Moderna and Pfizer recently announced they had potential vaccines for COVID-19 that are more than 90% effective. With that, the market surged, and a rotation into “economically sensitive” sectors occurred. While a “vaccine” will eventually come to the market, it will only ensure a return to the “New New Normal.”

The Old “New Normal”

Following the “Financial Crisis,” there was much discussion in the media about the “New Normal.”

The term originated cautioning economists and policy-makers’ belief industrial economies would revert to levels seen before the financial crisis. In other words, the “new normal” economy would look a lot different, and worse, after the financial crisis was over.

Such did turn out to be the case. Economic growth struggled to maintain a 2.2% annualized growth rate, interest rates remained abnormally low, and inflation was nascent. Despite the Fed’s best efforts, productive investments or increases in the labor force participation rate failed to appear.

The chart below shows productivity increases through automation, and technology did not lead to higher employment levels relative to the population.

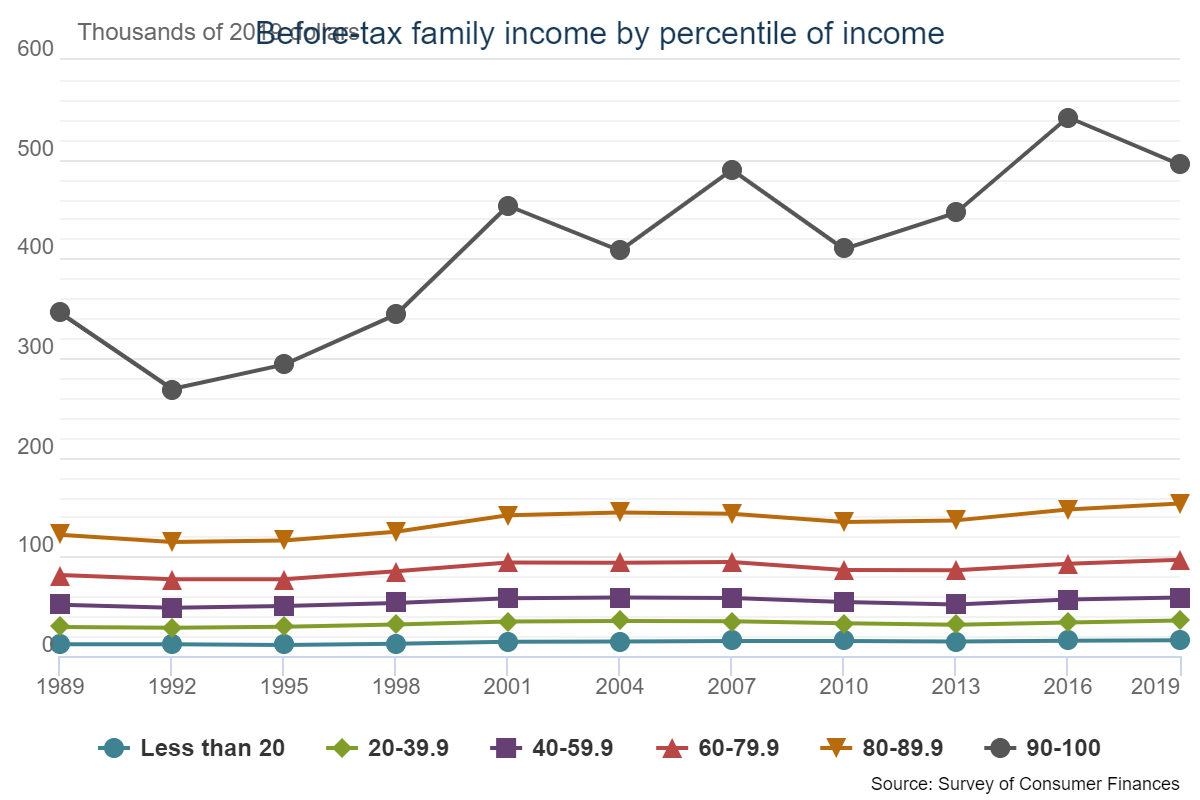

In the “Old-New Normal,” the shift in employment, combined with increased productivity, led to weaker income growth for the bottom 80% of the population. Such was a point we discussed recently concerning the Federal Reserve’s latest study on consumer finances. To wit:

“The real story becomes much more apparent when breaking incomes into deciles.”

“Interestingly, the ONLY TWO age-groups where incomes have improved since 2007 are those in the top 20% of income earners. Again, this suggests the plunge in the LFPR is not a function of “retirement.” Individuals are working well into their retirement years, not because of a desire to, but due to necessity.”

The Vaccine Doesn’t Solve The Problem.

Please understand me. “Vaccine news” is certainly good and very welcome. However, don’t get too excited just yet. Even if Pfizer and Moderna get through Phase-IV trials and produce a drug, most of the population will not see it for many months. As noted by the Wall Street Journal:

“However, it could be many months before any vaccine is administered to enough people to ease the need for lockdown measures that have been recently reimposed across the West. Duke Global Health Innovation Center estimates that there won’t be enough vaccines to cover the world’s population until 2024.

Of course, such also assumes you can get people to get vaccinated.

“While previous vaccination programs have spread over years and focused on specific demographics such as children or the elderly, governments are hoping to do something they never have done before and inoculate a majority of the population in a matter of months.

Even for rich nations with developed vaccination programs, that presents a host of problems including building new databases to track who is getting the shot, working out ways to encourage mass uptake among younger people, ensuring adequate supply and running large-scale inoculation centers where the shots can be safely and quickly administered.

Those challenges mean that even if a vaccine is soon approved, it could be many months before it is administered to enough people to ease the need for lockdown measures that have been recently reimposed across the West.” – WSJ

However, even if we assume we get an effective vaccine produced starting in January, AND we get everyone in the country vaccinated, it won’t change the math.

The New “New Normal”

Here is the problem. There is currently much hope that following the “pandemic,” the world will experience an explosion of growth. The issue is the “Old Normal,” as shown above, wasn’t all that great for the bottom 80% of the population.

The lockdowns accelerated the “work-from-home” mentality for many companies and employees. That trend will not reverse quickly, if ever.

Corporations are now seeing the benefit of reduced labor forces, less office space, and increased productivity through technology. All of these are significant “cost-savings” to the corporation’s bottom lines.

The consumer also will likely continue to do more things online. While travel will likely increase, it may be quite some time to see airlines, hotels, and rental car companies back to previous capacities. As Bloomberg noted in “Get Ready For The New Normal 2.0:”

“The U.S. economy post-Covid-19 will look a lot like the one that struggled to recover from the 2008-09 financial crisis –- only in some ways worse.

Growth will be disappointingly tepid after an initial rebound and, for a time at least, inflation dangerously lower and unemployment heartbreakingly higher than they were back then. Government debt -– and the Federal Reserve’s balance sheet -– will be much bigger, while interest rates stay low.”

The Fed’s New Mandate

The last paragraph is the most important. As we discussed previously in “The Fed Will Monetize All The Debt:”

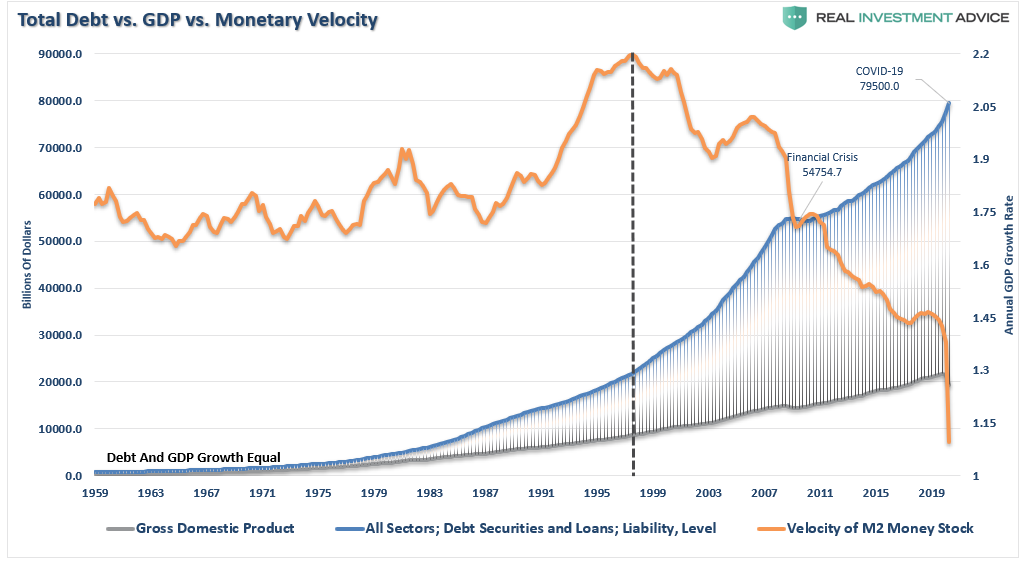

“in 1998, the Federal Reserve “crossed the ‘Rubicon,’ whereby lowering interest rates failed to stimulate economic growth or inflation as the ‘debt burden’ detracted from it. When compared to the total debt of the economy, monetary velocity shows the problem facing the Fed.”

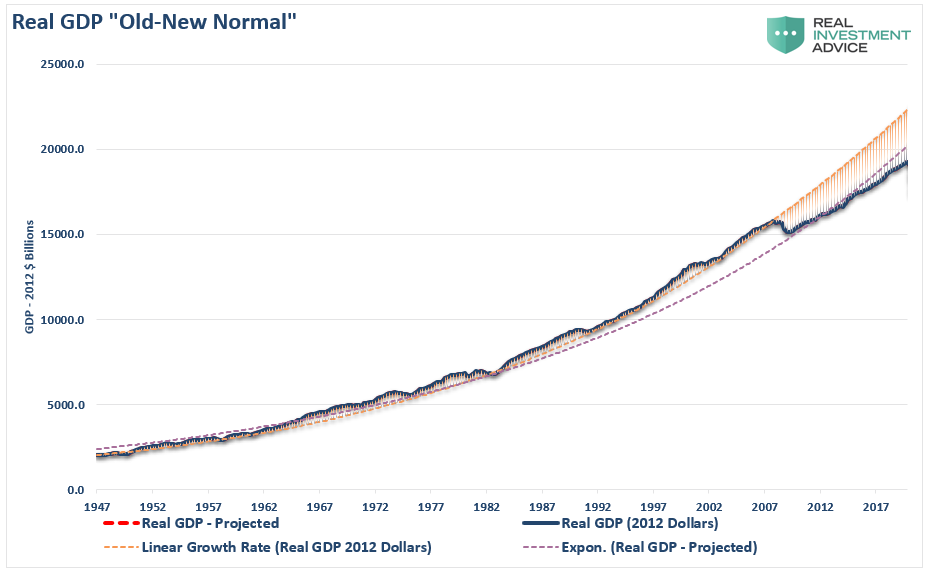

Following the “Financial Crisis,” the massive expansion of debt, deficits, and continues Federal Reserve interventions led to collapsing monetary velocity rates and retardation of economic growth. Before 2008, the long-term growth trend of the real economy was 3.2%. That collapsed to 2.2% as debt exploded.

Bloomberg noted that the “New-New Normal” would consist of even more massive debts, deficits, and Federal Reserve monetizations, with sustained interest rates near zero. Such will see the trend of economic growth step down again to below 2%.

Even with a “vaccine,” an even slower economic growth rate has substantial consequences on employment and the wealth gap.

Employment Will Recover Only On Paper

Companies’ fast adoption of technology, along with increased productivity and change in demand, will further retard employment in the “New-New Normal.”

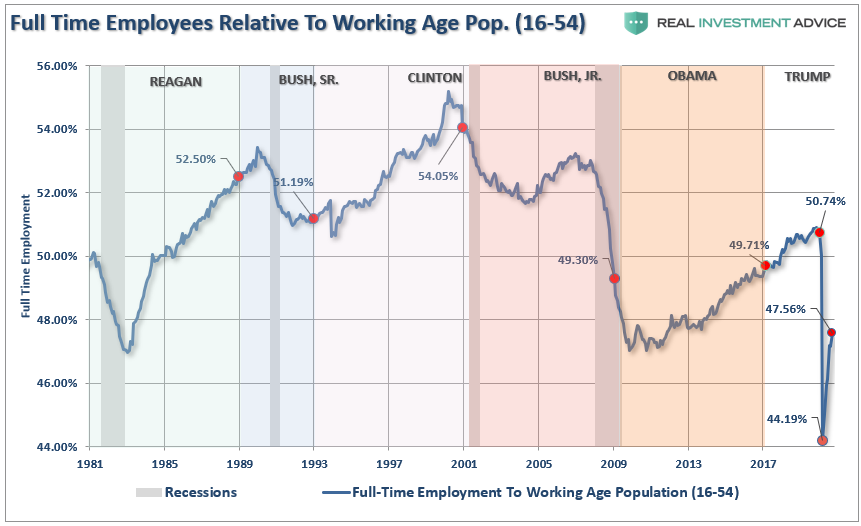

To generate economic growth and prosperity, “full-time” employment is critical. After the “Financial Crisis,” the number of “full-time” jobs relative to the population collapsed and only recovered about half of what was lost. We witnessed the same following the “dot.com” crash. It is highly likely that “full-time” employment will take another stop down as weaker demand requires fewer full-time staff.

Furthermore, participation in the labor force has dropped to levels not seen since 1973 and is a crucial measure to watch. Since the “Financial Crisis,” the participation in the “Labor Force” never significantly rose despite “record low unemployment rates.” Such is because the labor force was shrinking sharply over the last decade as more and more participants were “no longer counted.”

Those “Not In Labor Force” are individuals that are considered out of the labor force and no longer seeking employment. Do you believe that nearly 50% of the working-age population are no longer looking for work?

Such is the “New New Normal.”

The New-New Normal

The structural transformation over this past year and the last decade has permanently changed the economy’s financial underpinnings as a whole. Such would suggest the current state of slow economic growth is the new normal. As such, interest rates will remain stuck near the zero-bound as we continue to struggle with the myriad of problems plaguing growth.

- A low savings rate for 80% of Americans

- An aging demographic

- A heavily indebted economy

- A decline in exports

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases

The lynchpin remains demographics and interest rates. As the aging population grows, they will become a net drag on “savings.” Such increases the dependency on the “social welfare net,” which will continue to expand over time.

“Demography, however, is destiny for entitlements, so arithmetic will do the meddling.” – George Will

The end game of three decades of excess is upon us, and we can’t deny the weight of the debt imbalances currently in play. The medicine the Federal Reserve is prescribing is a treatment for the common cold; in this case, a typical business cycle recession.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read