollar is supposed to be dying. We’ve heard that argument for the better part of a...

AI Productivity And Innovation: Prosperity Or Engels Pause?

Innovation drives productivity growth, which in turn raises the standard of living for a...

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

After three decades of watching market cycles play out from both sides of the trade, I’ve...

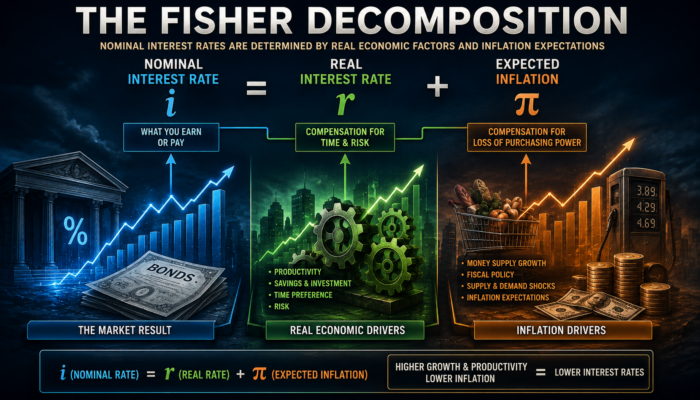

Rising Interest Rates: Why The Narrative Fails Against The Data

A funny thing about bull markets is that investors develop a very short memory about the previous...

Inside You’ll Find:

- The Money-Savvy Guide to Maximum Retirement Income

- Investment & Planning Rules for Financial Success

- The Real Investment Advice Investing Manifesto

- The Savvy Financial Advice Survival Guide

- Much more!

Financial Survival Guides

Real Investment Advice offers a series of in-house financial survival guides to help you navigate the markets and achieve your financial life benchmarks.

Get this guide and many others by signing up below!