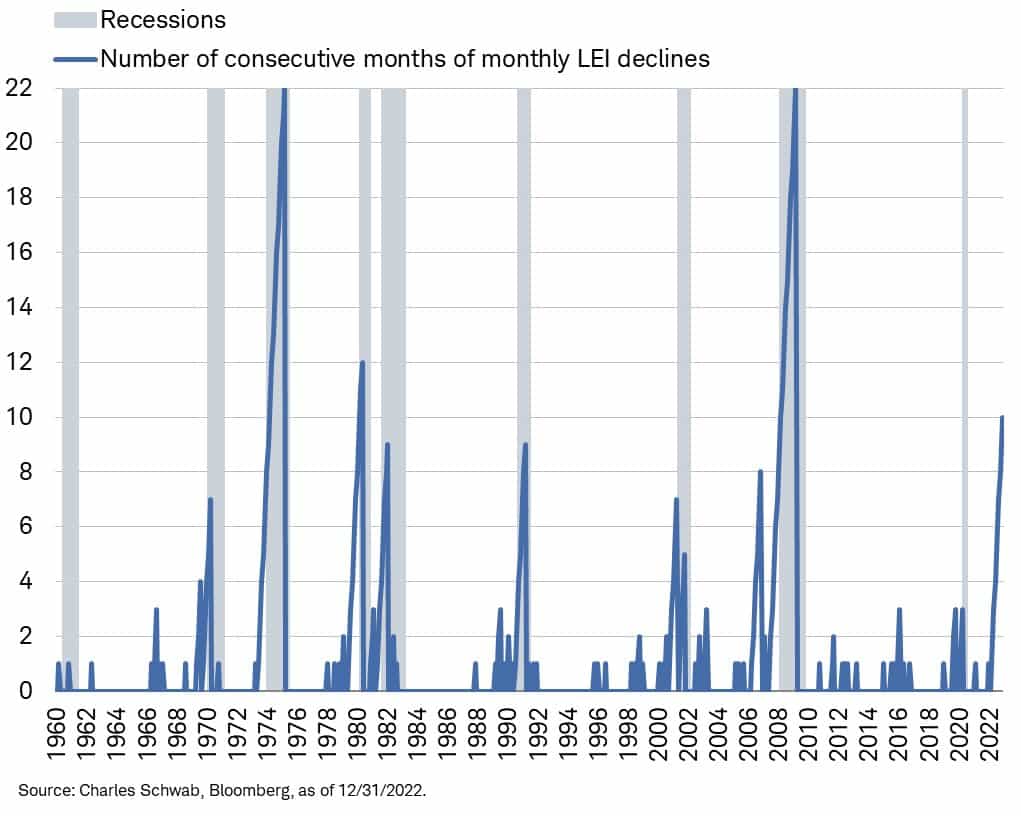

The U.S. Leading Economic Indicators, compiled by the Conference Board, fell by 1.0%. The decline was the tenth in a row. As shown below, such a streak of consecutive monthly declines has led to seven of the last eight recessions. The pandemic-related recession is the outlier. Given the unexpected and somewhat random nature of the pandemic, it is not surprising that this indicator or any leading indicator could not forecast it. The following quotes are from the report.

There was widespread weakness among leading indicators in December, indicating deteriorating conditions for labor markets, manufacturing, housing construction, and financial markets in the months ahead. … The Conference Board’s Leading Economic Indicators continue to decline and foreshadow a recession is coming.

The breakdown of the ten components of the index is interesting. The financial components, primarily a function of asset market expectations, are flat over the last month and six months. Non-financial components, such as ISM, Building Permits, are Consumer Expectations are fully responsible for the streak of consecutive declines in this leading indicator measure. Two of the three financial indicators, stocks and credit spreads, are not foreshadowing a recession, but the yield curves are. Are the stock and corporate bond markets correct, or will they be surprised if the indicator again proves prescient?

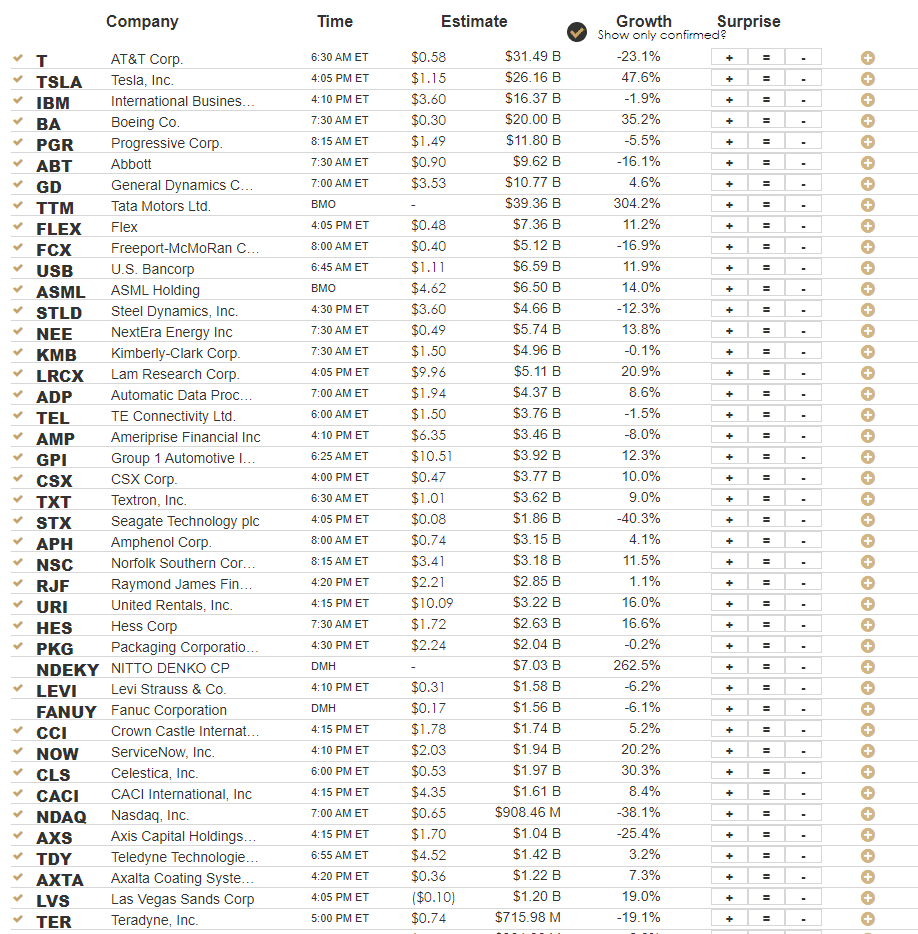

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, the week ended Jan. 20 (27.9% prior)

Earnings

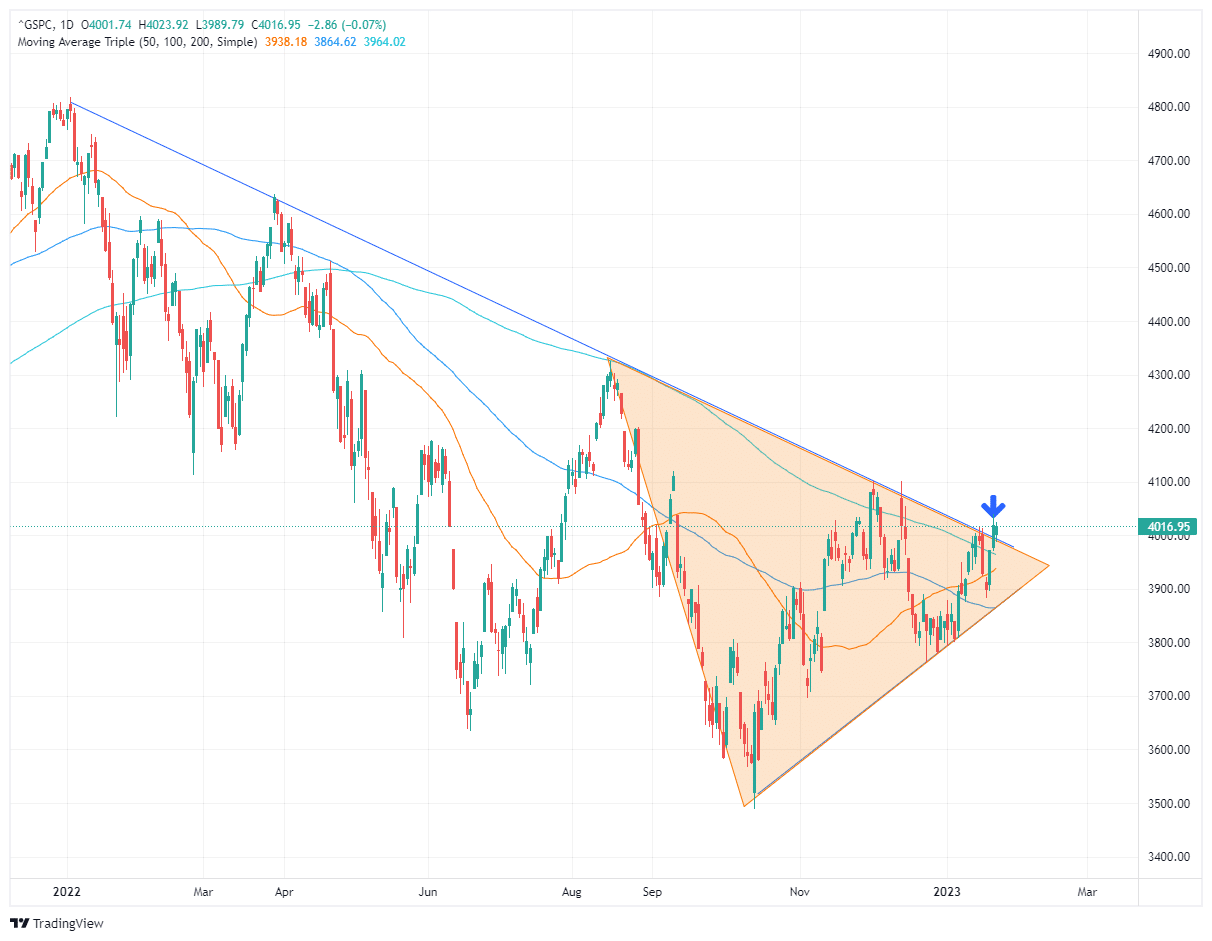

Market Trading Update

Yesterday, the market started off on the weak side, testing the breakout of the downtrend level. From a bullish perspective, the test of the breakout level is a good first test to see if this rally has some legs. With the market recovering through the day and closing near breakeven, the bullish bias remains. Investors should keep equity exposure for now, expecting a rally to continue. However, the FOMC meeting is next Wednesday, and given the easing in financial conditions, a strong message from the Fed to knock prices down will not be a surprise.

The market bias is improving, but we are not back in a bull market mode. Continue to hold higher cash levels and manage risk accordingly until the market trend becomes clearer.

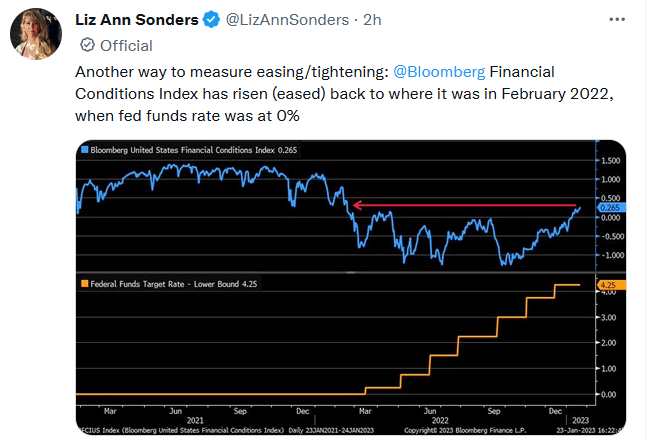

Financial Conditions Are Easing

As we noted above, financial conditions are relatively easy to measure using the stock, dollar, and corporate bond markets. The graph below shows that financial conditions are now back to similar levels as a year ago when Fed Funds were zero and stocks near their all-time highs. Such investor optimism is not likely to sit well with the Fed. Per a speech Jerome Powell gave in early December: “Officials seek to reduce inflation by slowing the economy through tighter financial conditions—such as higher borrowing costs, lower stock prices, and a stronger dollar—which typically curb demand.”

As we approach the FOMC meeting next week, we must ask will Jerome Powell and the Fed once again try to push markets lower and tighten financial conditions.

Navigating Contrarianism

Lance Roberts just published Contrarian Trade which discusses current market sentiment and provides tips on managing investments when many investors are bearish. Per the article:

As Bob Farrell’s Rule Number 9 states:

“When all the experts and forecasts agree – something else is going to happen.

As a contrarian investor, excesses are built by everyone betting on the same side of the trade. When the market peaked in January 2022, everyone was exceedingly bullish, and no one was looking for a 20% decline. Sam Stovall, the investment strategist for Standard & Poor’s, once stated:

“If everybody’s optimistic, who is left to buy? If everybody’s pessimistic, who’s left to sell?”

Today, everyone remains bearish, suggesting the possibility of the market doing something no one expects.

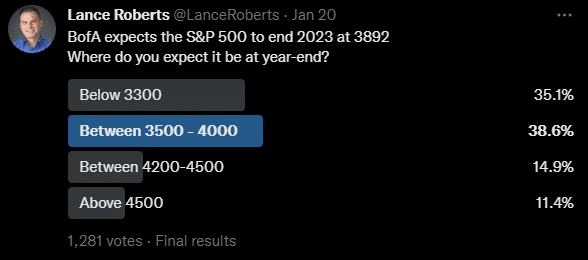

The screenshot below is from a recent Twitter poll Lance administered. As shown, over 70% of the 1280 responders expect the market to end lower than it is now.

Cyclical Stocks and Goldilocks

As gauged by the SimpleVisor Relative and Absolute reports over the last two weeks, market leadership has shown cyclical industries such as materials, industrials, and financials leading the way higher. Our takeaway is that investors are banking on a goldilocks economy and, thus, no recession. Further, recent weaknesses in technology and growth companies may account for the defensive lean.

The graph below shows a growing divergence between the outlook for manufacturing and the stock price performance of cyclical/defensive stocks. If industry leaders (ISM) are correct, a recession is likely; therefore, the recent outperformance of cyclical stocks may be negated. Conversely, maybe investors are correct, and the broad manufacturing surveys will start to show improvement. Either way, such a divergence is not commonplace over the last eight years.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.