Cherry-picking data is one of the many things you must be careful with when reading market or investing analysis. Here is a good example from Jeff Somner at the New York Times:”

“Mutual Funds That Consistently Beat the Market? Not One of 2,132.” reads the headline. The subheading continues:

“No actively managed stock or bond funds outperformed the market convincingly and regularly over the last five years. Index funds have generally been better.”

That statement is not “untrue;” it is just misleading in its analysis.

It is true that ZERO mutual funds consistently beat its benchmark index each year over the last five years. More accurately, we can say zero mutual funds consistently, meaning each and every year, beat their respective benchmarks over the last 20 years.

However, index funds have done no better.

Over the last 5- or 20 years, ZERO index funds have beaten their respective benchmarks. In fact, after the expenses those funds charge, as shown below, they have “gasp,” NEVER beaten their respective benchmark. (You will notice the 8% performance lag over the 20-year time span.)

The analysis above is just another of many written by journalists in the “active vs. passive” debate. Unsurprisingly, many investors became lulled into complacency after a 12-year monetary and fiscal policy-fueled advance.

“Nobody needs an active manager in a bull market; index returns are adequate. Active management shows its value in its ability to protect against adverse market conditions. The market downturn in the first quarter gave us that opportunity.” – Robert Huebscher, Advisor Perspectives

Over the next decade, as monetary and fiscal policies lose efficacy, the question is whether active managers will regain their lost luster.

Time Frames Matter

From one year to the next, all active portfolio managers will make bets which either outperform or underperform their relative benchmark. Such is why “investing has risk.” However, given that we are supposed to be long-term investors, such suggests focusing on longer-term results rather than short-term variations.

The following chart of the Fidelity Contra Fund versus the Vanguard S&P 500 Index makes an invaluable point. If you listened to Jeff Somner and bought an index fund, you would have lost out on massive wealth generation. However, there were more than a few years when the ContraFund underperformed its benchmark.

Which fund would you have rather owned?

(Source: Portfolio Visualizer)

Finding funds with long-term track records is difficult because most mutual funds didn’t launch until the late “go-go 90s” and early 2000s. However, I quickly looked up and added 3-more active mutual funds with long-term track records for comparison. The charts below compare Sequoia Fund, Dodge & Cox Stock Fund, and Growth Fund of America to the Vanguard S&P 500 Index.

(Source: Portfolio Visualizer)

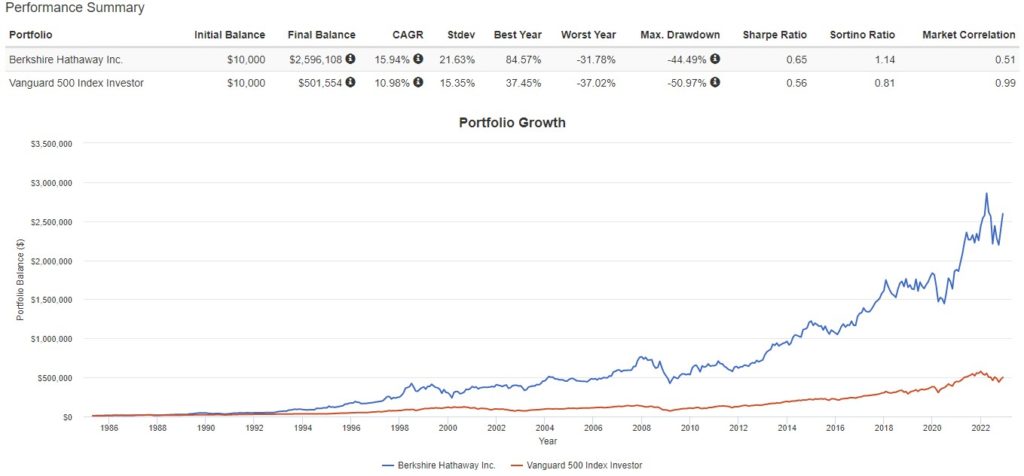

Or, for all those who still want to argue that an “active manager can’t beat an index,” you don’t have to look much further than Warren Buffett.

I don’t know about you, but an investment into any of the actively managed funds over the long-term horizon certainly seems to have been a better bet than a passive index fund.

Strive To Be Better Than Average

So, how is it that an index fund that is supposed to purely replicate an index failed to exactly match the performance of the index?

Simple.

Fees, taxes, and expenses.

Unfortunately, in the “real world,” where people invest their “hard-earned savings,” their overall returns are constantly under siege from taxes, fees, and, most importantly – taxes.

An “index” is simply a mathematical calculation of priced securities and has no such detriments.

The chart below is the S&P 500 Total Return Index before and after the same expense ratio charged by the Vanguard S&P 500 Index Fund. Since most advisers don’t manage client money for free, I have included an “adviser fee” of 0.5% annually.

This is the point where you should ask yourself an important question.

“If your advisor is passively investing in index funds, and charging you a fee, then exactly what are you paying for? “

The major learning points regarding the fallacy of chasing a “benchmark index” are:

1) The index contains no cash

2) It has no life expectancy requirements – but you do.

3) It does not have to compensate for distributions to meet living requirements – but you do.

4) It requires you to take on excess risk (potential for loss) in order to obtain equivalent performance – this is fine on the way up, but not on the way down.

5) It has no taxes, costs or other expenses associated with it – but you do.

6) It has the ability to substitute at no penalty – but you don’t.

7) It benefits from share buybacks – but you don’t.

To win the long-term investing game, your portfolio should be built around the things that matter most to you.

– Capital preservation

– A rate of return sufficient to keep pace with the rate of inflation.

– Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

– Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

– You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

– Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

The index is a mythical creature, like the Unicorn, and chasing it takes your focus off of what is most important – your money and your specific goals. Investing is not a competition, and there are horrid consequences for treating it as such.

The Only Question That Matters

There are many reasons why you shouldn’t chase an index over time, and why you see statistics such as “80% of all fund underperform the S&P 500.” The impact of share buybacks, substitutions, lack of taxes and trading expenses all contribute to the outperformance of the index over those actually investing real dollars who do not receive the same advantages.

More importantly, any portfolio that is allocated differently than the benchmark to provide for lower volatility, create income, or provide for long-term financial planning and capital preservation will underperform the index as well. Therefore, comparing your portfolio to the S&P 500 is inherently “apples to oranges” and will always lead to disappointing outcomes.

“But it gets worse. Often times, these comparisons are made without even considering the right way to quantify ‘risk’. That is, we don’t even see measurements of risk-adjusted returns in these ‘performance’ reviews. Of course, that misses the whole point of implementing a strategy that is different than a long only index.

It’s fine to compare things to a benchmark. In fact, it’s helpful in a lot of cases. But we need to careful about how we go about doing it.” – Cullen Roche

For all of these reasons, and more, the act of comparing your portfolio to that of a “benchmark index” will ultimately lead you to taking on too much risk and into making emotionally based investment decisions.

But here is the only question that really matters in the active/passive debate:

“What’s more important – matching an index during a bull cycle, or protecting capital during a bear cycle?”

You can’t have both.

If you benchmark an index during the bull cycle, you will lose equally during the bear cycle. However, while an active manager that focuses on “risk” may underperform during a bull market, the preservation of capital during a bear cycle will salvage your investment goals.

Investing is not a competition and, as history shows, there are horrid consequences for treating it as such. So, do yourself a favor and forget about what the benchmark index does from one day to the next. Focus instead on matching your portfolio to your own personal goals, objectives, and time frames. In the long run, you may not beat the index, but you are likely to achieve your own personal investment goals which is why you invested in the first place.