The Crosscurrents of In/De-flation

The remarkable deflationary and inflationary crosscurrents swirling through the economy are grossly underappreciated and misunderstood. Need proof? Watch CNBC or read Wall Street research and consider the likelihood of the smooth path back to “normal” they tout.

It is comforting to think about “normal” and what that may entail for our lives and portfolios. However, given the global economic tsunami and extraordinary monetary and fiscal stimulus, we would be remiss if we did not raise awareness that economic and market recovery may be far different from “normal.”

One of our deepest concerns is a highly inflationary outcome, an experience not seen in fifty years, and one for which we are least prepared. Markets always have a strange way of finding investors weakest points.

Disequilibrium Defined

“Inflation defined is, in fact, a disequilibrium between the amount of currency entering an economic system relative to the productive output of that same system.” – From our recent article, Jerome Powell & The Fed’s Great Betrayal:

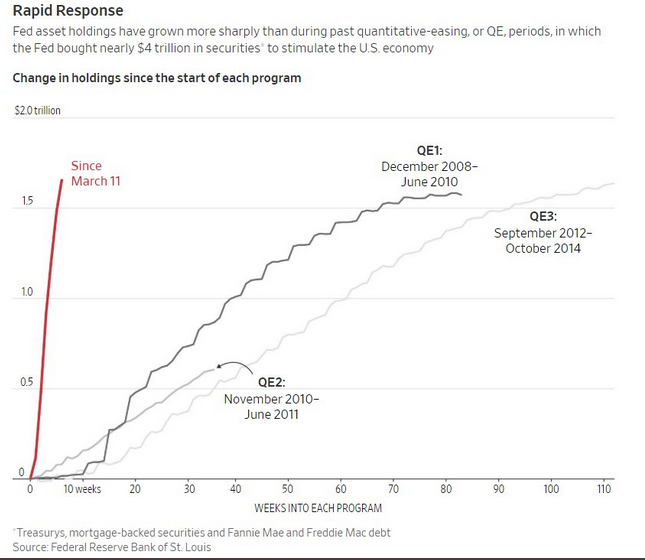

As of April 13, 2020, the money supply, measured by M2, has grown 15.9% on a year over year basis. The vast majority of the growth occurred over the last month as the Fed’s balance sheet exploded by 61%, dwarfing all prior QE operations.

The apparent reason for the Fed’s actions is a plunge in consumption and the productive output of the nation combined with an unprecedented flood of unemployment claims.

Despite those maneuvers, the economic decline is destroying economic output and is, thus far, deflationary in aggregate. We expect deflationary imbalances to continue to dwarf inflationary impulses while economic conditions languish.

However, we must consider that all of the newly created money and debt, crippled supply chains, and many other economic, social, demographic, and geopolitical factors can suddenly offset deflationary imbalances and supercharge prices when the economy does pick up.

In this article, we look back at history and gauge what has driven past bouts of inflation and compare them to the current one. In the next part two, for RIA Pro subscribers only, we share analysis of how 49 different industry sectors performed during prior inflation eras.

Given the enormous monetary and fiscal policy response to current circumstances, the growth in money supply and debt, and the low probability that the economy will ever be capable of servicing those obligations without inflation, this overlooked topic is essential.

The Monetary Exchange Equation

Before sharing our analysis, it is worth revisiting our article, Stoking the Embers of Inflation. In the article, we presented the well-known equation below, which provides a foundation for understanding how prices change.

Monetary Exchange Equation

To understand how the Fed’s commitment to continued interest rate hikes and balance sheet reduction (Quantitative Tightening – QT) affect inflation or deflation, the Monetary Exchange Equation should be analyzed closely. The equation is not a theory, like most economic frameworks based on assumptions and probabilities. The equation is a mathematical identity, meaning the result will always be true no matter the values of its variables. The monetary exchange equation is as follows:

PQ = MV

The equation states that the amount of nominal output purchased during any period is equal to the money spent. Said differently, the price level (P) times real output (Q) is equal to the monetary base (M) times the rate of turnover or velocity of the monetary base (V). The monetary base – currency plus bank reserves, is the only part of the equation that the Federal Reserve can directly control. Therefore, we believe to form future price expectations, an analysis of the Monetary Exchange Equation using the forecasted monetary base is imperative.

The Inflation Identity

Through simple algebra, we can alter the Monetary Exchange Equation and solve for prices. Once the formula is rearranged, the change in prices (%P) can be solved for, as shown below. In doing so, what is left is called the Inflation Identity.

%P = %M + %V – %Q

Prices are a function of the change in the money supply and the velocity of money less the economic output.

Today’s Equation

We know the money supply is soaring, but at the same time, the velocity of money and economic output are plummeting. The destruction of monetary velocity is offsetting inflationary pressures.

Someday soon, consumers and corporations will spend again, causing monetary velocity to pick up. At the same time, the Fed has been vocal that they will remain cautious about removing stimulus.

Our inflation concerns stem from the Fed’s sentiment and its track record over the last decade.

After the Financial Crisis and recession of 2008/09 ended, it took the Fed five years to halt the multiple quantitative easing (QE) campaign, seven years to begin raising interest rates from zero, and nearly a decade to attempt reducing the size of their balance sheet. In fact, in September of 2019, despite a strong economy, a 50-year low unemployment rate, and historically easy financial conditions, the Fed started up QE 4. The basis for that decision was that the repo markets were not allowing hedge funds to maximize their leverage, thus threatening support for risky assets.

Even in its infancy, this recession is worse than the previous crisis and recession. Based on the Fed’s activities from the last ten years, what is the likelihood that current or future Fed leadership will be any quicker to remove stimulus this time?

Historical Bouts of Inflation

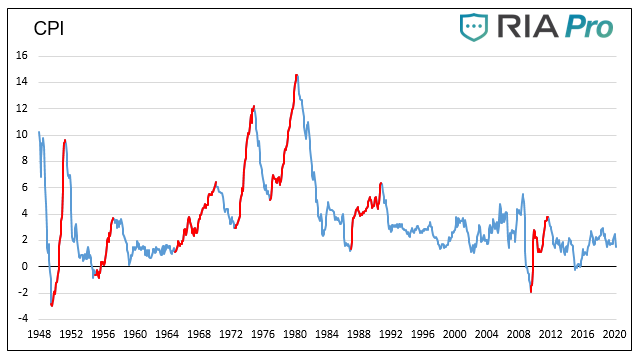

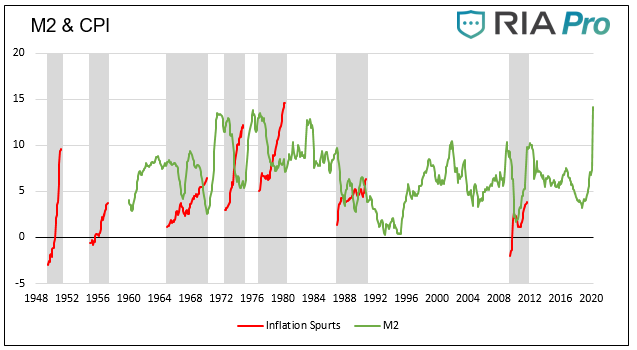

Since the late 1940s, there have been seven periods in which inflation rose significantly over a relatively short period. Those periods, forming the basis of our analysis, are shown in red below.

The impetus for inflation during each instance is unique to that period. For example, inflation of the early late 1960s and the 1970s was, in part, the result of oil embargos, the emergence of the baby boomer generation, the Vietnam War, and the sexual revolution.

In 1971, President Nixon stoked inflationary pressures when he suspended the Gold standard. His action gave the Fed more flexibility to increase the money supply at its whim. For more on Nixon’s fateful decision, please read our article- The Fifteenth of August.

Inflation of the late 1940s and mid-1950s was in large part due to post-WWII global rebuilding and the suburbanization of America, respectively. The Fed played its role by goosing the money supply to cap interest rates from 1942 to 1951.

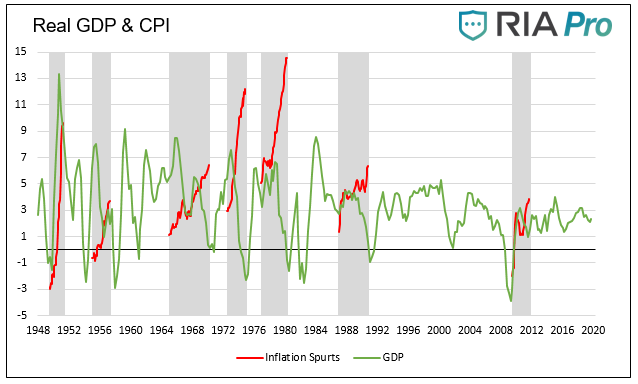

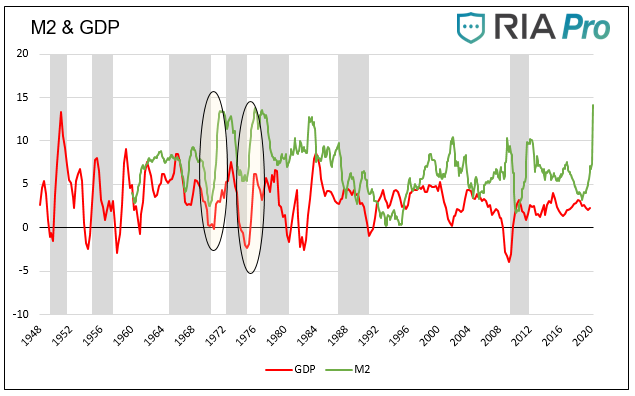

The following two graphs show how GDP and money supply varied during the highlighted inflationary periods.

Data Courtesy St. Louis Federal Reserve

As the graphs show, and as a reflection of the complexity of an economic system, there is no prescribed set of monetary and economic circumstances that determine if inflation will occur. We only know that inflation is a “monetary phenomenon” and is the result of a deliberate act of policy. Still, there are some important takeaways that we can apply to the current situation.

Note that in the GDP CPI graph, six of the seven inflation “events” happened during or after substantial increases in real (inflation-adjusted) GDP.

Data on money supply (M2) only goes back to 1960, so the first two instances of inflation are not comparable. The two most substantial increases in M2, the 1970s, were followed shortly by inflation. Looking at the others, however, the correlation between M2 growth and inflation is not as evident.

Comparing GDP and money supply to prior bouts of inflation leads us to consider that the two inflationary episodes of the 1970s are most applicable to current circumstances. Make no mistake; there are many economic and social differences between then and now.

But, the synchronization of increasing economic activity and the money supply was, in large part, responsible for inflation in the 1970s. It might also be the recipe for inflation in the coming years.

1970s Redux?

Once a reliable treatment and/or vaccine for COVID-19 is developed, economic activity will come out of its coma. The combination of people finding jobs, companies spending to grow production to meet rising demand, and the release of pent up consumption pressures will produce a sharp increase in GDP.

We have little doubt that the government will further fuel recovery with multi-trillion dollar deficits. We have even less doubt that the Fed will keep money flowing to fund the deficits at reasonable interest rates.

Such a scenario does not mean GDP will return to pre-COVID levels, but it implies that economic growth rates will be outsized compared to growth rates of the prior decade.

How does this experience compare to the 1970s?

Unshackled by the limits of the gold standard, the Fed twice sharply increased the money supply during the 1970s. As mentioned earlier, the first instance in the early 1970s was to fend off a recession and fund the Vietnam War. The second round of money printing was to combat economic weakness from 1973-1975 due to a gas price shock from the oil embargo. Both periods witnessed GDP growth of around 7% and annual money supply growth of about 10%.

Also, consider that even before the Coronavirus pandemic, there were only two periods on record where fiscal deficits expanded despite the economy running at full employment. One was during the Johnson administration in the mid-1960s, and the other was 2018-2019. Fiscal stimulus in the 1960s played a role in laying the foundation for inflation in the 1970s and early 1980s. It is an equally important point of consideration today.

It also bears mentioning that the extent of supply chain reconfigurations likely to take place will force companies to find alternative ways of sourcing and manufacturing products. That necessarily means companies will pay more for inputs, and customers will pay more for end products. That is not deflationary.

Maybe the economy will not grow as much as we think, but the Fed is sure to be very reluctant to remove stimulus. We believe the 1970s, with its corresponding economic and money supply growth, although imperfect, is a good analog for the future.

The graph below highlights the corresponding increases in GDP and M2 during the 1970s. As a point of comparison, the growth of M2 and GDP before the other three episodes in which M2 data is available occurred separately and thus sharply reduced the inflationary impact.

Summary

Given the scope of the current situation, a return to something other than normal is not a long-shot proposition. We would be failing you, our readers, if we did not put in the time and effort to think about and plan for something other than what supports the paychecks of “professionals.”

Inflation is a real and present danger, and policy decisions are the cause. A complex crosscurrent of influences will determine the magnitude of an inflation problem.

Make no mistake; regardless of whatever happens with the virus and economic activity, the Fed’s monetary actions today and tomorrow are the most significant input.

Having watched the Fed for decades and listened to many Fed Presidents’ urge for policies that drive inflation higher, it would be wise to think about how to structure a portfolio in times of inflation.

We cannot predict, but we can prepare, and the road ahead is likely to be very different than the road behind.