Conviction (kan-vik-shan): noun, a strong persuasion or belief; the state of being convinced.

In life, there are things that we should be convicted and committed to. For example, the love for our families, spouses, and religious beliefs. We can also be convicted about other things, such as political ideologies, social issues, and environmental causes. With the rise of social media, individuals’ conviction is easy to see and the source of the “great divide” in today’s society (and I would argue not for the better.)

However, when investing, having an absolute conviction in any ideology or thesis can lead to lost opportunity or lost capital over time. Friederik Gieschen wrote an interesting post about great investors and the risk of conviction to capital.

“This presents an obvious challenge. Not only do you have to be right, but you also have to survive until reality and the market catch up with your view. Otherwise, you won’t get paid. Just ask van Gogh. Or Michael Burry, almost. And in the interim, the market can throw all kinds of antics. Short seller John Hempton: ‘We found the Wirecard fraud in 2009. It went from 9 to 191 euros and then to zero. It was our biggest ever loser.'”

So, what are your convictions regarding investing and your portfolio? Here is a short list of some of the most current:

- The dollar is “fiat” and is going to zero.

- The dollar will lose its reserve currency status.

- There is too much debt, and the U.S. will eventually default.

- A recession or depression is coming because (fill-in-the-blank) said so.

- There is going to be a worldwide shortage of food and oil.

- Interest rates can only go higher.

- The Government is going to confiscate everything.

- Society is on the edge of collapse.

- Add your personal conviction here.

There are obviously many more.

Importantly, all of these things could indeed happen. I am surely not prescient enough to see that far into the future.

The Beauty Contest

However, when it comes to investing, these “convictions” can take longer to come to fruition than you have years to live. Furthermore, given that both the markets and the economy evolve over time, it is likely that many of these convictions will never come to pass or will take some far less dire form.

As Gieschen noted, not only is the market always shifting and reconfiguring itself, but it’s also a complex adaptive system. This means its participants are aware of their own history. Indicators are a great example of the Keynesian beauty contest in which observers move from observing the object to observing each other.

“It is not a case of choosing those [faces] that, to the best of one’s judgment, are really the prettiest, nor even those that average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth and higher degrees.” (Keynes, General Theory of Employment, Interest and Money, 1936).

In other words, if the market, which is a living, breathing organism of the collective minds of investors, begins to sense your conviction, it will take advantage of your positioning to take money away from you. As the old saying goes, the market is adept at shifting capital from “weak hands to strong hands.”

An Example Of Conviction Gone Wrong

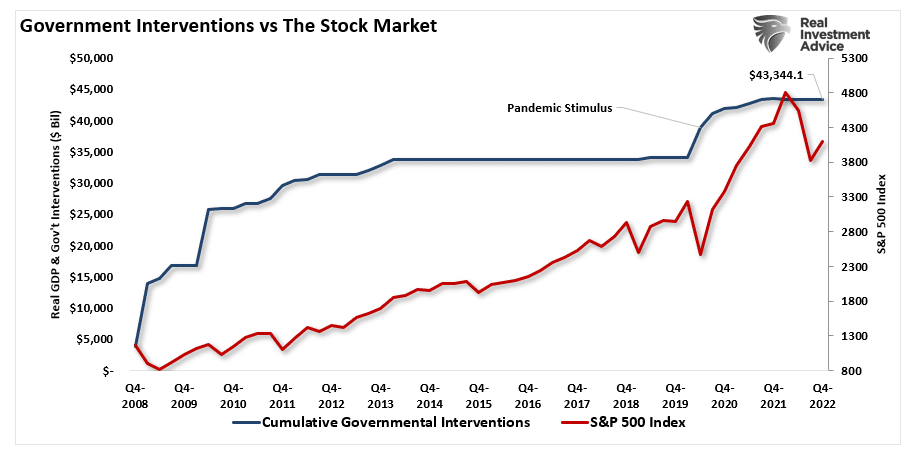

Over my many years of managing money, I have received countless emails from individuals convinced that certain things would happen. One good example was during the “financial crisis” in 2008. In February 2009, I wrote an article discussing 8-reasons why investors should start buying stocks. I was inundated by emails berating me for such a call as it was obvious the “world had just ended, and the stock market was going to zero.”

Of course, that didn’t happen as the Federal Reserve and the Government intervened with various bailouts, liquidity supports, and forcing interest rates to zero.

But, the “gold bugs” doubled down on their conviction as it was apparent the Government was printing money which would lead to the dollar’s demise, surging inflation, and interest rates.

Such certainly seemed logical.

But it didn’t happen.

Then in 2020, the pandemic struck the U.S., and the Government shut down the economy. Again, it was believed the market was going to zero, the world would end, and gold was the only investment worth owning.

For a second time, the conviction of the “end of the civilized world” scenario has failed to come to fruition as the Government again intervened by dropping rates to zero and flooding the system with liquidity. Such was a point made recently in Bullish Investors Fight The Fed.”

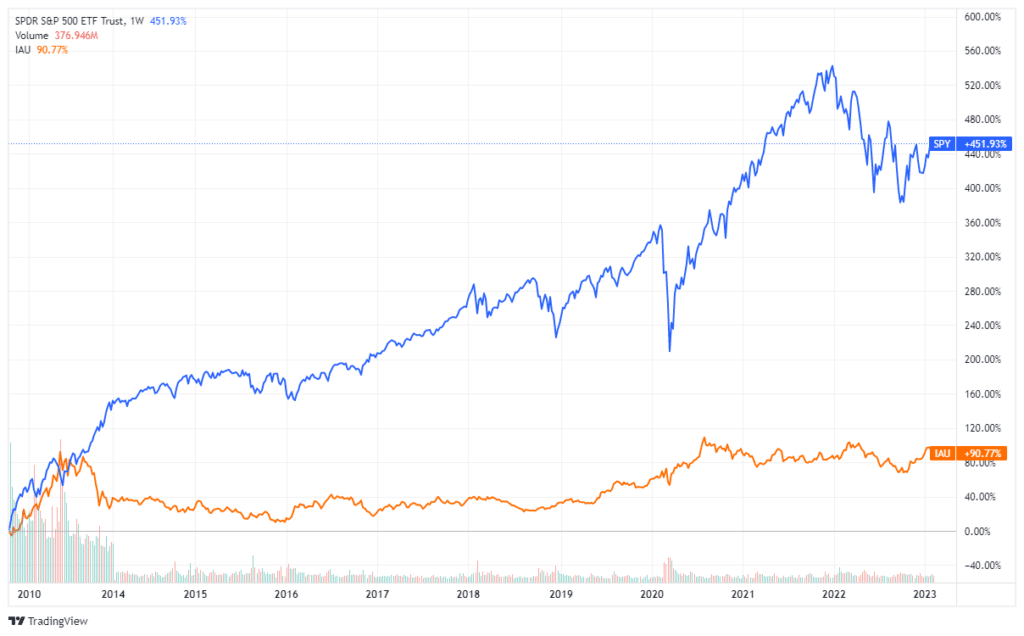

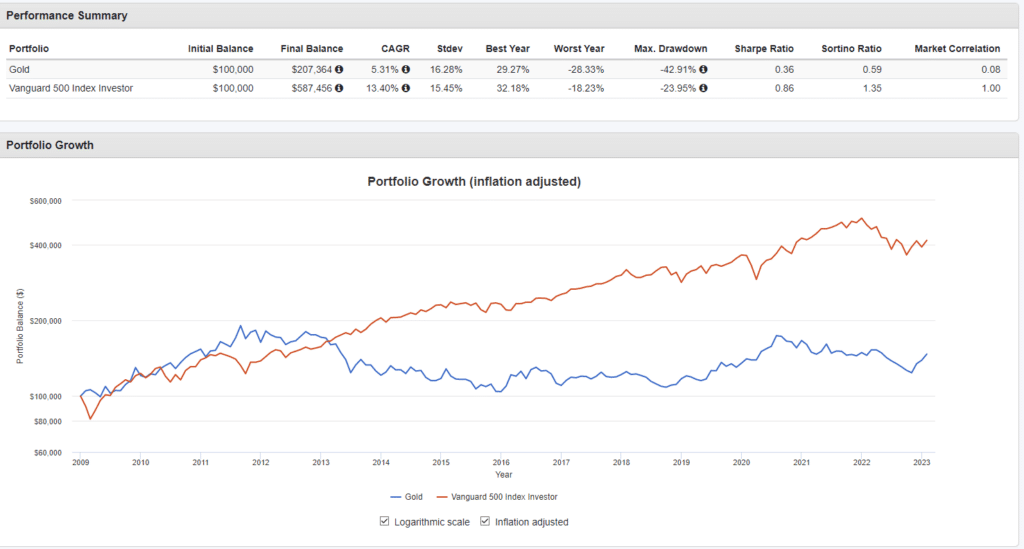

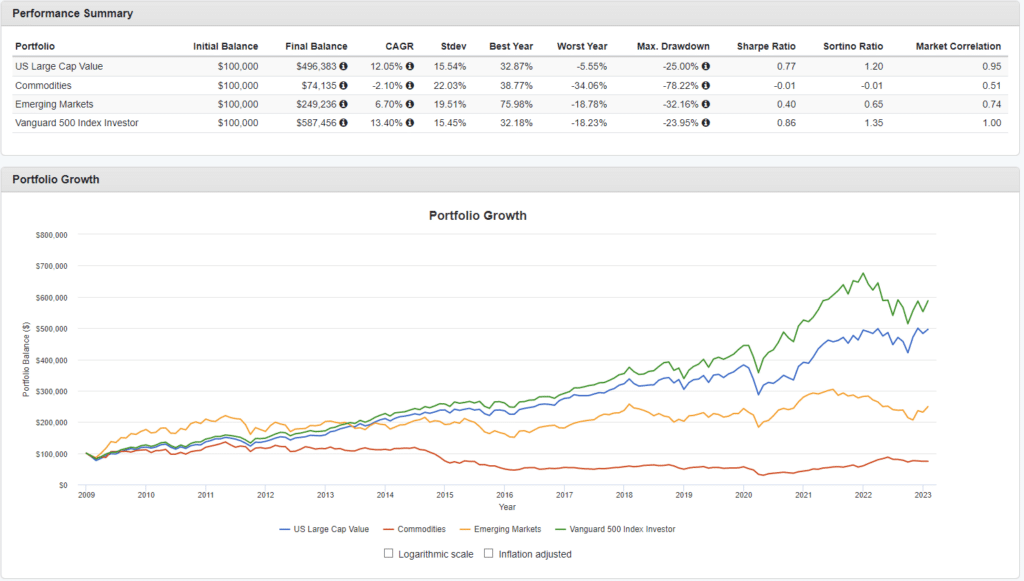

Conviction Leads To Poor Returns

It is possible that someday, the world will end. It just isn’t today and hasn’t been over the last decade. As shown, that conviction to a thesis has cost individuals dearly over time.

Even on an inflation-adjusted basis, the performance differential is extraordinary.

While I am using gold as an example, many had convictions about numerous investment themes that failed to materialize, such as emerging markets, BRICs, fundamentals (value over growth), and commodities.

Importantly, even the conviction of a diversified portfolio of stocks and bonds left investors hunting for returns to meet their financial goals.

One final example is a recent post by Michael Maharrey via SchiffGold.com, suggesting gold was a great way to hedge the inflation of buying a suit.

“As an example, let’s consider a high-end men’s suit. In 1900, the average price of a high-end men’s suit was around $35. Today, the average price of a high-end suit is around $2,000.

Looking at it another way, if you had stuffed $41.34 under your mattress in 1900, today you might be able to buy a couple of Polo shirts if you find a deal. But if you had bought two 1-ounce gold coins and stuffed those under your mattress in 1900, today you’d be able to buy a fancy suit and have about $1,600 left over.“

He is correct in his math. However, the same investment in the stock (price appreciation only since gold doesn’t pay a dividend) allowed an individual to buy 15 suits with money left over.

The problem with “conviction” is that it leads to various behavioral biases that interfere with portfolio returns over longer-term time horizons. We discussed these biases in our January Resolutions, but the most important are confirmation bias, recency bias, loss aversion, and narrow framing.

The hard part of becoming a better investor is to lose your “conviction.”

4-Things & Investment Rules To Follow

The problem with having a strong “conviction” about some economic, political, or financial outcome is it builds on itself. Crucially, we only acknowledge the information that confirms our beliefs and exclude all opposing facts. This is “confirmation bias” and has been enhanced by the “information silos” of social media.

There are four things that we can do to become better long-term investors:

- Turn off the mainstream media

- Do your homework

- Understand that what you believe and reality can be two very different things.

- Diversification is lazy portfolio management.

But most importantly, we must remember as investors that we only have a finite period to invest and save for retirement. Such is why the “duration” of our conviction, such as the “death of the dollar,” can not be longer than our investment time horizon. If it does, we may die broke waiting for the “end of the world” to arrive.

Such is why we agree with Roy Neuberger:

“My advice is to learn from the great investors-not follow them. You can benefit from their mistakes and successes, and you can adapt what fits your temperament and circumstances.“

Here are the investment rules you will find in common with many of the greatest investors in history.

- Cut Losers Short And Let Winners Run.

- Investing Without Specific End Goals Is A Big Mistake.

- Emotional And Cognitive Biases Are Not Part Of The Process.

- Follow The Trend.

- Don’t Turn A Profit Into A Loss.

- Odds Of Success Improve Greatly When Technical Analysis Supports Fundamental Analysis.

- Try To Avoid Adding To Losing Positions.

- In Bull Markets, You Should Be “Long.” In Bear Markets – “Neutral” Or “Short.”

- Invest First with Risk in Mind, Not Returns.

- The Goal Of Portfolio Management Is A 70% Success Rate.

Is the world going to end eventually? Maybe.

But it probably isn’t today or in the next 10 years.

So, what will you do with your money between today and retirement?

Remember, it isn’t “being wrong” that is the biggest risk to your money. It’s “staying wrong,” that is.