“Based on its current assessment, the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to target.” And with that statement, the European Central Bank (ECB) appears to have halted its rate hiking cycle. The announcement followed a surprise rate hike from 4.25% to 4.50%. Unlike the U.S. economy, Europe has witnessed sluggish economic growth. To wit, the ECB reduced their economic growth forecasts, cutting this year to +0.7% and reducing next year from +1.5% to +1.0%. The underlying message in today’s announcement is that they appear comfortable that weak economic growth coupled with high-interest rates will, in time, reduce inflation back to normal levels.

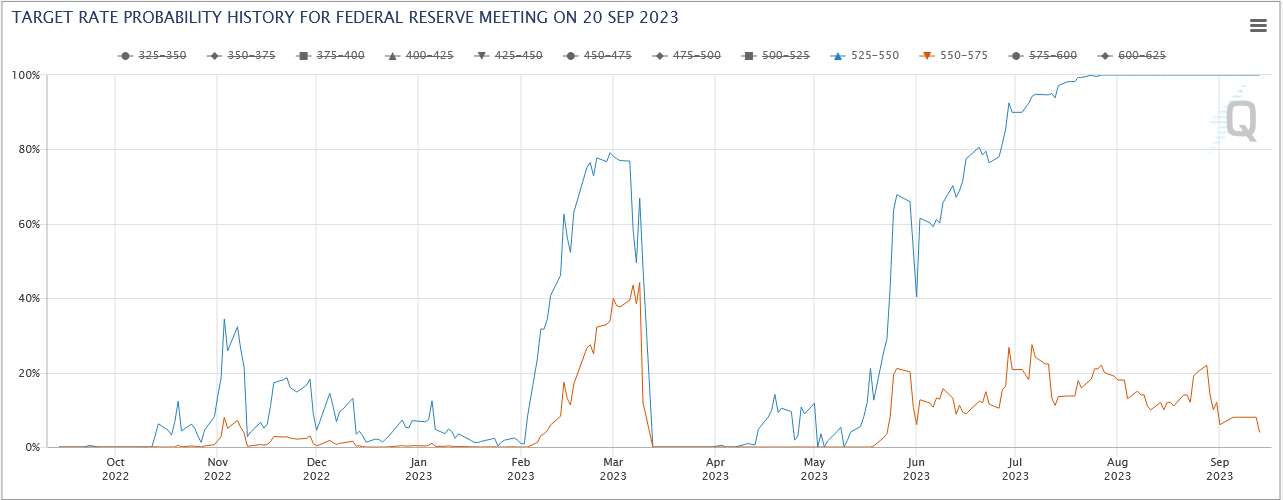

So, what might this mean for the Fed? For starters, central banks often coordinate their actions. With next week’s Fed meeting, some Fed watchers must now think the Fed takes a similar step. However, based on everything Powell has said, he will likely maintain the threat of higher interest rates until inflation is back to 2%. Letting up on his inflation vigilance could prove troublesome. If he follows the ECB, he risks roiling the bond markets and reigniting the regional banking crisis. We think they keep its “higher for longer” messaging until inflation reaches its target, the economy falters, or a financial crisis erupts. The Fed Funds futures market doesn’t expect the Fed to hike rates next week. The odds (orange) of a rate hike are 6%. The November odds are also the same as before the ECB, meaning the market doesn’t expect the hiking cycle to end.

What To Watch Today

Earnings

- No notable releases today

Economy

Market Trading Update

Despite two stronger-than-expected inflation reports, the market traded strongly higher on bets the Federal Reserve is done hiking rates. The market held support at the 50-DMA, and the rally kept the “buy signal” intact. With the market not overbought, there is further room for the market to rally into the end of the month. With volatility suppressed and volume light, there is certainly a risk of something cracking the market. Therefore, we continue to suggest remaining somewhat cautious on allocations but continue to maintain target weight exposures for now.

ARM IPO- The Next Nvidia?

SoftBank took ARM private seven years ago and is now selling some of its shares back to the public market via an IPO. The ARM IPO was priced at $51 per share, valuing the company at $54 billion. ARM’s IPO is well followed as their technology is used in almost 100% of mobile phone processors. Further, they are moving to design more chips for data centers and AI applications. Per Reuters:

Arm has told potential investors that the cloud computing market, of which it has only a 10% share and therefore more room to expand, could grow at an annual rate of 17% through 2025, mainly due to advances in artificial intelligence.

Given the recent hype around AI, its valuation is similar to Nvidia’s. Accordingly, per CNBC, ARM’s P/E based on the IPO price is approximately 104, just slightly below Nvidia’s 108. Apple, Google, Nvidia, and Samsung are among ARM’s largest clients, and all have said they will buy shares. While it may be tempting to buy the IPO and ride the AI wave, one should ask why, with such excellent prospects, SoftBank sold some of its stake in the company. As shown below, ARM shares rose by about 25% above the IPO price. Such a premium is common, but often, it is erased in the following weeks and months.

The Stimulus That Keeps Stimulating

The following joke helps us appreciate why the pandemic-related stimulus from 2020 and 2021 continues to buoy the economy.

Two economists are walking in the woods and come across a pile of bear poop. The first economist offers the second economist $100 to eat it. The second economist eats the pile of poop and collects his $100. They walk a little further and stumble upon another pile of poop. This time the second economist offers the first economist $100 to eat it. The first economist eats it and takes the $100.

They walk a little more and one economist turns to the other and says “I gave you $100 to eat poop and then you gave me back $100 to eat poop. I can’t help but feel like we both ate poop for nothing.” That’s not true, says the first economist, “we increased GDP by $200.”

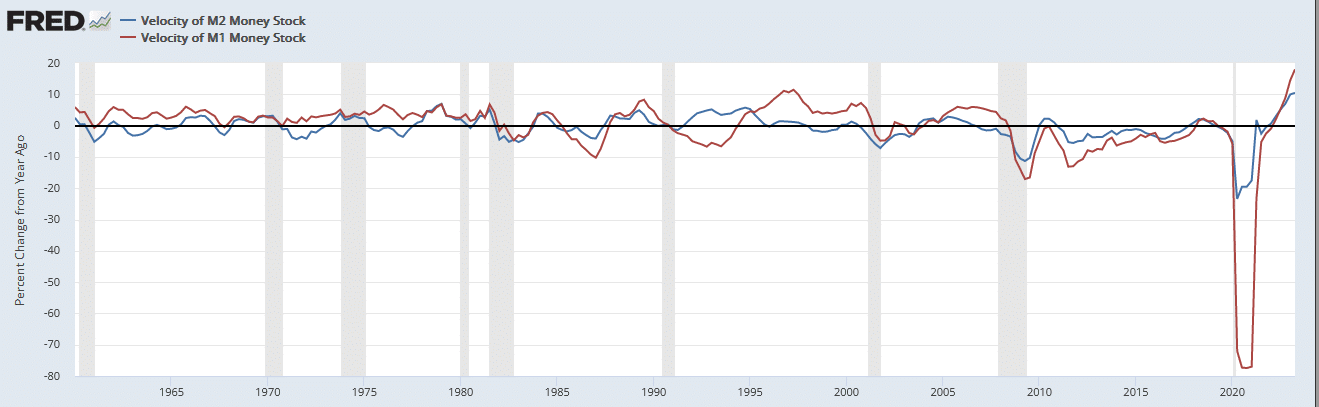

The point of the joke is that monetary velocity matters. Velocity measures how often dollars circulate in the economy. For example, if the government paid every citizen a million dollars and they all kept the money in their sock drawers, the monetary velocity of the stimulus would be zero, as would the economic benefit. Conversely, if everyone immediately went out and bought something, and then those they purchased from spent the money, and on and on, GDP would skyrocket. We have written about the importance of monetary velocity (HERE and HERE). These articles and others show how the combination of the money supply and monetary velocity determines inflation.

As the joke alludes, velocity also significantly affects GDP. It also helps further explain why we see such a lag between higher interest rates and economic weakness. Overconsumption is a well-known behavior resulting from the pandemic. Therefore, the stimulus dollars keep circulating and likely will until behaviors normalize.

As we show, two measures of the annual change in monetary velocity are at 60+ year highs.

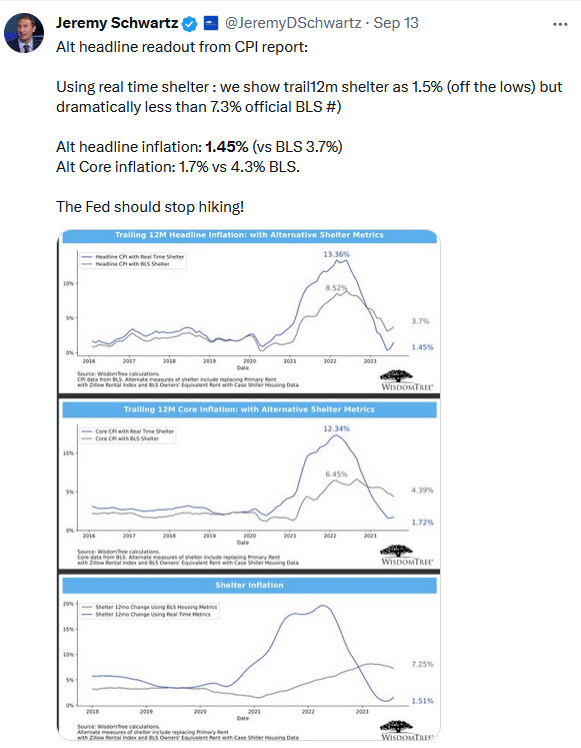

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.