Recently, President-Elect Joe Biden named Janet Yellen to be his administration’s Treasury Secretary. Yellen quickly proclaimed the reason “I became an economist was because I was concerned about the toll of unemployment on people, families, and communities.” Such provides excellent commentary, but her track record as Federal Reserve Chairman shows she is more for the top 10% of the economy than the bottom. In reality, and what the markets already suspect, her appointment is an “arranged marriage” to the Fed.

Janet Yellen, along with every Fed Chairman since Paul Volker, has almost single-handedly destroyed the bottom 90% of the American economy.

The one lesson that we have learned since the 2008 “Great Financial Crisis” is that monetary and fiscal policy interventions do not lead to increased economic wealth levels or prosperity. These programs act as a wealth transfer system from the bottom 90% to the top 10%.

However, since she is concerned about employment, let’s start there.

Employment

During Ms. Yellen’s tenure as Fed Chairman, she focused on the “official unemployment rate” as a reason to continue accommodative monetary policies. However, despite employment falling below 5% unemployment rates, such did not lead to a surge in wage growth or economic prosperity.

The chart below shows the “real situation” concerning employment.

Notice that post the “Financial Crisis,” the total number of employed persons fell below the previous long-term growth trend. While it is true, as shown below, that population growth has also slipped below the long-term growth trend. Such does not compensate for the massive divergence.

Following the “Financial Crisis,” the growth trend of employment has shifted lower once again. As we will show in a moment, the New “New Normal” won’t return to the “Old New Normal” anytime soon.

Has there been “job creation” since the last recession? Absolutely.

If you look at the actual number of those “counted” as employed, that number has risen from the recessionary trough. Unfortunately, as shown, employment remains far below the long-term historical trends that would suggest healthier economic growth levels. Currently, the deviation from the long-term trends did not improve since the “Financial Crisis” and have worsened now.

More Falling Off Than Going On

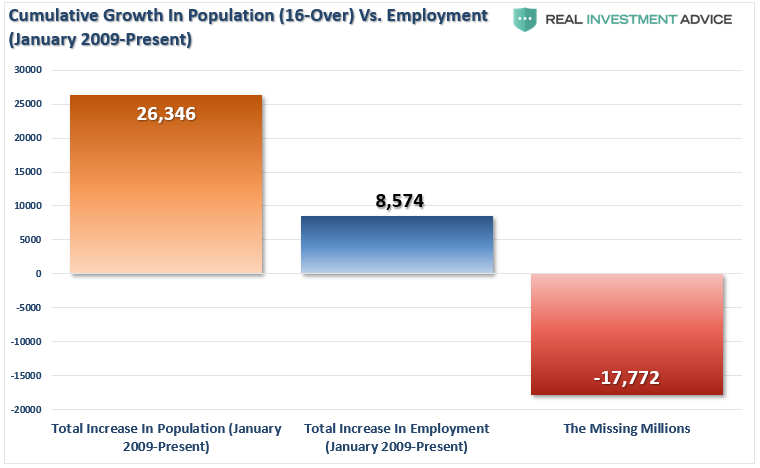

However, as it relates to economic growth, the number of new entrants into the working-age population each month is often overlooked.

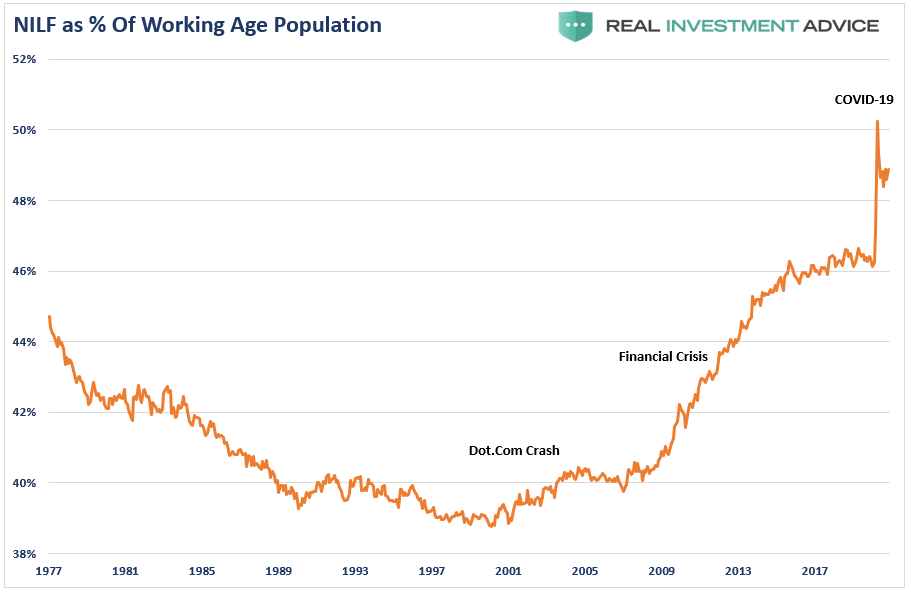

As you can see in the chart above, while total employment grew by 8.5-million, the working-age population grew by 26-million, leaving a 17.7-million person deficit sitting idle in the economy. Of course, after some time, these individuals are no longer counted as part of the labor force. Such is why, despite monthly headlines of employment growth, those no longer in the labor force (NILF) continues its pace higher.

Of course, suppose we stop counting individuals as part of the “labor force,” which is the denominator of the unemployment rate calculation. In that case, the economy will be at full-employment in no time.

Retiring Boomers

Such is where someone usually throws out the claim all those “baby boomers” are retiring. Maybe. But considering the financial preparedness statistics of those over-65, the more likely case is that most will be working until death.

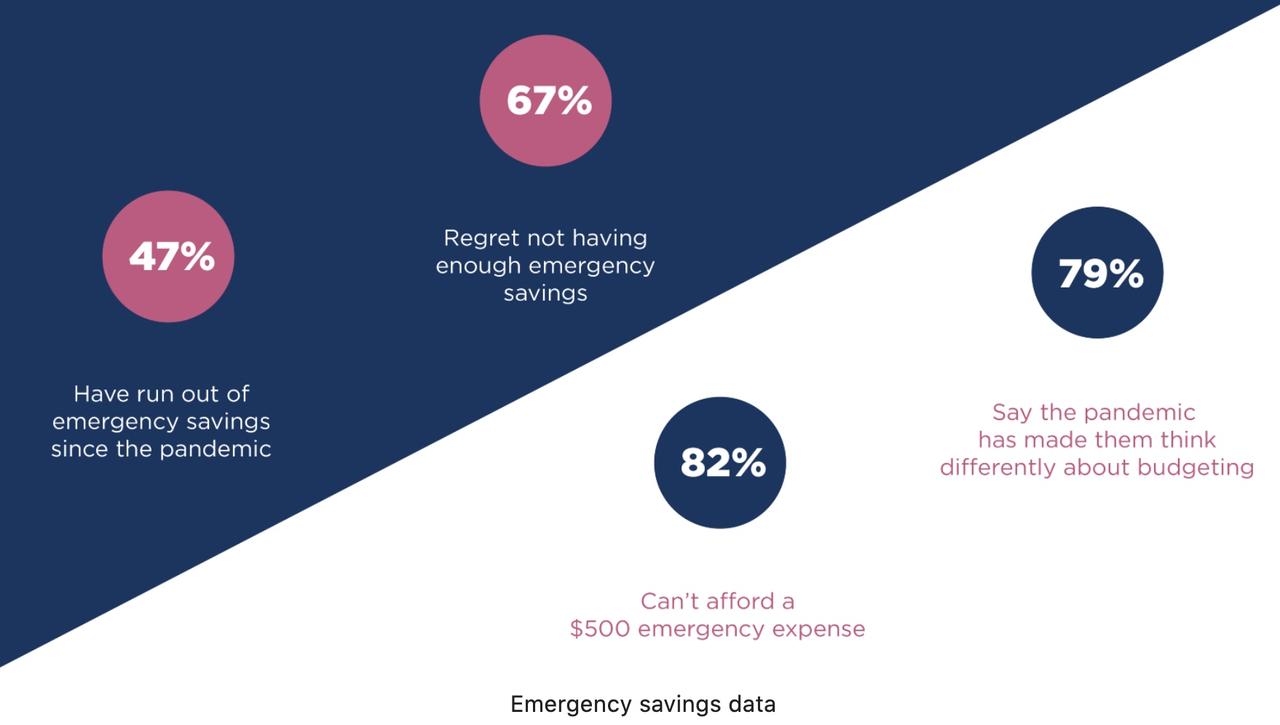

A recent study by Highland of 2000 Americans is just one of the latest, which shows the bottom 80% of Americans’ plight.

The most alarming number from the entire survey is that 82% of respondents said they wouldn’t be able to cover an emergency $500 expense without borrowing money. For context, this number is up from just roughly 50% of Americans pre-pandemic. Such means the number of people who say they couldn’t cover a small emergency has risen by a whopping 60%.

Importantly, and to a point discussed previously, nearly half added that they now regret living beyond their means for so long before the crisis.

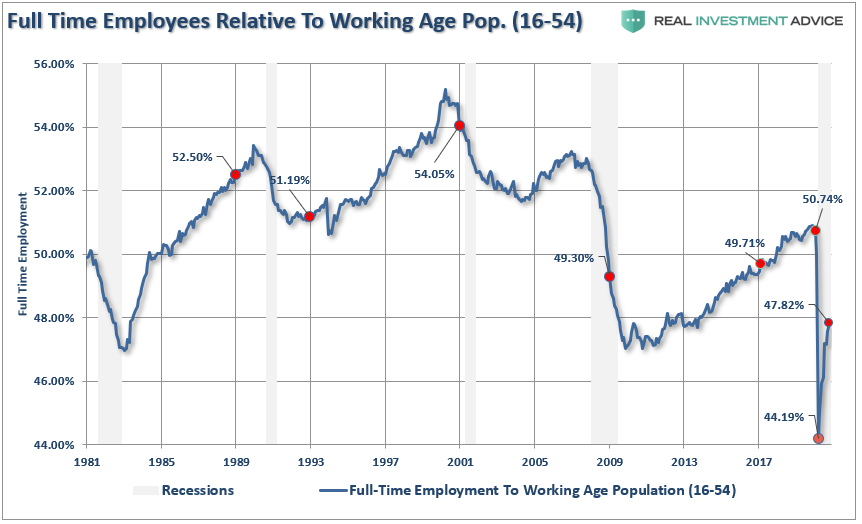

However, even if we look at the labor force participation rate of those that SHOULD be working (16-54 years of age), it remains at the lowest levels since the 1970s. This chart alone should give Ms. Yellen pause in her abilities to create employment growth in the real economy.

The critical difference is that the participation rate was rising in the 80s and 90s – not falling.

More Work, Less Pay

There are two very negative ramifications of this large and “available” labor pool. The first is that the longer an individual remains unemployed, the degradation of job skills weighs on future employment potential and income. The second, and most importantly, is that wages remain under significant downward pressure with a high competition level for existing jobs.

Business owners are highly aware of the employment and business climate. Regardless of the ranting and raving about the “cash on the sidelines,” businesses are not charities. Business owners are milking the current employment climate for all it is worth to maintain profitability. With high competition levels for existing jobs and the impending threat of job loss for those working, employers can work longer hours with only a modest increase in wages. Such is great for profit margins, and workers won’t complain because plenty of individuals will be happy to take their job and do it for less pay.

While Ms. Yellen claims she is a “champion of employment” for the “average Joe,” the Fed’s policies have not been beneficial.

Economy

As we discussed in “Rescues Ruining Capitalism,” to Ms. Yellen, when “you only have a hammer, everything looks like a nail.” Since the days of Ben Bernanke, the answer for every economic ill has been more “stimulus.” Such has led to the current trap Ms. Yellen will find herself in as Treasury Secretary.

“They are increasingly on what I call a no-exit paradigm.” – Mohammed El-Erian

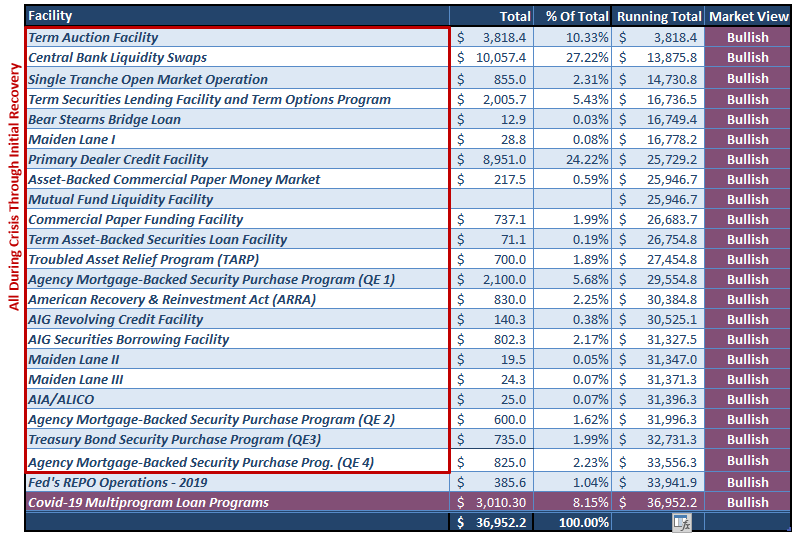

The bailouts and stimulus programs started in 2008 when the Federal Reserve intervened with the insolvency of Bear Stearns. They haven’t stopped since.

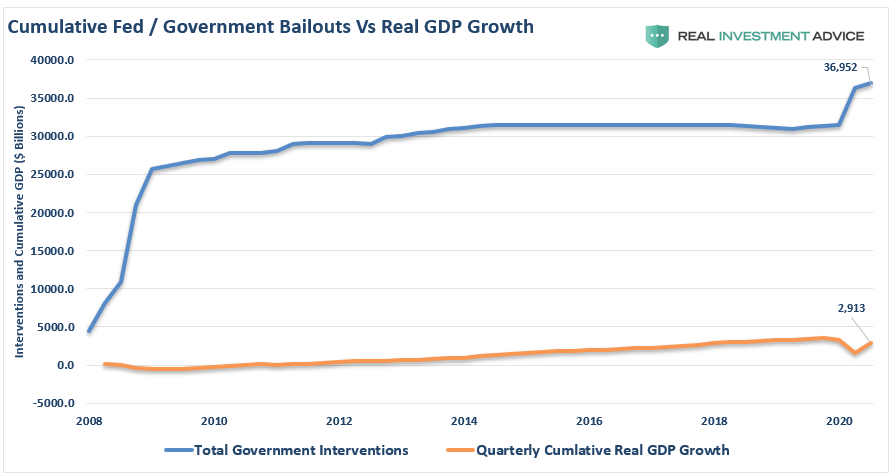

To date, the Federal Reserve, and the Government, have pumped more than $36 Trillion into the economy. As shown below, the amount of economic growth achieved has been minimal during that same time frame. (The chart is the cumulative growth of interventions compared to the incremental increase in GDP.)

What this equates to is more than $12 of liquidity for each $1 of economic growth.

Everything Is A Nail

If you read between the lines, policymakers are “spit-balling” solutions and making potentially erroneous monetary policy decisions on unreliable data. However, given Central Banks’ only policy tool (or hammer) is more liquidity, it is a “hammer first, ask questions later” response.

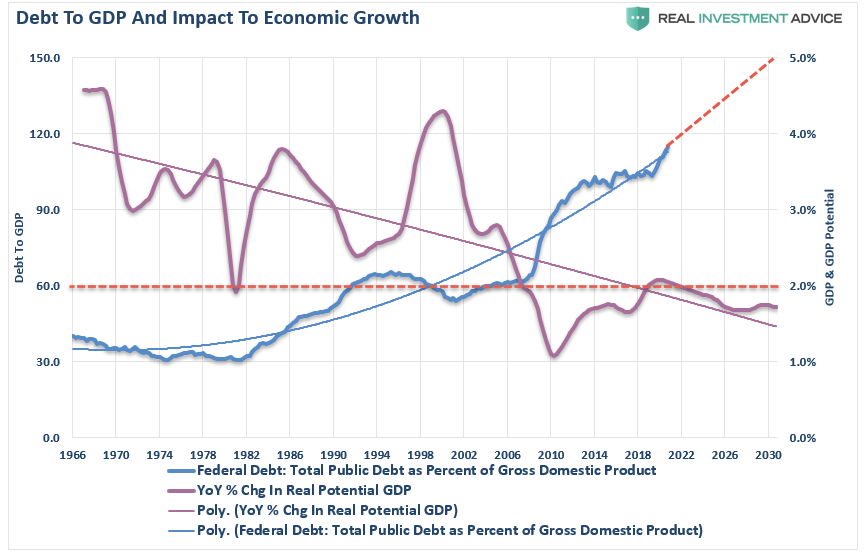

The problem is those policy measures continue to erode economic prosperity. Such is evident when the CBO’s own long-term economic growth potential projections fall below 2%.

Due to the debt, demographics, and monetary and fiscal policy failures, the long-term economic growth rate will run well below long-term trends. Such will ensure the widening of the wealth gap, increases in welfare dependency, and capitalism giving way to socialism.

“So for the Federal Reserve to intervene and support those asset prices, is creating a little bit of moral hazard in a sense you’re encouraging people to take on more debt.” – Bill Dudley

What could go wrong?

Financial Wealth Transfer

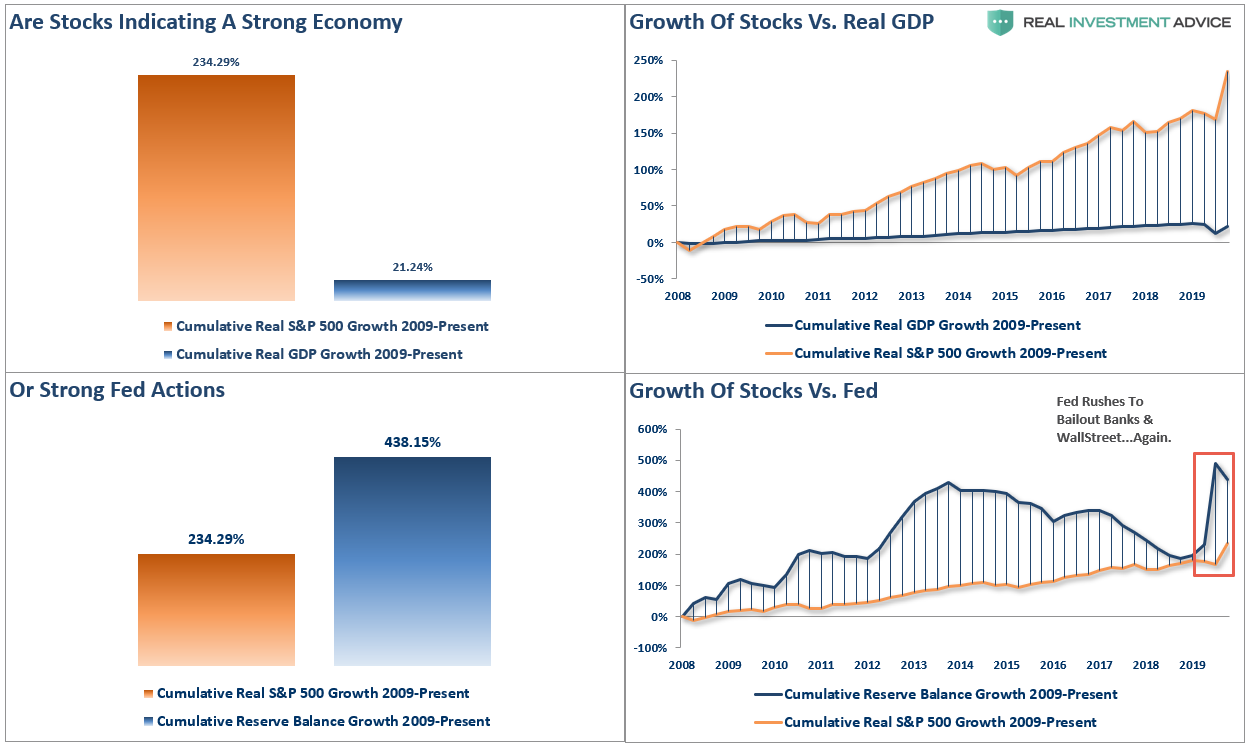

From Jan 1st, 2009 through the end of November, the stock market has risen by an astounding 234% or roughly 21% annualized. With such a large gain in the financial markets, there should be a commensurate growth rate in the economy.

After 4-massive Federal Reserve driven “Quantitative Easing” programs, a maturity extension program, bailouts of TARP, TGLP, TGLF, etc., HAMP, HARP, direct bailouts of Bear Stearns, AIG, GM, bank supports, etc., all of which totaled more than $36 Trillion, cumulative real economic growth was just 21.24%

While monetary interventions are supposed to be supporting economic growth through increases in consumer confidence, the outcome has been quite different.

Top 10% Or Bust

As noted by the WSJ previously:

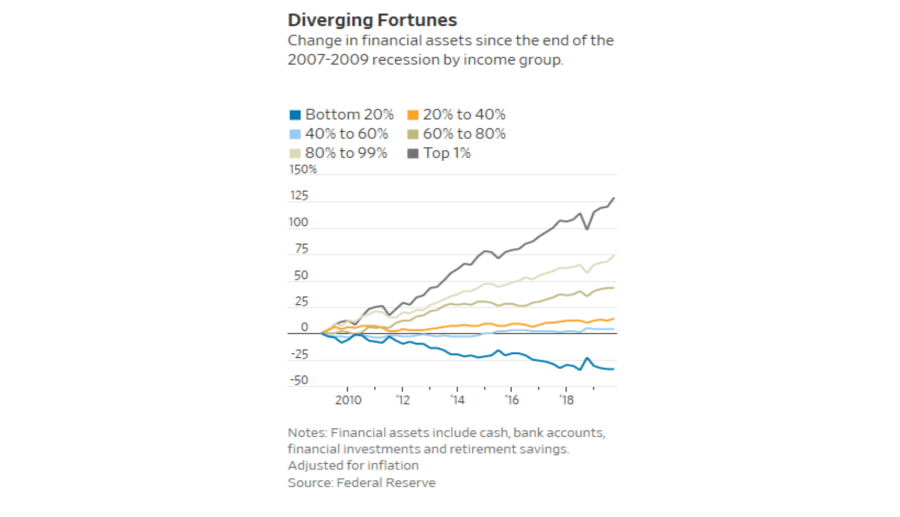

“As of December 2019—before the shutdowns—households in the bottom 20% of incomes had seen their financial assets, such as money in the bank, stock and bond investments or retirement funds, fall by 34% since the end of the 2007-09 recession, according to Fed data adjusted for inflation. Those in the middle of the income distribution have seen just 4% growth.” – WSJ

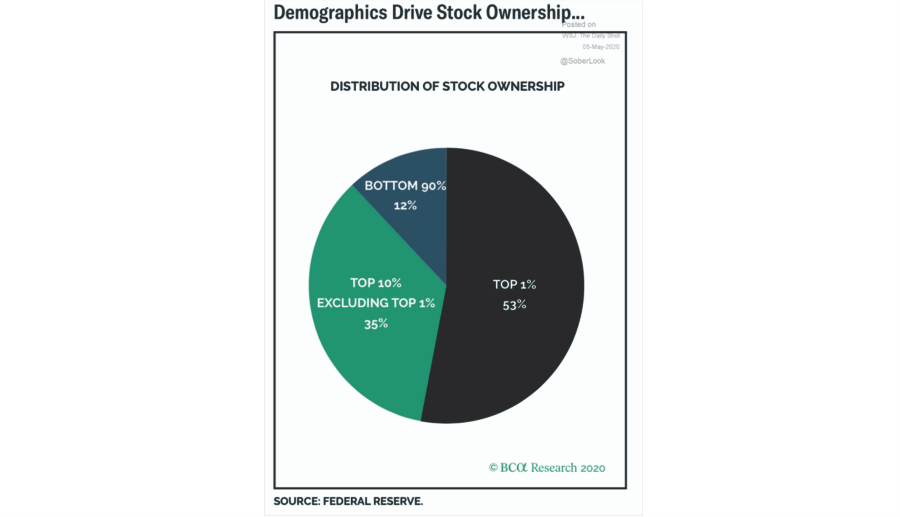

Such isn’t surprising. A recent research report by BCA confirms one of the causes of the rising wealth gap in the U.S. The top-10% of income earners own 88% of the stock market; the bottom-90% own just 12%.

An Arranged Marriage

As I started this note, Mrs. Yellen’s appointment is effectively an “arranged marriage” between the Treasury and the Fed. Such is a political move by the Biden Administration to “grease the wheels” so that monetary liquidity readily flows into the markets. Given Ms. Yellen’s politics and policies, such will inevitably lead to a repeat of past failures. We should expect to see current policies accelerated as we continue down the path of “Japanification.”

Given that debt is a retardant to organic economic growth, as it diverts dollars from productive investment to debt service, the problems that face Japan are similar to what we are, and will continue, to witness in the U.S.:

- A decline in real savings rates that depletes productive investments

- An aging demographic that is top-heavy and increasingly drawing on social benefits.

- A heavily indebted economy with debt/GDP ratios above 100%.

- Exports will continue to decline due to a weak global economic environment.

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases to offset reduced employment

Dependency

The lynchpin to Japan, and the U.S., remains demographics and interest rates. As the aging population grows, becoming a net drag on “savings,” the dependency on the “social welfare net” will continue to expand.

“Japan, like the U.S., is caught in an on-going ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse.

The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments and risk begins to outweigh the potential return.”

Concerning Ms. Yellen, I am sure she has the best of intentions. However, after four decades of monetary policy reducing economic growth, fueling one financial crisis after the next, and creating the widest wealth gap in history, maybe it’s time to try a different strategy.

If the economy, and employment, are Ms. Yellen’s true passions, then she has the opportunity to try a different set of policies to try and get a different result. However, her history and the data suggests this is likely not the case.

We suspect that by the end of her term as Treasury Secretary, the economy, and the markets, will be littered with corpses of more “monetary policy errors.”

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read