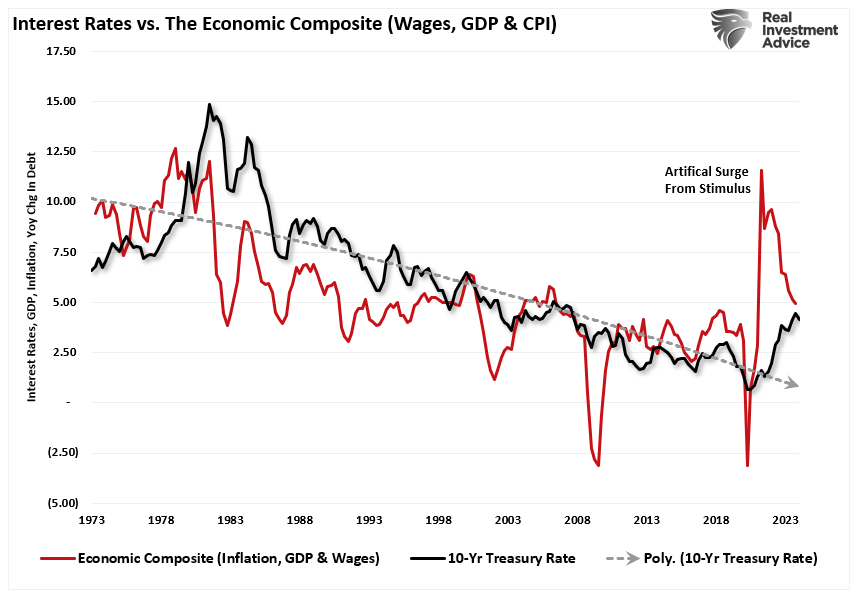

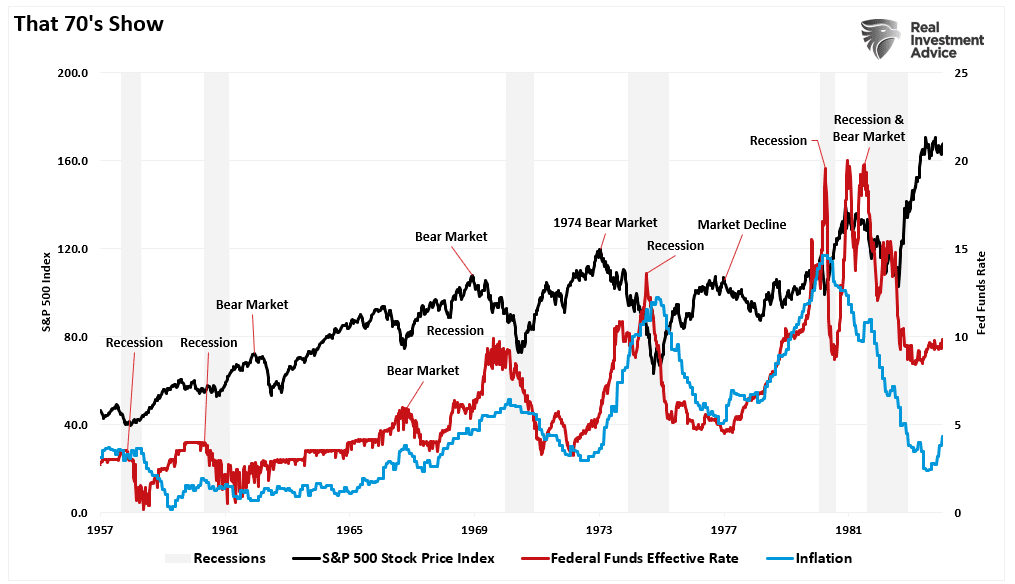

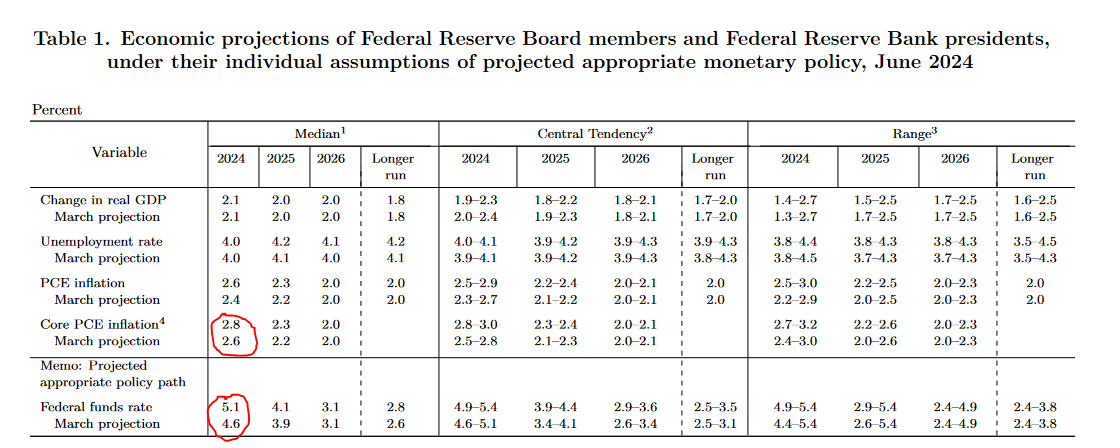

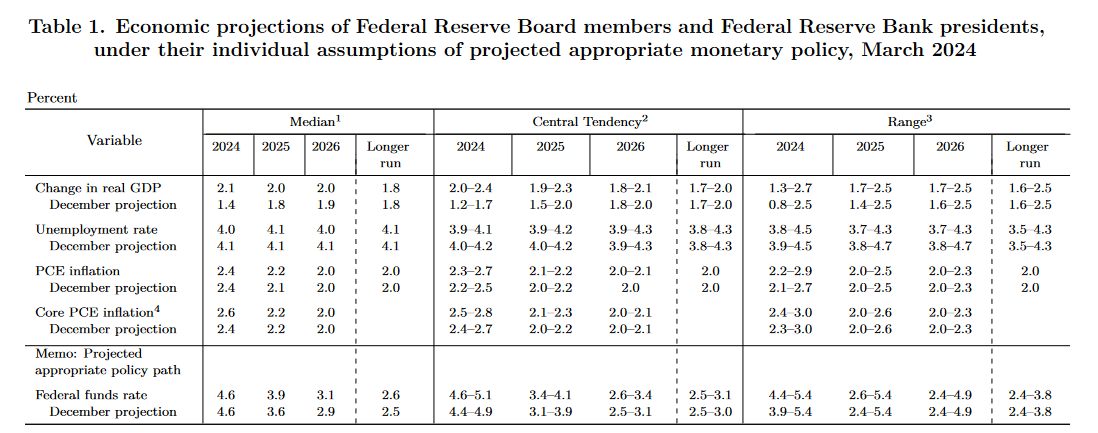

Let’s step back and ignore the last four years in which the economy cratered with the onset of the pandemic and then boomed on massive monetary and fiscal stimulus. Let’s also try to ignore the peak 6% core PCE inflation rate in 2022 and the historically low 3.4% unemployment rate in 2023. What if, in the years preceding the pandemic, we told you that in 2024, the Fed Funds rate would be 5.25-5.50%? You probably would have assumed inflation was at least 5% and the unemployment rate was exceptionally low.

The current unemployment rate is 4%, and the core PCE inflation rate is 2.6%. In December 2019, the unemployment rate was 3.6%, and the core PCE was 1.6%. At the time, Fed Funds were 1.5%. Here we sit today, with the unemployment rate .4% higher and core PCE 1% higher than in 2019. Yet, the Fed Funds rate is 4% more than in 2019. Does it seem a bit high? To help answer the question, consider the Fed’s long-term forecasts.

As we circle below, the Fed thinks the natural long-term unemployment rate is 4.2% and PCE 2.0%. Under such an outlook, the Fed believes Fed Funds should be 2.8%. While it’s hard to make a case for the Fed to cut rates today, a simple look at their two objectives, full employment and stable prices, and its long-term economic projections make one appreciate that the current Fed Funds rate is exceptionally high. Even if the economy continues to chug along without a recession, it appears that barring higher inflation, significant rate cuts in the coming year will be consistent with the Fed’s economic outlook.

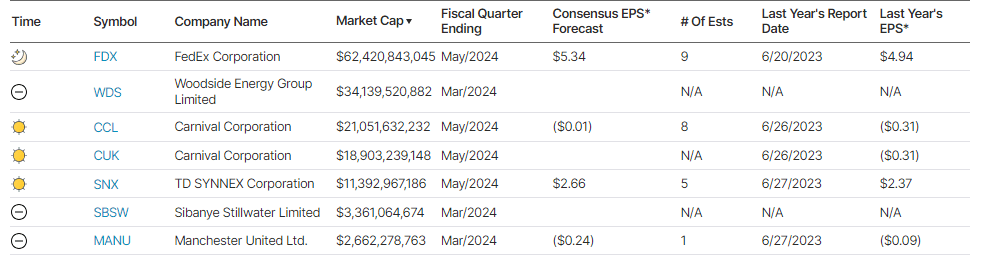

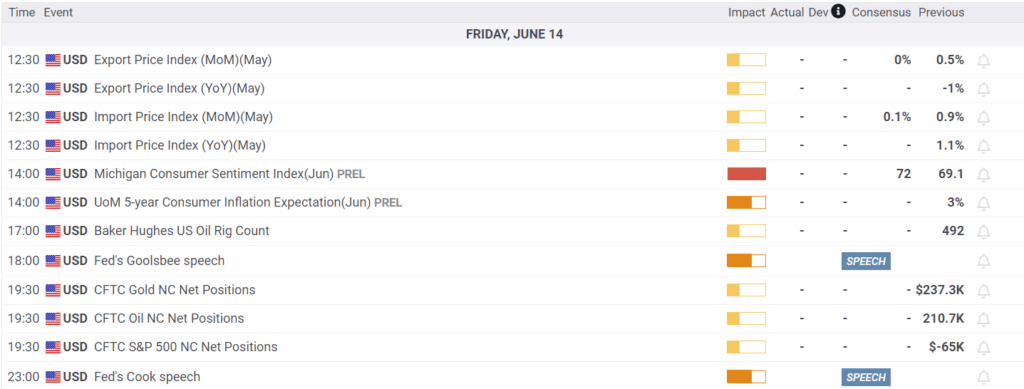

What To Watch Today

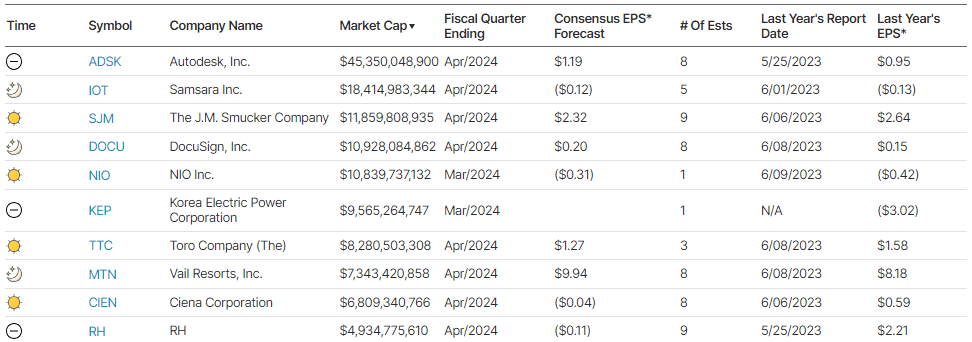

Earnings

No notable earnings releases today

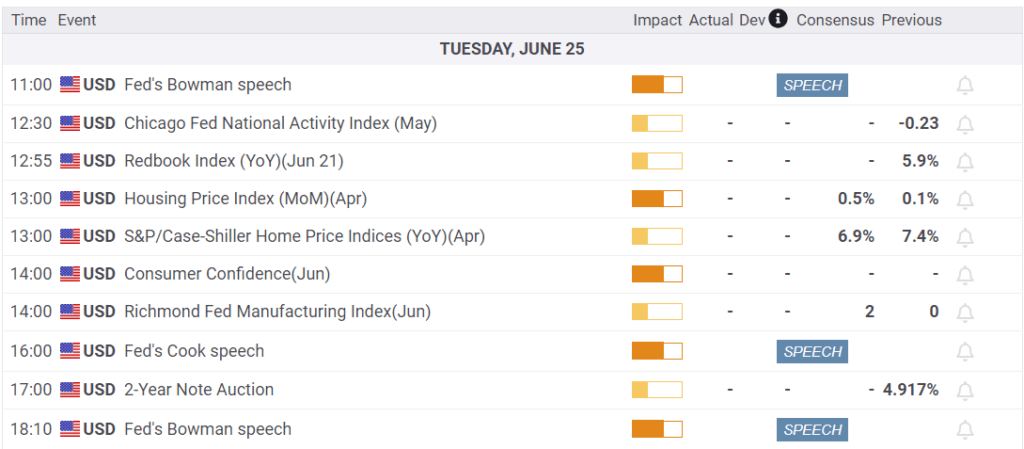

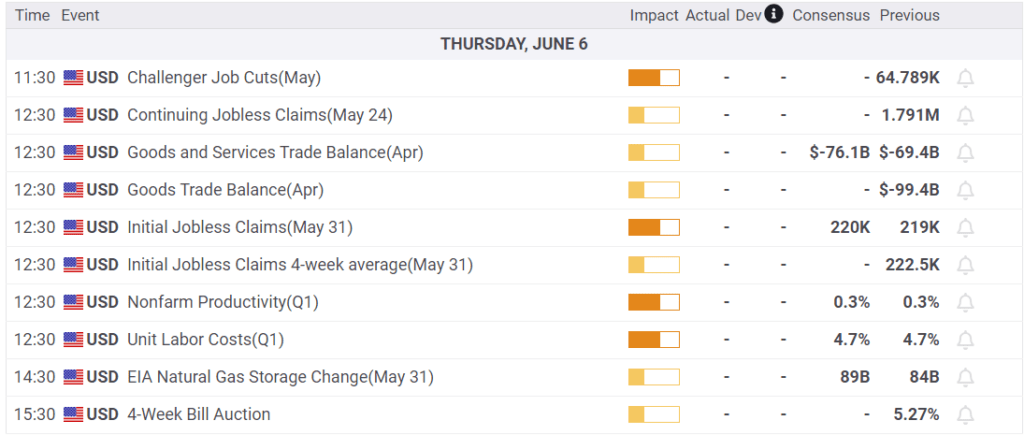

Economy

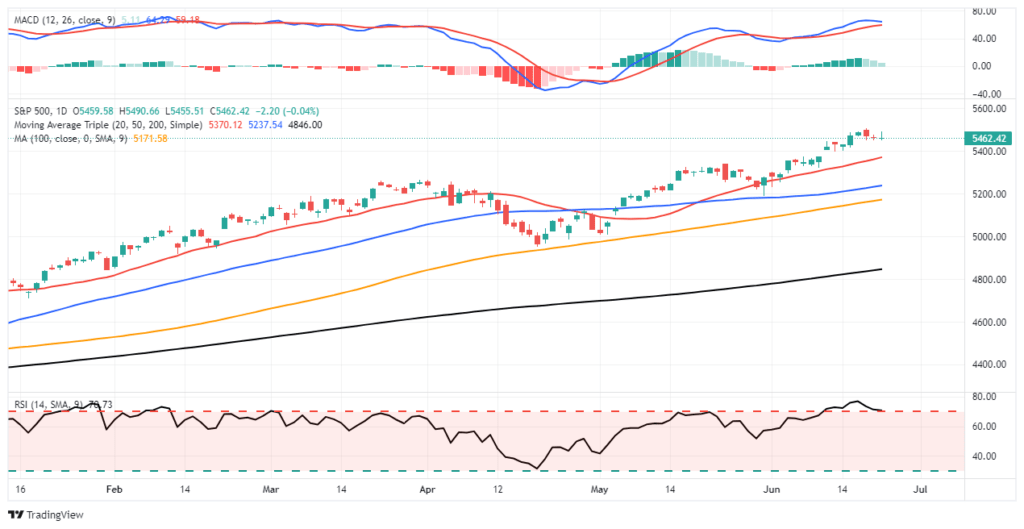

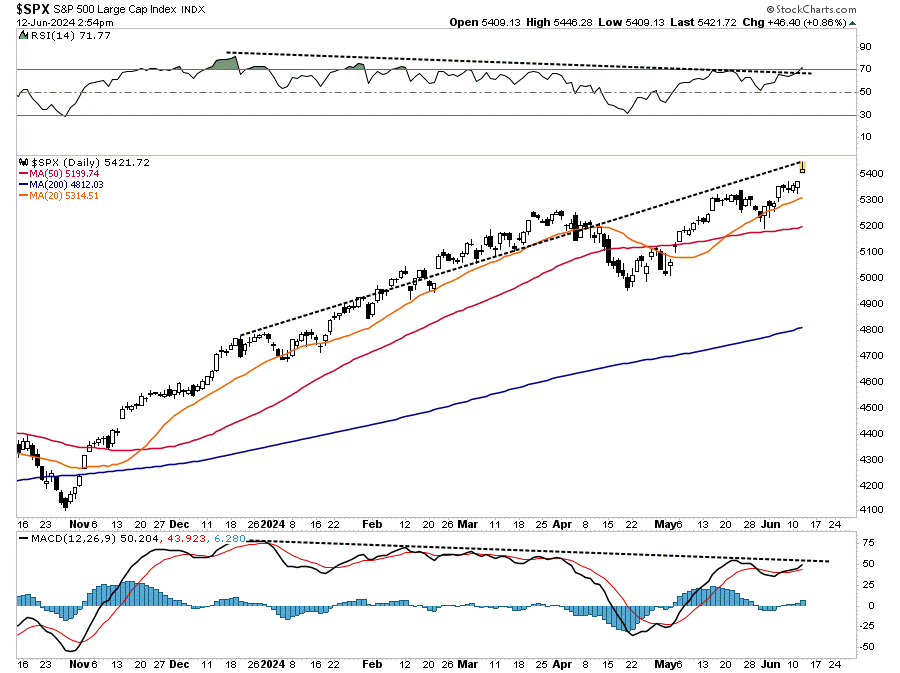

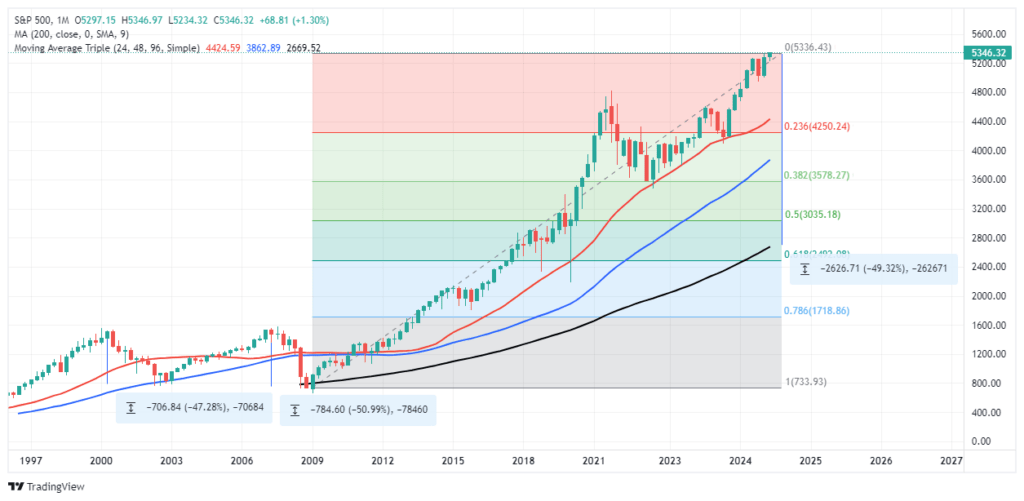

Market Trading Update

As discussed yesterday, this is the beginning of a new quarter, the end of the first half, and the beginning of the Q2 earnings season. We noted that with this holiday-shortened week, volatility could certainly pick up. Unsurprisingly, I received several emails about the sharp sell-off in long-date Treasury bond ETFs. As shown, bond ETFs had a sharp reversal due to end-of-quarter rebalancing and dividend distributions yesterday, temporarily suppressing the price. However, bonds had enjoyed a very nice rally and were overbought going into quarter-end, so the sell-off is unsurprising

The economic data continues to show economic deterioration, which is bond-supportive, so the recent selloff in bond ETFs is likely presenting a good buying opportunity for traders. The last time bonds approached this level of oversold conditions was in April and May before a decent rally occurred.

Economic Surprise Index

We have read articles warning of an imminent recession due to the low economic surprise index. While we rule nothing out, it’s best to appreciate what the index tells us. Surprise indexes measure specific economic data forecasts versus the actual data. When the surprise index declines, it simply means that economic forecasters are generally overly optimistic. Hence, economic data is weaker than expected. Initially, that typically means the economy is slowing. However, economists are quick to adjust their forecasts for trend changes. Once this occurs, data may still deteriorate, but economists’ forecasts tend to be closer to reality or often overly pessimistic. Frequently, the surprise index will rebound. However, that doesnt mean the economy is improving, it only means forecasts are more realistic.

As shown below, the surprise index tends to oscillate. Low readings can precede a recession, but they occur with enough frequency they often prove to be a false alarm.

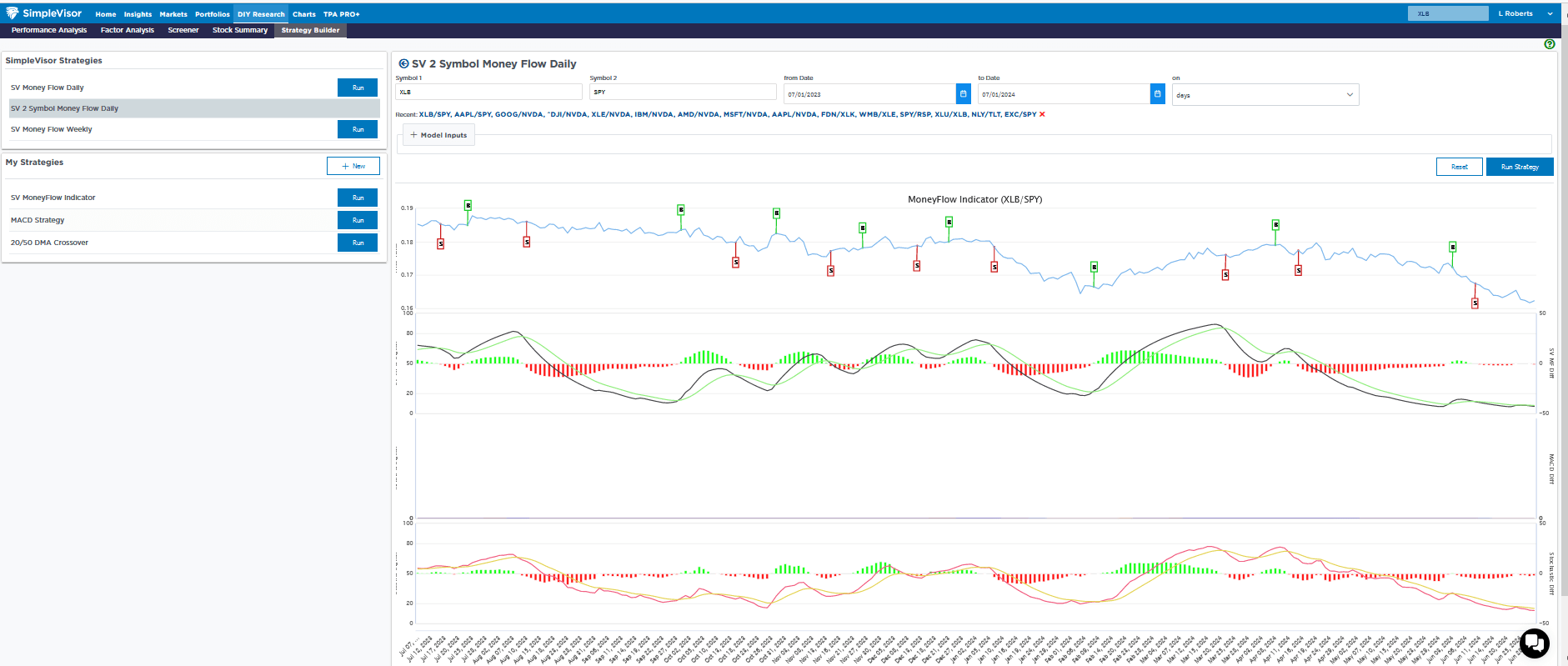

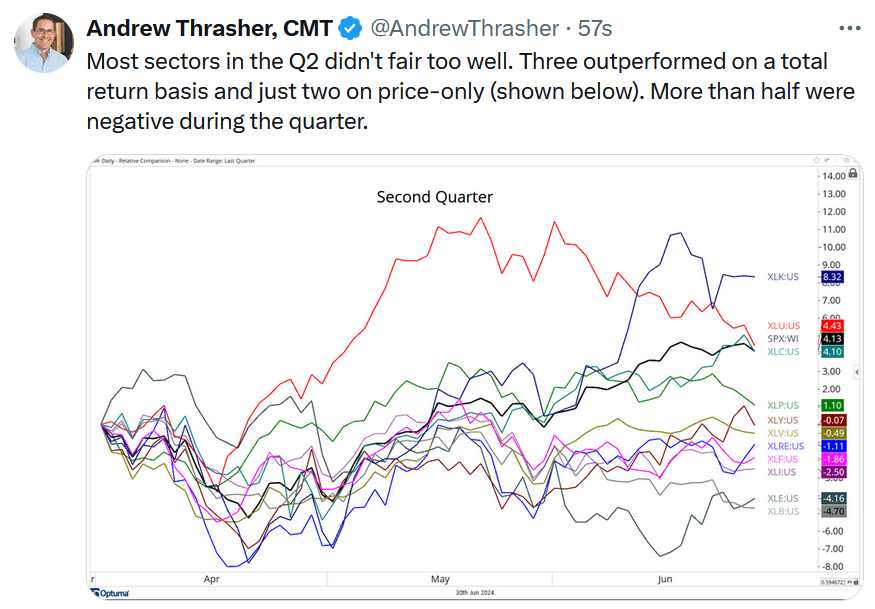

Sector Review- Materials Continue to Struggle

Over the last four weeks, the materials sector (XLB) has slipped by nearly 5% versus the S&P 500. Other than utilities, which are 6.5% worse than the S&P 500, it is the worst-performing sector over that period. Energy, which had the lowest relative SimpleVisor score for a few weeks running, was the market’s best-performing sector last week.

The second table, courtesy of SimpleVisor, shows the performance of each sector over consecutive periods ranging from the last five days to 20 and 60-day increments.

The third graph shows the price ratio of XLB to SPY. Other than XLB’s outperformance in the first quarter of 2024, XLB has been weak on a relative basis.

Some may say that the weakness in materials stocks is a telling signal about the state of the economy. We would counter, claiming that the service sector accounts for three-quarters of economic activity. The manufacturing sector has been in a recession for about two years, yet economic growth has been above average.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

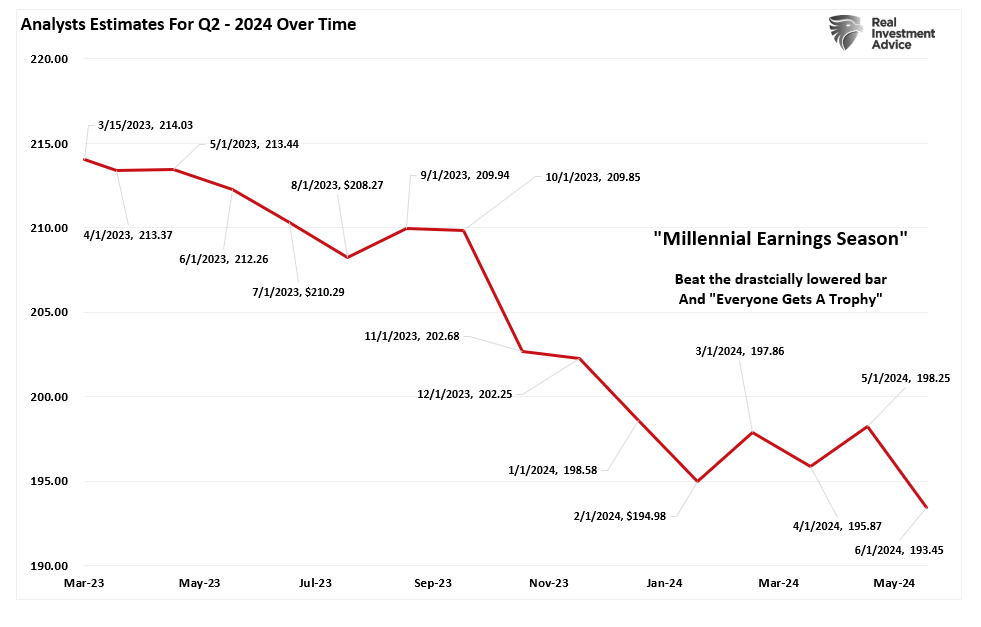

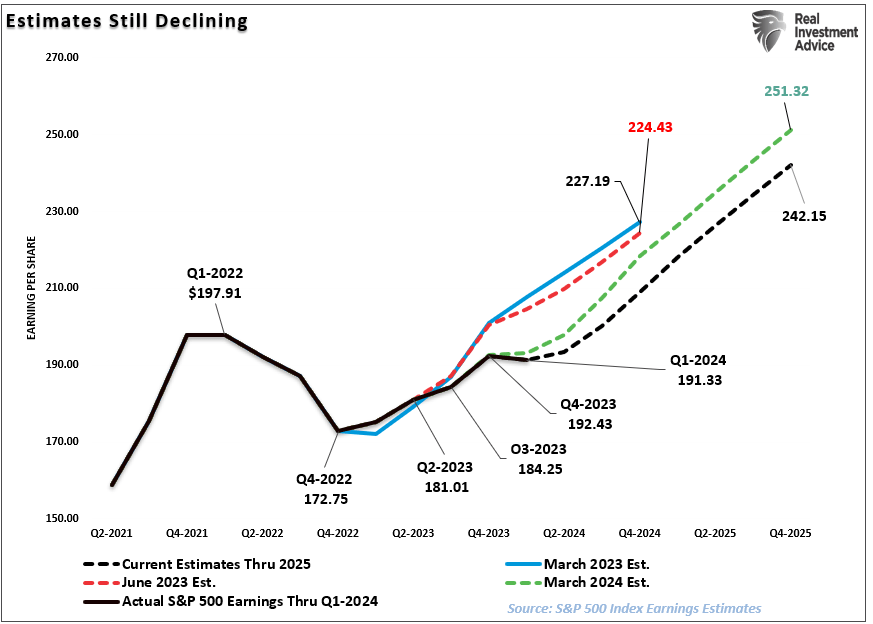

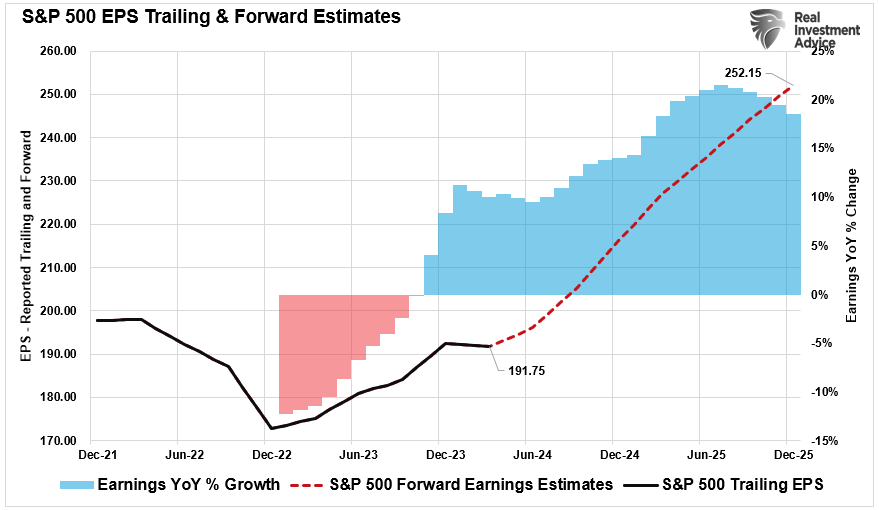

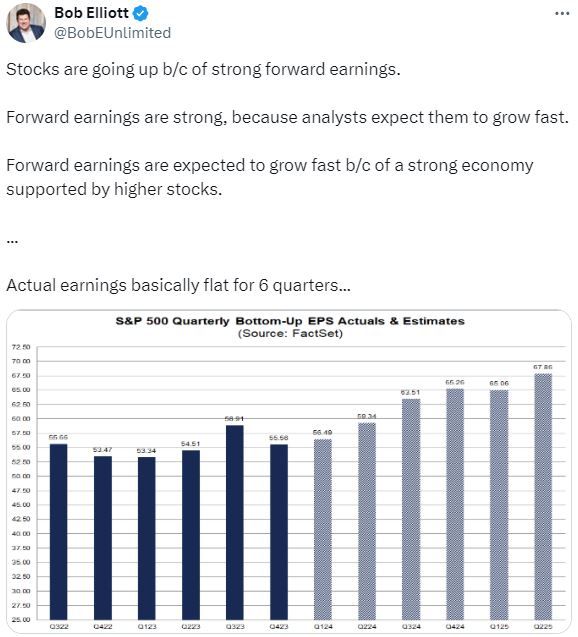

Earnings Bar Lowered As Q2 Reports Begin

Wall Street analysts continue significantly lowering the earnings bar as we enter the Q2 reporting period. Even as analysts lower that earnings bar, stocks have rallied sharply over the last few months.

As we have discussed previously, it will be unsurprising that we will see a high percentage of companies “beat” Wall Street estimates. Of course, the high beat rate is always the case due to the sharp downward revisions in analysts’ estimates as the reporting period begins. The chart below shows the changes for the Q2 earnings period from when analysts provided their first estimates in March 2023. Analysts have slashed estimates over the last 30 days, dropping estimates by roughly $5/share.

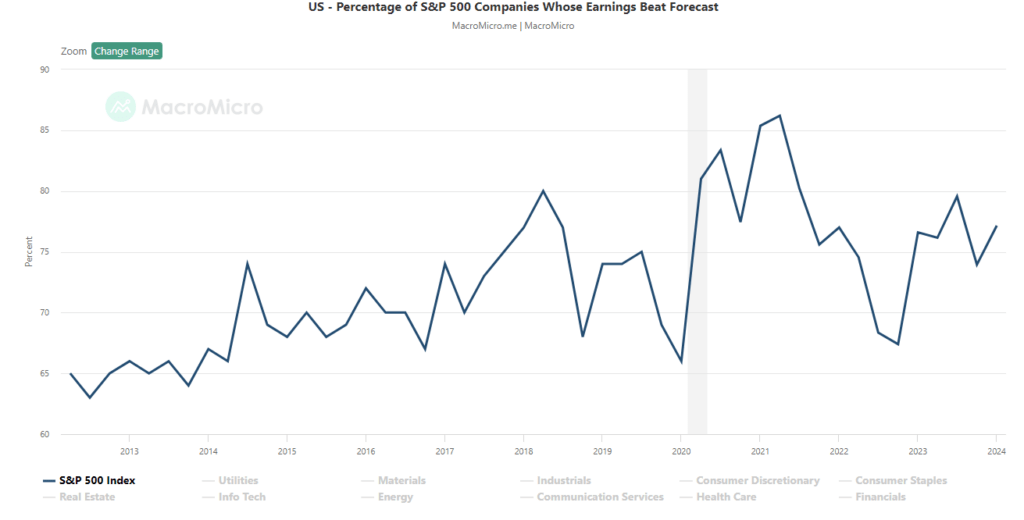

That is why we call it “Millennial Earnings Season.” Wall Street continuously lowers estimates as the reporting period approaches so “everyone gets a trophy.” An easy way to see this is the number of companies beating estimates each quarter, regardless of economic and financial conditions. Since 2000, roughly 70% of companies regularly beat estimates by 5%, but since 2017, that average has risen to approximately 75%. Again, that “beat rate” would be substantially lower if investors held analysts to their original estimates.

Analysts remain optimistic about earnings even with economic growth weakening, inflation remaining elevated, and liquidity declining. However, despite the decline in Q2 earnings estimates, analysts still believe that the first quarter of 2023 marked the bottom for the earnings decline. Again, this is despite the Fed rate hikes and tighter bank lending standards that will act to slow economic growth.

However, between March and June of this year, analysts cut forward expectations for 2025 by roughly $9/share.

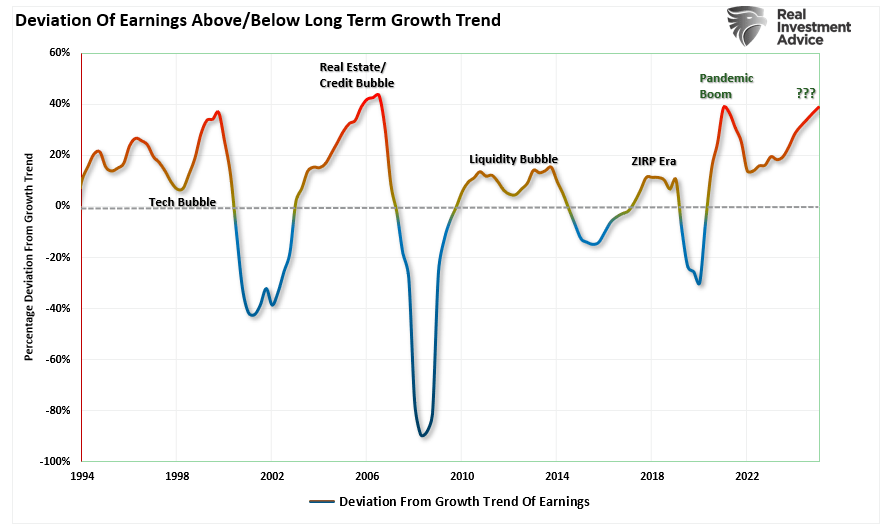

However, even with the earnings bar lowered going forward, earnings estimates remain detached from the long-term growth trend.

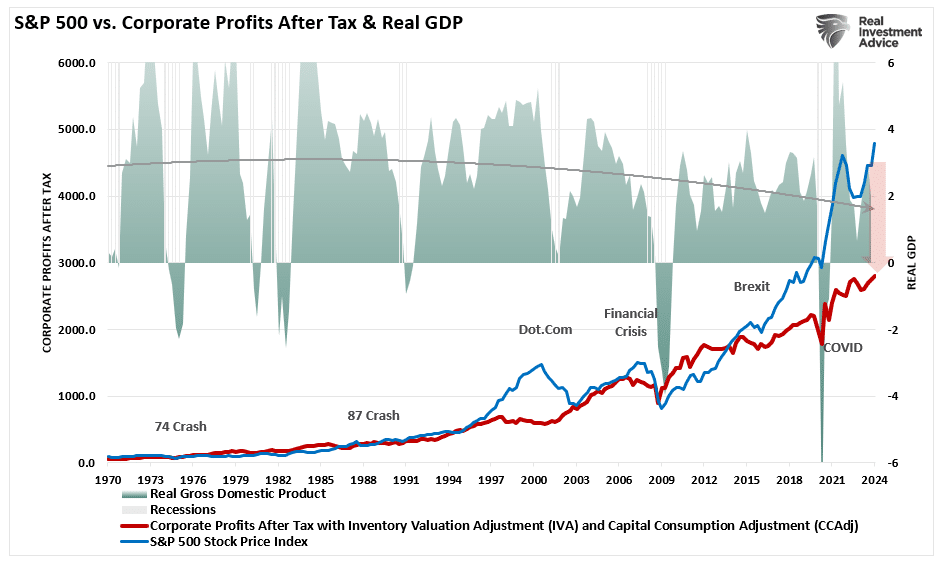

As discussed previously, economic growth, from which companies derive revenue and earnings, must also strongly grow for earnings to grow at such an expected pace.

Since 1947, earnings per share have grown at 7.72%, while the economy has expanded by 6.35% annually. That close relationship in growth rates is logical, given the significant role that consumer spending has in the GDP equation. However, while nominal stock prices have averaged 9.35% (including dividends), reversions to underlying economic growth will eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports. The same goes for corporate profits, where stock prices have significantly deviated.

Such is essential to investors due to the coming impact on “valuations.”

Given current economic assessments from Wall Street to the Federal Reserve, strong growth rates are unlikely. The data also suggest a reversion to the mean is entirely possible.

The Reversion To The Mean

Following the pandemic-driven surge in monetary policy and a shuttering of the economy, the economy is slowly returning to normal. Of course, normal may seem very different compared to the economic activity we have witnessed over the last several years. Numerous factors at play support the idea of weaker economic growth rates and, subsequently, weaker earnings over the next few years.

The economy is returning to a slow growth environment with a risk of recession.

Inflation is falling, meaning less pricing power for corporations.

No artificial stimulus to support demand.

Over the last three years, the pull forward of consumption will now drag on future demand.

“We have previously noted an inherent problem with ongoing monetary interventions. Notably, the fiscal policies implemented post the pandemic-driven economic shutdown created a surge in demand and unprecedented corporate earnings.”

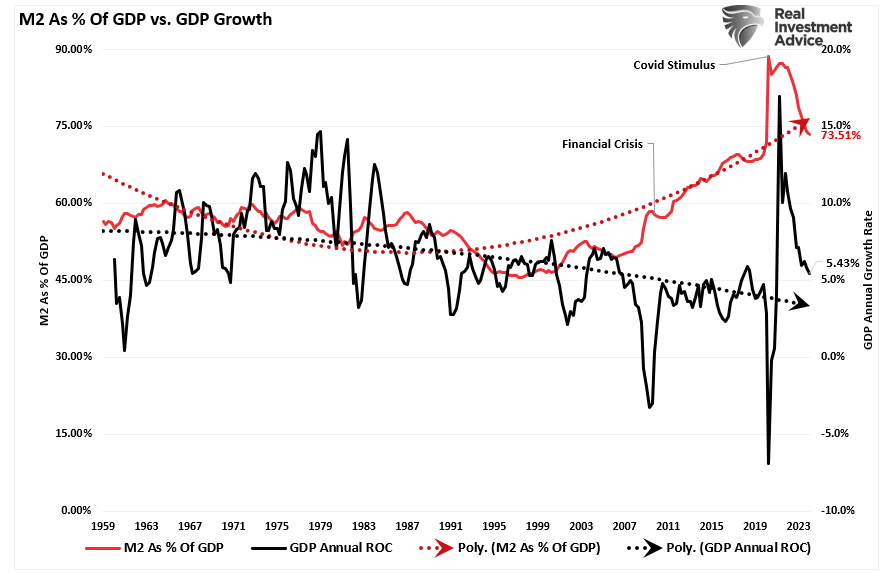

As shown below, the surge in the M2 money supply is over. Without further stimulus, economic growth will revert to more sustainable and lower levels.

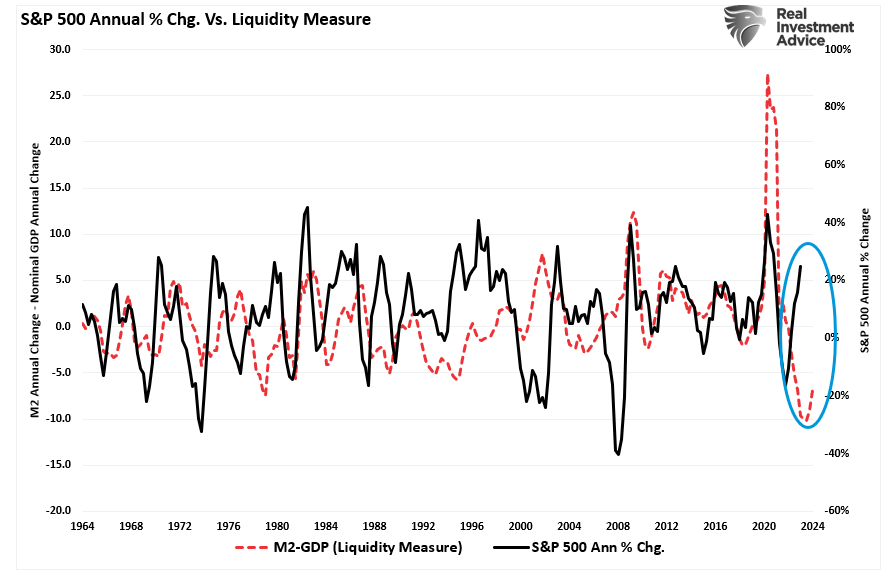

While the media often states that “stocks are not the economy,” as noted, economic activity creates corporate revenues and earnings. As such, stocks can not grow faster than the economy over long periods. A decent correlation exists between the expansion and contraction of M2 less GDP growth (a measure of liquidity excess) and the annual rate of change in the S&P 500 index. Currently, the deviation seems unsustainable. More notably, the current percentage annual change in the S&P 500 is approaching levels that have preceded a reversal of that growth rate.

So, either the annualized rate of return from the S&P 500 will decline due to repricing the market for lower-than-expected earnings growth rates, or the liquidity measure is about to turn sharply higher.

Valuations Remain A Risk

The problem with Wall Street consistently lowering the earnings bar by reducing forward estimates should be obvious. Given that Wall Street touts forward earnings estimates, investors overpay for investments. As should be obvious, overpaying for an investment today leads to lower future returns.

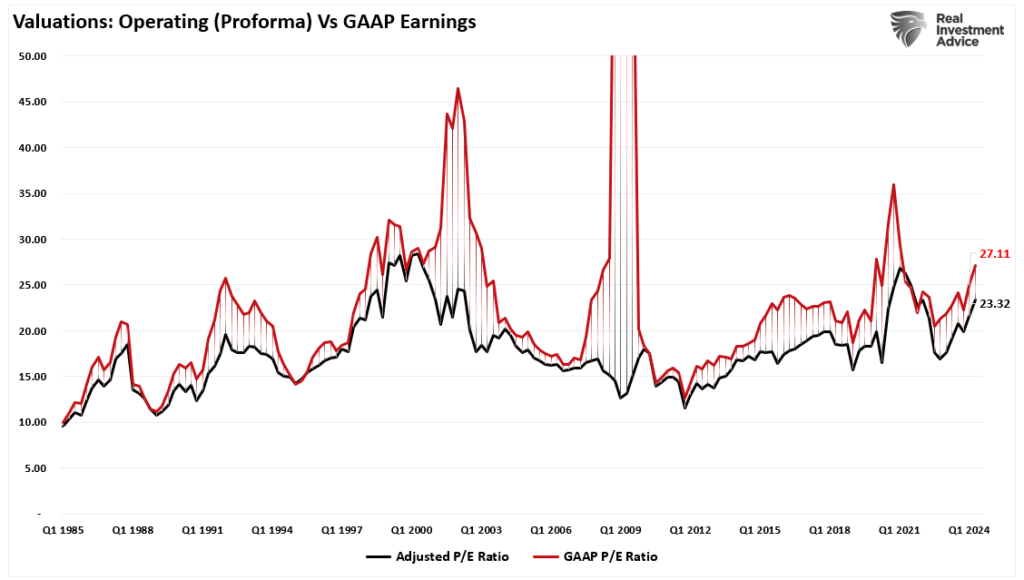

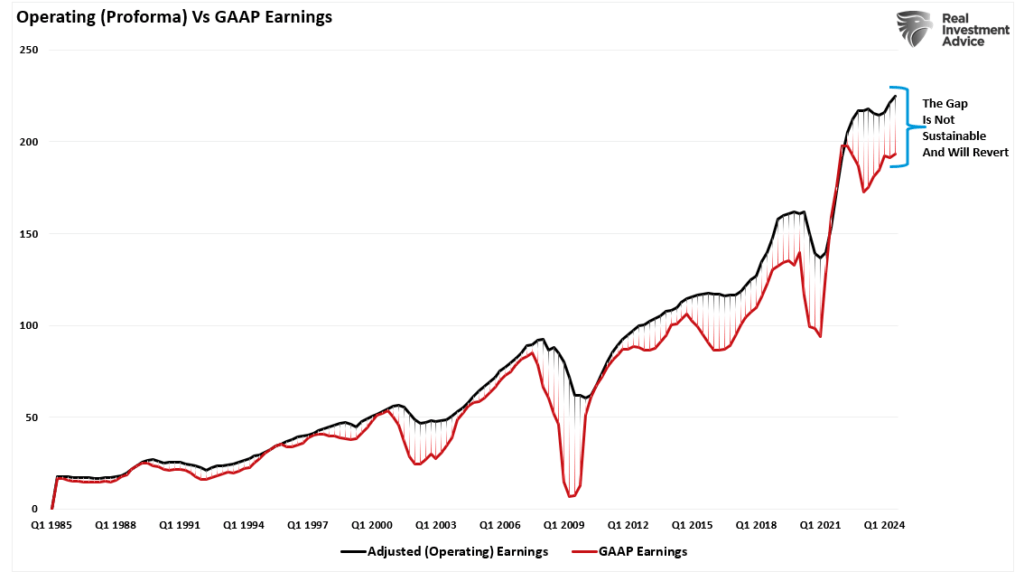

Even with the decline in earnings from the peak, valuations remain historically expensive on both a trailing and forward basis. (Notice the significant divergences in valuations during recessionary periods as adjusted earnings do NOT reflect what is occurring with actual earnings.)

Most companies report “operating” earnings, which obfuscate profitability by excluding all the “bad stuff.” A significant divergence exists between operating (or adjusted) and GAAP earnings. When such a wide gap exists, you must question the “quality” of those earnings.

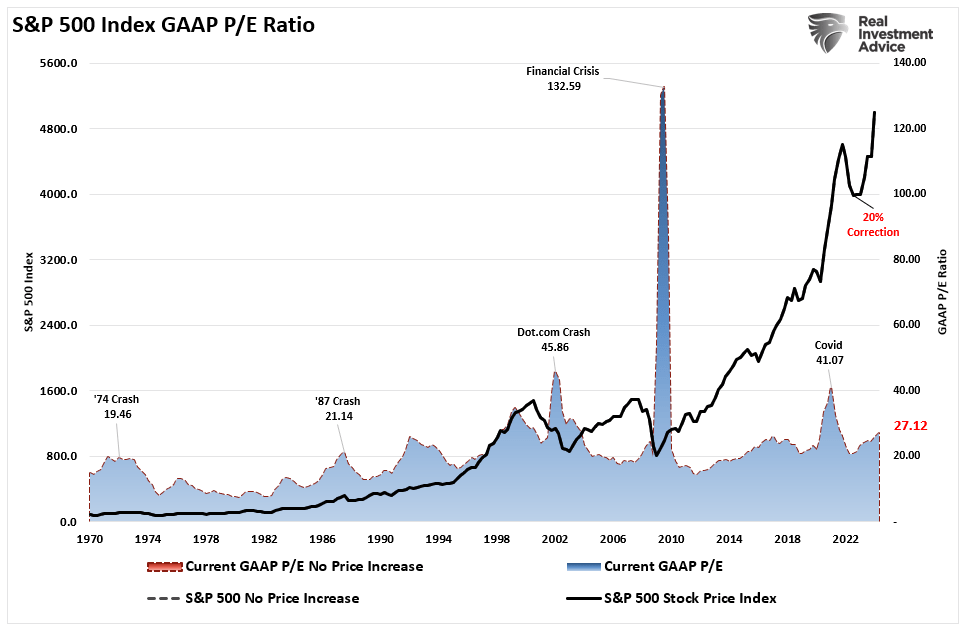

The chart below uses GAAP earnings. If we assume current earnings are correct, then such leaves the market trading above 27x earnings. (That valuation level remains near previous bull market peak valuations.)

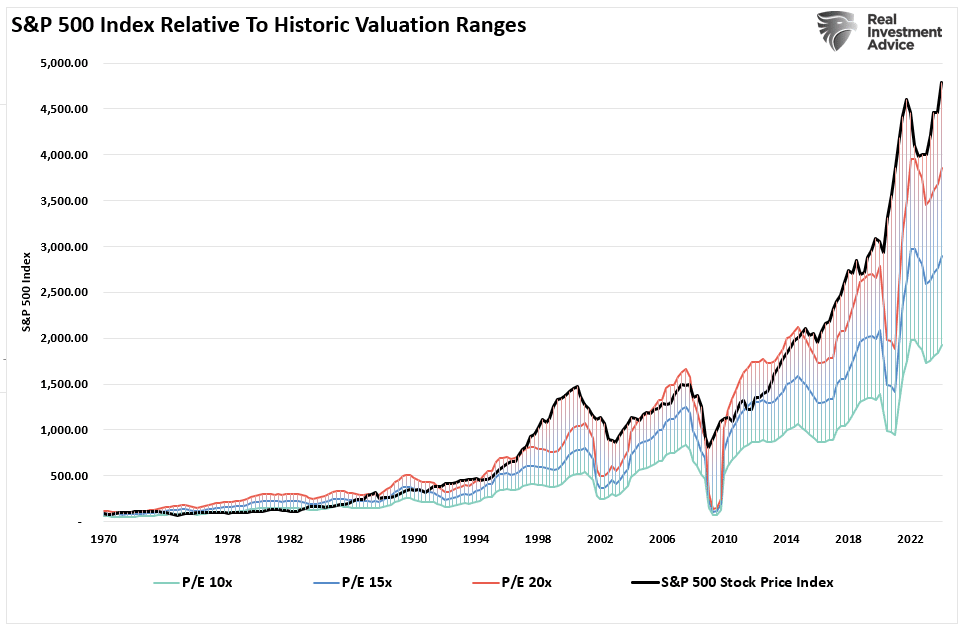

Since markets are already trading well above historical valuation ranges, this suggests that outcomes will likely not be as “bullish” as many currently expect. Such is particularly the case if more monetary accommodations from the Federal Reserve and the Government are absent.

Trojan Horses

As always, the hope is that Q2 earnings and the entire coming year’s reports will rise to justify the market’s overvaluation. However, when earnings are rising, so are the markets.

Most importantly, analysts have a long and sordid history of being overly bullish on growth expectations, which fall short. Such is particularly the case today. Much of the economic and earnings growth was not organic. Instead, it was from the flood of stimulus into the economy, which is now evaporating.

Overpaying for assets has never worked out well for investors.

With the Federal Reserve intent on slowing economic growth to quell inflation, it is only logical that earnings will decline. If this is the case, prices must accommodate lower earnings by reducing current valuation multiples.

When it comes to analysts’ estimates, always remain wary of “Greeks bearing gifts.”

Supercore PCE Is The Weakest Since August

Jerome Powell and his Fed colleagues breathed a sigh of relief Friday morning as the PCE inflation report was weaker than expected. The headline PCE price index was +0.0% versus expectations of a 0.1% increase and a previous monthly change of +0.3%. The Core PCE was +0.1%, also a tenth below expectations. Recent inflation data provides hope that the trend lower in inflation will resume after stalling out for about six months. Further encouraging is the newly popular Supercore PCE reading, a subset of inflation, which was only up 0.1%. This index surged by 0.8% in January, causing the Fed and the market to reduce their expectations for a Fed rate. This report provides further evidence that the instance was a one-time spike and not likely a trend reversal.

Supercore prices, accounting for roughly 50% of PCE, include the prices of core services, excluding housing. The Fed has mentioned Supercore PCE on numerous occasions. Their rationale for following it is that many of the categories in the Supercore calculation are labor-intensive sectors. Therefore, Supercore PCE is a decent indicator of tightness in the labor markets, which can impact wages and, ultimately, inflation. The graphs below, courtesy of ZeroHedge, break out Supercore by its components. If it weren’t for health insurance, Supercore PCE would have been negative. Five of the eight components are negative, with one at essentially zero and two (healthcare and food service/accommodations) positive.

What To Watch Today

Earnings

No notable reports today.

Economy

Market Trading Update

Last week, we did an in-depth discussion of the worsening breadth of the market. However, the important point was that investors make two mistakes regarding such data. To wit:

“The first is overreacting to these technical signals, thinking a more severe correction is coming. The second is taking action too soon.

Yes, these signals often precede corrections, but there are also periods of consolidation when the market trades sideways. Secondly, reversals of overbought conditions tend to be shallow in a momentum-driven bullish market. These corrections often find support at the 20 and 50-day moving averages (DMA), but the 100 and 200-DMAs are not outside regular corrective periods.

If you remember, in March, we discussed the potential for a 5% to 10% correction due to many of the same concerns noted above. That correction of 5.5% came in April. We are again at a juncture where a 5-10% correction is likely. The only issue is that it could come anytime between now and October. As is always the case, timing is always the most significant risk.”

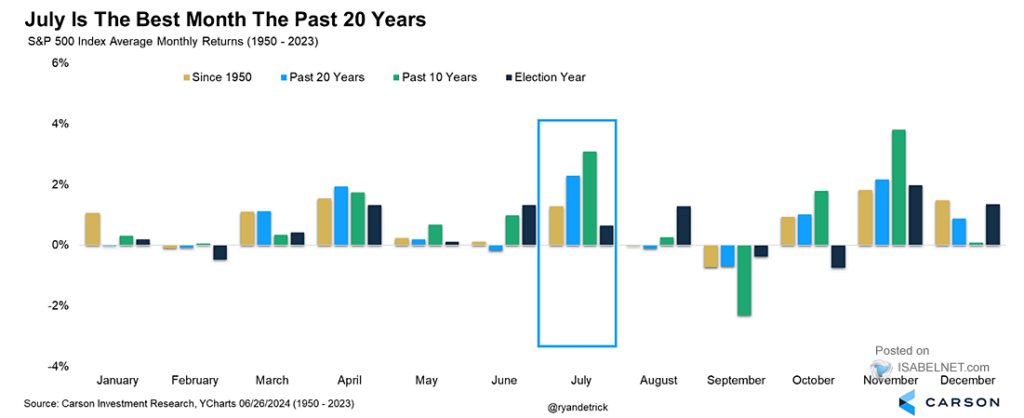

As shown, the market’s monthly seasonality supports that view of a potential correction later this summer. July tends to be a decent performance month, with an average return of more than 2%.

That boost in performance in July is supported by the kick-off of the Q2 earnings season. Such is particularly the case as investor sentiment is extremely bullish, which will continue to put a bid under stocks in the short term.

Speaking of earnings, analysts have been extremely busy over the last 30 days, slashing estimates. In June, Q2 earnings estimates for the S&P 500 index were cut by $5/share to the lowest level yet. Interestingly, while Wall Street continues to boast confidence in rising asset prices, they have cut estimates from $214/share in March last year to just $193/share. Such suggests a dichotomy between expected market performance and the economy, which is where earnings come from.

Nonetheless, the market remains overbought short-term and has triggered a short-term MACD “sell signal,” which could limit the upside in the near term. Continue to manage portfolio risk accordingly, but the bullish trend remains intact for now.

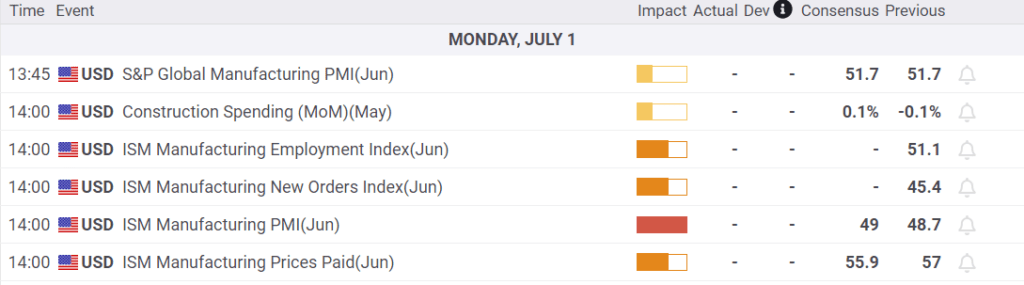

The Week Ahead

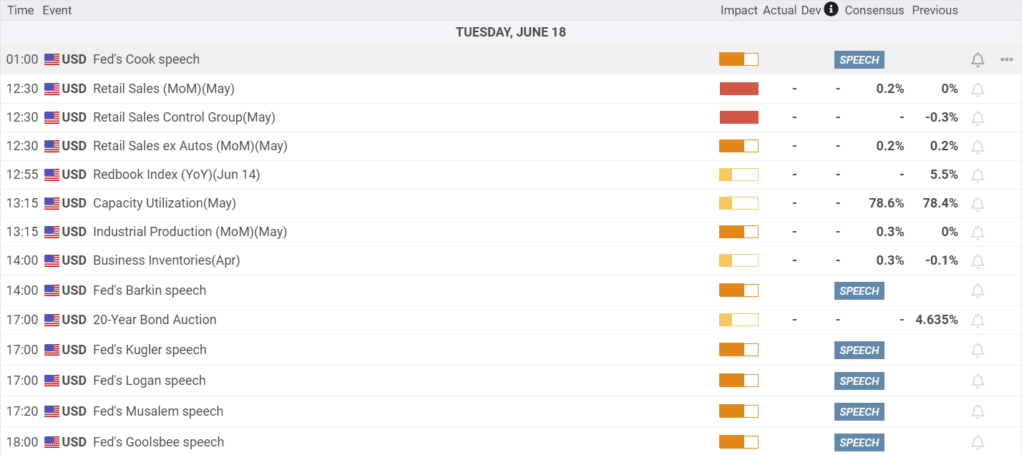

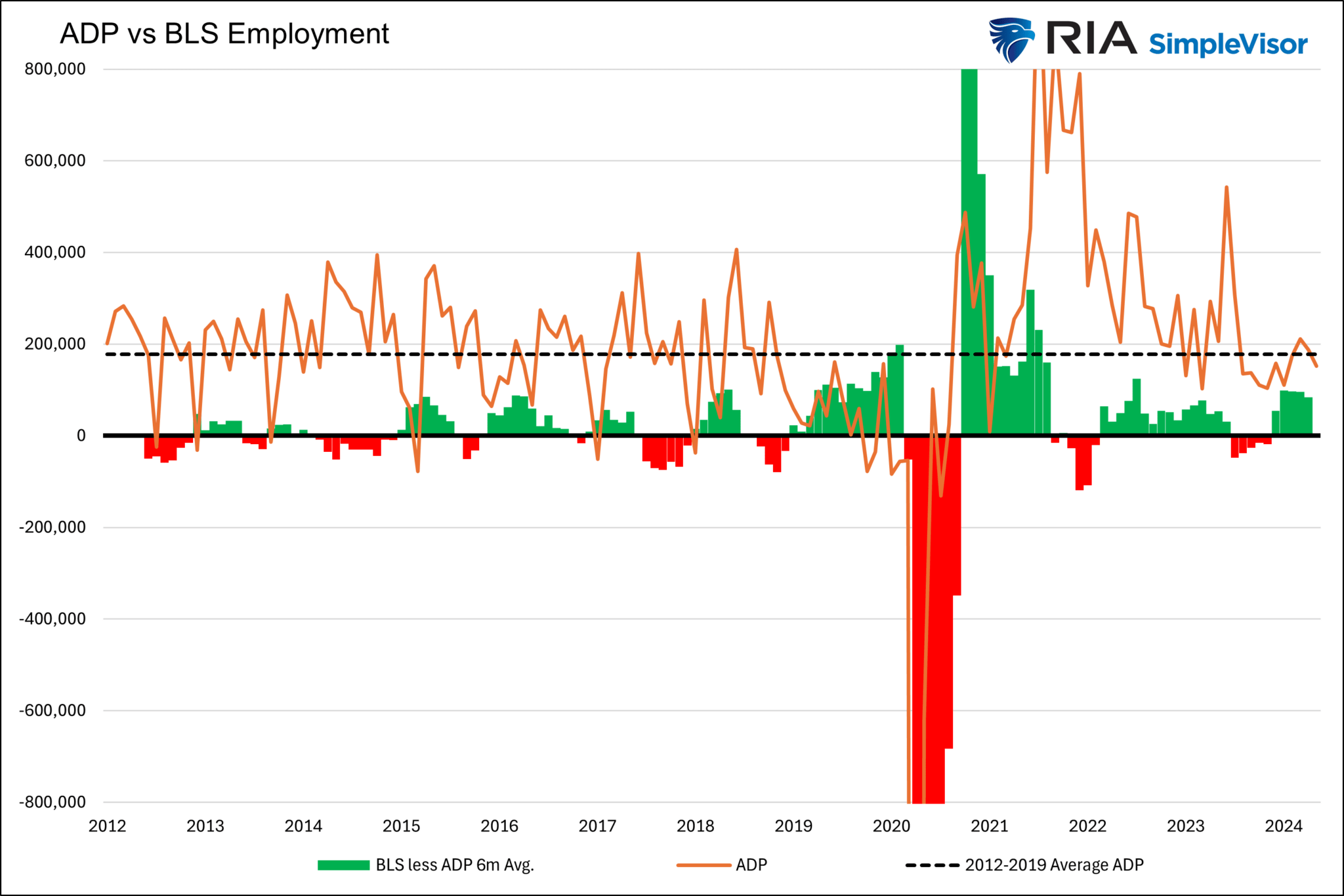

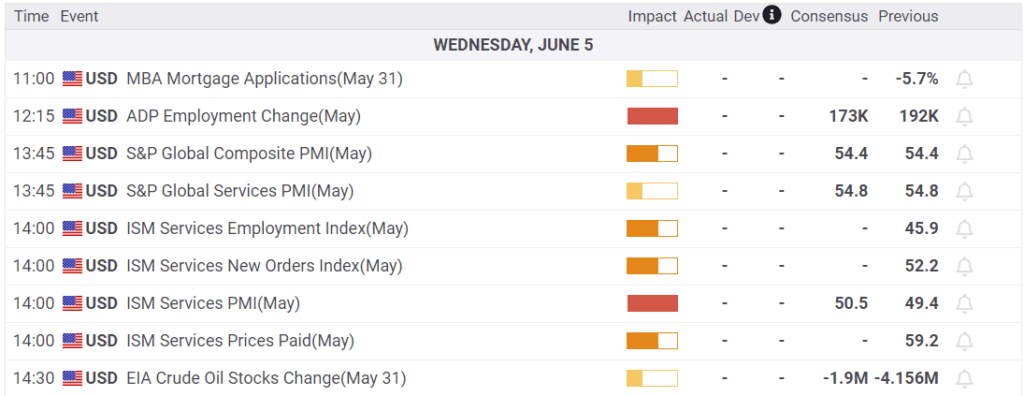

Despite the holiday-shortened week, investors will have plenty of economic data to digest. The ISM manufacturing survey will be released on Monday, and the services survey will be released on Wednesday. After Friday’s robust Chicago PMI survey, investors will look for confirmation in the ISM reports. Employment data, including JOLTs on Tuesday, ADP on Wednesday, and the BLS employment report on Friday, will be the most critical data points of the week. Recent jobless claims data point to some weakness in the labor markets.

Jerome Powell will be speaking on Tuesday at 8:30. By that time, he may have a good sense of what the BLS employment report holds. Further, investors will be looking to see if the recent weakness in economic data is starting to sway the Fed’s comfort regarding cutting rates. The next Fed meeting is July 31st.

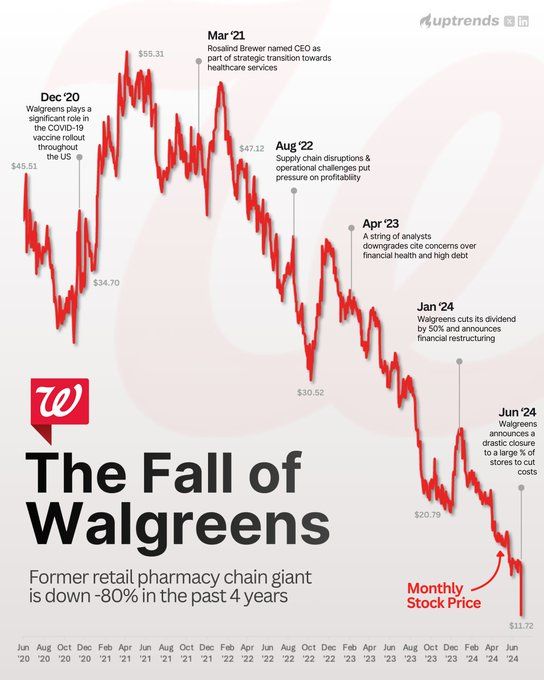

Nike and Walgreens Tumble On Weakening Sales

Nike and Walgreens’ off-calendar earnings highlight a continuation of weakening personal consumption. In late May, we discussed this troubling theme in retail and food services earnings. Those Commentaries can viewed HERE and HERE.

On Thursday night, Nike disclosed that it bettered earnings expectations by .17 cents due to cost-cutting. However, it missed revenue forecasts by $250 million. Furthermore, they guided expectations down for fiscal year 2025. Nike can no longer hike prices to keep up with inflation, which indicates that the consumer is becoming more frugal. They also speak to weakness in China. Many companies have echoed similar sentiments about China’s economy.

NIke’s poor earnings are not just about slowing consumption. It also appears that “lifestyle brand competitors” are taking market share from Nike. Per the CEO:

There was a shift in our lifestyle brands that caught us by surprise, and without new products, we’ve had less interest. Newness is driving the consumer and we’ve got to move to more newness. We are also chasing our competition in women’s apparel and running. We said last quarter we had a new playbook that will start our comeback with new innovations. We aren’t there yet, and our numbers are going to be worse in 2025 than we previously thought.

Walgreens also struggles partly due to weaker consumption. Like Nike, it is losing market share due to its business model. They reported earnings of $.63, $.05 short of estimates. However, revenues were slightly better than expected. While revenues were okay, they lowered EPS guidance from $3.20-$3.35 to $2.80-$2.95. Further, they are Closing 25% of their 8,600 stores over the next three years, which will lead to a decrease of 57,000 employees.

“We assumed the consumer would get somewhat stronger,” but “that is not the case,” said Walgreens CEO.

In regards to their business model, he states:

We are at a point where the current pharmacy model is not sustainable, and the challenges in our operating environment require we approach the market differently.

As we share below, NKE opened trading about 15% lower on the news last Friday and is at five-year lows. Walgreens is down about 20% since earnings. It has declined by 80% over the last five years, sitting at its lowest price since 1997!

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Career Risk Traps Advisors Into Taking On Excess Risk

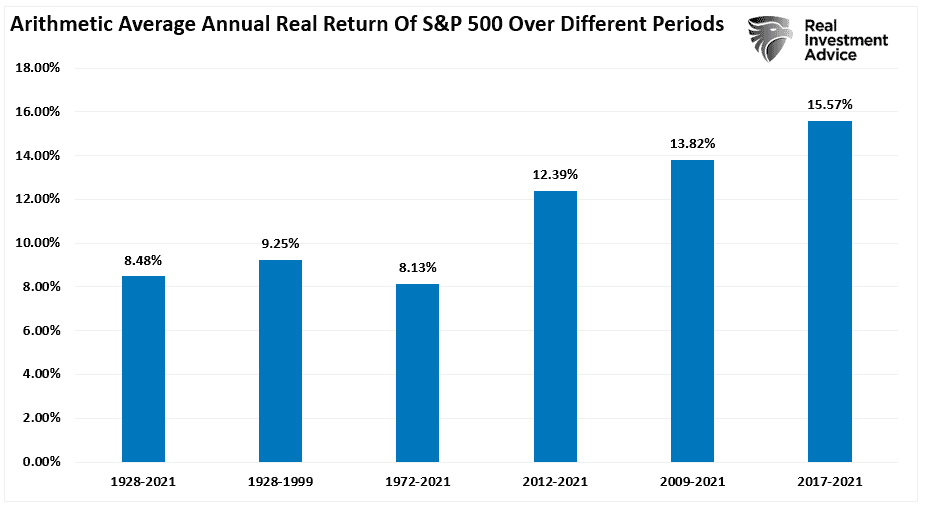

Financial advisors get a bad rap. Some deserve it; most don’t. The problem for the entire investment advisory and portfolio management community stems from the “career risk” they inevitably face. That “career risk” has been exacerbated over the last decade as massive monetary interventions and zero interest rates created outsized returns. A point we discussed last week in “A Permanent Shift Higher In Valuations.”

“The chart below shows the average annual inflation-adjusted total returns (dividends included) since 1928. I used the total return data from Aswath Damodaran, a Stern School of Business professor at New York University. The chart shows that from 1928 to 2021, the market returned 8.48% after inflation. However, notice that after the financial crisis in 2008, returns jumped by an average of four percentage points for the various periods.”

With social and mainstream media reporting on the latest investment hype surrounding market phases like “disruptive technology,”“meme stocks,” and “artificial intelligence,” it is unsurprising investors will salivate over the next “get rich quick” scheme. In addition, the annual reports from SPIVA measuring the performance of actively managed funds against their benchmark index intensify the “fear of missing out.”

The SPIVA report further fuels the debate over active versus passive indexing, or the “if you can’t beat ’em, join ’em” mentality.

Unsurprisingly, the result is the increasing pressure on financial advisors and portfolio managers to “chase performance.” Such is the basis of “career risk.”

“Career risk is the probability of a negative outcome in your career due to action or inaction.”

In other words, if financial advisors or portfolio managers don’t meet or beat benchmark returns from one year to the next, they risk losing clients. Lose enough clients, and your “career” is over. However, it is worse than that because even if the client states they are “conservative” and want little risk, they then compare their returns to that of an all-equity benchmark index. (Read this to understand why benchmarking your portfolio increases risk.)

Therefore, this career risk forces financial advisors and portfolio managers to push boundaries due to the risk of losing clients.

That brings us to two primary questions. The first is how we got here. The second is what you (as an investor or financial advisor) should do about it.

Performance Chases Performance

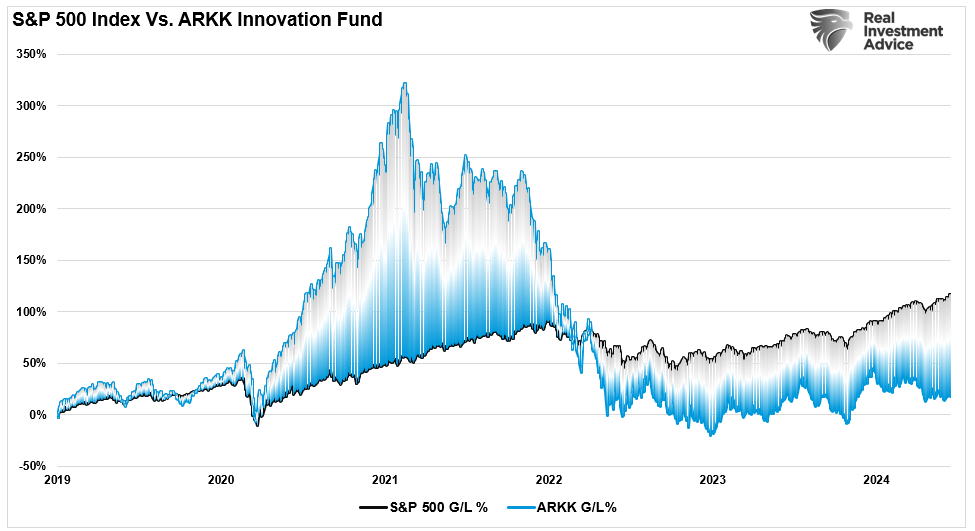

I recently discussed on the “Real Investment Show” that there is a big difference between a financial advisor or portfolio manager and an individual investor. The difference is the “career risk” of underperformance from one year to the next. Therefore, advisors and managers MUST own the assets that are rising in the market or risk losing assets. A great example of career risk is seen with Cathy Wood’s ARK Innovation Fund. That fund was the darling of Wall Street during the “disruptive technology” mania phase of the market following the stimulus-fueled investing craze following the Pandemic shutdown.

Unsurprisingly, during the mania phase, investors poured billions into the fund. Unfortunately, as with all mania phases, that investing style lost favor, and the fund has recently underperformed the S&P 500. That underperformance resulted in a massive loss of assets under management for ARK and Cathy Woods

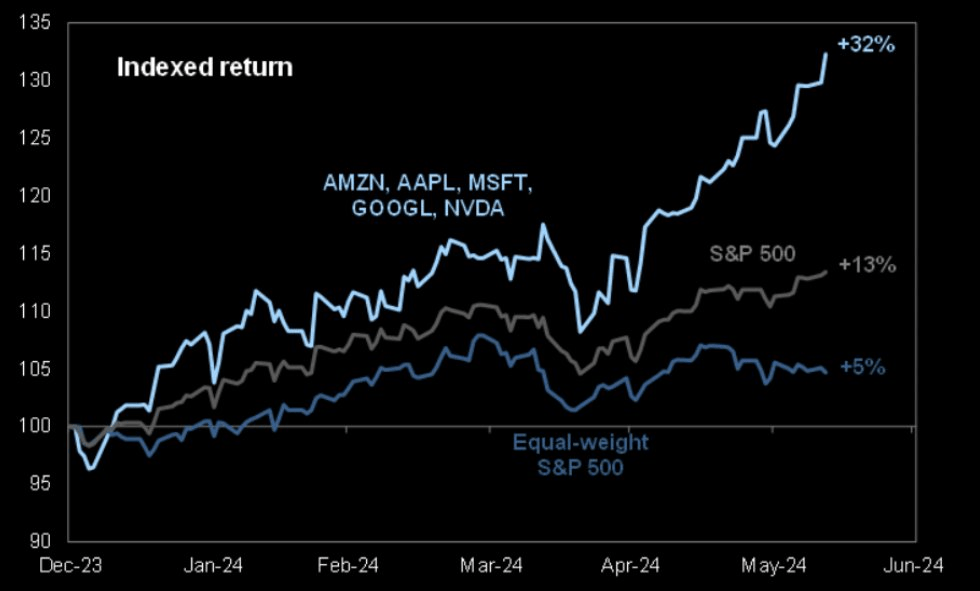

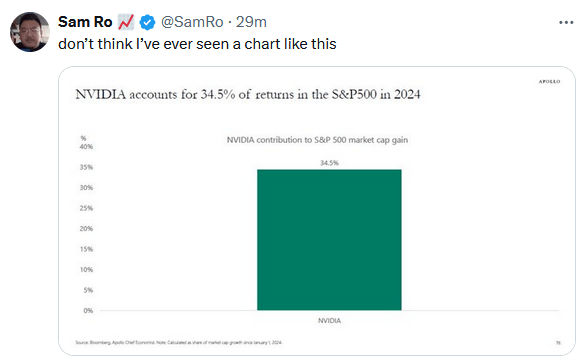

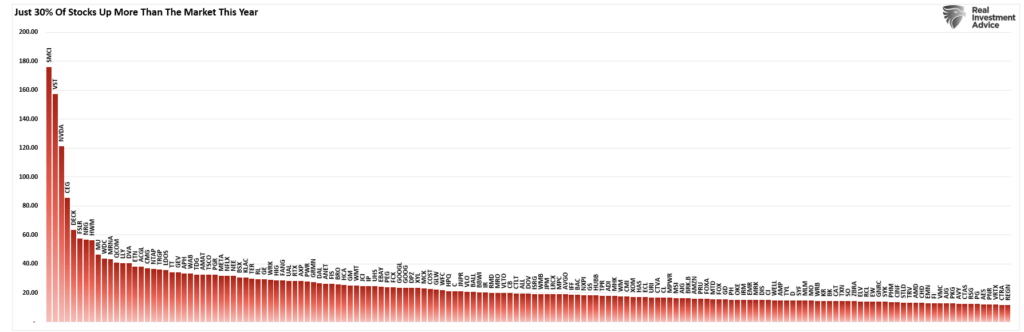

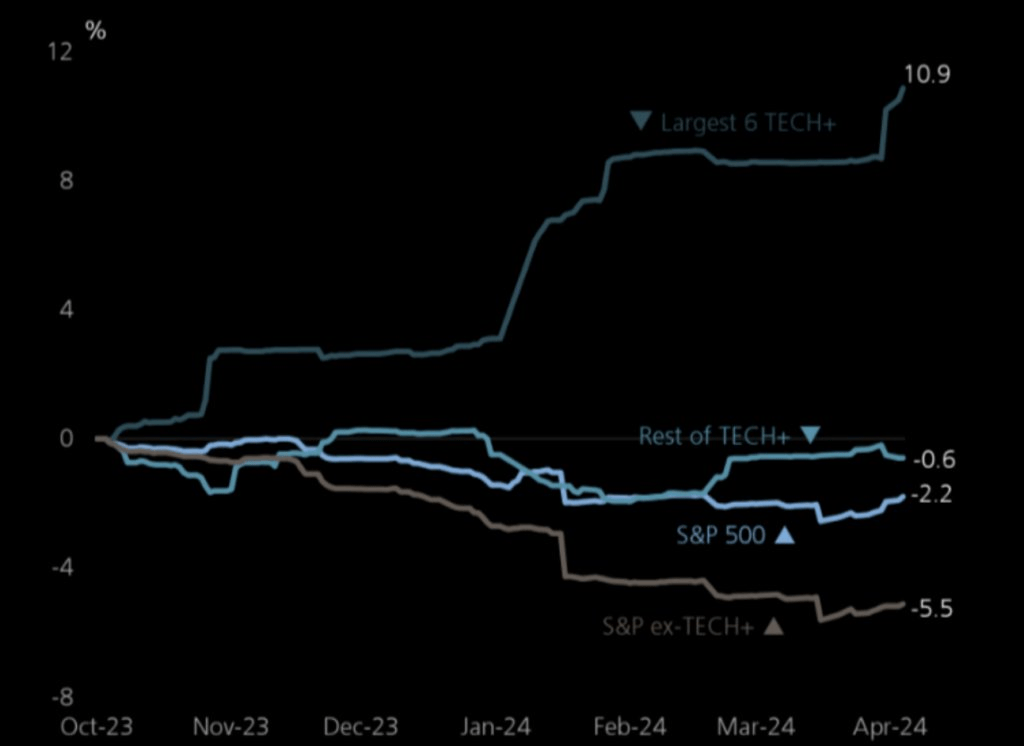

Today, the investment chase is all about “artificial intelligence.” Such has led to an enormous bifurcation in the market as a handful of stocks increasingly rise versus the rest of the market, as shown.

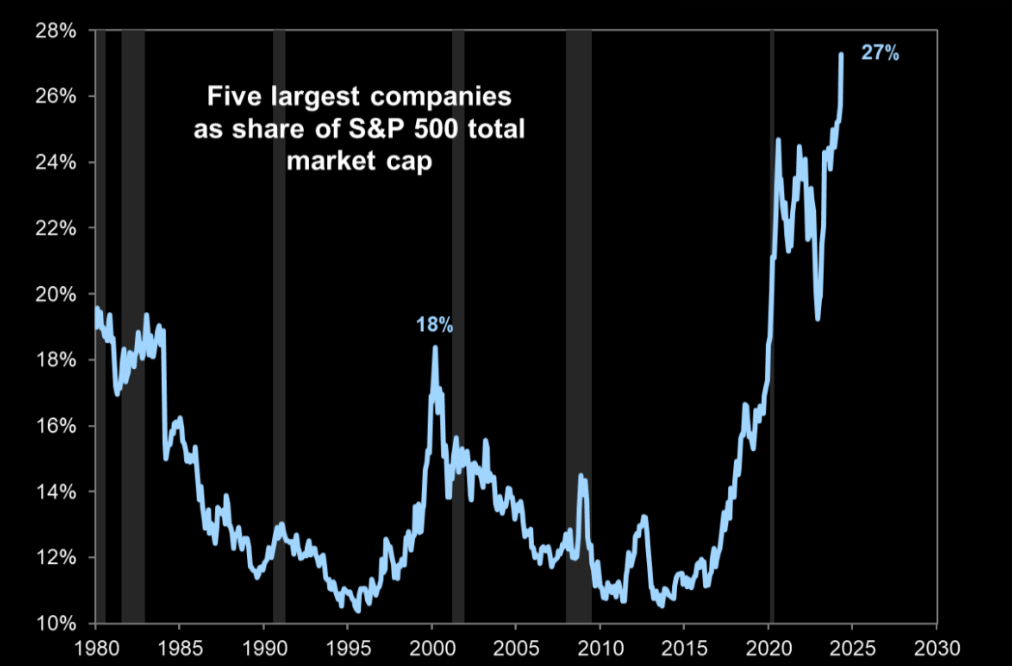

Once again, portfolio managers and financial advisors face enormous “career risk” pressure. As discussed in “It’s Not 2000,” as the market’s breadth narrows, advisors and managers must take on increasingly larger weights of fewer stocks in portfolios.

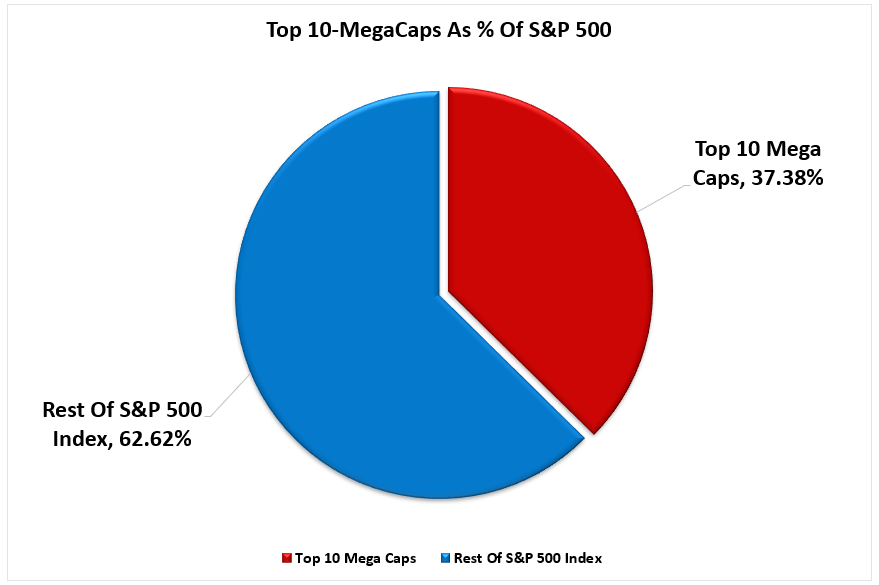

“The top-10 stocks in the S&P 500 index comprise more than 1/3rd of the index. In other words, a 1% gain in the top-10 stocks is the same as a 1% gain in the bottom 90%.As investors buy shares of a passive ETF, the shares of all the underlying companies must get purchased. Given the massive inflows into ETFs over the last year and subsequent inflows into the top-10 stocks, the mirage of market stability is not surprising.

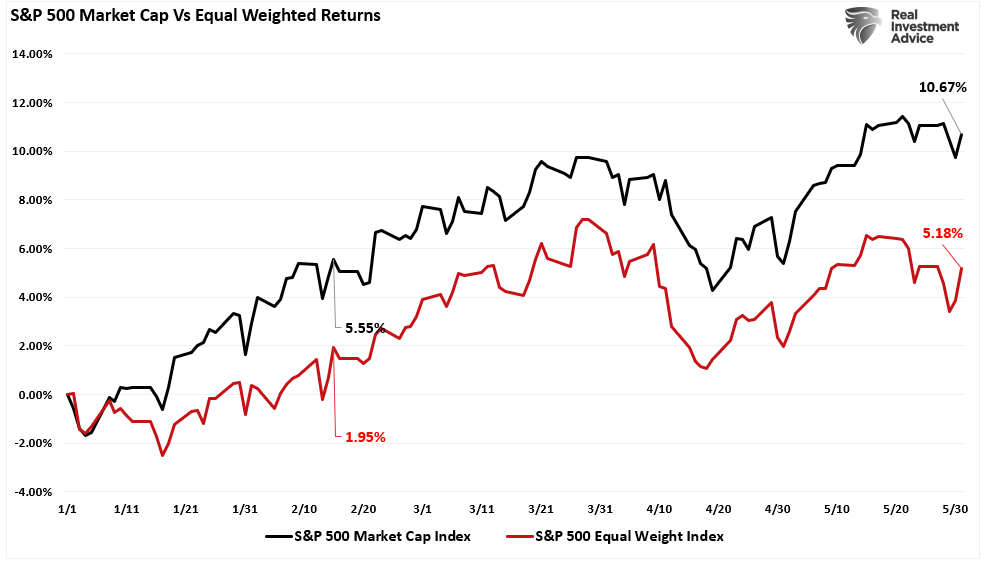

“That lack of breadth is far more apparent when comparing the market-capitalization-weighted index to the equal-weighted index.”

The question every investor should be asking themselves is:

“Is it really wise from risk management perspective to have nearly 40% of my portfolio in just 10-stocks?”

However, if you answer that question “no,” or if you have any other type of investment allocation, you will underperform the benchmark index. If you have an advisor or manager that matches a portfolio to your financial goals, they will also underperform. They now face the potential “career risk” of getting fired if the client fails to understand the reason for the underperformance.

So, what should financial advisors and clients do?

What Should Advisors Do?

For advisors, “career risk” is a real and present danger. Many opt for simplistic ETFs or mutual fund-based portfolios that track an index. The question is, as a client, what are you paying for?

Knowing that clients are emotional and subject to market volatility, Dalbar suggests four practices to reduce harmful behaviors:

Set Expectations Below Market Indices: Set reasonable expectations and do not permit expectations to be inferred from historical records, market indexes, personal experiences, or media coverage. The average investor cannot be above average. Investors should understand this fact and not judge the performance of their portfolio based on broad market indices.

Control Exposure to Risk: Explicit, reasonable expectations should be set by agreeing on predetermined risk and expected return. Focusing on the goal and the probability of its success will divert attention away from frequent fluctuations that lead to imprudent actions.

Monitor Risk Tolerance: Even when presented as alternatives, investors intuitively seek capital preservation and appreciation. Risk tolerance is the proper alignment of an investor’s need for preservation and desire for capital appreciation. The determination of risk tolerance is highly complex and is not rational, homogenous, or stable.

Present forecasts in terms of probabilities: Provide credible information by specifying probabilities or ranges that create the necessary sense of caution without adverse effects. Measuring progress based on a statistical probability enables the investor to make a rational choice among investments based on the reward probability.

When Must Advisors Take Action?

Dalbar’s data shows that the “cycle of loss” starts when investors abandon their investments, followed by remorse as the markets recover (sell low). Unsurprisingly, the investor eventually re-enters the market when their confidence gets restored (buys high).

Preventing this cycle requires having a plan in place beforehand.

When markets decline, investors become fearful of total loss. Those fears compound as the barrage of media outlets “fan the flames” of those fears. Advisors must remain aware of client’s emotional behaviors and substantially reduce portfolio risk during major impact events while repeatedly delivering counter-messaging to keep clients focused on long-term strategies.

Dalbar notes that during impact events, messages delivered to clients should have three characteristics to be effective at calming emotional panic:

Deliver messages when fear is present. Statements made well before the investor experiences the event will not be effective. On the other hand, if the messages are delivered too long after the fact, investors will already have made decisions and taken actionsthat are difficult to reverse.

Messages must relate directly to the event causing the fear. Providing generic messages such as the market has its ups and downs is of little use during a time of anxiety.

Messages must assure recovery. Qualified statements regarding recovery tend to fuel fear instead of calming it.

Messages must ALSO present evidence that forms the basis for forecasting recovery. Credible and quotable data, analysis, and historical evidence can provide an answerto the investor when the pressure mounts to “just do something.”

Providing “generic media commentary” with a litany of qualifiers to specific questions will likely fail to calm their fears.

Conclusion

An experienced advisor does more than “invest money in the market.” The professionals’ primary job is providing counsel, planning, and stewardship of the client’s financial capital. In addition, the advisor’s job is to understand how individuals respond to impact events and get in front of them to plan, prepare, and initiate an appropriate response.

Negative behaviors all have one trait in common. They lead individuals to deviate from a sound investment strategy tailored to their goals, risk tolerance, and time horizon. The best way to ward off the aforementioned negative behaviors is to employ an approach that focuses on one’s goals and is not reactive to short-term market conditions.

The data shows that the average investor does not stay invested long enough to reap the market’s rewards for more disciplined investors. The data also shows that investors often make the wrong decision when they react.

But here is the only question that matters in the active/passive debate:

“What’s more important – matching an index during a bull cycle, or protecting capital during a bear cycle?”

You can’t have both.

If you benchmark an index during the bull cycle, you will lose equally during the bear cycle. However, while an active manager focusing on “risk” may underperform during a bull market, preserving capital during a bear cycle will salvage your investment goals.

Investing is not a competition, and as history shows, treating it as such has horrid consequences. So, do yourself a favor and forget what the benchmark index does from one day to the next. Instead, match your portfolio to your personal goals, objectives, and time frames.

In the long run, you may not beat the index, but you are likely to achieve your personalinvestment goals, which is why you invested in the first place.

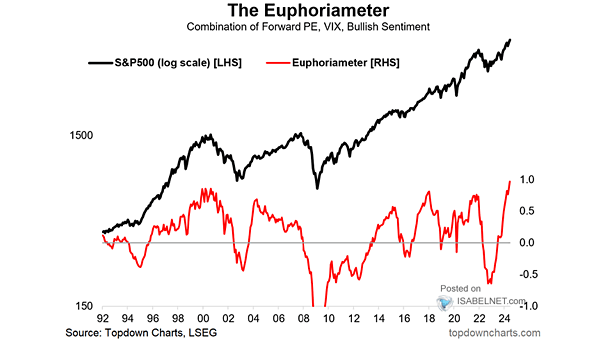

Cognitive Dissonance Is On Full Display

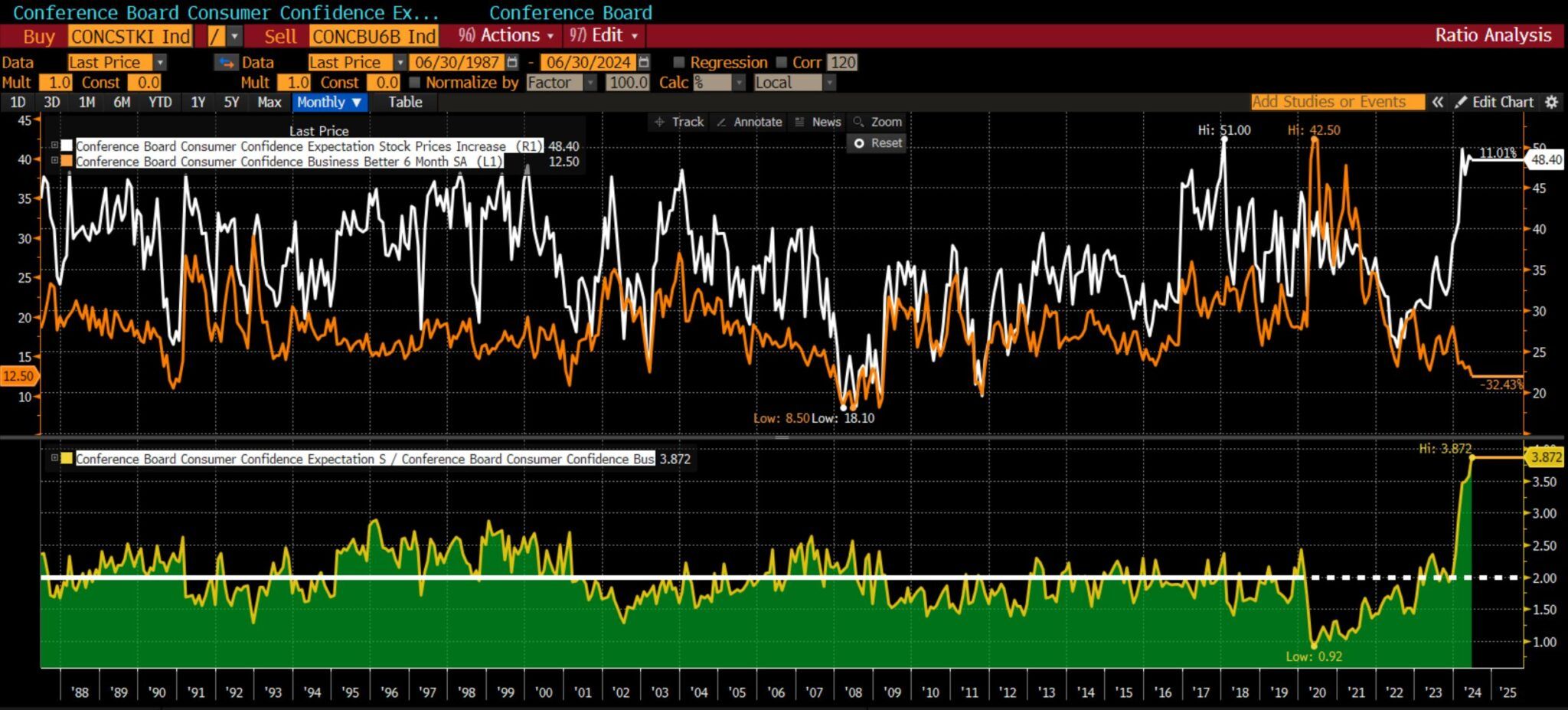

The recent Conference Board Consumer Confidence survey data show a state of cognitive dissonance among U.S. citizens. Cognitive dissonance occurs when a person believes in two contradictory things simultaneously. For instance, the latest Conference Board survey shows that expectations for increasing stock prices are among the highest since the late 1980s. However, citizens believe the business climate for the next six months will be among the worst environments over the last 35+ years. The graph below, courtesy of Michael Green, shows the two data series. Most often, they are correlated, rising and falling in unison. However, the recent gap is well beyond past experiences. The green chart at the bottom divides stock expectations by business expectations. It sits well above anything witnessed since the late 1980s.

In the short term, stock prices are a function of liquidity and investor behaviors. Over extended periods, prices represent the value of a company’s cash flows, which are highly predicated on economic activity and the business climate. Thus, investors can, at times, have cognitive dissonance, being bullish on stocks and bearish on the economy. However, the gap will most certainly close. Will it be due to improving economic confidence or stocks catching down with poor economic expectations?

What To Watch Today

Earnings

No notable earnings reports today.

Economy

Market Trading Update

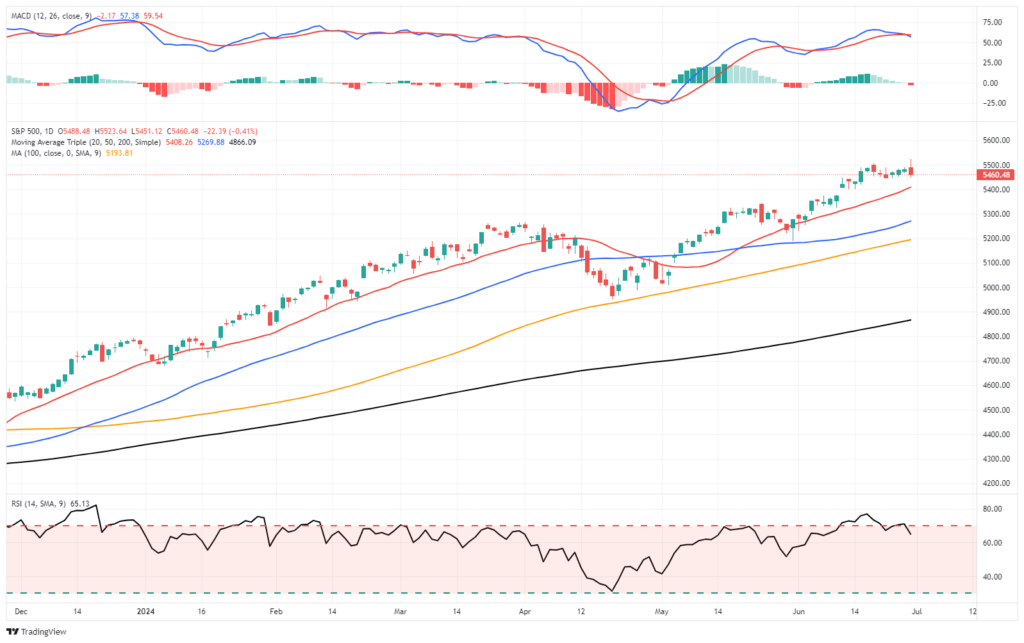

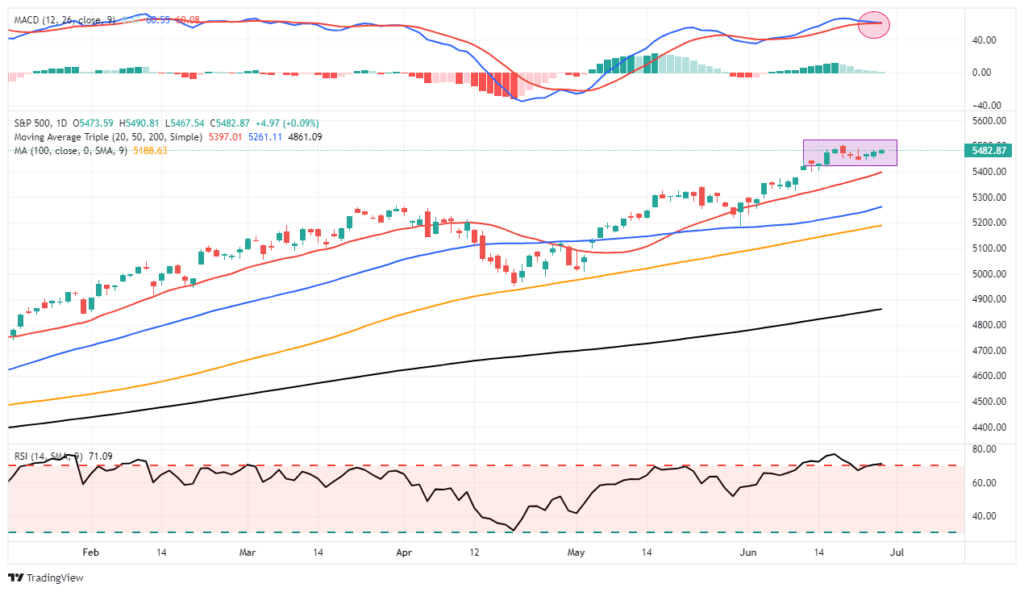

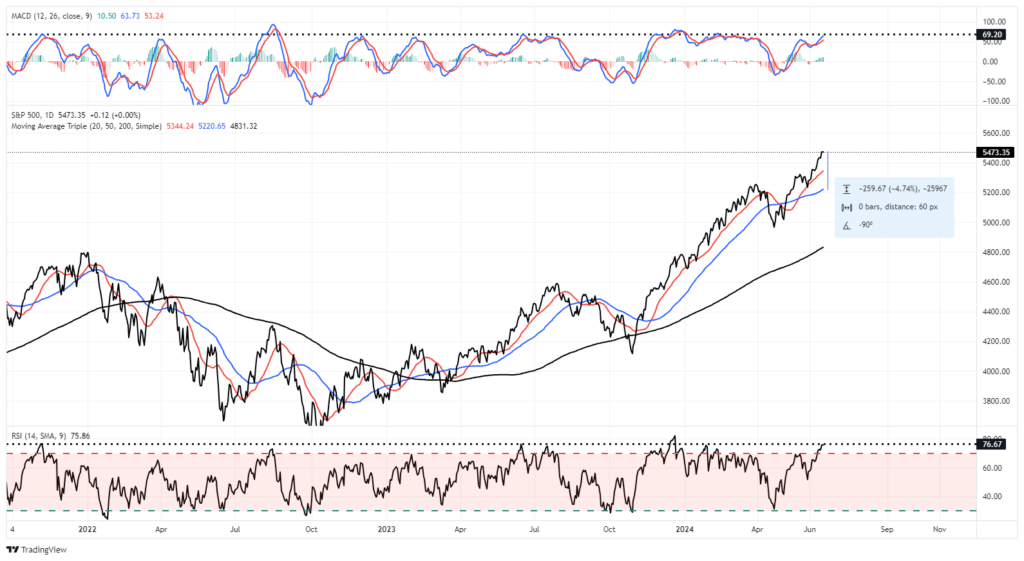

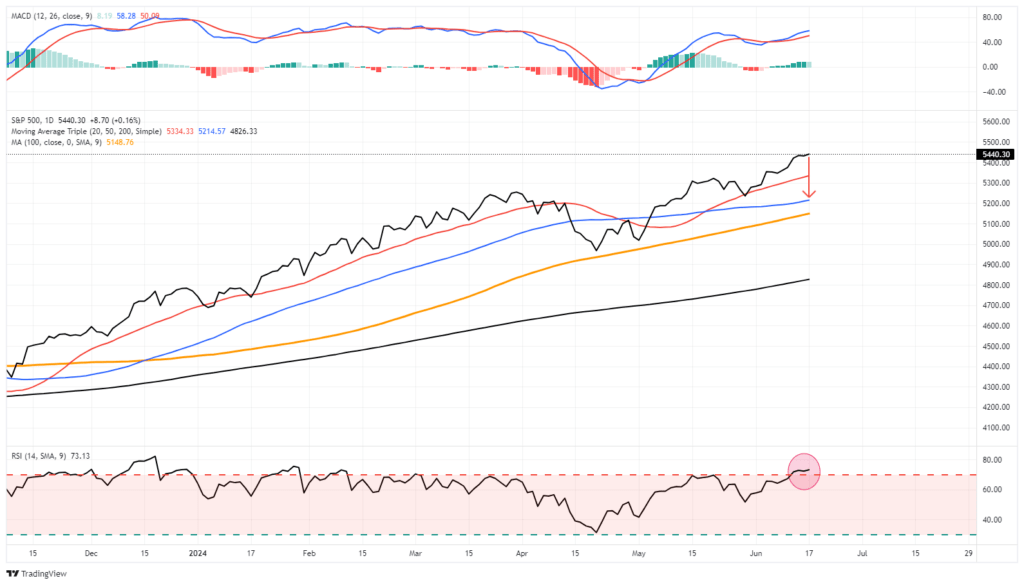

As we head into the last trading day of the month, the market remains range-bound near all-time highs. With the market still overbought, the upside remains limited near-term. However, we are close to triggering a short-term MACD “sell signal,” which further confirms that markets may be somewhat contained regarding further upside over the next week.

It has been a rather boring week of trading with little movement. Next week promises much of the same, with the July 4th holiday falling on Thursday. We expect to see a rather light trading week, but due to the lack of volume, there is a risk of a pickup in volatility.

There is little to be concerned about currently. Continue to let your equity positions play out. However, continue to follow risk-management protocols as needed to rebalance risk.

The Definition of Euphoria

While on the topic of cognitive dissonance, we think a recent segment from CNBC seems appropriate to share. On CNBC, hedge fund manager Eric Jackson of EMJ Capital stated:

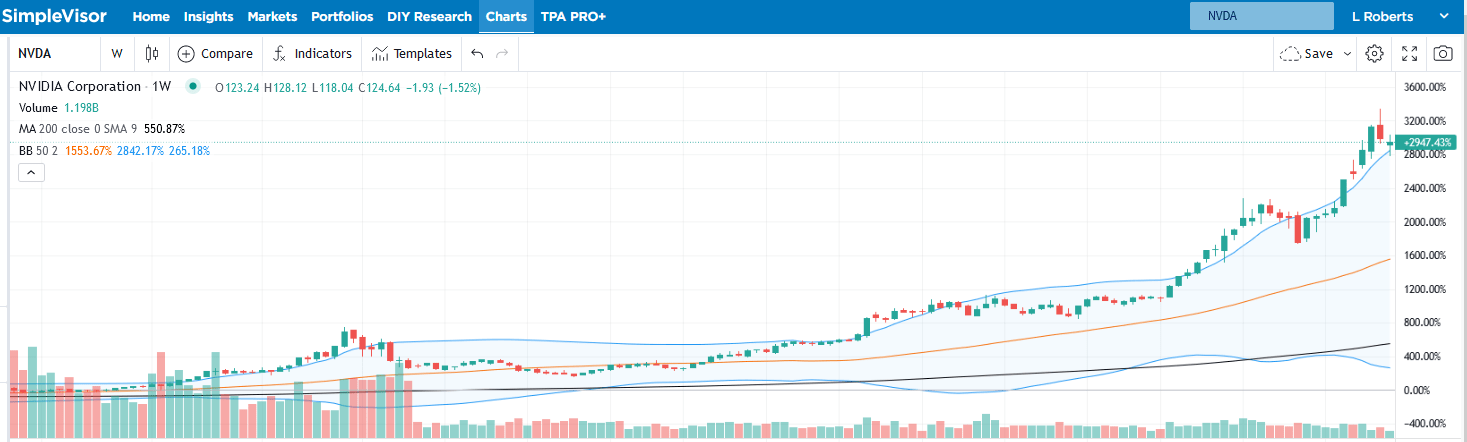

Over the last five years, Nvidia’s average look forward price to earnings multiple has been 40x. Yesterday (Monday), after this two day correction, it was 39x forward price to earnings. But there have been three times in the last five years where it had a look forward price to earnings multiple of over 50x, and two times in the last five years where it’s gotten just about to 70x and then pulled back. So we haven’t see that euphoria yet.

Jackson thinks Nvidia could have a $6 trillion valuation by the end of the year. Such means its stock price will double. He claims Nvidia investors haven’t seen euphoria yet. The stock is up nearly 3,000% in about five years, as shown below. That is euphoria! We are not sure there is a word to describe investor sentiment if Jackson proves accurate. However, stocks trading in a euphoric phase are often followed by a dysphoric feeling.

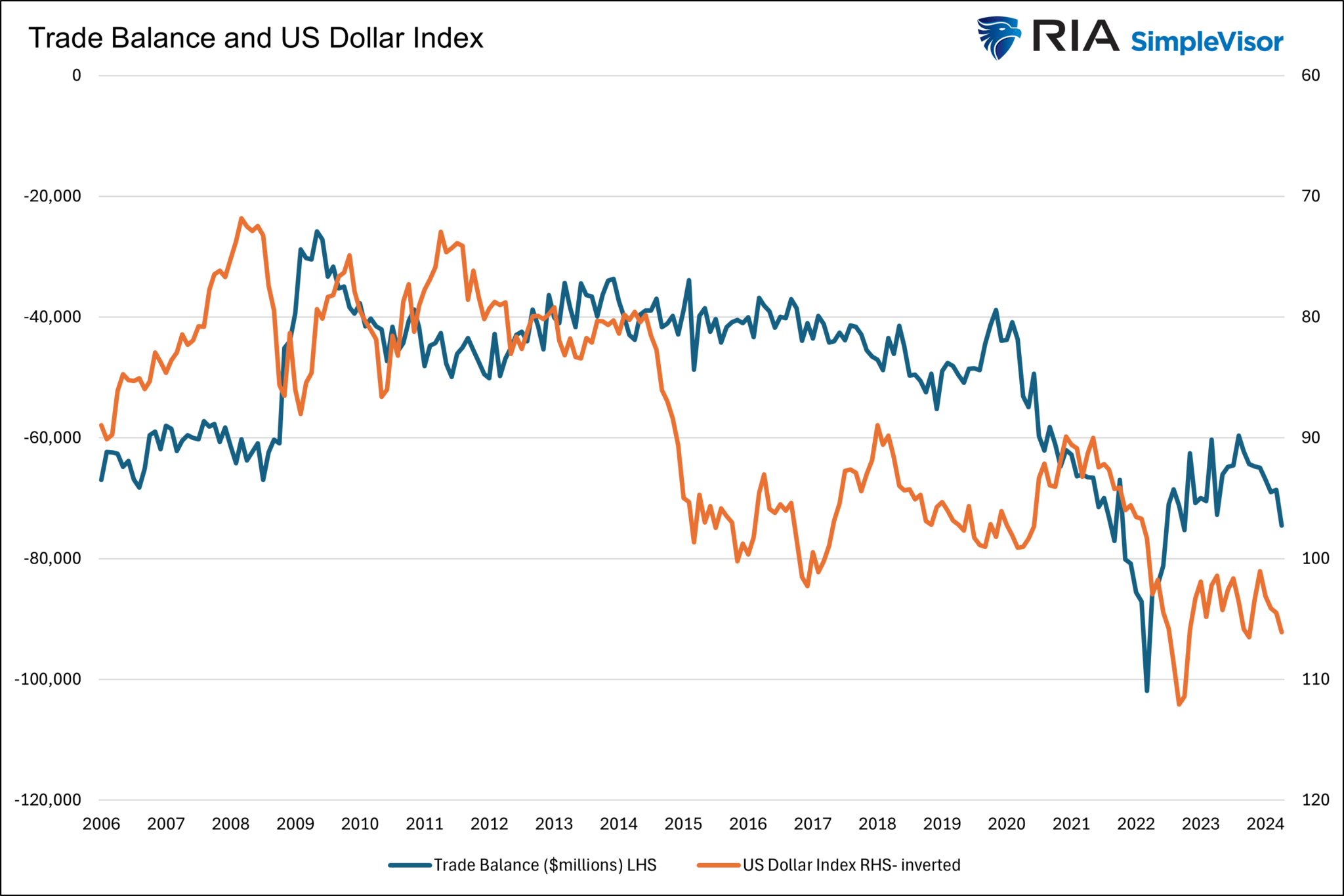

Weaker Trade Balances Accompany’s A Strong Dollar

The U.S. dollar index has been up about 4% this year. A stronger dollar results in lower import prices because America runs trade deficits, i.e., we import more than we export. On the margin, trade deficits reduce prices. That is a positive. However, from a GDP perspective, it is not good news.

The formula for GDP is C+I+G+(X-M). C is consumer spending, I is business investment, G is government spending, and (X-M) is net exports. The X-M part of the formula is exports less imports. Running a trade deficit, as we consistently do, makes the net result negative. The graph below shows that trade deficits and dollar value correlate decently. Recently, dollar strength has pushed net exports further into deficit territory, thus dampening economic growth.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

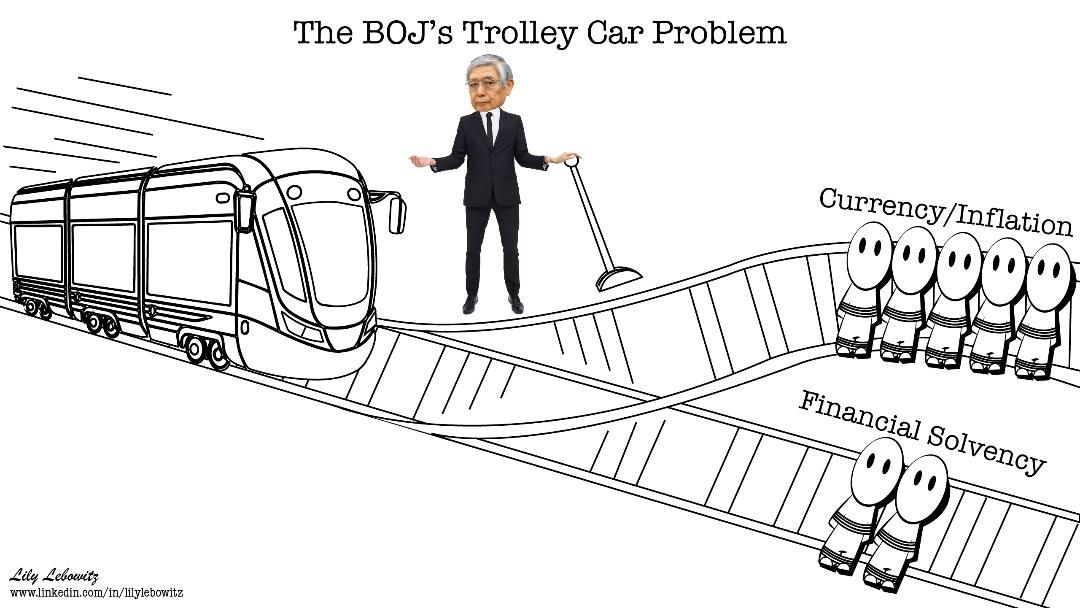

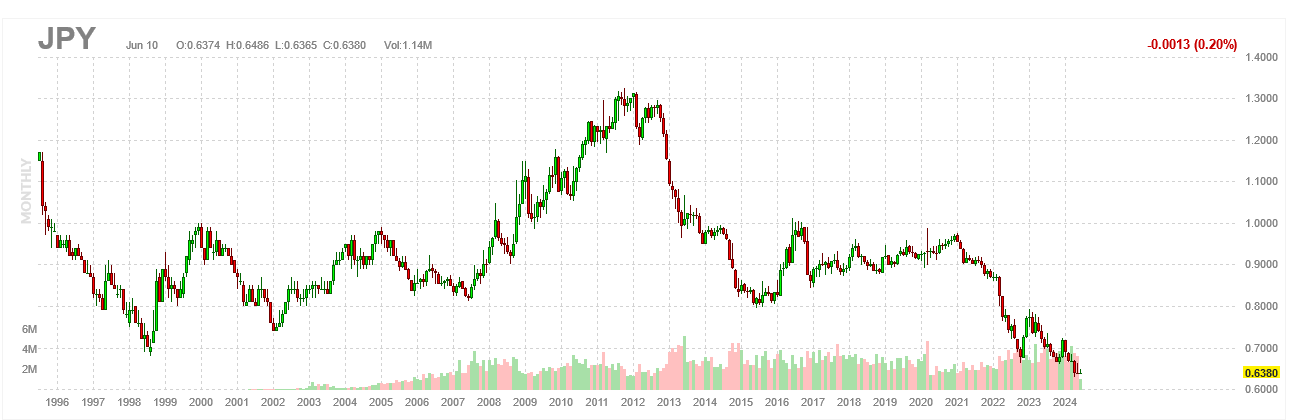

Will Japan Dump U.S. Treasury Securities?

Japan holds $1.150 trillion of U.S. Treasury securities, well above the next major foreign holder, China, which has $770 billion. Therefore, given Japan holds 3.3% of all Treasury debt, it is worth appreciating the recent news that Japan is selling bonds. First, to dispel some fear, Nornichukin Bank, not the Bank of Japan or the Japanese government, is selling U.S. Treasury bonds. Their goal is to sell $63 billion of U.S. and European government bonds by March 2025. Importantly, this is not a government policy decision but one the bank is making to fortify its deteriorating balance sheet. According to SIFMA, $879.8 billion Treasuries trade daily on average. With 262 days to sell less than $63 billion, their actions should have zero impact on Treasury yields.

However, persistent rumors have been circulating for years that the Japanese government and/or BOJ will sell bonds to prop up its currency. The yen has been in a free fall recently. On Wednesday morning, it traded at levels last seen in 1986! To appreciate Japan’s dilemma of selling Treasuries, providing it with dollars in which to buy the yen, consider a quote we wrote two years ago (LINK):

“However, as the BOJ tries to stop rates from rising, they weaken the yen. Japan is in a trap. They can protect interest rates or the yen, but not both. Further, its actions are circular. As the yen depreciates, inflation increases, and the Japanese central bank must do even more QE to keep interest rates capped.”

The cartoon below helps answer our question. Selling Treasuries in large quantities to support the yen risks increasing interest rates, which can increase the odds of insolvency.

What To Watch Today

Earnings

Economy

Market Trading Update

As discussed yesterday, the market was under pressure recently due to the decline in Nvidia ($NVDA). However, that sell-off seems to have abated for now, and there has been little other data to move the market as we head into the month’s end. Since this is the second quarter’s end, portfolio managers must rebalance their holdings by Friday. Furthermore, next week is shortened by the July 4th holiday, so trading will be light. Today and tomorrow are full of economic data that will be eyed closely for further clues to the upcoming Federal Reserve meeting in July. Furthermore, next week starts the beginning of the Q2 earnings season.

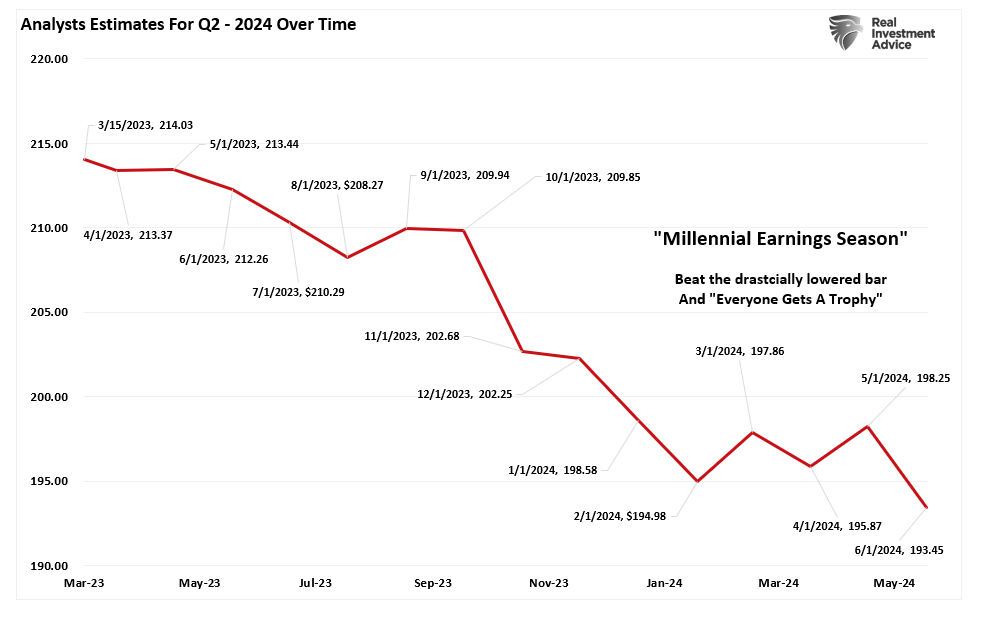

Speaking of earnings season, analysts have slashed estimates over the last 30 days. Despite ratcheting their views on the market outlook, with Goldman Sachs leading the way at 6300 by year-end, analysts reduced estimates from $198.25 to $193.45. That is the lowest estimate for this quarter since last year, when they started at $214.03.

As noted, this is why we call it “MIllennial Earnings Season,” as analysts keep lowering the bar until “everyone gets a trophy.”

Small Cap Stocks Are Relatively Cheap

Much of the recent market conversation revolves around the strength of large-cap stocks and the relative weakness of most other stocks. What is not often heard is how the performance is affecting valuations. The graph below, courtesy of Yardeni Research, shows that the forward P/E ratio for large-cap stocks is near the highest level since the dot com bust. Yet, the forward P/E for small and mid-cap stocks has been lingering at their lowest levels in over ten years. More importantly, the current valuation has been the lowest since 2008, excluding periods when the market was in a correction. The gap between large and small-cap stocks will likely converge at some point. However, it can get more dislocated before such a normalization occurs.

Office Carnage Continues

The price decline of some office properties in many major cities is startling. We follow @TripleNetInvest on X/Twitter to keep us updated on commercial real estate fire sales. On Wednesday, he posted the following:

An office tower (pictured below) in San Francisco’s Mid Market area shockingly sold for 90% LESS than what it last traded for.

The previous owner paid $62M in 2018 for the 90k SF building.

It was recently acquired by a Starwood affiliate for $6.5M ($72 per SF)

Despite the post-Covid normalization across most economic sectors, vacancy rates around the country are not falling. San Francisco has the highest vacancy rate of big cities, at 37%. For context, it was 7% in 2019. Furthermore, it has an occupancy rate of 44%. Per Optimize Reality:

As those drastically under-occupied leases come due, they will exaggerate an already market clogged by empty office space. The over-saturation will become far worse indicated already by dropping rents and hundreds of thousands of square feet hitting the sublease market.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

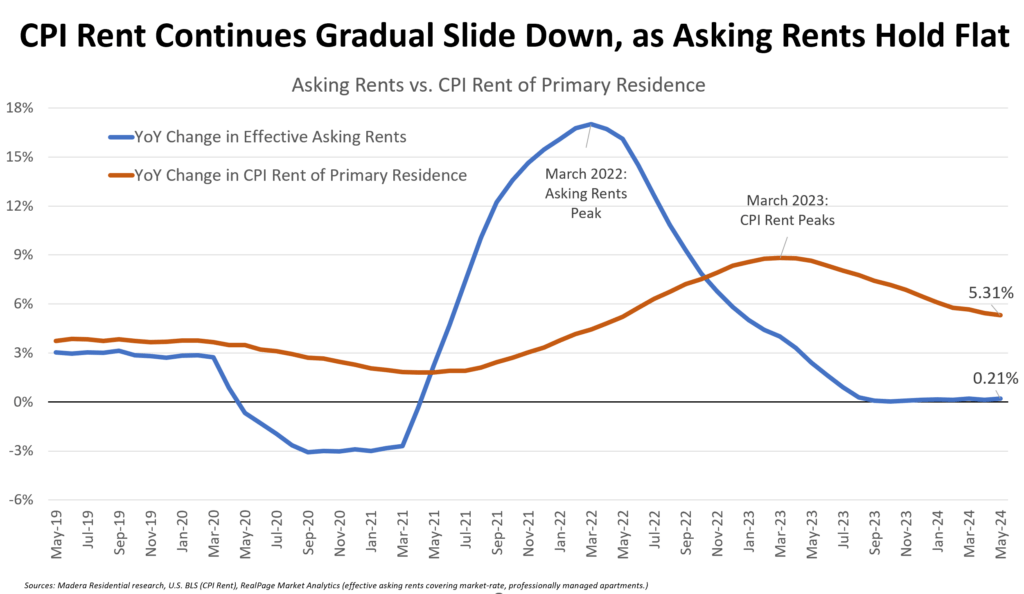

Why Economists And Citizens Have Different Inflation Realities

The Fed and economists are encouraged because CPI is down to 3.3% from a high of nearly 9% in 2022. Despite the Fed’s “significant progress” in lowering inflation, most citizens are outraged and confused by economists’ relatively rosy inflation observations. Most citizens believe inflation is still rampant.

The Fed and economists are correct in that inflation is now tame. At the same time, citizens dissatisfied with high prices have solid grounds on which to base their disapproval.

Let’s better understand how such contradictory beliefs can both be factual. Furthermore, in the process, we can help Jerome Powell understand why economic sentiment is poor despite a near-record low unemployment rate.

You know, I don’t think anyone knows, has a definitive answer why people are not as happy about the economy as they might be. -Jerome Powell 6/12/2024

Visualizing Divergent Inflation Opinions

The graph below of the BLS CPI New Vehicles price index, a CPI component, demonstrates why economists and citizens have such grossly contrasting opinions of inflation.

Economists focus on the blue line, graphing the year-over-year change in new vehicle prices. Over the last year, the price index of new vehicles has decreased by .60%. Economists can say the cost of buying a new vehicle is in a deflationary state.

While the chart may warm the hearts of economists and the Fed, most individuals see the orange line, the CPI price index for new vehicles instead. It shows that new vehicle prices are up about 20% since the pandemic. Yes, they may have recently declined slightly, but today’s prices are nowhere close to where they were four years ago. In their minds, there is significant inflation in new vehicles.

Economists Prefer Growth Rates, Not Absolutes

Ask an economist what the nation’s GDP is, and they will quote an annualized growth rate to a decimal point. We bet almost all of them will get the answer correct within one or two-tenths of one percent.

Ask them again, but request the answer in dollars. It would not be surprising if many economists are off by a trillion or even two trillion dollars, representing anywhere from 3.00% to 7.00% of the economy.

Economists prefer to analyze and quote many economic data points in terms of percentage change. For instance, how much did industrial production or retail sales change versus last month or over the previous quarter or year? They vastly prefer growth rates because it gives them a comparable and insightful way of analyzing economic data. Let’s review why this is the case.

Comparative Analysis

Economists are more adept at comparing data from different periods, industries, and countries if they have a common measurement calculation. Instead of absolute change, which doesn’t account for the starting point, a growth rate captures the absolute change and the starting point. Consider the following:

If GDP increases by $1 trillion this year, how would that compare to a $1 trillion increase in 2000? The question is challenging to answer using absolute numbers. However, growth rates allow us to evaluate the two periods quickly. Today, GDP is $28.284 trillion; therefore, a $1 trillion increase would represent 3.50% growth. In 2000, GDP was close to $10 trillion. Adding a trillion dollars of economic growth would have resulted in a 10% growth rate. While a trillion dollars is a trillion dollars in absolute terms, there is a stark difference between 10% and 3.50% growth.

Trend Analysis

Growth rates highlight trends and changes over time more clearly than absolute numbers. They can show whether an economy is accelerating, decelerating, or maintaining a steady pace.

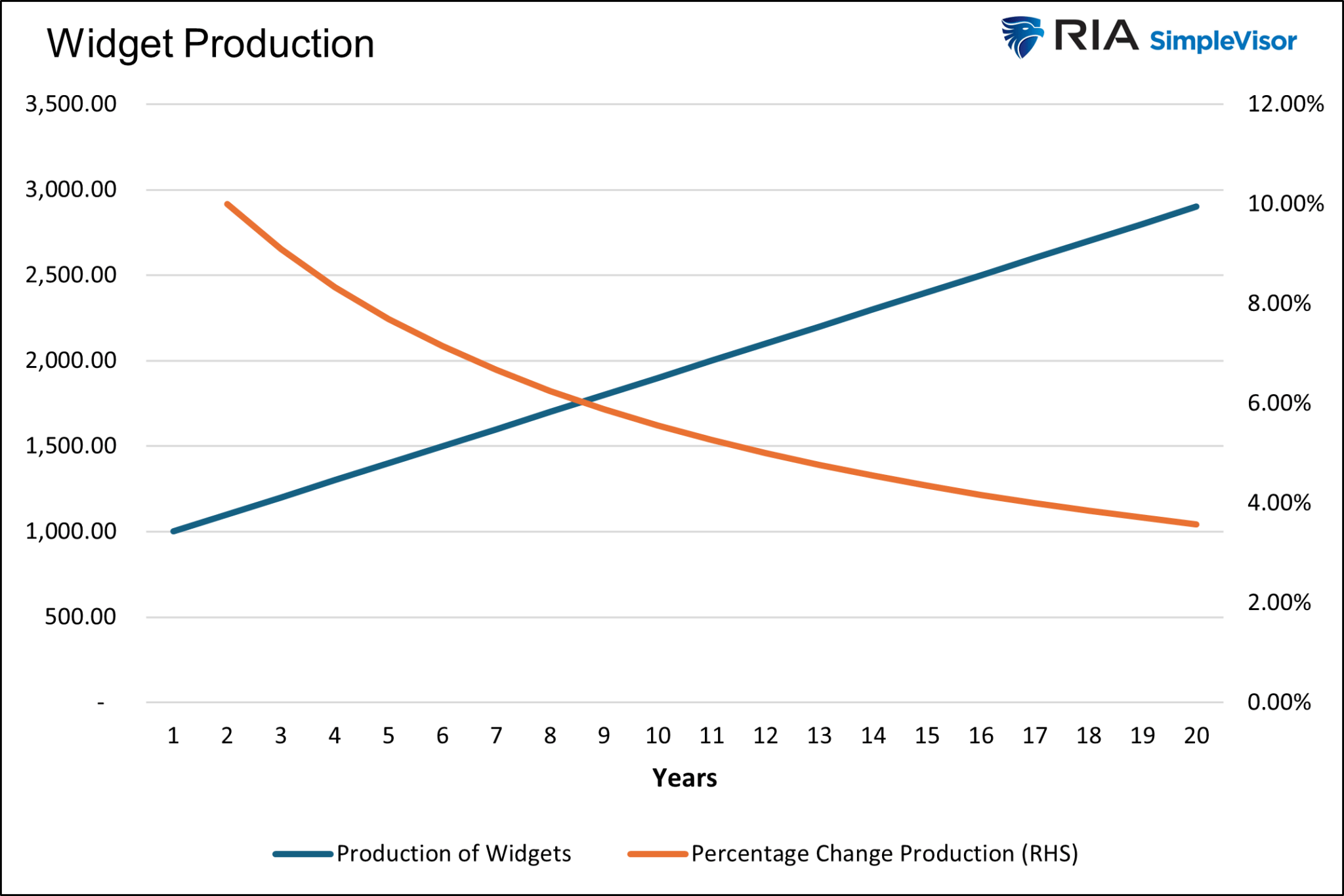

Consider the graph below. The blue line, showing the make-believe production of widgets, starts at 1,000 widgets and increases by 100 widgets annually. The steady growth in absolute terms is a linear upward trending line. However, the annual growth rate steadily declines from 10% to 4% by year 20. An economist looking at the graph would say the rate of the production of widgets is declining despite the upward trend in the number of widgets being produced annually.

Policy Decision Making

The Fed aims to promote stable economic growth. To do so they balance the level of interest rates with inflation and economic activity. Having like figures to analyze, such as growth rates, makes their task significantly more straightforward. Imagine if the Fed had to determine the appropriate interest rate given that the economy grew by $750 billion last year and the CPI price index rose by 2.45.

Investors prefer growth rates for the same reason. If I can estimate the economy’s growth rate and other critical economic figures, they can better determine a growth rate or interest rate they would accept for taking risks.

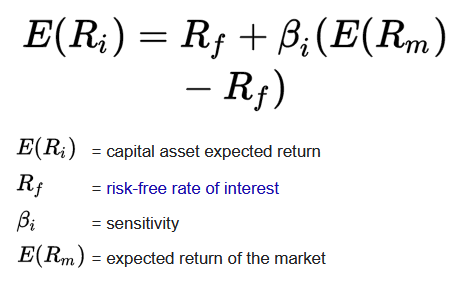

The capital asset pricing model (CAPM) is a bedrock for finance. The formula states that an asset’s expected return should equal the risk-free interest rate plus the asset’s sensitivity (beta) times the market’s expected return. This formula can only work with growth rates, not absolute numbers.

Consumer’s Point Of View

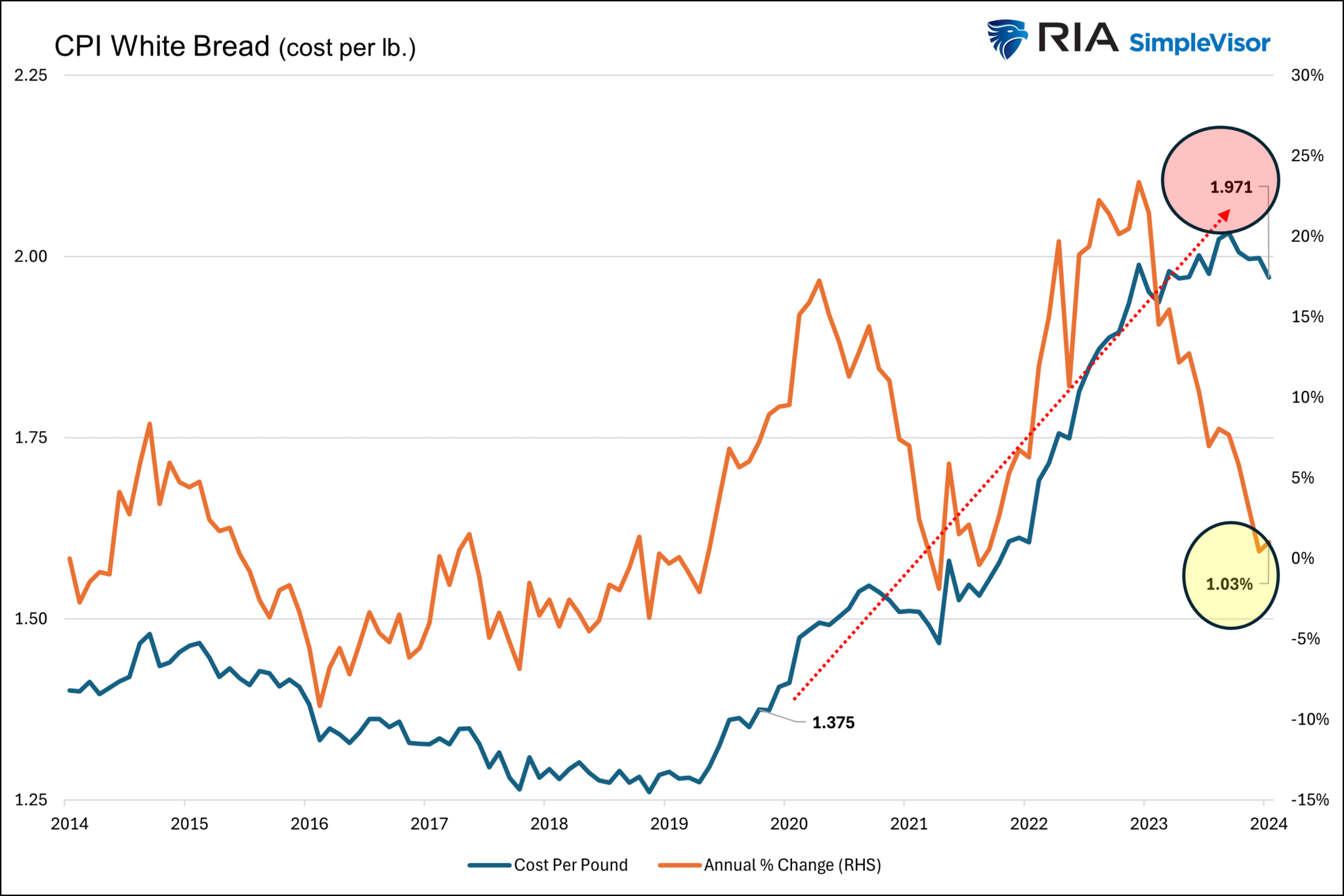

Regarding inflation, consumers are less concerned with growth rates and heavily focused on absolute prices. They remember that bread used to cost $4 a loaf and now costs $7. The graph below shows the price of white bread was stable between $1.25 and $1.50 a pound from 2008 to the pandemic. It is now close to $2 a pound.

That is significant inflation. But it doesn’t tell the whole story. If wages also rose similarly, purchasing power hasn’t changed. It is similar to hearing stories from your parents or grandparents about going to the movies and getting popcorn and a soda, all for $1. Did you ever ask them how much money they made at the time?

Summary

We want to make it clear that we do not condone inflation. It accelerates an already wide wealth gap and creates hardships for many citizens. For more, please read our article, Fed Policies Turn The Wealth Gap Into A Chasm.

We analyze inflation data similarly to economists. We accept that absolute prices are much higher today than a few years ago, but we also acknowledge that, in general, wages are higher as well. Just like we can’t realistically compare a 15-cent McDonald’s hamburger to a $3.00 one today, we should be careful comparing prices today to their prices a few years ago.

Prices are not returning to 2020 levels. In fact, any hint that aggregate prices retreat from current levels will cause the Fed to panic and quickly stimulate inflation via lower interest rates and QE. We remind you that the Fed was lamenting that we didn’t have enough inflation throughout most of the period between the financial crisis and the pandemic.

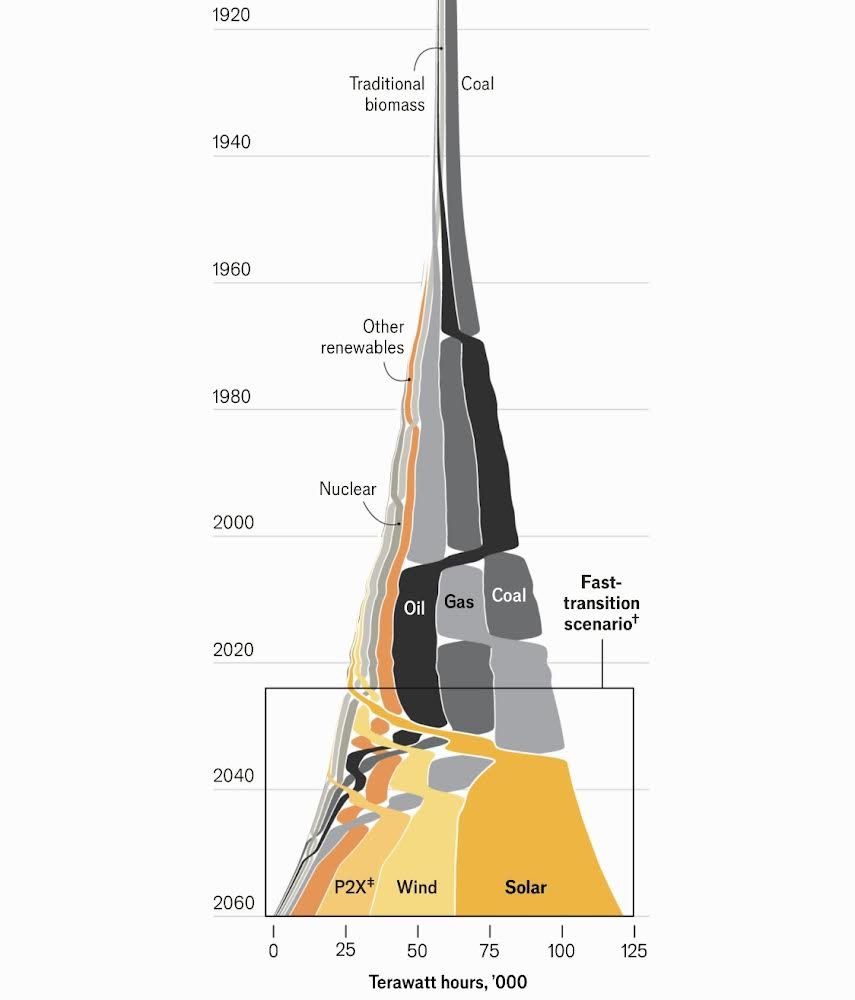

The Economist Makes A Case For Solar Energy

The unique graph below caught our attention, compelling us to read Solar Power Is Going To Be Huge by the Economist. The graph shows that solar energy will be the primary energy source for the world by 2040 under its “fast transition scenario.” The Economist article walks through some stats on the growth of solar energy as well as obstacles. Given the immense growing demand for electricity from AI data centers and EVs, it’s worth appreciating what energy sources will fuel the power grid and their respective investment opportunities. For more on the topic, we wrote a three-part article, which can be accessed here (parts ONE, TWO, and THREE ).

The Economist shares some interesting statistics on the rise of solar energy. For instance, solar energy is on track to produce “more electricity than all the world’s nuclear power plants in 2026, than its wind turbines in 2027, than its dams in 2028, its gas-fired power plants in 2030 and its coal-fired ones in 2032.” The increasing use of solar energy is due not only to its environmental benefits but also its falling cost. Per the Economist:

Since the 1960s…the levelised cost of solar energy—the break-even price a project needs to get paid in order to recoup its financing for a fixed rate of return—has dropped by a factor of more than 1,000.” Over the period, “prices dropped by a factor of 500. That is a 27% decrease in costs for each doubling of installed capacity, which means a halving of costs every time installed capacity increases by 360%.

The Economist makes a strong case for solar energy being dominant in fifteen years. If they are correct, there are some investment ideas worth researching with solar panel and battery manufacturers and producers of solar energy. However, investors must also consider the near future. Specifically, which energy source can fuel the current rapid expansion of power grids today and for the next fifteen years? As portrayed in the graph, natural gas is likely to remain the primary fuel for the power grid for at least another ten years.

What To Watch Today

Earnings

Economy

Market Trading Update

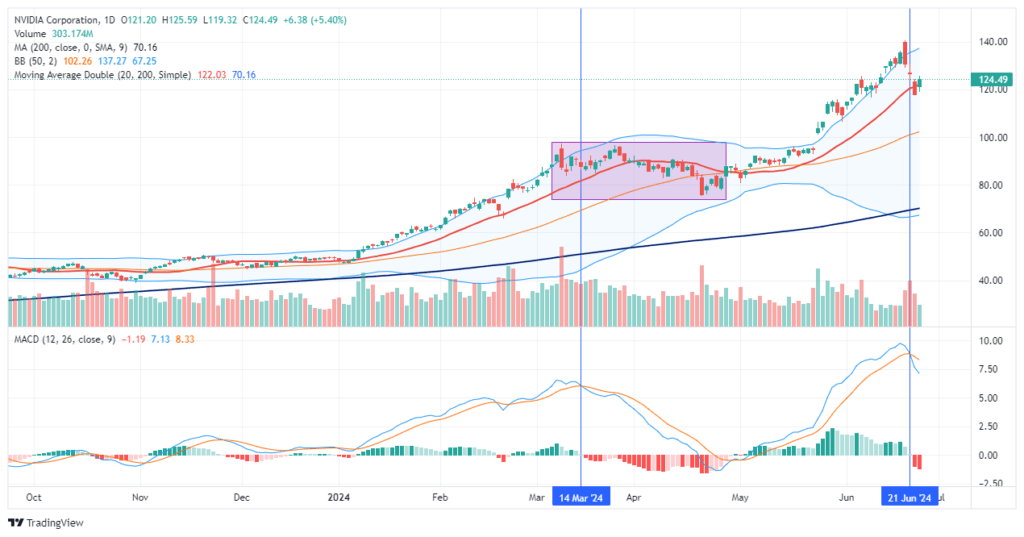

Over the last three days, the mainstream financial media has expressed much angst about the 13% decline in Nvidia (NVDA) shares. Of course, as noted yesterday, Nvidia is a leader in the technology sector (in terms of weighting), and its decline has impacted the entire S&P 500.

As discussed on theReal Investment Showyesterday, despite the nail-biting by the mainstream media and Nvidia bears discussing the end of the A.I. run, the reality was that portfolio managers were overweight shares of Nvidia heading into month end given the post-split run up, and options expiration last Friday, all contributed to the short-term bought of selling. As shown, it is not surprising that Nvidia found support at the 20-DMA and bounced sharply higher as the “A.I. chase” is still in full swing and buyers were looking for a dip to buy.

Notably, while NVDA held support at the 20-DMA and will likely push back towards $135-140/share, we suggest using that rally to rebalance risk. The last time NVDA triggered a MACD “sell signal,” the stock retested the previous highs and drifted lower for a month to reverse the overbought condition. We suspect we could see similar action over the next couple of months heading into the summer. While there is still much momentum behind NVDA, it is overbought, which will likely limit the current upside. To some degree, a reversal would provide a much better entry point to rebuild or increase exposures as needed.

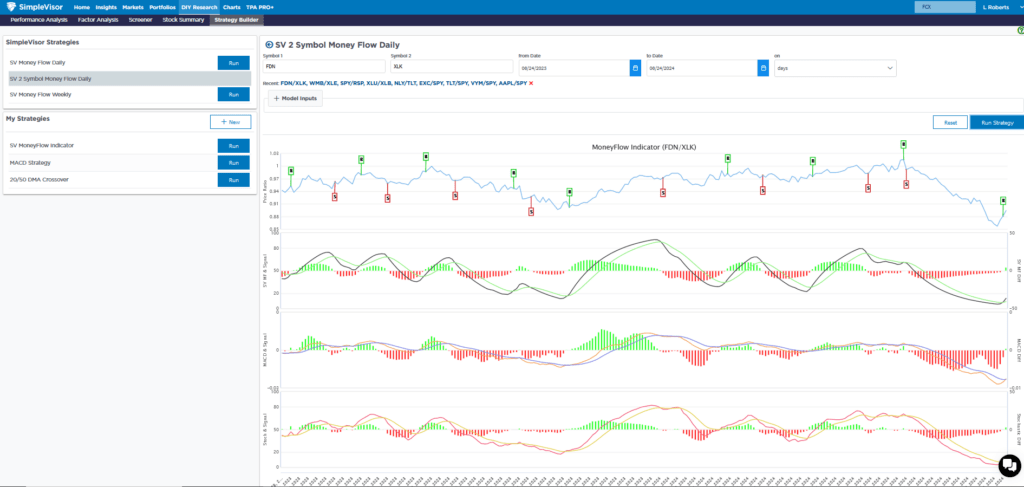

TPA Spots A Rare Divergence Worth Following

Jeffrey Marcus of TPA Analytics recently provided his subscribers with a summary of a critical ETF divergence. The first graph below, from his article, compares the price performance of FDN (internet stocks) and XLK (technology stocks). Nearly 50% of XLK is comprised of Microsoft, Apple, and Nvidia. Amazon, Meta, and Google make up about 30% of the FDN internet ETF. As shown, the two indexes tend to correlate very well. However, recently, they have diverged. Consequently, the unusual price behavior has resulted in what Jefferey believes is a good trade opportunity.

SimpleVisor subscribers can add Jeffrey’s TPA-RRG summary to their subscription package. TPA-RRG analyzes momentum and relative strength to help pick stocks and sectors likely to outperform or underperform the market. XLK is among the best performers, and FDN is near the bottom. Jeffery also points out that the RSI on the top four XLK stocks are decently overbought. As such, he offers the following advice:

Focusing on the 14-day RSI, it is clear that the top 4 stocks on XLK have gotten ahead of themselves (they are overbought). TPA expects that in thenext several weeks, a convergence of XLK and FDN will be seen. This would demand that AMZN, META, GOOGL, and GOOG outperform MSFT, AAPL, NVDA, and AVG as the long-term pattern ofcorrelated performance returns.

The second graphic from SimpleVisor compares the price ratio of FDN to XLK. It too shows that the pair is grossly oversold (FDN compared to XLK), thus supporting TPA’s view that FDN is likely due for better returns than XLK in the coming weeks.

Sector Performance Following Rate Cuts

The Strategas graphic below shows how each sector performed in the six months following the first cut since 1995. Strategas sorts the sectors left to right by the average return. Utilities, staples, and healthcare have the three highest averages. Utilities are the only sector that was positive in all four instances. The recent leading market sector, technology, has the worst average, including two double-digit declines.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

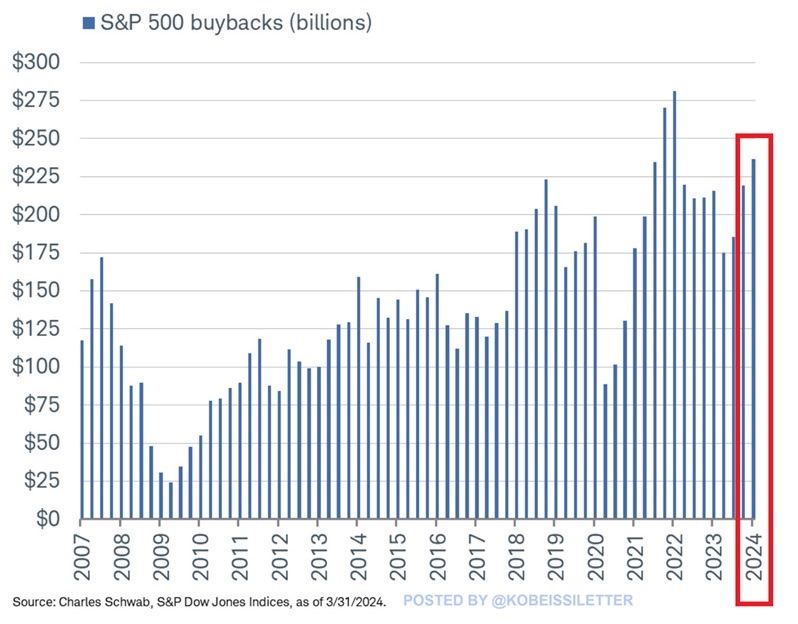

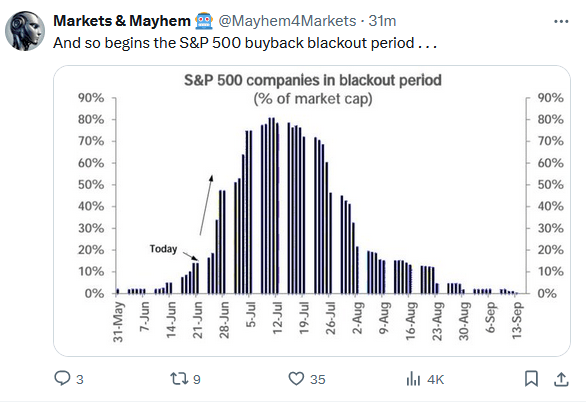

Buybacks Are Back

Over the last six-plus months, we have written plenty on how a few stocks lead the market higher while a large majority languishes. For example, in our latest Newsletter, Bad Breadth Keeps Getting Worse, we wrote the following: “With a market sitting at all-time highs, combined with robust money flows, the breadth of the market should be healthy. However, despite the market advance, the number of stocks above their respective moving averages has declined since April.” Why is this occurring? While there are many reasons, the most impactful may be stock buybacks.

The graph below by @kobeissiletter shows that, as he highlights, $237 billion of stock buybacks occurred in the first quarter. A similar or even greater number of buybacks likely occurred this quarter ending Friday. Furthermore, Goldman Sachs forecasts $925 billion in buybacks this year and over $1 trillion in 2025. Now consider that the 20 largest companies in the S&P 500 account for slightly over half of all buybacks in the first quarter. If buybacks continue at the pace Goldman expects, it will provide a nice tailwind for the largest stocks. Therefore, the bad breadth may continue longer than many think.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we touched on the negative divergences and weakening market breadth. As we noted, while these indicators suggest internal market weakness that precedes corrections historically, the timing of such an event is always problematic. One thing these internals do suggest, from a more immediate impact view, is a limited upside to the market’s advance. Over the last three days, the market has started consolidating recent gains and is working off some overbought conditions. Keep a watch on the MACD signal in the top panel. If it triggers a “sell signal,” we will see further consolidation or a correction until that signal reverses. Such a signal would give investors a better entry point for additional exposure.

The bullish trend remains intact, and investor sentiment remains very bullish. As such, continue to maintain exposure as needed, but, as always, follow risk management protocols for rebalancing as needed.

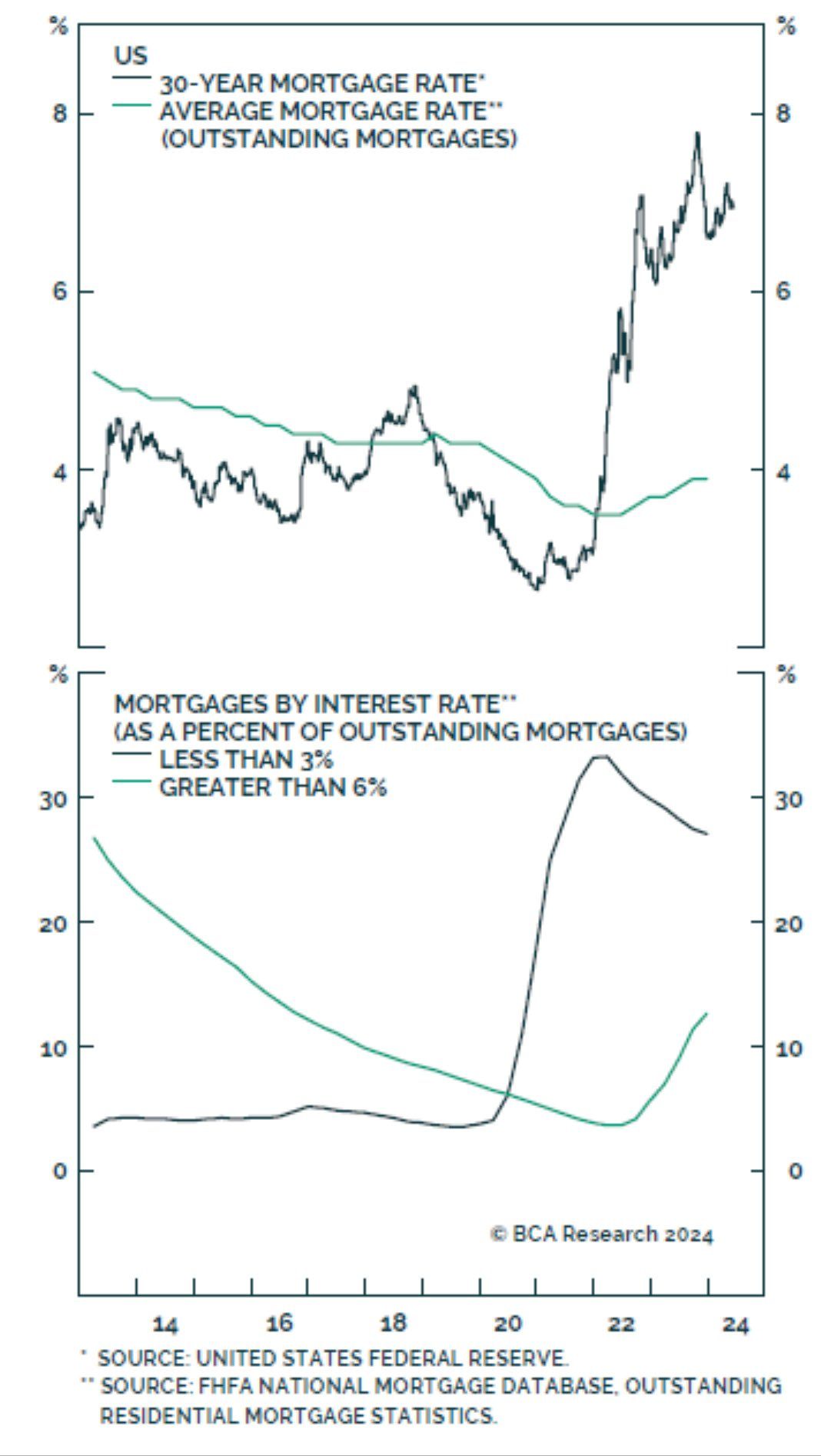

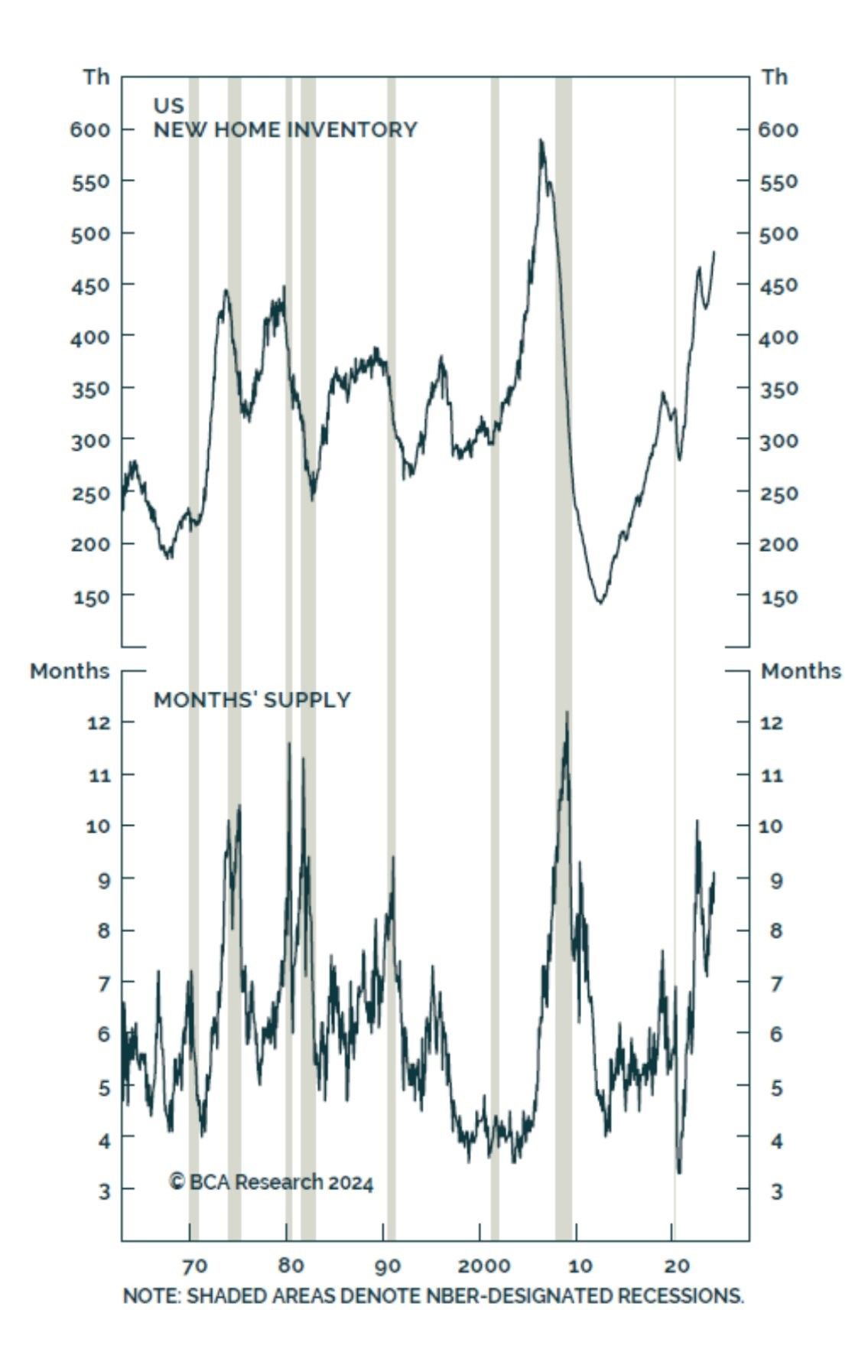

Fed Rate Cuts May Not Help The Real Estate Market

Typically, the Fed has been able to boost economic growth with lower rates. This occurs, in part, because some debtors can refinance debt at lower rates. For example, it has become commonplace to refinance a mortgage when rates fall. Lower payments, in turn, allow consumers to spend more, thus boosting economic activity.

What has worked in the past may be much less effective the next time the Fed cuts rates. The top graph below, courtesy of BCA Research, shows that the average mortgage rate is still below 4%. Mortgage rates would have to drop by nearly 4% to entice the average borrower to refinance. The lower graph shows that about a third of mortgages are 3% or below. Those borrowers will need ten-year yields of near zero percent to refinance.

A similar construct exists in the business world. Many large corporations refinanced their debt in 2020 and 2021 when rates were historically low. If the Fed slowly decreases rates, it’s quite possible the benefits will be much more limited than in the past.

Relative Sector and Factor Analysis

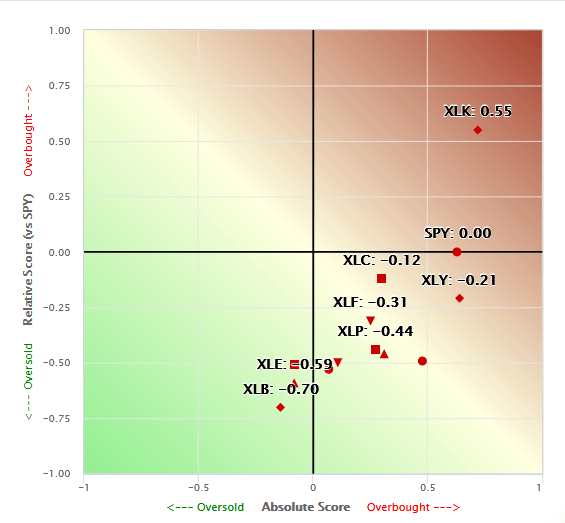

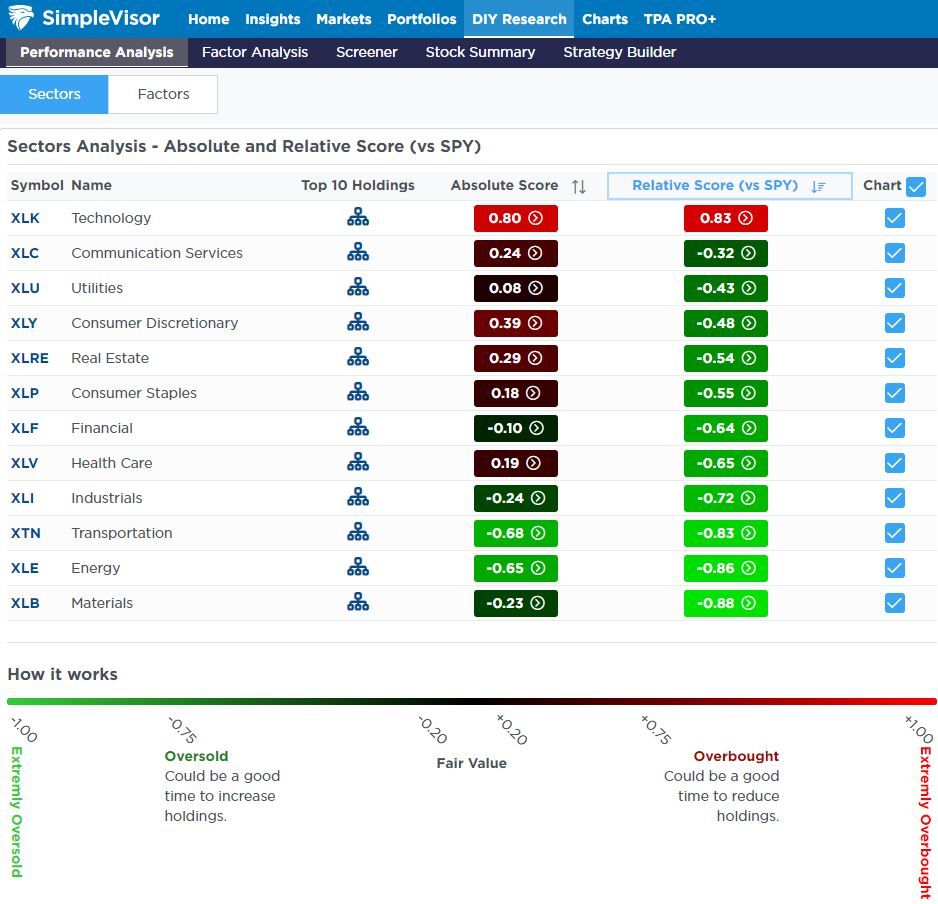

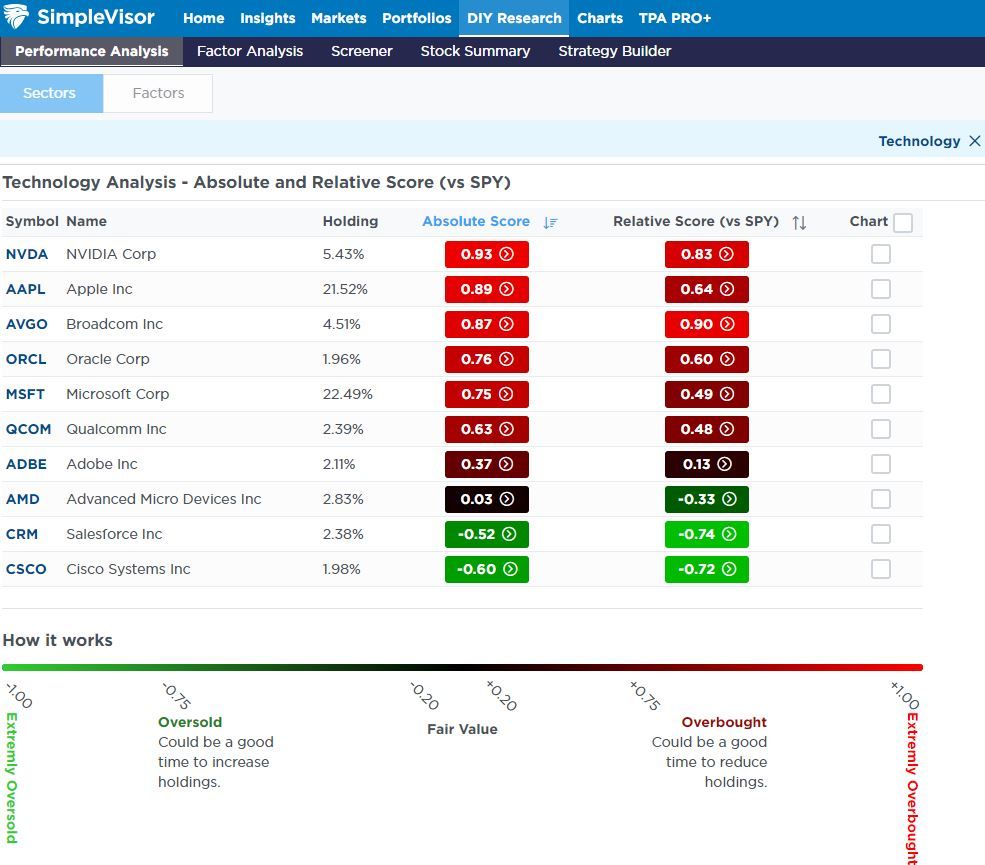

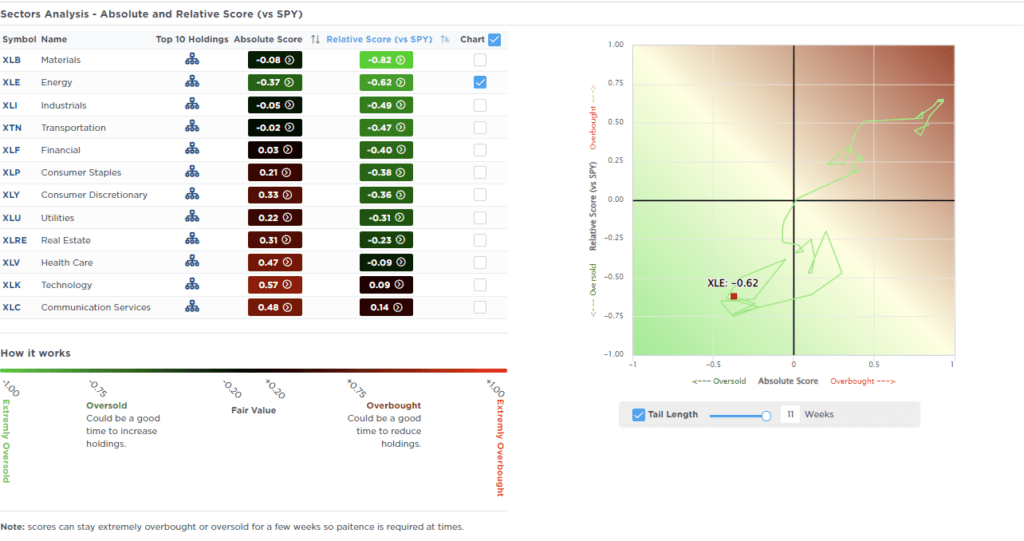

Once again, technology stocks are considerably overbought on a relative analysis. At the same time, every other sector is oversold versus the S&P 500. The first graph charts each sector’s relative and absolute SimpleVisor proprietary scores. XLK (technology) is the only sector with a relative score above zero. Many economically sensitive sectors (materials XLB, energy XLE, and XLI industrials) are very oversold.

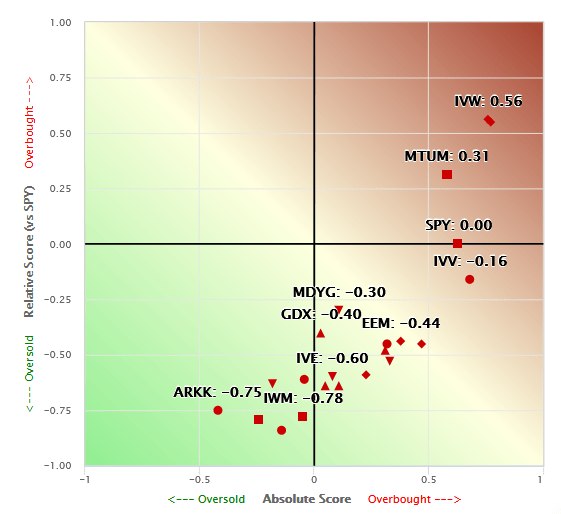

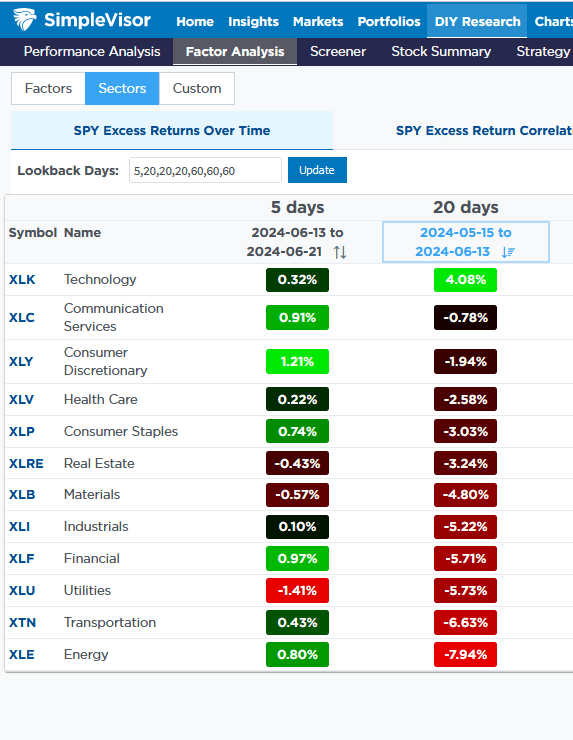

The second scatter plot using stock factors and indexes is very similar. S&P 500 Growth (IVW), Megacap Growth (MGK), and Momentum (MTUM) are the only factors with positive relative scores. Many other factors are grossly oversold. The two most oversold are foreign markets (EFA and VEA). The third table shows that XLK is up 4.08% over the last four weeks. Conversely, every other sector is lower over the period. Furthermore, half of the sectors are down by 5% or more.

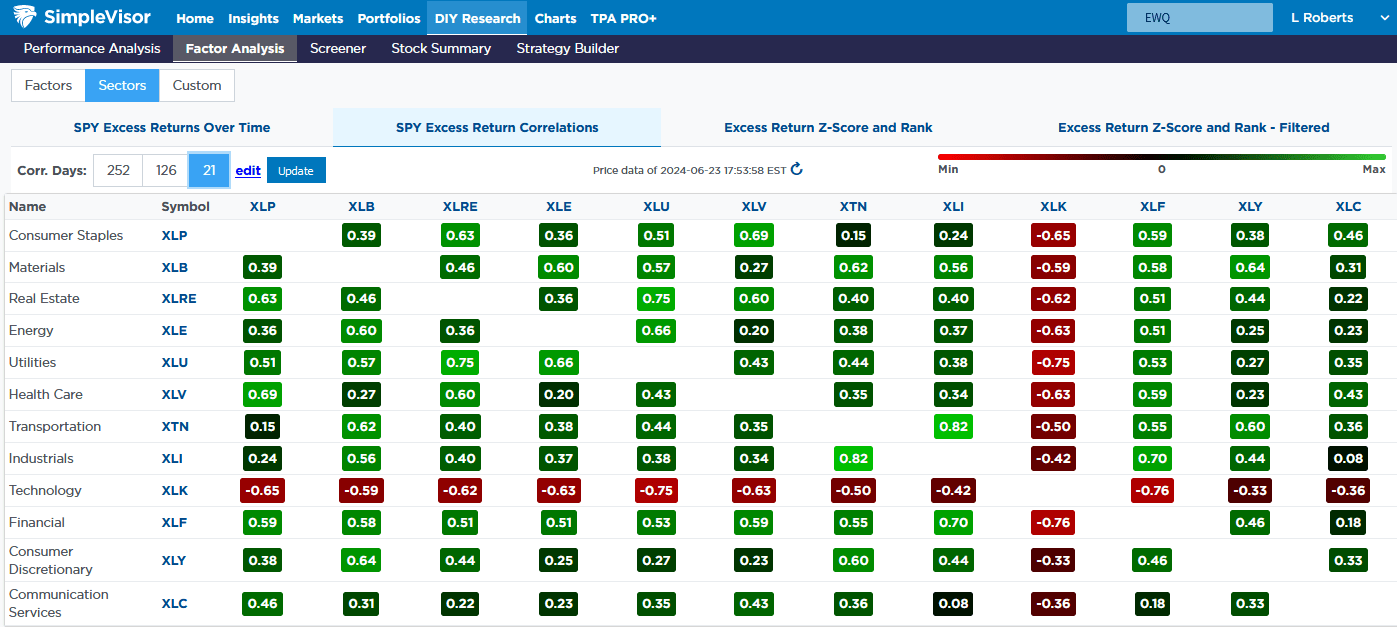

Lastly, the fourth table shows the price correlations of each sector versus every other sector for the last 21 days. XLK has a negative correlation to every sector, while every other sector is positively correlated to each other. The set of images below helps better appreciate the horrendous market breadth.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

S&P 6300? Is That Outside The Realm Of Possibility?

Goldman Sachs recently upped its price target to S&P 6300 for the end of this year, along with Evercore ISI upping its year-end target to 6000. Such is not surprising given the strong run in the markets this year. Just two weeks ago, I posted the following chart saying:

“We should soon start getting a raft of S&P 500 price target upgrades for year-end.”

While such a bold number may seem unrealistic, there is a fundamental case to support it.

“There are many reasons why valuations have shifted higher over the years. The increase is partly due to economic expansion, globalization, and increased profitability. However, since the turn of the century, changes in accounting rules, share buybacks, and greater public adoption of investing (aka ETFs) have also contributed to the shift. Furthermore, as noted above, the massive monetary and fiscal interventions since the “Financial Crisis” created a seemingly “risk-free” environment for equity risk.

The chart shows the apparent shift in valuations.”

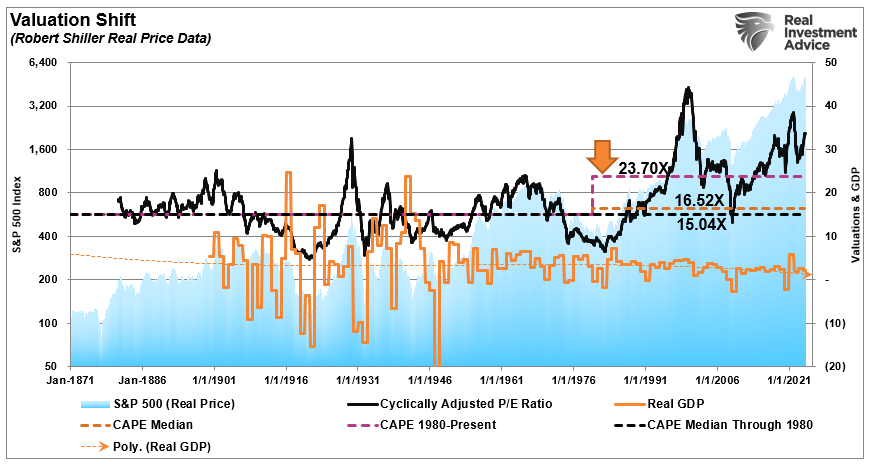

The “median” CAPE ratio is 15.04 times earnings from 1871-1980.

The long-term “median” CAPE is 16.52 times earnings from 1871-Present (all years)

The “median” CAPE is 23.70 times earnings from 1980 to the present.

There are two critical things to consider concerning the chart above.

The shift higher in MEDIAN valuations was a function of falling economic growth and deflationary pressures, and,

Increasing levels of leverage and debt, which eroded economic growth, facilitated higher prices.

So, the question is, “IF” valuations have permanently shifted higher, what will the next market mean-reverting event look like to reset fundamental valuations to a more attractive level?

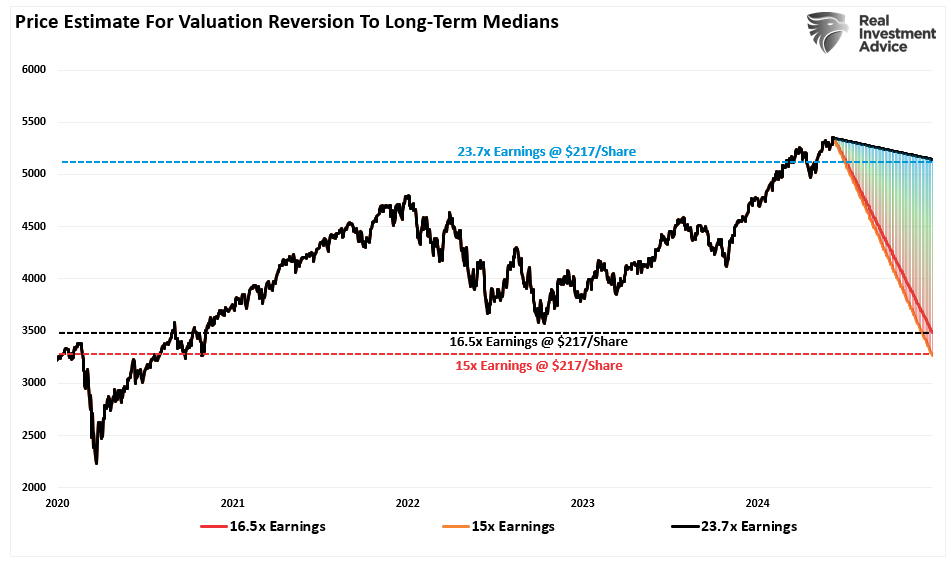

We answered that question by analyzing current market prices and expected earnings to determine the shape of such a valuation reversion.

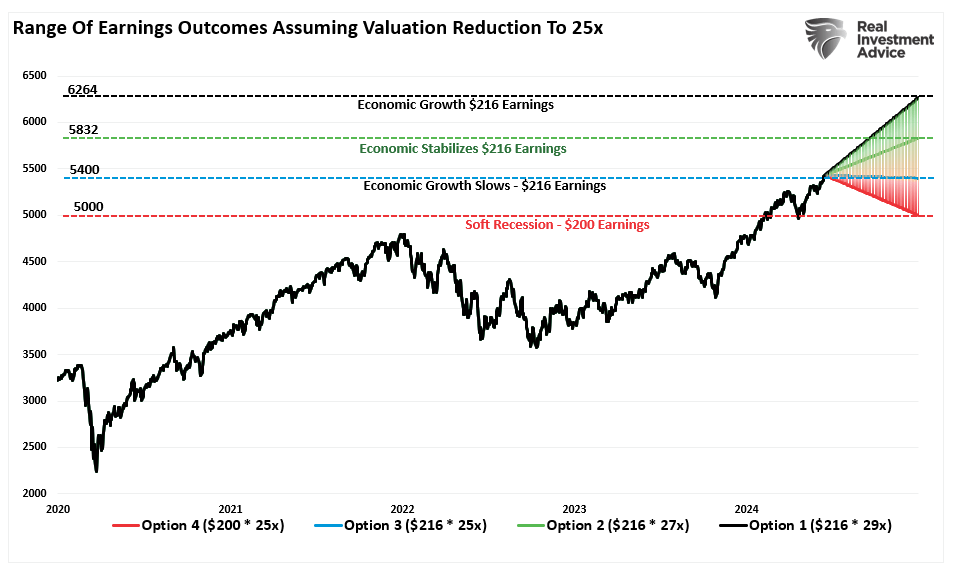

As of this writing, the S&P 500 is trading at roughly $5,300 (we will use a round number for easy math). The projected earnings for 2024 are approximately $217/share. We can plot the price decline needed to revert valuations using the abovementioned median valuation levels.

23.70x = 5142.90 = 3% decline

16.52x = 3584.84 = 33% decline

15.04x = 3263.68 = 38.5% decline

However, that story’s “other side” is where a multiple expansion occurs.

S&P 6300 – The Other Side Of The Story

How did we pick S&P 6300? We used a standard Fibonacci sequence to identify the logical, numerical sequence from the November 2023 lows. From those lows, an extension of 1.62% would take the market to roughly 6300 (6255, to be exact). However, for the market to make that advance, the underlying earnings will need to support the continued rise.

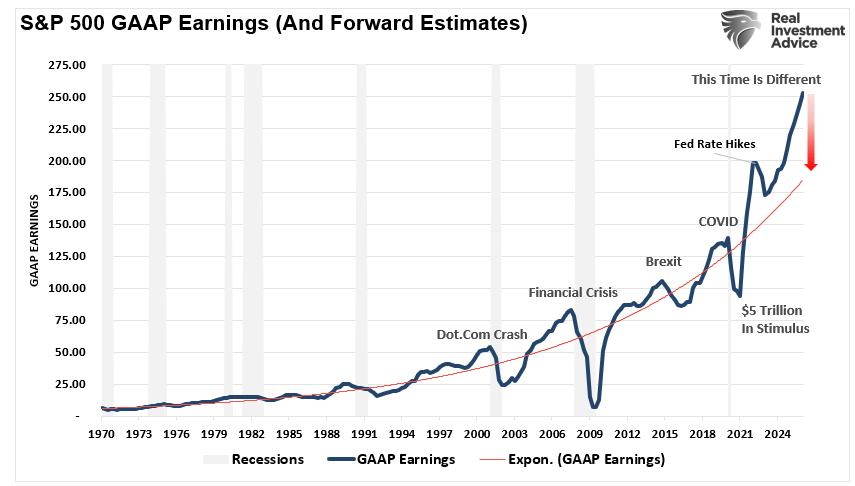

As noted in the previous article, valuation contractions happen during recessionary and bear market periods. During such a phase, the exuberance of the market realigns the price of the market with the underlying fundamentals. However, multiple expansions are underway before the beginning of the reversion process. During this bullish phase, Wall Street analysts continue to ratchet earnings estimates higher to justify rising prices. Currently, we are in the multiple expansion phase, where analysts are dramatically increasing earnings estimates to more extreme levels. As shown, the earnings estimates for 2025 are at a record deviation from the long-term exponential growth trend.

So, how can the S&P 500 get to 6300? We can use current Wall Street estimates to work backward through the valuation process. As we did previously, we usually look at the market’s price and determine the “fair value” of the market based on expected earnings. In this case, we will take the denominator (earnings) of the valuation equation to find the “fair price” of the market.

While Goldman is looking at 6300 for the end of this year, for this thought experiment, we will use S&P Global’s current estimates of $216/share for the end of 2024. For Goldman’s estimate of 6300, trailing one-year valuations will rise to 29x earnings. However, we will also assume some lower valuation of 27x and 25x earnings by year-end if economic growth continues to slow. Furthermore, we will consider a drop in earnings to $200/share if the economy starts heading into a soft recession. However, given that Wall Street estimates are always overly optimistic, a deeper discount in earnings is possible. However, those parameters give us the following results.

$216/share * 29x Trailing Earnings = 6264(Assumes continued economic growth)

As we did previously, we can use these forecasts to build a chart showing the range of potential outcomes over the next 6 months.

Those outcomes are just one set of assumptions. By adjusting valuation and earnings expectations, we could create infinite possibilities. The purpose of the exercise, however, is to establish a reasonable range of possibilities for the market at the end of the year. As shown, the range of potential outcomes is broad from market levels at the time of this writing. The bullish argument of “no recession” suggests a possible upside from 7.4% to 15%. However, if the economy slows or slips into a soft recession, the potential downside ranges from a -1% loss to -8%.

Challenges Remain

Let me state that I have no idea what the next 6 to 18 months hold in store. As noted, there are an infinite number of possibilities. What happens in the November election, Fed policy, and the potential for a recession will all affect one of those outcomes.

Here is our concern with the bullish scenario. It entirely depends on a “no recession” outcome, and the Fed must reverse its monetary tightening. The issue with that view is that IF the economy does indeed have a soft landing, there is no reason for the Federal Reserve to reverse its balance sheet reduction or cut interest rates drastically.

More importantly, the rise in asset prices continues to ease financial conditions, keeping inflation “sticky,” thereby eroding consumer purchasing power. The bull case also suggests that employment remains strong, along with wage growth, but there is clear evidence of erosion on both.

While the bullish scenario of S&P 6300 is possible, that outcome faces many challenges heading into 2025, given the market already trades at fairly lofty valuations. Even in a “soft landing” environment, earnings should weaken, making current valuations more challenging to sustain.

Our best guess is that reality lies somewhere in the middle. Yes, there is a bullish scenario in which earnings decline, and a monetary policy reversal leads investors to pay more for lower earnings. However, that outcome has a limited lifespan as valuations matter to long-term returns.

As investors, we should hope for lower valuations and prices, which gives us the best potential for long-term returns. Unfortunately, we don’t want the pain of getting there.

Regardless of which scenario plays out in real-time, there is a substantial risk of poor returns over the next 6-18 months. As investors, we must manage the risk of an unexpected turn of events undermining Wall Street’s continued optimistic views.

After all, the math is just the math.

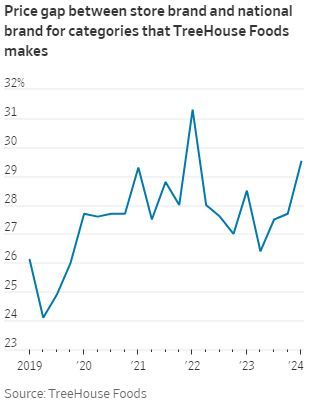

Consumers Are Turning to Private Label Brands

Consumers are turning away from name-brand foods in an attempt to cut back on spending. Consumer Packaged Goods (CPG) companies such as Proctor & Gamble, General Mills, and Kellogg benefited from supply chain disruptions during the pandemic as private label products saw restricted supply. Thus, the CPG brands with more resilient supply chains used the combination of shortages and heightened demand for food at home to exercise pricing power. As shown below, the price premium between national and store brands for TreeHouse Foods, a private-label manufacturer, remains substantially higher than pre-pandemic levels.

However, this advantage also meant that CPG brands relaxed their efforts to innovate their product lines. Private-label brands are also honing in on quality, meaning CPG brands must compete through innovation or lowering prices to maintain market share. The latter seems more likely, given the recent retail sales data. Now that supply chain pressures have alleviated and inflation is straining household budgets, consumers are turning to private-label brands to control costs. Per the Wall Street Journal:

Amid elevated demand for food at home and consumer wallets flush with stimulus cash, CPG companies were able to raise prices without much resistance. But that is now quickly changing as retailers deal with price-sensitive consumers increasingly exhausted with the cumulative impact of inflation: Grocery prices are about 26% higher than they were in 2019. In a recent survey of U.S. consumers by Jefferies, some 51% of respondents said they are buying more private-label products to save money on grocery bills.

What To Watch Today

Earnings

No notable earnings releases.

Economy

Market Trading Update

Last week, we discussed the issue of the negative divergences and bad breadth of the market. To wit:

“While the bullish trend remains intact, along with a MACD ‘buy signal,’ which suggests an increased allocation to equity exposure, we have some concerns.

While the market is making all-time highs as momentum continues, its breadth is narrowing. The number of stocks trading above their respective 50-DMA continues to decline as the market advances, along with the MACD signal. Furthermore, the NYSE Advance-Decline line and the Relative Strength Index (RSI) have reversed, adding to the negative divergences from a rising market. While this does not mean the market is about to crash, it does suggest that the current rally is weaker than the index suggests.

As we discussed, these negative divergences have often preceded short- and intermediate-term corrective market actions. Such is the point where Investors tend to make two mistakes. The first is overreacting to these technical signals, thinking a more severe correction is coming. The second is taking action too soon.

Yes, these signals often precede corrections, but there are also periods of consolidation where the market trades sideways. Secondly, reversals of overbought conditions tend to be shallow in a momentum-driven bullish market. These corrections often find support at the 20 and 50-day moving averages (DMA), but the 100 and 200-DMAs are not outside normal corrective periods.

If you remember, in March, we discussed the potential for a 5 to 10% correction due to many of the same concerns noted above. That correction of 5.5% came in April. We are again at a juncture where a 5-10% is likely. The only issue is it could come anytime between now and October.

As is always the case, timing is always the biggest risk. Therefore, be careful not to overreact or act too soon. The market will let us know when to become more aggressive in reducing risk.

The Week Ahead

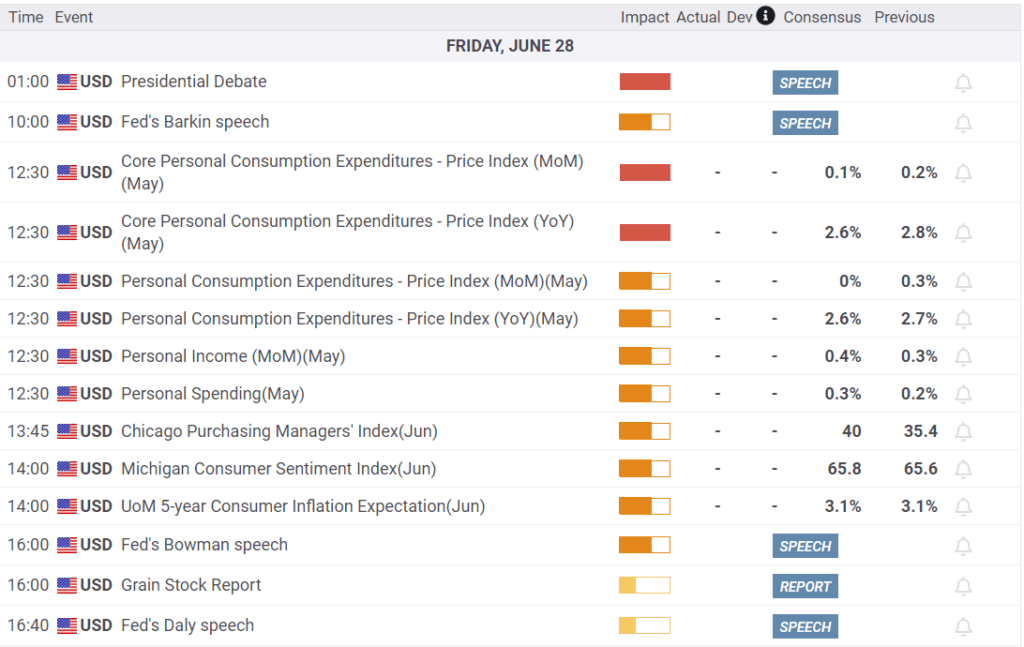

The second quarter comes to an end this week. The primary focus will be PCE prices plus personal income and outlays on Friday. The all-important core PCE price index is the Fed’s preferred measure of inflation; thus, it carries extra weight. The consensus expects personal income to rise 0.4% MoM in May versus the 0.3% increase in April. Meanwhile, the consensus expects personal expenditures to rise by 0.3% MoM in May after increasing by 0.2% in April.

This week starts slowly with speeches by the Fed’s Waller and Daly today. Tomorrow, we will hear from Bowman and Cook and get data on April home prices via the Case-Shiller Home Price Index. We’ll also get updated consumer confidence data, where the consensus forecasts a decrease to 100 in June from 102 in May. Wednesday will bring New Home Sales data for May. We don’t expect any positive surprises, given that consumers are turning down purchases due to high mortgage rates. Durable Goods Orders for May are released on Thursday. The consensus expects a slowdown in growth to 0.3% in May from 0.7% in April. As mentioned above, we cap off the quarter with PCE prices and personal income & outlays on Friday.

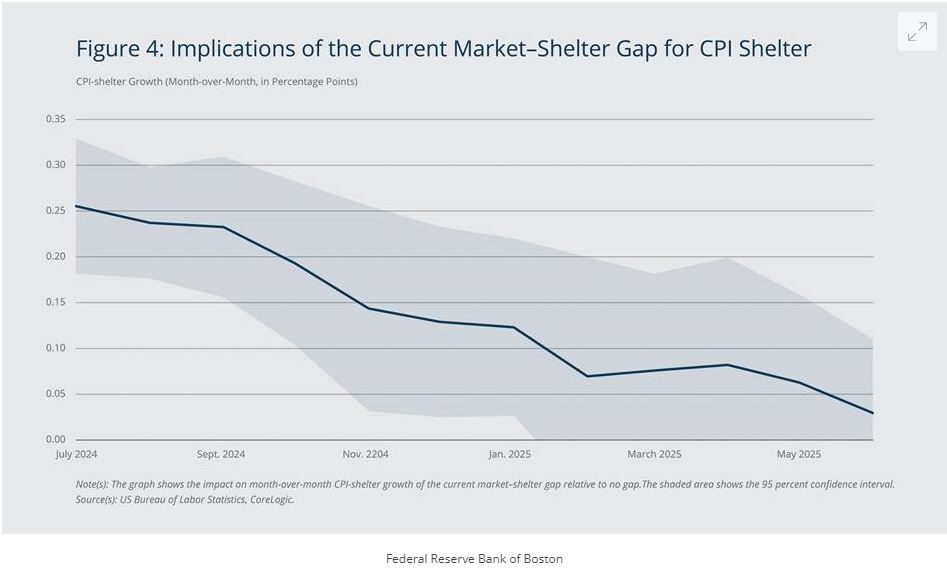

Boston Fed Economist: Shelter Inflation May Be Stubborn Through Year-End

A recently published paper by a Boston Fed Economist suggests that rent increases will keep inflation above the Fed’s target for longer than most expect. The Author proposes that the effect will be most notable through the end of 2024 and diminish significantly in 2025. In addition, the Author expects CPI shelter inflation to slow considerably in periods beyond the next twelve months. His research focuses on the gap between market rent and the shelter component of CPI and how those dynamics pass through to CPI and PCE. Below, we provide excerpts and a chart from the paper that sums it up nicely.

The overall trend is clear: CPI shelter is expected to grow quickly in the summer and fall of 2024 but then slow down markedly when we move into 2025. Therefore, according to the estimates, the market–shelter gap is likely to pose a significant, but diminishing, challenge to the Fed’s ability to achieve its 2 percent inflation target over the next year.

Back-of-the-envelope calculations show how high CPI shelter could raise overall inflation this year. Given that shelter comprises 36.1 percent of the CPI and 15.5 percent of the PCE, the post-pandemic pass-through estimates imply that the current market–shelter gap will lead to an additional 0.59 and 0.25 percentage point growth in headline (including food and energy) CPI and headline PCE, respectively, from June 2024 to June 2025 relative to there being no market–shelter gap. The estimates also show that the deviation will lead to an additional growth in core (excluding food and energy) CPI and core PCE of 0.74 percentage point and 0.29 percentage point, respectively, from June 2024 to June 2025.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

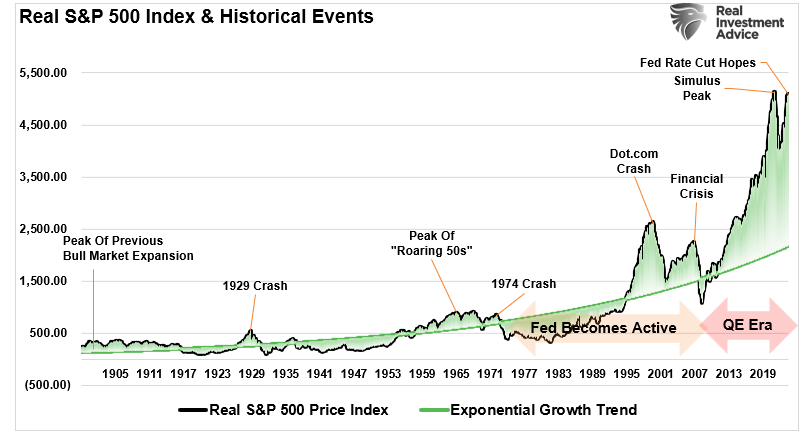

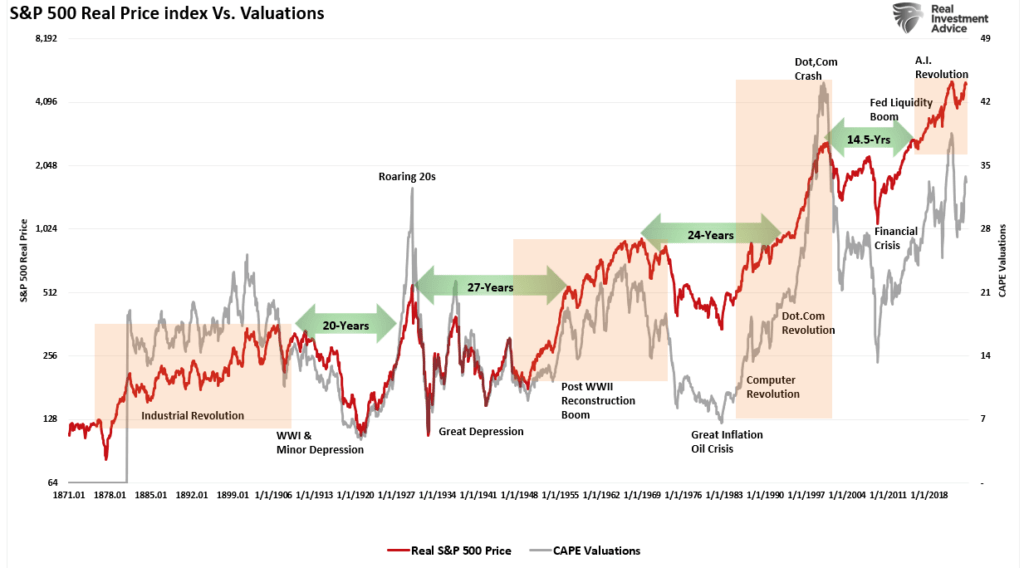

A Fundamental Shift Higher In Valuations

Over the last decade, there has been an ongoing fundamental debate about markets and valuations. The bulls have long rationalized that low rates and increased liquidity justify overpaying for the underlying fundamentals. For the last decade, that view appears correct as zero interest rates combined with massive monetary and fiscal support increased market returns by 50% since 2009. We discussed this point in“Long-Term Returns Are Unsustainable.” To wit:

“The chart below shows the average annual inflation-adjusted total returns (dividends included) since 1928. I used the total return data from Aswath Damodaran, a Stern School of Business professor at New York University. The chart shows that from 1928 to 2021, the market returned 8.48% after inflation. However, notice that after the financial crisis in 2008, returns jumped by an average of four percentage points for the various periods.”

As noted, an unprecedented amount of monetary accommodation drove those excess returns. Unsurprisingly, this resulted in one of the most significant deviations from the market’s exponential growth trend.

(Usually, when charting long-term stock market prices, I would use a log-scale to minimize the impact of large numbers on the whole. However, in this instance, such is not appropriate as we examine the historical deviations from the underlying growth trend.)

Wall Street Exuberance

The fiscal policies implemented after the pandemic-driven economic shutdown created a surge in demand that further exacerbated an already extended market. As shown, those fiscal interventions led to an unprecedented surge in earnings, with current expectations through 2025 significantly extended.

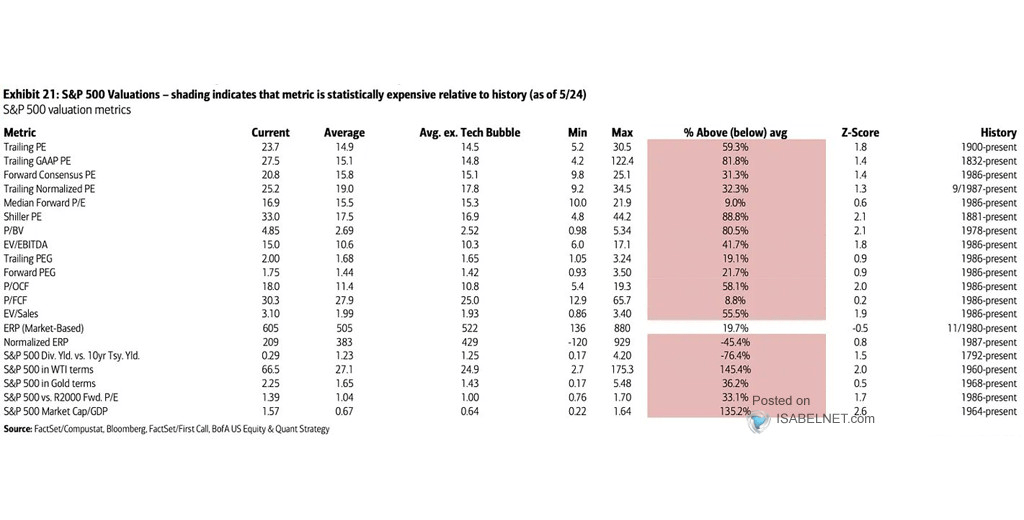

Given that markets historically track the annual change in earnings, it is unsurprising that stocks have once again reached more extreme valuation levels, given the rather ebullient forecast. The table below, from BofA, shows 20 different valuation measures for the S&P 500 index. Except for market-based equity risk premium (ERP), every other measure is at some of the most extreme levels.

Unsurprisingly, when discussing more extreme fundamental valuations, the expectation is that a more significant correction will eventually occur. While historically, the markets have often experienced “mean reverting events,” we will explore how the past 20 years of monetary and fiscal interventions have potentially permanently shifted market valuations higher.

A Permanent Shift Higher

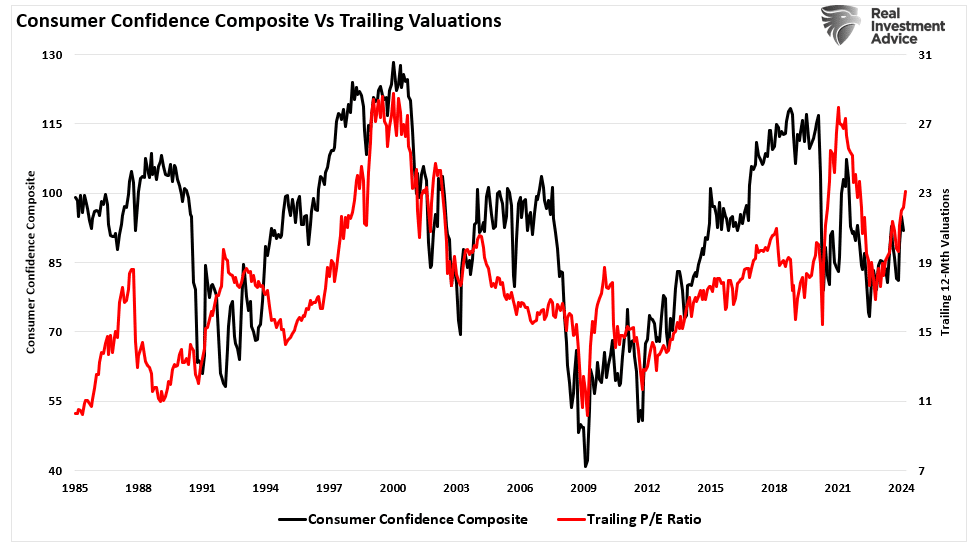

As discussed in “Technical Measures,“ valuations are a terrible market timing tool. Valuations only measure when prices are moving faster or slower than earnings. As we noted, in the short-term valuations are a measure of psychology. To wit:

“Valuation metrics are just that – a measure of current valuation. More importantly, when valuation metrics are excessive, it is a better measure of ‘investor psychology’ and the manifestation of the ‘greater fool theory.’ As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations.”

However, just because current valuations are elevated, does that mean a massive mean reverting event is required?

Maybe not.

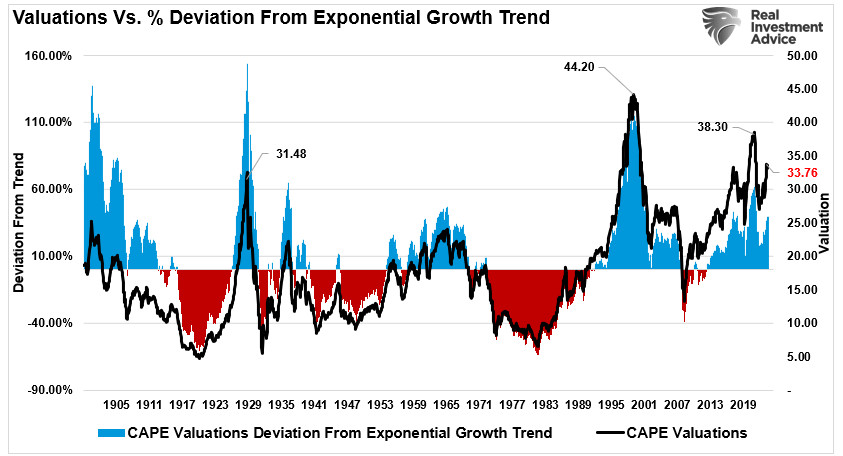

Dr. Robert Shiller’s fundamental valuation method, using ten years of earnings, or the cyclically adjusted price-earnings ratio (CAPE), is over 33 times trailing earnings. While that valuation level seems elevated on a nominal basis, its deviation from the long-term exponential growth trend is not. While 33x earnings is a high price for future earnings (implying 33 years to break even), the reduced deviation from the long-term exponential growth trend exposes the shift higher in valuation levels.

There are many reasons why valuations have shifted higher over the years. The increase is partly due to economic expansion, globalization, and increased profitability. However, since the turn of the century, changes in accounting rules, share buybacks, and greater public adoption of investing (aka ETFs) have also contributed to the shift. Furthermore, as noted above, the massive monetary and fiscal interventions since the “Financial Crisis” created a seemingly “risk-free” environment for equity risk.

The chart shows the apparent shift in valuations.

The “median” CAPE ratio is 15.04 times earnings from 1871-1980.

The long-term “median” CAPE is 16.52 times earnings from 1871-Present (all years)

The “median” CAPE is 23.70 times earnings from 1980 to the present.

There are two critical things to consider concerning the chart above.

The shift higher in MEDIAN valuations was a function of falling economic growth and deflationary pressures, and,

Increasing levels of leverage and debt, which eroded economic growth, facilitated higher prices.

So, the question is, “IF” valuations have permanently shifted higher, what will the next market mean-reverting event look like to reset fundamental valuations to a more attractive level?

Mapping A Reversion To The Mean

Many video channels, commentators, and media types suggest another “major market correction” is coming. There are many reasons for their claims running the gamut, including de-dollarization, loss of the reserve currency, higher rates, debt defaults, etc. As we noted previously, while these arepossibilities, they are pretty remote.

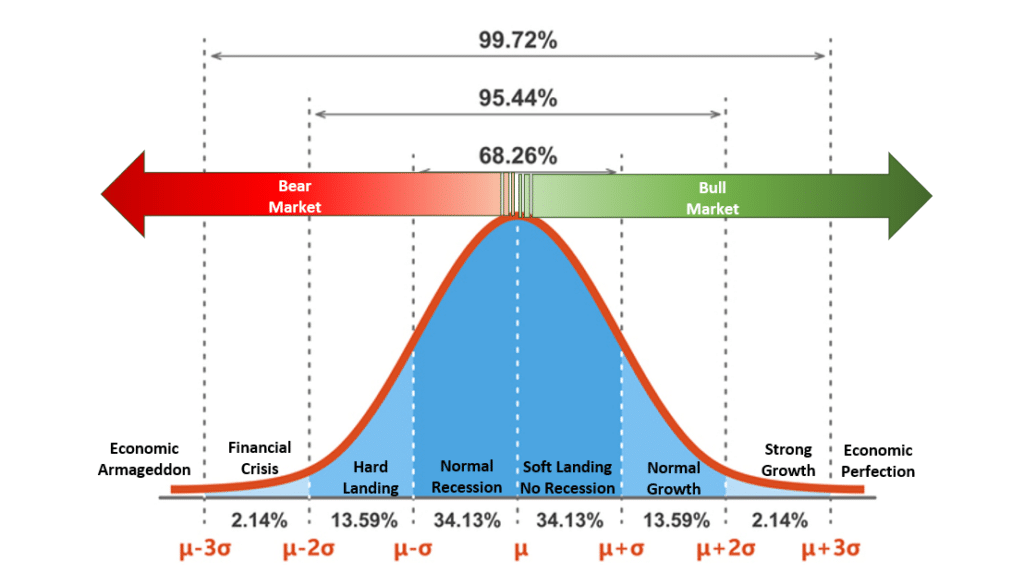

“The chart below is a normally distributed “bell curve” of potential events and outcomes. In simple terms, 68.26% of the time, typical outcomes occur. Economically speaking, such would be a normal recession or the avoidance of a recession. 95.44% of the time, we are most likely dealing with a range of outcomes between a reasonably deep recession and standard economic growth rates. However, there is a 2.14% chance that we could see another economic crisis like the 2008 Financial Crisis.

But what about “economic armageddon?”

That event where nothing matters but “gold, beanie weenies, and bunker.” That is a 0.14% possibility.“

While “fear sells,” we must assess the “probabilities” versus “possibilities” of various outcomes. Since valuations are a fundamental function of price and earnings, we can use the current price of the market and earnings to map out various valuation reversions.

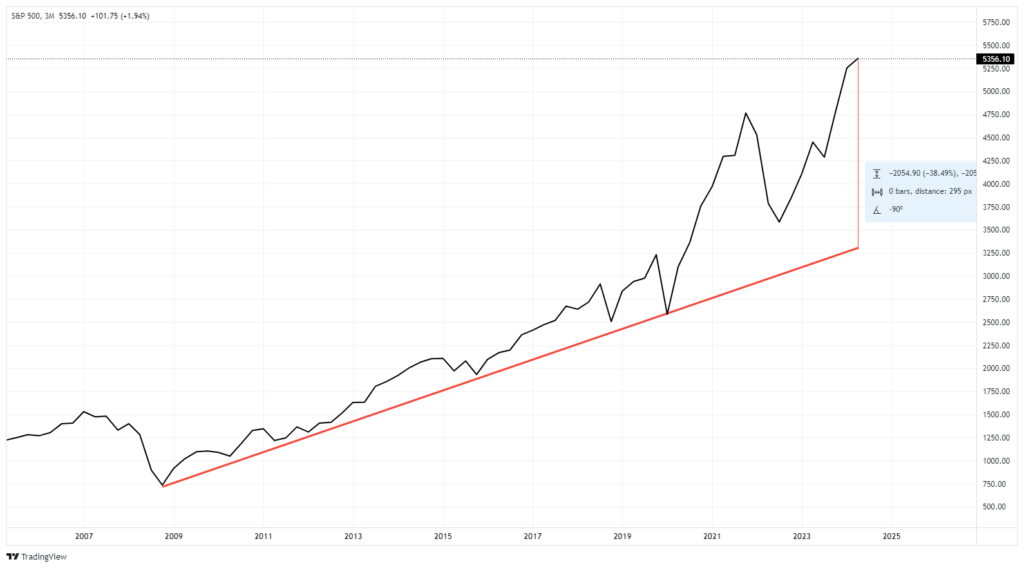

As of this writing, the S&P 500 is trading at roughly $5,300 (we will use a round number for easy math). The projected earnings for 2024 are approximately $217/share. We can plot the price decline needed to revert valuations using the abovementioned median valuation levels.

23.70x = 5142.90 = 3% decline

16.52x = 3584.84 = 33% decline

15.04x = 3263.68 = 38.5% decline

Here is the vital point.

While a near 40% decline in stocks is quite significant and would undoubtedly send the Federal Reserve scrambling to cut rates and restart “Quantitative Easing,” the reversion would only reverse the post-pandemic stimulus-driven gains. In other words, a near 40% correction would NOT be a “bear market” but just a correction in the ongoing bull market since 2009. (This shows how egregious the price deviation has become from the long-term price trend since the pandemic.)

Conclusion

While this is just a thought experiment, there are two critical takeaways.

The deviation from the long-term means is extreme, suggesting a more significant decline is possible in the future and

While valuations are elevated relative to long-term history, if there has been a permanent shift in valuations, the subsequent correction may not be as deep as some expect.

Importantly, investors repeatedly make the mistake of dismissing valuations in the short term because there is no immediate impact on price returns. As noted above, valuations, by their very nature, are HORRIBLE predictors of 12-month returns. Therefore, investors should avoid any investment strategy that has such a focus. However, in the longer term, valuations excellent predictors of expected returns.

From current valuation levels, investors’ expected rate of return over the next decade will be lower than it was over the past decade. That is unless the Federal Reserve and the government launch another massive round of monetary stimulus and cut interest rates to zero.

This does not mean that markets will produce single-digit rates of return each year for the next decade. There will likely be some tremendous investing years over that period and a couple of tough years in between.

That is the nature of investing and the market cycles.

Communication Data Implies Remote Work is Here to Stay