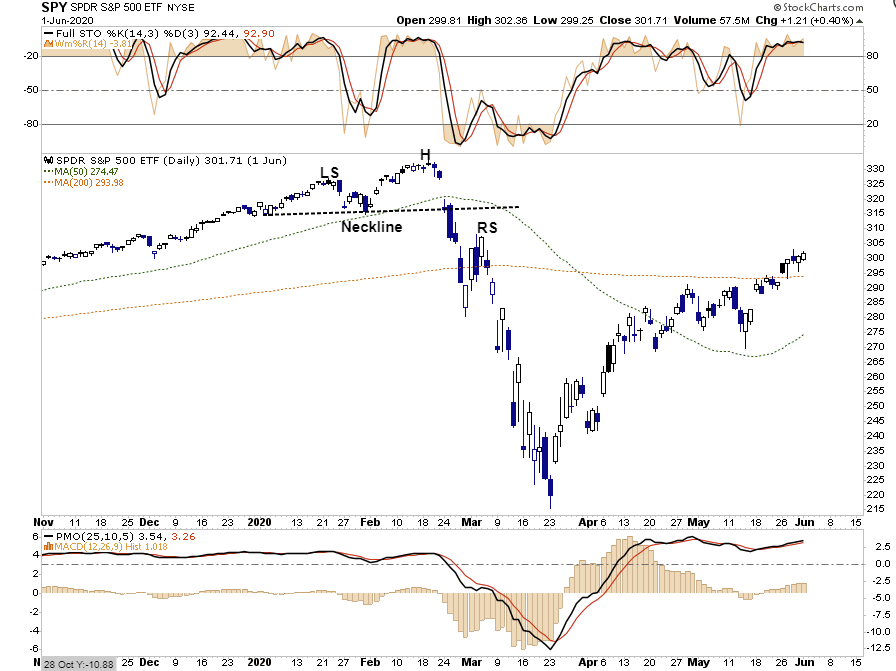

As I worked through this past weekend’s newsletter, I noticed that multiple markets are starting to exhibit topping patterns. It will be crucial for markets to reverse these patterns in the short-term if the bullish advance continues.

As we discussed with our RIAPRO.NET subscribers yesterday:

“The good news is that the S&P 500 held its 50-dma during its recent selloff. With the market getting back to more oversold levels, we are likely to see a counter-trend rally for a few days that could get us back above the 20-dma. It will be necessary for the rally to set new highs to negate the “head and shoulders” pattern. If the market rallies, fails, and breaks the neckline, we could well see a deeper correction ensue.”

There is an important caveat to this analysis.

The start of “head and shoulder” patterns occurs with quite some regularity during an advancing market. However, they are quite often not completed as the market moves to new highs negating the pattern. Therefore, while we are pointing this pattern out, we are not saying the market is about to go lower. Such will only be if the pattern completes with a break of the “neckline” support.

However, it is important not to dismiss this pattern entirely as it often preceded more substantial declines, as we saw in March of 2020.

Notably, we see this pattern elsewhere.

Same Pattern Popping up Everywhere

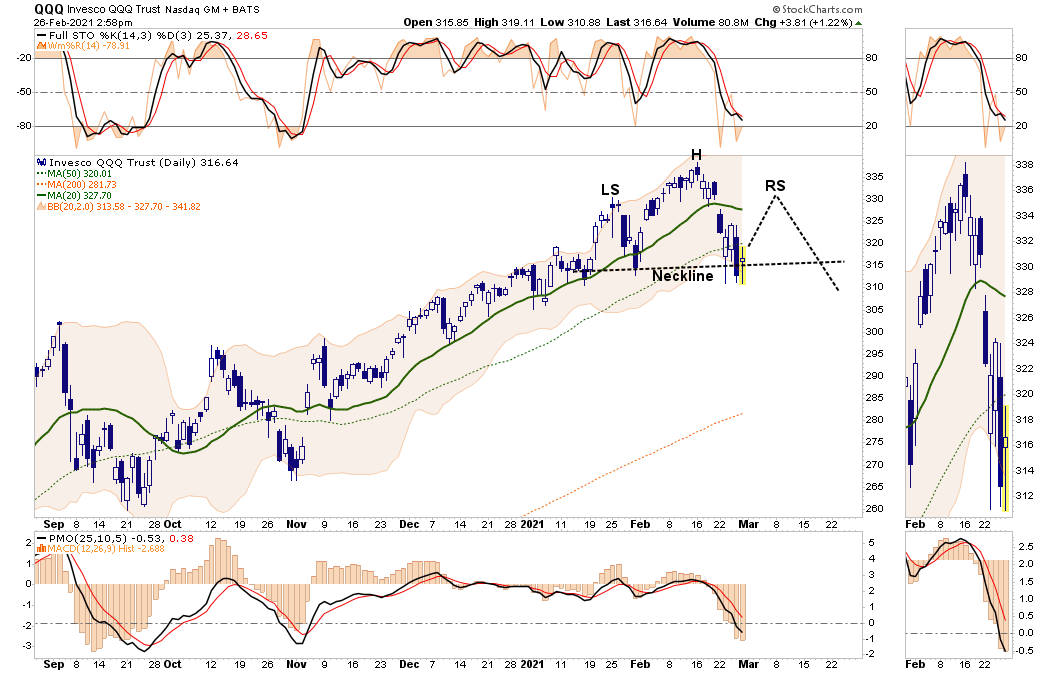

Nasdaq Index

The “head and shoulder” pattern is defined better in the Nasdaq. Currently, the neckline support needs to hold, or we will see a more significant correction in the technology sector. With the index more oversold than the S&P 500, I suspect we will see a rally shortly in these stocks, which we will use as a “selling” opportunity to reduce exposure.

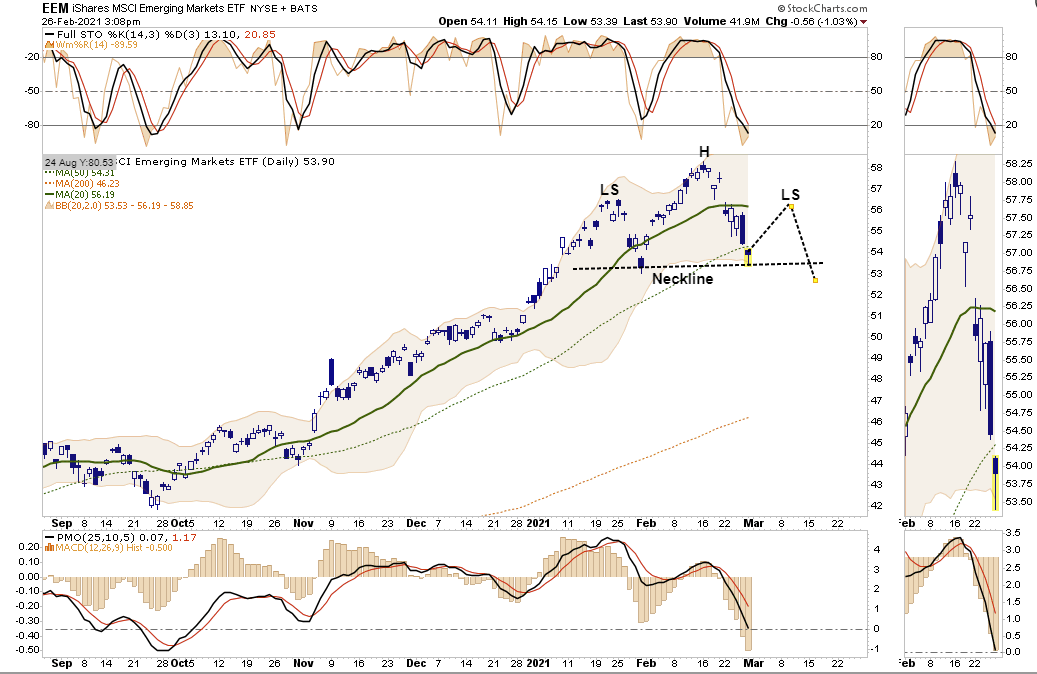

Emerging Markets

Like the Nasdaq, we see a very well-defined “head and shoulders” pattern developing here as well. Emerging Markets are very oversold at current levels, so a counter-trend bounce is likely. A failure at the 20-dma is an excellent point to reduce exposure to these cyclical sensitive areas. If economic growth weakens in the U.S., we could see a much deeper correction in Emerging Markets. Watch for a break of the neckline as a “stop-loss” for now.

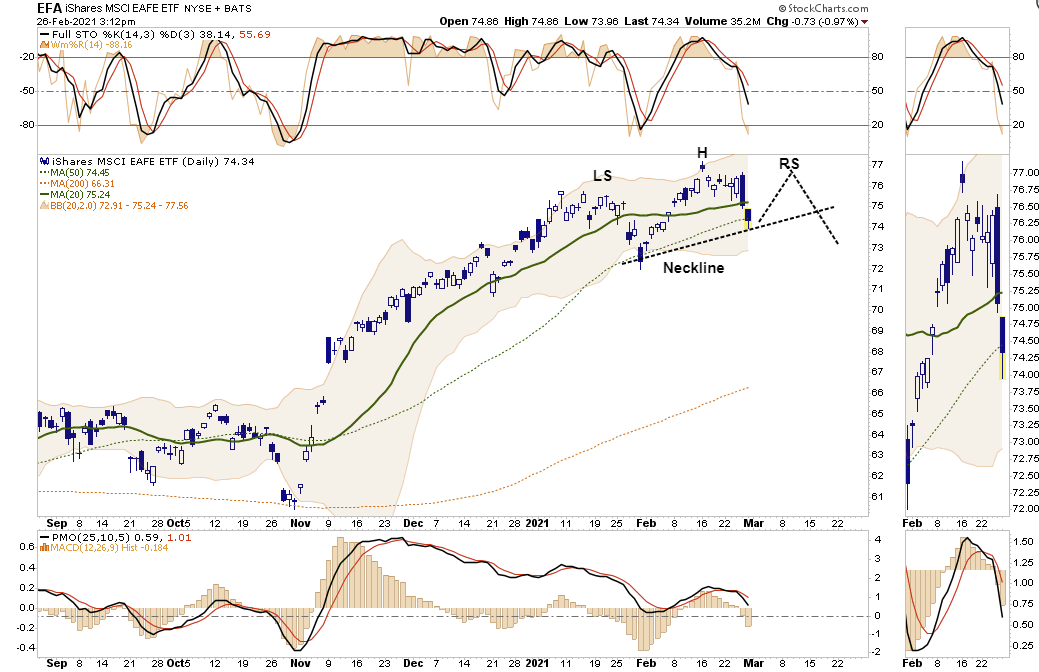

International Markets

Industrialized International Markets look much the same as the S&P 500. Watch the rising neckline as a trailing “stop-loss.” A failed rally should get used as an opportunity to reduce risk to international markets. Both international and emerging markets are well ahead of any expected growth in the U.S. economy, so the risk of disappointment is high.

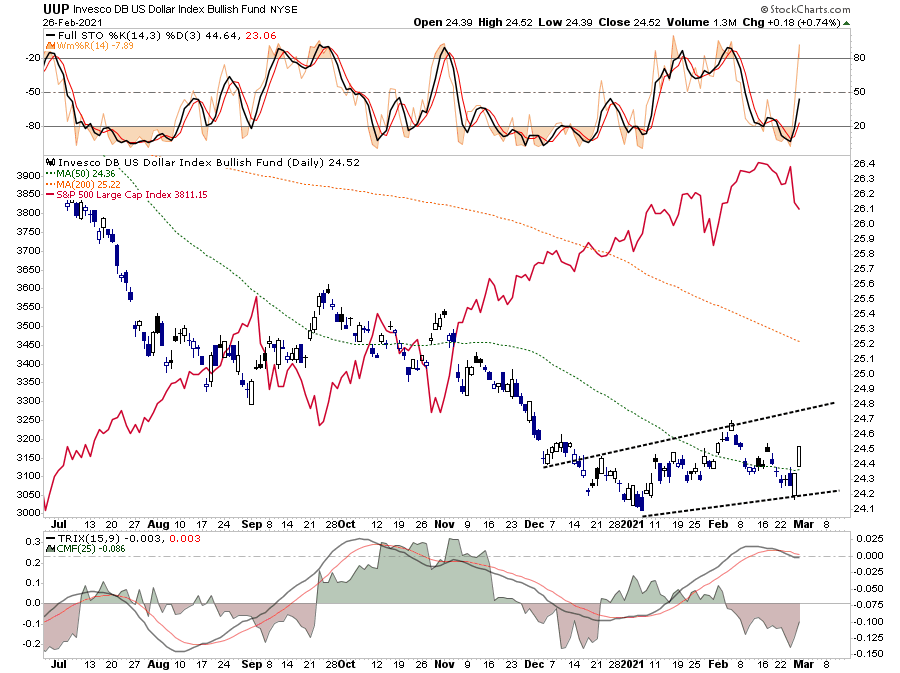

Dollars & Rates Continue To Be The Key

Currently, the market is betting on perfection. With valuations high, the bullish rationalization why prices can go higher is a bet on explosive economic growth, a falling dollar, low-interest rates, and a consumer spending surge, all while inflation remains muted.

In other words, there is a LOT of room for something to go wrong. In our view, the two key issues that have the most significant potential to undermine market confidence remain the dollar and rates.

As noted previously, everyone expects the dollar to continue to decline, and the falling dollar has been the tailwind for the emerging market, commodity, and equity-risk trade. Whatever causes the dollar to reverse will likely bring the equity market down with it.

The dollar has started building higher bottoms and is currently triggering buy signals suggesting there may be more to this rally. Given the highly negative correlation of stocks, we need to pay close attention to what happens next.

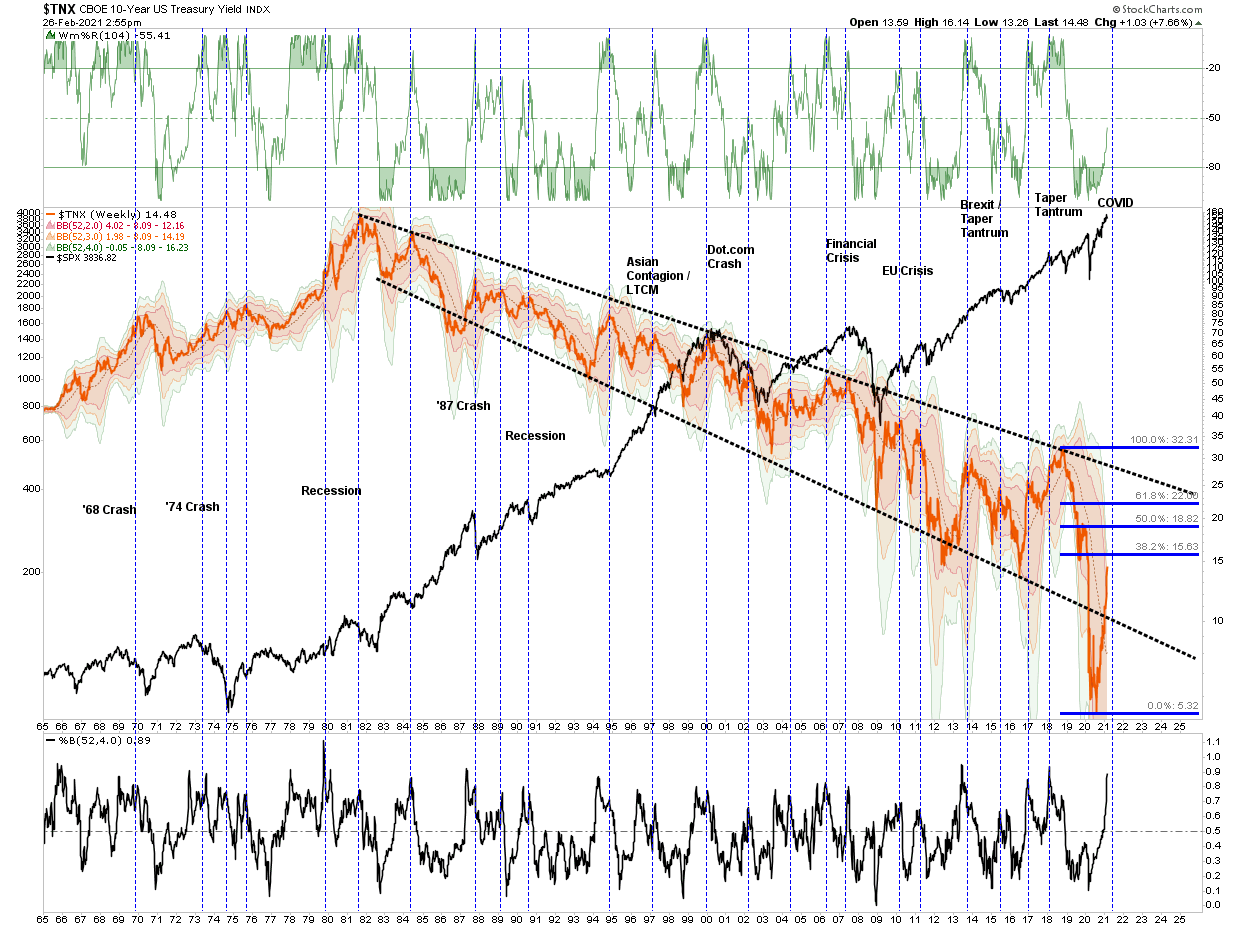

The second risk, of course, is rates. As we saw last week, the entire market complex (including small and mid-cap markets) is sensitive to sharp increases in rates. With inflationary pressures rising, input costs will have to be passed along to cash-strapped consumers or absorbed by companies with already razor-thin margins in many cases. The outcome is not acceptable in either case.

Furthermore, the spike in rates, as shown below, which corresponds with higher inflationary pressures, quickly reaches the point that something tends to break in a debt-laden economy.

With the dollar and rates both rising, it is just a function of time until something breaks. Such is why, for now, we continue to suggest using rallies to reduce exposure to equities.

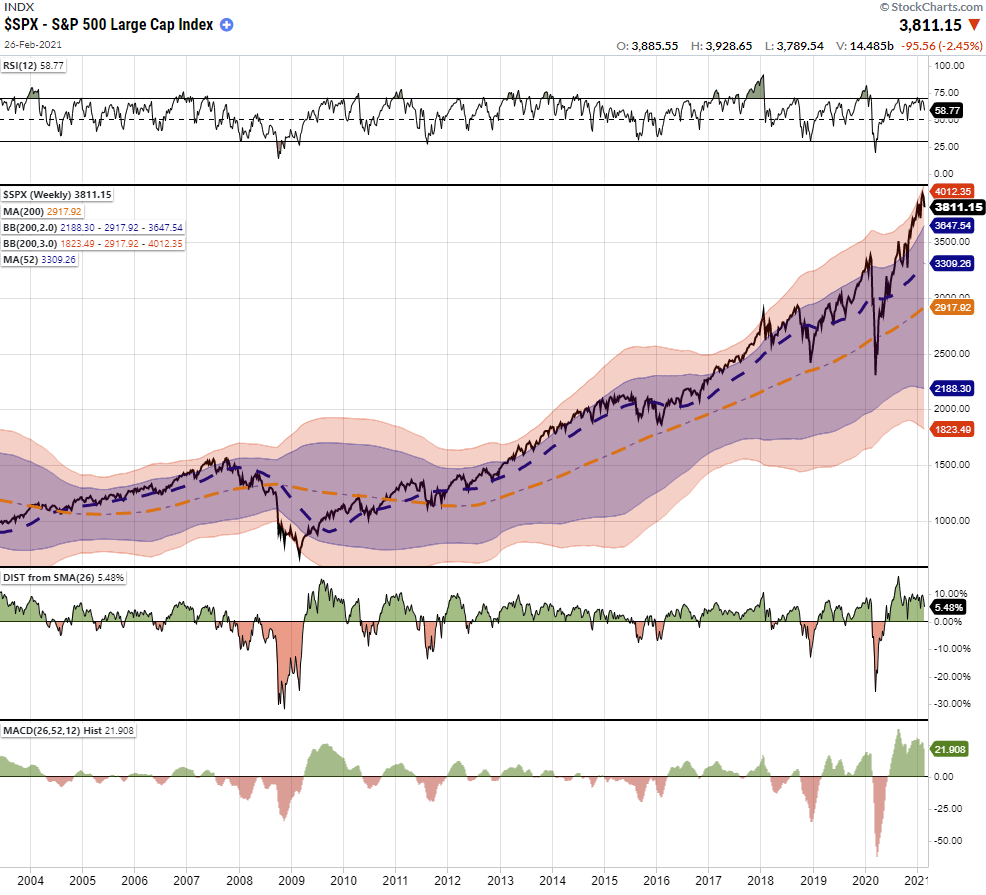

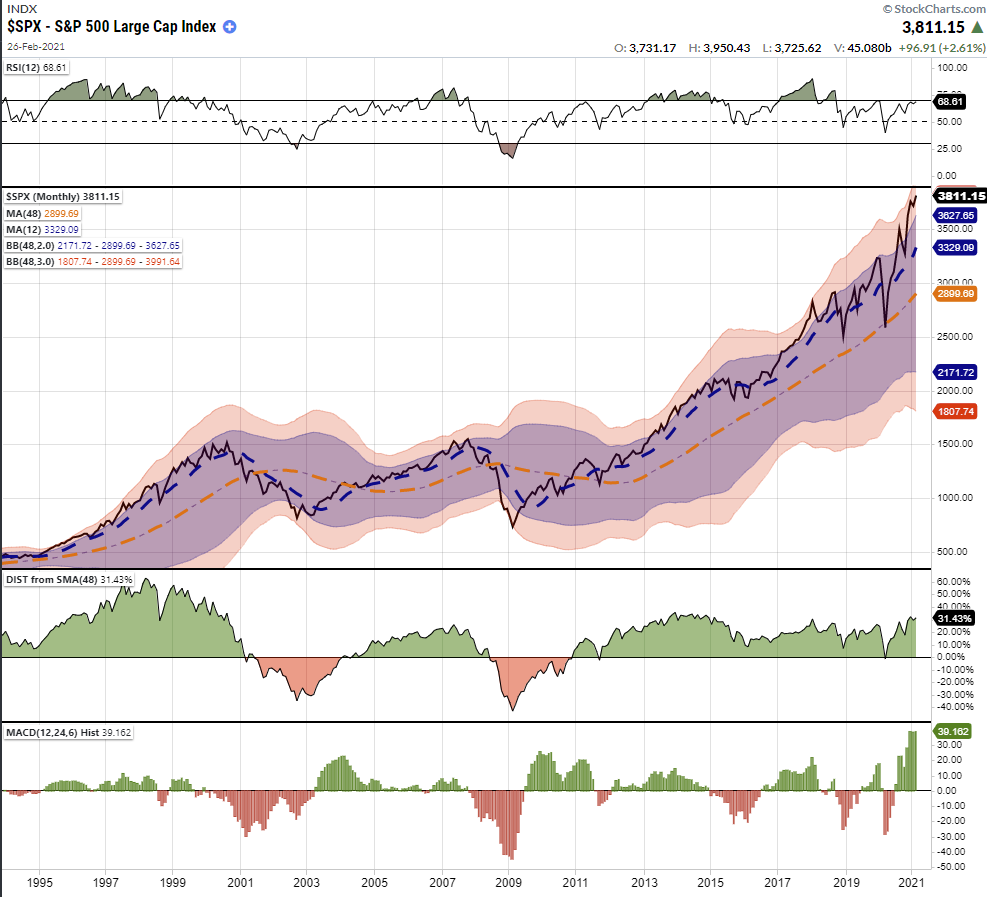

Month End S&P Technical Review

With February now closed, we can review our longer-term charts for better clarity as to overall portfolio risk and allocations.

On an intermediate-term basis, using weekly closing data as of Friday, the market is trading well into 3-standard deviations above its long-term mean. It is incredibly overbought on a weekly basis. At the same time, there is a negative divergence in relative strength (RSI), which is also a cause of concern.

Since weekly charts are slower moving, such does not mean the markets will crash immediately. Long-term charts indicate that price volatility will likely be higher in the months ahead, and investors should monitor their risk accordingly. While momentum-driven markets can remain irrational much longer than logic would predict, eventually, a reversion has always occurred.

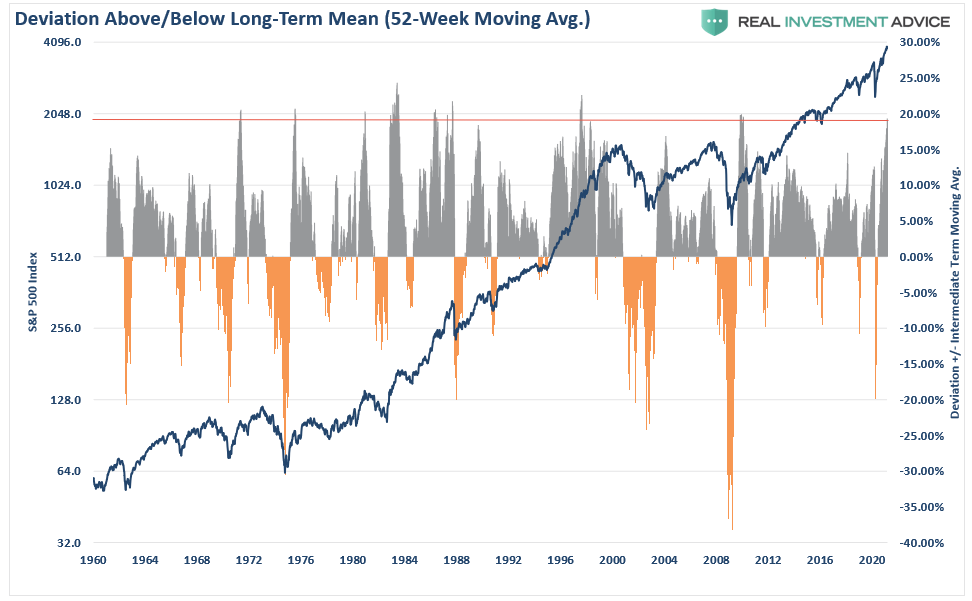

The chart below shows the price deviation from the one-year weekly moving average. Given the divergence is almost 20%, deeper price corrections have always been nearby. (Such does not mean a market crash. A correction of 10-20% is well within norms.)

Long-Term View Is Bearish

The monthly chart of the S&P 500 is likewise just as problematic. Again, long-term charts predict long-term outcomes and are NOT SUITABLE for trading portfolios short-term.

As shown, the deviation from long-term monthly means is extreme. Also, note the negative divergence in relative strength (going down while the market is rising,) which has previously warned of more significant corrections.

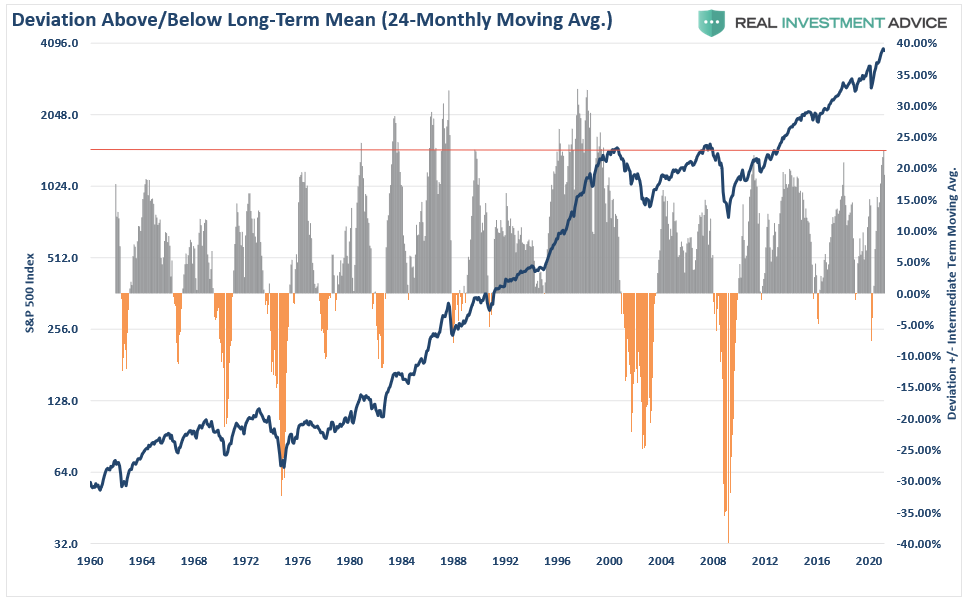

We see the same problematic setup when viewing the market’s current deviation from its 2-year monthly moving average. The current deviation has only occurred 5-times since 1960 and has always led to a correction over the next several months. (Some worse than others.)

There is little to suggest investors who are currently too “long equity risk” in portfolios now won’t eventually suffer a more severe “mean-reverting event.”

While valuations and long-term deviations suggest problems for the markets ahead, such can remain the case for quite some time. It is this long lead time that always leads investors to believe “this time is different.”

Because of the time required for long-term data to revert, monthly data is only useful as a guide to managing expectations, allocations, and long-term exposures. In other words, this data is not helpful if you are trading markets and chasing short-term gains.

Repeating For Effect

Every time I post longer-term technical analysis, I get emails chastising me for “being bearish” or “missing out.”

Therefore, let me repeat something to ensure there is no confusion.

“What this analysis DOES NOT mean is that you should ‘sell everything’ and ‘hide in cash.’”

As always, long-term portfolio management is about managing “risk” by “tweaking” things over time. We are currently primarily long equity exposure in our portfolio models, but we have raised cash as of late, heading into last week’s sell-off. (I will admit I wish I had sold more.)

As discussed this past weekend, “risk happens fast.” As such, it is essential not to react emotionally to a sell-off.

Instead, fall back on your investment discipline and strategy.

- Is the premise of why you bought a position previously still intact?

- Has anything fundamentally changed for the company?

- Review the positioning of your portfolio relative to the benchmark? Are you out of tolerance in your allocations?

- Review your positions. Are they out of tolerance relative to your sizing rules?

Last but not least, keep your portfolio management process as simplistic as possible.

- Trim Winning Positions back to their original portfolio weightings. (ie. Take profits)

- Sell Those Positions That Aren’t Working. If they don’t rally with the market during a bounce, they will decline more when the market sells off again.

- Move Trailing Stop Losses Up to new levels.

- Review Your Portfolio Allocation Relative To Your Risk Tolerance. If you have an aggressive allocation to equities at this point of the market cycle, you may want to try and recall how you felt during 2008. Raise cash levels and increase fixed income accordingly to reduce relative market exposure.

Conclusion

Nobody ever went broke taking profits.

While keeping your capital intact is hard, making up lost capital is even more challenging.

Could I be wrong? Absolutely.

If we are, we will increase our exposure back reasonably quickly. However, if the indicators warn us of something more significant, ask yourself, what’s worse?

- Missing out temporarily on the initial stages of a longer-term advance, or;

- Spending time getting back to even which is not the same as making money.

As an investor, it is merely your job to step away from your “emotions” for a moment. Look objectively at the market around you. Is it currently dominated by “greed” or “fear?” Your long-term returns will depend not only on how you answer that question but how you manage the inherent risk.

“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read