After much anticipation, SpaceX (SPCX) begins trading tomorrow. The headlines will focus on the $2 trillion valuation and the likely significant volatility in the price once the SPCX begins trading. Before you decide whether to participate, it is worth understanding what you are actually buying, because SPCX is not one business. It is three very different businesses.

Starlink, the satellite internet business, is the financial bedrock supporting SPCX. It generated over $11 billion in revenue in 2025, a 38x increase since 2021. Estimates suggest revenue could approach $16 billion for full-year 2026. It accounts for 61% of SPCX’s total revenue and is the only profitable segment. Starlink has 9 million subscribers across 164 countries, a 63% EBITDA margin, and a $1.2 billion quarterly profit run rate. Starlink would be a premier standalone public company. While the financial data is good, there are some concerns as Starlink is pushing into lower-priced international markets. The larger customer volumes are beneficial, but they come at the cost of a steadily declining average revenue per user. To wit, revenue per user has fallen from $99 per month in 2023 to $66 today.

The rocket launch business and the AI (xAI) segment are not currently financially rewarding. The rocket division is a long-term bet on Starship’s unproven economics, while its AI business is burning cash at a concerning rate. We continue this commentary in a second article below with more details on its rocket and AI divisions.

SPCX is priced as a bundle. You are buying Starlink’s proven cash flows alongside two businesses whose outcomes could be enormous but are very uncertain. The float is just 5% of shares outstanding, which means liquidity will be thin and volatility will likely be high in the early days of trading. Over time, pre-IPO holders of SPCX will be able to sell shares, thus increasing the float and liquidity.

What To Watch Today

Earnings

Economy

Market Trading Update

Editor’s note: I’m traveling this week, so I’m writing this about an hour ahead of Wednesday’s close. The levels below are intraday as of roughly 3 p.m. ET on June 10. Treat the closing prints as approximate.

Yesterday, we discussed the ongoing correction in the semiconductor market. The market action on Wednesday was much the same. The technology selloff that began with Broadcom’s guidance miss on June 3 refuses to quit. As I write, the S&P 500 is off about 1.3%, the Nasdaq is down roughly 1.7%, and the semiconductors are taking the worst of it again. The chip ETF has now given back better than 10% from its June 3 peak. That’s a textbook correction in a single week, and it happened while the broad index barely flinched.

So what’s actually pulling this market lower? Three things. Only one of them is the story everyone wants to tell.

First, the chips got too far over their skis. Broadcom’s failure to raise its AI outlook was the pin, and momentum money has been heading for the exits ever since. Second, today’s catalyst is macro, not tech. Oil jumped after the U.S. and Iran traded fresh strikes near the Strait of Hormuz, and this morning’s inflation print came in warm. Pricier oil plus stickier inflation pushes rate cuts further out, and none of that is about chips.

Third, and here’s the piece I think matters most over the next 48 hours. SpaceX prices Thursday night and starts trading Friday on the Nasdaq under the ticker SPCX. It’s the largest IPO in history, a $75 billion raise at a $1.75 trillion valuation, with up to 30% of the deal, call it north of $22 billion, set aside for retail buyers. Make no mistake, that cash has to come from somewhere. When the biggest liquidity sponge Wall Street has ever built is set to soak up money Friday, selling your crowded tech winners on Wednesday to raise dry powder isn’t panic. It’s housekeeping.

So is this selloff “just” SpaceX derisking? No. But pre-IPO positioning is the quiet third leg, and it explains why the selling keeps concentrating in exactly the mega-cap tech names a retail investor would trim to go chase SPCX.

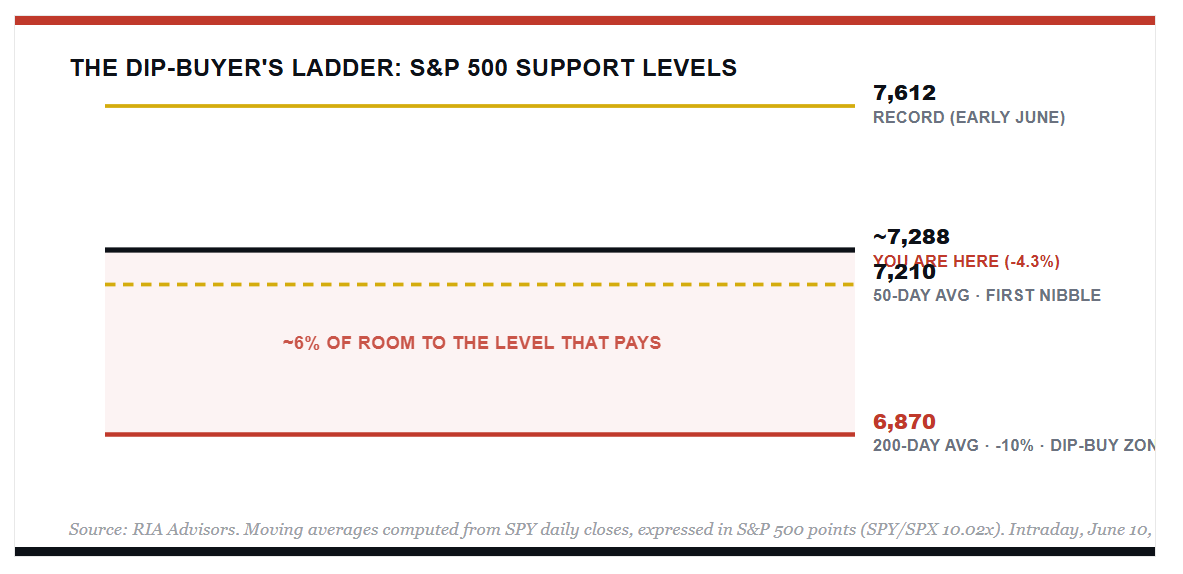

Here’s the question I keep getting on the road, and my framework for it. The S&P is only about 4% below its early-June record. That’s not a correction. That’s a wobble. The 50-day average sits right beneath us near 7,210, and we’re testing it now. Treat that as a first nibble, not a back-up-the-truck signal. The level I actually want is the 200-day near 6,870, about 6% lower and a full 10% off the highs. As we’ve noted before, that’s where corrections inside an ongoing bull market find real buyers.

Bob Farrell’s Rule No. 4 still applies. Exponential moves go further than anyone expects, then correct the same way. We saw the up leg. We’re watching the down leg now, and it tends to overshoot. That’s why I’m not in a hurry. If Friday’s deal goes well, this week’s raised cash flows right back into the tape. If it stumbles, you’ll be glad you waited.

The bottom line is simple. Don’t chase the bounce, and don’t buy the first 4%. Scale into your targets in tranches, keep your stops honest, and let Friday’s liquidity event clear before you commit real capital.

The Other Two Businesses: Rockets And AI

In the opening, we made the case that Starlink is the compelling core of the SpaceX investment thesis. Now we dig into the rocket launch business and xAI.

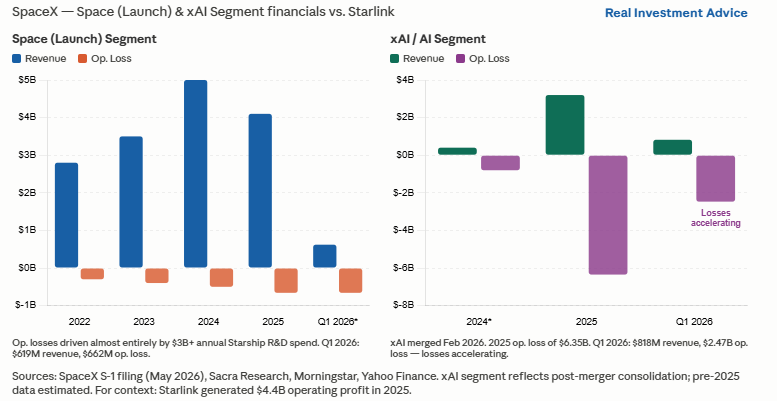

The space launch segment generated $4.1 billion in revenue in 2025 but posted a $657 million operating loss. Revenues, which had been climbing, fell by $1 billion last year from 2024. While the launch division is profitable, R&D expenses result in a net loss. The bullish case is straightforward: if Starship delivers on its promise of reusable heavy-lift rockets at lower cost, it will transform the economics of the entire launch industry. Total Starship spending now exceeds $15 billion and is likely to continue growing. The potential payoff is tremendous, but the timeline remains uncertain. While they are the industry leader, there is competition from Blue Origin (Jeff Bezos) and Rocket Lab (RKLB)

The xAI segment is riskier. The AI business encompasses the Colossus supercomputing facility, the Grok assistant, and the X platform. It generated $3.2 billion in revenue in 2025, while incurring a $6.4 billion operating loss. Based on its first quarter 2026 numbers, it is on pace for a $10 billion loss. Unlike its Starlink and rocket divisions, competition is fierce for AI products. Grok has fewer than 10% of the users that ChatGPT and Gemini have, and even less revenue per customer. With the enormous capital being spent by ChatGPT, Anthropic, and Gemini, xAI has a difficult path to profitability.

Taken together, the launch business is a long-term infrastructure bet, and xAI is a gamble that it can compete with dominant AI players. Both divisions have investment merit as well as significant risks. Starlink is the business you are paying for. These are the businesses you are getting alongside it.

The IPO Boom: Where Will The Capital Come From

Think of the stock market as a jar full of marbles. For the new SpaceX (SPCX) and other IPO marbles to fit in the jar, either the jar must be enlarged, or some of the other marbles must shrink.

Given the current monetary environment, the jar, or available capital, is unlikely to grow significantly. The Fed is no longer providing the flood of liquidity that enabled the easy digestion of the SPAC boom in 2020 and 2021. Rates are higher, savings rates are lower, and the equity market is already trading at elevated valuations. Simply put, there isn’t much extra liquidity. Thus, the other option is for the collective market cap of everything else to decline.

In reality, there will be some shrinkage of marbles and an enlargement of the jar. The extent of both will help determine how the IPO boom is received and its impact on other stocks.

Tweet of the Day

New UPDATED Trading Rules With Desktop Printout

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.