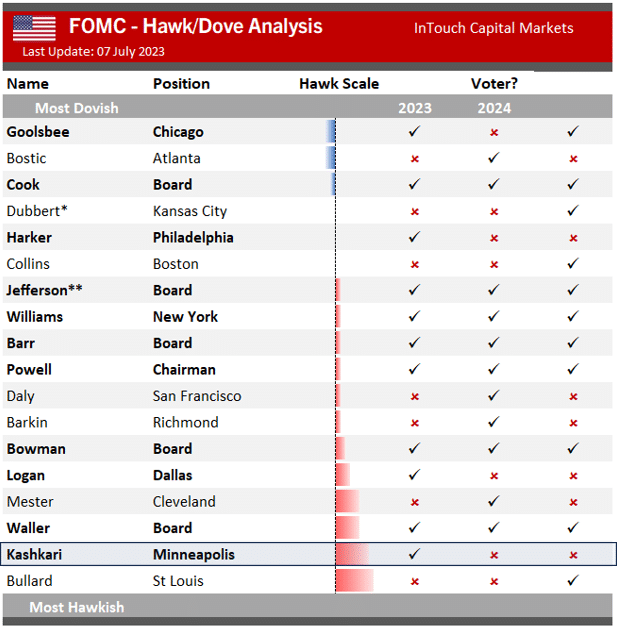

In last week’s Commentary, Doves Versus Hawks, we stated: “There appear to be two camps emerging, the doves and the hawks, with differing opinions on what to do next. We think this battle will become more pronounced over the coming months. Therefore, understanding the dove’s and the hawk’s points of view is critical to forecasting monetary policy.” Given the importance of understanding the views and, equally important, gauging how the opinions of individual Fed members shift, it’s worth looking at one of the more hawkish Fed members, Neel Kashkari. For background, Kashkari often tends above the more dovish members of the Fed. However, his policy prescriptions tend to overly focus on the lower-income earners. Inflation, and the harm it causes to lower and middle-income classes, has resulted in a more hawkish Kashkari. Per the table below from InTouch, Kashkari is now the second most hawkish on the board. That may change the next time they publish the table.

On Face the Nation this last weekend, he highlighted that core inflation is still running double the Fed’s 2% target. Despite much lower inflation rates, Kashkari said, “We don’t want to declare victory yet.” This is important because the risk of fighting inflation is higher unemployment, a topic Kashkari is also sympathetic to. Kashkari appears willing to let it rise from 3.6% to 4% to meet the Fed’s inflation goal. His views are shifting toward a dovish stance because he believes a recession is no longer on the horizon. As such, he seems willing to sacrifice employment for lower inflation. Kashkari’s recent opinions are now middle of the road. If other hawks follow him, we may have seen the last rate hike for this cycle.

What To Watch Today

Earnings

Economy

5-Straight Up Months – What Happens Next?

As we wrap up the month of July, the S&P has gained ground consecutively for 5-months straight. The table below shows that such is a fairly rare occurrence but portends to higher returns over the next 12 months.

However, what is overlooked is that IF such a win streak is rare, it suggests that it tends to end rather quickly. Therefore, as we move into the seasonally weak months of the year, August and September, we should expect a cooling off of the market, and a potential retest of support, before the market makes a push into the end of the year.

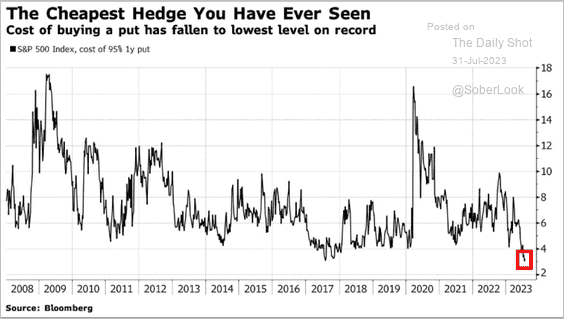

That idea of short-term correction is also supported by the extremely low cost of hedging a portfolio by buying put options. That cost of hedging a portfolio is now the lowest level on record and well below levels seen during the financial crisis. Not surprisingly, such low levels of “fear” often coincide with short-term market peaks.

Remain cautious for now, take profits as needed, and look for a correction to short-term support levels to increase equity exposure as needed.

More Economic Surprises

In Monday’s Commentary, we asked if you were surprised the U.S. economy was doing so well. We followed the question as follows:

If your answer is yes, you are not alone. As we show below, the Citi Economic Surprise Index is at its highest level in over two years. This indicates that economists have been underestimating the economy.

We have another surprise for you. While U.S. economic data surprises to the upside, economic data from the rest of the world fails to meet expectations. Disregarding the 2020 covid related instance, the difference between U.S. and economic data from the rest of the world is the largest on record, as shown below courtesy of Deutsche Bank. This data indicates that the outsized U.S. fiscal response to the pandemic and continued enormous fiscal spending, which is and was more extensive than most countries, continues to echo through the U.S. economy.

Is This Time Different?

Over the last few months, we have asked if this time is different on numerous occasions. Simply, there are irregular data divergences and recession signals that have thus far proven false. Add the graph below to the growing list. As it shows, Leading Economic Indicators, which include stock prices, tend to be well correlated with the S&P 500. Are the leading indicators a false negative, or is the stock market due for a correction?

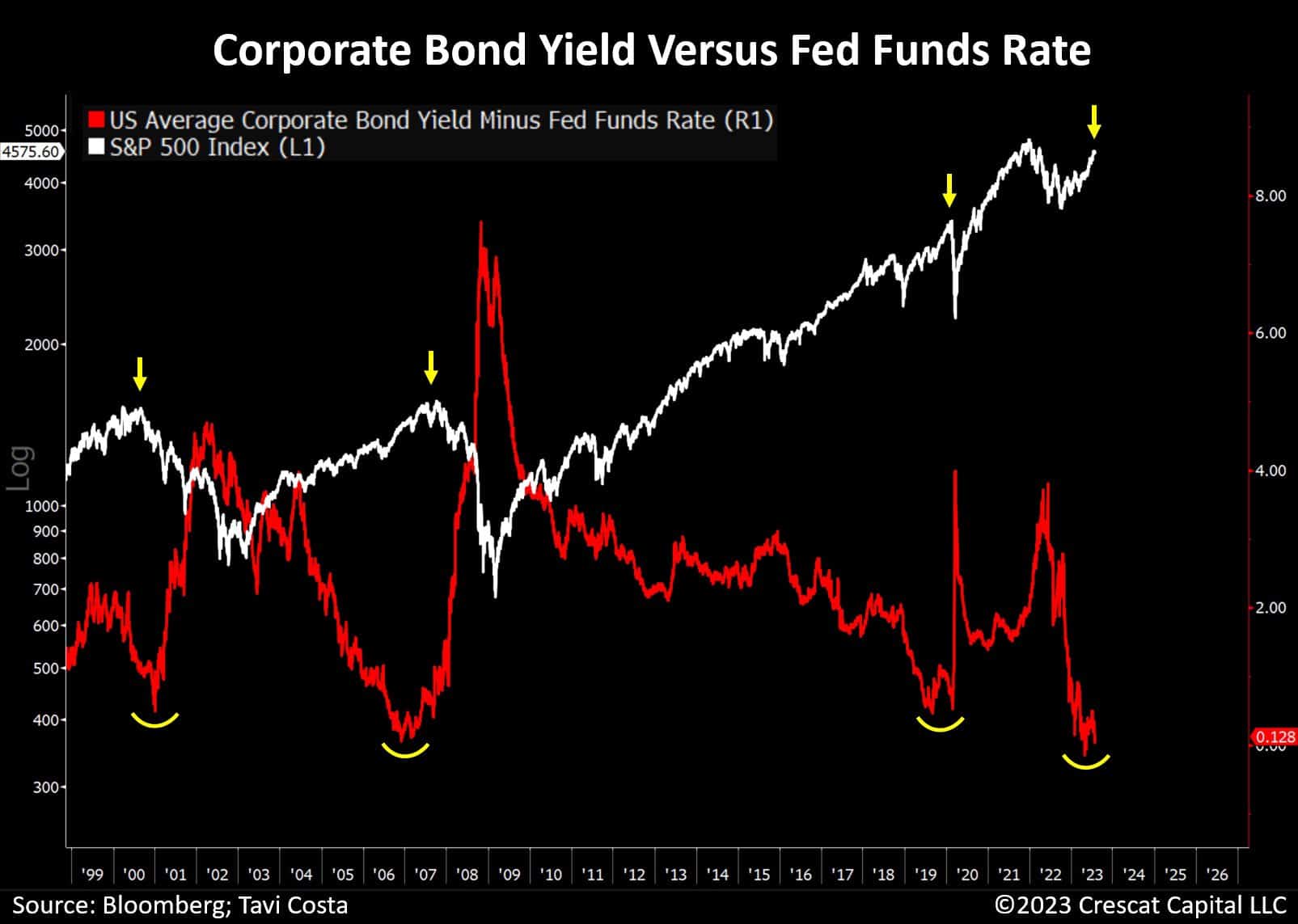

Corporate Bond Yield Inversions- More Is this Time Different Part 2

Tavi Costa provides another example in which we must ask if this time is different. The following graph and commentary are from a recent tweet of his.

Corporate bonds now yield only 0.12% above the Fed Funds rate. The lowest level since 2007, preceding the Global Financial Crisis. Every time credit spreads were at historically suppressed levels, a hard-landing scenario followed. Perhaps this time is indeed different, but I would rather base my perspective on numerous indicators pointing towards an impending severe recession. The profound issue of yield curve inversions is yet another example.

Recently, over 90% of the Treasury curve was inverted, a measure that has accurately predicted every major economic contraction in the last 50 years. Moreover, the Fed’s policy stance should also be taken into consideration. As we have learned repeatedly throughout history, tightening monetary policies work with a lag and we are yet to witness a significant credit contraction that could lead to further economic issues. Even the apparent strength of the labor market should be taken with a grain of caution. Historically low unemployment rates have served as one of the most reliable contrarian indicators in history.

Either these macro indicators are on the brink of being proven wrong, or the overall equity valuations are entirely out of line.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.