On Thursday, the executives at Service Now (NOW) and IBM learned an important lesson the hard way as their stocks fell by 18% and nearly 10%, respectively. The stark message from Wall Street is that forward sales and earnings guidance now take precedence over recent financial results.

IBM beat earnings expectations across the board. However, they didn’t change their forward guidance for the year. Its CFO, Jim Kavanaugh, noted, “I don’t think we’ve ever raised guidance in a first quarter.” Despite good earnings, the market wasn’t happy because they didn’t provide a first-quarter outlook, as is typical for the company.

The NOW situation was a little different from IBM’s. They withheld earnings guidance specifically because of the situation in Iran. Per an interview on CNBC, its CFO, Gina Mastantuono, said she “took a little bit of incremental conservatism because of the ongoing conflict in the Middle East and its potential impact on deal timing.” The market didn’t like the company’s conservative posture.

As we share below, both companies’ stocks were trading poorly before earnings. Investors wanted more than good earnings reports; based on the strong negative reaction, they wanted guidance on how AI is impacting the companies. The simple lesson, especially for technology stocks, is that silence on guidance is bearish.

What To Watch Today

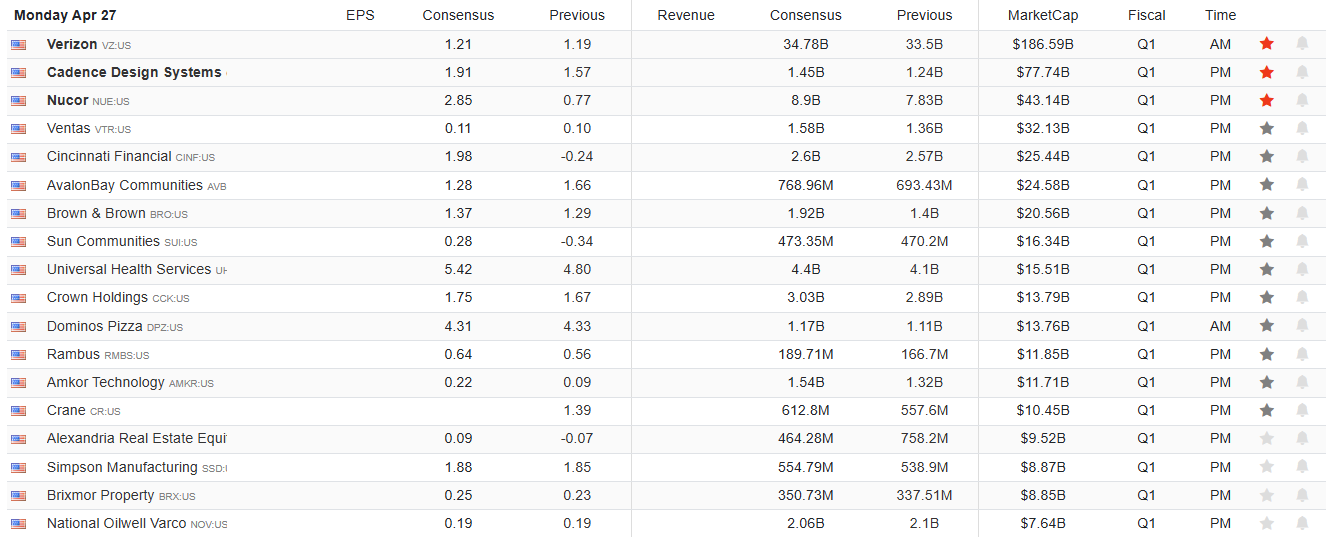

Earnings

Economy

Market Trading Update

The S&P 500 closed Friday at a fresh all-time high of 7,165, up 0.80% on the session and extending the index’s remarkable run off the March lows. The week, however, was anything but smooth. Thursday’s session delivered a gut-check: reports of air defense systems activating over Tehran sent WTI past $106, and the S&P dropped 0.41% as the oil-volatility transmission mechanism briefly reasserted itself. Friday’s recovery came on Intel’s blowout earnings (+21%), Trump’s three-week extension of the Israel-Lebanon ceasefire, and crude pulling back to $94. The VIX settled at 18.92, below our 20 thresholds, but Thursday’s spike was a reminder of how quickly that can change.

The technical picture remains unambiguously bullish across all time frames. Investing.com shows 12 of 12 moving average signals at “Strong Buy.” The 14-day RSI is near 70, indicating an overbought condition. The MACD, a measure of momentum, is on a “buy signal” and rising. The index is trading above the 50-DMA (~6,790) and above the 200-DMA (~6,705), both of which are rising. Breadth has held with roughly 52% of constituents above their 50-DMA, but needs to strengthen if the rally is going to continue.

The tension in this tape lies between technical strength and fundamental fragility. As noted below, the Michigan consumer sentiment printed its lowest reading on record. Furthermore, the Iran peace talks have stalled, with Thursday’s Tehran episode a stark reminder that the geopolitical risk premium hasn’t fully unwound. Oil’s $94 price represents the kind of volatility that whipsaws systematic strategies and undermines the VIX’s descent. The Fed remains on hold at 3.5–3.75% with markets pricing no cuts in 2026. At BofA’s target zone of 7,168–7,206, now just 0.4–1.0% overhead, the index is approaching a natural ceiling where profit-taking is likely.

For now, the market continues to climb a wall of worry, and the technicals say respect the trend. RSI is elevated but not grossly overbought, and while breadth is improving, all moving averages remain green. Our March 200-DMA analysis continues to play out textbook. But Thursday’s reversal on the Tehran headlines was a shot across the bow; this market remains one oil headline away from a 2–3% air pocket. The pullback we flagged last week hasn’t materialized so far, which is making the setup increasingly stretched. New money should wait for a retest of 7,000 or the 50-DMA (~6,979). Stay long but trail stops and take partial profits into BofA’s 7,168–7,206 target. Trade accordingly.

The Week Ahead

After a couple of weeks of limited economic data, investors will start to get a picture of how inflation is reacting to higher oil prices. On Thursday, the PCE prices index for March is expected to show +0.3% growth excluding food and energy. The headline number is expected to rise by 0.6%. Despite Friday being the first Friday of the month, the BLS employment data will not be released until May 8th. The Fed may provide further guidance on inflation as the FOMC meets on Wednesday. No changes to rates are expected, but we may get some more information on why they reduced QE from $40 billion to $25 billion a month.

As we share below, courtesy of SensaMarket, there will be plenty of important earnings reports due this week. Thursday could be a volatile day as Google, Microsoft, Amazon, and Meta all report after the market closes on Wednesday.

Government Debt: Not What The Doom Crowd Thinks It Is

Every few years, someone discovers that the United States government owes a very large amount of dollars and concludes that Rome is about to fall. A recent piece in RealClearMarkets by Nash, Thomas, Lang, and Rastin does exactly this. They rely on the Roman Empire’s collapse and the Weimar Republic’s hyperinflation as cautionary parallels to America’s $39 trillion in federal government debt.

The argument is tidy, emotionally satisfying, but wrong in several important ways. Crucially, government debt is not what the doom crowd thinks it is, and the historical comparisons they love most have almost nothing in common with the American fiscal situation today.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.