In a stunning reversal of opinion, ex. New York Fed Governor Bill Dudley now calls on the Fed to immediately cut rates. In a Bloomberg article titled I Changed My Mind. The Fed Needs To Cut Rates Now, he states:

“I’ve long been in the ‘higher for longer’ camp…The facts have changed, so I’ve changed my mind. The Fed should cut, preferably at next week’s policy-making meeting.…Although it might already be too late to fend off a recession

Like ourselves, Bill Dudley is noticing a degradation of important but lesser-followed labor market data. He notes that the household employment survey from the BLS shows the economy only added 195k jobs in the last year. Conversely, the well-followed BLS establishment survey shows gains of over 2.6 million jobs. He also justifies his decision with the core PCE prices data showing that inflation is nearing the Fed’s 2% target. He concludes as follows:

Although it might already be too late to fend off a recession by cutting rates, dawdling now unnecessarily increases the risk.

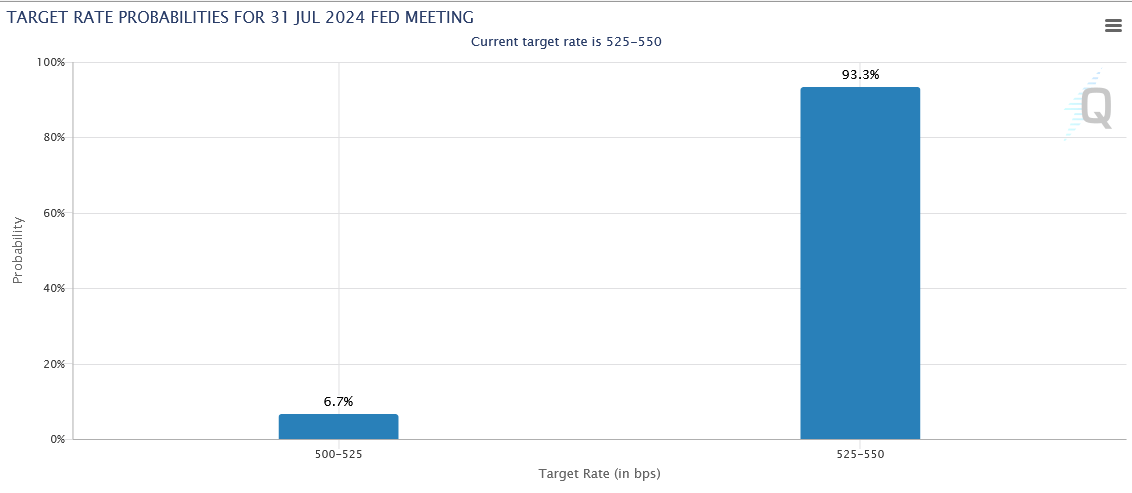

The next FOMC meeting is next Wednesday. As we share below the market, pricing in a slim 6.7% chance of a rate cut, does not agree with the logic of Bill Dudley.

What To Watch Today

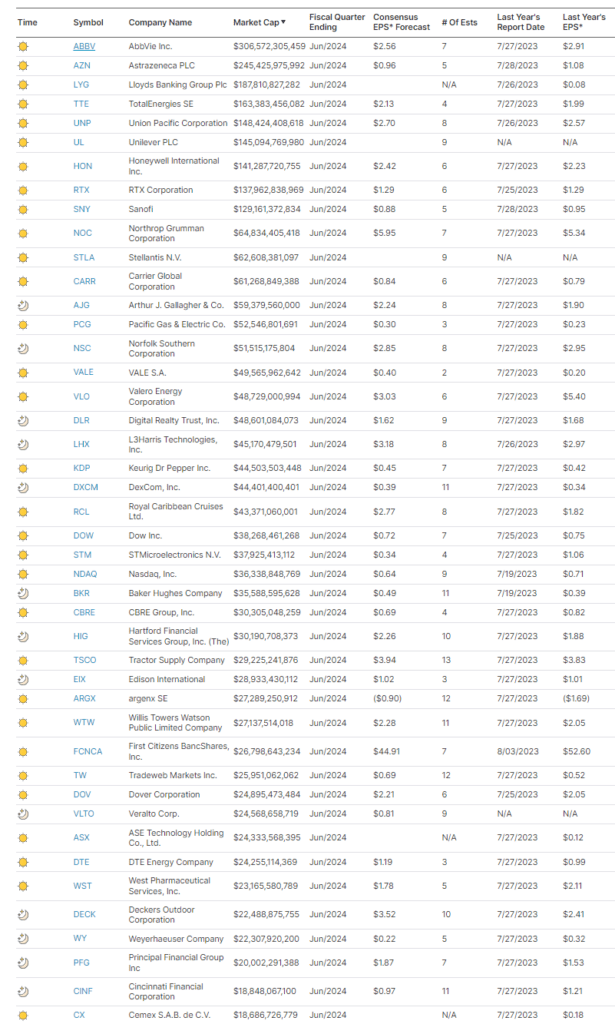

Earnings

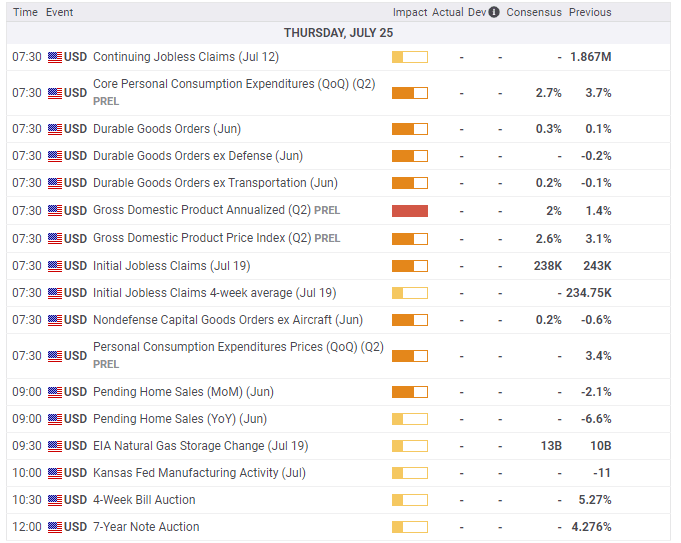

Economy

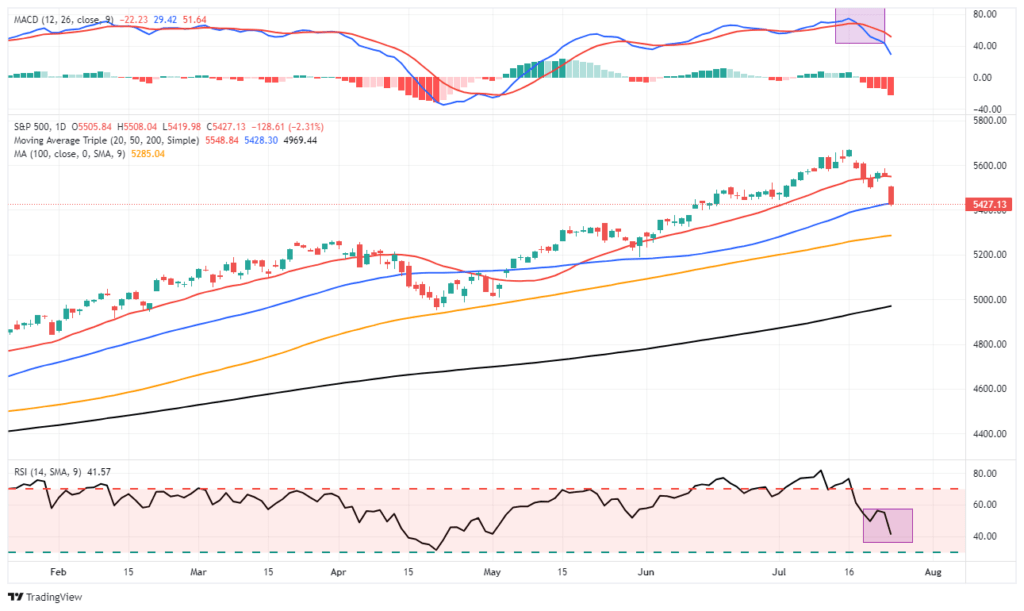

Market Trading Update

Yesterday, we discussed the average Presidential election year path for markets and the rules to follow to navigate this current corrective process. The correction that started last week continued yesterday despite good earnings and revenue numbers from Google (GOOG). Hence, with the market retesting and failing the 20-DMA, the 50-DMA becomes the next logical support.

So far, this correction is very close to what we saw in April. The market initially broke the 20-DMA, rallied above it, then failed and took out the 50-DMA, eventually finding support at the 100-DMA. If we replay that episode, the current correction will again encompass a roughly 5-7% decline from the previous peak. As of yesterday’s close, the market is testing the 50-DMA and is moving into more oversold conditions. The market needs to hold support here, or we will retest the 100-DMA once again, which we think is ultimately most likely.

That statement should be unsurprising, as we have repeatedly discussed the need for a 5-10% correction to resolve the overbought and extended conditions. While we have previously suggested that we though such a correction may occur later in the summer, we may be in the process now.

Manage your risks accordingly.

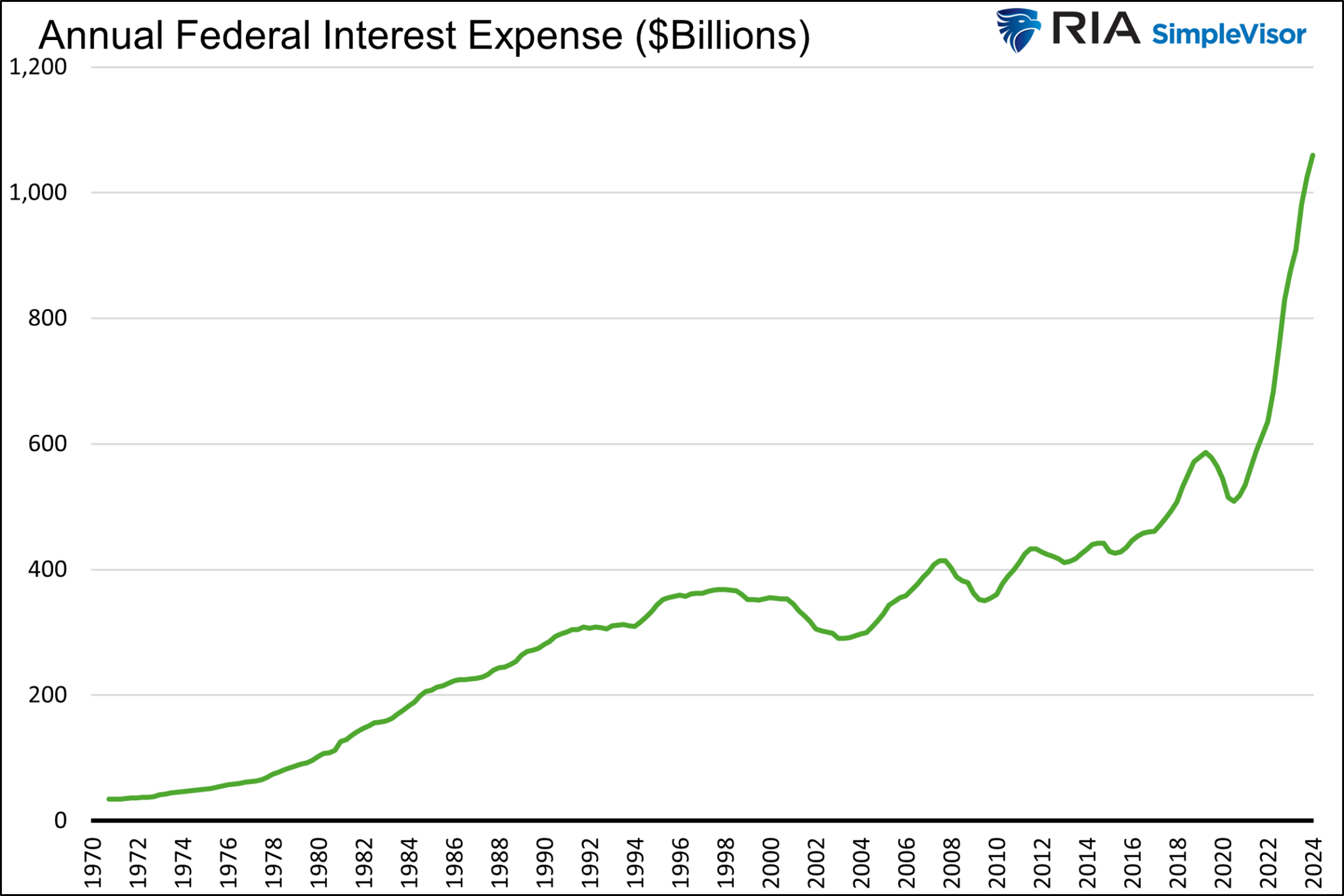

The Deficit Is Misleading

The federal deficit is massive and growing too rapidly. It is obscene, whether you measure it in absolute terms or as a percentage of GDP. This is one crucial factor that warrants concern for bond investors and keeps yields higher than they should be.

However, deficit analysis is complicated. Our latest article, Interest Rates Are Too High, helps ease some concerns about the deficit. It is essential to consider the effect of higher interest rates on the deficit and the circular relationship between rates and the deficit. Fears over high deficits keep interest rates high, which adds to deficit spending. To explain, consider the first graph below. It shows that over $500 billion of the recent annual deficit is solely a function of higher interest expenses. However, on the bright side, lower interest rates will lower government spending, easing bond investors’ concerns. As we wrote:

Assuming no significant changes to the rate of government spending, deficits will fluctuate with interest rates. Therefore, in a circular fashion, when interest rates fall, the market’s fear of fiscal deficits will likely lessen.

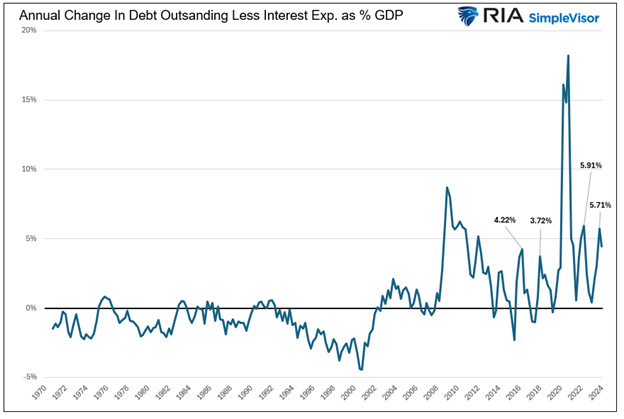

The second graph helps put context to the deficit sans interest expenses. To wit:

The graph below puts the deficit and interest expenses into context. It shows deficits, sans interest expenses, as a percentage of GDP. The recent peak, 5.71%, is historically high, but notice the deficit spending of the financial crisis and pandemic-related stimulus dwarf it. Further, last quarter’s peak is not far from the 2016 and 2018 highs when spending was not generally considered out of control.

Capital One Paints A Mixed Picture Of The Consumer

Capital One is a good barometer for the financial health of the average consumer as they are a large retail bank and credit card company. Its earnings report on Wednesday paints a mixed picture. Regarding consumer savings, Richard Fairbank, Capital One’s CEO, appears optimistic. To wit:

“When we look at our customers, we see that on average, they have higher bank balances than before the pandemic, and this is true across income levels….on the whole, I’d say consumers are in reasonably good shape relative to most historical benchmarks”

However, while consumers, at least those with Capital One Bank accounts, seem to have relatively substantial savings on average, Capital One’s credit card division is worried about growing losses. The following figures indicate they are building their financial buffer to protect against increasing credit card losses.

- Provision for credit losses increased $1.2 billion to $3.9 billion

- Net charge-offs of $2.6 billion

- $1.3 billion loan reserve build

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.