Thomas Barkin, President of the Richmond Fed, made a very important pronouncement on Thursday. In a speech he states: “It’s difficult to imagine inflation falling without demand falling.” His message seems to be have fallen on deaf investor ears. In plain English, Barkin is telling us that demand, i.e., personal consumption, will have to decline, not slow, to bring inflation back to the Fed’s 2% target. Given the Fed remains vigilent in its quest to get inflation back to its 2% target, Barkin is warning that a recession may be required. We remind you that personal consumption accounts for about two-thirds of economic activity.

The most recent indicator of demand, personal consumption expenditures rose 0.2%, equating to a 2.4% annualized rate. The graph below shows the relatively tight relationship between consumer expenditures and inflation. Demand is finally starting to slow and inflation will likely follow. The 2.4% annualized monthly consumption rate is well below the 7.6% year-over-year change. Friday’s Michigan Consumer Sentiment Survey shows weakening consumer sentiment which will likely temper demand. In their latest report, consumer expectations fell from 64.7 to 59.2. The shakeout from the banking crisis and the effect is has on lending will materialize over the next few months and provide better guidance on demand, economic activity, and inflation.

What To Watch Today

Economy

Earnings

- No notable earnings releases are scheduled.

Market Trading Update

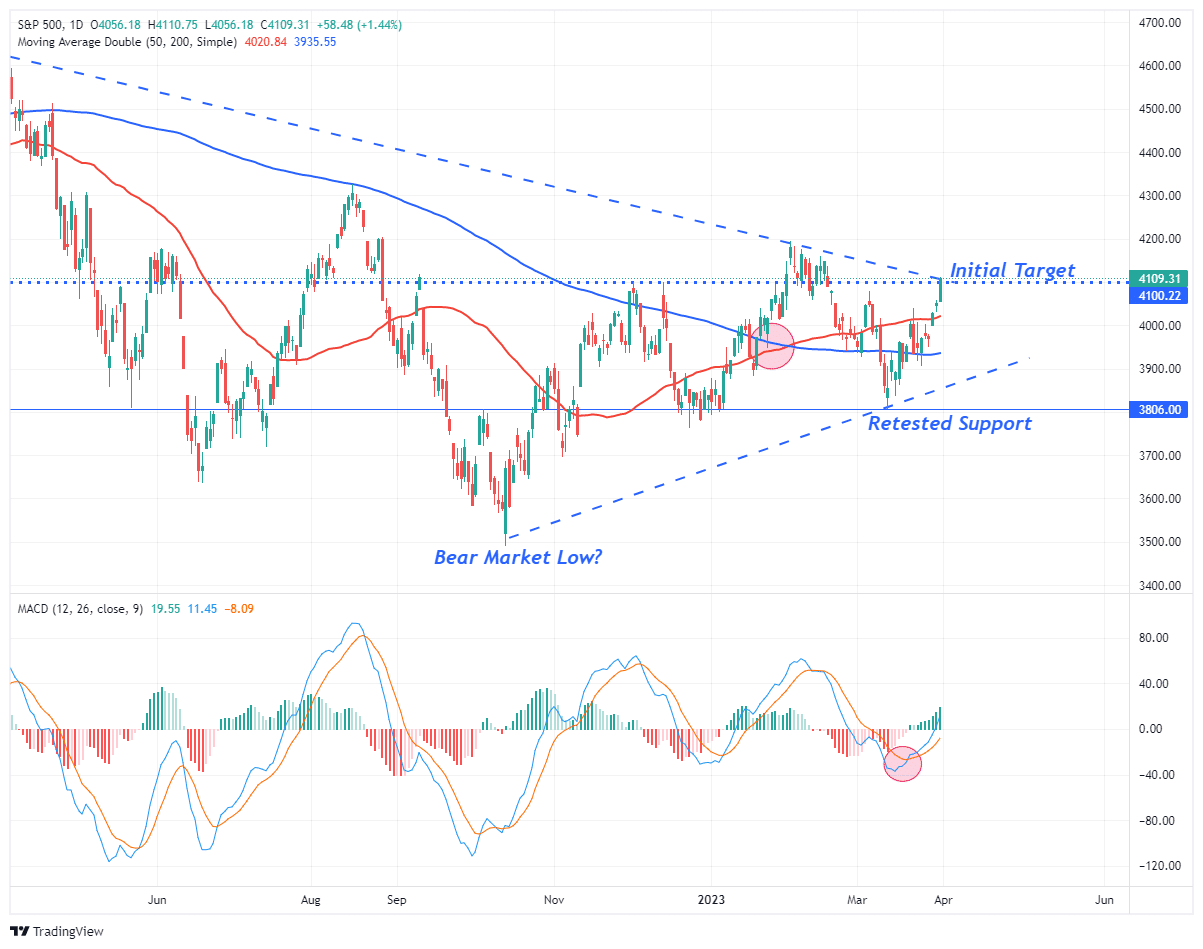

With the month of April starting, so do the 1st quarter earnings season. Given rather low expectations currently, a high beat rate and positive spin from earnings will not be surprising. The question will be whether Wall Street analysts are correct that Q1 will mark the trough for the recent earnings decline and earnings will improve in Q2.

IF that is the case, then that is also what the markets have been pricing in for the last several months. As shown, while the market is short-term very overbought and due for a pullback, the trend is clearly positive, suggesting October was the market low. The market closed last week on a strong note of broad participation and a test of the downtrend line from the August peak. A pullback to the 50-DMA will provide a good entry point to increase portfolio risk for another push higher into April and May. With our MACD buy signals intact and not overbought, the current most likely path for prices is higher.

The Week Ahead

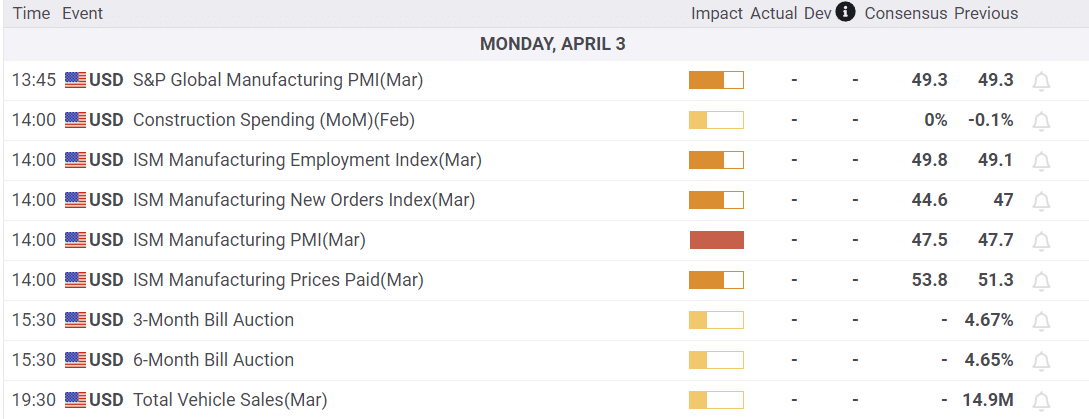

We kick off the week with the latest ISM manufacturing survey. Readings below 45 have preceded almost every recession in the last 40 years. The expectation is for a slight decline from 47.7 to 47.5. The wild card in this report and other survey data is when the survey was conducted and did it reflect any new anxieties regarding the banking sector and the potential for banks to tighten lending standards.

This is jobs week. JOLTs on Wednesday and ADP on Thursday will help analysts hone in on their BLS forecast for Friday’s employment report. The current estimate is for a gain of 240k jobs, a brisk pace but a decline from the prior month’s 311k. Expectations for ADP are 242k, on par with the BLS forecasts.

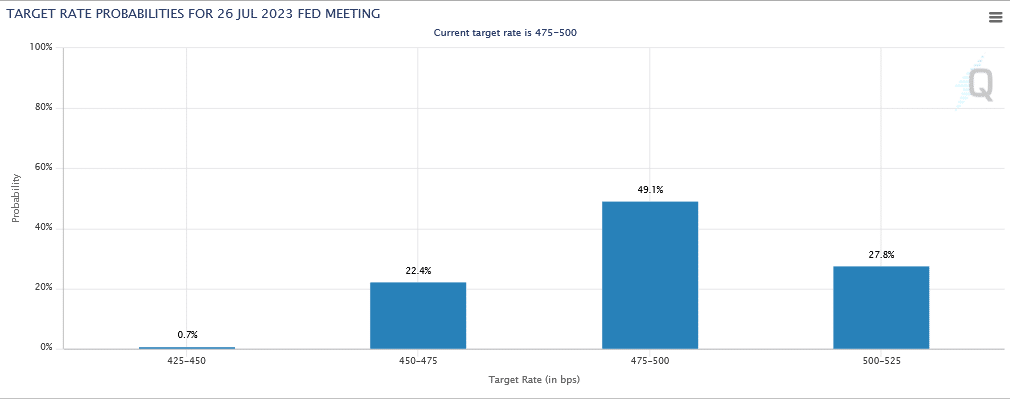

As usual, there will be a slew of Fed speakers. We will see if their opinions shift with the latest PCE report and employment data mentioned above. Currently, the market assigns a 50/50 chance of a 25bps rate hike in early May. Interestingly, the market is torn about the July meeting, as they are pricing in equal chances of a rate hike and rate cut.

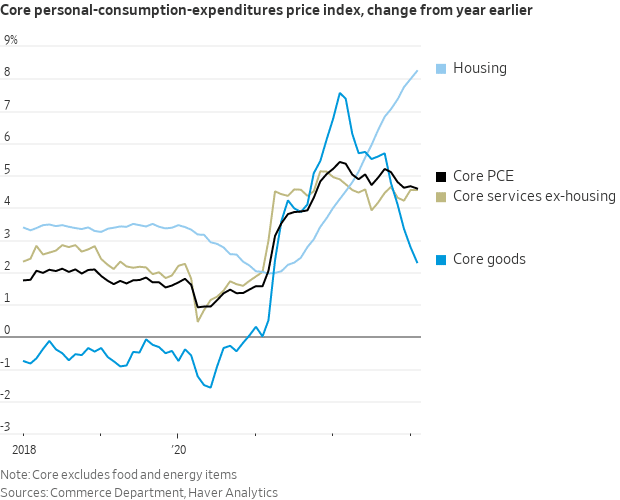

PCE Inflation Tamer Than Expected

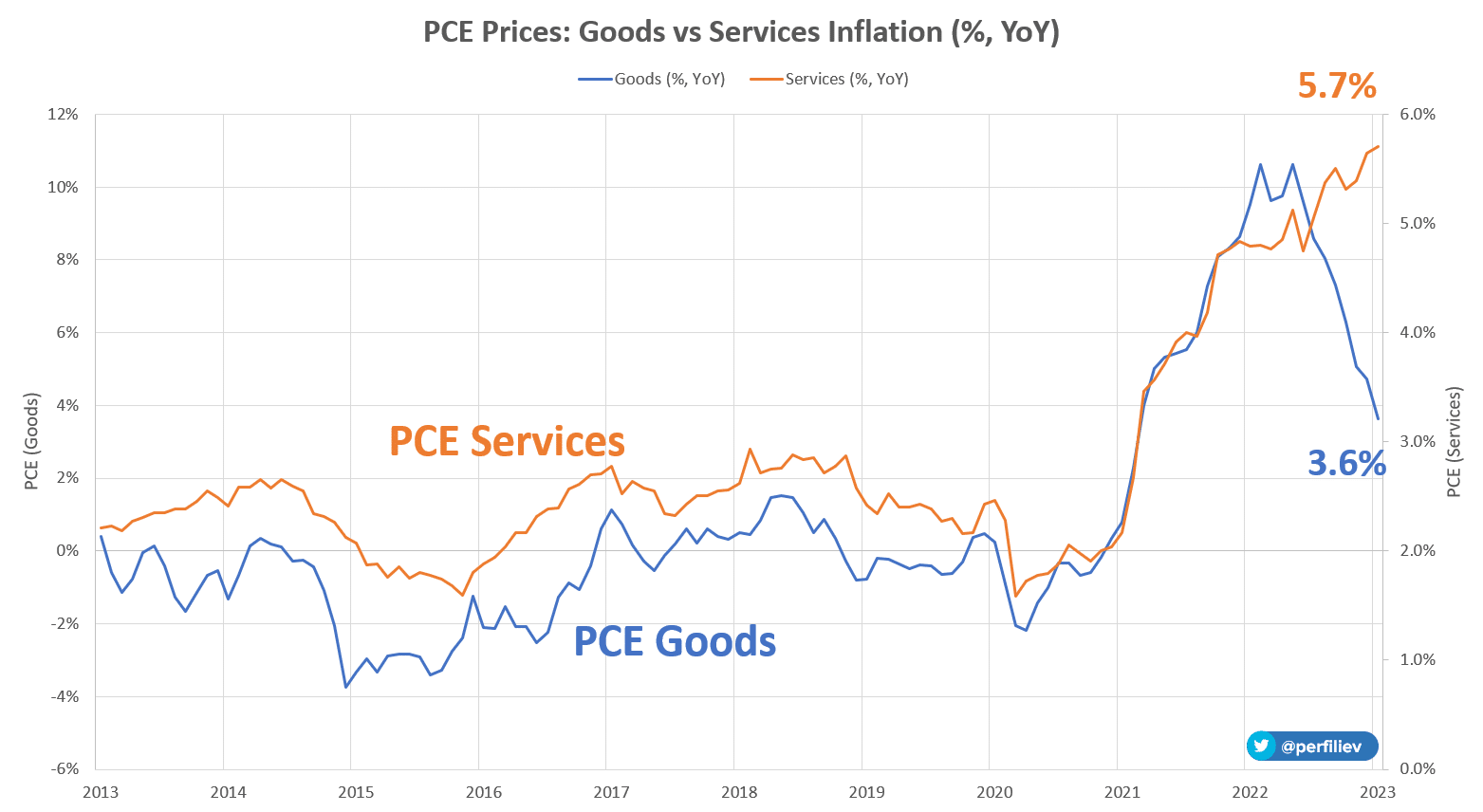

The Fed’s preferred inflation gauge, PCE Prices, fell to 5.0% year over year, the lowest level since September 2021. Both the monthly and year-over-year data were .10% below expectations. Core inflation was also .10% below expectations. While the data is generally good news, the Fed is hyper-focused on core services excluding housing. As shown below in beige, this sub-inflation indicator is not declining like the broader inflation measures. Another forward-looking concern from non-government data is that used car and rent prices have started rising again. If the price gains, especially in rent, are sustainable, inflation will prove challenging to bring down without a full-on recession. Lastly, as shown in the second graph, courtesy of @perfiliev, services inflation has yet to peak.

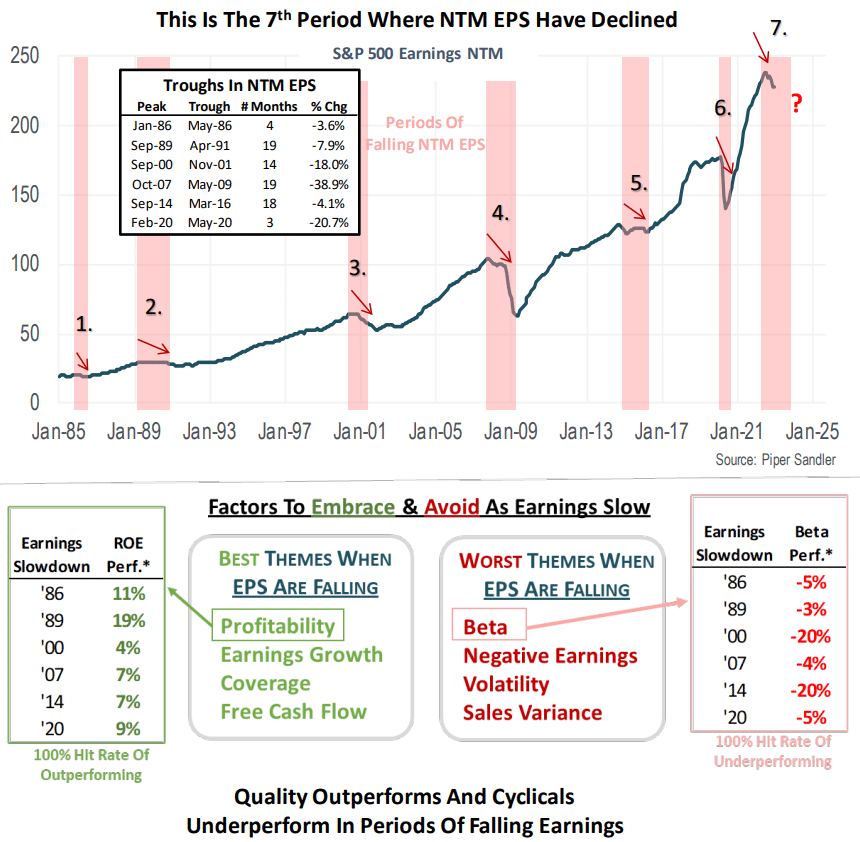

What to Buy in an Earnings Recession

The Piper Sandler graphic below provides valuable guidance on what type of stocks to buy if earnings continue to decline. Companies with a good track record of earnings growth, high amounts of cash, strong cash flows, and manageable debt have provided a positive return over the last six earnings recessions. Conversely, stocks with high betas and large variances in revenue tend to do poorly. Investors prefer earnings and revenue stability during recessions.

Due to high-interest rates and the distinct possibility lending standards tighten, we should focus more heavily on stocks with a high-interest coverage ratio, strong cash flows, and recession-proof revenue and earnings growth.

While the road map for an earnings recession is helpful, it’s worth noting that current Wall Street earnings estimates do not price in a recession. Per our March 4th Bull Bear Report:

Analysts remain optimistic about earnings even with economic growth weakening as inflation increases, reduced liquidity, and declining profit margins. As shown above, analysts expect the first quarter of 2023 will mark the bottom for the earnings decline, and growth will accelerate into year-end. Again, this is despite the Fed continuing to hike interest rates specifically to slow economic growth.

The problem with these expectations is the detachment of earnings estimates above the long-term growth trend.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.