Several years ago, I began writing an annual update discussing Dalbar’s Quantitative Analysis Of Investor Behavior study. The study showed just how poorly investors perform relative to market benchmarks over time and the reasons for that underperformance.

With the release of Dalbar’s 2017 study, I can update, and remind you, of the problems investors continue to face despite the ongoing media and mainstream rhetoric about “investing for the long-term” and other such nonsense like “dollar cost averaging” and “buy and hold” investing.

Let’s jump right in.

You Can’t Beat An Index…Period

First of all, let’s dismiss the notion that it is possible for an investor to consistently “beat” an index over long periods of time.

You can’t.

Indexes do not account for the impact of taxes, trading costs, and fees, over time. There are also internal dynamics of an index that affect long-term performance which does not apply to an actual portfolio such as share buybacks, substitution, and market-cap valuation.

(For more on the reasons why benchmarking is a bad strategy click here.)

However, even the issues shown above do not fully account for the underperformance of investors over time. The key findings of the study show that:

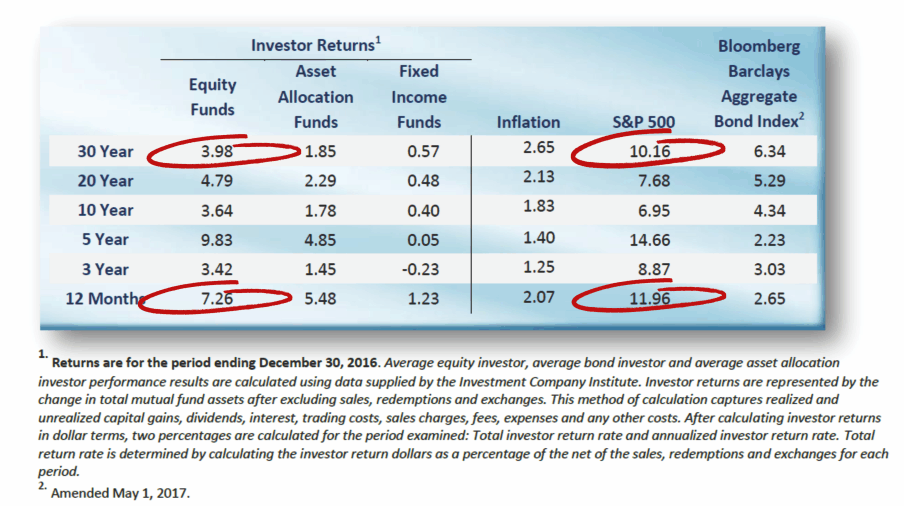

- In 2016, the average equity mutual fund investor underperformed the S&P 500 by a margin of -4.70%. While the broader market made gains of 11.96%, the average equity investor earned only 7.26%.

- In 2016, the average fixed income mutual fund investor underperformed the Bloomberg Barclays Aggregate Bond Index by a margin of -1.42%. The broader bond market realized a return of 2.65% while the average fixed income fund investor earned 1.23%.

- Equity fund retention rates decreased materially in 2016 from 4.10 years to 3.80 years. (This is directly related to psychology and behavior.)

- In 2016, the 20-year annualized S&P return was 7.68% while the 20-year annualized return for the Average Equity Fund Investor was only 4.79%, a gap of -2.89% annualized.

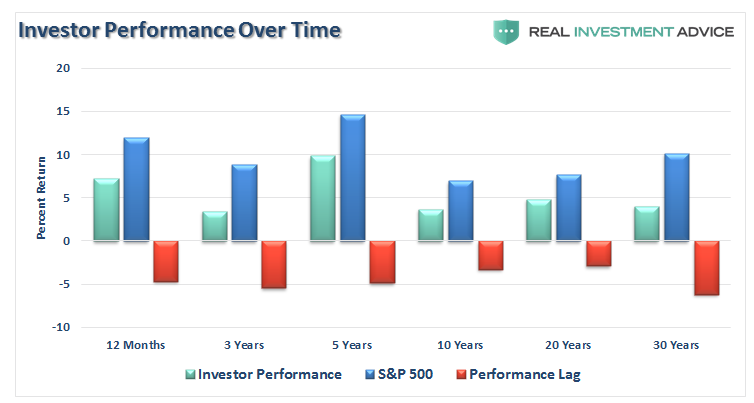

Here is a visual of the lag between expectations and reality.

The underperformance in 2017 directly relates to the psychological behaviors of individual investors. Despite ongoing rhetoric about “buy and hold” and “dollar cost averaging”, both of which are failed strategies as discussed at length here, the reality is that investor psychology is the biggest impediment to long-term success.

As noted by Dalbar:

“The retention rate data for equity, fixed income and asset allocation mutual funds strongly suggests that investors lack the patience and long-term vision to stay invested in any one fund for much more than four years. Jumping into and out of investments every few years is not a prudent strategy because investors are simply unable to correctly time when to make such moves.”

Of course, there are two main drivers behind both the long-term underperformance of investors and their movements in and out of investments.

Yes, You (Still) Suck At Investing

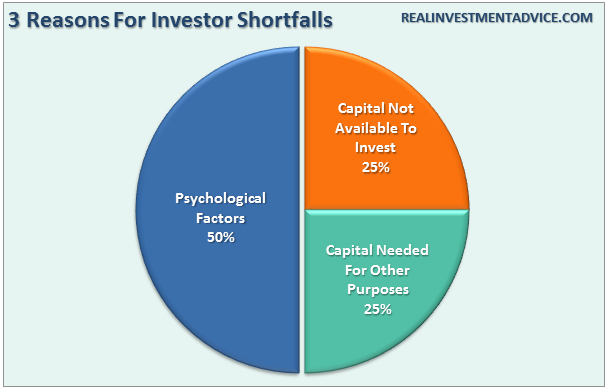

Accordingly to the Dalbar study, there are three primary causes for the chronic shortfall for both equity and fixed income investors is shown in the chart below.

Notice that while “fees” are important to overall returns, they are not a key issue to the majority of underperformance by individual investors. As shown above, the key issues come down to primarily a lack of capital to invest and psychology.

As stated, the issue of “costs” are an important consideration when choosing between two specific investment options; however, the emotional mistakes made by investors over time are much more important.

While the inability to participate in the financial markets is certainly a major issue, the biggest reason for underperformance by investors who do participate in the financial markets over time is psychology. Behavioral biases that lead to poor investment decision-making is the single largest contributor to underperformance over time. Dalbar defined nine of the irrational investment behavior biases specifically:

- Loss Aversion – The fear of loss leads to a withdrawal of capital at the worst possible time. Also known as “panic selling.”

- Narrow Framing – Making decisions about on part of the portfolio without considering the effects on the total.

- Anchoring – The process of remaining focused on what happened previously and not adapting to a changing market.

- Mental Accounting – Separating performance of investments mentally to justify success and failure.

- Lack of Diversification – Believing a portfolio is diversified when in fact it is a highly correlated pool of assets.

- Herding– Following what everyone else is doing. Leads to “buy high/sell low.”

- Regret – Not performing a necessary action due to the regret of a previous failure.

- Media Response – The media has a bias to optimism to sell products from advertisers and attract view/readership.

- Optimism – Overly optimistic assumptions tend to lead to rather dramatic reversions when met with reality.

The biggest of these problems for individuals is the “herding effect” and “loss aversion.”

These two behaviors tend to function together compounding the issues of investor mistakes over time. As markets are rising, individuals are lead to believe that the current price trend will continue to last for an indefinite period. The longer the rising trend last, the more ingrained the belief becomes until the last of “holdouts” finally “buys in” as the financial markets evolve into a “euphoric state.”

As the markets decline, there is a slow realization that “this decline” is something more than a “buy the dip” opportunity. As losses mount, the anxiety of loss begins to mount until individuals seek to “avert further loss” by selling.

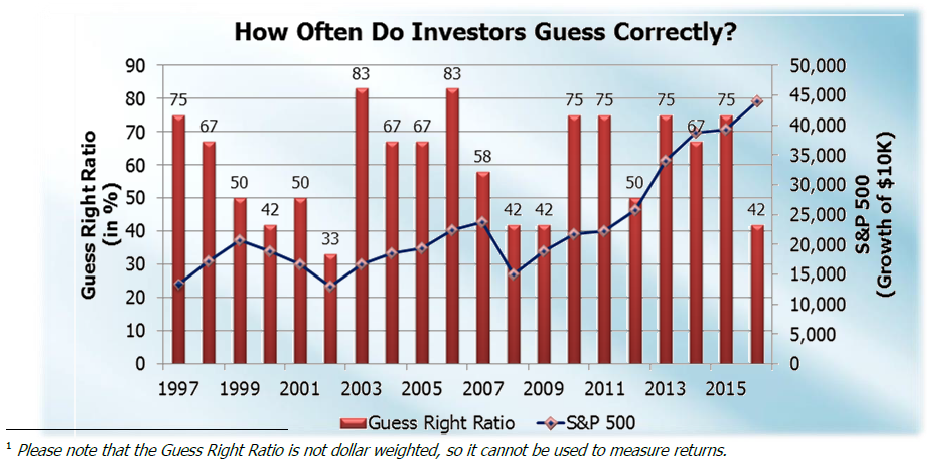

As shown in the chart below, this behavioral trend runs counter-intuitive to the “buy low/sell high” investment rule.

In the end, we are just human. Despite the best of our intentions, it is nearly impossible for an individual to be devoid of the emotional biases that inevitably lead to poor investment decision-making over time. This is why all great investors have strict investment disciplines that they follow to reduce the impact of human emotions.

More importantly, while there are many articles chiding investors into “buy and hold,” and “passive indexing” strategies, the reality is that few will ever survive the downturns in order to see the benefits.

Tips For Advisors

Dalbar reveals the importance of event recognition and risk management. Knowing that advisory clients are emotional, and subject to emotional swings caused by market volatility, advisors must take on a role of both psychological counselor and portfolio manager. Here are some guidelines:

- Expectations for future returns and withdrawal rates should be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerate the principal bleed. Plans should be made during rising market years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last 8-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Chasing an arbitrary index that is 100% invested in the equity market requires your clients to take on far more risk than they likely want or can endure. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME that was needed to reach their retirement goals.

As an advisor, your job is not to beat some random arbitrary index. Your goal is to help your client focus on these important areas:

– Capital preservation

– A rate of return sufficient to keep pace with the rate of inflation.

– Expectations based on realistic objectives. (The market does not compound at 8%)

– Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

– You can regain lost capital – but you can’t replace their lost time. Time is a precious commodity they cannot afford to lose.

– Portfolios are time-frame specific. If the client has 5-years to retirement but a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

The challenge, of course, is understanding the next major impact event, and market reversion, will NOT HAVE the identical characteristics of the previous events. This is why comparing today’s market to that of 1994 or 2000 is pointless. As I have stated many times previously:

“When the crash ultimately comes the reasons will be different than they were in the past – only the outcome will remain same.”

However, it is extremely critical that careful judgment is used when identifying a potential impact event which was best summed up by Howard Marks:

“Being early is the same as being wrong.”

Advisors Must Take Action Before The Event

Dalbar’s data shows that the “cycle of loss” starts when the investor abandons their investments which is followed by a period of remorse as the markets recover (sells low). Of course, the investor eventually re-enters the market when their confidence is restored (buys high). Preventing this cycle requires having a plan in place beforehand.

When markets decline, investors become fearful of total loss. Those fears are compounded by the barrage of media outlets that “fan the flames” of those fears. Advisors, need to remain cognizant of client’s emotional behaviors and substantially reduce portfolio risk during major impact events while repeatedly delivering counter-messaging to keep clients focused on long-term strategies.

Dalbar previously noted that during impact events messages delivered to clients should have three characteristics to be effective at calming emotional panic:

- Messages must be delivered at the time the fear is present. As mentioned earlier, messages delivered before the investor actually experiences the event will not be effective. If the messages are too long after the fact, decisions will have been made, and actions taken that are very difficult to reverse.

- Messages must relate directly to the event causing the fear. Providing generic messages such as the market has its ups and downs are of little use during a time of anxiety.

- Messages must assure recovery. Qualified statements regarding recovery tend to fuel fear instead of calming it.

Messages must ALSO present evidence that forms the basis for forecasting recovery. Credible and quotable data, analysis and historical evidence can provide an answer to the investor when the pressure mounts to “just do something”. Providing “generic media commentary” with a litany of qualifiers to specific questions will most likely fail to calm their fears.

Understanding how individuals respond to impact events will allow advisors to get in front of their clients to discuss the planning, preparation, and response to an impact event and recovery.

One thing that all the negative behaviors have in common is that they can lead investors to deviate from a sound investment strategy that was narrowly tailored towards their goals, risk tolerance, and time horizon. The best way to ward off the aforementioned negative behaviors is to employ a strategy that focuses on one’s goals and is not reactive to short-term market conditions. The data shows that the average mutual fund investor has not stayed invested for a long enough period of time to reap the rewards that the market can offer more disciplined investors. The data also shows that when investors react, they generally make the wrong decision.

The reality is that the majority of advisors are ill-prepared for an impact event to occur. This is particularly the case in late-stage bull market cycles where complacency runs high.

This complacency can be seen in the shift from active portfolio management strategies to passive indexing which is a hallmark sign of a late-stage bull market. When the impact event occurs, the calls to 1-800-ROBOADVISOR for calming messages and a plan to avoid major losses of capital will go unanswered. Advisors who are prepared to handle those responses, provide clear messaging and an action plan for both conserving investment capital and eventual recovery will find success in obtaining new clients.

So, do yourself, and your clients, a favor and forget about what the benchmark index does from one day to the next. Focus instead on matching their portfolio to their personal goals, objectives, and time frames. In the long run, they may not beat the index, but they aren’t going to anyway. So, help them focus instead on achieving their own personal goals.

But, isn’t that why they hired you in the first place?

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read