Turn on financial television or pick up a financially related magazine or newspaper and you will hear, or read, about what an analyst from some major Wall Street brokerage has to say about the markets or a particular company. For the average person, and for most financial advisors, this information as taken as “fact” and is used as a basis for portfolio investment decisions.

But why wouldn’t you?

After all, Carl Gugasian of Dewey, Cheatham & Howe just rated Bianchi Corp. a “Strong Buy.” That rating is surely something that you can “take to the bank”, right?

Maybe not.

For many years, I have been counseling individuals to disregard mainstream analysts, Wall Street recommendations, and even MorningStar ratings, due to the inherent conflict of interest between the firms and their particular clientèle. Here is the point:

- YOU, are NOT Wall Street’s client.

- YOU are the CONSUMER of the products sold FOR Wall Street’s clients.

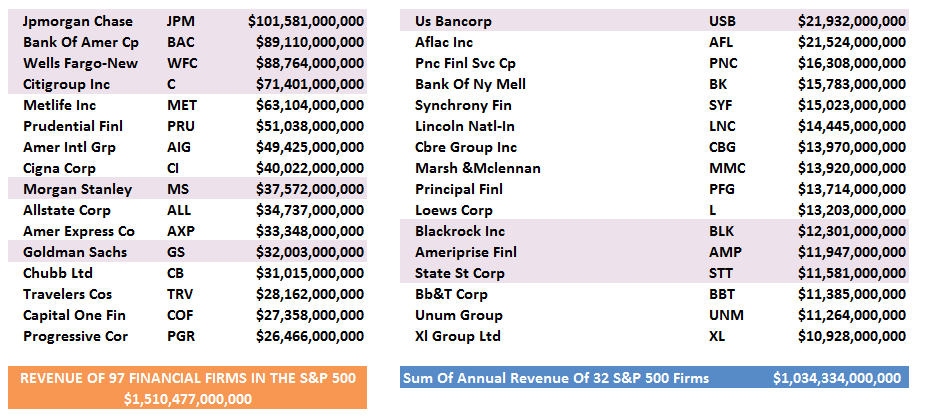

Major brokerage firms are big business. I mean REALLY big business. As in $1.5 Trillion a year in revenue big. The table below shows the annual revenue of 32 of the largest financial firms in the S&P 500.

(The combined revenue of the 32 largest firms last year was in excess of $1 Trillion with the revenue of the 97 financial firms in the S&P 500 bringing in $1.5 Trillion.)

As such, like all businesses, these companies are driven by the needs of increasing corporate profitability on an annual basis regardless of market conditions.

This is where the conflict of interest arises.

When it comes to Wall Street profitability the most lucrative transactions are not coming from servicing “Mom and Pop” retail clients trying to work their way towards retirement. Wall Street is not “invested” along with you, but rather “use you” to make income.

This is why “buy and hold” investment strategies are so widely promoted. As long as your dollars are invested the mutual funds, stocks, ETF’s, etc, brokerage firms collect fees regardless of what happens in the market. These strategies are certainly in their best interest – they are not necessarily in yours.

But those retail management fees are simply a sideline to the really big money.

Wall Street’s real clients are multi-million, and billion, dollar investment banking transactions, such as public offerings, mergers, acquisitions and bond offerings which generate hundreds of millions to billions of dollars in fees for Wall Street each year.

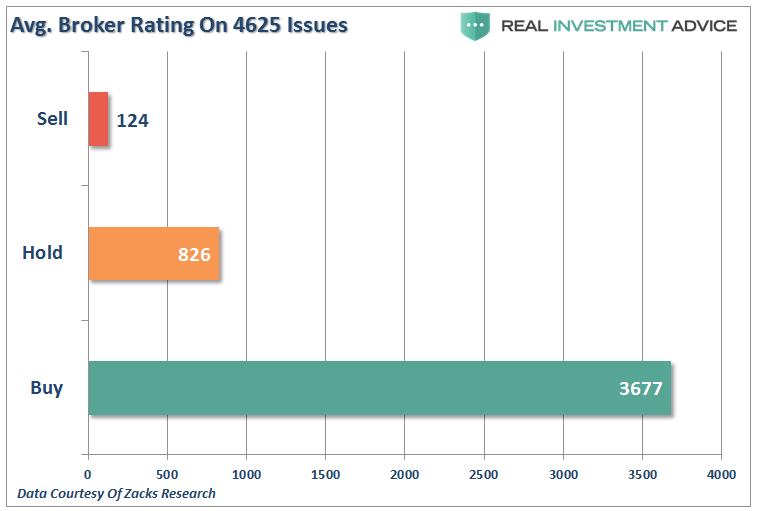

In order for a firm to “win” that business, Wall Street firms must cater to those prospective clients. In this respect, it is extremely difficult for the firm to gain investment banking business from a company they have a “sell” rating on. This is why “hold” is so widely used rather than “sell” as it does not disparage the end client. To see how prevalent the use of the “hold” rating is I have compiled a chart of 4625 stocks ranked by the number of “Buy”, “Hold” or “Sell.”

See the problem here. There are just 2.8% of all stocks with a “sell” rating.

Do you actually believe that out of 4625 stocks only 124 should be “sold?”

You shouldn’t. But for Wall Street, a “sell” rating is simply not good for business.

The conflict doesn’t end just at Wall Street’s pocketbook. Companies depend on their stock prices rising as it is a huge part of executive compensation packages.

Corporations apply pressure on Wall Street firms, and their analysts, to ensure positive research reports on their companies with the threat that they will take their business to another “friendlier” firm. This is also why up to 40% of corporate earnings reports are “fudged” to produce better outcomes.

Earnings Magic Exposed, an article written by Michael Lebowitz last year, provides details on the games played on Wall Street when it comes to forecasting corporate earnings. He summarized the article as follows:

Consider the ploy that companies and Wall Street are using to fool the investing public.

- First, they grossly overestimate earnings for the upcoming year. By overestimating earnings, they tout financial ratios based upon inaccurate expected earnings and sell investors on a bright future. How many times have analysts claimed that forward looking price to earnings ratios are constructive for price gains? How “constructive” would they be if the expectations were reconciled to reality and lowered by 75%?

- Second, they progressively lower expectations prior to the earnings release so that financial results are effectively underestimated. The same analysts that peddled double digit earnings growth a year earlier somehow can now claim that earnings are better than they expected.

If actual earnings varied somewhat randomly from above expectations to below expectations, we would likely fault the analysts and corporations with being poor forecasters. But when such one-directional forecasting errors routinely and consistently occur, it is more than bad forecasting. At best one can accuse Wall Street analysts and the companies that feed them information of incompetence. At worst this is another pure and simple case of institutions gaming the system through a fraud designed to prop up stock prices. Take your pick, but in either case it is advisable to ignore the spin that accompanies earnings releases and apply the rigor of doing your own analysis to get at the veracity of corporate earnings.

Wall Street Needs You To Sell Product To

When Wall Street wants to do a stock offering for a new company they have to sell that stock to someone in order to provide their client, a company, with the funds they need. The Wall Street firm also makes a very nice commission from the transaction.

Generally, these publicly offered shares are sold to the firm’s biggest clients such as hedge funds, mutual funds, and other institutional clients. But where do those firms get their money? From you.

Whether it is the money you invested in your mutual funds, 401k plan, pension fund or insurance annuity – at the bottom of the money grabbing frenzy is you. Much like a pyramid scheme – all the players above you are making their money…from you.

In a study by Lawrence Brown, Andrew Call, Michael Clement and Nathan Sharp it is clear that Wall Street analysts are clearly not that interested in you. The study surveyed analysts from the major Wall Street firms to try and understand what went on behind closed doors when research reports were being put together. In an interview with the researchers John Reeves and Llan Moscovitz wrote:

“Countless studies have shown that the forecasts and stock recommendations of sell-side analysts are of questionable value to investors. As it turns out, Wall Street sell-side analysts aren’t primarily interested in making accurate stock picks and earnings forecasts. Despite the attention lavished on their forecasts and recommendations, predictive accuracy just isn’t their main job.”

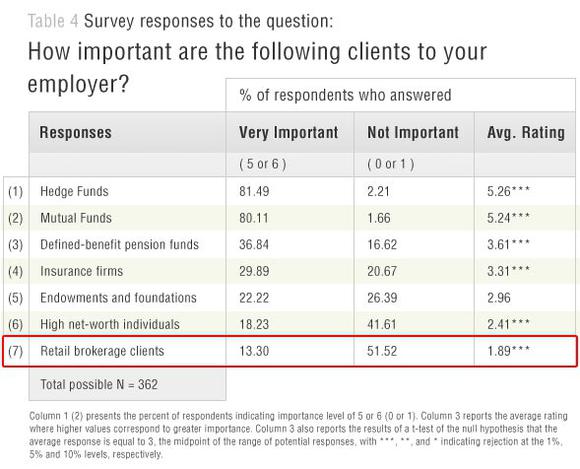

The chart below is from the survey conducted by the researchers which shows the main factors that play into analysts compensation. It is quite clear that what analysts are “paid” to do is quite different than what retail investors “think” they do.

“Sharp and Call told us that ordinary investors, who may be relying on analysts’ stock recommendations to make decisions, need to know that accuracy in these areas is ‘not a priority.’ One analyst told the researchers:

‘The part to me that’s shocking about the industry is that I came into the industry thinking [success] would be based on how well my stock picks do. But a lot of it ends up being “What are your broker votes?”‘

A ‘broker vote’ is an internal process whereby clients of the sell-side analysts’ firms assess the value of their research and decide which firms’ services they wish to buy. This process is crucial to analysts because good broker votes result in revenue for their firm. One analyst noted that broker votes ‘directly impact my compensation and directly impact the compensation of my firm.'”

The question really becomes then “If the retail client is not the focus of the firm then who is?” The survey table below clearly answers that question.

Not surprisingly you are at the bottom of the list. The incestuous relationship between companies, institutional clients, and Wall Street is the root cause of the ongoing problems within the financial system. It is a closed loop that is portrayed to be a fair and functional system; however, in reality, it has become a “money grab” that has corrupted not only the system but the regulatory agencies that are supposed to oversee it.

Why You Need Independence

So, where can you go to get “real investment advice” and a true consideration of the value of YOUR money?

Thankfully, starting at the turn of the century, the rise of independent, fee-only, financial advisors, private investment analysts, research and rating firms began to infiltrate the system.

Here is an example of the difference.

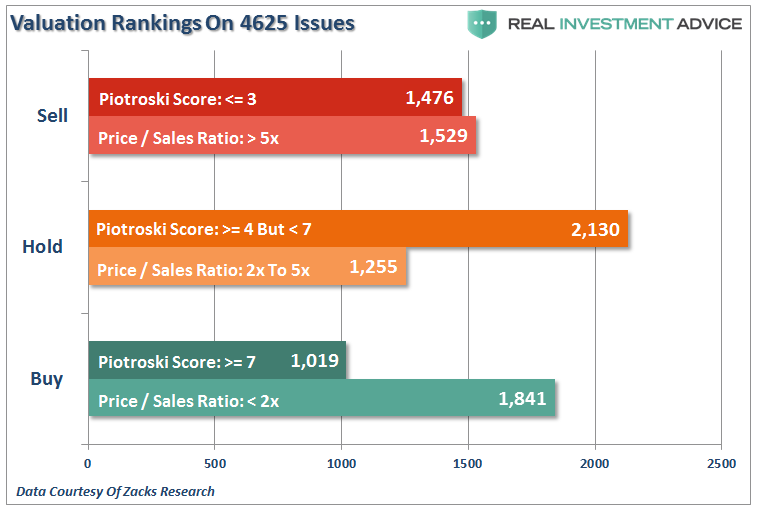

As an independent money manager, I use valuation analysis to determine what equities should be bought, sold or held in client’s portfolios. While there are many measures of valuation, two of my favorites are Price to Sales and the Piotroski f-score among others. I took the same 4625 stocks as above and ranked them by these two measures.

See the difference. Not surprisingly, there are far fewer “buy” rated, and far more “sell” rated, companies than what is suggested by Wall Street analysts.

Here is something even more alarming.

Just after the “dot.com” bust, I wrote a valuation article quoting Scott McNeely, who was the CEO of Sun Microsystems at the time. At its peak the stock was trading at 10x its sales. (Price-to-Sales ratio) In a Bloomberg interview Scott made the following point.

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees.That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

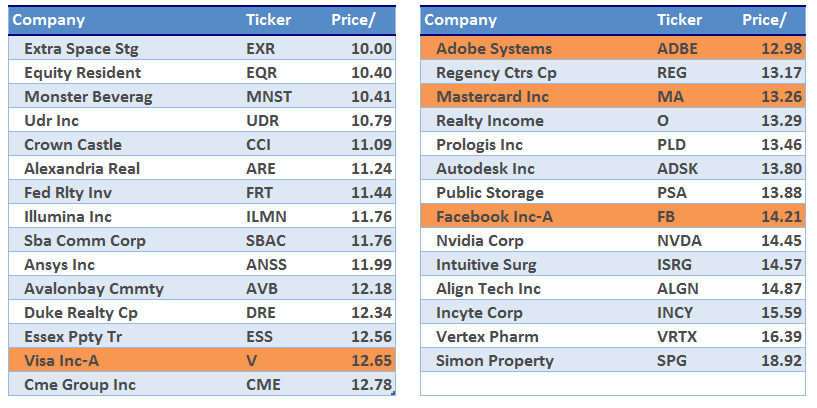

How many of the following “Buy” rated companies do you currently own that are currently carrying price-to-sales valuations in excess of 10x?

So, what are you thinking?

As more and more “baby boomers” head into retirement the need for firms that can do organic research, analysis and make investment decisions free from “conflict,” and in the client’s best interest, will continue to be in high demand in the years to come.

This is particularly the case when the next downturn occurs and the dangers of passive ETF indexing and robo-advisors are readily exposed.

Independent advice can help remove those emotional biases from the investing process that lead to poor investment outcomes over time. There are a raft of advisors with the the right team, tools and data, who can spend the time necessary to manage portfolios, monitor trends, adjust allocations and protect capital through risk management.

The next time someone tells you that you can’t “risk manage” your portfolio and just have to “ride things out,” just remember, you don’t.

You, and your money, deserve better.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read