Yen Carry Trade Blows Up Sparking Global Sell-Off

On Monday morning, investors woke up to plunging stock markets as the “Yen Carry Trade” blew up. While media headlines suggested the sell-off was due to fears of a recession, slowing employment growth, or fears over Israel and Iran, such is not the case. As previously noted, headline events like the economy, employment, or geopolitical conflict are quickly evaluated and hedged by market participants. However, as we saw on Monday, what sparks a global sell-off is always an “unexpected, exogenous event.” To wit:

“If I gave you a bunch of ingredients such as nitrogen, glycerol, sand, and shell, you would probably stick them in the garbage and think nothing of it. They are innocuous ingredients and pose little real danger by themselves. However, you make dynamite using a process to combine and bind them. However, even dynamite is safe as long as it is stored properly. Only when dynamite comes into contact with the appropriate catalyst does it become a problem.

‘Mean reverting events,’ bear markets, and financial crises result from a combined set of ingredients that a catalyst ignites. Like dynamite, the individual ingredients are relatively harmless but dangerous when combined.

Leverage + Valuations + Psychology + Ownership + Momentum = “Mean Reverting Event”

Importantly, this particular formula remains supportive of higher asset prices in the short term. Of course, the more prices rise, the more optimistic investors become. While the combination of ingredients is dangerous, they remain “inert” until exposed to the right catalyst.

That catalyst is always an unexpected, exogenous event that triggers a rush for the exits.“

On Monday, that unexpected, exogenous event was the forced unwinding of the “Yen Carry Trade.” Of course, such begs the question, precisely what is it?

The Yen Carry Trade

The Yen carry trade has been going on in the financial markets for decades. It has been a significant driver for hedge funds in leveraging their portfolios to generate higher returns. An elementary example of the Yen carry trade is as follows:

- A hedge fund sells short $10 million in Japanese Government Bonds that yield zero percent. (The hedge fund sold an asset they didn’t own, netting the fund $10 million and effectively shorting the Japanese Yen.)

- The hedge fund then buys $10 million in U.S. Treasuries, yielding 4%, capturing the spread between the bonds.

- Then, the hedge fund leverages that $10 million into $100 million (10x leverage) to buy risk assets.

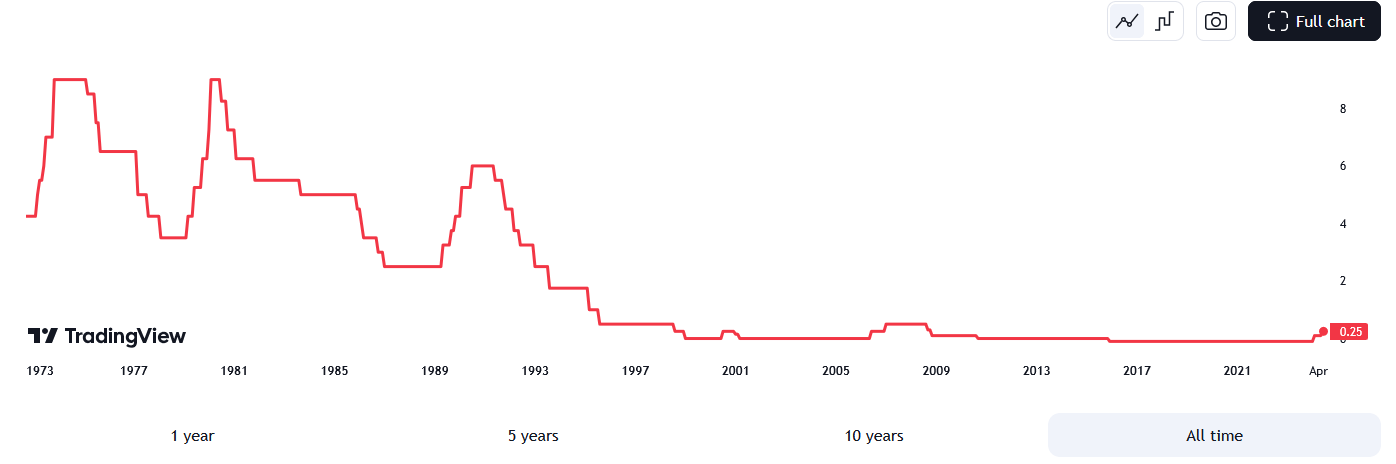

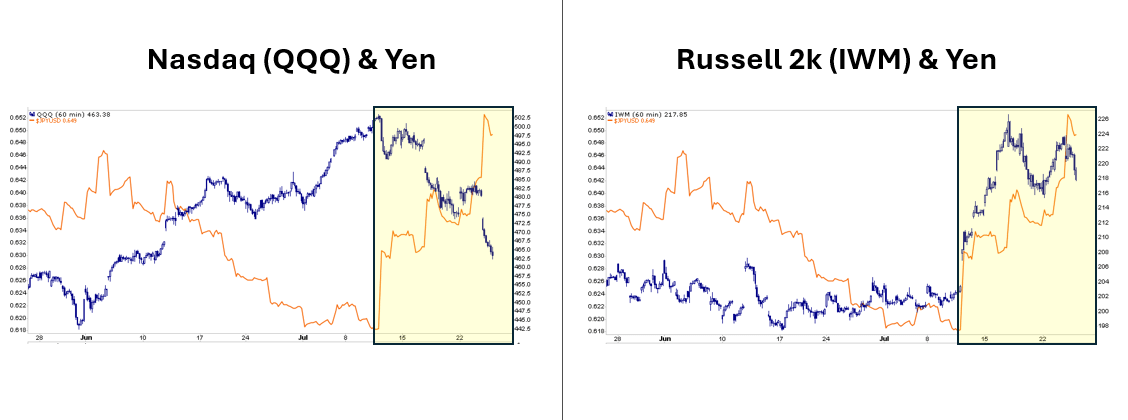

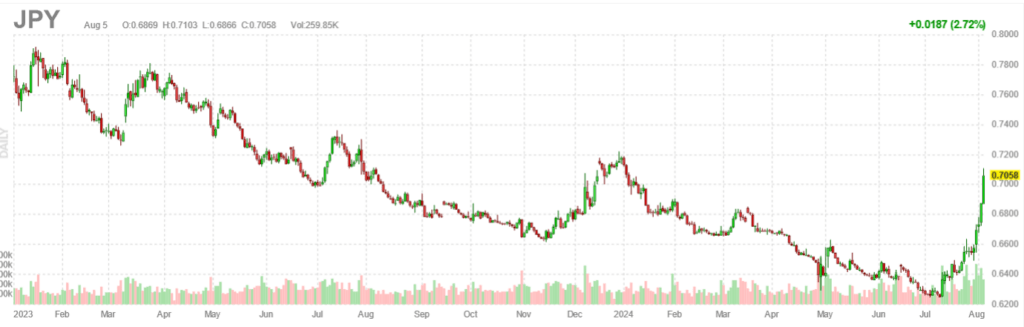

Now, consider that “yen carry traders” have leveraged highly volatile risk assets like cryptocurrencies, small-cap stocks, mega-cap stocks, and even the Japanese market. The carry trade works well as long as the Japanese Yen does not markedly appreciate, forcing a liquidation of the market leverage.

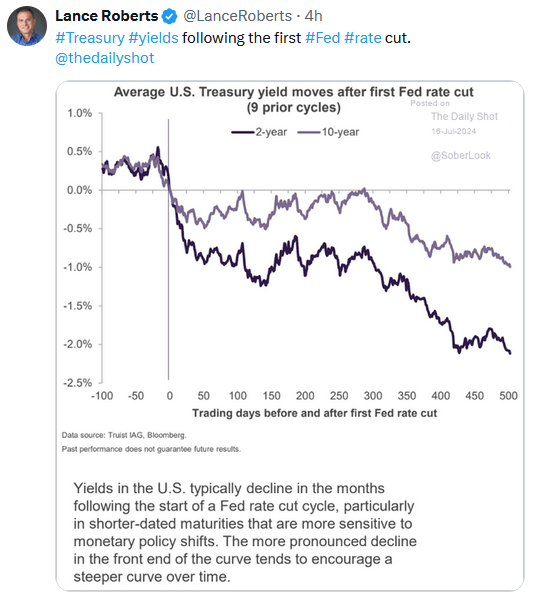

The problem, as shown below, is that the Yen has appreciated more than 15% in the last few weeks. As the Yen appreciates, the Japanese banks demand margin calls (i.e., the catalyst). When that occurs, the hedge funds, pension funds, insurance companies, or investors using the “Yen carry trade” must either put up more collateral or sell the leveraged assets. That reversal and forced liquidation created a vicious spiral by pushing the Yen higher and risk assets lower.

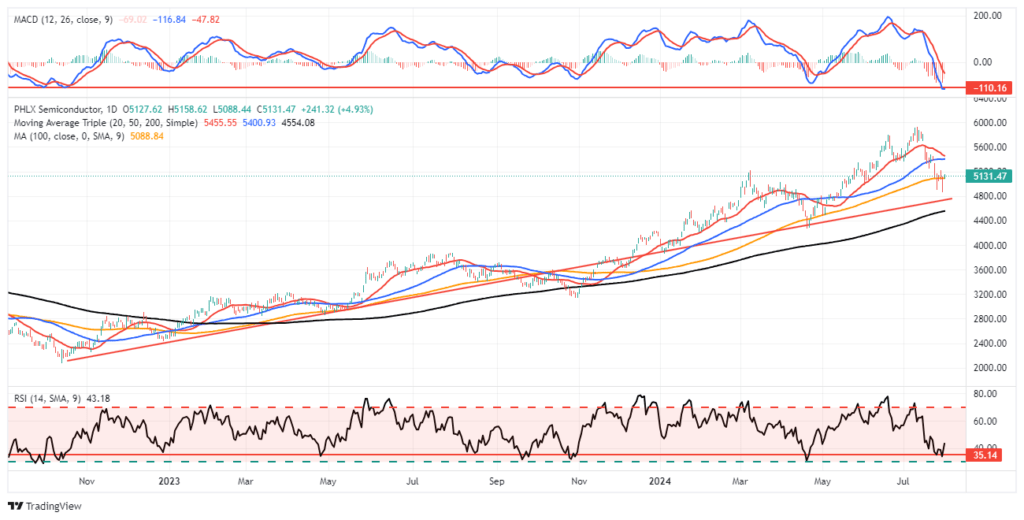

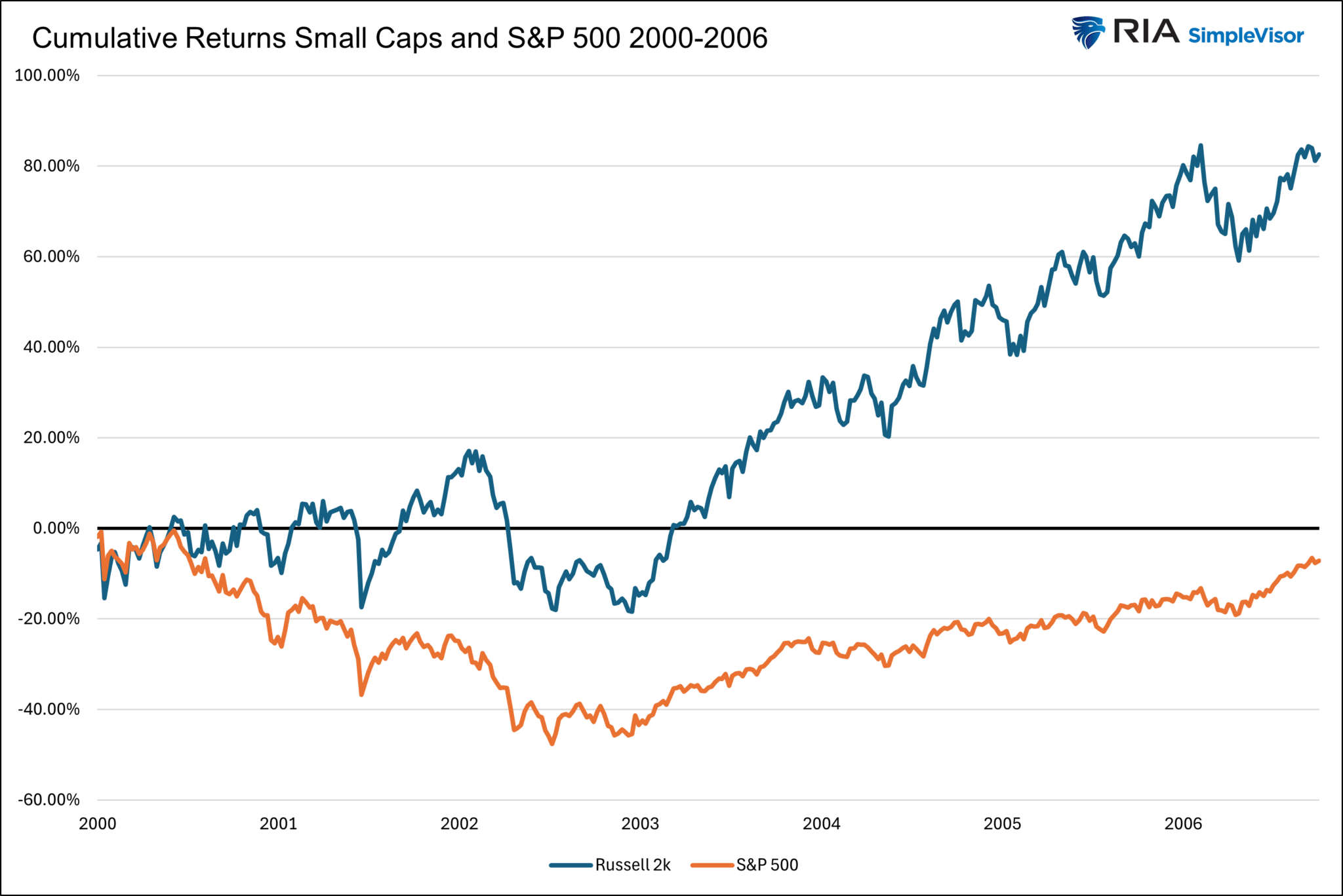

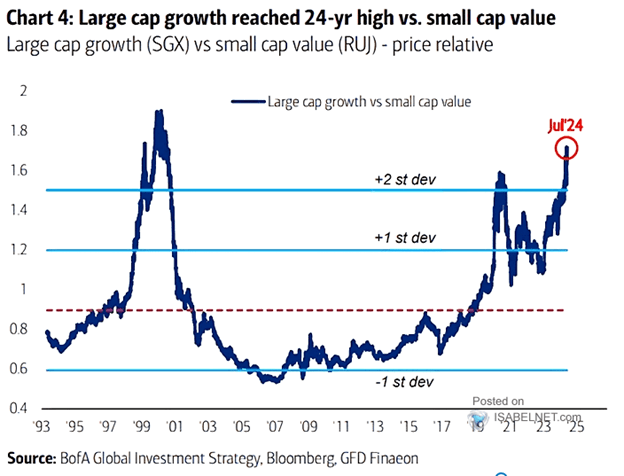

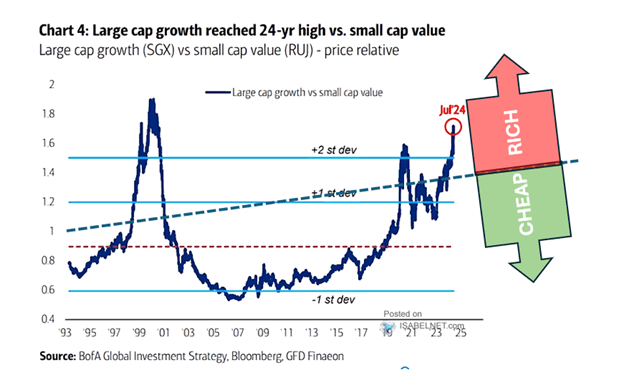

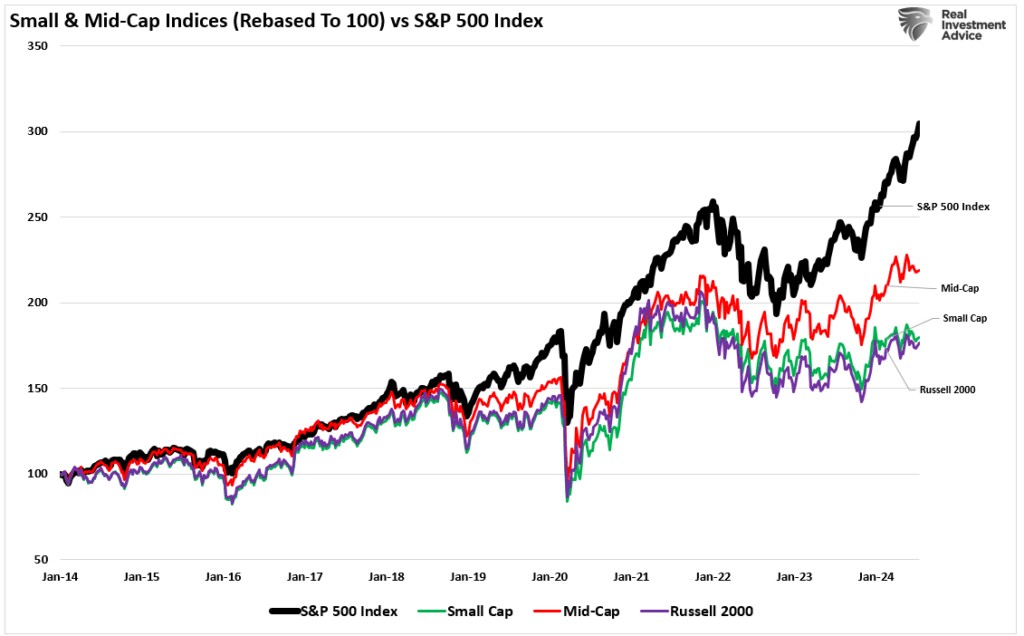

An excellent example of the “yen carry trade” was seen in the recent surge in the Russell 2000 index. As we warned in “Risks To The Russell,” the fundaments didn’t support the rotation.

For a deeper discussion on the “Yen Carry Trade,” Michael Lebowitz and I discussed the issue in a video update we sent to our clients Monday morning.

So, what happens next?

Market Unwind – More To Go?

As an investor, the most crucial action to take during”an “unexpected, exogenous event” is to DO NOTHING.

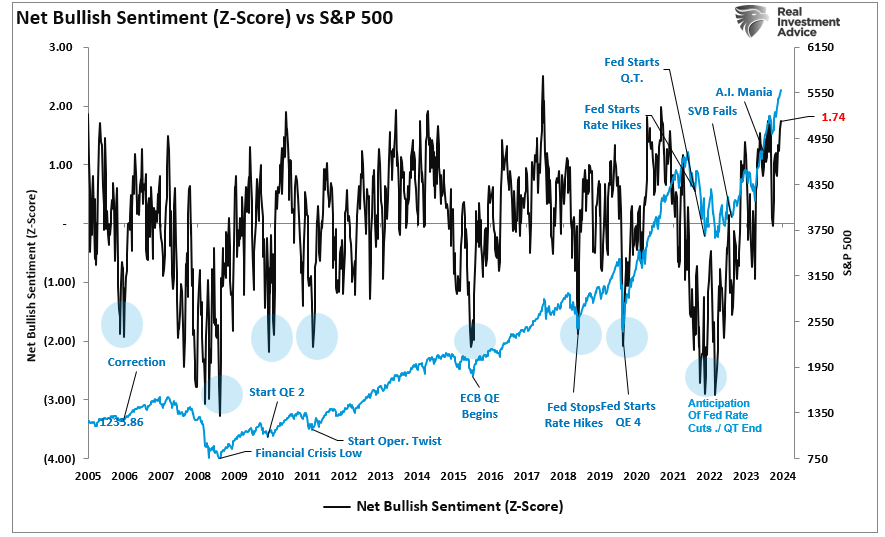

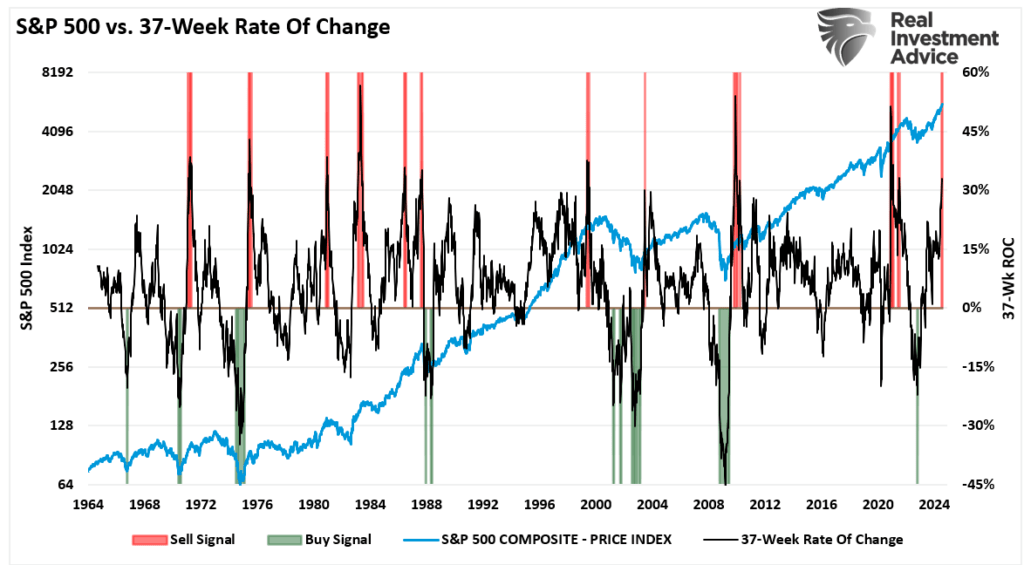

That’s right, don’t do anything. When something occurs, like a sharp market correction, our initial emotional response is to take action and begin liquidating positions. Such would certainly seem to be a logical reaction; however, more often than not, the time to sell positions was ahead of the event. Over the last two months, we have repeatedly warned that a 5-10% market correction was likely heading into the election. To wit:

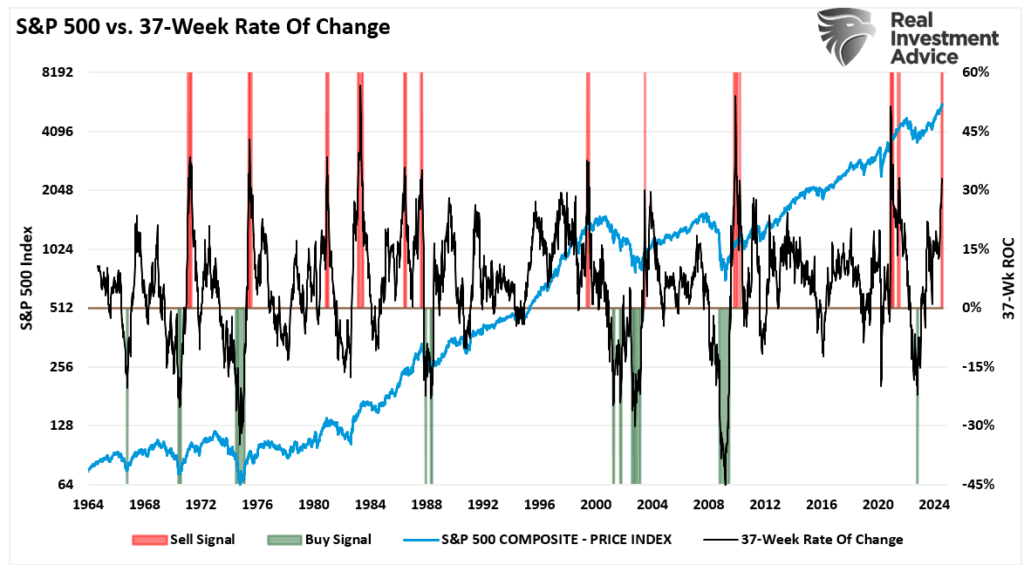

Historically, when the 37-week rate of change is greater than 30%, such events typically precede short—to intermediate-term corrections. While the bulls are very confident, the risk of a 5% to 10% correction over the next three months remains elevated.

In our non-options models, we will transition to more “defensive” positions, raise cash levels, and hedge as needed. Nothing suggests anything more than a 5-10% correction between now and November. Such will be the same as last year and historically in line with Presidential election cycles. While many often ignore the warning signs while markets rise, they tend to be the same ones panic-selling when they should buy.” – July 13, 2024

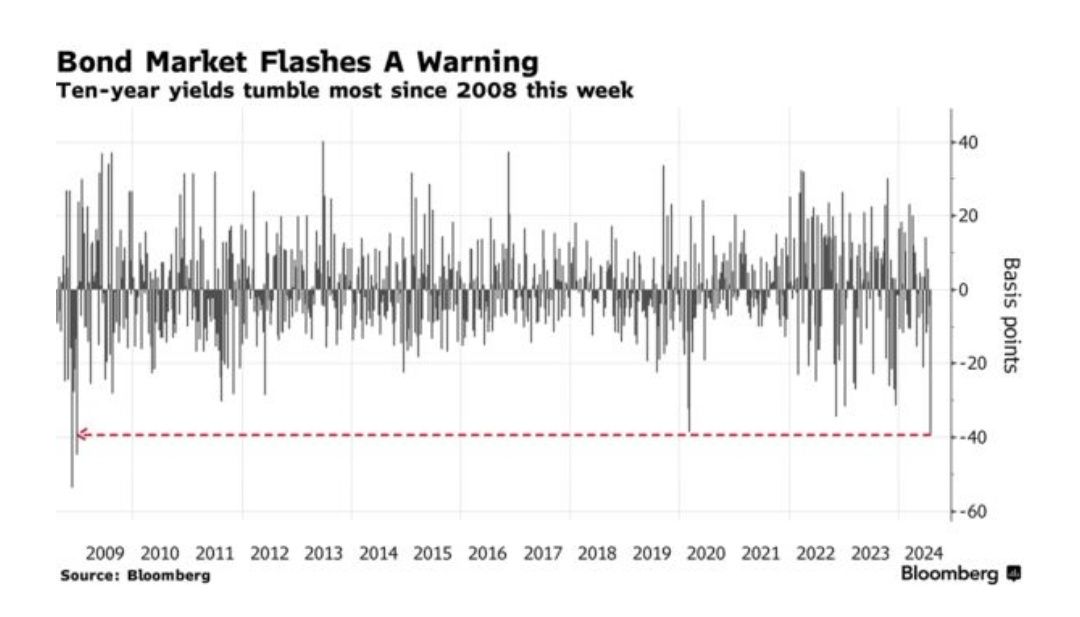

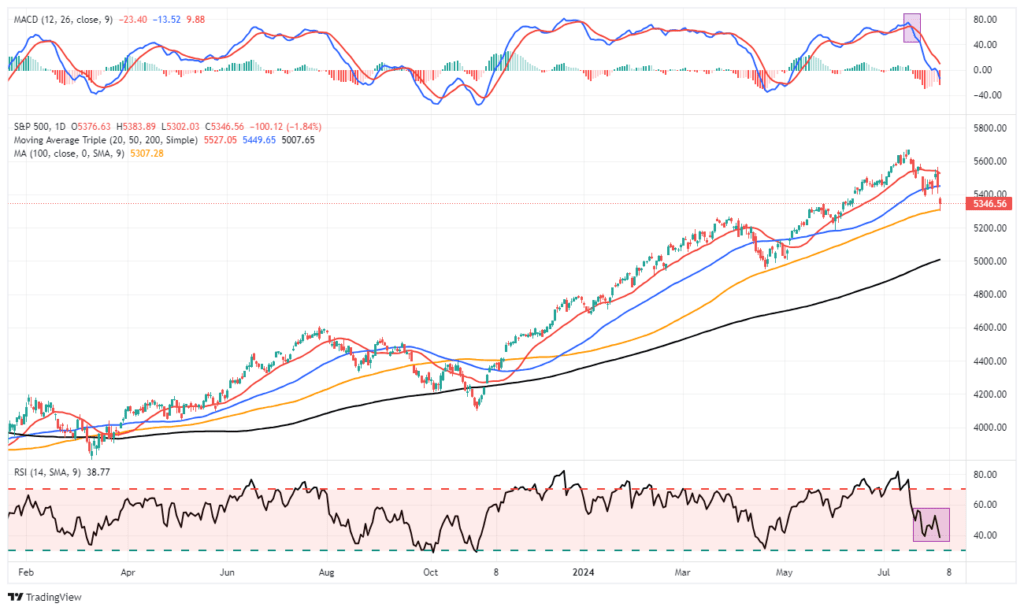

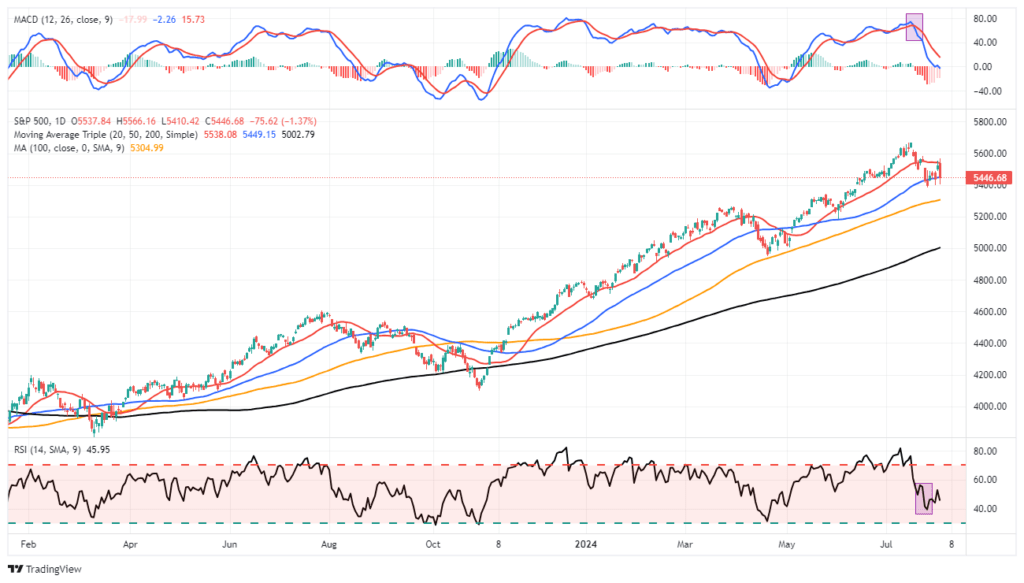

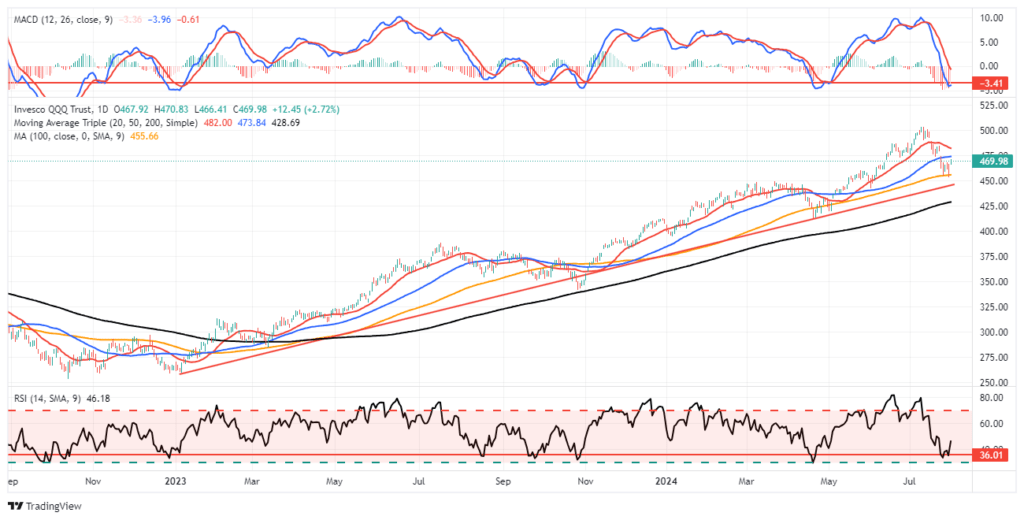

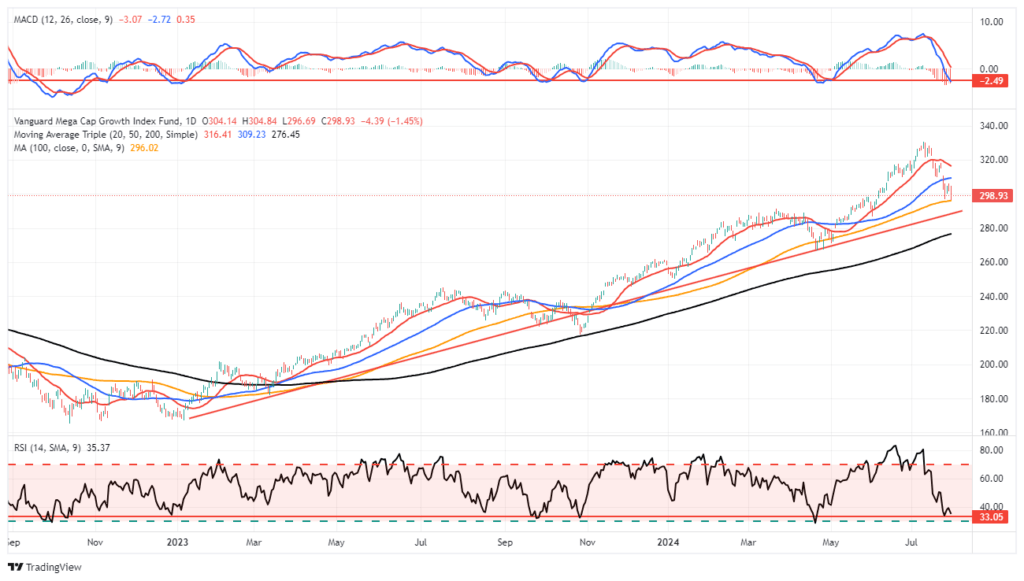

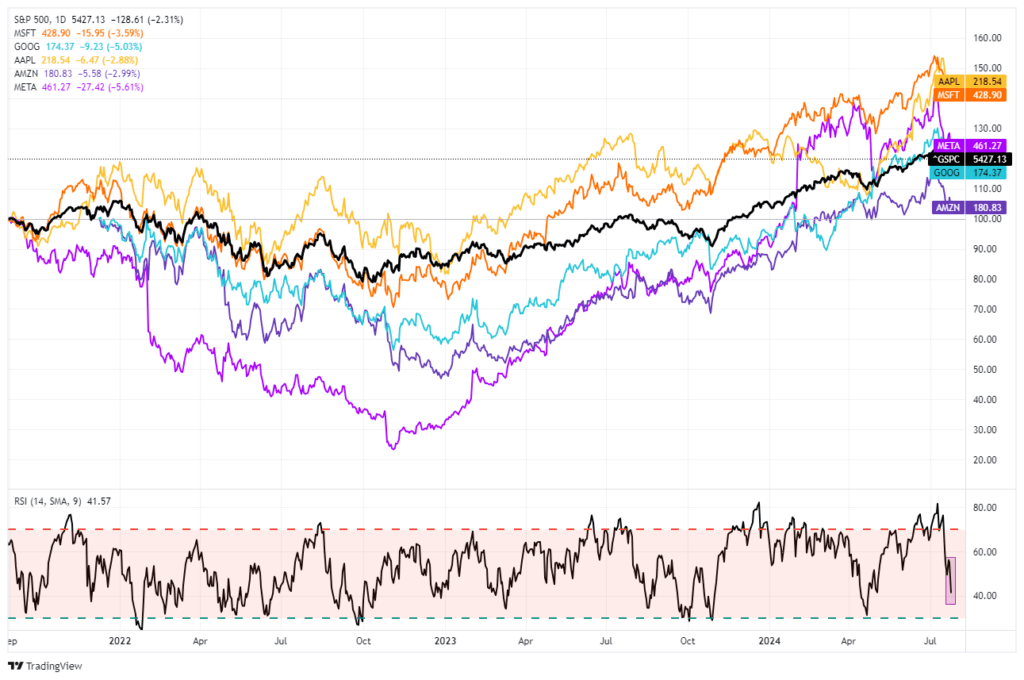

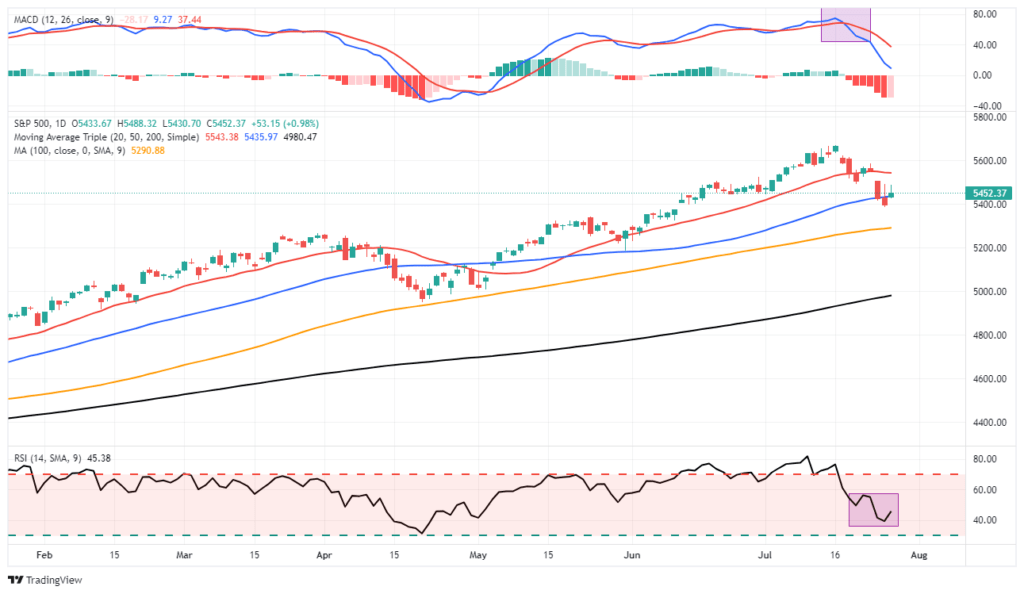

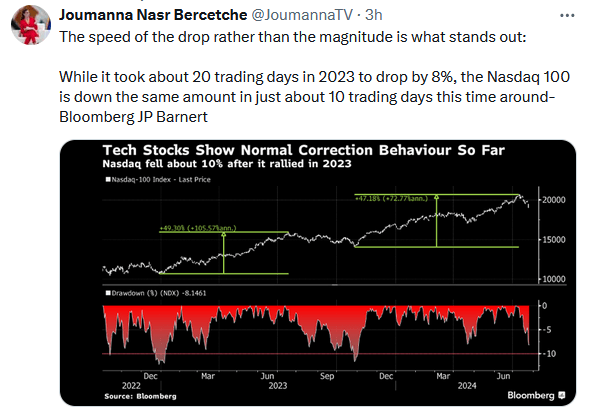

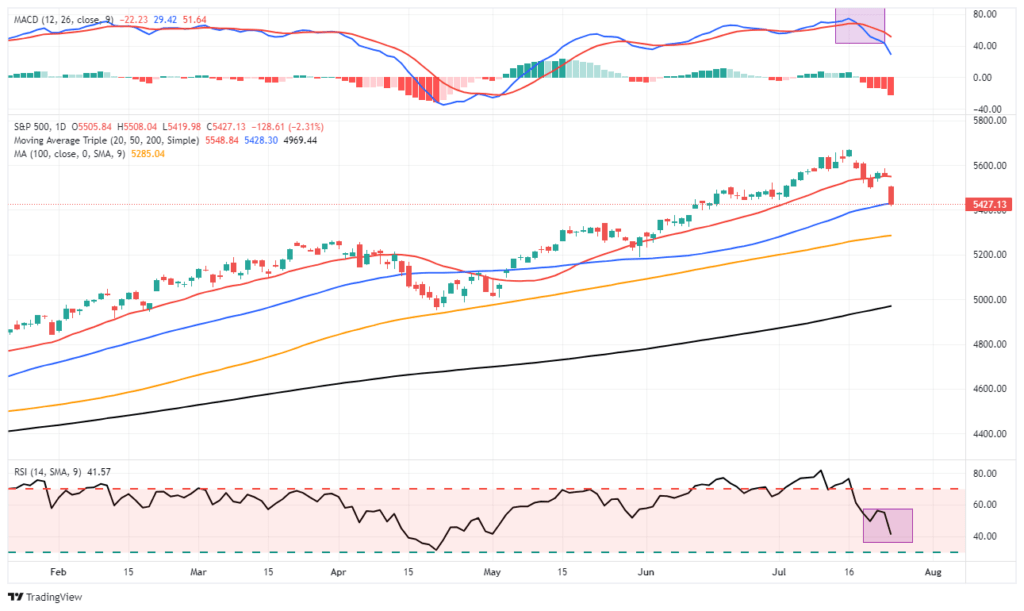

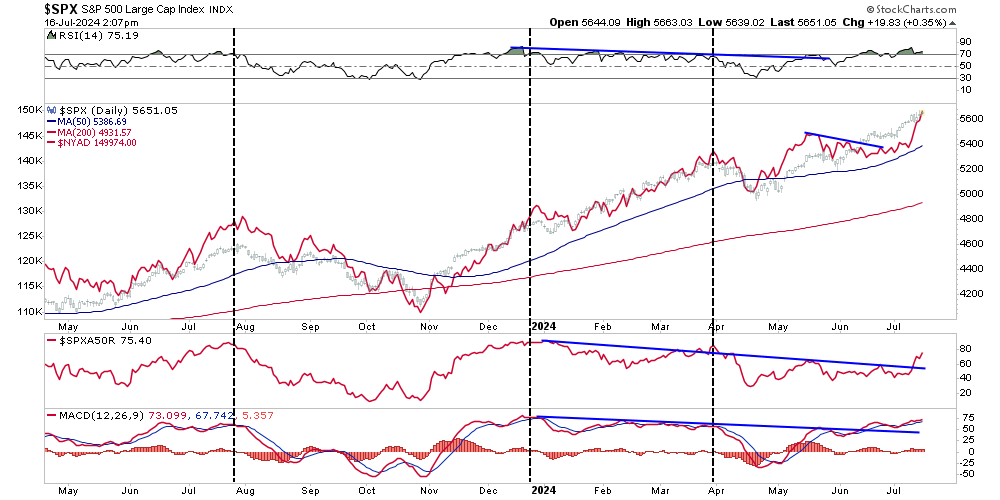

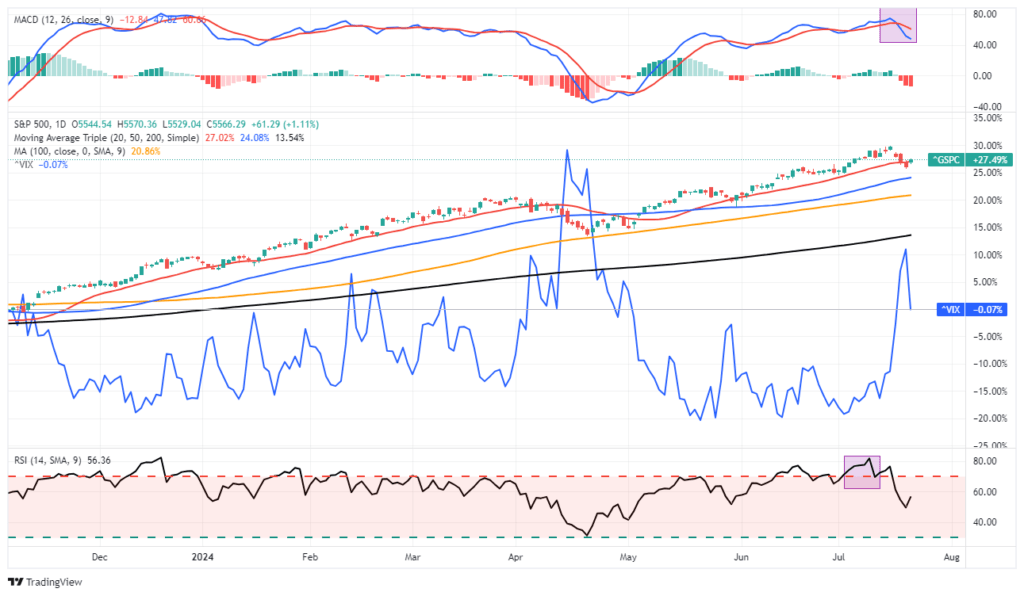

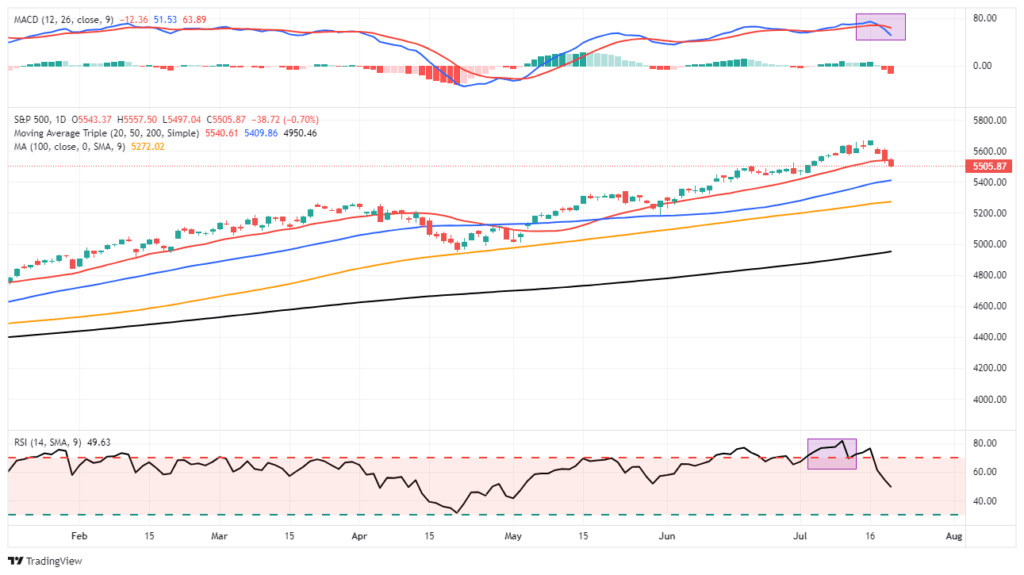

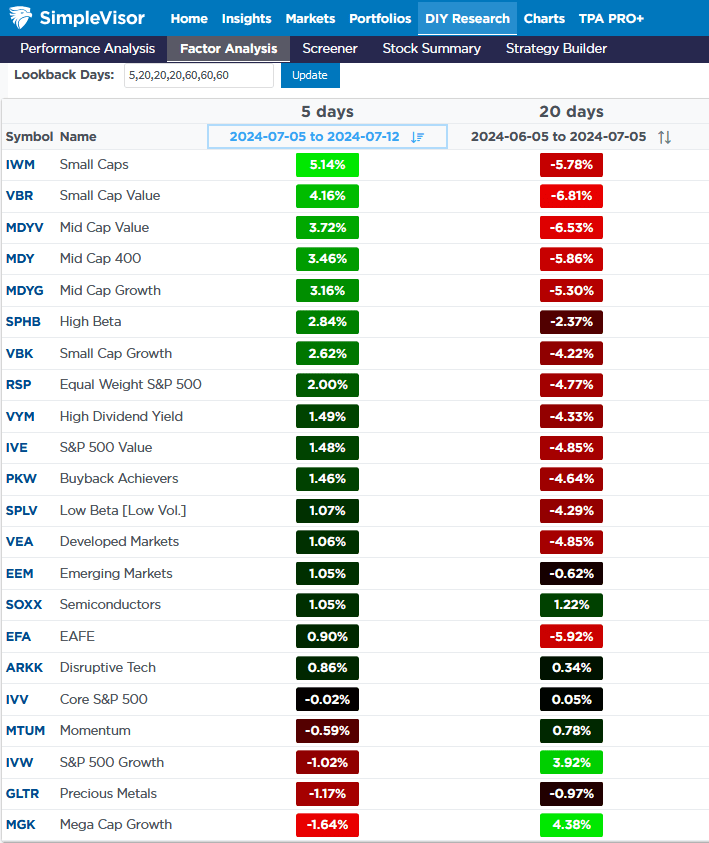

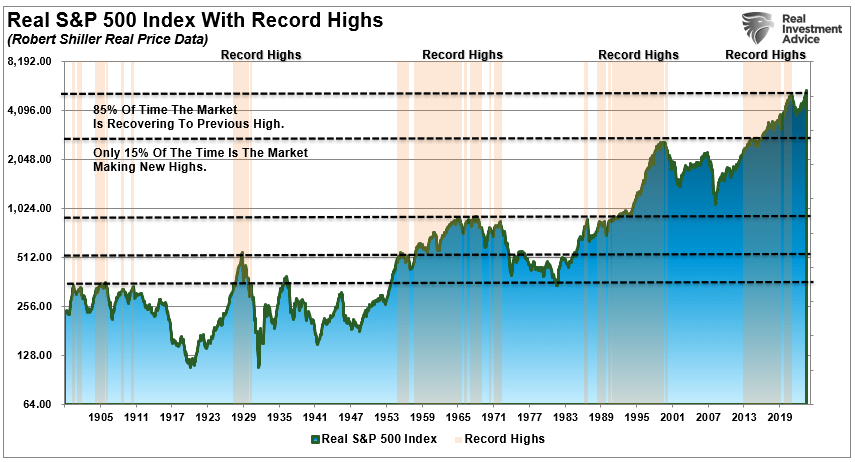

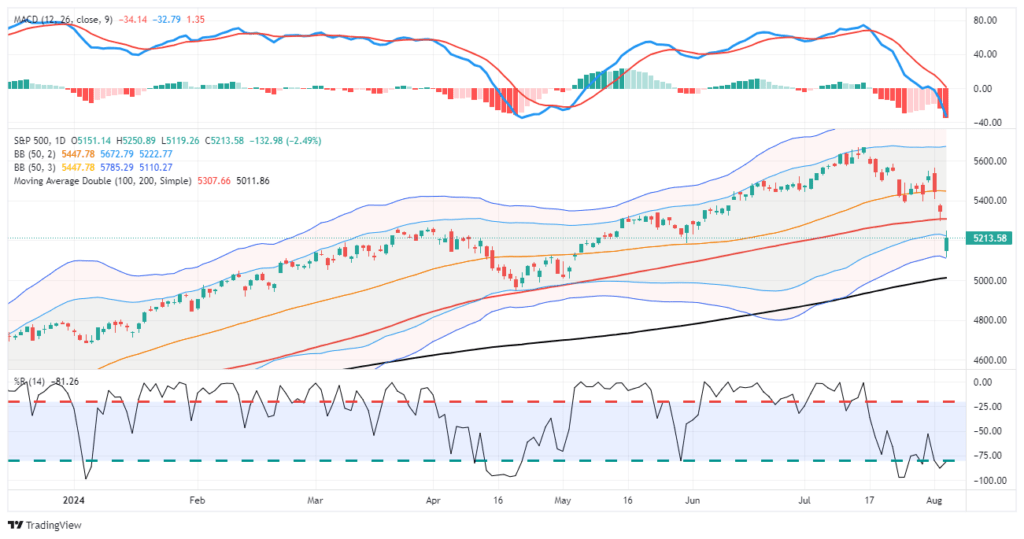

With the major markets deeply oversold short-term and sentiment becoming more bearish, it is quite likely the market will bounce over the next several days to a couple of weeks. However, as shown below, many investors were caught by the swiftness of the sell-off across all markets. These “trapped longs” will look for a rally to sell into, particularly in the more speculative areas of the market like small and mid-cap stocks, cryptocurrencies, and meme-stocks.

As shown, as of yesterday, the S&P 500 traded well into three (3) standard deviations below the 50-DMA. These more extreme and sharp declines are often met with buyers looking to “buy the dip.” However, with the market “gapping down” over the last couple of sessions, many of these “trapped longs” will look to exit closer to the 100-DMA. Following that, I would be unsurprised to see the market retest recent lows or decline further over the next month towards the 200-DMA.

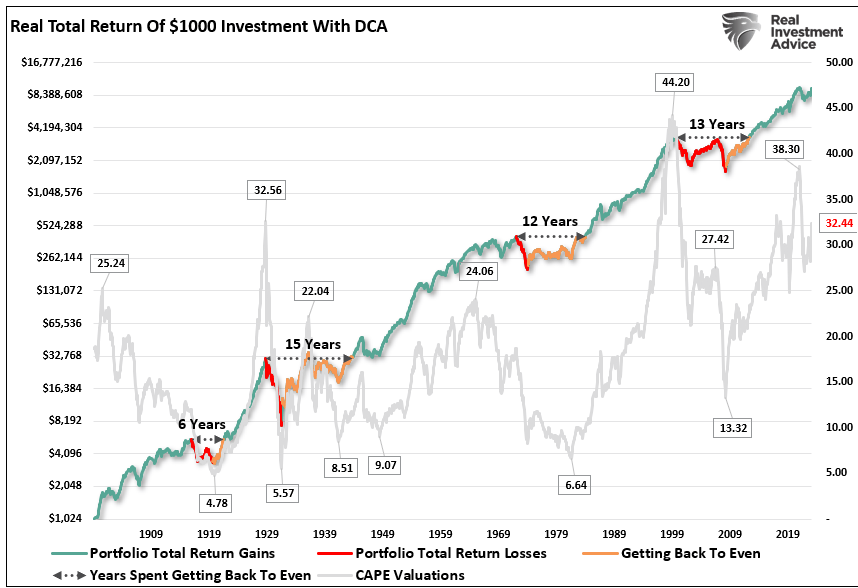

Crucially, this event will pass, and patient investors will be rewarded with an opportunity to acquire assets at discounted prices. Such is, in fact, the very essence of investing and the goal of “selling high and buying low.” However, we must survive the turmoil until the next buying opportunity arrives.

Navigating The Pullback

While the sell-off will certainly impair investor confidence, the demise of the “yen carry trade” is temporary. Wall Street has been using that strategy for the last 20 years. However, while expected, this decline could be with us for a while longer, particularly as the economy continues to show signs of slowing down. While the economy will likely avoid a “deep recession,” the odds of a “no landing scenario” are slim. Therefore, we should at least prepare for a slower earnings growth rate as economic activity recedes. The rules are simple but effective.

- Use near-term rallies to raise cash levels in portfolios.

- Reduce equity risk, particularly in areas highly dependent on economic growth.

- Add or increase the duration of bond allocations, which tend to offset risk during recessionary downturns.

- Reduce exposure to commodities and inflation trades as economic growth slows.

If the market declines further or a recession occurs, preparation allows you to survive the impact. Protecting capital will mean less time spent getting back to breakeven afterward. Alternatively, it is relatively easy to reallocate funds to equity risk if we avoid a recession and achieve a “soft landing.”

Other steps to take to ensure better portfolio outcomes are:

- Have excess emergency savings, so you are not “forced” to sell during a decline to meet obligations.

- Extend your time horizon to 5-7 years, as buying distressed stocks can get more distressed.

- Don’t obsessively check your portfolio.

- Consider tax-loss harvesting (selling stocks at a loss) to offset those losses against future gains.

- Stick to your investing discipline regardless of what happens.

However, if I am wrong and the bull market resumes, it is an easy process to reallocate cash to equities and rebalance portfolios for growth as needed,

Most importantly, follow your process and keep your emotions in check.