The fiscal and monetary responses to the “coronavirus” created a surge in savings. While many hope those savings will go back to work, the “savings mirage” won’t save the economy.

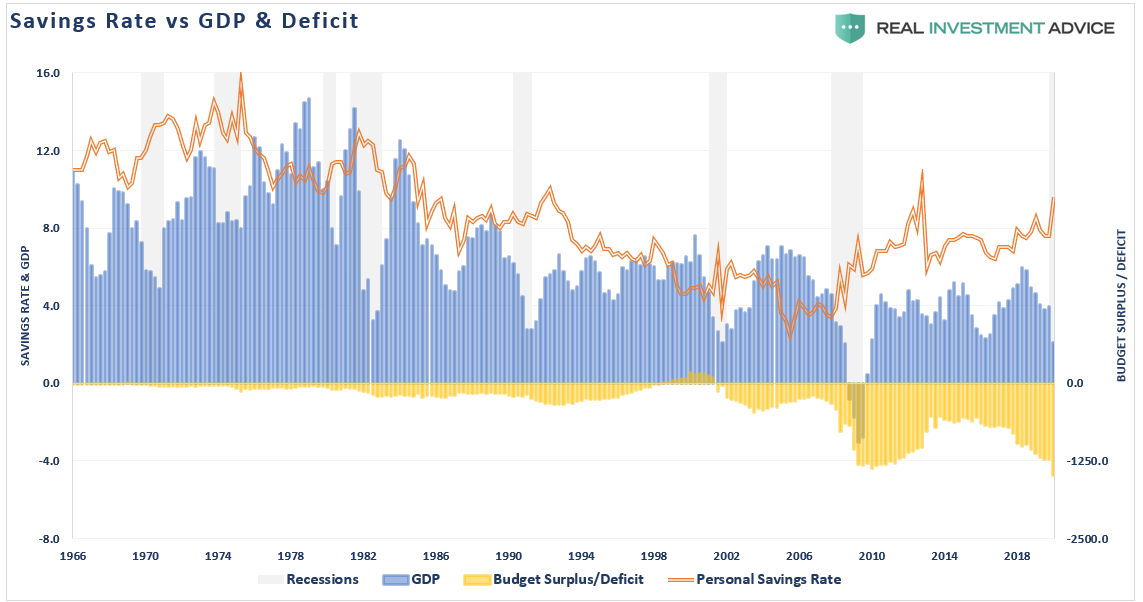

In recent weeks, there has been a good bit of chatter about the surge in the “savings rate.” The rate has now jumped to the highest levels seen in the last couple of decades, suggesting the consumer is now “well-positioned” for a “consumption comeback.”

As Bank of America’s Michael Hartnett suggests, the consumer has the “ability” to finance the recovery.

The hope is that these “cash hoards” will eventually begin to flow back into the economy through increased applications for mortgages, autos, and durable goods. That increase in consumption will also lead to a decrease in the staggering $3.8 Trillion deficit by the end of the year.

Such is the “hope” anyway, and a point we discussed in our previous series on capitalism (Read Here).

“Deficits are self-financing, deficits push [interest] rates down, deficits raise private savings.” – Stephanie Kelton

On the surface, there does seem to be a correlation between surging deficits and increases in private savings.

However, the “savings rate” is a mirage, and like all mirages, they disappear upon closer inspection.

The Savings Mirage

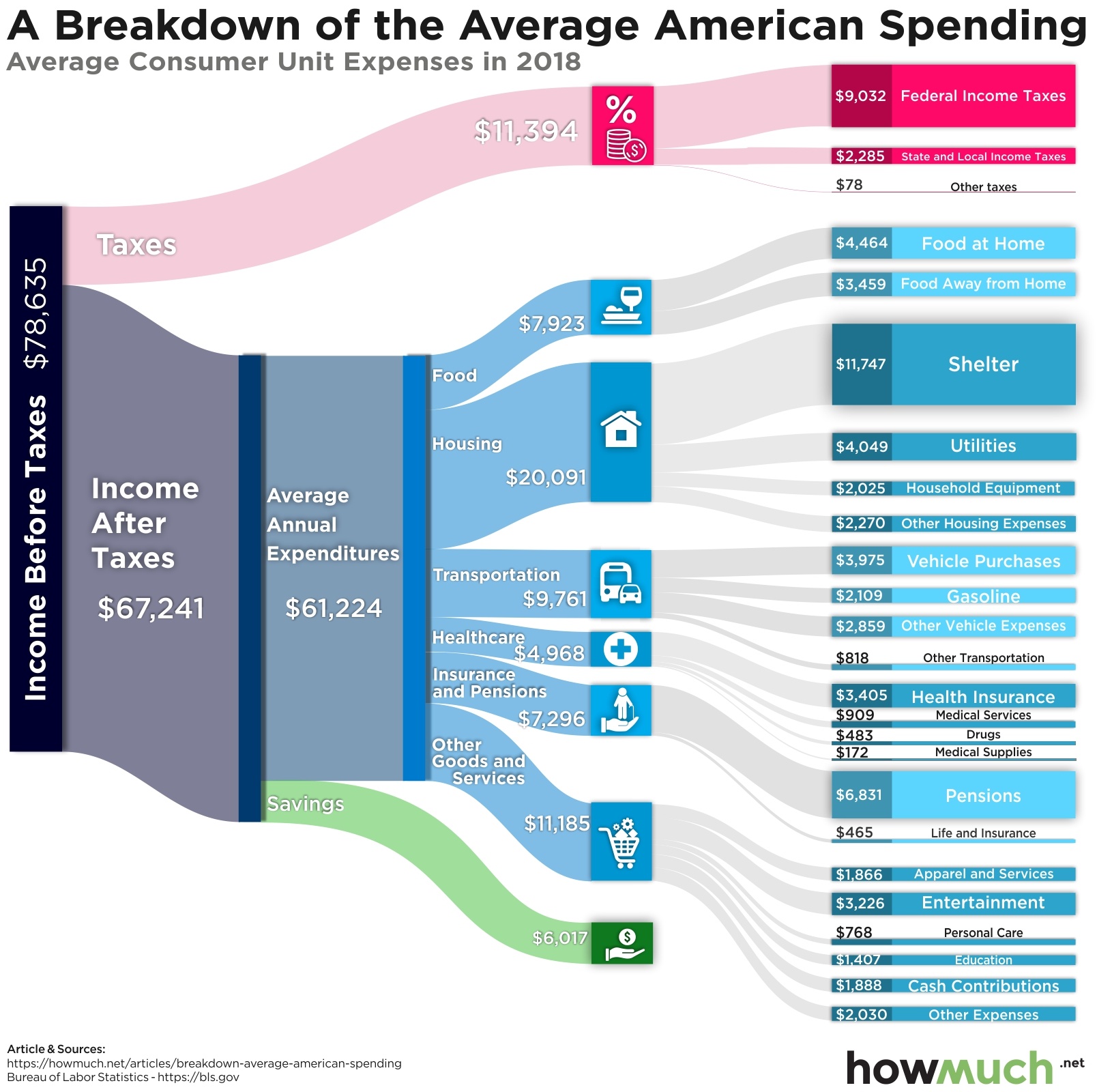

To understand why the “savings rate” is not what it appears to be, you have to understand its underlying construction. The website HowMuch.com recently provided that calculation of us.

While the table is dated, as the savings rate has jumped to 13.1%, you gain a perspective of the calculation.

Lies, Damn Lies, and Statistics

The are multiple problems with the calculation.

- It assumes that everyone in the U.S. lives on the budget outlined above.

- It also assumes the cost of housing, healthcare, food, utilities, etc. are standardized across the country.

- That everyone spends the same percentages and buys the same items as everyone else.

The cost of living between California and Texas is quite substantial. While the inflation-adjusted median household income of $63,179 may raise a family of four in Houston, it is going to be problematic in San Francisco.

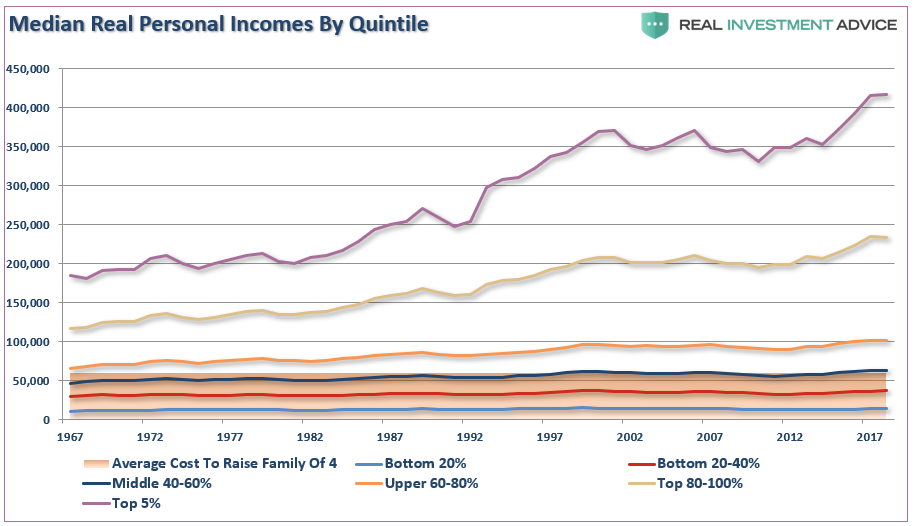

While those flaws are apparent, the biggest issue is the top 10% of income earners skew the rate sharply upwards. The same problem also plagues disposable personal income and debt ratios, as previously discussed in “America’s Debt Burden Will Fuel The Next Crisis.” To wit:

“The calculation of disposable personal income (which is income less taxes) is largely a guess, and very inaccurate, due to the variability of income taxes paid by households.

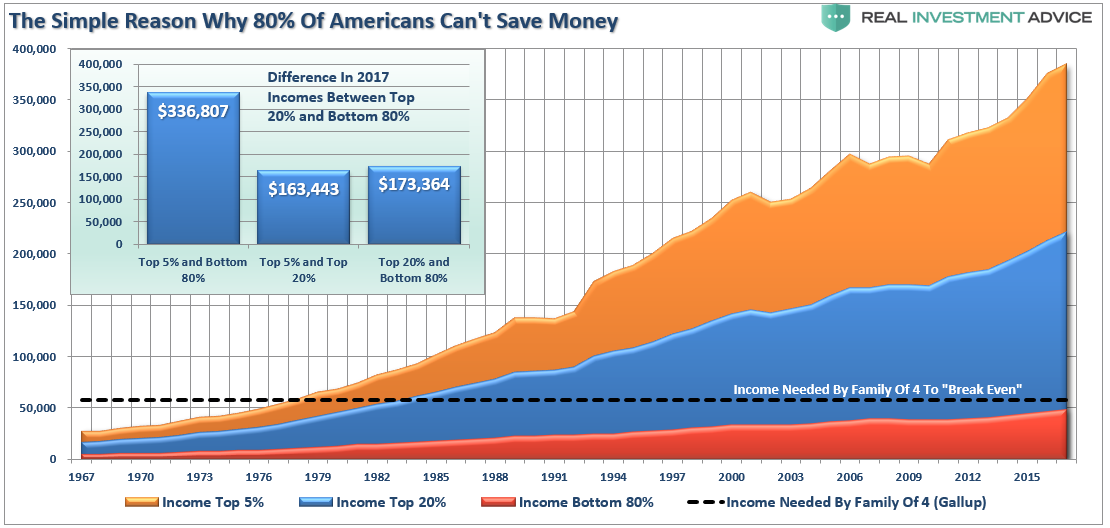

More importantly, the top 20%, and specifically the top 5%, of income earners skew the measure. Those in the top 20% have seen substantially larger median wage growth versus the bottom 80%. (Note: all data used below is from the Census Bureau and the IRS.)”

Since the top income earners have more than enough income to maintain their standard of living, the balance falls into savings. This disparity in incomes also generates a “skew” to the savings rate.

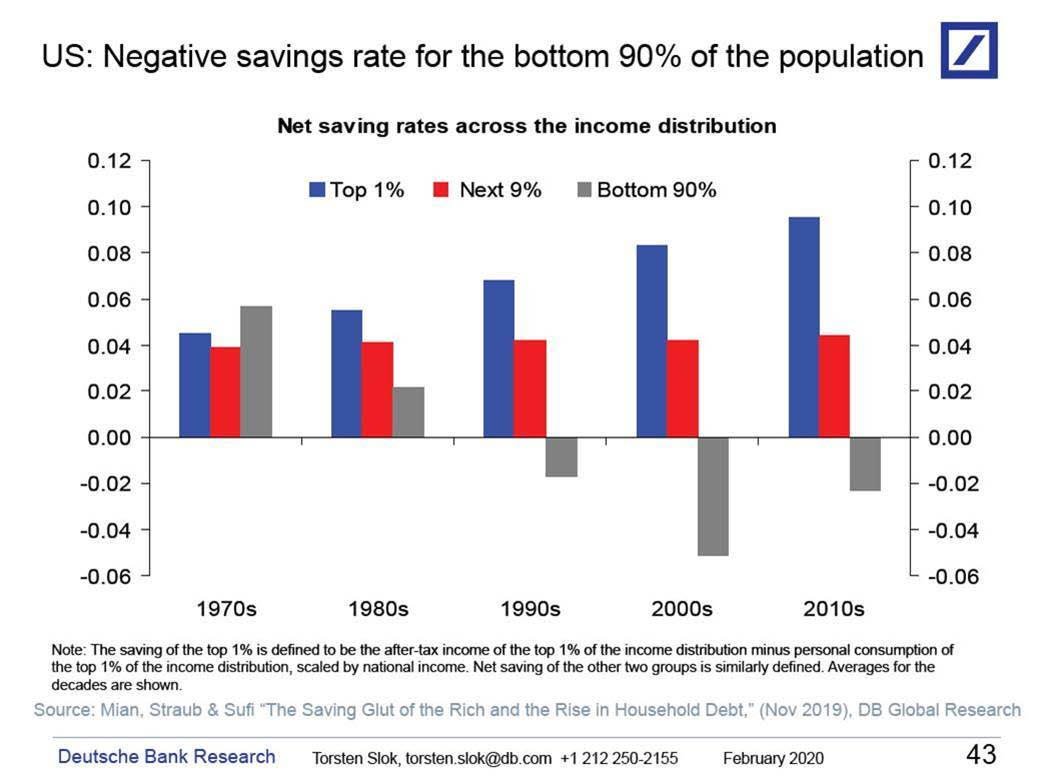

Just The 10%

The chart below from Deutsche Bank shows that “savings” are confined to the top-10% of income earners, as the bottom 90% struggle to make ends meet by increasing debt levels.

While Government numbers suggest average Americans are saving 13% of their income, the majority of “savings” is coming from the differential in incomes between the top 20% and the bottom 80%.

In other words, if you aren’t in the “Top 20%” of income earners, you probably aren’t saving a chunk of money.

No Savings

The recent uptick in the savings rate isn’t what it seems. As Frank Hollenbeck recently penned for The Mises Institute.

“In response to a likely worldwide recession, governments have turned on full blast the fiscal and monetary spigots. A $2 trillion spending plan. Central banks are on a buying spree. And the $1200 stimulus payment is just helicopter money.

Since the government does not have a magical tree of plenty. They can only redistribute from the left pocket to the right. Such is done by taxing, borrowing, or printing money. How does this make any economic sense or make any country better off?

He is correct.

The bottom 80% of the population spend roughly the entirety of their income every month. Therefore, when jobs are lost, wages are cut, or interest rates rise, there is no excess income to cover the shortfall.

As we discussed recently in why the Federal Reserve are stuck at zero interest rates:

“The differential between incomes and the actual “cost of living” is quite substantial. Researchers at Purdue University issued a study of global data. In the U.S., researchers found that $132,000 annually was optimal for “feeling” happy when raising a family of four. (I can attest to this personally as a father of a family of six)

A previous Gallup survey found it required $58,000 to support a family of four in the U.S. (Forget about being happy, we are talking about “just getting by.”)”

The Calvary Isn’t Coming

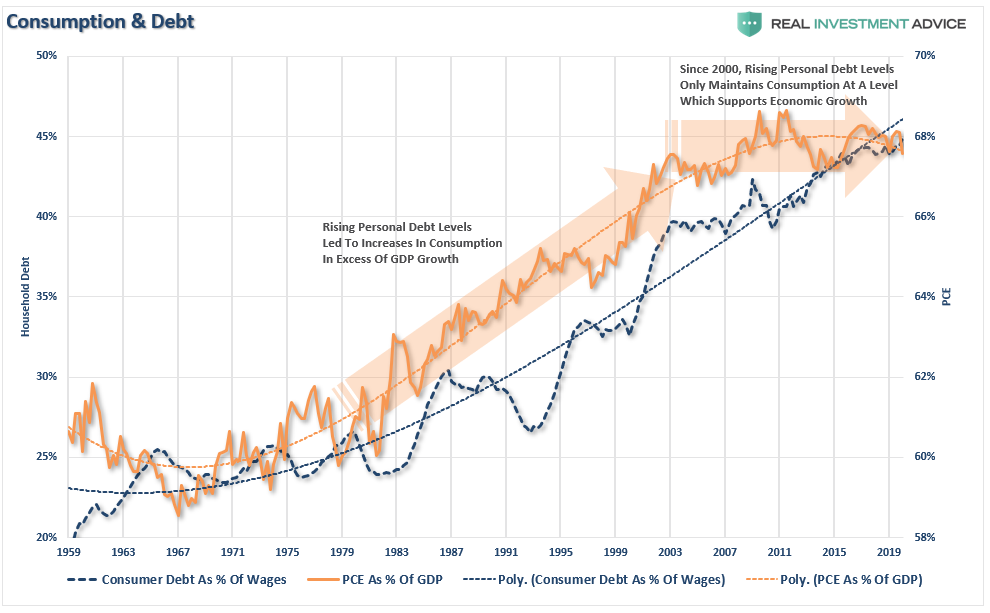

The issue with the lack of savings for the bottom 80-90% is that economic growth is roughly 70% consumption. Those in the top 10%, which have capacity to spend, have little need to substantially increase their rate of spending.

As noted, while consumption does make up 70% of the economy, it has been a function of debt growth over the last 40–years. Prior to 2000, expansions in personal debt increased consumption and fueled economic growth. Since 2000, increases in debt are simply sustaining consumption at levels to “maintain” economic growth.

Mind The Gap

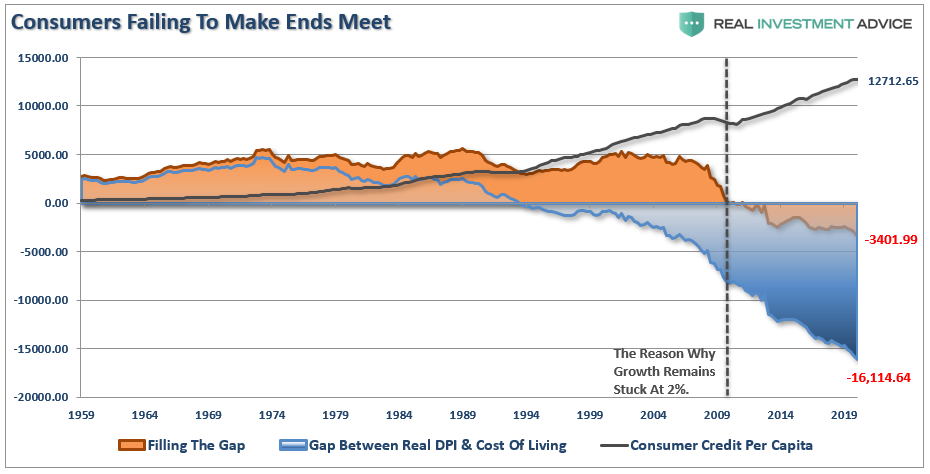

The reason this is occurring is the “gap” between the “standard of living” and real disposable incomes has widened. Beginning in 1990, incomes alone were no longer able to maintain the standard of living so debt filled the “gap.” However, following the “financial crisis,” even the combined levels of income and debt no longer solve the shortfall. Currently, there is a $3400 annual deficit that is filled by increases in debt.

The “gap” explains why consumer debt is at historic highs and growing each year. If individuals were saving 13% of their money every year, debt balances would at least be flat, if not declining, as debt is paid down.

No V-Shaped Recovery

The impact to the economy from record levels of unemployment are going to have a wide range of impacts which will forestall an economic recovery.

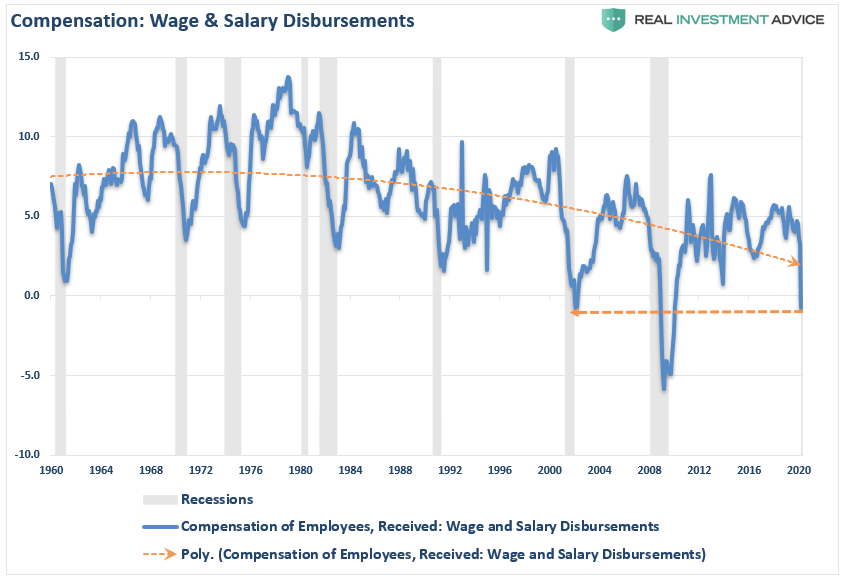

The first, of course, is a deep suppression of wage growth which is derived from both recessionary drags and job losses.

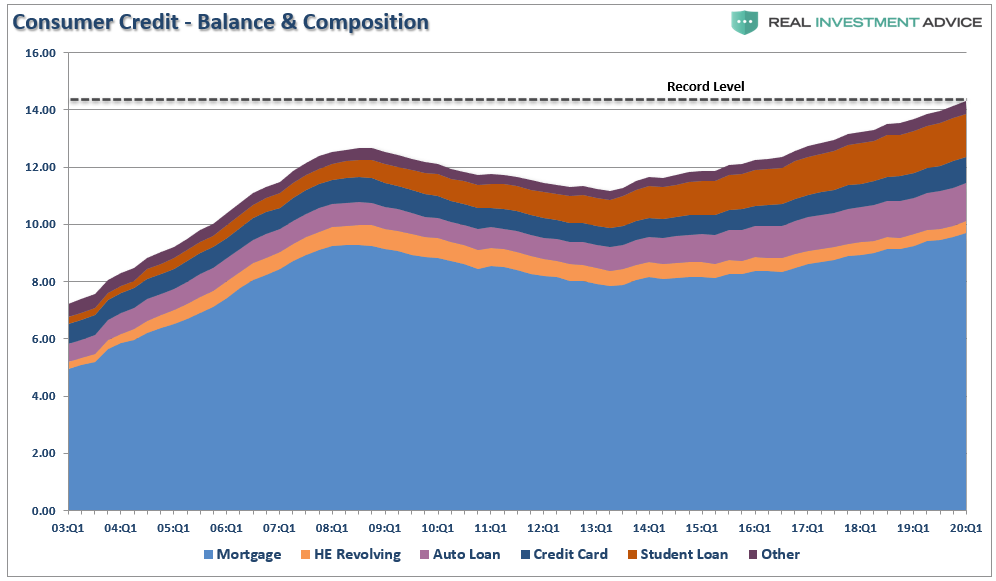

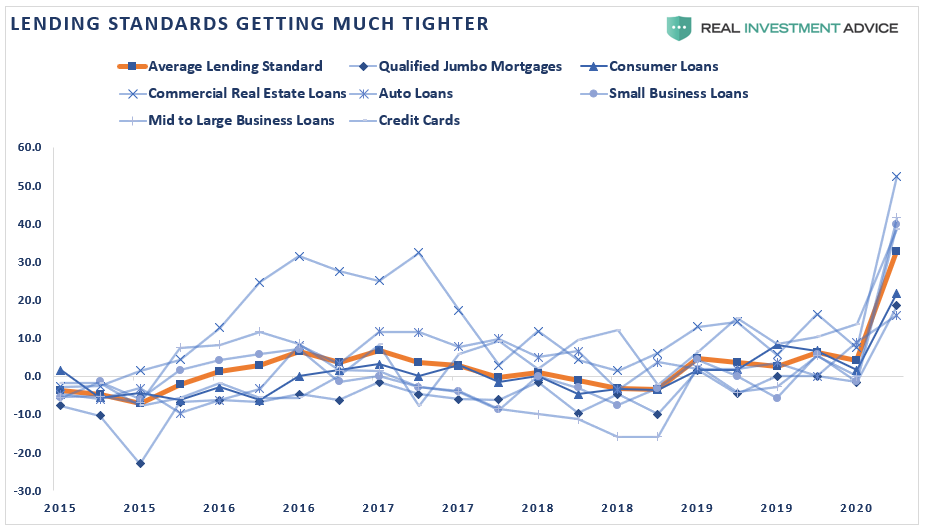

With reduced incomes, it is not only harder to make ends meet, but also harder to obtain additional credit. Given consumers are dependent upon credit to “fill the gap,” and with banks tightening lending standards, access to credit will become more difficult.

Both of these factors will likely ensure the expected “V-shape” recovery in the economy is overly optimistic. While there will most assuredly be a bounce in the data as the economy is reopened, the headwinds will likely stall the advance.

Broken Economics

The Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the end result, has been clearly wrong.

It hasn’t happened in 40-years.

MMT supporters also share the view that if the government hands out money, it will create stronger economic growth. There is no evidence which supports the case.

Savings rates didn’t fall in the ’80s and ’90s because consumers decided to just spend more. If that was the case, then economic growth rates would have been rising on a year-over-year basis.

Unfortunately, as the economy shifted from a manufacturing to service-based economy, increases in productivity suppressed wage and economic growth rates. Consumers were forced to lever up their household balance sheet to support their standard of living. In turn, higher levels of debt-service ate into their savings rate.

Conclusion

American’s are not “saving more money.” They are just spending less as weak wage growth, an inability to access additional leverage, and a need to maintain debt service, restricts their spending.

Unless, of course, you are in the top 20% of income earners.

By the time the current recession, and bear market, are over, it will take much longer than anticipated for the economy, and markets, to bounce back. Each recovery has already been slower, and weaker, than the last, and the next recovery will be no different.

With growth rates below two-percent on average, wage growth suppressed, and a large contingent of boomers withdrawing assets to sustain their living requirements, the ability to generate higher levels of economic growth will be limited.

This will especially be the case as exceedingly large debt levels, and deficits, which were used for non-productive purposes, further inhibits economic prosperity.

For those hoping “savings” will save the economy, they are likely to disappointed when the mirage fades into dust.