Friday’s employment report revealed that Nonfarm Payrolls rose 253,000 last month, crushing expectations of a 185,000 increase. Meanwhile, the unemployment rate fell to 3.4%— its lowest since 1969, and average hourly earnings rose 0.5%, their fastest pace in a year.

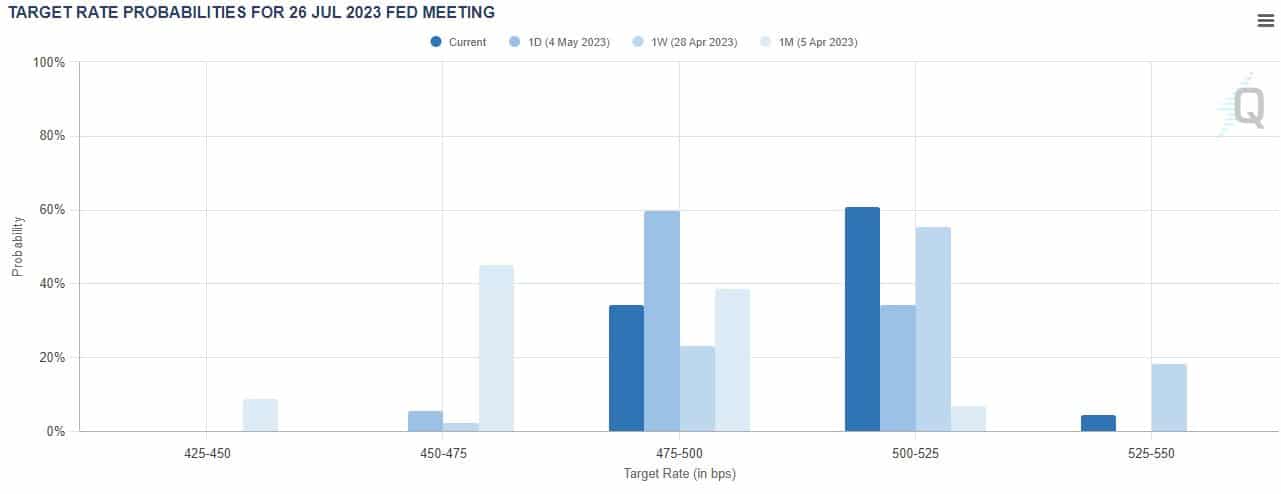

Before Friday’s report, Fed Funds futures priced in a 60% chance of a rate cut at the July FOMC meeting. Those odds fell sharply to settle near 35% following further evidence of a resilient labor market. While the employment report lowers the chance of rate cuts coming sooner than later, it’s not enough to increase the likelihood of further rate hikes. Given the Fed’s growing emphasis on incoming data to drive decision-making, expectations priced into the Fed Funds futures market may see higher volatility going forward.

What To Watch Today

Economy

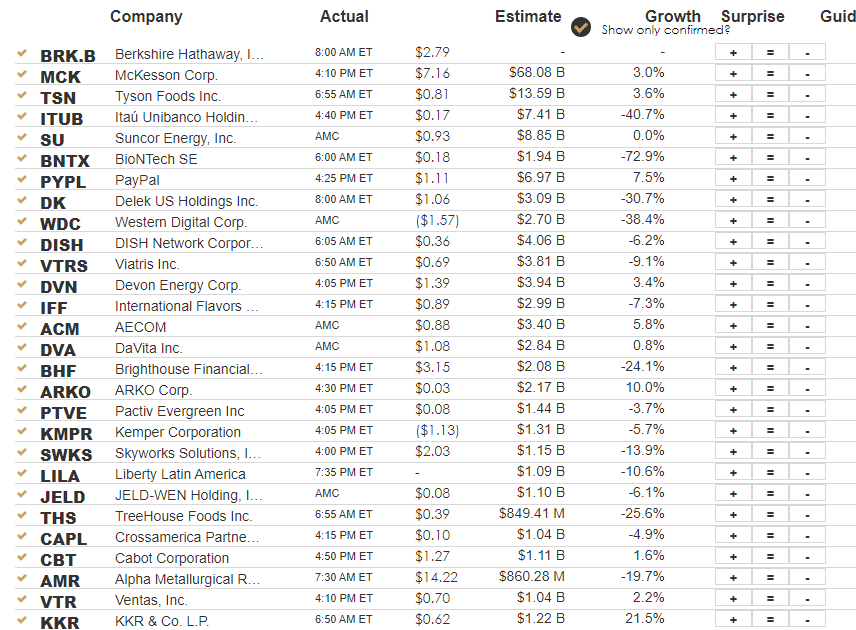

Earnings

Market Trading Update

With the majority of S&P 500 earnings behind us, the focus will turn to economic data, which has remained weak as of late outside employment numbers. Nonetheless, we are likely near a trough in economic activity and should start seeing improvement as we approach the end of the summer.

The reductions we made a couple of weeks ago helped shield portfolios from last week’s correction, which was both needed and expected. While technical signals often don’t make sense, more often than not, they are picking up on the “herd mentality” of the market. When an event happens, we immediately look for headlines to blame for the sell-off or advance, but the market is usually ahead of whatever the trigger turned out to be.

The market remains on a “sell signal” and again tested and held critical support at the 50-DMA and the downtrend support line from the April highs. The consistent test and holding of support remain bullish overall, and unless or until that is broken, the more bearish concerns are secondary.

The Week Ahead

This week will be quiet on the economic data front following last week’s FOMC rate decision and employment data. On Wednesday, we’ll receive an update on inflation with the April CPI data release. This release is highly anticipated given the Fed’s increasingly data-dependent attitude and Friday’s strong employment results. Market participants expect headline inflation to tick up to 0.4% MoM in April from 0.1% in March. However, expectations call for a decrease in Core Inflation to 0.3% MoM from its previous 0.4% MoM. Following the CPI data, April PPI data will drop on Thursday. The consensus is for an increase of 0.3% MoM after a negative surprise in March. Finally, we’ll receive the preliminary University of Michigan Consumer Sentiment and inflation expectations data for May on Friday.

Cyclicals are Shining This Earnings Season

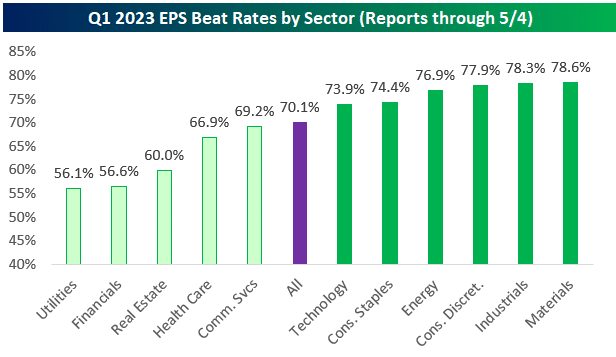

More than 1,200 companies have reported 1st quarter earnings through Friday. The chart below from Bespoke highlights that 70% of companies have topped earnings estimates. Cyclical sectors are outshining defensive sectors on average, with Materials, Industrials, and Consumer Discretionary beat rates all near 78%. Resilient employment keeps consumption intact despite inflation, translating to the highest beat rate for S&P 500 companies since Q4 2021.

Lofty Assumptions Meet Reality

The Financial Times published an interesting article by Drew Dickson outlining the gap between perception and reality within the Tesla story. Dickson discusses Tesla’s price cuts in the months leading up to the investor day in March. Were they a strategic bid for market share, or rather a defensive move amid increasing competition? Musk made it seem like a bid for market share. “Even small changes in the price have a very big effect on demand.” However, TSLA bulls were left scratching their heads when Q1 results were released on April 3rd.

It turned out that Tesla couldn’t sell every car it made. Despite sequential price cuts of approximately 10-15 per cent, deliveries only grew by 6 per cent sequentially. In fact, Tesla actually overproduced in the quarter, growing inventories. An implied price elasticity of much less than 1.0 was evidence that price changes, whether big or small, had very little effect on demand.

On top of the lack of incremental demand from price reductions, gross margins fell by more than leadership had predicted.

Tesla failed to reduce costs through scale effects or lower input costs so first-quarter automotive gross margins (ex regulatory credits and leases) were 18.3 per cent, down from the 29.7 per cent generated a year before. A reminder that management had guided for “at least 20 per cent” just a month earlier.

Moreover, Tesla received Inflation Reduction Act (IRA) tax credits during the quarter. In a filing with the SEC, Tesla stated that a higher cost per unit during the first quarter was “partially offset by manufacturing credits earned as part of the IRA”. Management didn’t disclose a precise number but if, hypothetically, 17.5 per cent of costs was the “partial” offset then Tesla would receive a $269mn subsidy against production expenses. In this (theoretical but plausible) example, this means automotive gross margins ex all the funnies didn’t merely drop to 18.3 per cent, they may have plummeted to around 16.9 per cent. Tesla did not reveal anything about the IRA credits optically supporting margins on the conference call.

Decomposing the numbers, I estimate that the profit per vehicle likely dropped from circa $15,000 last year to just above $7,500. In other words, here was a price cut of approximately 12.5 per cent and profits almost halved.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.