Over the last quarter, the “Death of Fundamentals” has become apparent as investors ignore earnings to chase market momentum. However, throughout history, such large divergences between fundamentals and price have resulted in low future returns.

This time is unlikely to be different.

Biggest Decline In Earnings…Ever

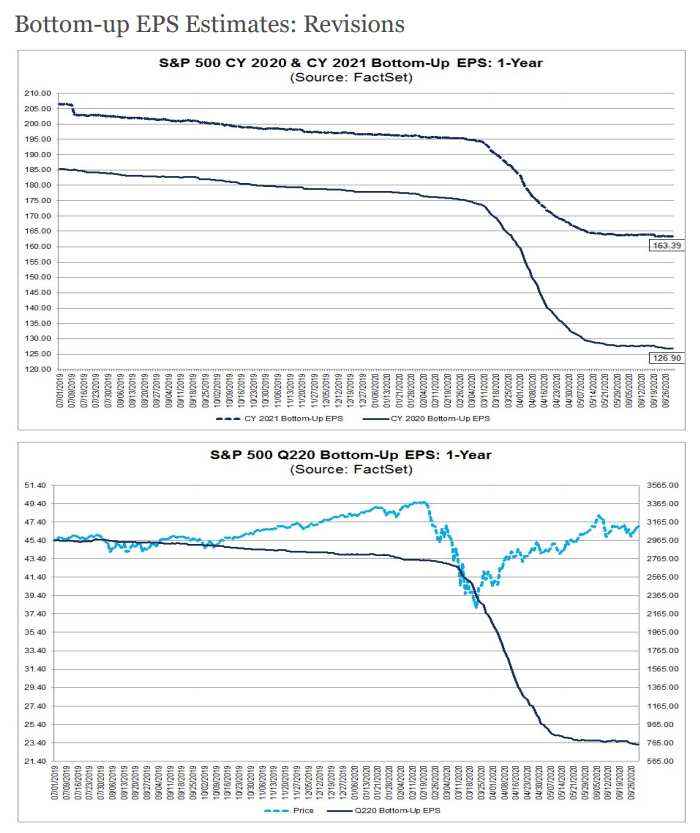

“During the second quarter, analysts lowered earnings estimates for companies in the S&P 500 for the quarter. The Q2 bottom-up EPS estimate (which is an aggregation of the median Q2 EPS estimates for all the companies in the index,) declined by 37.0% (to $23.25 from $36.93) during this period. How significant is a 37.0% decrease in the bottom-up EPS estimate during a quarter? How does this decrease compare to recent quarters?

During the past five years (20 quarters), the average decline in the bottom-up EPS estimate has been 3.2%. Over the past ten years, (40 quarters), the average decline in the bottom-up EPS estimate has been 3.4%. During the past fifteen years, (60 quarters), the average decline in the bottom-up EPS estimate has been 4.6%. Thus, the decline in the bottom-up EPS estimate recorded during the second quarter was much larger than the 5-year average, the 10-year average, and the 15-year average.

In fact, this marked the largest decline in the quarterly EPS estimate during a quarter since FactSet began tracking this data in Q1 2002. The previous record was -34.3%, which occurred in Q4 2008.” – FactSet

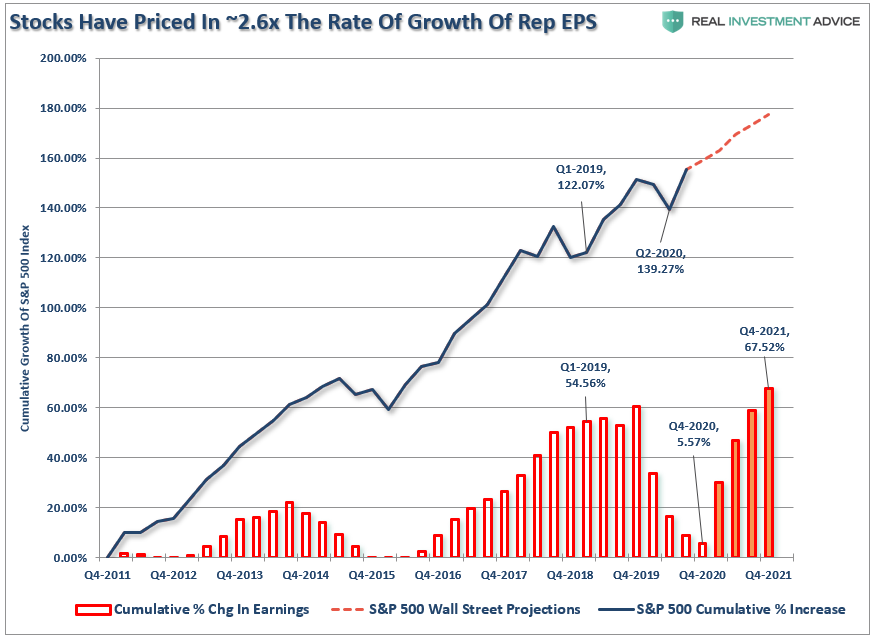

Wishing For A Hockey Stick

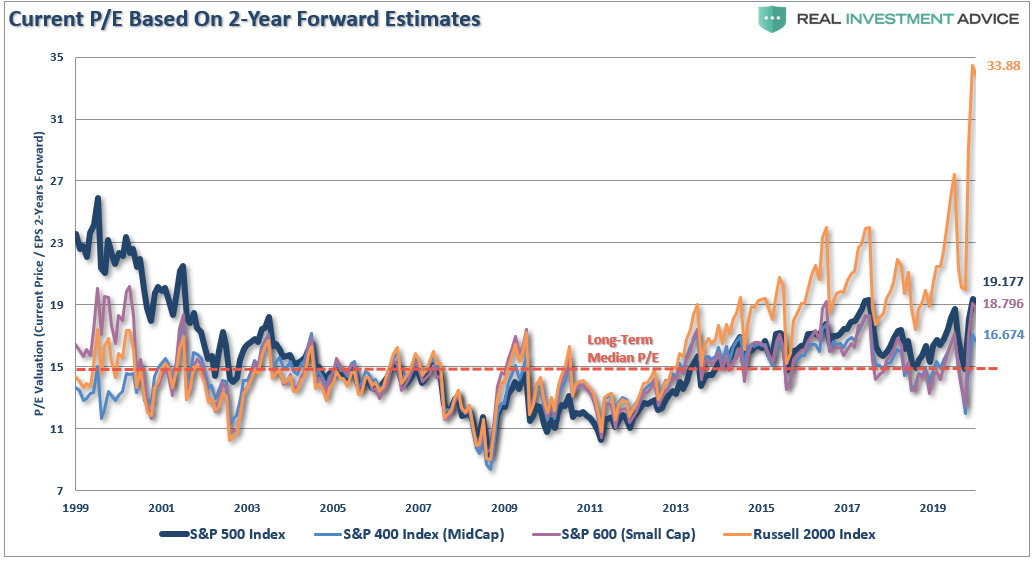

The chart above is telling. Investors continue to bet on a “hockey stick” recovery in earnings to justify overpaying for stocks with the highest price momentum. As discussed in “The Bullish Test Comes:”

“Such makes the mantra of using 24-month estimates to justify paying exceedingly high valuations today, even riskier.”

Importantly, earnings estimates did not decline due to just the onset of the “pandemic.” Earnings began to decline in earnest in late 2018 as economic growth had started to weaken.

As we warned in mid-2019, the inversion of the yield curve had also set the stage for an economic contraction:

“Despite commentary to the contrary, the yield curve is a ‘leading indicator’ of what is happening in the economy currently, as opposed to economic data, which is ‘lagging’ and subject to massive revisions.”

All that was needed was an unexpected, exogenous catalyst to trigger the actual event.

The important point is that investors have been overpaying for earnings by more than 2.5x since the peak in earnings in 2018. Slower economic and wage growth and a widening of the “wealth gap,” has stalled revenue growth. Such has forced companies to engage in a wide variety of accounting “gimmickry” to manufacture earnings to support higher asset prices.

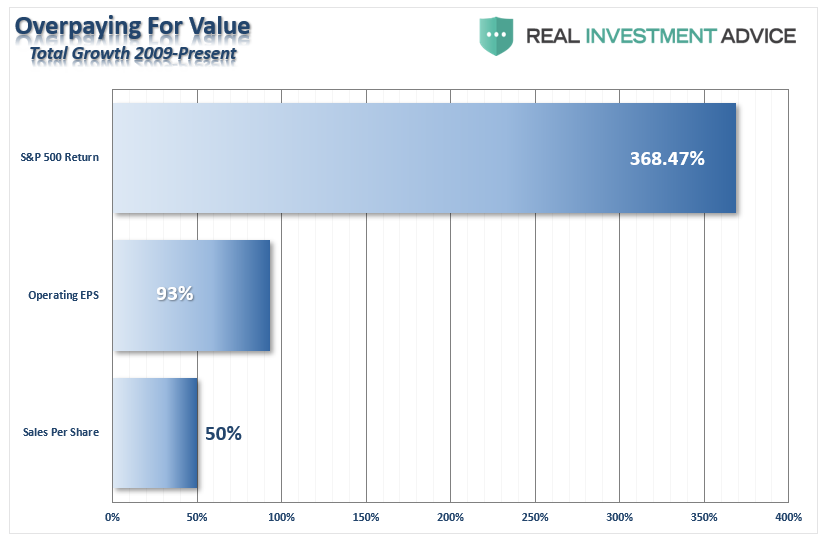

Overpaying For Value

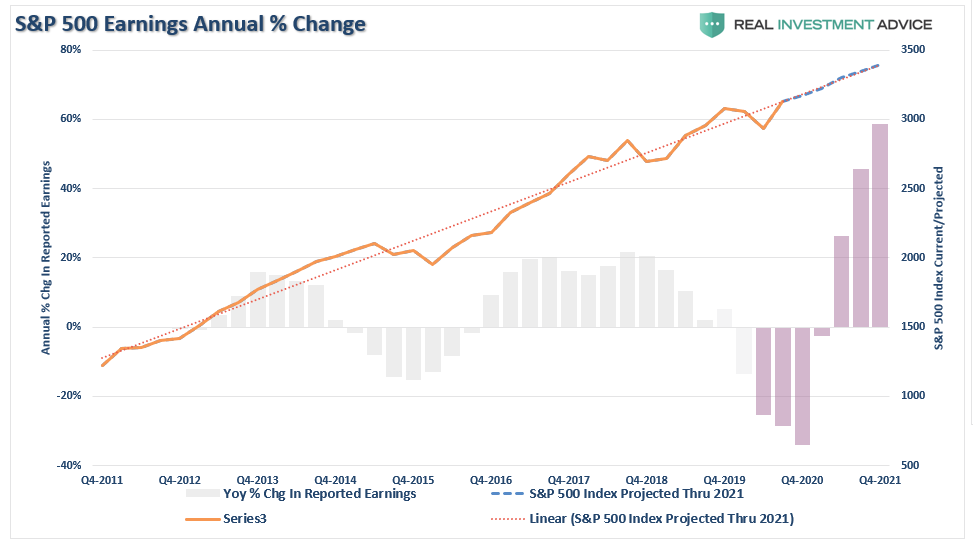

Since 2009, investors have bid up stock prices by more than 368%. Yet, cumulative operating earnings and revenue have only grown by 93% and 50%, respectively.

Even if the expected “hockey stick recovery” in earnings occurs, earnings will only return to the same level as they were in 2018.

If we assume analysts are correct, and historically they overly estimate by 33%, investors have vastly overpaid for earnings. Such has historically guaranteed investors disappointing investment outcomes.

However, as we enter “earnings season,” we are again seeing analysts and companies adjusting their numbers to win the “beat the estimate” game. Such is why I call it “Millennial Soccer.” Earnings season is now a “game” where no one keeps score, the media cheers, and everyone gets a “participation trophy” just to show up.

Wall Street Analysis Isn’t For You

When it comes to earnings season, the media will be complicit in pushing Wall Street’s recommendations. However, those “buy, sell and hold” recommendations aren’t for you. Those recommendations are the “bait” to camouflage the “hook.”

I will let you in on a “dirty little secret.”

Wall Street doesn’t care about you or your money. Such is because their profits don’t come from servicing “Mom and Pop” retail clients trying to save their way into retirement. Wall Street is not “invested” along with you, but “uses you” to generate income for their “real” clients.

Such is why “buy and hold” investment strategies are so widely promoted. As long as your dollars are invested, the mutual funds, stocks, ETF’s, etc, the Wall Street firms collect their fees. These strategies are certainly in their best interest – just not necessarily yours.

However, those retail management fees are a “rounding error” compared to the really big money.

Wall Street’s real clients are multi-million and billion-dollar investment banking transactions. These deals include public offerings, mergers, acquisitions, and debt offerings, which generate hundreds of millions to billions of dollars in fees for Wall Street each year.

You know, companies like Uber, Lyft, Snapchat, Tesla, and Shopify.

Buy, Sell or Hold

For Wall Street firms to “win” that very lucrative business, they must cater to their prospective clients. Not surprisingly, it is difficult for a firm to gain investment banking business from a company with a “sell” rating.

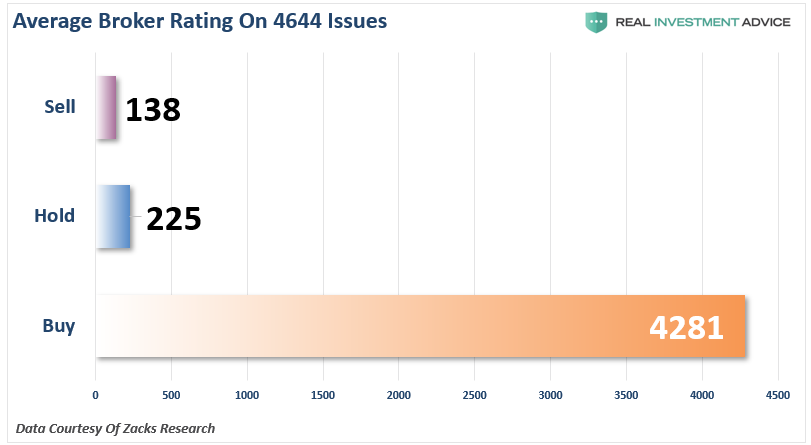

Such is why “buy” ratings are so prevalent versus “hold” or “sell,” as it keeps the client happy. I have compiled a chart of 4644 rated stocks ranked by the number of “Buy”, “Hold” or “Sell” recommendations.

There are just 2.97% of all stocks with a “sell” rating.

Do you believe that out of 4644 rated companies, only 138 should be “sold?”

You shouldn’t.

But for Wall Street, a “sell” rating is not good for business.

The conflict doesn’t end just at Wall Street’s pocketbook. Companies depend on their stock prices rising as it is a huge part of executive compensation packages.

Corporations apply pressure on Wall Street firms, and analysts, to ensure positive research reports with the threat they will take their business to a “friendlier” firm. The goal of boosting share prices for compensation is also why roughly 40% of corporate earnings reports are “fudged” to produce better outcomes.

As the Associated Press exposed in “Experts Worry That Phony Numbers Are Misleading Investors:”

“Those record profits that companies are reporting may not be all they’re cracked up to be.

As the stock market climbs ever higher, professional investors are warning that companies are presenting misleading versions of their results that ignore a wide variety of normal costs of running a business to make it seem like they’re doing better than they really are.

What’s worse, the financial analysts who are supposed to fight corporate spin are often playing along. Instead of challenging the companies, they’re largely passing along the rosy numbers in reports recommending stocks to investors.“

You Have To Do Your Own Homework

So, what can you do?

You have two choices.

You can do your homework using a research tool like “RIAPro.Net” (Try Risk-Free for 30-days) where you can screen for fundamental value.

Or, you can hire an independent, fee-only advisor who knows how to do the work for you.

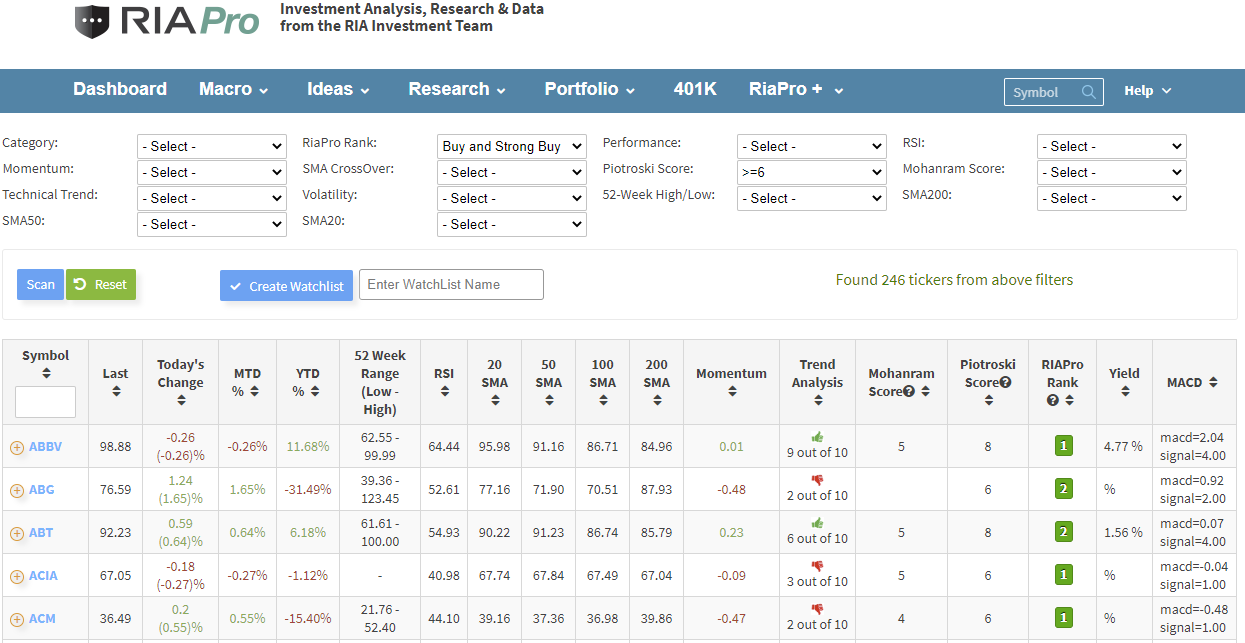

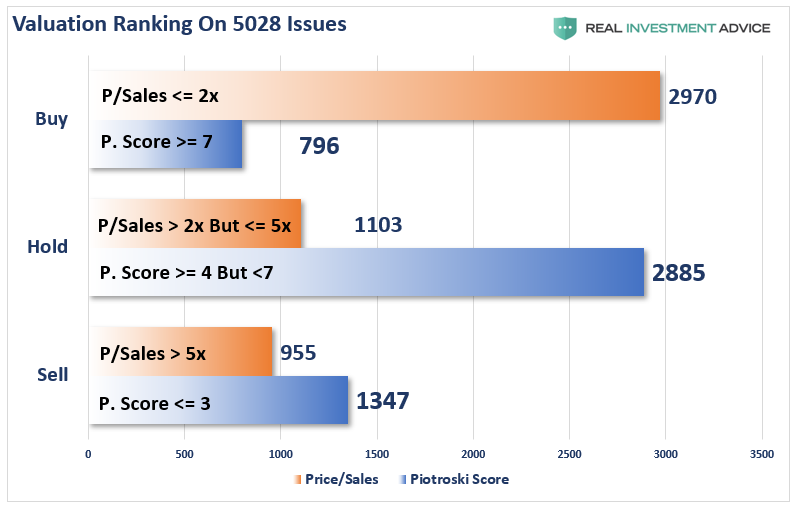

Let me show you the difference between Wall Street’s “buy, sell, hold” analysis versus how we break the universe of stocks we screen at RIA Advisors.

As an independent money manager, I use valuation analysis to determine what equities should be bought, sold or held in client’s portfolios. While there are many valuation measures, two of my favorites are Price-to-Sales and the Piotroski f-score. For this example, I sorted the entire Zacks Research equity universe of 5028 issues. I ranked them by just these two measures.

See the difference. Not surprisingly, there are far fewer “buy” rated, and far more “sell” rated, companies than what is suggested by Wall Street analysts.

Price-To-Sales Sends A Warning

Here is something even more alarming.

Just after the “dot.com” bust, I wrote a valuation article quoting Scott McNeely. He was the CEO of Sun Microsystems at the time. At its peak, the stock was trading at 10x its sales. (Price-to-Sales ratio) In a Bloomberg interview, Scott made the following point.

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. It also assumes I have zero cost of goods sold, which is very hard for a computer company.

That assumes zero expenses, which is really hard with 39,000 employees.That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10-years, I can maintain the current revenue run rate.

Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes.

What were you thinking?

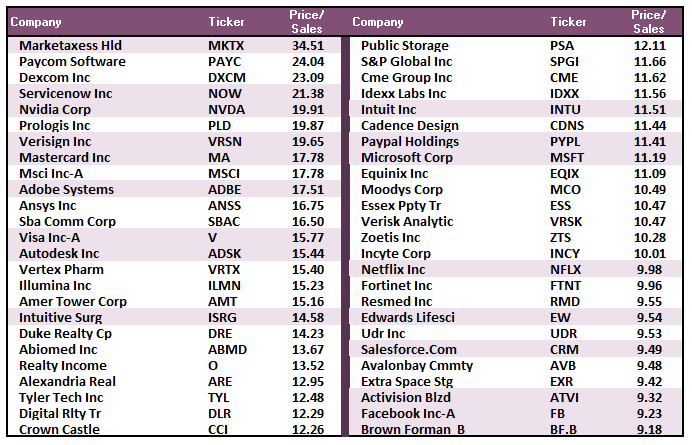

What’s In Your Portfolio

How many of the following “Buy” rated companies do you own carrying price-to-sales valuations above 9 or 10 times?

So, what are you thinking?

As an increasing number of “baby boomers” head into retirement, the need for independent, organic research and analysis, which is in the client’s best interest, is more critical now, than ever.

Independent advice can help remove those emotional biases from the investing process that lead to poor investment outcomes. There are many great advisors with the right team, tools, and data, who can manage portfolios, monitor trends, adjust allocations, and protect capital through risk management.

The next time someone tells you that you can’t “risk-manage” your portfolio and just have to “ride things out,” just remember, you don’t.