A recent article on MarketWatch by Sanjib Saha caught my attention:

“After taking the Series 65 exam last February, I set a goal for 2019: Help 10 friends and family members with their finances. Instead of giving specific investment advice, I wanted to educate them on money matters. I knew that they would benefit from one-on-one discussions, well-regarded books, educational videos and credible websites.”

Think about that for a moment. Here is a young man, who grew up during the longest bull market in history, just took his exam last year, has no real investment experience to speak of, and is now giving advice to people with no investment knowledge.

What could possibly go wrong?

While the majority of the article is grossly misinformed and a regurgitation of the “bullish mantras,” there was one paragraph that jumped out with respect to investment success and failure over time. To wit:

“Many years ago, Aisha, received a windfall that she needed to invest. She interviewed a few financial advisers and went with someone who had an impressive job title, a long list of designations and a friendly demeanor. She regularly reviewed her portfolio with the adviser, but never considered there might be performance problems. After all, a paid professional ought to do better than the market, not worse—or so she thought.

As it turned out, her portfolio had more than doubled over 16½ years.Aisha was impressed, until she backtested an identical asset allocation—one with half U.S. stocks and half corporate bonds. A 50-50 allocation consisting of just two broadly diversified index funds would have quadrupled her money over the same holding period. She stared at the results in disbelief. The opportunity cost was huge.”

The Comparison Trap

This is one of the biggest tools used by financial advisors to get clients to switch their accounts over to a “better” program. Let me explain.

Comparison is the cause of more unhappiness in the world than anything else. Perhaps it is inevitable that human beings as social animals have an urge to compare themselves with one another. Maybe it is just because we are all terminally insecure in some cosmic sense. Social comparison comes in many different guises. “Keeping up with the Joneses,” is one well-known way.

Think about it this way.

If your boss gave you a Mercedes as a yearly bonus, you would be thrilled, right? However, what if you found out shortly afterward that everyone else in the office got two cars.

WTF? Now, you are ticked.

But really, are you deprived of getting a Mercedes? Shouldn’t that enough?

Comparison-created unhappiness and insecurity is pervasive, judging from the amount of spam touting everything from weight-loss to plastic surgery. The basic principle seems to be that whatever we have is enough, until we see someone else who has more. Whatever the reason, comparison in financial markets can lead to remarkably bad decisions.

It is this ongoing measurement against some random benchmark index which remains the key reason why investors have trouble patiently sitting on their hands, letting whatever process they are comfortable with, work for them. They get waylaid by some comparison along the way and lose their focus.

If you tell a client that they made 12% on their account, they are very pleased. If you subsequently inform them that “everyone else” made 14%, you’ve now made them upset. The whole financial services industry, as it is constructed now, is predicated on making people upset so they will move their money around in a frenzy.

Therein lies the dirty little secret. Money in motion creates revenue. The creation of more and more benchmarks, indexes, and style boxes is nothing more than the creation of more things to COMPARE to, allowing clients to stay in a perpetual state of outrage.

Aisha, for example, was completely happy with doubling her money over the last 16-years, until our young, inexperienced, newly minted financial advisor showed her “what she could have had.” Now she will make decisions which will potentially increase the amount of risk she is taking in the second most expensive bull market in history.

Our Worst Enemy

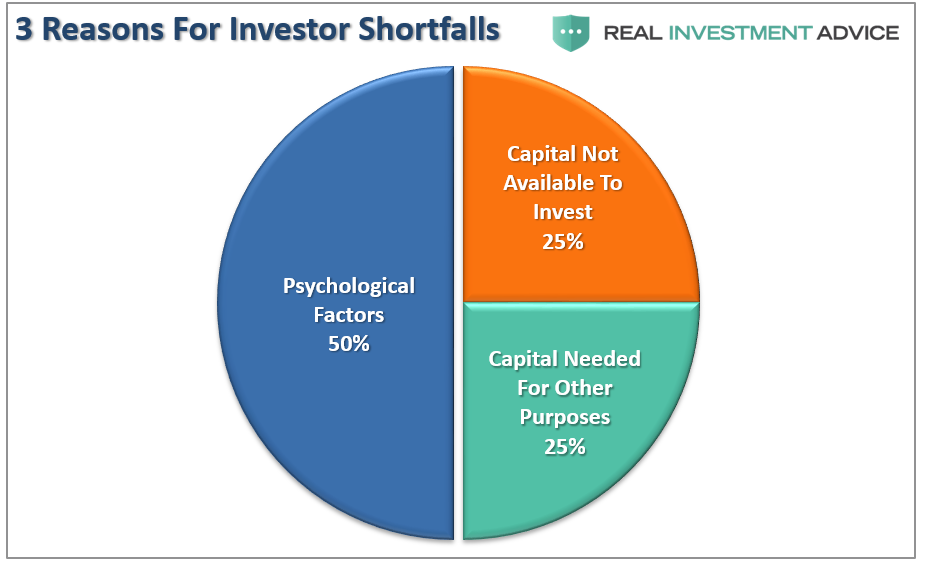

I have written about the psychological issues which impede investors returns over longer-term time frames in the past. The two biggest factors, according to Dalbar Research, which lead to chronic investor underperformance over time are:

- Lack of capital to invest, and;

- Psychological behaviors

Psychological factors account for fully 50% of investor shortfalls in the investing process. Of course, not having the capital to invest is equally important.

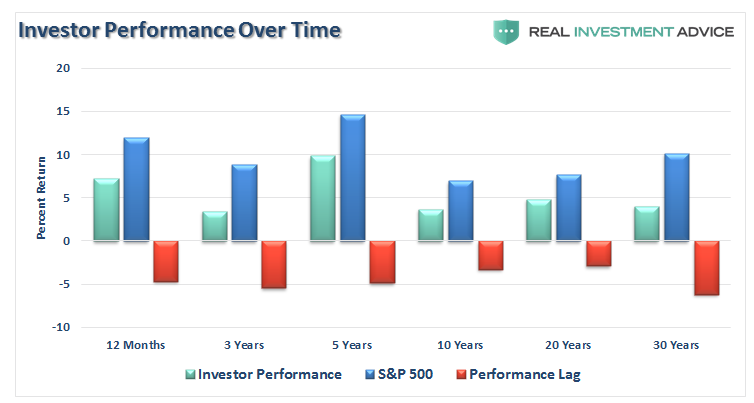

These factors, as shown by data from Dalbar, lead to the lag in performance between investors and the markets over all time periods.

Behavioral biases are an issue which remains little understood and accounted for when individuals begin their investing journey. There are (9) nine of these behavioral biases specifically which impact investors the most.

- Loss Aversion – The fear of loss leads to a withdrawal of capital at the worst possible time. Also known as “panic selling.”

- Narrow Framing – Making decisions about on part of the portfolio without considering the effects on the total.

- Anchoring – The process of remaining focused on what happened previously and not adapting to a changing market.

- Mental Accounting – Separating performance of investments mentally to justify success and failure.

- Lack of Diversification – Believing a portfolio is diversified when in fact it is a highly correlated pool of assets.

- Herding– Following what everyone else is doing. Leads to “buy high/sell low.”

- Regret – Not performing a necessary action due to the regret of a previous failure.

- Media Response – The media has a bias to optimism to sell products from advertisers and attract view/readership.

- Optimism – Overly optimistic assumptions tend to lead to rather dramatic reversions when met with reality.

These cognitive biases impair our ability to remain emotionally disconnected from our money. As a consequence, we are continually lured into making decisions which are inherently bad for our long-term outcomes.

The Advisor’s Role

These psychological and behavioral issues are exceedingly difficult to control and lead us regularly to making poor investment decisions over time. But this is where the role of an “experienced advisor” should be truly defined and valued.

While the performance chase, a by-product of the very behavioral issues we wish to control, leads everyone to seek out last years “hottest” performing manager or advisor, this is not really the advisor’s main role. The role of an advisor is NOT beating some random benchmark index or to promote a “buy and hold” strategy. (There is no sense in paying for a model you can do yourself.)

Jason Zweig summed it well:

“The only legitimate response of the investment advisory firm, in the face of these facts, is to ensure that it gets no blood on its hands. Asset managers must take a public stand when market valuations go to extremes — warning their clients against excessive enthusiasm at the top and patiently encouraging clients at the bottom.”

Given that individuals are emotional and subject to emotional swings caused by market volatility, the advisors role is not only to be a portfolio manager, but also a psychologist. Dalbar suggested four successful practices to reduce harmful behaviors:

- Set Expectations Below Market Indices: Change the threshold at which the fear of failure causes investors to abandon an investment strategy. Set reasonable expectations and do not permit expectations to be inferred from historical records, market indexes, personal experiences or media coverage. The average investor cannot be above average. Investors should understand this fact and not judge the performance of their portfolio based on broad market indices.

- Control Exposure to Risk: Include some form of portfolio protection that limits losses during market stresses. Explicit, reasonable expectations are best set by agreeing on a goal that consists of a predetermined level of risk and expected return. Keeping the focus on the goal and the probability of its success will divert attention away from frequent fluctuations that lead to imprudent actions

- Monitor Risk Tolerance: Periodically reevaluate investor’s tolerance for risk, recognizing that the tolerance depends on the prevailing circumstances and that these circumstances are subject to change. Even when presented as alternatives, investors intuitively seek both capital preservation and capital appreciation. Risk tolerance is the proper alignment of an investor’s need for preservation and desire for capital appreciation. Determination of risk tolerance is highly complex and is not rational, homogenous nor stable.

- Present Forecasts In Terms Of Probabilities: Simply stating that past performance is not predictive creates a reluctance to embark on an investment program. Provide credible information by specifying probabilities, or ranges, that create the necessary sense of caution without negative effects. Measuring progress based on a statistical probability enables the investor to make a rational choice among investments based on the probability of reward.

The challenge, of course, it understanding that the next major impact event, and market reversion, will NOT HAVE the identical characteristics of the previous events. This is why comparing today’s market to that of 2000 or 2007 is pointless. Only the outcome will be the same.

One thing that all the negative behaviors have in common is that they can lead investors to deviate from a sound investment strategy which was narrowly tailored towards their goals, risk tolerance, and time horizon.

The best way to ward off the aforementioned negative behaviors is to employ a strategy that focuses on one’s goals and is not reactive to short-term market conditions. The data shows that the average mutual fund investor has not stayed invested for a long enough period of time to reap the rewards that the market can offer more disciplined investors. The data also shows that when investors react, they generally make the wrong decision.

The reality is that the majority of advisors are ill-prepared for an impact event to occur. This is particularly the case in late-stage bull market cycles where complacency runs high.

When the impact event occurs, advisors who are prepared to handle responses, provide clear messaging, and an action plan for both conserving investment capital and eventual recovery will find success in obtaining new clients.

The “do-it-yourself” crowd will also come to learn the value of experience. When the impact event occurs, the losses in passive investments, “yield-chase” investments, and ETF’s will be substantially larger than individuals currently imagine. Those losses will permanently impair individuals ability to obtain their financial goals.

If you don’t believe me, then explain why, with 30 of the last 40 years in major bull market trends, is a large majority of the population woefully underfunded for retirement?

The reason is that investing is not simple. If it was, everyone would be rich. The reality is that whatever gains investors have garnered over the last decade will be largely wiped away by the next impact event.

Of course, this is the sad history of individual investors in the financial markets as they are always “told to buy” but never “when to sell.”

You can do better.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read