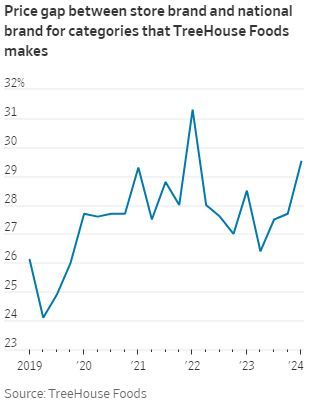

Consumers are turning away from name-brand foods in an attempt to cut back on spending. Consumer Packaged Goods (CPG) companies such as Proctor & Gamble, General Mills, and Kellogg benefited from supply chain disruptions during the pandemic as private label products saw restricted supply. Thus, the CPG brands with more resilient supply chains used the combination of shortages and heightened demand for food at home to exercise pricing power. As shown below, the price premium between national and store brands for TreeHouse Foods, a private-label manufacturer, remains substantially higher than pre-pandemic levels.

However, this advantage also meant that CPG brands relaxed their efforts to innovate their product lines. Private-label brands are also honing in on quality, meaning CPG brands must compete through innovation or lowering prices to maintain market share. The latter seems more likely, given the recent retail sales data. Now that supply chain pressures have alleviated and inflation is straining household budgets, consumers are turning to private-label brands to control costs. Per the Wall Street Journal:

Amid elevated demand for food at home and consumer wallets flush with stimulus cash, CPG companies were able to raise prices without much resistance. But that is now quickly changing as retailers deal with price-sensitive consumers increasingly exhausted with the cumulative impact of inflation: Grocery prices are about 26% higher than they were in 2019. In a recent survey of U.S. consumers by Jefferies, some 51% of respondents said they are buying more private-label products to save money on grocery bills.

What To Watch Today

Earnings

- No notable earnings releases.

Economy

Market Trading Update

Last week, we discussed the issue of the negative divergences and bad breadth of the market. To wit:

“While the bullish trend remains intact, along with a MACD ‘buy signal,’ which suggests an increased allocation to equity exposure, we have some concerns.

While the market is making all-time highs as momentum continues, its breadth is narrowing. The number of stocks trading above their respective 50-DMA continues to decline as the market advances, along with the MACD signal. Furthermore, the NYSE Advance-Decline line and the Relative Strength Index (RSI) have reversed, adding to the negative divergences from a rising market. While this does not mean the market is about to crash, it does suggest that the current rally is weaker than the index suggests.

As we discussed, these negative divergences have often preceded short- and intermediate-term corrective market actions. Such is the point where Investors tend to make two mistakes. The first is overreacting to these technical signals, thinking a more severe correction is coming. The second is taking action too soon.

Yes, these signals often precede corrections, but there are also periods of consolidation where the market trades sideways. Secondly, reversals of overbought conditions tend to be shallow in a momentum-driven bullish market. These corrections often find support at the 20 and 50-day moving averages (DMA), but the 100 and 200-DMAs are not outside normal corrective periods.

If you remember, in March, we discussed the potential for a 5 to 10% correction due to many of the same concerns noted above. That correction of 5.5% came in April. We are again at a juncture where a 5-10% is likely. The only issue is it could come anytime between now and October.

As is always the case, timing is always the biggest risk. Therefore, be careful not to overreact or act too soon. The market will let us know when to become more aggressive in reducing risk.

The Week Ahead

The second quarter comes to an end this week. The primary focus will be PCE prices plus personal income and outlays on Friday. The all-important core PCE price index is the Fed’s preferred measure of inflation; thus, it carries extra weight. The consensus expects personal income to rise 0.4% MoM in May versus the 0.3% increase in April. Meanwhile, the consensus expects personal expenditures to rise by 0.3% MoM in May after increasing by 0.2% in April.

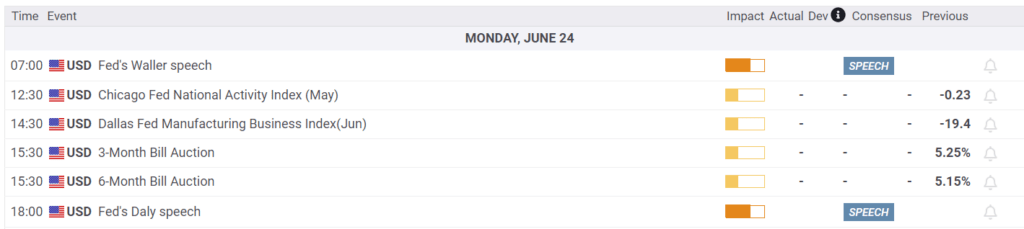

This week starts slowly with speeches by the Fed’s Waller and Daly today. Tomorrow, we will hear from Bowman and Cook and get data on April home prices via the Case-Shiller Home Price Index. We’ll also get updated consumer confidence data, where the consensus forecasts a decrease to 100 in June from 102 in May. Wednesday will bring New Home Sales data for May. We don’t expect any positive surprises, given that consumers are turning down purchases due to high mortgage rates. Durable Goods Orders for May are released on Thursday. The consensus expects a slowdown in growth to 0.3% in May from 0.7% in April. As mentioned above, we cap off the quarter with PCE prices and personal income & outlays on Friday.

Boston Fed Economist: Shelter Inflation May Be Stubborn Through Year-End

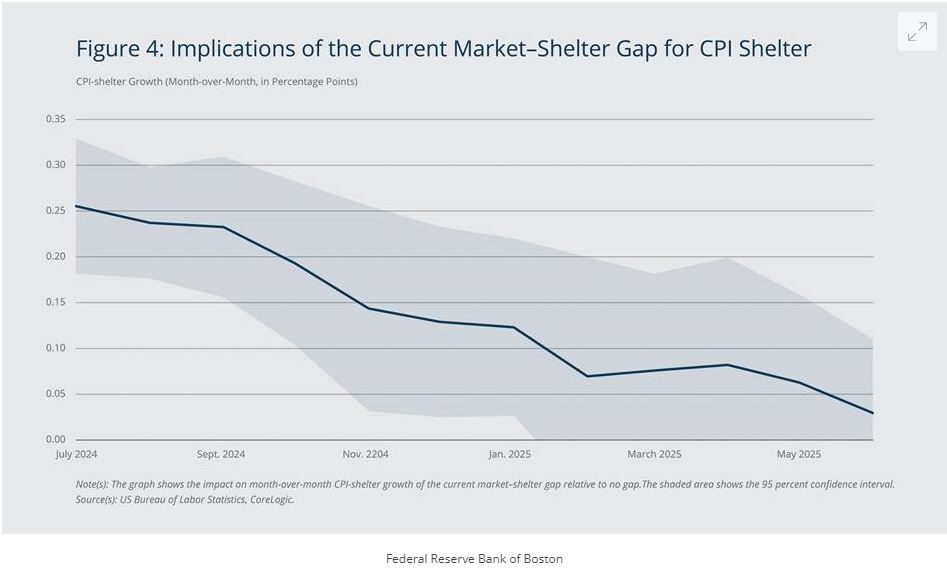

A recently published paper by a Boston Fed Economist suggests that rent increases will keep inflation above the Fed’s target for longer than most expect. The Author proposes that the effect will be most notable through the end of 2024 and diminish significantly in 2025. In addition, the Author expects CPI shelter inflation to slow considerably in periods beyond the next twelve months. His research focuses on the gap between market rent and the shelter component of CPI and how those dynamics pass through to CPI and PCE. Below, we provide excerpts and a chart from the paper that sums it up nicely.

The overall trend is clear: CPI shelter is expected to grow quickly in the summer and fall of 2024 but then slow down markedly when we move into 2025. Therefore, according to the estimates, the market–shelter gap is likely to pose a significant, but diminishing, challenge to the Fed’s ability to achieve its 2 percent inflation target over the next year.

Back-of-the-envelope calculations show how high CPI shelter could raise overall inflation this year. Given that shelter comprises 36.1 percent of the CPI and 15.5 percent of the PCE, the post-pandemic pass-through estimates imply that the current market–shelter gap will lead to an additional 0.59 and 0.25 percentage point growth in headline (including food and energy) CPI and headline PCE, respectively, from June 2024 to June 2025 relative to there being no market–shelter gap. The estimates also show that the deviation will lead to an additional growth in core (excluding food and energy) CPI and core PCE of 0.74 percentage point and 0.29 percentage point, respectively, from June 2024 to June 2025.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.